Project Methodologies

VerifiedAdded on 2023/01/19

|29

|3173

|50

AI Summary

This study focuses on project methodologies, specifically mean variance analysis and covariance matrix. It evaluates the stationary factor and provides regression statistics for ASTRAZENECA, BAE SYSTEMS, COCA COLA HOLDING AG, and BRITISH AMERICAN TOBAE SYSTEMSCO PLC. The study also discusses the concept of efficient frontier and its application in portfolio optimization.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

PROJECT METHODOLOGIES

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

(A) Evaluation of stationary factor..................................................................................................1

B.......................................................................................................................................................6

(1) Mean variance analysis..........................................................................................................6

(2) Covariance matrix.................................................................................................................7

3 Efficient frontier.......................................................................................................................7

........................................................................................................................................................10

(C) GARCH results........................................................................................................................11

........................................................................................................................................................13

(D) ARMA.....................................................................................................................................20

CONCLUSION..............................................................................................................................22

REFERENCE................................................................................................................................................24

Table 1ASTRAZENECA PACF.....................................................................................................1

Table 2BAE SYSTEMS PACF.......................................................................................................2

Table 3COCA COLA HOLDING AG PACF.................................................................................3

Table 4BRITISH AMERICAN TOBAE SYSTEMSCO PLC PACF.............................................4

Table 5Covariance matrix................................................................................................................7

Table 6Descriptive statistics............................................................................................................7

Table 7Covariance matrix................................................................................................................8

Table 8Target return and average return.........................................................................................9

Table 9Input for efficient frontier....................................................................................................9

Table 10Efficient frontier..............................................................................................................10

Table 15GARCH for ASTRAZENECA 10 months......................................................................11

Table 11ASTRAZENECA regression...........................................................................................11

Table 16Statistics for ASTRAZENECA 10 months.....................................................................12

Table 17GARCH for 2 months......................................................................................................13

Table 13ASTRAZENECA 2 months regression...........................................................................13

INTRODUCTION...........................................................................................................................1

(A) Evaluation of stationary factor..................................................................................................1

B.......................................................................................................................................................6

(1) Mean variance analysis..........................................................................................................6

(2) Covariance matrix.................................................................................................................7

3 Efficient frontier.......................................................................................................................7

........................................................................................................................................................10

(C) GARCH results........................................................................................................................11

........................................................................................................................................................13

(D) ARMA.....................................................................................................................................20

CONCLUSION..............................................................................................................................22

REFERENCE................................................................................................................................................24

Table 1ASTRAZENECA PACF.....................................................................................................1

Table 2BAE SYSTEMS PACF.......................................................................................................2

Table 3COCA COLA HOLDING AG PACF.................................................................................3

Table 4BRITISH AMERICAN TOBAE SYSTEMSCO PLC PACF.............................................4

Table 5Covariance matrix................................................................................................................7

Table 6Descriptive statistics............................................................................................................7

Table 7Covariance matrix................................................................................................................8

Table 8Target return and average return.........................................................................................9

Table 9Input for efficient frontier....................................................................................................9

Table 10Efficient frontier..............................................................................................................10

Table 15GARCH for ASTRAZENECA 10 months......................................................................11

Table 11ASTRAZENECA regression...........................................................................................11

Table 16Statistics for ASTRAZENECA 10 months.....................................................................12

Table 17GARCH for 2 months......................................................................................................13

Table 13ASTRAZENECA 2 months regression...........................................................................13

Table 18ASTRAZENECA for two months...................................................................................15

Table 19BAE SYSTEMS 10 months............................................................................................16

Table 12BAE SYSTEMSL Regression.........................................................................................16

Table 20Statistics for BAE SYSTEMS 10 months.......................................................................17

Table 21BAE SYSTEMS 2 months..............................................................................................18

Table 14BAE SYSTEMS 2 months regression.............................................................................18

Table 22Statistics for BAE SYSTEMS 2 months.........................................................................20

Table 23ASTRAZENECA regression...........................................................................................20

Table 24BAE SYSTEMS Regression...........................................................................................21

Table 19BAE SYSTEMS 10 months............................................................................................16

Table 12BAE SYSTEMSL Regression.........................................................................................16

Table 20Statistics for BAE SYSTEMS 10 months.......................................................................17

Table 21BAE SYSTEMS 2 months..............................................................................................18

Table 14BAE SYSTEMS 2 months regression.............................................................................18

Table 22Statistics for BAE SYSTEMS 2 months.........................................................................20

Table 23ASTRAZENECA regression...........................................................................................20

Table 24BAE SYSTEMS Regression...........................................................................................21

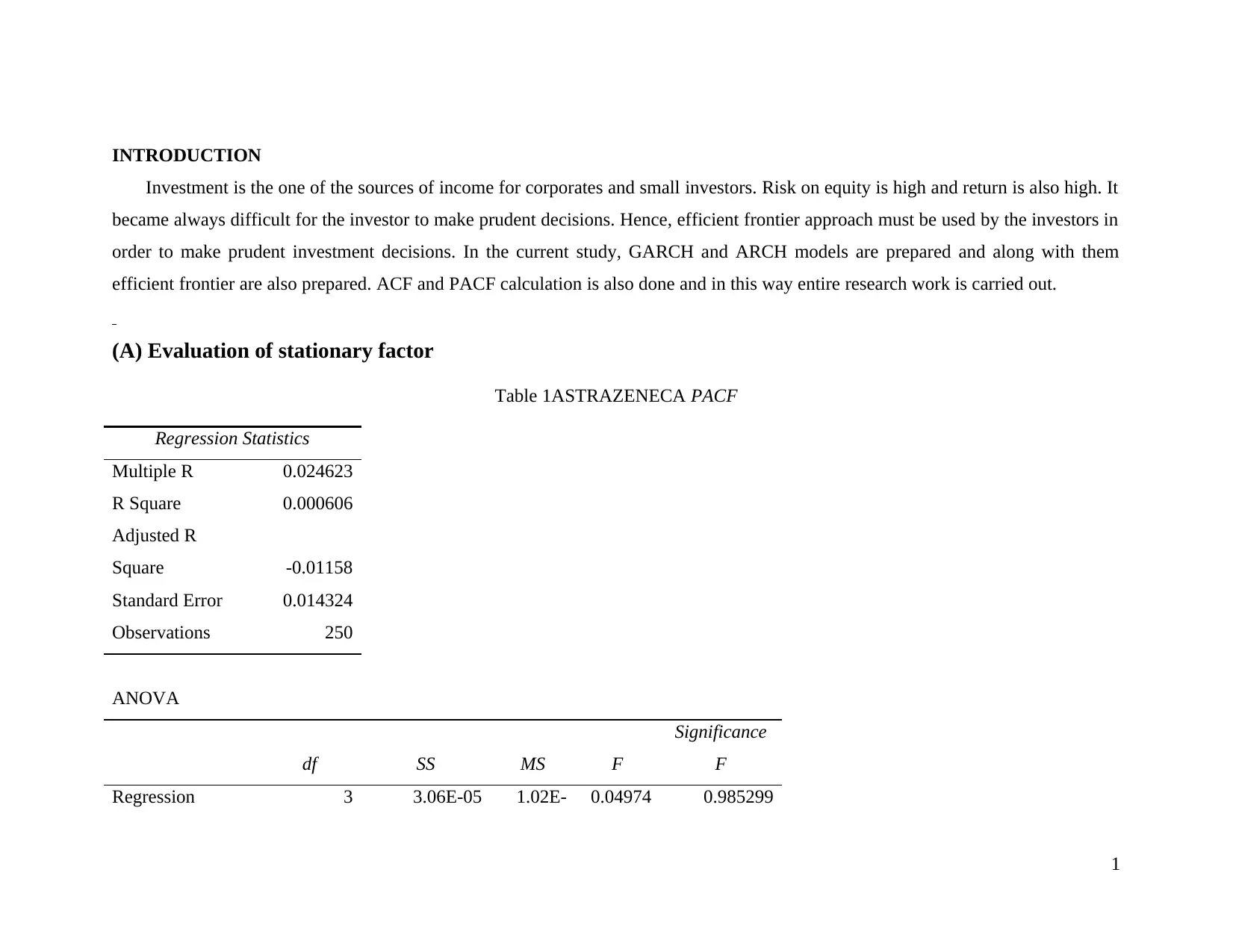

INTRODUCTION

Investment is the one of the sources of income for corporates and small investors. Risk on equity is high and return is also high. It

became always difficult for the investor to make prudent decisions. Hence, efficient frontier approach must be used by the investors in

order to make prudent investment decisions. In the current study, GARCH and ARCH models are prepared and along with them

efficient frontier are also prepared. ACF and PACF calculation is also done and in this way entire research work is carried out.

(A) Evaluation of stationary factor

Table 1ASTRAZENECA PACF

Regression Statistics

Multiple R 0.024623

R Square 0.000606

Adjusted R

Square -0.01158

Standard Error 0.014324

Observations 250

ANOVA

df SS MS F

Significance

F

Regression 3 3.06E-05 1.02E- 0.04974 0.985299

1

Investment is the one of the sources of income for corporates and small investors. Risk on equity is high and return is also high. It

became always difficult for the investor to make prudent decisions. Hence, efficient frontier approach must be used by the investors in

order to make prudent investment decisions. In the current study, GARCH and ARCH models are prepared and along with them

efficient frontier are also prepared. ACF and PACF calculation is also done and in this way entire research work is carried out.

(A) Evaluation of stationary factor

Table 1ASTRAZENECA PACF

Regression Statistics

Multiple R 0.024623

R Square 0.000606

Adjusted R

Square -0.01158

Standard Error 0.014324

Observations 250

ANOVA

df SS MS F

Significance

F

Regression 3 3.06E-05 1.02E- 0.04974 0.985299

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

05 4

Residual 246 0.050471

0.00020

5

Total 249 0.050502

Coefficient

s

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0.000596 0.000909

0.65583

8

0.51254

1 -0.00119 0.002386 -0.00119 0.002386

Lag 2 0.023965 0.063764 0.37583

0.70736

7 -0.10163 0.149559 -0.10163 0.149559

Lag 3 -0.00472 0.063757 -0.0741

0.94099

3 -0.1303 0.120855 -0.1303 0.120855

Lag 4 -0.0036 0.062989 -0.05708

0.95453

1 -0.12766 0.120471 -0.12766 0.120471

Table 2BAE SYSTEMS PACF

Regression Statistics

Multiple R 0.115003739

R Square 0.01322586

Adjusted R

Square 0.001192029

2

Residual 246 0.050471

0.00020

5

Total 249 0.050502

Coefficient

s

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0.000596 0.000909

0.65583

8

0.51254

1 -0.00119 0.002386 -0.00119 0.002386

Lag 2 0.023965 0.063764 0.37583

0.70736

7 -0.10163 0.149559 -0.10163 0.149559

Lag 3 -0.00472 0.063757 -0.0741

0.94099

3 -0.1303 0.120855 -0.1303 0.120855

Lag 4 -0.0036 0.062989 -0.05708

0.95453

1 -0.12766 0.120471 -0.12766 0.120471

Table 2BAE SYSTEMS PACF

Regression Statistics

Multiple R 0.115003739

R Square 0.01322586

Adjusted R

Square 0.001192029

2

Standard Error 0.014060995

Observations 250

ANOVA

df SS MS F

Significance

F

Regression 3 0.000652 0.000217 1.099056 0.350169

Residual 246 0.048637 0.000198

Total 249 0.049289

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0.000380909 0.00089 0.427991 0.669032 -0.00137 0.002134 -0.00137 0.002134

