Report on Project Cost Management Techniques for a Call Center

VerifiedAdded on 2020/05/04

|11

|2019

|333

Report

AI Summary

This report delves into the intricacies of project cost management, specifically within the context of establishing a new call center. It begins by outlining the importance of budgeting, detailing the inputs required, and exploring various tools such as analog estimation, parametric modeling, and computerized tools. The report then moves on to cost control, emphasizing the significance of monitoring expenditures, analyzing performance, and managing changes. It highlights the inputs necessary for effective cost control, including cost baselines and performance reports, and discusses methods like cost change control systems and performance measurement. The report also provides a finalized cost analysis, including budget plans and operational costs, and proposes improvements using techniques such as Kaizen costing and Six Sigma to reduce costs and optimize processes. Overall, the report provides a comprehensive overview of project cost management strategies for a new call center, aiming to minimize risks and ensure project success.

Running head: PROJECT COST MANAGEMENT TECHNIQUES

PROJECT COST MANAGEMENT TECHNIQUES

Name of the Student

Name of the university

Authors Note:

PROJECT COST MANAGEMENT TECHNIQUES

Name of the Student

Name of the university

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PROJECT COST MANAGEMENT TECHNIQUES

Table of Contents

Introduction......................................................................................................................2

Budget..............................................................................................................................3

Inputs required for cost Budgeting..............................................................................3

Tools for cost Budgeting.............................................................................................3

Cost management.............................................................................................................4

Inputs to cost controlling.............................................................................................5

Tools and methods for cost controlling.......................................................................5

Benefits of Cost control...............................................................................................6

Finalization of Cost..........................................................................................................6

Improvements..................................................................................................................7

References............................................................................................................................9

Table of Contents

Introduction......................................................................................................................2

Budget..............................................................................................................................3

Inputs required for cost Budgeting..............................................................................3

Tools for cost Budgeting.............................................................................................3

Cost management.............................................................................................................4

Inputs to cost controlling.............................................................................................5

Tools and methods for cost controlling.......................................................................5

Benefits of Cost control...............................................................................................6

Finalization of Cost..........................................................................................................6

Improvements..................................................................................................................7

References............................................................................................................................9

2PROJECT COST MANAGEMENT TECHNIQUES

Introduction

The report relates us to the topic of cost management involved in managing the cost

required for the setup of a new call center. It helps the various business in predicting various

expenses in an organization which will ultimate reduce their risk of going over the budget.

Reducing the cost involved in a project can be achieved by increasing hiring, coaching and lastly

better training of staff members, keeping an eye on the action or activities of various agents,

improving the resolution of first call, Improving the schedule of cost and reducing or minimizing

the cost of attrition.

Various responsibilities which are involved for applying proper techniques for the

development of new call center for large organization. Various factors like budget, monitoring

expenditure, finalizing of cost, improvements which are involved in this project cost

management has been discussed in details. Budget of a project mainly depends on following

parameters like labor, materials, equipment, services and facilities. Cost control of project mainly

comprises of following things like meeting of targets, progression as planned, cost as planned.

Budgeting of project mainly comprises of following parameters like baseline of the cost involved

in project. Project cost management consist of various process which mainly checks that the

given project is completed in given time. It mainly helps in ensuring that the given project is

completed within project.

Introduction

The report relates us to the topic of cost management involved in managing the cost

required for the setup of a new call center. It helps the various business in predicting various

expenses in an organization which will ultimate reduce their risk of going over the budget.

Reducing the cost involved in a project can be achieved by increasing hiring, coaching and lastly

better training of staff members, keeping an eye on the action or activities of various agents,

improving the resolution of first call, Improving the schedule of cost and reducing or minimizing

the cost of attrition.

Various responsibilities which are involved for applying proper techniques for the

development of new call center for large organization. Various factors like budget, monitoring

expenditure, finalizing of cost, improvements which are involved in this project cost

management has been discussed in details. Budget of a project mainly depends on following

parameters like labor, materials, equipment, services and facilities. Cost control of project mainly

comprises of following things like meeting of targets, progression as planned, cost as planned.

