Project Financial Management: Expansion, Financing, and Variance

VerifiedAdded on 2021/02/19

|10

|2134

|321

Report

AI Summary

This report on Project Financial Management analyzes a manufacturing company's expansion options, focusing on identifying the most profitable choices through time-value and non-time-value measures, concluding that option C is the best. It explores various financing options available to project managers, categorizing them under equity and debt, with a recommendation for equity funds and capital markets. The report also conducts a variance analysis of actual versus budgeted costs for Xyz Company, highlighting discrepancies in direct labor, direct material, and variable overheads, and identifies market value and trends as contributing factors. Finally, the report outlines five approaches to project cost estimation: analogous, parametric, rough order of magnitude, subject matter experts, and three-point estimation.

PROJECT FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION.......................................................................................................................................................................................3

MAIN BODY..............................................................................................................................................................................................3

SECTION A.................................................................................................................................................................................................3

Question 1 Feasibility of the expansion options......................................................................................................................................3

SECTION B.................................................................................................................................................................................................5

Question 2 Financing options available for project managers.................................................................................................................5

Question 3 Variance Analysis.................................................................................................................................................................6

Question 4 Approaches for project cost estimation.................................................................................................................................7

CONCLUSION............................................................................................................................................................................................8

REFERENCES................................................................................................................................................................................................................. 1

Table 1Time and non-time based analysis...................................................................................................................................................3

Table 2Variance analysis.............................................................................................................................................................................6

INTRODUCTION.......................................................................................................................................................................................3

MAIN BODY..............................................................................................................................................................................................3

SECTION A.................................................................................................................................................................................................3

Question 1 Feasibility of the expansion options......................................................................................................................................3

SECTION B.................................................................................................................................................................................................5

Question 2 Financing options available for project managers.................................................................................................................5

Question 3 Variance Analysis.................................................................................................................................................................6

Question 4 Approaches for project cost estimation.................................................................................................................................7

CONCLUSION............................................................................................................................................................................................8

REFERENCES................................................................................................................................................................................................................. 1

Table 1Time and non-time based analysis...................................................................................................................................................3

Table 2Variance analysis.............................................................................................................................................................................6

INTRODUCTION

Project Financial Management can be basically defined as a process through which planned and budgeted data and

accounting done with relation to a specific project is brought together with the actual one and the performance is then evaluated

(Livdan and Nezlobin, 2017). In the current report, it has been identified how a company can evaluate its growth options and then take

decisions accordingly identifying the most profitable ones. Further in this report, different financing options which can be used by the

project managers will be discussed and variance between the actual and estimated costs will be identified along with the reasons for

such variance. Lastly, this report will also evaluate the different methods of estimating project costs.

MAIN BODY

SECTION A

Question 1 Feasibility of the expansion options

A manufacturing company is looking for expansion and has identified three main options for the desired expansion. In the

following calculation all the three options have been evaluated to identify the best one and then select accordingly:-

Table 1Time and non-time based analysis

Particulars Data

Cost of capital 12%

Expected rate of return 11%

RFR 5%

Beta 0.50

Debt equity 1:03

Taxation 28%

Asset sale value 10% of cost of purchase

Tax deduction wear and tear 33%

Project A B C

Project Financial Management can be basically defined as a process through which planned and budgeted data and

accounting done with relation to a specific project is brought together with the actual one and the performance is then evaluated

(Livdan and Nezlobin, 2017). In the current report, it has been identified how a company can evaluate its growth options and then take

decisions accordingly identifying the most profitable ones. Further in this report, different financing options which can be used by the

project managers will be discussed and variance between the actual and estimated costs will be identified along with the reasons for

such variance. Lastly, this report will also evaluate the different methods of estimating project costs.

