Kaplan Professional Diploma in Finance and Mortgage Broking Project

VerifiedAdded on 2020/06/05

|106

|27174

|54

Project

AI Summary

This project, designed for the Diploma of Finance and Mortgage Broking Management (DIPMB), focuses on client identification, complex lending, and business management skills. The project is split into two sections. Section 1 requires answering questions based on case studies of different lending scenarios. Section 2 involves completing tasks related to business management. The project assesses competence through a series of tasks, with feedback provided for improvement. The project also examines strategic alliances, business expansion, and relationship management within Capital City Finance and Mortgage Brokers (CCF & MB), including considerations for existing strategic partners and the company's vision, mission, and values. The solution provides detailed responses to tasks, feedback analysis, and resubmission considerations for tasks marked as "Not Yet Competent."

Project

Diploma of Finance and Mortgage Broking Management

(DIPMB_AS_v1A3)

Client identification (client to complete)

Please complete the fields shaded grey.

Project result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Not Yet Competent

Parts that must be resubmitted:

1, 2, 3, 7 and 8

Result — resubmission (if applicable)

Diploma of Finance and Mortgage Broking Management

(DIPMB_AS_v1A3)

Client identification (client to complete)

Please complete the fields shaded grey.

Project result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Not Yet Competent

Parts that must be resubmitted:

1, 2, 3, 7 and 8

Result — resubmission (if applicable)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

