Cash Flow Budget Analysis for Eyemen Ltd: Challenges and Solutions

VerifiedAdded on 2023/01/12

|7

|2078

|59

Project

AI Summary

This project presents a detailed analysis of a cash flow budget for Eyemen Ltd, covering the months of October, November, and December 2018. The analysis includes the creation of a cash budget, outlining cash inflows and outflows, and identifying potential financial challenges. The student examines the company's cash flow patterns, highlighting issues such as negative cash balances and the impact of interest and tax payments. The project provides recommendations for improving cash flow management, including adjusting collection policies, reducing variable costs, and optimizing payment schedules. The report emphasizes the importance of cash flow budgeting for business success and offers practical strategies for financial stability. The report also references several academic journals and books to support its analysis.

PROJECT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

a) Cash budget of the company for the month of October, November and December 2018.......1

b) Analysing the cash flow budget and identifying the issues faced regarding the budget and

making recommendations for overcoming the issues..................................................................2

CONCLUSION ...............................................................................................................................4

REFERENCES................................................................................................................................5

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

a) Cash budget of the company for the month of October, November and December 2018.......1

b) Analysing the cash flow budget and identifying the issues faced regarding the budget and

making recommendations for overcoming the issues..................................................................2

CONCLUSION ...............................................................................................................................4

REFERENCES................................................................................................................................5