MAIN BODY

SECTION A

Question 1 Feasibility of the expansion options

A manufacturing company is looking for expansion and has identified three main options for the desired expansion. In the

following calculation all the three options have been evaluated to identify the best one and then select accordingly:-

Table 1Time and non-time based analysis

Particulars Data

Cost of capital 12%

Expected rate of return 11%

RFR 5%

Beta 0.50

Debt equity 1:03

Taxation 28%

Asset sale value 10% of cost of purchase

Tax deduction wear and tear 33%

Project A B C

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

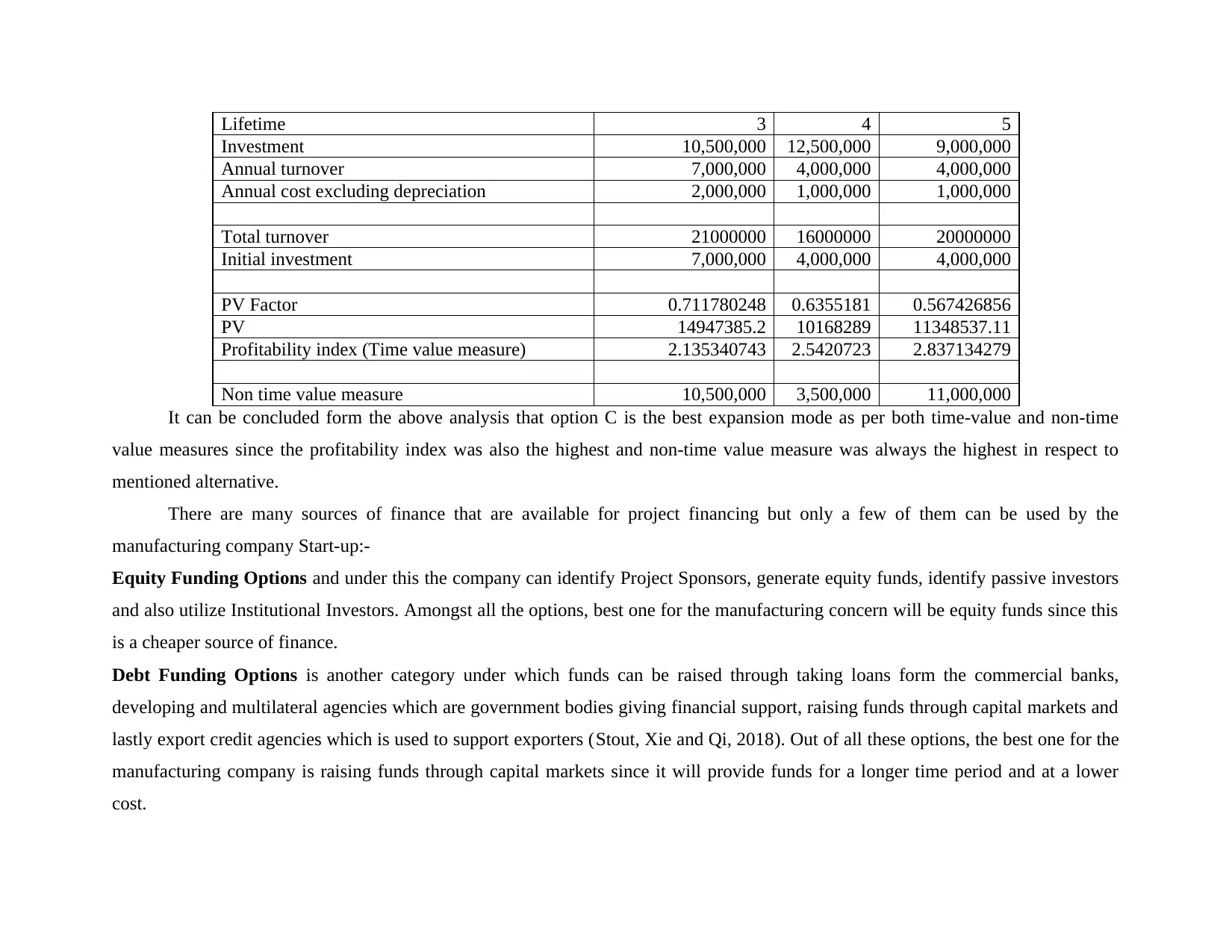

Lifetime 3 4 5

Investment 10,500,000 12,500,000 9,000,000

Annual turnover 7,000,000 4,000,000 4,000,000

Annual cost excluding depreciation 2,000,000 1,000,000 1,000,000

Total turnover 21000000 16000000 20000000

Initial investment 7,000,000 4,000,000 4,000,000

PV Factor 0.711780248 0.6355181 0.567426856

PV 14947385.2 10168289 11348537.11

Profitability index (Time value measure) 2.135340743 2.5420723 2.837134279

Non time value measure 10,500,000 3,500,000 11,000,000

It can be concluded form the above analysis that option C is the best expansion mode as per both time-value and non-time

value measures since the profitability index was also the highest and non-time value measure was always the highest in respect to

mentioned alternative.

There are many sources of finance that are available for project financing but only a few of them can be used by the

manufacturing company Start-up:-

Equity Funding Options and under this the company can identify Project Sponsors, generate equity funds, identify passive investors

and also utilize Institutional Investors. Amongst all the options, best one for the manufacturing concern will be equity funds since this

is a cheaper source of finance.

Debt Funding Options is another category under which funds can be raised through taking loans form the commercial banks,

developing and multilateral agencies which are government bodies giving financial support, raising funds through capital markets and

lastly export credit agencies which is used to support exporters (Stout, Xie and Qi, 2018). Out of all these options, the best one for the

manufacturing company is raising funds through capital markets since it will provide funds for a longer time period and at a lower

cost.

Investment 10,500,000 12,500,000 9,000,000

Annual turnover 7,000,000 4,000,000 4,000,000

Annual cost excluding depreciation 2,000,000 1,000,000 1,000,000

Total turnover 21000000 16000000 20000000

Initial investment 7,000,000 4,000,000 4,000,000

PV Factor 0.711780248 0.6355181 0.567426856