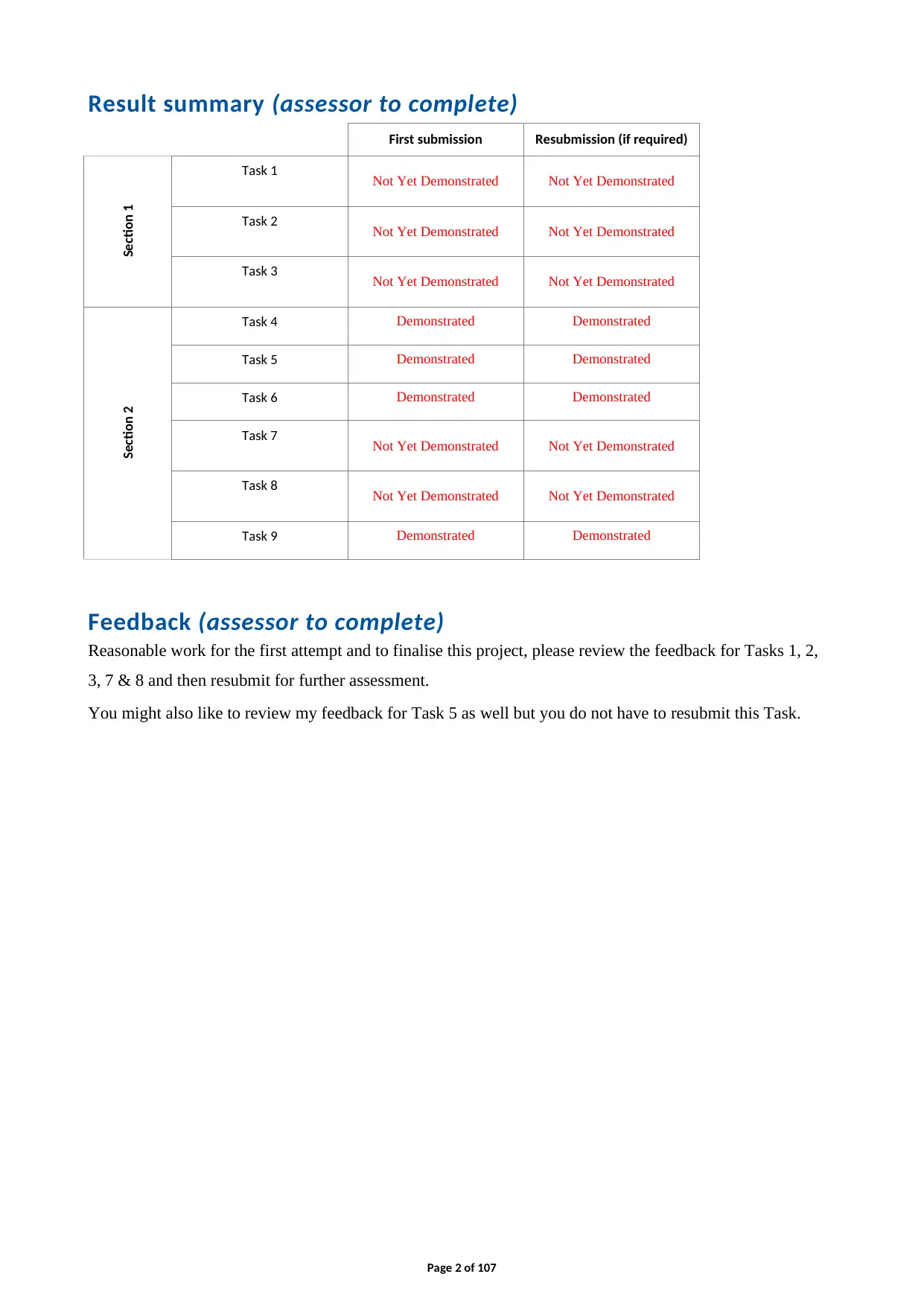

Result summary (assessor to complete)

First submission Resubmission (if required)

Section 1

Task 1 Not Yet Demonstrated Not Yet Demonstrated

Task 2 Not Yet Demonstrated Not Yet Demonstrated

Task 3 Not Yet Demonstrated Not Yet Demonstrated

Section 2

Task 4 Demonstrated Demonstrated

Task 5 Demonstrated Demonstrated

Task 6 Demonstrated Demonstrated

Task 7 Not Yet Demonstrated Not Yet Demonstrated

Task 8 Not Yet Demonstrated Not Yet Demonstrated

Task 9 Demonstrated Demonstrated

Feedback (assessor to complete)

Reasonable work for the first attempt and to finalise this project, please review the feedback for Tasks 1, 2,

3, 7 & 8 and then resubmit for further assessment.

You might also like to review my feedback for Task 5 as well but you do not have to resubmit this Task.

Page 2 of 107

First submission Resubmission (if required)

Section 1

Task 1 Not Yet Demonstrated Not Yet Demonstrated

Task 2 Not Yet Demonstrated Not Yet Demonstrated

Task 3 Not Yet Demonstrated Not Yet Demonstrated

Section 2

Task 4 Demonstrated Demonstrated

Task 5 Demonstrated Demonstrated

Task 6 Demonstrated Demonstrated

Task 7 Not Yet Demonstrated Not Yet Demonstrated

Task 8 Not Yet Demonstrated Not Yet Demonstrated

Task 9 Demonstrated Demonstrated

Feedback (assessor to complete)

Reasonable work for the first attempt and to finalise this project, please review the feedback for Tasks 1, 2,

3, 7 & 8 and then resubmit for further assessment.

You might also like to review my feedback for Task 5 as well but you do not have to resubmit this Task.

Page 2 of 107

Page 3 of 107

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Before you begin

Read everything in this document before you start your project for .

About this document

This document includes the following parts:

• Instructions for completing and submitting this project

• Results and feedback

• Section 1: Complex lending and broking

• Section 2: Business management skills

Instructions for completing and submitting this project

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to

complete the project within your enrolment period. Your study plan is in the KapLearn

subject room.

Completing the project

The project

This project is split over 2 sections. The information and data you need to complete Sections 1 & 2

is presented in case studies at the beginning of those sections and each task.

Section 1: Complex Lending and Broking

The first section on complex lending and broking, requires you to answer the questions for one (1)

of the three (3) available case studies. Each case study focuses on different lending scenario, (see

diagram below).

Page 4 of 107

Read everything in this document before you start your project for .

About this document

This document includes the following parts:

• Instructions for completing and submitting this project

• Results and feedback

• Section 1: Complex lending and broking

• Section 2: Business management skills

Instructions for completing and submitting this project

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to

complete the project within your enrolment period. Your study plan is in the KapLearn

subject room.

Completing the project

The project

This project is split over 2 sections. The information and data you need to complete Sections 1 & 2

is presented in case studies at the beginning of those sections and each task.

Section 1: Complex Lending and Broking

The first section on complex lending and broking, requires you to answer the questions for one (1)

of the three (3) available case studies. Each case study focuses on different lending scenario, (see

diagram below).