Lag 2 0.113199299 0.063782 1.774779 0.077171 -0.01243 0.238828 -0.01243 0.238828

Lag 3 0.007945121 0.064332 0.123502 0.901811 -0.11877 0.134657 -0.11877 0.134657

Lag 4

-

0.017024478 0.064132 -0.26546 0.790876 -0.14334 0.109293 -0.14334 0.109293

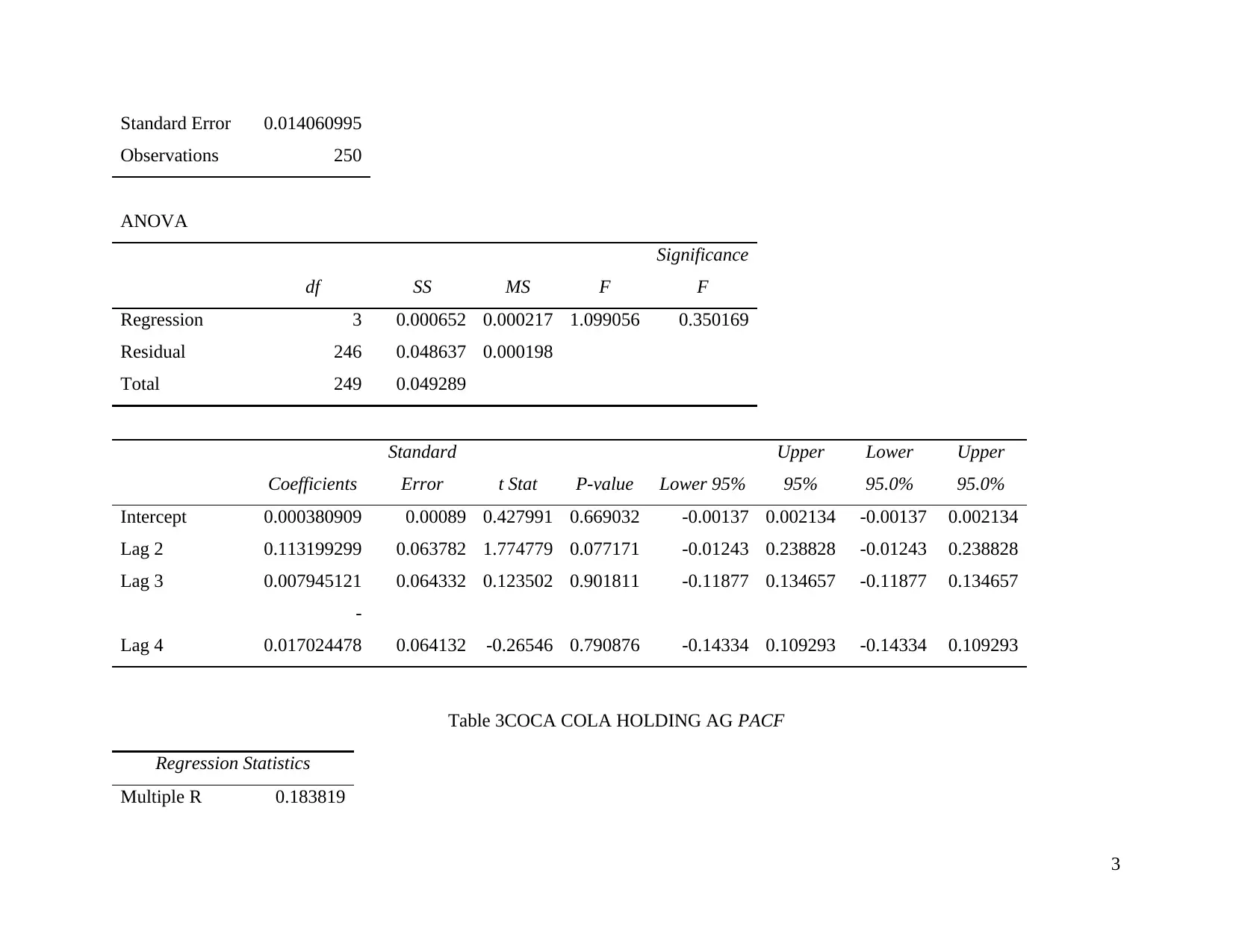

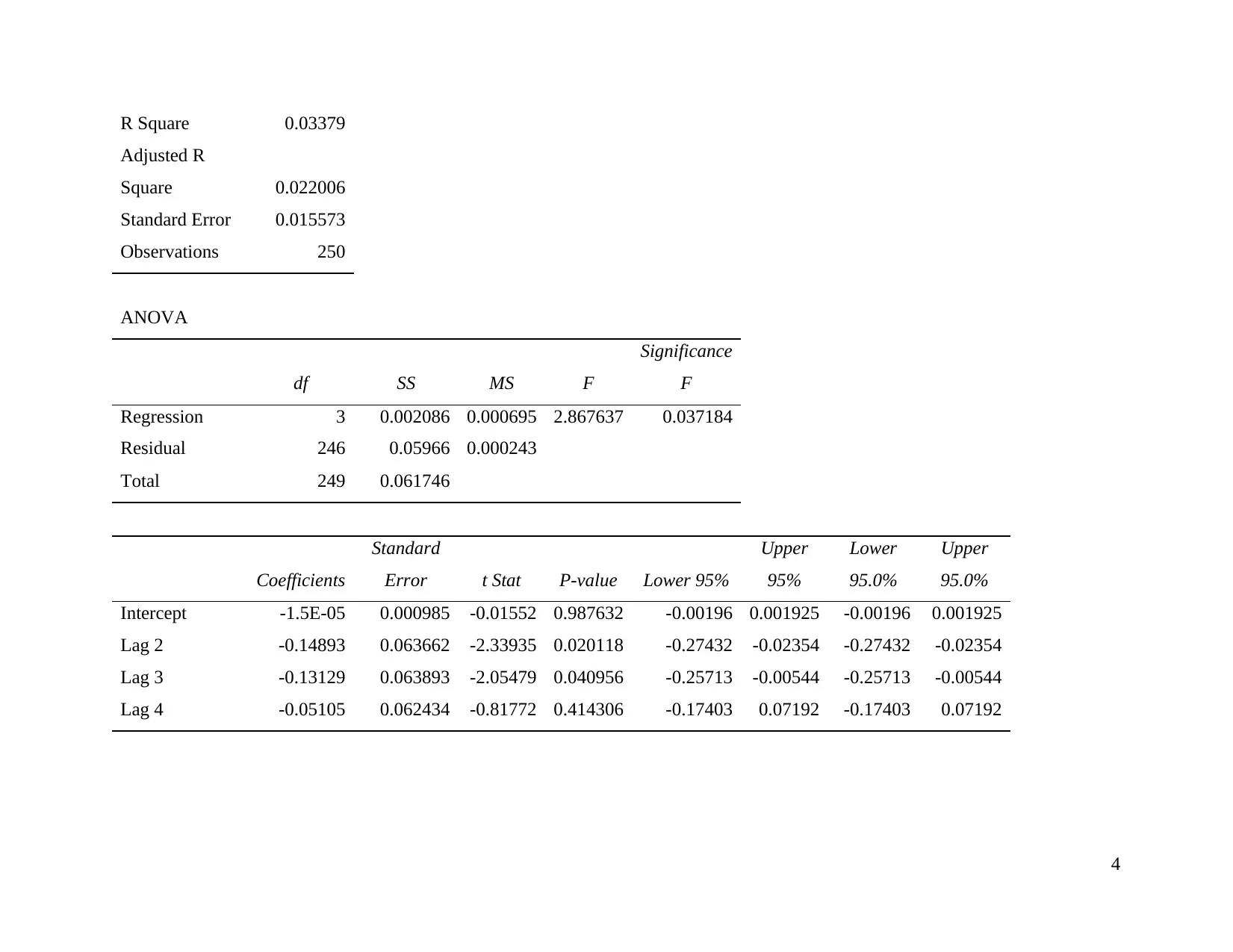

Table 3COCA COLA HOLDING AG PACF

Regression Statistics

Multiple R 0.183819

3

Observations 250

ANOVA

df SS MS F

Significance

F

Regression 3 0.000652 0.000217 1.099056 0.350169

Residual 246 0.048637 0.000198

Total 249 0.049289

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0.000380909 0.00089 0.427991 0.669032 -0.00137 0.002134 -0.00137 0.002134

Lag 2 0.113199299 0.063782 1.774779 0.077171 -0.01243 0.238828 -0.01243 0.238828

Lag 3 0.007945121 0.064332 0.123502 0.901811 -0.11877 0.134657 -0.11877 0.134657

Lag 4

-

0.017024478 0.064132 -0.26546 0.790876 -0.14334 0.109293 -0.14334 0.109293

Table 3COCA COLA HOLDING AG PACF

Regression Statistics

Multiple R 0.183819

3

R Square 0.03379

Adjusted R

Square 0.022006

Standard Error 0.015573

Observations 250

ANOVA

df SS MS F

Significance

F

Regression 3 0.002086 0.000695 2.867637 0.037184

Residual 246 0.05966 0.000243

Total 249 0.061746

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -1.5E-05 0.000985 -0.01552 0.987632 -0.00196 0.001925 -0.00196 0.001925

Lag 2 -0.14893 0.063662 -2.33935 0.020118 -0.27432 -0.02354 -0.27432 -0.02354

Lag 3 -0.13129 0.063893 -2.05479 0.040956 -0.25713 -0.00544 -0.25713 -0.00544

Lag 4 -0.05105 0.062434 -0.81772 0.414306 -0.17403 0.07192 -0.17403 0.07192

4

Adjusted R

Square 0.022006

Standard Error 0.015573

Observations 250

ANOVA

df SS MS F

Significance

F

Regression 3 0.002086 0.000695 2.867637 0.037184

Residual 246 0.05966 0.000243

Total 249 0.061746

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -1.5E-05 0.000985 -0.01552 0.987632 -0.00196 0.001925 -0.00196 0.001925