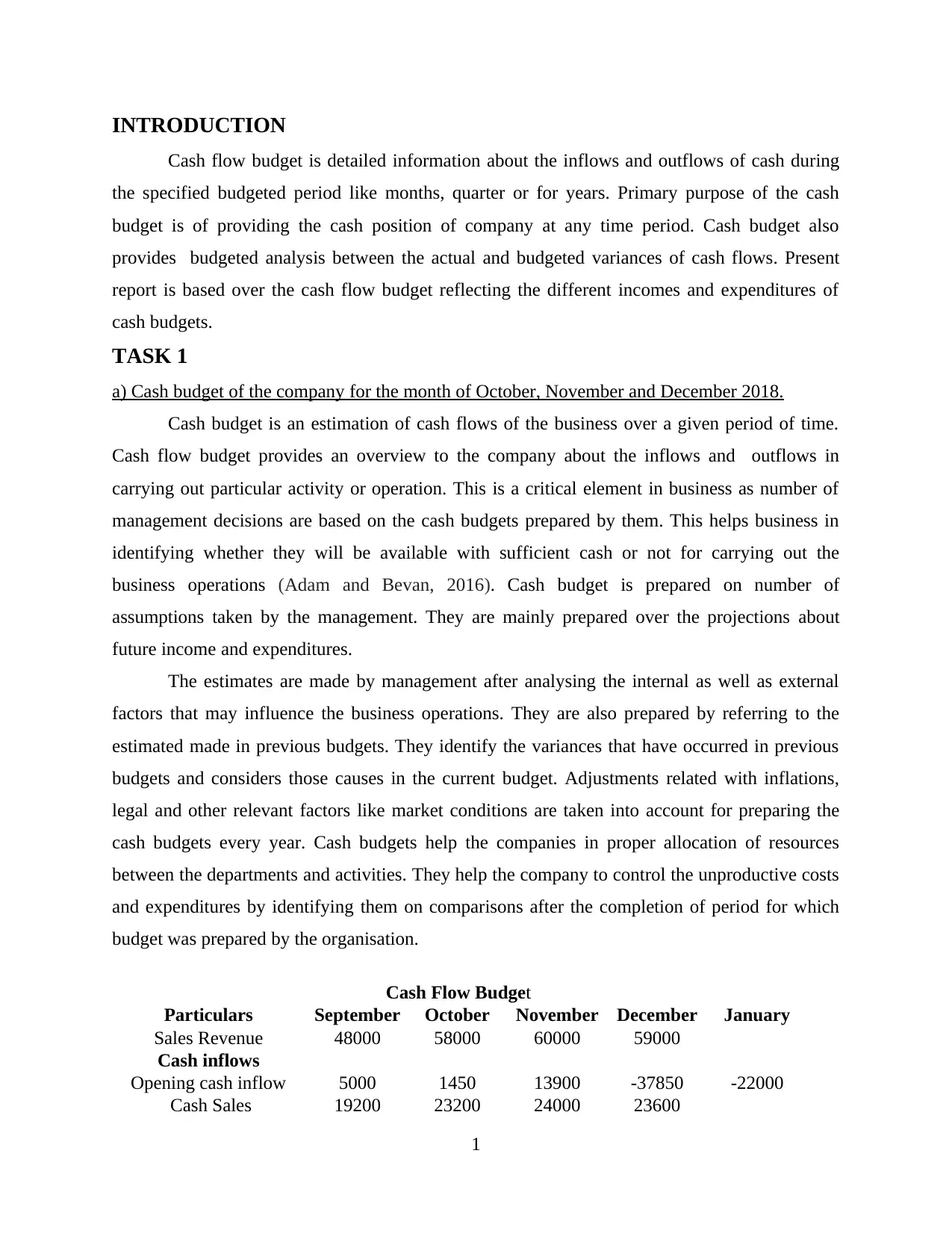

INTRODUCTION

Cash flow budget is detailed information about the inflows and outflows of cash during

the specified budgeted period like months, quarter or for years. Primary purpose of the cash

budget is of providing the cash position of company at any time period. Cash budget also

provides budgeted analysis between the actual and budgeted variances of cash flows. Present

report is based over the cash flow budget reflecting the different incomes and expenditures of

cash budgets.

TASK 1

a) Cash budget of the company for the month of October, November and December 2018.

Cash budget is an estimation of cash flows of the business over a given period of time.

Cash flow budget provides an overview to the company about the inflows and outflows in

carrying out particular activity or operation. This is a critical element in business as number of

management decisions are based on the cash budgets prepared by them. This helps business in

identifying whether they will be available with sufficient cash or not for carrying out the

business operations (Adam and Bevan, 2016). Cash budget is prepared on number of

assumptions taken by the management. They are mainly prepared over the projections about

future income and expenditures.

The estimates are made by management after analysing the internal as well as external

factors that may influence the business operations. They are also prepared by referring to the

estimated made in previous budgets. They identify the variances that have occurred in previous

budgets and considers those causes in the current budget. Adjustments related with inflations,

legal and other relevant factors like market conditions are taken into account for preparing the

cash budgets every year. Cash budgets help the companies in proper allocation of resources

between the departments and activities. They help the company to control the unproductive costs

and expenditures by identifying them on comparisons after the completion of period for which

budget was prepared by the organisation.

Cash Flow Budget

Particulars September October November December January

Sales Revenue 48000 58000 60000 59000

Cash inflows

Opening cash inflow 5000 1450 13900 -37850 -22000

Cash Sales 19200 23200 24000 23600

1

Cash flow budget is detailed information about the inflows and outflows of cash during

the specified budgeted period like months, quarter or for years. Primary purpose of the cash

budget is of providing the cash position of company at any time period. Cash budget also

provides budgeted analysis between the actual and budgeted variances of cash flows. Present

report is based over the cash flow budget reflecting the different incomes and expenditures of

cash budgets.

TASK 1

a) Cash budget of the company for the month of October, November and December 2018.

Cash budget is an estimation of cash flows of the business over a given period of time.

Cash flow budget provides an overview to the company about the inflows and outflows in

carrying out particular activity or operation. This is a critical element in business as number of

management decisions are based on the cash budgets prepared by them. This helps business in

identifying whether they will be available with sufficient cash or not for carrying out the

business operations (Adam and Bevan, 2016). Cash budget is prepared on number of

assumptions taken by the management. They are mainly prepared over the projections about

future income and expenditures.

The estimates are made by management after analysing the internal as well as external

factors that may influence the business operations. They are also prepared by referring to the

estimated made in previous budgets. They identify the variances that have occurred in previous

budgets and considers those causes in the current budget. Adjustments related with inflations,

legal and other relevant factors like market conditions are taken into account for preparing the

cash budgets every year. Cash budgets help the companies in proper allocation of resources

between the departments and activities. They help the company to control the unproductive costs

and expenditures by identifying them on comparisons after the completion of period for which

budget was prepared by the organisation.