PV 14947385.2 10168289 11348537.11

Profitability index (Time value measure) 2.135340743 2.5420723 2.837134279

Non time value measure 10,500,000 3,500,000 11,000,000

It can be concluded form the above analysis that option C is the best expansion mode as per both time-value and non-time

value measures since the profitability index was also the highest and non-time value measure was always the highest in respect to

mentioned alternative.

There are many sources of finance that are available for project financing but only a few of them can be used by the

manufacturing company Start-up:-

Equity Funding Options and under this the company can identify Project Sponsors, generate equity funds, identify passive investors

and also utilize Institutional Investors. Amongst all the options, best one for the manufacturing concern will be equity funds since this

is a cheaper source of finance.

Debt Funding Options is another category under which funds can be raised through taking loans form the commercial banks,

developing and multilateral agencies which are government bodies giving financial support, raising funds through capital markets and

lastly export credit agencies which is used to support exporters (Stout, Xie and Qi, 2018). Out of all these options, the best one for the

manufacturing company is raising funds through capital markets since it will provide funds for a longer time period and at a lower

cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SECTION B

Question 2 Financing options available for project managers

There are a wide variety of financing options that are available to the project managers and can be categorized under equity as

well as debt. Some of these financing options have been described below:-

Fixed-Term Loans- This is a debt financing option available with the project managers under which they acquire loan amount

form the lender which is repaid by borrower i.e. project manager in instalments over a fixed time period (Beidleman, Fletcher

and Veshosky, 2019). This is the best option when manager is sure that instalments can be repaid in regular intervals.

Revolving Credit Facility- This is another short term debt financing option which allows the borrower to get access of the

funds anytime upto an established maximum limit. This ensures that the project managers have sufficient cash for operating

purpose and revolver is usually paid off quickly.

Lease Financing- Under Lease financing, the project managers are entitled to use the asset without actually owning them by

paying regular instalments to the owner of the asset termed as lease rentals. This helps in getting tax allowances and

deductions which is an added benefit for the project manager.