Lag 2 -0.14893 0.063662 -2.33935 0.020118 -0.27432 -0.02354 -0.27432 -0.02354

Lag 3 -0.13129 0.063893 -2.05479 0.040956 -0.25713 -0.00544 -0.25713 -0.00544

Lag 4 -0.05105 0.062434 -0.81772 0.414306 -0.17403 0.07192 -0.17403 0.07192

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

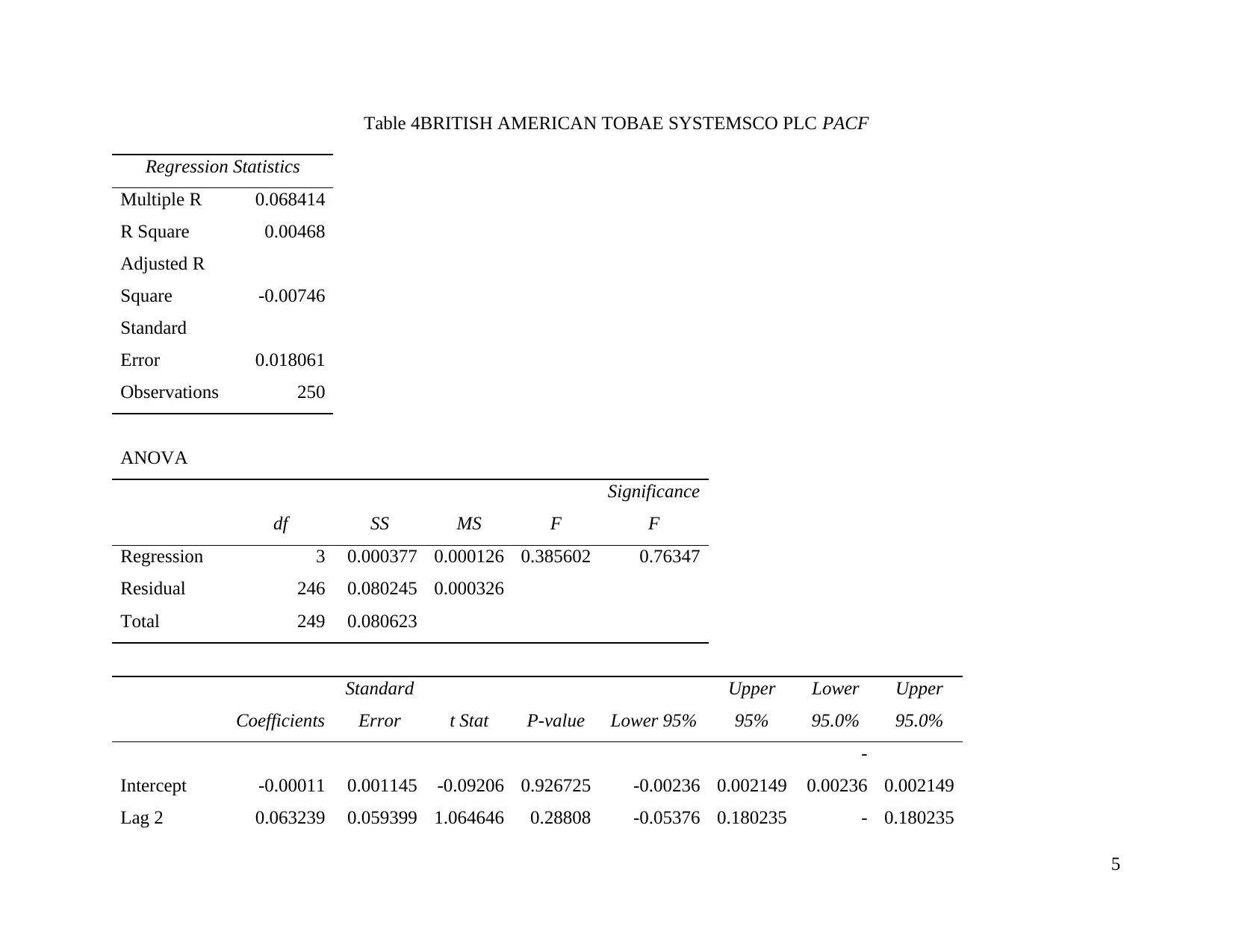

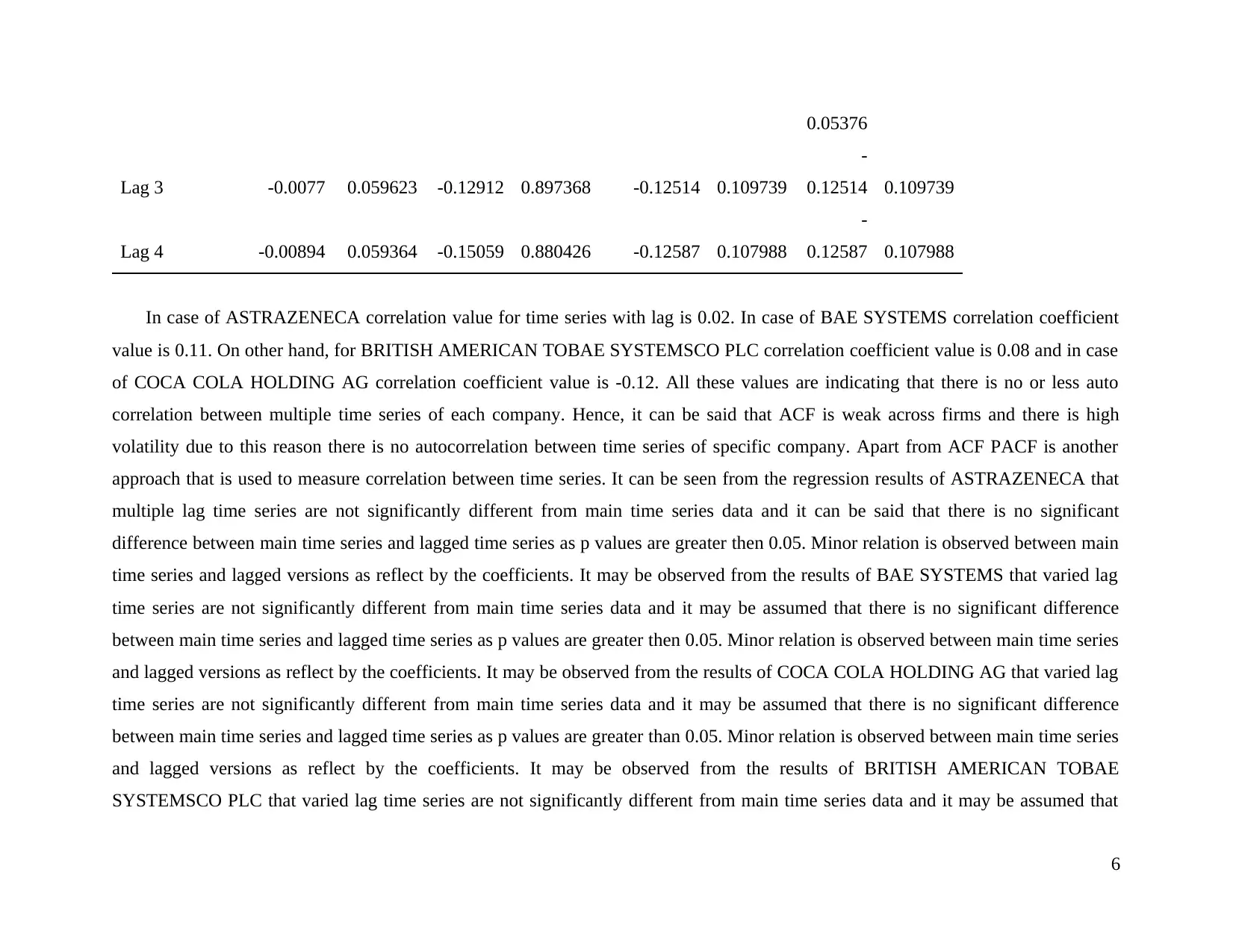

Table 4BRITISH AMERICAN TOBAE SYSTEMSCO PLC PACF

Regression Statistics

Multiple R 0.068414

R Square 0.00468

Adjusted R

Square -0.00746

Standard

Error 0.018061

Observations 250

ANOVA

df SS MS F

Significance

F

Regression 3 0.000377 0.000126 0.385602 0.76347

Residual 246 0.080245 0.000326

Total 249 0.080623

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -0.00011 0.001145 -0.09206 0.926725 -0.00236 0.002149

-

0.00236 0.002149

Lag 2 0.063239 0.059399 1.064646 0.28808 -0.05376 0.180235 - 0.180235

5

Regression Statistics

Multiple R 0.068414

R Square 0.00468

Adjusted R

Square -0.00746

Standard

Error 0.018061

Observations 250

ANOVA

df SS MS F

Significance

F

Regression 3 0.000377 0.000126 0.385602 0.76347

Residual 246 0.080245 0.000326

Total 249 0.080623

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -0.00011 0.001145 -0.09206 0.926725 -0.00236 0.002149

-

0.00236 0.002149

Lag 2 0.063239 0.059399 1.064646 0.28808 -0.05376 0.180235 - 0.180235

5

0.05376

Lag 3 -0.0077 0.059623 -0.12912 0.897368 -0.12514 0.109739

-

0.12514 0.109739

Lag 4 -0.00894 0.059364 -0.15059 0.880426 -0.12587 0.107988

-

0.12587 0.107988

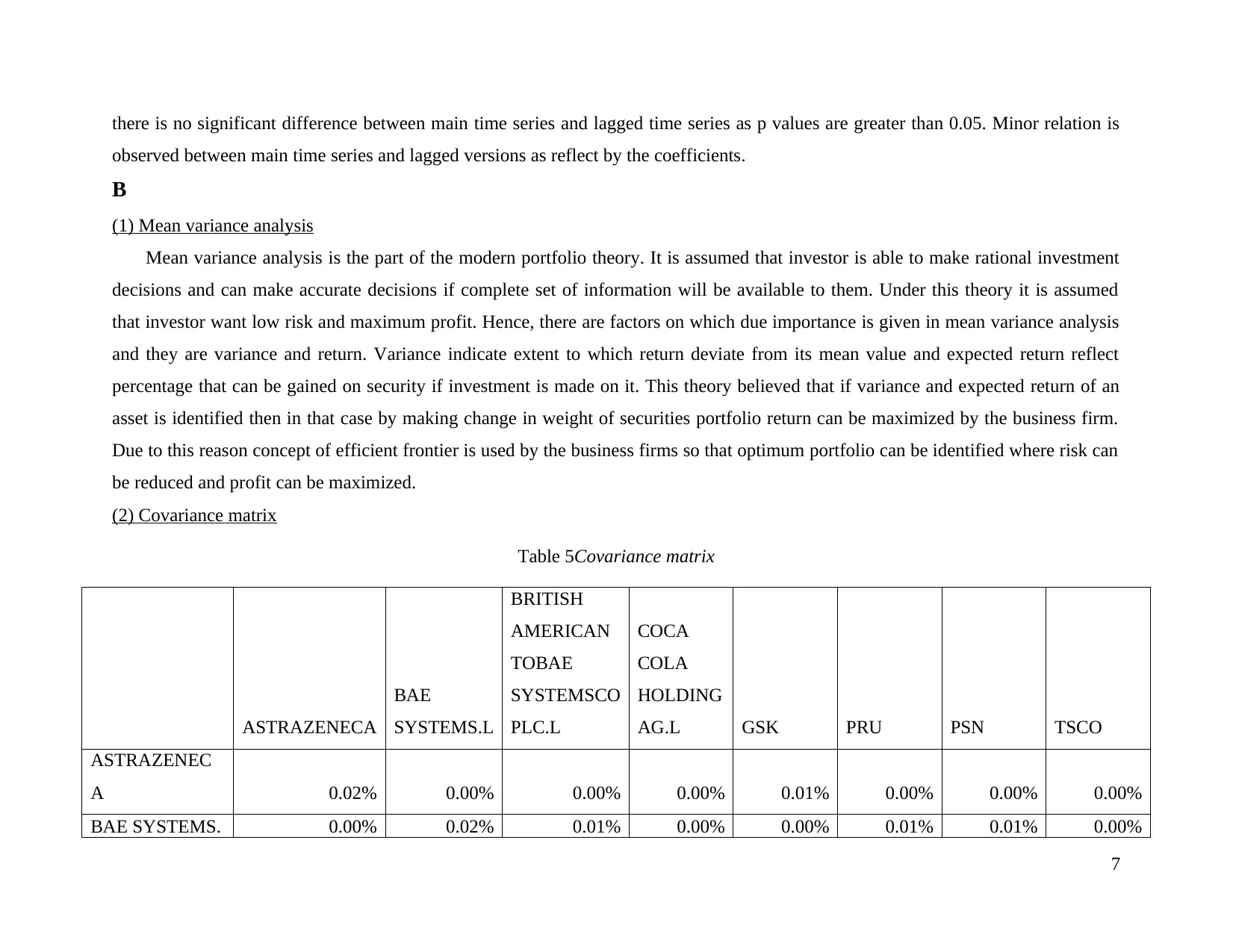

In case of ASTRAZENECA correlation value for time series with lag is 0.02. In case of BAE SYSTEMS correlation coefficient

value is 0.11. On other hand, for BRITISH AMERICAN TOBAE SYSTEMSCO PLC correlation coefficient value is 0.08 and in case

of COCA COLA HOLDING AG correlation coefficient value is -0.12. All these values are indicating that there is no or less auto

correlation between multiple time series of each company. Hence, it can be said that ACF is weak across firms and there is high

volatility due to this reason there is no autocorrelation between time series of specific company. Apart from ACF PACF is another

approach that is used to measure correlation between time series. It can be seen from the regression results of ASTRAZENECA that

multiple lag time series are not significantly different from main time series data and it can be said that there is no significant

difference between main time series and lagged time series as p values are greater then 0.05. Minor relation is observed between main

time series and lagged versions as reflect by the coefficients. It may be observed from the results of BAE SYSTEMS that varied lag

time series are not significantly different from main time series data and it may be assumed that there is no significant difference

between main time series and lagged time series as p values are greater then 0.05. Minor relation is observed between main time series

and lagged versions as reflect by the coefficients. It may be observed from the results of COCA COLA HOLDING AG that varied lag

time series are not significantly different from main time series data and it may be assumed that there is no significant difference

between main time series and lagged time series as p values are greater than 0.05. Minor relation is observed between main time series

and lagged versions as reflect by the coefficients. It may be observed from the results of BRITISH AMERICAN TOBAE

SYSTEMSCO PLC that varied lag time series are not significantly different from main time series data and it may be assumed that

6

Lag 3 -0.0077 0.059623 -0.12912 0.897368 -0.12514 0.109739

-

0.12514 0.109739

Lag 4 -0.00894 0.059364 -0.15059 0.880426 -0.12587 0.107988

-

0.12587 0.107988

In case of ASTRAZENECA correlation value for time series with lag is 0.02. In case of BAE SYSTEMS correlation coefficient

value is 0.11. On other hand, for BRITISH AMERICAN TOBAE SYSTEMSCO PLC correlation coefficient value is 0.08 and in case

of COCA COLA HOLDING AG correlation coefficient value is -0.12. All these values are indicating that there is no or less auto

correlation between multiple time series of each company. Hence, it can be said that ACF is weak across firms and there is high

volatility due to this reason there is no autocorrelation between time series of specific company. Apart from ACF PACF is another

approach that is used to measure correlation between time series. It can be seen from the regression results of ASTRAZENECA that

multiple lag time series are not significantly different from main time series data and it can be said that there is no significant

difference between main time series and lagged time series as p values are greater then 0.05. Minor relation is observed between main

time series and lagged versions as reflect by the coefficients. It may be observed from the results of BAE SYSTEMS that varied lag

time series are not significantly different from main time series data and it may be assumed that there is no significant difference

between main time series and lagged time series as p values are greater then 0.05. Minor relation is observed between main time series

and lagged versions as reflect by the coefficients. It may be observed from the results of COCA COLA HOLDING AG that varied lag

time series are not significantly different from main time series data and it may be assumed that there is no significant difference

between main time series and lagged time series as p values are greater than 0.05. Minor relation is observed between main time series

and lagged versions as reflect by the coefficients. It may be observed from the results of BRITISH AMERICAN TOBAE

SYSTEMSCO PLC that varied lag time series are not significantly different from main time series data and it may be assumed that

6

there is no significant difference between main time series and lagged time series as p values are greater than 0.05. Minor relation is

observed between main time series and lagged versions as reflect by the coefficients.

B

(1) Mean variance analysis

Mean variance analysis is the part of the modern portfolio theory. It is assumed that investor is able to make rational investment

decisions and can make accurate decisions if complete set of information will be available to them. Under this theory it is assumed

that investor want low risk and maximum profit. Hence, there are factors on which due importance is given in mean variance analysis

and they are variance and return. Variance indicate extent to which return deviate from its mean value and expected return reflect

percentage that can be gained on security if investment is made on it. This theory believed that if variance and expected return of an

asset is identified then in that case by making change in weight of securities portfolio return can be maximized by the business firm.

Due to this reason concept of efficient frontier is used by the business firms so that optimum portfolio can be identified where risk can

be reduced and profit can be maximized.