Cash Flow Budget

Particulars September October November December January

Sales Revenue 48000 58000 60000 59000

Cash inflows

Opening cash inflow 5000 1450 13900 -37850 -22000

Cash Sales 19200 23200 24000 23600

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

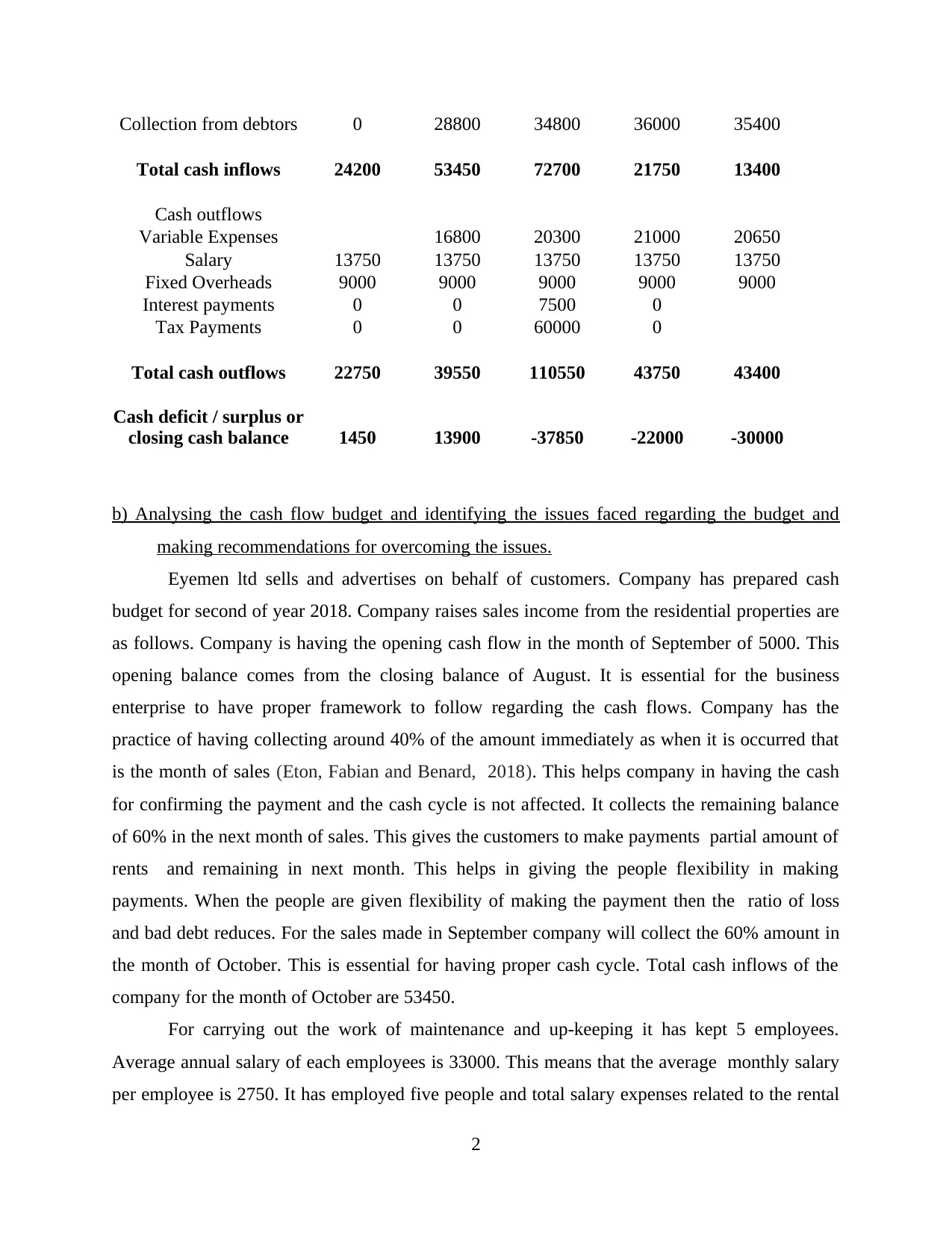

Collection from debtors 0 28800 34800 36000 35400

Total cash inflows 24200 53450 72700 21750 13400

Cash outflows

Variable Expenses 16800 20300 21000 20650

Salary 13750 13750 13750 13750 13750

Fixed Overheads 9000 9000 9000 9000 9000

Interest payments 0 0 7500 0

Tax Payments 0 0 60000 0

Total cash outflows 22750 39550 110550 43750 43400

Cash deficit / surplus or

closing cash balance 1450 13900 -37850 -22000 -30000

b) Analysing the cash flow budget and identifying the issues faced regarding the budget and

making recommendations for overcoming the issues.