Debentures- These debt instruments are redeemed after reaching the maturity debt and the owners of these bonds can claim the

stated amount (Akintoye and et.al., 2018). Project managers can raise funds through this which can be later repaid on project

completion.

Share Capital- This is an equity financing option using which the project manager can raise equity capital i.e. sell shares to the

shareholders which represent their ownership share. In return of such shares, these shareholders get dividends regularly.

Question 3 Variance Analysis

Below is the evaluation of the actual and budgeted costs of Xyz company buy using standard costing and variance analysis

method in order to evaluate the differences and their reasons i.e. the cause of excess expenditure if any:-

Question 2 Financing options available for project managers

There are a wide variety of financing options that are available to the project managers and can be categorized under equity as

well as debt. Some of these financing options have been described below:-

Fixed-Term Loans- This is a debt financing option available with the project managers under which they acquire loan amount

form the lender which is repaid by borrower i.e. project manager in instalments over a fixed time period (Beidleman, Fletcher

and Veshosky, 2019). This is the best option when manager is sure that instalments can be repaid in regular intervals.

Revolving Credit Facility- This is another short term debt financing option which allows the borrower to get access of the

funds anytime upto an established maximum limit. This ensures that the project managers have sufficient cash for operating

purpose and revolver is usually paid off quickly.

Lease Financing- Under Lease financing, the project managers are entitled to use the asset without actually owning them by

paying regular instalments to the owner of the asset termed as lease rentals. This helps in getting tax allowances and

deductions which is an added benefit for the project manager.

Debentures- These debt instruments are redeemed after reaching the maturity debt and the owners of these bonds can claim the

stated amount (Akintoye and et.al., 2018). Project managers can raise funds through this which can be later repaid on project

completion.

Share Capital- This is an equity financing option using which the project manager can raise equity capital i.e. sell shares to the

shareholders which represent their ownership share. In return of such shares, these shareholders get dividends regularly.

Question 3 Variance Analysis

Below is the evaluation of the actual and budgeted costs of Xyz company buy using standard costing and variance analysis

method in order to evaluate the differences and their reasons i.e. the cause of excess expenditure if any:-