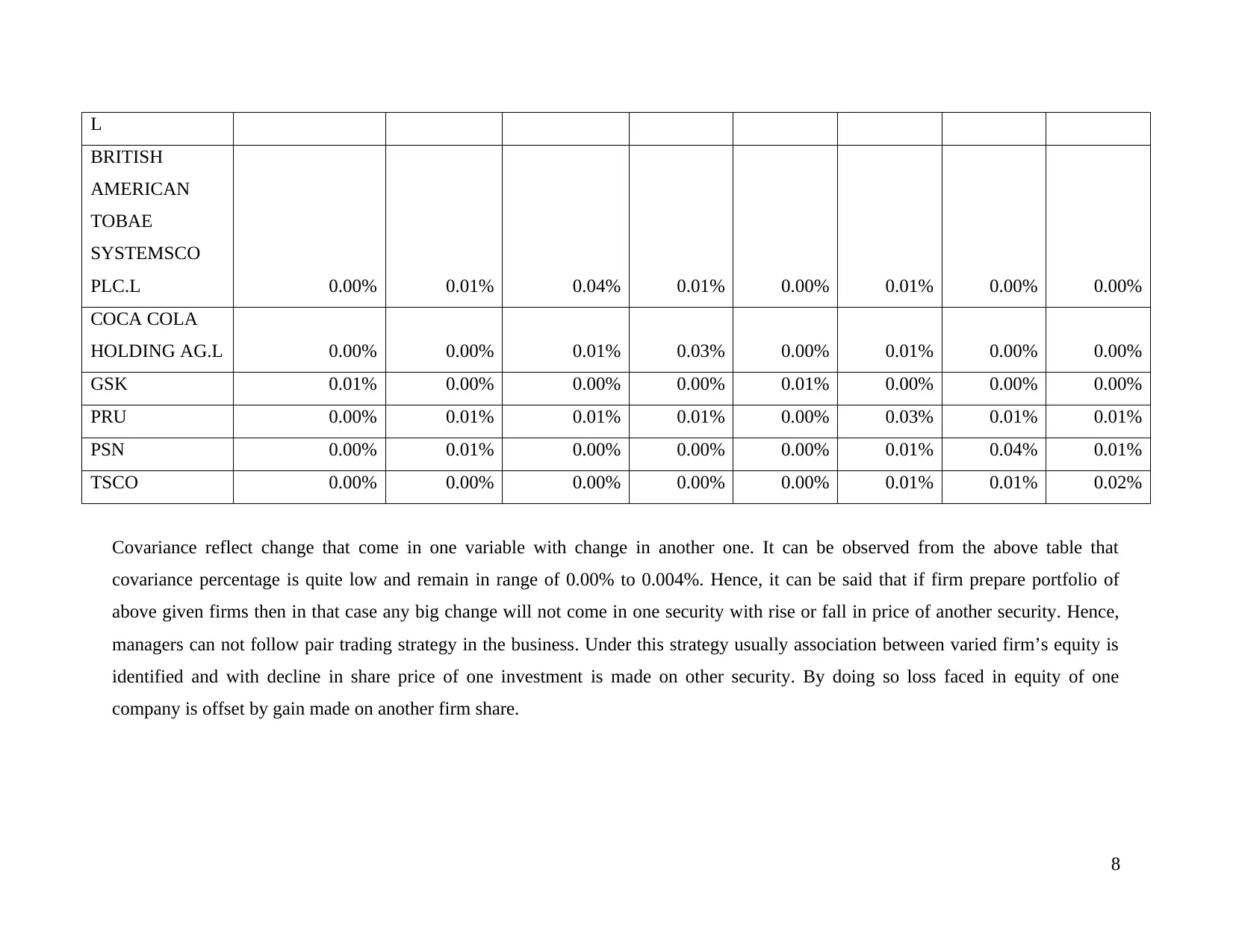

(2) Covariance matrix

Table 5Covariance matrix

ASTRAZENECA

BAE

SYSTEMS.L

BRITISH

AMERICAN

TOBAE

SYSTEMSCO

PLC.L

COCA

COLA

HOLDING

AG.L GSK PRU PSN TSCO

ASTRAZENEC

A 0.02% 0.00% 0.00% 0.00% 0.01% 0.00% 0.00% 0.00%

BAE SYSTEMS. 0.00% 0.02% 0.01% 0.00% 0.00% 0.01% 0.01% 0.00%

7

observed between main time series and lagged versions as reflect by the coefficients.

B

(1) Mean variance analysis

Mean variance analysis is the part of the modern portfolio theory. It is assumed that investor is able to make rational investment

decisions and can make accurate decisions if complete set of information will be available to them. Under this theory it is assumed

that investor want low risk and maximum profit. Hence, there are factors on which due importance is given in mean variance analysis

and they are variance and return. Variance indicate extent to which return deviate from its mean value and expected return reflect

percentage that can be gained on security if investment is made on it. This theory believed that if variance and expected return of an

asset is identified then in that case by making change in weight of securities portfolio return can be maximized by the business firm.

Due to this reason concept of efficient frontier is used by the business firms so that optimum portfolio can be identified where risk can

be reduced and profit can be maximized.

(2) Covariance matrix

Table 5Covariance matrix

ASTRAZENECA

BAE

SYSTEMS.L

BRITISH

AMERICAN

TOBAE

SYSTEMSCO

PLC.L

COCA

COLA

HOLDING

AG.L GSK PRU PSN TSCO

ASTRAZENEC

A 0.02% 0.00% 0.00% 0.00% 0.01% 0.00% 0.00% 0.00%

BAE SYSTEMS. 0.00% 0.02% 0.01% 0.00% 0.00% 0.01% 0.01% 0.00%

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

L

BRITISH

AMERICAN

TOBAE

SYSTEMSCO

PLC.L 0.00% 0.01% 0.04% 0.01% 0.00% 0.01% 0.00% 0.00%

COCA COLA

HOLDING AG.L 0.00% 0.00% 0.01% 0.03% 0.00% 0.01% 0.00% 0.00%

GSK 0.01% 0.00% 0.00% 0.00% 0.01% 0.00% 0.00% 0.00%

PRU 0.00% 0.01% 0.01% 0.01% 0.00% 0.03% 0.01% 0.01%

PSN 0.00% 0.01% 0.00% 0.00% 0.00% 0.01% 0.04% 0.01%

TSCO 0.00% 0.00% 0.00% 0.00% 0.00% 0.01% 0.01% 0.02%

Covariance reflect change that come in one variable with change in another one. It can be observed from the above table that

covariance percentage is quite low and remain in range of 0.00% to 0.004%. Hence, it can be said that if firm prepare portfolio of

above given firms then in that case any big change will not come in one security with rise or fall in price of another security. Hence,

managers can not follow pair trading strategy in the business. Under this strategy usually association between varied firm’s equity is

identified and with decline in share price of one investment is made on other security. By doing so loss faced in equity of one

company is offset by gain made on another firm share.

8

BRITISH

AMERICAN

TOBAE

SYSTEMSCO

PLC.L 0.00% 0.01% 0.04% 0.01% 0.00% 0.01% 0.00% 0.00%

COCA COLA

HOLDING AG.L 0.00% 0.00% 0.01% 0.03% 0.00% 0.01% 0.00% 0.00%

GSK 0.01% 0.00% 0.00% 0.00% 0.01% 0.00% 0.00% 0.00%

PRU 0.00% 0.01% 0.01% 0.01% 0.00% 0.03% 0.01% 0.01%

PSN 0.00% 0.01% 0.00% 0.00% 0.00% 0.01% 0.04% 0.01%

TSCO 0.00% 0.00% 0.00% 0.00% 0.00% 0.01% 0.01% 0.02%

Covariance reflect change that come in one variable with change in another one. It can be observed from the above table that

covariance percentage is quite low and remain in range of 0.00% to 0.004%. Hence, it can be said that if firm prepare portfolio of

above given firms then in that case any big change will not come in one security with rise or fall in price of another security. Hence,

managers can not follow pair trading strategy in the business. Under this strategy usually association between varied firm’s equity is

identified and with decline in share price of one investment is made on other security. By doing so loss faced in equity of one

company is offset by gain made on another firm share.

8

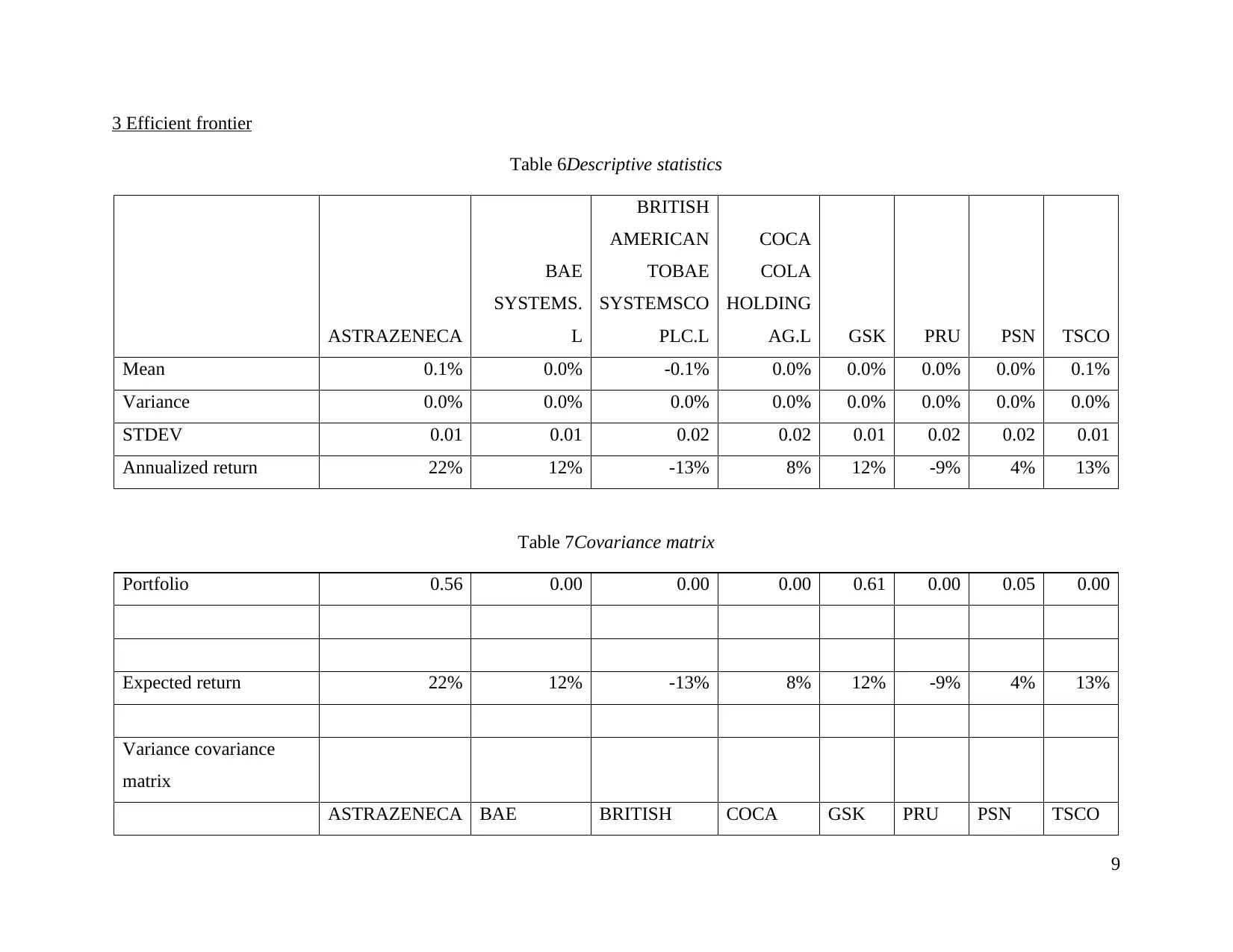

3 Efficient frontier

Table 6Descriptive statistics

ASTRAZENECA

BAE

SYSTEMS.