Eyemen ltd sells and advertises on behalf of customers. Company has prepared cash

budget for second of year 2018. Company raises sales income from the residential properties are

as follows. Company is having the opening cash flow in the month of September of 5000. This

opening balance comes from the closing balance of August. It is essential for the business

enterprise to have proper framework to follow regarding the cash flows. Company has the

practice of having collecting around 40% of the amount immediately as when it is occurred that

is the month of sales (Eton, Fabian and Benard, 2018). This helps company in having the cash

for confirming the payment and the cash cycle is not affected. It collects the remaining balance

of 60% in the next month of sales. This gives the customers to make payments partial amount of

rents and remaining in next month. This helps in giving the people flexibility in making

payments. When the people are given flexibility of making the payment then the ratio of loss

and bad debt reduces. For the sales made in September company will collect the 60% amount in

the month of October. This is essential for having proper cash cycle. Total cash inflows of the

company for the month of October are 53450.

For carrying out the work of maintenance and up-keeping it has kept 5 employees.

Average annual salary of each employees is 33000. This means that the average monthly salary

per employee is 2750. It has employed five people and total salary expenses related to the rental

2

Total cash inflows 24200 53450 72700 21750 13400

Cash outflows

Variable Expenses 16800 20300 21000 20650

Salary 13750 13750 13750 13750 13750

Fixed Overheads 9000 9000 9000 9000 9000

Interest payments 0 0 7500 0

Tax Payments 0 0 60000 0

Total cash outflows 22750 39550 110550 43750 43400

Cash deficit / surplus or

closing cash balance 1450 13900 -37850 -22000 -30000

b) Analysing the cash flow budget and identifying the issues faced regarding the budget and

making recommendations for overcoming the issues.

Eyemen ltd sells and advertises on behalf of customers. Company has prepared cash

budget for second of year 2018. Company raises sales income from the residential properties are

as follows. Company is having the opening cash flow in the month of September of 5000. This

opening balance comes from the closing balance of August. It is essential for the business

enterprise to have proper framework to follow regarding the cash flows. Company has the

practice of having collecting around 40% of the amount immediately as when it is occurred that

is the month of sales (Eton, Fabian and Benard, 2018). This helps company in having the cash

for confirming the payment and the cash cycle is not affected. It collects the remaining balance

of 60% in the next month of sales. This gives the customers to make payments partial amount of

rents and remaining in next month. This helps in giving the people flexibility in making

payments. When the people are given flexibility of making the payment then the ratio of loss

and bad debt reduces. For the sales made in September company will collect the 60% amount in

the month of October. This is essential for having proper cash cycle. Total cash inflows of the

company for the month of October are 53450.

For carrying out the work of maintenance and up-keeping it has kept 5 employees.

Average annual salary of each employees is 33000. This means that the average monthly salary

per employee is 2750. It has employed five people and total salary expenses related to the rental

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

properties is 13750. Salary payments are to be paid by them every year. It cannot reduce the

salaries of employees and cannot make payments other than monthly (Benzell, Kotlikoff and

LaGarda, 2017). The average monthly salary is required to be paid by company every month.

Variable expenses associated with the rental properties are carried out every month.

Variable expenses are 35% of the total sales during month. Like for the month of October it had

the sales revenue of 48000 and as against it incurs 35% of the variable expenses that are 16800.

It is paying the variable expenses in the next month in which they are incurred. Variable expense

of September are paid in the month of October. Variable expenses will change with the change in

number of rental properties (Isle, Freudenberg and Sarker, 2018). It could have control over its

variable costs using the appropriate strategies and eliminating the unproductive costs consuming

money.

It incurs fixed costs of 9000 per month. Payment are made in the month in which they

arise that means expense of October month will be paid in the same month. They are not paid in

the following month. Fixed costs are required to be paid every year by company. These are

related to the power, heat, municipal taxes and other charges that are required to be paid every

month as it attracts penalties on late payments. Variable and fixed expenses are associated with

every business that company carries out. Fixed expenses are incurred in every circumstances and

required to be paid when the cash flows are zero. Fixed costs cannot be avoided by company and

are required to be considered in cash budgets.

It has taken loan of 500000 for renovation of the rental properties. Loan is taken on

interest rate of 6% and interest is to be paid quarterly by the company. Firs payment was made

by company in August and next payment after three months will be made in November. Yearly

interest expense is 30000 and monthly expense is 2500. Therefore, it is required to make

payments amounting to 7500 for three months (Das and Parida, 2016). It should make the

interest payment monthly rather than quarterly as it make difficult for company to have

aggregate payments this affects the cash cycle and takes considerable part of money in single

month.