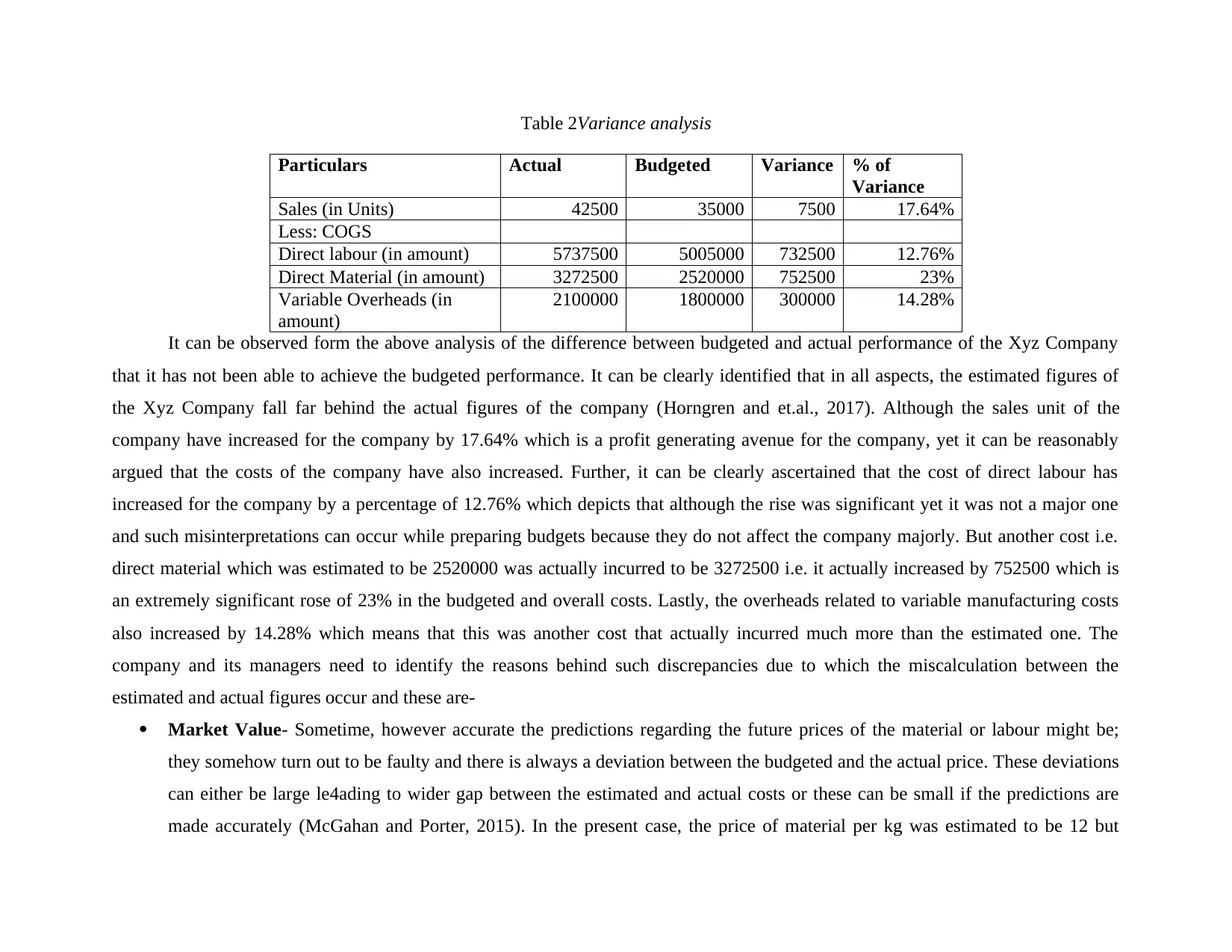

Table 2Variance analysis

Particulars Actual Budgeted Variance % of

Variance

Sales (in Units) 42500 35000 7500 17.64%

Less: COGS

Direct labour (in amount) 5737500 5005000 732500 12.76%

Direct Material (in amount) 3272500 2520000 752500 23%

Variable Overheads (in

amount)

2100000 1800000 300000 14.28%

It can be observed form the above analysis of the difference between budgeted and actual performance of the Xyz Company

that it has not been able to achieve the budgeted performance. It can be clearly identified that in all aspects, the estimated figures of

the Xyz Company fall far behind the actual figures of the company (Horngren and et.al., 2017). Although the sales unit of the

company have increased for the company by 17.64% which is a profit generating avenue for the company, yet it can be reasonably

argued that the costs of the company have also increased. Further, it can be clearly ascertained that the cost of direct labour has

increased for the company by a percentage of 12.76% which depicts that although the rise was significant yet it was not a major one

and such misinterpretations can occur while preparing budgets because they do not affect the company majorly. But another cost i.e.

direct material which was estimated to be 2520000 was actually incurred to be 3272500 i.e. it actually increased by 752500 which is

an extremely significant rose of 23% in the budgeted and overall costs. Lastly, the overheads related to variable manufacturing costs

also increased by 14.28% which means that this was another cost that actually incurred much more than the estimated one. The

company and its managers need to identify the reasons behind such discrepancies due to which the miscalculation between the

estimated and actual figures occur and these are-

Market Value- Sometime, however accurate the predictions regarding the future prices of the material or labour might be;

they somehow turn out to be faulty and there is always a deviation between the budgeted and the actual price. These deviations

can either be large le4ading to wider gap between the estimated and actual costs or these can be small if the predictions are

made accurately (McGahan and Porter, 2015). In the present case, the price of material per kg was estimated to be 12 but

Particulars Actual Budgeted Variance % of

Variance

Sales (in Units) 42500 35000 7500 17.64%

Less: COGS

Direct labour (in amount) 5737500 5005000 732500 12.76%

Direct Material (in amount) 3272500 2520000 752500 23%

Variable Overheads (in

amount)