Budgeting of project mainly comprises of following parameters like baseline of the cost involved

in project. Project cost management consist of various process which mainly checks that the

given project is completed in given time. It mainly helps in ensuring that the given project is

completed within project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PROJECT COST MANAGEMENT TECHNIQUES

Budget

Budget mainly involves development of an approximation or estimation of cost of

resources which are needed for completion of various project activities. Cost Budgeting

generally comprises of overall estimation of cost involved in project which will help in

establishing a baseline for measuring the performance of various project.

Inputs required for cost Budgeting: There are certain tools involved in cost budgeting that are

estimation of cost, Work breakdown structure, schedule of project. It helps in estimation of cost

of various resources like hardware, software, development of team salaries, training, operation

labor which are involved in a project has been discussed in details. It can be present in summary

or in details (McNeil, Frey and Embrechts., 2015). Scheduling of project is inclusive of planned

start and proper finished dates for a project.

Tools for cost Budgeting: Tools and techniques are considered to be mandatory for project

development and estimation of cost and development of budget of various work items involved

in a project (Meng., 2012). There are certain tools like Analog estimation, parametric modelling,

Bottom-up estimation, tools for computerized, bottom up estimation, computerized tools.

Analog estimation: Analog estimation is also known as top down estimation which

means the cost of a previous project is compared with the present cost of project that is the

implementation of new call center in a large firm. This method is generally less expensive than

other method or techniques.

Parametric Modelling: Parametric modelling consist of various parameters of project in

a mathematical model which helps in analyzing the involved cost of this project that is the

implementation of new call center. Models can be simple or complex as per the needs it is used

Budget

Budget mainly involves development of an approximation or estimation of cost of

resources which are needed for completion of various project activities. Cost Budgeting

generally comprises of overall estimation of cost involved in project which will help in

establishing a baseline for measuring the performance of various project.

Inputs required for cost Budgeting: There are certain tools involved in cost budgeting that are

estimation of cost, Work breakdown structure, schedule of project. It helps in estimation of cost

of various resources like hardware, software, development of team salaries, training, operation

labor which are involved in a project has been discussed in details. It can be present in summary

or in details (McNeil, Frey and Embrechts., 2015). Scheduling of project is inclusive of planned

start and proper finished dates for a project.

Tools for cost Budgeting: Tools and techniques are considered to be mandatory for project

development and estimation of cost and development of budget of various work items involved

in a project (Meng., 2012). There are certain tools like Analog estimation, parametric modelling,

Bottom-up estimation, tools for computerized, bottom up estimation, computerized tools.

Analog estimation: Analog estimation is also known as top down estimation which

means the cost of a previous project is compared with the present cost of project that is the

implementation of new call center in a large firm. This method is generally less expensive than

other method or techniques.

Parametric Modelling: Parametric modelling consist of various parameters of project in

a mathematical model which helps in analyzing the involved cost of this project that is the

implementation of new call center. Models can be simple or complex as per the needs it is used

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PROJECT COST MANAGEMENT TECHNIQUES

accordingly. This model depends on various parameters like accurate information, various

parameters used are quantifiable and lastly it should be flexible that is it can work for large

project as well as for small project.

Bottom- up estimation: Techniques which are involved in estimation of specific and

individual work items and then adding the individual items for the various cost involved in a

project.

Computerized Tools: Various software tools like project management software and

spreadsheets are widely used for analyzing and estimation of cost (Schwalbe, 2015). Theses

software products can help in simplifying the use of tools involved in the project.

Outputs of cost Budgeting: Cost budgeting helps in analyzing the cost baseline of a

project. In this project that is the implementation of a new call center in an organization cost

baseline is a time phased budget which will help in measuring and controlling the performance

of cost involved in a project (Mir and Pinnington., 2014). It is developed by the help of

estimation of cost and displaying it in the form of S curve.