Page 4 of 107

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

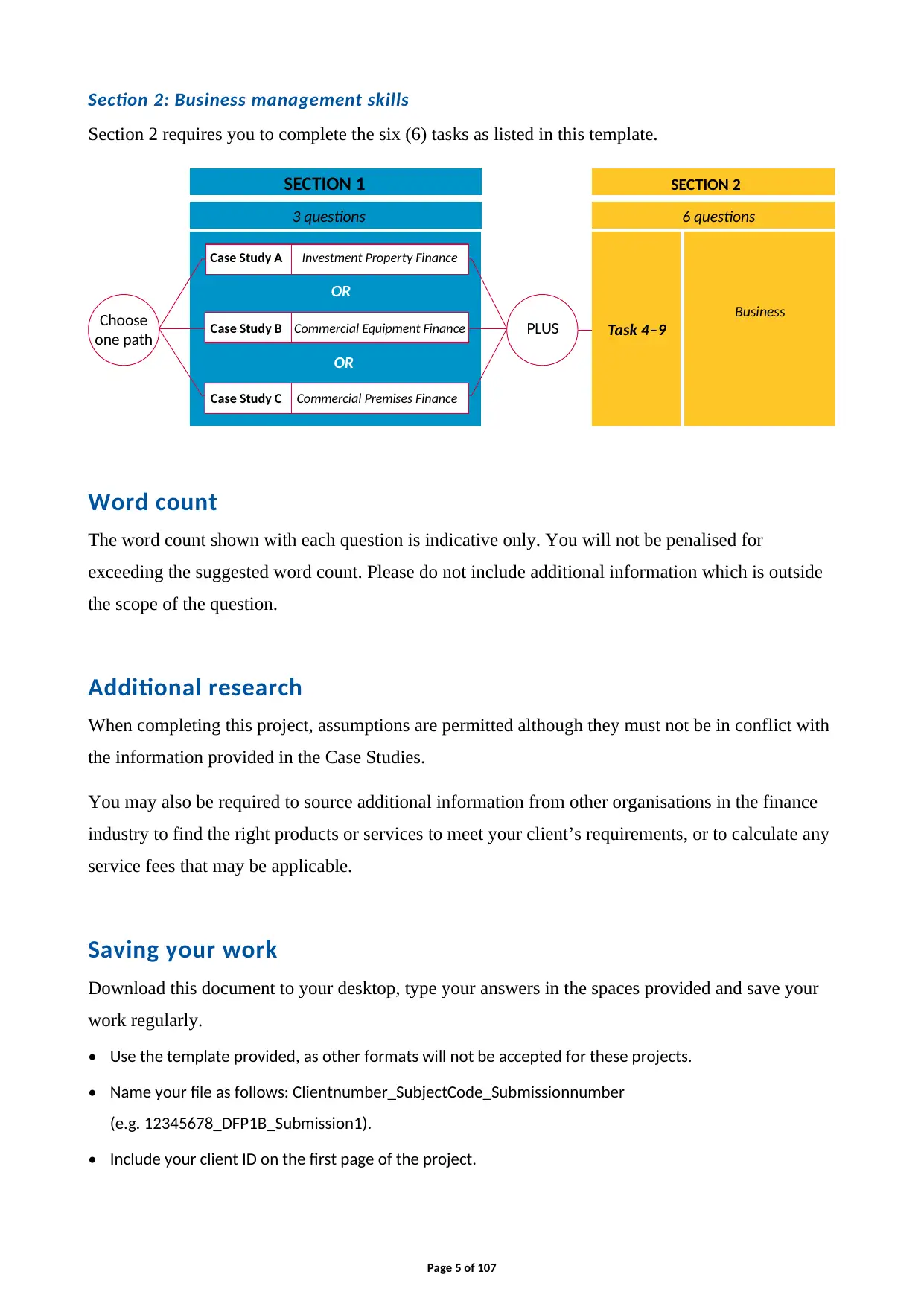

Section 2: Business management skills

Section 2 requires you to complete the six (6) tasks as listed in this template.

SECTION 1 SECTION 2

3 questions 6 questions

Choose

one path PLUS

Case Study A

Case Study B

Case Study C

Investment Property Finance

Commercial Equipment Finance

Commercial Premises Finance

OR

OR

Task 4–9

Business

Word count

The word count shown with each question is indicative only. You will not be penalised for

exceeding the suggested word count. Please do not include additional information which is outside

the scope of the question.

Additional research

When completing this project, assumptions are permitted although they must not be in conflict with

the information provided in the Case Studies.