It is also required to make payments of tax liability. It is a statutory obligation that cannot

be avoided by company. Tax payments are required to be made by the company at the time of

submission of tax returns. They cannot be avoided or allocated in more months. The aggregate

payment of 60000 in November has made the cash flows negative. This has affected the cash

3

salaries of employees and cannot make payments other than monthly (Benzell, Kotlikoff and

LaGarda, 2017). The average monthly salary is required to be paid by company every month.

Variable expenses associated with the rental properties are carried out every month.

Variable expenses are 35% of the total sales during month. Like for the month of October it had

the sales revenue of 48000 and as against it incurs 35% of the variable expenses that are 16800.

It is paying the variable expenses in the next month in which they are incurred. Variable expense

of September are paid in the month of October. Variable expenses will change with the change in

number of rental properties (Isle, Freudenberg and Sarker, 2018). It could have control over its

variable costs using the appropriate strategies and eliminating the unproductive costs consuming

money.

It incurs fixed costs of 9000 per month. Payment are made in the month in which they

arise that means expense of October month will be paid in the same month. They are not paid in

the following month. Fixed costs are required to be paid every year by company. These are

related to the power, heat, municipal taxes and other charges that are required to be paid every

month as it attracts penalties on late payments. Variable and fixed expenses are associated with

every business that company carries out. Fixed expenses are incurred in every circumstances and

required to be paid when the cash flows are zero. Fixed costs cannot be avoided by company and

are required to be considered in cash budgets.

It has taken loan of 500000 for renovation of the rental properties. Loan is taken on

interest rate of 6% and interest is to be paid quarterly by the company. Firs payment was made

by company in August and next payment after three months will be made in November. Yearly

interest expense is 30000 and monthly expense is 2500. Therefore, it is required to make

payments amounting to 7500 for three months (Das and Parida, 2016). It should make the

interest payment monthly rather than quarterly as it make difficult for company to have

aggregate payments this affects the cash cycle and takes considerable part of money in single

month.

It is also required to make payments of tax liability. It is a statutory obligation that cannot

be avoided by company. Tax payments are required to be made by the company at the time of

submission of tax returns. They cannot be avoided or allocated in more months. The aggregate

payment of 60000 in November has made the cash flows negative. This has affected the cash

3

budget of company. Once a company goes negative in cash balance it becomes hared for the

company to return back to positive balance as it is required to carry out monthly expenses and if

it is not able to make payments this will affect the business. In such situations when companies

go out of cash they for meeting the cash requirements borrows money from the market this

causes the company to incur extra costs of borrowings and interests. This affects the whole cash

cycle and organisational structure therefore it is required to make changes in the present structure

of its cash flows. Given the present revenues and expenditures it is having positive cash flows

only in month of October of 13900. From the month of November it has gone negative in cash

due to two big cash outflows in quarterly interest payment and second the tax payments. In

November it has negative in cash amounting to 37850 even after earning revenues of 72700.

Negative cash flow represents that company is not available with sufficient cash fr

carrying out its operations. In the month of December company had negative cash balance of

22000 that is lower than November as it has not made payment related to interest and tax in this

year. For becoming positive in cash it will be required to reduce the credit period given to

people. It will be required to change its collection policy for few months from November

(WESONGA, 2017). It should have 60% collection in current period and remaining in next

period. This is essential so that the tax burdens are reduced and it can have money to carry out

the business. Apart from this it may eliminate unwanted variable costs so that the costs could be

reduced.

CONCLUSION

The report concludes that cash flow budgets are very important for the organisation. This

helps the business to identify whether the company will be available with the sufficient cash or

not following the proposed structures. This helps the business enterprise to have proper

arrangements of cash in the business.

4

company to return back to positive balance as it is required to carry out monthly expenses and if

it is not able to make payments this will affect the business. In such situations when companies

go out of cash they for meeting the cash requirements borrows money from the market this

causes the company to incur extra costs of borrowings and interests. This affects the whole cash

cycle and organisational structure therefore it is required to make changes in the present structure

of its cash flows. Given the present revenues and expenditures it is having positive cash flows

only in month of October of 13900. From the month of November it has gone negative in cash

due to two big cash outflows in quarterly interest payment and second the tax payments. In

November it has negative in cash amounting to 37850 even after earning revenues of 72700.

Negative cash flow represents that company is not available with sufficient cash fr

carrying out its operations. In the month of December company had negative cash balance of

22000 that is lower than November as it has not made payment related to interest and tax in this

year. For becoming positive in cash it will be required to reduce the credit period given to

people. It will be required to change its collection policy for few months from November

(WESONGA, 2017). It should have 60% collection in current period and remaining in next

period. This is essential so that the tax burdens are reduced and it can have money to carry out

the business. Apart from this it may eliminate unwanted variable costs so that the costs could be

reduced.