2100000 1800000 300000 14.28%

It can be observed form the above analysis of the difference between budgeted and actual performance of the Xyz Company

that it has not been able to achieve the budgeted performance. It can be clearly identified that in all aspects, the estimated figures of

the Xyz Company fall far behind the actual figures of the company (Horngren and et.al., 2017). Although the sales unit of the

company have increased for the company by 17.64% which is a profit generating avenue for the company, yet it can be reasonably

argued that the costs of the company have also increased. Further, it can be clearly ascertained that the cost of direct labour has

increased for the company by a percentage of 12.76% which depicts that although the rise was significant yet it was not a major one

and such misinterpretations can occur while preparing budgets because they do not affect the company majorly. But another cost i.e.

direct material which was estimated to be 2520000 was actually incurred to be 3272500 i.e. it actually increased by 752500 which is

an extremely significant rose of 23% in the budgeted and overall costs. Lastly, the overheads related to variable manufacturing costs

also increased by 14.28% which means that this was another cost that actually incurred much more than the estimated one. The

company and its managers need to identify the reasons behind such discrepancies due to which the miscalculation between the

estimated and actual figures occur and these are-

Market Value- Sometime, however accurate the predictions regarding the future prices of the material or labour might be;

they somehow turn out to be faulty and there is always a deviation between the budgeted and the actual price. These deviations

can either be large le4ading to wider gap between the estimated and actual costs or these can be small if the predictions are

made accurately (McGahan and Porter, 2015). In the present case, the price of material per kg was estimated to be 12 but

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

actually the price that was incurred was lower i.e. 11. Still the overall cost has increased due to wrong estimation of the

quantity of material required which later increased by almost 100000 units.

Trends- This is the another factor which states that change in trends pertaining to the project can also be a reason not only

trends, but unforeseen circumstances like strike, implementation of ban on certain raw materials, unnecessary price hike etc.

are some of the aspects that can cause the cost of a project to increase unnecessarily.

Question 4 Approaches for project cost estimation

There are five major approaches of estimating project costs and these are detailed in following points:-

Analogous Cost Estimation- Under this, cost is estimated on the basis of a similar project carried out in past and this helps in

saving time of the project manager.

Parametric Cost Estimation- Under this different measurable aspects like size, weight, features etc. are used of past project to

estimate the cost incurred in the present project (Takano, Ishii and Muraki, 2017). This is different form analogous estimation

since here past project is not exactly similar, rather it is similar in design.

Rough Order-of Magnitude Estimation- This method of estimating cost is used when no detailed information regarding the

project is available and cost is assigned using apportionment method for different project stages which are based on the

estimated project cost.

Subject Matter Experts- Experts are approached by project managers so that they can estimate the cost related to different

aspects of the p0roject based on their expert knowledge and experience.

Three point Estimation- Three point or Pert technique normally uses a range of estimated costs rather that a single estimate

and uncertainty aspect is also included such estimation of costs ( Harrison and Lock, 2017).

CONCLUSION

It can be concluded from the research conducted in this report that Project Financial Management is an extremely important in

estimating the costs related to the project and its implementation in various phases. Section A in this report analysed the various

quantity of material required which later increased by almost 100000 units.

Trends- This is the another factor which states that change in trends pertaining to the project can also be a reason not only

trends, but unforeseen circumstances like strike, implementation of ban on certain raw materials, unnecessary price hike etc.

are some of the aspects that can cause the cost of a project to increase unnecessarily.

Question 4 Approaches for project cost estimation

There are five major approaches of estimating project costs and these are detailed in following points:-

Analogous Cost Estimation- Under this, cost is estimated on the basis of a similar project carried out in past and this helps in

saving time of the project manager.

Parametric Cost Estimation- Under this different measurable aspects like size, weight, features etc. are used of past project to

estimate the cost incurred in the present project (Takano, Ishii and Muraki, 2017). This is different form analogous estimation

since here past project is not exactly similar, rather it is similar in design.