You may also be required to source additional information from other organisations in the finance

industry to find the right products or services to meet your client’s requirements, or to calculate any

service fees that may be applicable.

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your

work regularly.

• Use the template provided, as other formats will not be accepted for these projects.

• Name your file as follows: Clientnumber_SubjectCode_Submissionnumber

(e.g. 12345678_DFP1B_Submission1).

• Include your client ID on the first page of the project.

Page 5 of 107

Section 2 requires you to complete the six (6) tasks as listed in this template.

SECTION 1 SECTION 2

3 questions 6 questions

Choose

one path PLUS

Case Study A

Case Study B

Case Study C

Investment Property Finance

Commercial Equipment Finance

Commercial Premises Finance

OR

OR

Task 4–9

Business

Word count

The word count shown with each question is indicative only. You will not be penalised for

exceeding the suggested word count. Please do not include additional information which is outside

the scope of the question.

Additional research

When completing this project, assumptions are permitted although they must not be in conflict with

the information provided in the Case Studies.

You may also be required to source additional information from other organisations in the finance

industry to find the right products or services to meet your client’s requirements, or to calculate any

service fees that may be applicable.

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your

work regularly.

• Use the template provided, as other formats will not be accepted for these projects.

• Name your file as follows: Clientnumber_SubjectCode_Submissionnumber

(e.g. 12345678_DFP1B_Submission1).

• Include your client ID on the first page of the project.

Page 5 of 107

Before you submit your work, please do a spell check and proofread your work to ensure that

everything is clear and unambiguous.

Page 6 of 107

everything is clear and unambiguous.

Page 6 of 107

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Submitting the project

You must submit your completed project in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not delete/remove any sections of the document template.

Do not save your completed project as a PDF.

The project must be completed before submitting it to Kaplan Professional Education.

Incomplete projects will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your project for marking you will be unable

to make any further changes to it.

You are able to submit your project earlier than the deadline if you are confident you have

completed all parts and have prepared a quality submission.

The project marking process

You have 12 weeks from the date of your enrolment in this subject to submit your

completed project.

Should your project be deemed ‘not yet competent’ you will be give an additional four (4) weeks to

resubmit your project.

Your assessor will mark your project and return it to you in the subject room in KapLearn under

the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your project. Failure to do so will mean that your project will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your

submission deadline to submit your completed project.

Page 7 of 107

You must submit your completed project in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not delete/remove any sections of the document template.

Do not save your completed project as a PDF.

The project must be completed before submitting it to Kaplan Professional Education.

Incomplete projects will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your project for marking you will be unable

to make any further changes to it.

You are able to submit your project earlier than the deadline if you are confident you have

completed all parts and have prepared a quality submission.

The project marking process

You have 12 weeks from the date of your enrolment in this subject to submit your

completed project.

Should your project be deemed ‘not yet competent’ you will be give an additional four (4) weeks to

resubmit your project.

Your assessor will mark your project and return it to you in the subject room in KapLearn under

the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your project. Failure to do so will mean that your project will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your

submission deadline to submit your completed project.

Page 7 of 107

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

How your project is graded

Project tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet

competent.

Your assessor will follow the below process when marking your project:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

Page 8 of 107

Project tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet

competent.

Your assessor will follow the below process when marking your project:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

Page 8 of 107

‘Not yet competent’ and resubmissions

Should sections of your project be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the

required level.

You must address the assessor’s feedback in your amended responses. You only need amend those

sections where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission.

Your assessor will be in a better position to gauge the quality and nature of your changes. Ensure

you leave your first assessor’s comments in your project, so your second assessor can see the

instructions that were originally provided for you. Do not change any comments made by a

Kaplan assessor.

We are here to help

If you have any questions about this project you can post your query at the ‘Ask your Tutor’ forum

in your subject room. You can expect an answer within 24 hours of your posting from one of our

technical advisers or client support staff.

Page 9 of 107

Should sections of your project be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the

required level.

You must address the assessor’s feedback in your amended responses. You only need amend those

sections where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission.

Your assessor will be in a better position to gauge the quality and nature of your changes. Ensure

you leave your first assessor’s comments in your project, so your second assessor can see the

instructions that were originally provided for you. Do not change any comments made by a

Kaplan assessor.

We are here to help

If you have any questions about this project you can post your query at the ‘Ask your Tutor’ forum

in your subject room. You can expect an answer within 24 hours of your posting from one of our

technical advisers or client support staff.