Monitoring Cost management

Cost management generally comprises of following factors like changes in the cost of

baseline to check for changes which can be beneficial for a firm and it also helps in analyzing the

bassline of cost involved in a project and also managing the changes which can occur in a project

like implementation of new call center in an organization.

It generally comprises of four factors that are:

accordingly. This model depends on various parameters like accurate information, various

parameters used are quantifiable and lastly it should be flexible that is it can work for large

project as well as for small project.

Bottom- up estimation: Techniques which are involved in estimation of specific and

individual work items and then adding the individual items for the various cost involved in a

project.

Computerized Tools: Various software tools like project management software and

spreadsheets are widely used for analyzing and estimation of cost (Schwalbe, 2015). Theses

software products can help in simplifying the use of tools involved in the project.

Outputs of cost Budgeting: Cost budgeting helps in analyzing the cost baseline of a

project. In this project that is the implementation of a new call center in an organization cost

baseline is a time phased budget which will help in measuring and controlling the performance

of cost involved in a project (Mir and Pinnington., 2014). It is developed by the help of

estimation of cost and displaying it in the form of S curve.

Monitoring Cost management

Cost management generally comprises of following factors like changes in the cost of

baseline to check for changes which can be beneficial for a firm and it also helps in analyzing the

bassline of cost involved in a project and also managing the changes which can occur in a project

like implementation of new call center in an organization.

It generally comprises of four factors that are:

5PROJECT COST MANAGEMENT TECHNIQUES

Analyzation of performance of cost to checking the plan.

Checking the various changes as recorded in the baseline of the cost involved.

It prevents incorrect and unauthorized changes being implanted in the cost

baseline.

Altering the various involved stakeholders about the authorized changes.

Inputs to cost controlling

There are generally four parameters involved in it and this are cost baseline, performance

report, change request and lastly cost management plan.

Report of performance: It helps in analyzing information on performance of cost like

the budget which has successfully completed and which has not been successfully completed

(Reiss., 2013). This report can beneficial to project team to tackle problem which can arise in

future.

Change in request: Change in request may in many forms which can be oral or written,

direct or indirect, external or internal which can be legally mandated or optional. Changes may

be considered to be important for increasing the budget or decreasing it.

Cost management plan: This plan describes how the variances in cost can be managed.

A cost management can be formal or informal which can have details on the various

requirements of the project.

Tools and methods for cost controlling

Change in cost control system: This system generally defines the various methods by

which the cost baseline can be easily changed. It is inclusive of paperwork, tracking systems and

Analyzation of performance of cost to checking the plan.

Checking the various changes as recorded in the baseline of the cost involved.

It prevents incorrect and unauthorized changes being implanted in the cost

baseline.

Altering the various involved stakeholders about the authorized changes.

Inputs to cost controlling

There are generally four parameters involved in it and this are cost baseline, performance

report, change request and lastly cost management plan.

Report of performance: It helps in analyzing information on performance of cost like

the budget which has successfully completed and which has not been successfully completed

(Reiss., 2013). This report can beneficial to project team to tackle problem which can arise in

future.

Change in request: Change in request may in many forms which can be oral or written,

direct or indirect, external or internal which can be legally mandated or optional. Changes may

be considered to be important for increasing the budget or decreasing it.

Cost management plan: This plan describes how the variances in cost can be managed.

A cost management can be formal or informal which can have details on the various

requirements of the project.

Tools and methods for cost controlling

Change in cost control system: This system generally defines the various methods by

which the cost baseline can be easily changed. It is inclusive of paperwork, tracking systems and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PROJECT COST MANAGEMENT TECHNIQUES

approval levels. Cost change control system should be added with the overall change control

system.

Measurement of performance: This technique is very useful in controlling the cost

involved in a project.

Additional Planning: Generally, few project run according to the plan and changes may

be required. Changes may be need new or update value of estimation of cost involved in a

project.

Computerized Tool: Various software equipment’s like project management software or

spreadsheet can be considered to be beneficial for keeping a track of expected cost vs real cost

and keeping a track of various effects of changes involved in it.