CONCLUSION

The report concludes that cash flow budgets are very important for the organisation. This

helps the business to identify whether the company will be available with the sufficient cash or

not following the proposed structures. This helps the business enterprise to have proper

arrangements of cash in the business.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Adam, C.S. and Bevan, D.L., 2016. 8 The Cash-Budget as a Restraint: The

Experience. Investment and Risk in Africa. p.185.

Eton, M., Fabian, M. and Benard, P.O., 2018. Cash Budgeting and Organizational Performance

of Private Firms in Uganda: A Case of Kabale District, Western Uganda.

Benzell, S.G., Kotlikoff, L.J. and LaGarda, G., 2017. Simulating business cash flow taxation: An

illustration based on the “Better Way” corporate tax reform (No. w23675). National

Bureau of Economic Research.

Isle, M.B., Freudenberg, B. and Sarker, T., 2018. Is the Literacy of Small Business Owners

Important for Cash Flow Management: The Experts' Perspective. J. Australasian Tax

Tchrs. Ass'n. 13. p.31.

Das, C.P. and Parida, M., 2016. A Study on Cash Management and Determinants of Cash

Holding. Splint International Journal of Professionals. 3(3). p.102.

WESONGA, M., 2017. Influence of cash management practices on performance of Small scale

enterprises in Mbale town, Kenya (Doctoral dissertation, Maseno University).

Lu, L., and et.al., 2016. Work engagement, job satisfaction, and turnover

intentions. International Journal of Contemporary Hospitality Management.

Hoboubi, N., and et.al., 2017. The impact of job stress and job satisfaction on workforce

productivity in an Iranian petrochemical industry. Safety and health at work. 8(1). pp.67-

71.

Yousef, D.A., 2017. Organizational commitment, job satisfaction and attitudes toward

organizational change: A study in the local government. International Journal of Public

Administration. 40(1). pp.77-88.

Yalabik, Z.Y., Rayton, B.A. and Rapti, A., 2017, December. Facets of job satisfaction and work

engagement. In Evidence-based HRM: a global forum for empirical scholarship. Emerald

Publishing Limited.

(Lu and et.al., 2016)

(Hoboubi and et.al., 2017)

(Yousef, 2017)

(Yalabik, Rayton and Rapti, 2017)

5

Books and Journals

Adam, C.S. and Bevan, D.L., 2016. 8 The Cash-Budget as a Restraint: The

Experience. Investment and Risk in Africa. p.185.

Eton, M., Fabian, M. and Benard, P.O., 2018. Cash Budgeting and Organizational Performance

of Private Firms in Uganda: A Case of Kabale District, Western Uganda.

Benzell, S.G., Kotlikoff, L.J. and LaGarda, G., 2017. Simulating business cash flow taxation: An

illustration based on the “Better Way” corporate tax reform (No. w23675). National

Bureau of Economic Research.

Isle, M.B., Freudenberg, B. and Sarker, T., 2018. Is the Literacy of Small Business Owners

Important for Cash Flow Management: The Experts' Perspective. J. Australasian Tax

Tchrs. Ass'n. 13. p.31.

Das, C.P. and Parida, M., 2016. A Study on Cash Management and Determinants of Cash

Holding. Splint International Journal of Professionals. 3(3). p.102.

WESONGA, M., 2017. Influence of cash management practices on performance of Small scale

enterprises in Mbale town, Kenya (Doctoral dissertation, Maseno University).

Lu, L., and et.al., 2016. Work engagement, job satisfaction, and turnover

intentions. International Journal of Contemporary Hospitality Management.

Hoboubi, N., and et.al., 2017. The impact of job stress and job satisfaction on workforce

productivity in an Iranian petrochemical industry. Safety and health at work. 8(1). pp.67-

71.

Yousef, D.A., 2017. Organizational commitment, job satisfaction and attitudes toward

organizational change: A study in the local government. International Journal of Public

Administration. 40(1). pp.77-88.

Yalabik, Z.Y., Rayton, B.A. and Rapti, A., 2017, December. Facets of job satisfaction and work

engagement. In Evidence-based HRM: a global forum for empirical scholarship. Emerald

Publishing Limited.

(Lu and et.al., 2016)

(Hoboubi and et.al., 2017)

(Yousef, 2017)

(Yalabik, Rayton and Rapti, 2017)

5

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.