Rough Order-of Magnitude Estimation- This method of estimating cost is used when no detailed information regarding the

project is available and cost is assigned using apportionment method for different project stages which are based on the

estimated project cost.

Subject Matter Experts- Experts are approached by project managers so that they can estimate the cost related to different

aspects of the p0roject based on their expert knowledge and experience.

Three point Estimation- Three point or Pert technique normally uses a range of estimated costs rather that a single estimate

and uncertainty aspect is also included such estimation of costs ( Harrison and Lock, 2017).

CONCLUSION

It can be concluded from the research conducted in this report that Project Financial Management is an extremely important in

estimating the costs related to the project and its implementation in various phases. Section A in this report analysed the various

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expansion options that were available with the company and it was concluded that option C was the best one due to maximum return.

In Section B of this report various methods of project cost estimations were discussed and it different sources of raising funds were

identified and analysed. Lastly, in this report, differences i.e. variance between actual and budgeted costs were identified and reasons

were ascertained for such deviations.

In Section B of this report various methods of project cost estimations were discussed and it different sources of raising funds were

identified and analysed. Lastly, in this report, differences i.e. variance between actual and budgeted costs were identified and reasons

were ascertained for such deviations.

REFERENCES

Books and journals

Akintoye, A. and et.al., 2018, September. The financial structure of private finance initiative

projects. In Proceedings of the 17th ARCOM Annual Conference, Salford University,

Manchester (Vol. 1, pp. 361-369).

Beidleman, C.R., Fletcher, D. and Veshosky, D., 2019. On allocating risk: the essence of project

finance. MIT Sloan Management Review 31(3) p.47.

Harrison, F. and Lock, D., 2017. Advanced project management: a structured approach.

Routledge.

Horngren, C.T. and et.al., 2017. Management and cost accounting. Harlow: Financial

Times/Prentice Hall.

Livdan, D. and Nezlobin, A., 2017. Accounting rules, equity valuation, and growth

options. Review of Accounting Studies 22(3) pp.1122-1155.

McGahan, A.M. and Porter, M.E., 2015. What do we know about variance in accounting

profitability?. Management Science 48(7) pp.834-851.

Stout, D.E., Xie, Y.A. and Qi, H., 2018. Improving capital budgeting decisions with real

options. Management accounting quarterly 9(4) p.1.

Takano, Y., Ishii, N. and Muraki, M., 2017. Multi-period resource allocation for estimating

project costs in competitive bidding. Central European Journal of Operations

Research 25(2) pp.303-323.

Online

[Online]. Available through: <>

1

Books and journals

Akintoye, A. and et.al., 2018, September. The financial structure of private finance initiative

projects. In Proceedings of the 17th ARCOM Annual Conference, Salford University,

Manchester (Vol. 1, pp. 361-369).

Beidleman, C.R., Fletcher, D. and Veshosky, D., 2019. On allocating risk: the essence of project

finance. MIT Sloan Management Review 31(3) p.47.

Harrison, F. and Lock, D., 2017. Advanced project management: a structured approach.

Routledge.

Horngren, C.T. and et.al., 2017. Management and cost accounting. Harlow: Financial

Times/Prentice Hall.

Livdan, D. and Nezlobin, A., 2017. Accounting rules, equity valuation, and growth

options. Review of Accounting Studies 22(3) pp.1122-1155.

McGahan, A.M. and Porter, M.E., 2015. What do we know about variance in accounting

profitability?. Management Science 48(7) pp.834-851.

Stout, D.E., Xie, Y.A. and Qi, H., 2018. Improving capital budgeting decisions with real

options. Management accounting quarterly 9(4) p.1.

Takano, Y., Ishii, N. and Muraki, M., 2017. Multi-period resource allocation for estimating

project costs in competitive bidding. Central European Journal of Operations

Research 25(2) pp.303-323.

Online

[Online]. Available through: <>

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.