Page 9 of 107

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital City Finance and Mortgage Brokers (CCF &

MB)

George and Mildred are very happy with the way you service your clients and are sure that you are

a good fit for the team. They now want you to turn your focus to your primary task which is to

assist in expanding the business by building relationships with selected real estate agents,

accountants and legal firms through strategic alliances. They also want you to consider how CCF &

MB can consolidate its relationships with its existing strategic partners.

Let’s recap on what you already know about Capital City Finance and Mortgage Brokers (CCF &

MB).

It’s a family owned business providing a range of mortgage and finance broking services to the

business and private sectors, with experience in all facets of finance and insurance providing expert

advice covering a multitude of products and options existing within the market.

CCF & MB specialises in home loans, commercial lending, business lending, personal and motor

vehicle finance and insurance (life and general), and focuses on helping clients find the finance

service suited to their individual circumstances.

It provides its services through its association with the following partners:

• Australian Aggregators, a rising business in the aggregation business with an extensive panel of

residential and commercial lenders, and asset finance.

• ABC General Insurance, a boutique insurance company specializing in a full range of general insurances.

• XYZ Life a small family-owned insurance brokerage specializing in the full range of life insurance

products.

Based in the city, CCF & MB has the capacity to service clients from their office or anywhere at

their clients’ convenience through its team of mobile brokers.

CCF & MB does not hold a credit license but operates as a credit representative of Australian

Aggregators.

Since its inception 13 years ago CCF & MB has built a loan book of almost $1.2 billion and

averages over $120 million in new loans annually.

CCF & MB’s vision is to be the mortgage and finance broker of choice in the greater metropolitan

area

CCF & MB’s mission statement is to operate professionally in accordance with legislation, our

licence and professional standards

Page 10 of 107

MB)

George and Mildred are very happy with the way you service your clients and are sure that you are

a good fit for the team. They now want you to turn your focus to your primary task which is to

assist in expanding the business by building relationships with selected real estate agents,

accountants and legal firms through strategic alliances. They also want you to consider how CCF &

MB can consolidate its relationships with its existing strategic partners.

Let’s recap on what you already know about Capital City Finance and Mortgage Brokers (CCF &

MB).

It’s a family owned business providing a range of mortgage and finance broking services to the

business and private sectors, with experience in all facets of finance and insurance providing expert

advice covering a multitude of products and options existing within the market.

CCF & MB specialises in home loans, commercial lending, business lending, personal and motor

vehicle finance and insurance (life and general), and focuses on helping clients find the finance

service suited to their individual circumstances.

It provides its services through its association with the following partners:

• Australian Aggregators, a rising business in the aggregation business with an extensive panel of

residential and commercial lenders, and asset finance.

• ABC General Insurance, a boutique insurance company specializing in a full range of general insurances.

• XYZ Life a small family-owned insurance brokerage specializing in the full range of life insurance

products.

Based in the city, CCF & MB has the capacity to service clients from their office or anywhere at

their clients’ convenience through its team of mobile brokers.

CCF & MB does not hold a credit license but operates as a credit representative of Australian

Aggregators.

Since its inception 13 years ago CCF & MB has built a loan book of almost $1.2 billion and

averages over $120 million in new loans annually.

CCF & MB’s vision is to be the mortgage and finance broker of choice in the greater metropolitan

area

CCF & MB’s mission statement is to operate professionally in accordance with legislation, our

licence and professional standards

Page 10 of 107

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CCF & MB’s values are as follows:

• To act with honesty and integrity at all times

• To provide unbiased advice and conduct business, free from any conflict of interest

• To maintain confidentiality in all dealings

• To meet all NCCP regulatory requirements

• To comply with all mortgage industry laws and regulations

• ensure quality and efficiency in its loan processes.

Page 11 of 107

• To act with honesty and integrity at all times

• To provide unbiased advice and conduct business, free from any conflict of interest

• To maintain confidentiality in all dealings

• To meet all NCCP regulatory requirements

• To comply with all mortgage industry laws and regulations

• ensure quality and efficiency in its loan processes.

Page 11 of 107

CCF & MB’s people

CCF & MB is owned by husband and wife, George and Mildred Spencer.