L

BRITISH

AMERICAN

TOBAE

SYSTEMSCO

PLC.L

COCA

COLA

HOLDING

AG.L GSK PRU PSN TSCO

Mean 0.1% 0.0% -0.1% 0.0% 0.0% 0.0% 0.0% 0.1%

Variance 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

STDEV 0.01 0.01 0.02 0.02 0.01 0.02 0.02 0.01

Annualized return 22% 12% -13% 8% 12% -9% 4% 13%

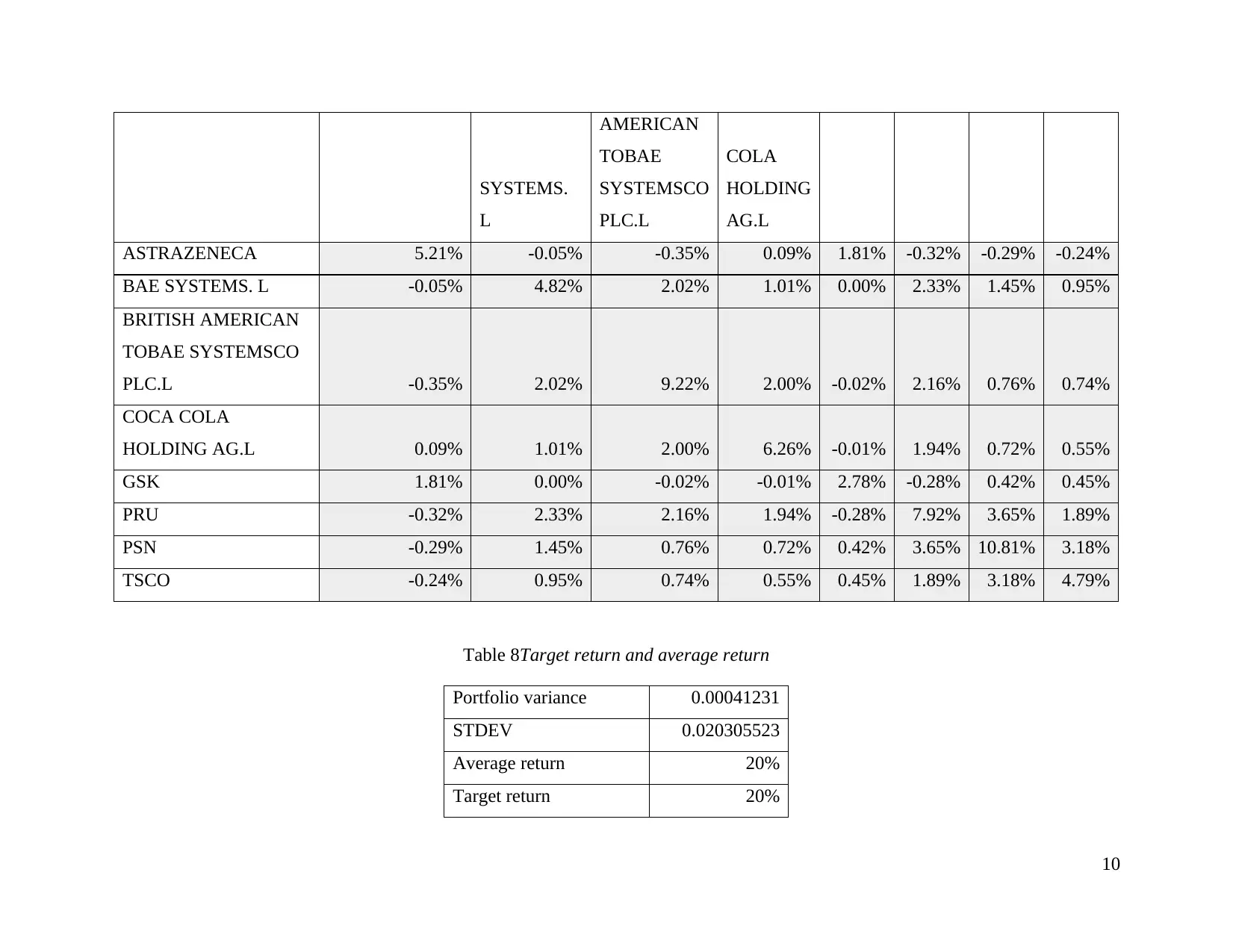

Table 7Covariance matrix

Portfolio 0.56 0.00 0.00 0.00 0.61 0.00 0.05 0.00

Expected return 22% 12% -13% 8% 12% -9% 4% 13%

Variance covariance

matrix

ASTRAZENECA BAE BRITISH COCA GSK PRU PSN TSCO

9

Table 6Descriptive statistics

ASTRAZENECA

BAE

SYSTEMS.

L

BRITISH

AMERICAN

TOBAE

SYSTEMSCO

PLC.L

COCA

COLA

HOLDING

AG.L GSK PRU PSN TSCO

Mean 0.1% 0.0% -0.1% 0.0% 0.0% 0.0% 0.0% 0.1%

Variance 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

STDEV 0.01 0.01 0.02 0.02 0.01 0.02 0.02 0.01

Annualized return 22% 12% -13% 8% 12% -9% 4% 13%

Table 7Covariance matrix

Portfolio 0.56 0.00 0.00 0.00 0.61 0.00 0.05 0.00

Expected return 22% 12% -13% 8% 12% -9% 4% 13%

Variance covariance

matrix

ASTRAZENECA BAE BRITISH COCA GSK PRU PSN TSCO

9

SYSTEMS.

L

AMERICAN

TOBAE

SYSTEMSCO

PLC.L

COLA

HOLDING

AG.L

ASTRAZENECA 5.21% -0.05% -0.35% 0.09% 1.81% -0.32% -0.29% -0.24%

BAE SYSTEMS. L -0.05% 4.82% 2.02% 1.01% 0.00% 2.33% 1.45% 0.95%

BRITISH AMERICAN

TOBAE SYSTEMSCO

PLC.L -0.35% 2.02% 9.22% 2.00% -0.02% 2.16% 0.76% 0.74%

COCA COLA

HOLDING AG.L 0.09% 1.01% 2.00% 6.26% -0.01% 1.94% 0.72% 0.55%

GSK 1.81% 0.00% -0.02% -0.01% 2.78% -0.28% 0.42% 0.45%

PRU -0.32% 2.33% 2.16% 1.94% -0.28% 7.92% 3.65% 1.89%

PSN -0.29% 1.45% 0.76% 0.72% 0.42% 3.65% 10.81% 3.18%

TSCO -0.24% 0.95% 0.74% 0.55% 0.45% 1.89% 3.18% 4.79%

Table 8Target return and average return

Portfolio variance 0.00041231

STDEV 0.020305523

Average return 20%

Target return 20%

10

L

AMERICAN

TOBAE

SYSTEMSCO

PLC.L

COLA

HOLDING

AG.L

ASTRAZENECA 5.21% -0.05% -0.35% 0.09% 1.81% -0.32% -0.29% -0.24%

BAE SYSTEMS. L -0.05% 4.82% 2.02% 1.01% 0.00% 2.33% 1.45% 0.95%

BRITISH AMERICAN

TOBAE SYSTEMSCO

PLC.L -0.35% 2.02% 9.22% 2.00% -0.02% 2.16% 0.76% 0.74%

COCA COLA

HOLDING AG.L 0.09% 1.01% 2.00% 6.26% -0.01% 1.94% 0.72% 0.55%

GSK 1.81% 0.00% -0.02% -0.01% 2.78% -0.28% 0.42% 0.45%

PRU -0.32% 2.33% 2.16% 1.94% -0.28% 7.92% 3.65% 1.89%

PSN -0.29% 1.45% 0.76% 0.72% 0.42% 3.65% 10.81% 3.18%

TSCO -0.24% 0.95% 0.74% 0.55% 0.45% 1.89% 3.18% 4.79%

Table 8Target return and average return

Portfolio variance 0.00041231

STDEV 0.020305523

Average return 20%

Target return 20%

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

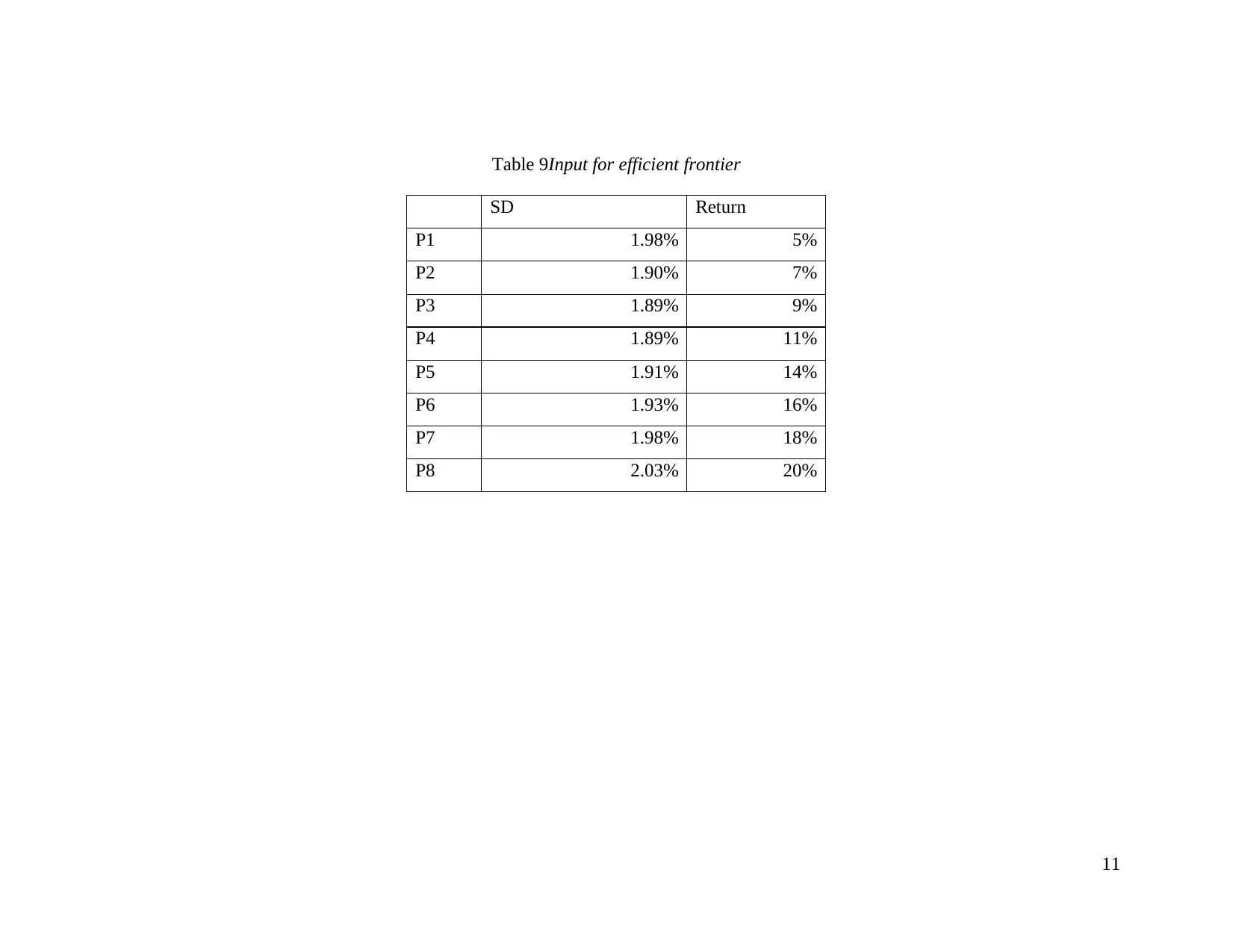

Table 9Input for efficient frontier

SD Return

P1 1.98% 5%

P2 1.90% 7%

P3 1.89% 9%

P4 1.89% 11%

P5 1.91% 14%

P6 1.93% 16%

P7 1.98% 18%

P8 2.03% 20%

11

SD Return

P1 1.98% 5%

P2 1.90% 7%

P3 1.89% 9%

P4 1.89% 11%

P5 1.91% 14%

P6 1.93% 16%

P7 1.98% 18%

P8 2.03% 20%

11

Figure 1Efficient frontier

Efficient frontier is the approach where by investor identify portfolio that must be taken in to account so that risk can be reduced and

profit can be maximized. If one will select portfolio that is on top then in that case risk and return both will be high. Opposite to this, if

one pick a portfolio that is at start of cure then risk will be moderate and return will be low ( Modern portfolio theory efficient and

optimal portfolios., 2019). Portfolio that is on the lowest standard deviation is considered as one of the best portfolios. In the above

chart two portfolio are indicated with green colour that are one of the best option to be picked because standard deviation is less then

1.90% which is lowest in above given chart and return percentage of 10% which to some extent can be considered good and moderate

return in the above chart. Hence, it can be said that efficient frontier assists one to choose best one from available options.

12

Efficient frontier is the approach where by investor identify portfolio that must be taken in to account so that risk can be reduced and

profit can be maximized. If one will select portfolio that is on top then in that case risk and return both will be high. Opposite to this, if

one pick a portfolio that is at start of cure then risk will be moderate and return will be low ( Modern portfolio theory efficient and

optimal portfolios., 2019). Portfolio that is on the lowest standard deviation is considered as one of the best portfolios. In the above

chart two portfolio are indicated with green colour that are one of the best option to be picked because standard deviation is less then

1.90% which is lowest in above given chart and return percentage of 10% which to some extent can be considered good and moderate

return in the above chart. Hence, it can be said that efficient frontier assists one to choose best one from available options.

