ALLCURE INC. Project Evaluation Report: FIN20014 Financial Management

VerifiedAdded on 2023/06/04

|21

|3980

|161

Report

AI Summary

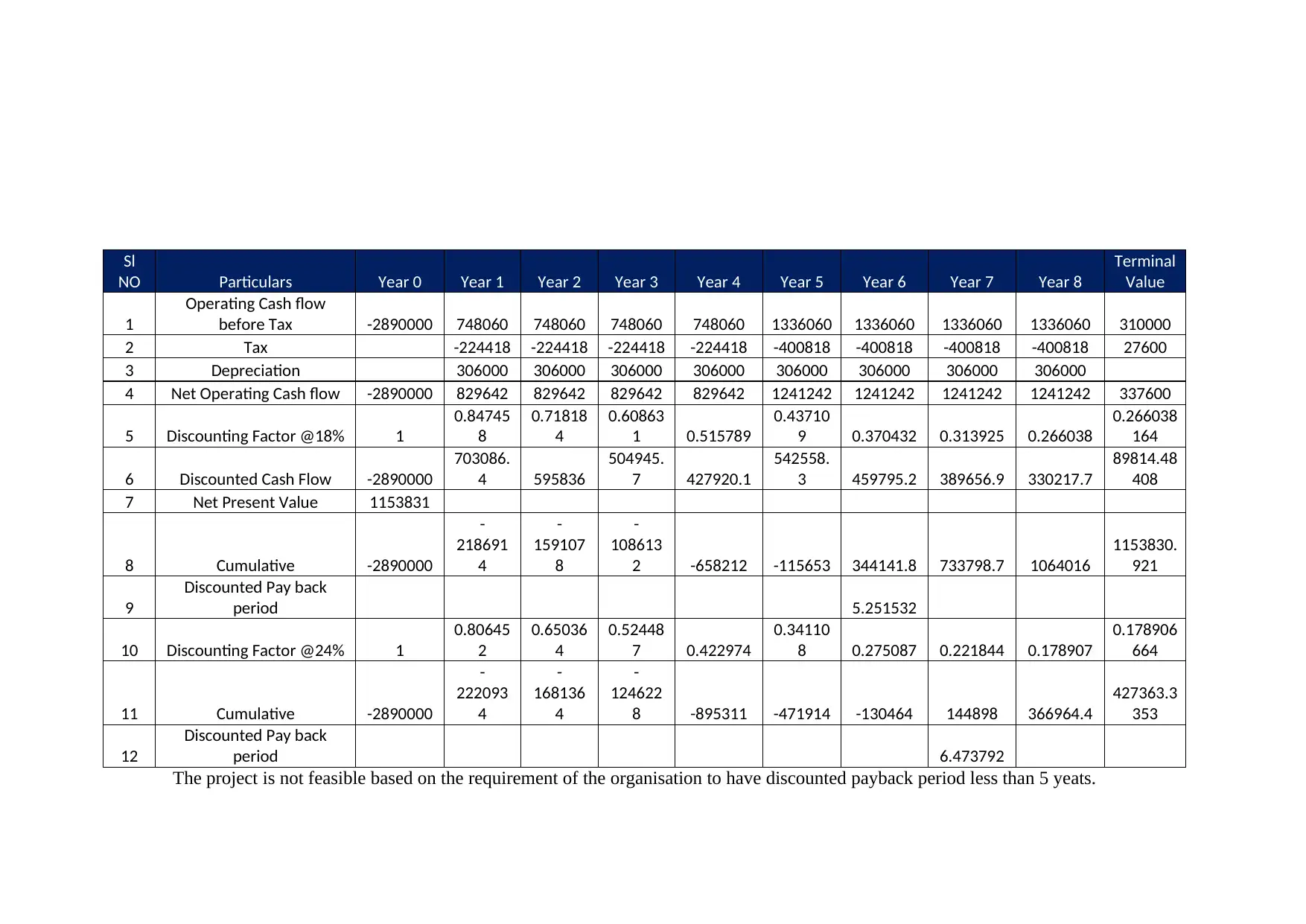

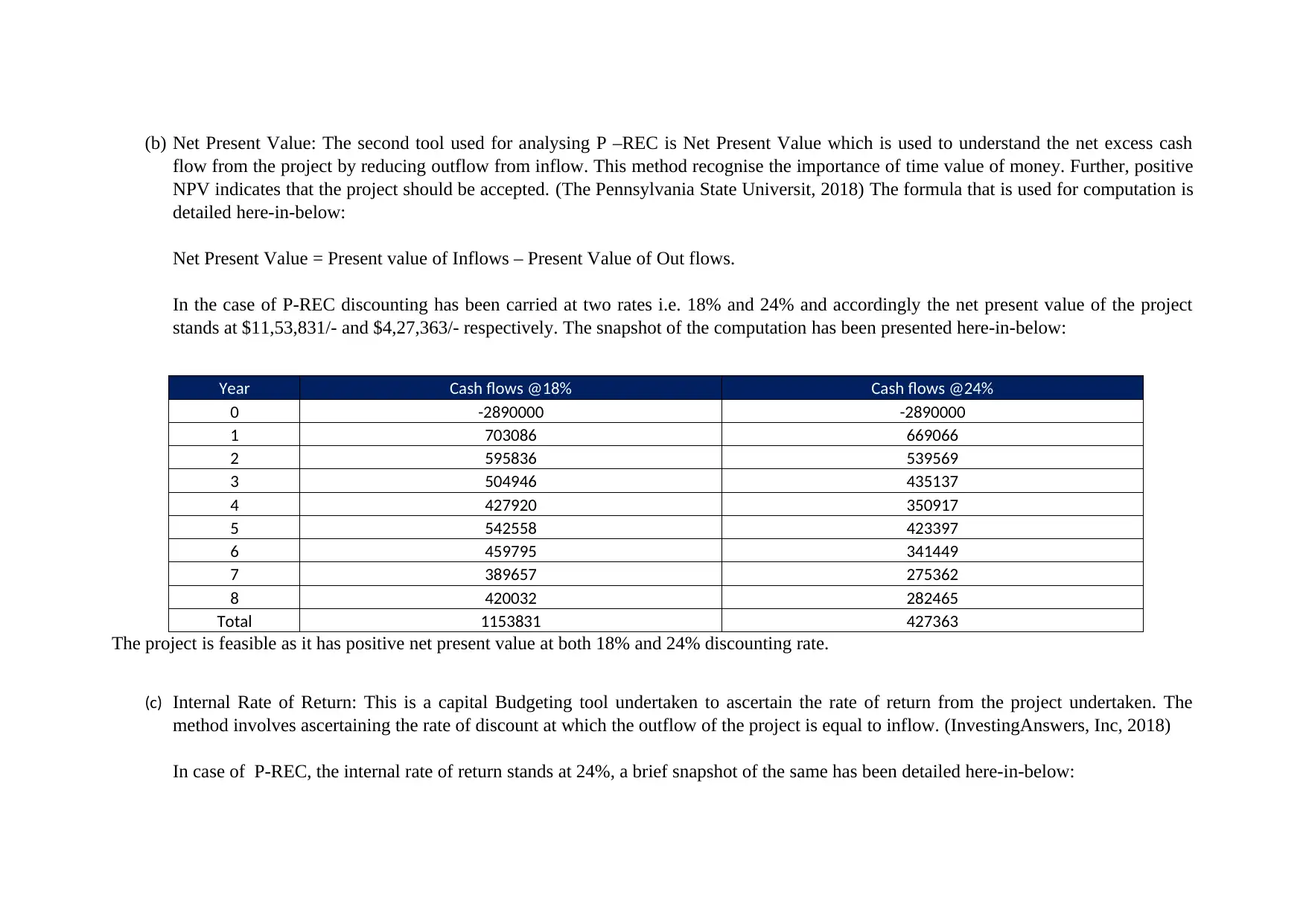

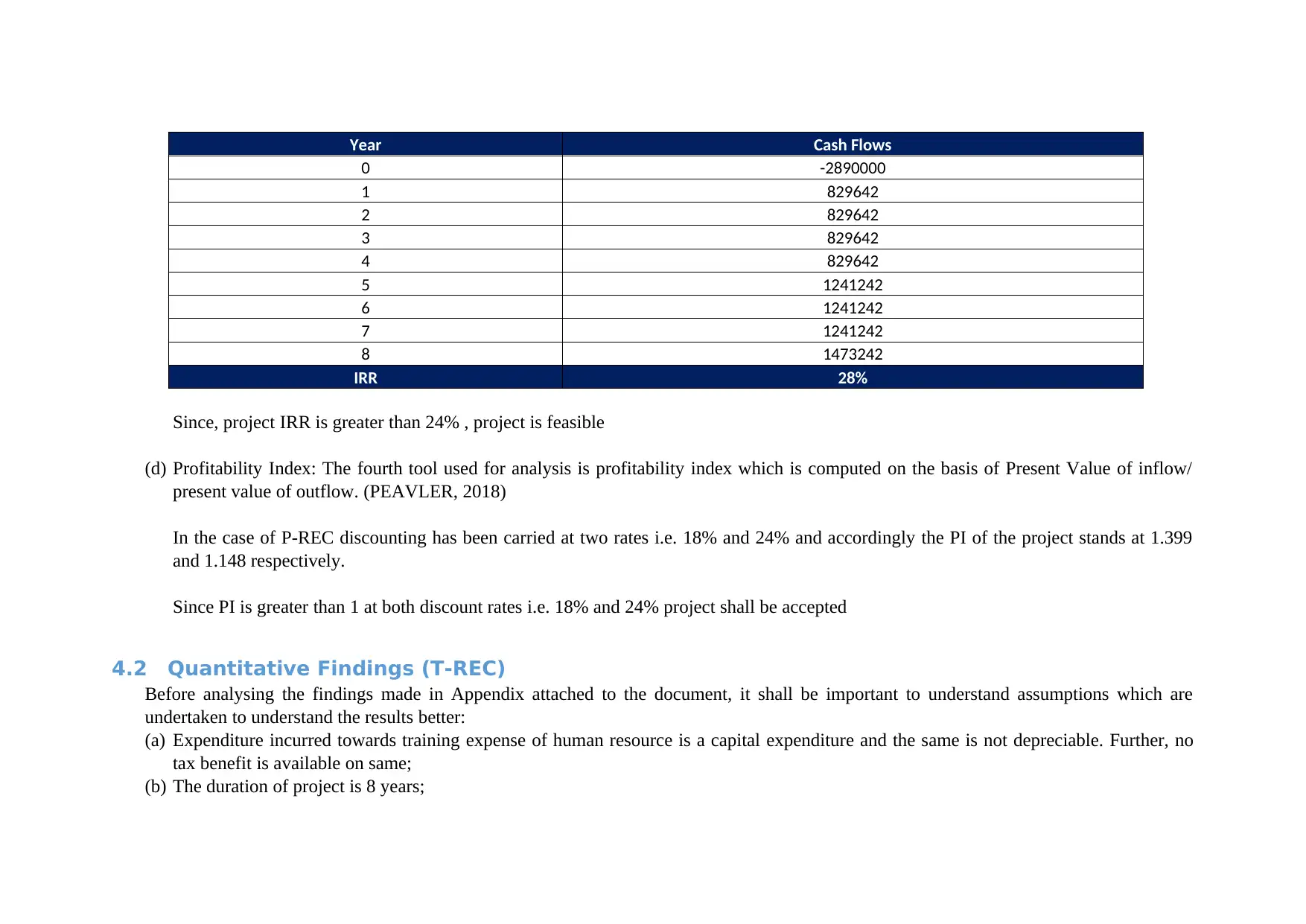

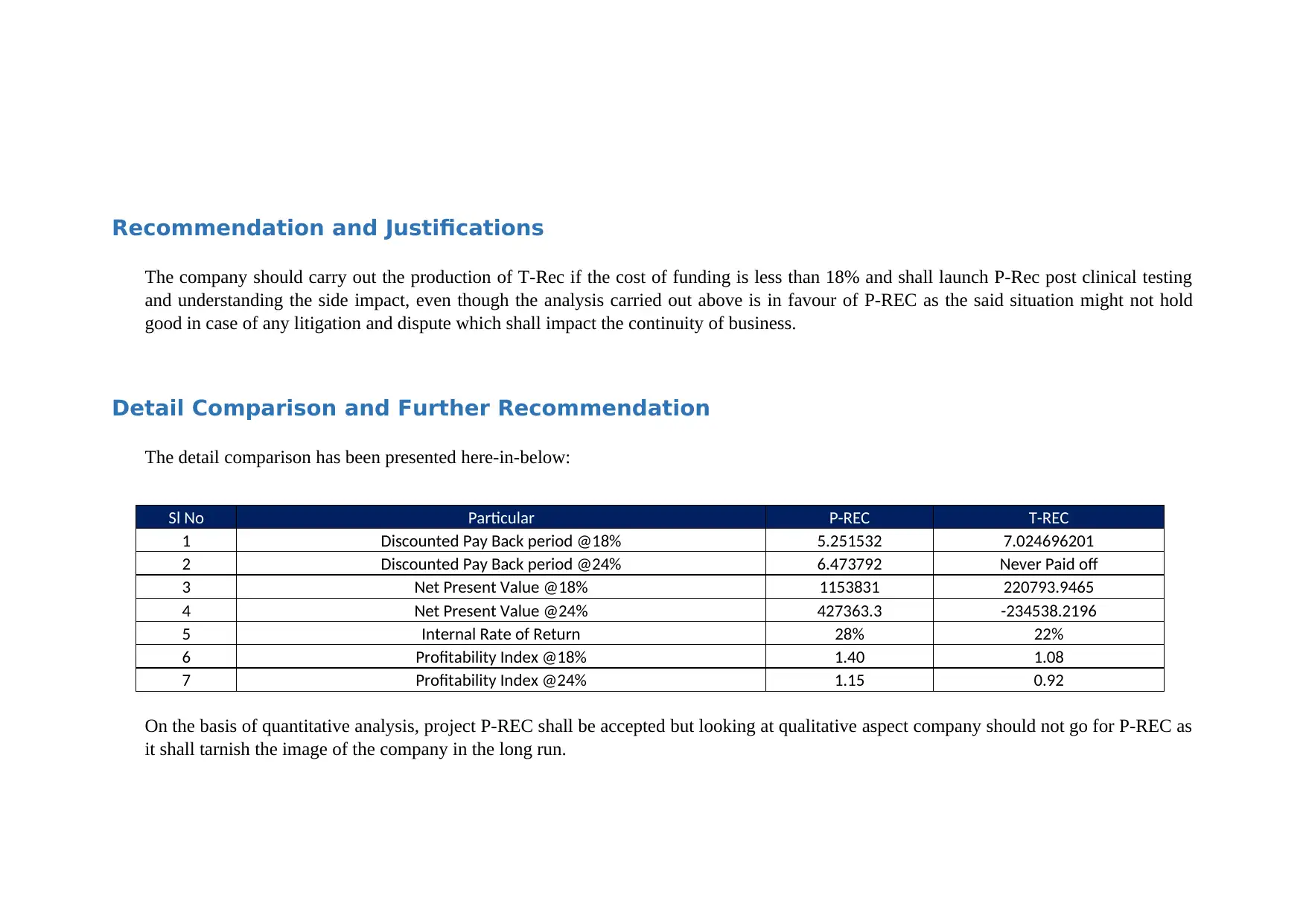

This report provides a detailed analysis of two investment proposals, T-REC and P-REC, for ALLCURE INC. The evaluation encompasses both quantitative and qualitative aspects, utilizing parameters such as Net Present Value (NPV), Profitability Index (PI), Internal Rate of Return (IRR), and Discounted Payback Period. Quantitative findings are presented for both projects under different discount rates (18% and 24%), revealing that both projects are feasible at an 18% discount rate. However, T-REC is deemed not feasible at 24%. The report includes assumptions, detailed computations, and a comparison of the projects based on financial metrics and qualitative factors like risk, potential litigation, and competitor actions. The report concludes with a recommendation to proceed with T-REC, given its clinical safety and lower risk profile, while suggesting further testing for P-REC before launch. The report also includes financial analysis and recommendations. References are also provided.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.