Benefits of Cost control

Helps in Revised estimation of cost: It is used for making changes in the cost

information which is helpful in managing the project. Right stakeholder must be informed as pefr

the need.

Budget Updates: Budget updates are nothing but updated form of cost estimation. In

other words, they can be stated as various changes which are involved in approval of cost

baseline.

Estimation at Completion: Estimation at cost or EAC is a forecast of total cost involved

in a project. Some of the techniques involved in a project are tracking of remaining portion of a

project, estimated of budget of the remaining work.

approval levels. Cost change control system should be added with the overall change control

system.

Measurement of performance: This technique is very useful in controlling the cost

involved in a project.

Additional Planning: Generally, few project run according to the plan and changes may

be required. Changes may be need new or update value of estimation of cost involved in a

project.

Computerized Tool: Various software equipment’s like project management software or

spreadsheet can be considered to be beneficial for keeping a track of expected cost vs real cost

and keeping a track of various effects of changes involved in it.

Benefits of Cost control

Helps in Revised estimation of cost: It is used for making changes in the cost

information which is helpful in managing the project. Right stakeholder must be informed as pefr

the need.

Budget Updates: Budget updates are nothing but updated form of cost estimation. In

other words, they can be stated as various changes which are involved in approval of cost

baseline.

Estimation at Completion: Estimation at cost or EAC is a forecast of total cost involved

in a project. Some of the techniques involved in a project are tracking of remaining portion of a

project, estimated of budget of the remaining work.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PROJECT COST MANAGEMENT TECHNIQUES