12

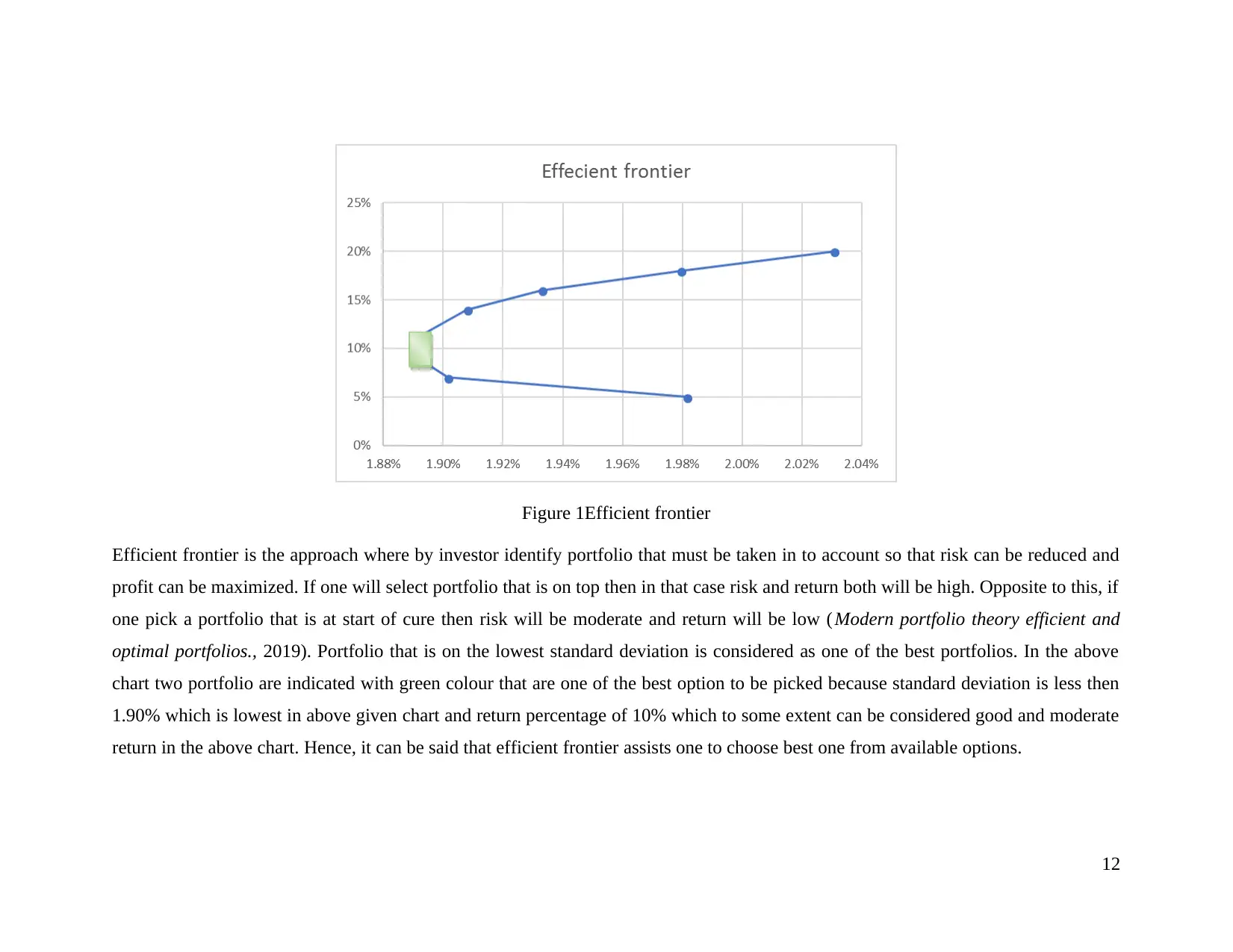

(C) GARCH results

Figure 2GARCH for ASTRAZENECA 10 months

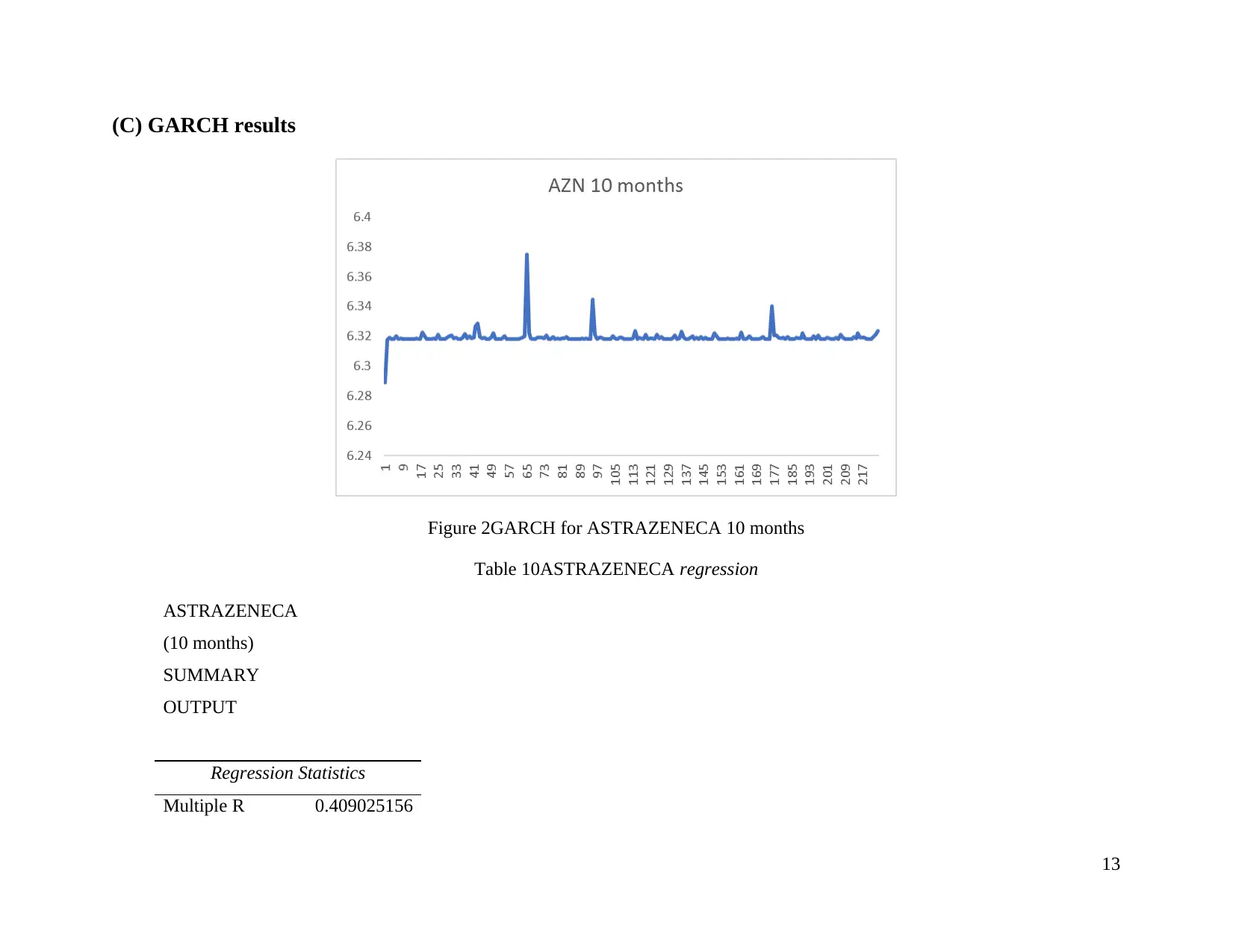

Table 10ASTRAZENECA regression

ASTRAZENECA

(10 months)

SUMMARY

OUTPUT

Regression Statistics

Multiple R 0.409025156

13

Figure 2GARCH for ASTRAZENECA 10 months

Table 10ASTRAZENECA regression

ASTRAZENECA

(10 months)

SUMMARY

OUTPUT

Regression Statistics

Multiple R 0.409025156

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

R Square 0.167301578

Adjusted R

Square 0.163584174

Standard Error 2.418216429

Observations 226

ANOVA

df SS MS F

Significance

F

Regression 1 263.1786 263.1786 45.00495 1.59E-10

Residual 224 1309.901 5.847771

Total 225 1573.079

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 7.224394936 4.961806 1.456001 0.146793 -2.5534 17.00219 -2.5534 17.00219

FTSE 100 0.004617626 0.000688 6.708573 1.59E-10 0.003261 0.005974 0.003261 0.005974

Table 11Statistics for ASTRAZENECA 10 months

Overall MLE -205.4008547

Persistence 7.229012562

14

Adjusted R

Square 0.163584174

Standard Error 2.418216429

Observations 226

ANOVA

df SS MS F

Significance

F

Regression 1 263.1786 263.1786 45.00495 1.59E-10

Residual 224 1309.901 5.847771

Total 225 1573.079

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 7.224394936 4.961806 1.456001 0.146793 -2.5534 17.00219 -2.5534 17.00219