With over 35 years’ experience in finance and business ownership, George established and built a

successful business dedicated to assisting clients with managing their finances effectively. Starting

the business with his wife Mildred 13 years ago, George gained immense satisfaction in seeing it

expand to service more and more clients across the city and greater metropolitan area. Although in

recent years he has stepped back from dealing directly with clients, he still maintains a small select

clientele. He also takes great pride in training and mentoring his team to enhance their performance.

Mildred has over 22 years of lending experience and is qualified not only to assist her clients with

their mortgage requirements but also to assist them with their commercial finance requirements. She

also holds financial planning qualifications. She specialises in asset finance.

The company has a small team of five additional consultants and two administration staff members.

Profiles for the team is as follows:

• Jennifer Dee is recognized as one of the top female brokers in Australia. She has been in the broking

industry for over 10 years and has a passion and dedication to assist and accommodate all of her clients’

needs with their financial dreams. Jennifer is an Accredited Mortgage Consultant with the Mortgage and

Finance Association of Australia (MFAA).

• Louise Spencer (George and Mildred’s eldest daughter) is an Accredited Mortgage Consultant with the

Mortgage and Finance Association of Australia (MFAA) and has been working as a loan consultant for

almost two years. Louise started off in the lending industry in the office as an administrator to gain as

much experience and knowledge as possible before taking a broking role. Her passion for helping her

clients ensures that she is always available to her clients at a time and place convenient for them.

• Michael Spencer is George’s younger brother and is CCF & MB’s equipment finance specialist. He has

over 25 years working in the equipment finance industry. He has developed an in depth understanding

of the transport and agricultural industries, and also provides finance for general equipment,

motor vehicles and computer equipment.

• Martin Long has specialized in equipment finance for the last three years, but prior to this he spent

five years operating his own retail food business. This practical experience allows him to see things from

his client’s point of view, including experience with equipment finance. He specializes in plant and

equipment in the machinery, woodworking and packaging industries. Examples of some of the

equipment he has financed are farm machinery, extrusion lines, plastic injection moulders,

commercial catering equipment, woodworking plant, packaging lines, forklifts, office fit-outs and many

different motor vehicles.

Page 12 of 107

CCF & MB is owned by husband and wife, George and Mildred Spencer.

With over 35 years’ experience in finance and business ownership, George established and built a

successful business dedicated to assisting clients with managing their finances effectively. Starting

the business with his wife Mildred 13 years ago, George gained immense satisfaction in seeing it

expand to service more and more clients across the city and greater metropolitan area. Although in

recent years he has stepped back from dealing directly with clients, he still maintains a small select

clientele. He also takes great pride in training and mentoring his team to enhance their performance.

Mildred has over 22 years of lending experience and is qualified not only to assist her clients with

their mortgage requirements but also to assist them with their commercial finance requirements. She

also holds financial planning qualifications. She specialises in asset finance.

The company has a small team of five additional consultants and two administration staff members.

Profiles for the team is as follows:

• Jennifer Dee is recognized as one of the top female brokers in Australia. She has been in the broking

industry for over 10 years and has a passion and dedication to assist and accommodate all of her clients’

needs with their financial dreams. Jennifer is an Accredited Mortgage Consultant with the Mortgage and

Finance Association of Australia (MFAA).

• Louise Spencer (George and Mildred’s eldest daughter) is an Accredited Mortgage Consultant with the

Mortgage and Finance Association of Australia (MFAA) and has been working as a loan consultant for

almost two years. Louise started off in the lending industry in the office as an administrator to gain as

much experience and knowledge as possible before taking a broking role. Her passion for helping her

clients ensures that she is always available to her clients at a time and place convenient for them.

• Michael Spencer is George’s younger brother and is CCF & MB’s equipment finance specialist. He has

over 25 years working in the equipment finance industry. He has developed an in depth understanding

of the transport and agricultural industries, and also provides finance for general equipment,

motor vehicles and computer equipment.

• Martin Long has specialized in equipment finance for the last three years, but prior to this he spent

five years operating his own retail food business. This practical experience allows him to see things from

his client’s point of view, including experience with equipment finance. He specializes in plant and

equipment in the machinery, woodworking and packaging industries. Examples of some of the

equipment he has financed are farm machinery, extrusion lines, plastic injection moulders,

commercial catering equipment, woodworking plant, packaging lines, forklifts, office fit-outs and many

different motor vehicles.

Page 12 of 107

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 106

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.