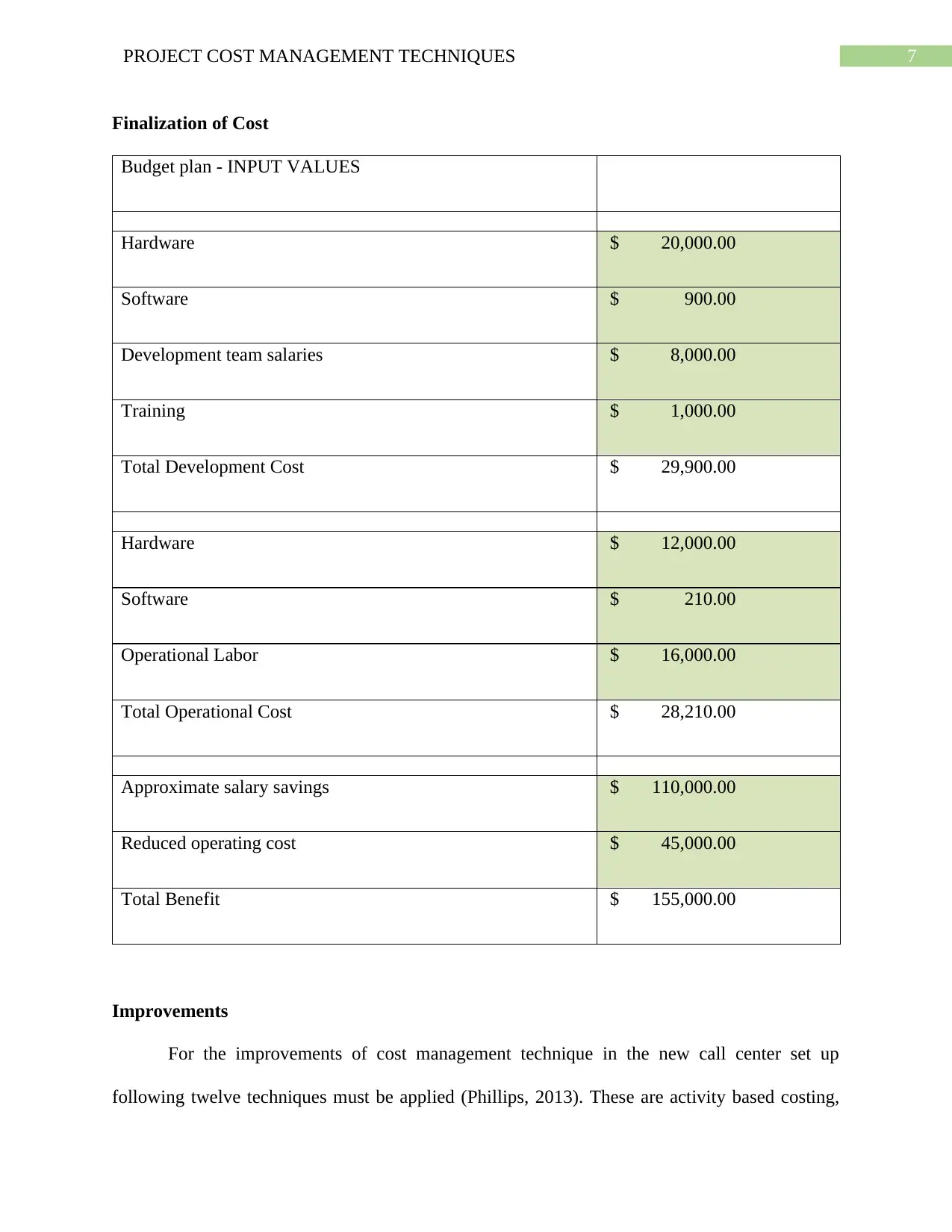

Finalization of Cost

Budget plan - INPUT VALUES

Hardware $ 20,000.00

Software $ 900.00

Development team salaries $ 8,000.00

Training $ 1,000.00

Total Development Cost $ 29,900.00

Hardware $ 12,000.00

Software $ 210.00

Operational Labor $ 16,000.00

Total Operational Cost $ 28,210.00

Approximate salary savings $ 110,000.00

Reduced operating cost $ 45,000.00

Total Benefit $ 155,000.00

Improvements

For the improvements of cost management technique in the new call center set up

following twelve techniques must be applied (Phillips, 2013). These are activity based costing,

Finalization of Cost

Budget plan - INPUT VALUES

Hardware $ 20,000.00

Software $ 900.00

Development team salaries $ 8,000.00

Training $ 1,000.00

Total Development Cost $ 29,900.00

Hardware $ 12,000.00

Software $ 210.00

Operational Labor $ 16,000.00

Total Operational Cost $ 28,210.00

Approximate salary savings $ 110,000.00

Reduced operating cost $ 45,000.00

Total Benefit $ 155,000.00

Improvements

For the improvements of cost management technique in the new call center set up

following twelve techniques must be applied (Phillips, 2013). These are activity based costing,

8PROJECT COST MANAGEMENT TECHNIQUES

target costing, total quality management, Benchmarking, Reengineering of various business

process, JIT inventory control system, maintaining a balance score card, six sigmas, life cycle

costing, Kaizan costing, Theory of constraints and lastly activity based management.

Kaizan Costing: It refers to the continuous and gradual upgradation through small

activities instead of large or radical movement which can be achieved through innovation or

innovation in technology (Potts and Ankrah, 2014). In other words, it can be stated as the method

of cost reduction which takes place during the manufacturing phase of the product. This method

can be used in the implementation of new call center as it can benefit it through a number of

ways.

Six Sigma: This method or technique was first implement in Motorola which is a well-

known organization. This method mainly focuses in reducing the cost, improvisation of process

and increase in profits (Potts and Ankrah., 2014). This method consists of six steps like

identification of process, defining of it, taking proper measure, analysis of it, improvisation and

lastly control. Above mentioned steps can be proved to be beneficial for this organization that is

call center. If this methodology is applied in this call center setup it can help in reducing different

cost involved in it. This will ultimately help in reducing various cost which are involved in the

set of this project.

target costing, total quality management, Benchmarking, Reengineering of various business

process, JIT inventory control system, maintaining a balance score card, six sigmas, life cycle

costing, Kaizan costing, Theory of constraints and lastly activity based management.