FTSE 100 0.004617626 0.000688 6.708573 1.59E-10 0.003261 0.005974 0.003261 0.005974

Table 11Statistics for ASTRAZENECA 10 months

Overall MLE -205.4008547

Persistence 7.229012562

14

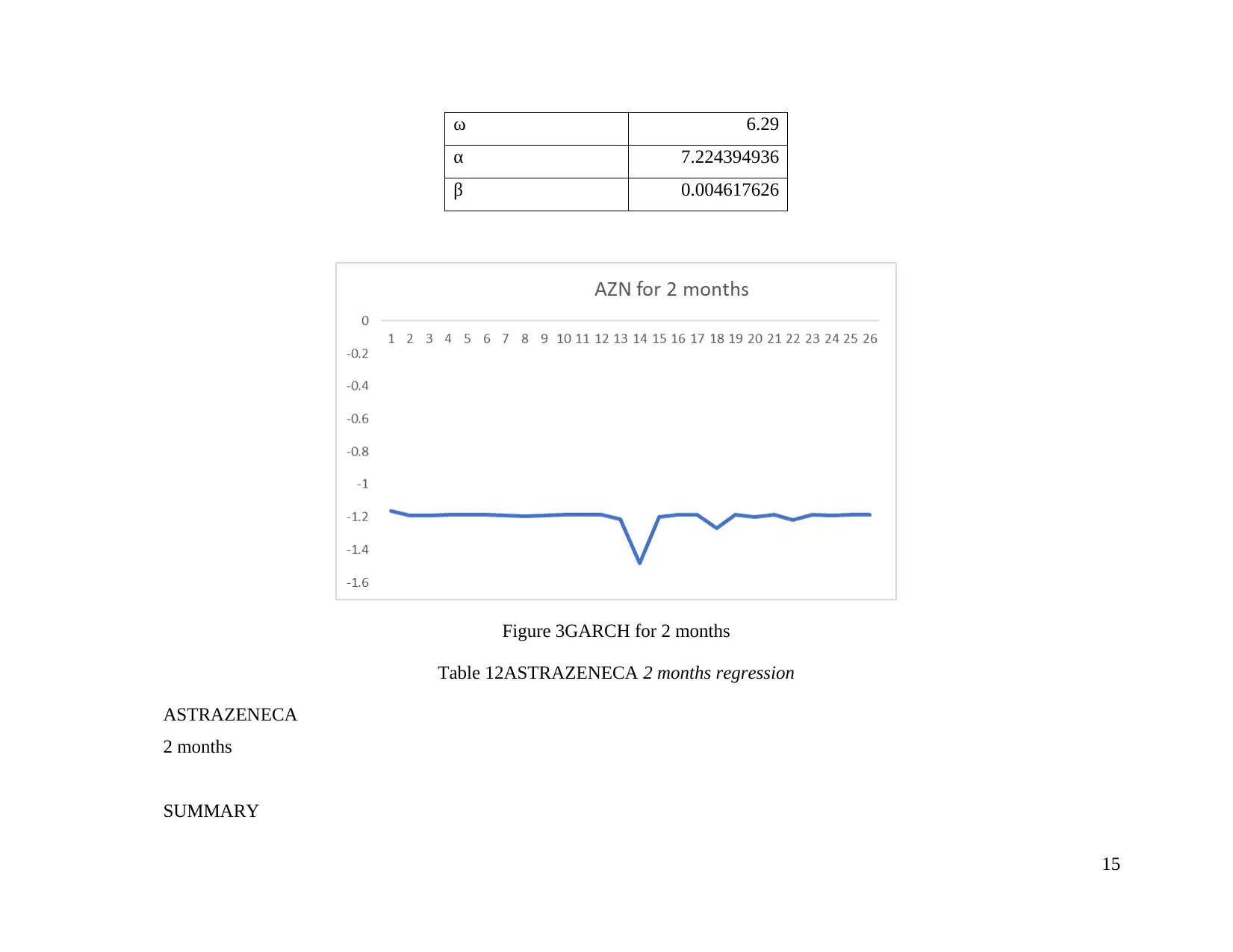

ω 6.29

α 7.224394936

β 0.004617626

Figure 3GARCH for 2 months

Table 12ASTRAZENECA 2 months regression

ASTRAZENECA

2 months

SUMMARY

15

α 7.224394936

β 0.004617626

Figure 3GARCH for 2 months

Table 12ASTRAZENECA 2 months regression

ASTRAZENECA

2 months

SUMMARY

15

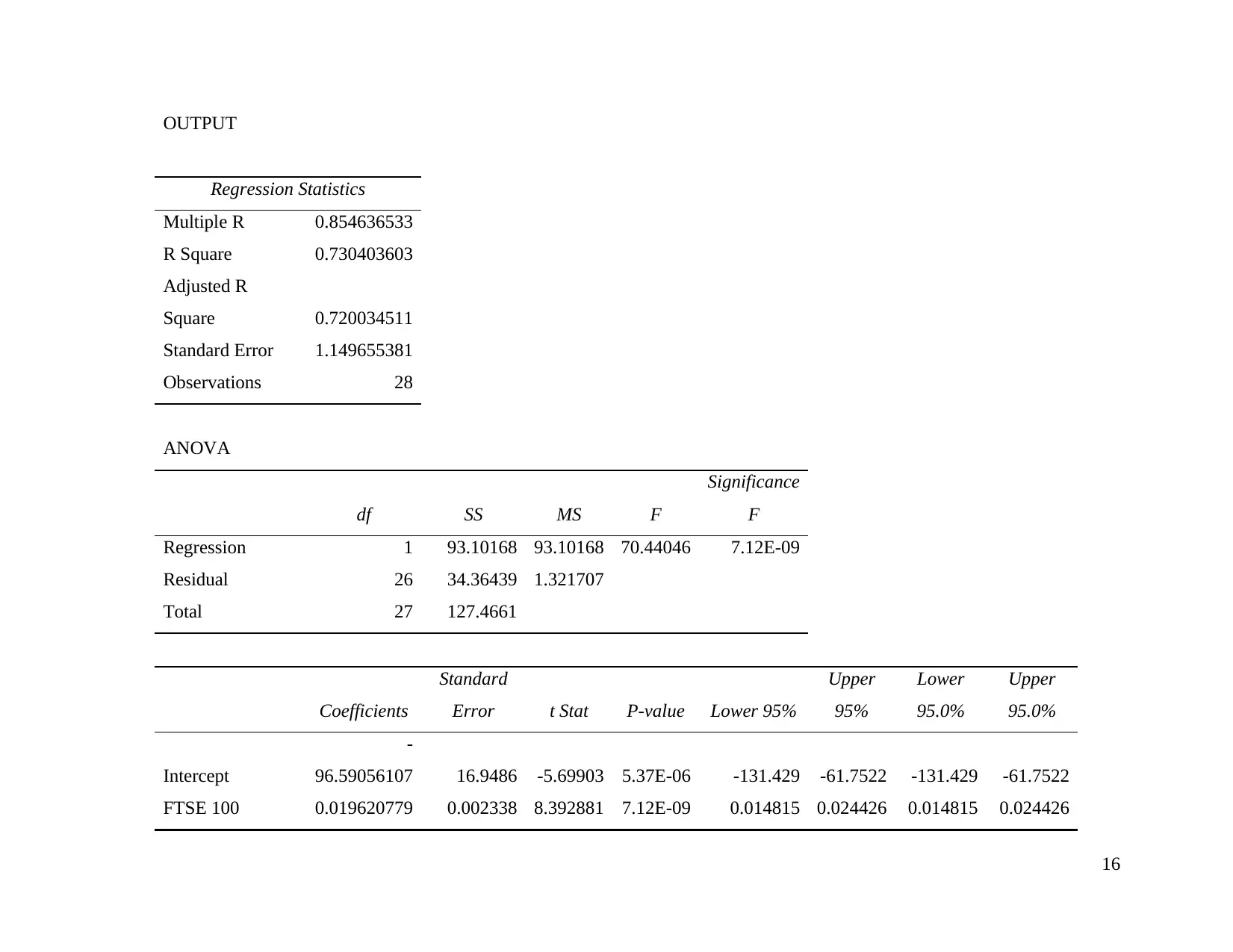

OUTPUT

Regression Statistics

Multiple R 0.854636533

R Square 0.730403603

Adjusted R

Square 0.720034511

Standard Error 1.149655381

Observations 28

ANOVA

df SS MS F

Significance

F

Regression 1 93.10168 93.10168 70.44046 7.12E-09

Residual 26 34.36439 1.321707

Total 27 127.4661

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

-

96.59056107 16.9486 -5.69903 5.37E-06 -131.429 -61.7522 -131.429 -61.7522

FTSE 100 0.019620779 0.002338 8.392881 7.12E-09 0.014815 0.024426 0.014815 0.024426

16

Regression Statistics

Multiple R 0.854636533

R Square 0.730403603

Adjusted R

Square 0.720034511

Standard Error 1.149655381

Observations 28

ANOVA

df SS MS F

Significance

F

Regression 1 93.10168 93.10168 70.44046 7.12E-09

Residual 26 34.36439 1.321707

Total 27 127.4661

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

-

96.59056107 16.9486 -5.69903 5.37E-06 -131.429 -61.7522 -131.429 -61.7522

FTSE 100 0.019620779 0.002338 8.392881 7.12E-09 0.014815 0.024426 0.014815 0.024426

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

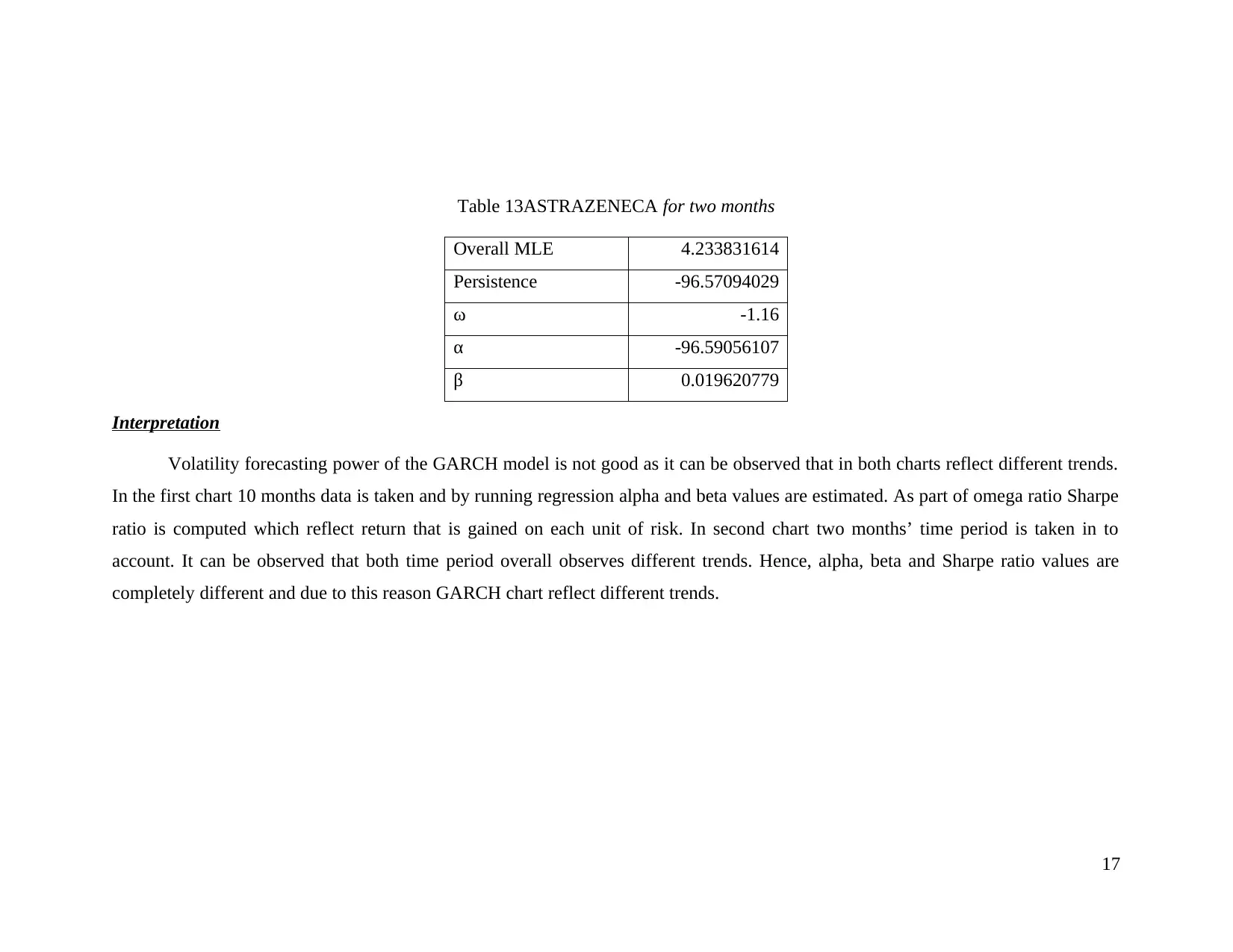

Table 13ASTRAZENECA for two months

Overall MLE 4.233831614

Persistence -96.57094029

ω -1.16

α -96.59056107

β 0.019620779

Interpretation

Volatility forecasting power of the GARCH model is not good as it can be observed that in both charts reflect different trends.

In the first chart 10 months data is taken and by running regression alpha and beta values are estimated. As part of omega ratio Sharpe

ratio is computed which reflect return that is gained on each unit of risk. In second chart two months’ time period is taken in to

account. It can be observed that both time period overall observes different trends. Hence, alpha, beta and Sharpe ratio values are

completely different and due to this reason GARCH chart reflect different trends.

17

Overall MLE 4.233831614

Persistence -96.57094029

ω -1.16

α -96.59056107

β 0.019620779

Interpretation

Volatility forecasting power of the GARCH model is not good as it can be observed that in both charts reflect different trends.

In the first chart 10 months data is taken and by running regression alpha and beta values are estimated. As part of omega ratio Sharpe

ratio is computed which reflect return that is gained on each unit of risk. In second chart two months’ time period is taken in to

account. It can be observed that both time period overall observes different trends. Hence, alpha, beta and Sharpe ratio values are

completely different and due to this reason GARCH chart reflect different trends.