Kaizan Costing: It refers to the continuous and gradual upgradation through small

activities instead of large or radical movement which can be achieved through innovation or

innovation in technology (Potts and Ankrah, 2014). In other words, it can be stated as the method

of cost reduction which takes place during the manufacturing phase of the product. This method

can be used in the implementation of new call center as it can benefit it through a number of

ways.

Six Sigma: This method or technique was first implement in Motorola which is a well-

known organization. This method mainly focuses in reducing the cost, improvisation of process

and increase in profits (Potts and Ankrah., 2014). This method consists of six steps like

identification of process, defining of it, taking proper measure, analysis of it, improvisation and

lastly control. Above mentioned steps can be proved to be beneficial for this organization that is

call center. If this methodology is applied in this call center setup it can help in reducing different

cost involved in it. This will ultimately help in reducing various cost which are involved in the

set of this project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PROJECT COST MANAGEMENT TECHNIQUES

References

DRURY, C.M., 2013. Management and cost accounting. Springer.

Flyvbjerg, B., 2013. From Nobel prize to project management: getting risks right. arXiv preprint

arXiv:1302.3642.

Kerzner, H., 2013. Project management: a systems approach to planning, scheduling, and

controlling. John Wiley & Sons.prize to project management: getting risks right. arXiv preprint

arXiv:1302.3642.

Larson, E.W. and Gray, C., 2013. Project Management: The Managerial Process with MS

Project. McGraw-Hill.

Martinelli, R.J. and Milosevic, D.Z., 2016. Project management toolbox: tools and techniques for

the practicing project manager. John Wiley & Sons.

McNeil, A.J., Frey, R. and Embrechts, P., 2015. Quantitative risk management: Concepts,

techniques and tools. Princeton university press.

Meng, X., 2012. The effect of relationship management on project performance in

construction. International journal of project management, 30(2), pp.188-198.

Mir, F.A. and Pinnington, A.H., 2014. Exploring the value of project management: linking

project management performance and project success. International journal of project

management, 32(2), pp.202-217.

Phillips, J., 2013. PMP, Project Management Professional (Certification Study Guides).

McGraw-Hill Osborne Media.

References

DRURY, C.M., 2013. Management and cost accounting. Springer.

Flyvbjerg, B., 2013. From Nobel prize to project management: getting risks right. arXiv preprint

arXiv:1302.3642.

Kerzner, H., 2013. Project management: a systems approach to planning, scheduling, and

controlling. John Wiley & Sons.prize to project management: getting risks right. arXiv preprint

arXiv:1302.3642.

Larson, E.W. and Gray, C., 2013. Project Management: The Managerial Process with MS

Project. McGraw-Hill.

Martinelli, R.J. and Milosevic, D.Z., 2016. Project management toolbox: tools and techniques for

the practicing project manager. John Wiley & Sons.

McNeil, A.J., Frey, R. and Embrechts, P., 2015. Quantitative risk management: Concepts,

techniques and tools. Princeton university press.

Meng, X., 2012. The effect of relationship management on project performance in

construction. International journal of project management, 30(2), pp.188-198.

Mir, F.A. and Pinnington, A.H., 2014. Exploring the value of project management: linking

project management performance and project success. International journal of project

management, 32(2), pp.202-217.

Phillips, J., 2013. PMP, Project Management Professional (Certification Study Guides).

McGraw-Hill Osborne Media.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PROJECT COST MANAGEMENT TECHNIQUES

Potts, K. and Ankrah, N., 2014. Construction cost management: learning from case studies.

Routledge.

Reiss, G., 2013. Project management demystified: Today's tools and techniques. Routledge.

Schwalbe, K., 2015. Information technology project management. Cengage Learning.

Potts, K. and Ankrah, N., 2014. Construction cost management: learning from case studies.

Routledge.

Reiss, G., 2013. Project management demystified: Today's tools and techniques. Routledge.

Schwalbe, K., 2015. Information technology project management. Cengage Learning.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.