17

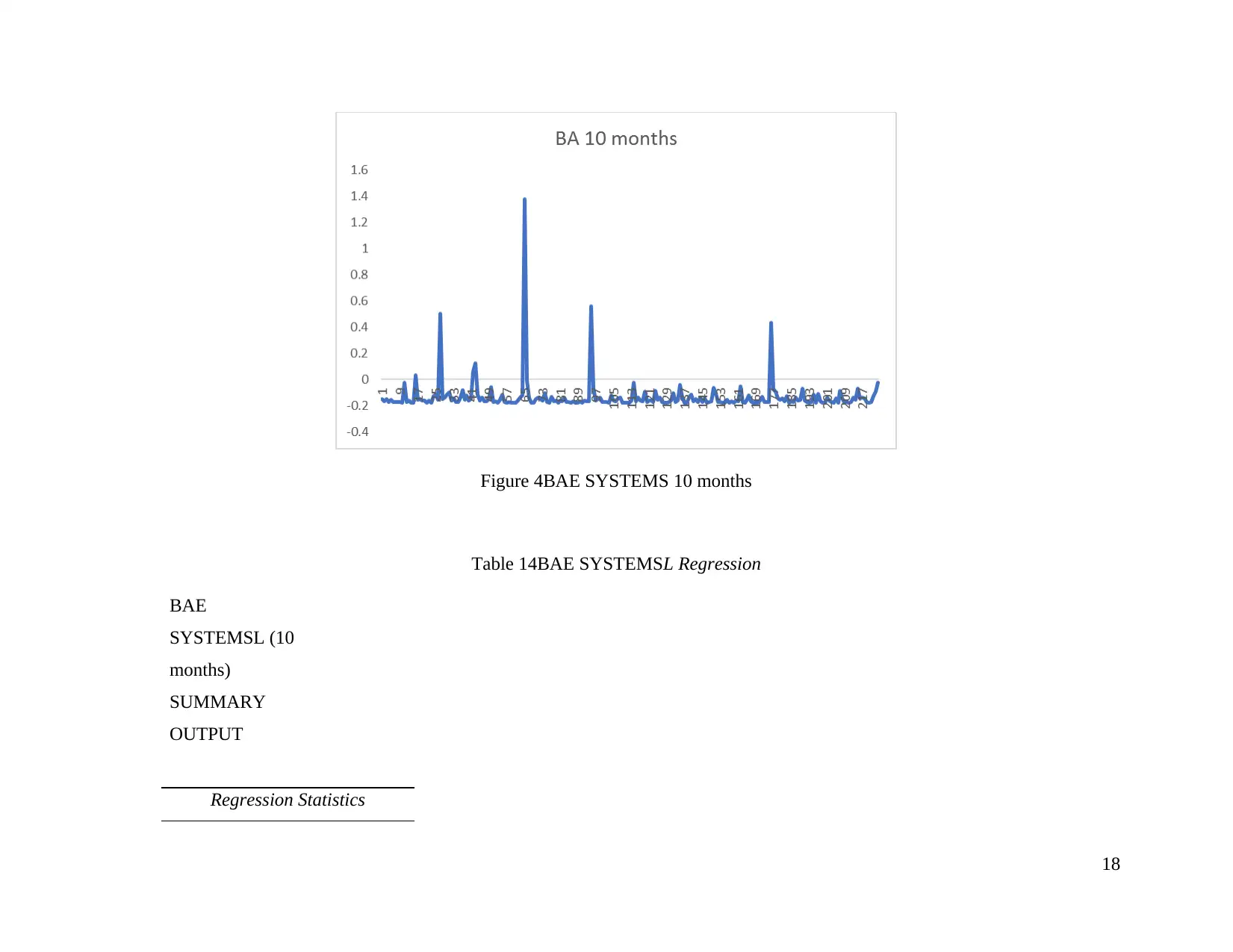

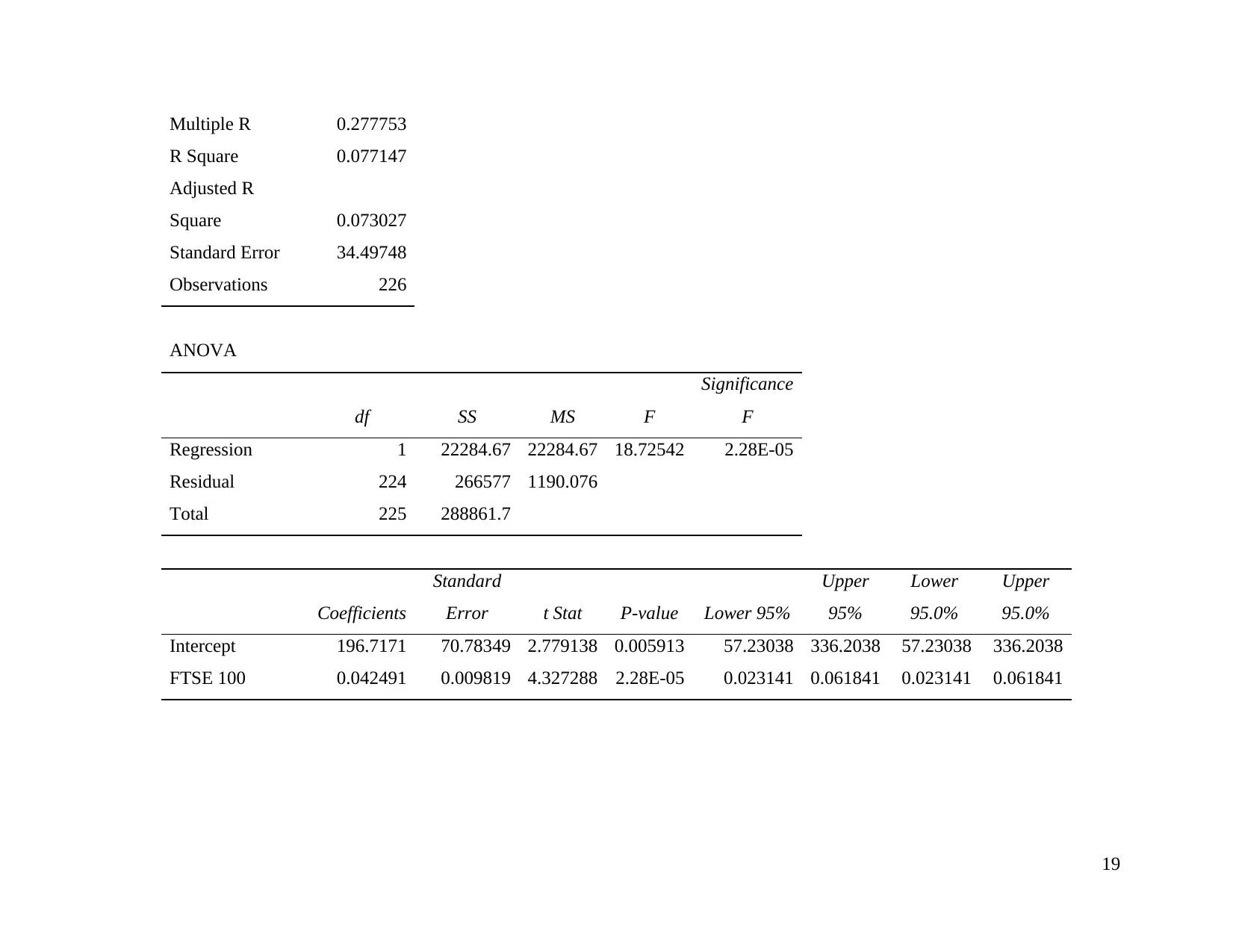

Figure 4BAE SYSTEMS 10 months

Table 14BAE SYSTEMSL Regression

BAE

SYSTEMSL (10

months)

SUMMARY

OUTPUT

Regression Statistics

18

Table 14BAE SYSTEMSL Regression

BAE

SYSTEMSL (10

months)

SUMMARY

OUTPUT

Regression Statistics

18

Multiple R 0.277753

R Square 0.077147

Adjusted R

Square 0.073027

Standard Error 34.49748

Observations 226

ANOVA

df SS MS F

Significance

F

Regression 1 22284.67 22284.67 18.72542 2.28E-05

Residual 224 266577 1190.076

Total 225 288861.7

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 196.7171 70.78349 2.779138 0.005913 57.23038 336.2038 57.23038 336.2038

FTSE 100 0.042491 0.009819 4.327288 2.28E-05 0.023141 0.061841 0.023141 0.061841

19

R Square 0.077147

Adjusted R

Square 0.073027

Standard Error 34.49748

Observations 226

ANOVA

df SS MS F

Significance

F

Regression 1 22284.67 22284.67 18.72542 2.28E-05

Residual 224 266577 1190.076

Total 225 288861.7

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 196.7171 70.78349 2.779138 0.005913 57.23038 336.2038 57.23038 336.2038

FTSE 100 0.042491 0.009819 4.327288 2.28E-05 0.023141 0.061841 0.023141 0.061841

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

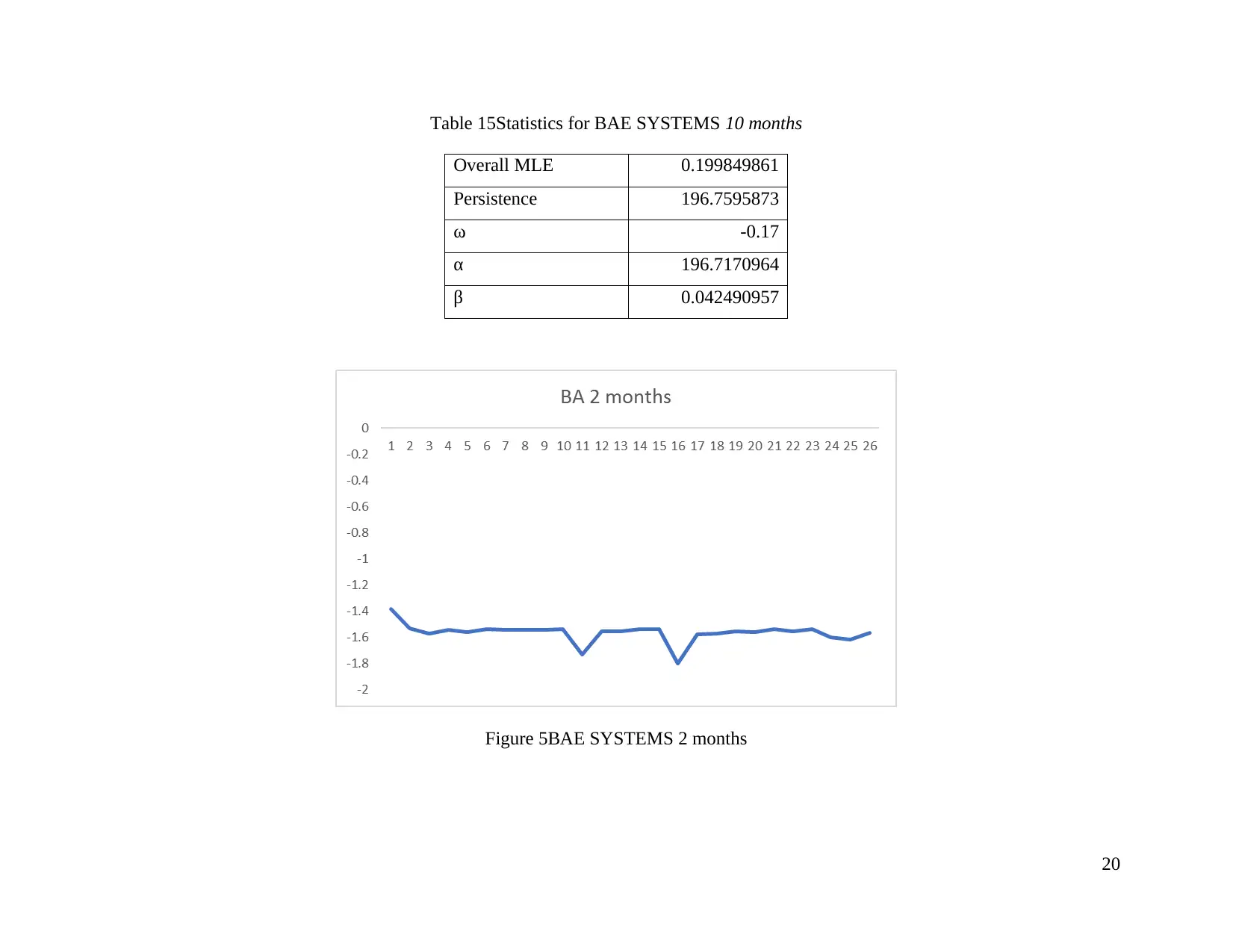

Table 15Statistics for BAE SYSTEMS 10 months

Overall MLE 0.199849861

Persistence 196.7595873

ω -0.17

α 196.7170964

β 0.042490957

Figure 5BAE SYSTEMS 2 months

20

Overall MLE 0.199849861

Persistence 196.7595873

ω -0.17

α 196.7170964

β 0.042490957

Figure 5BAE SYSTEMS 2 months

20

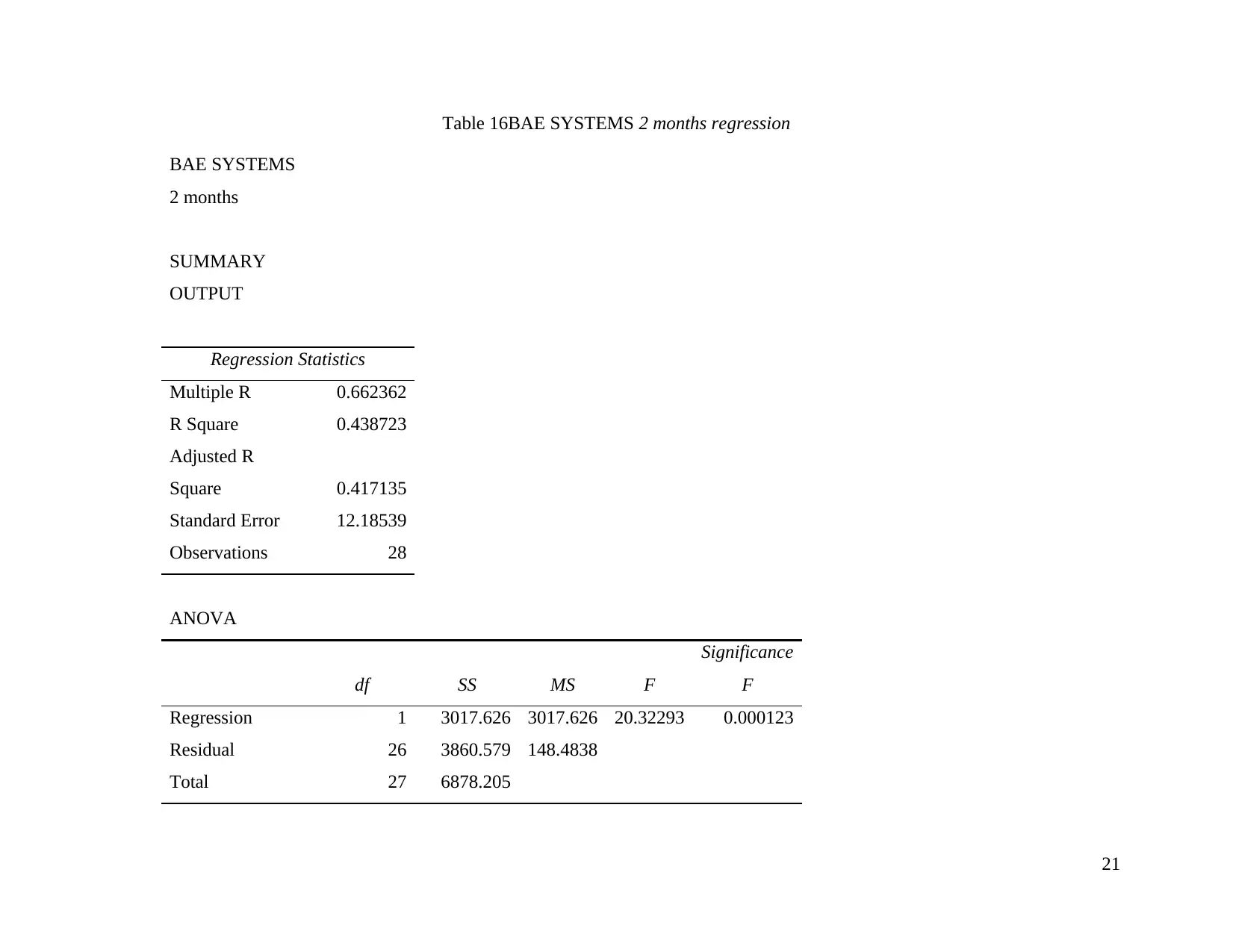

Table 16BAE SYSTEMS 2 months regression

BAE SYSTEMS

2 months

SUMMARY

OUTPUT

Regression Statistics

Multiple R 0.662362

R Square 0.438723

Adjusted R

Square 0.417135

Standard Error 12.18539

Observations 28

ANOVA

df SS MS F

Significance

F

Regression 1 3017.626 3017.626 20.32293 0.000123

Residual 26 3860.579 148.4838

Total 27 6878.205

21

BAE SYSTEMS

2 months

SUMMARY

OUTPUT

Regression Statistics

Multiple R 0.662362

R Square 0.438723

Adjusted R

Square 0.417135

Standard Error 12.18539

Observations 28

ANOVA

df SS MS F

Significance

F

Regression 1 3017.626 3017.626 20.32293 0.000123

Residual 26 3860.579 148.4838

Total 27 6878.205

21

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

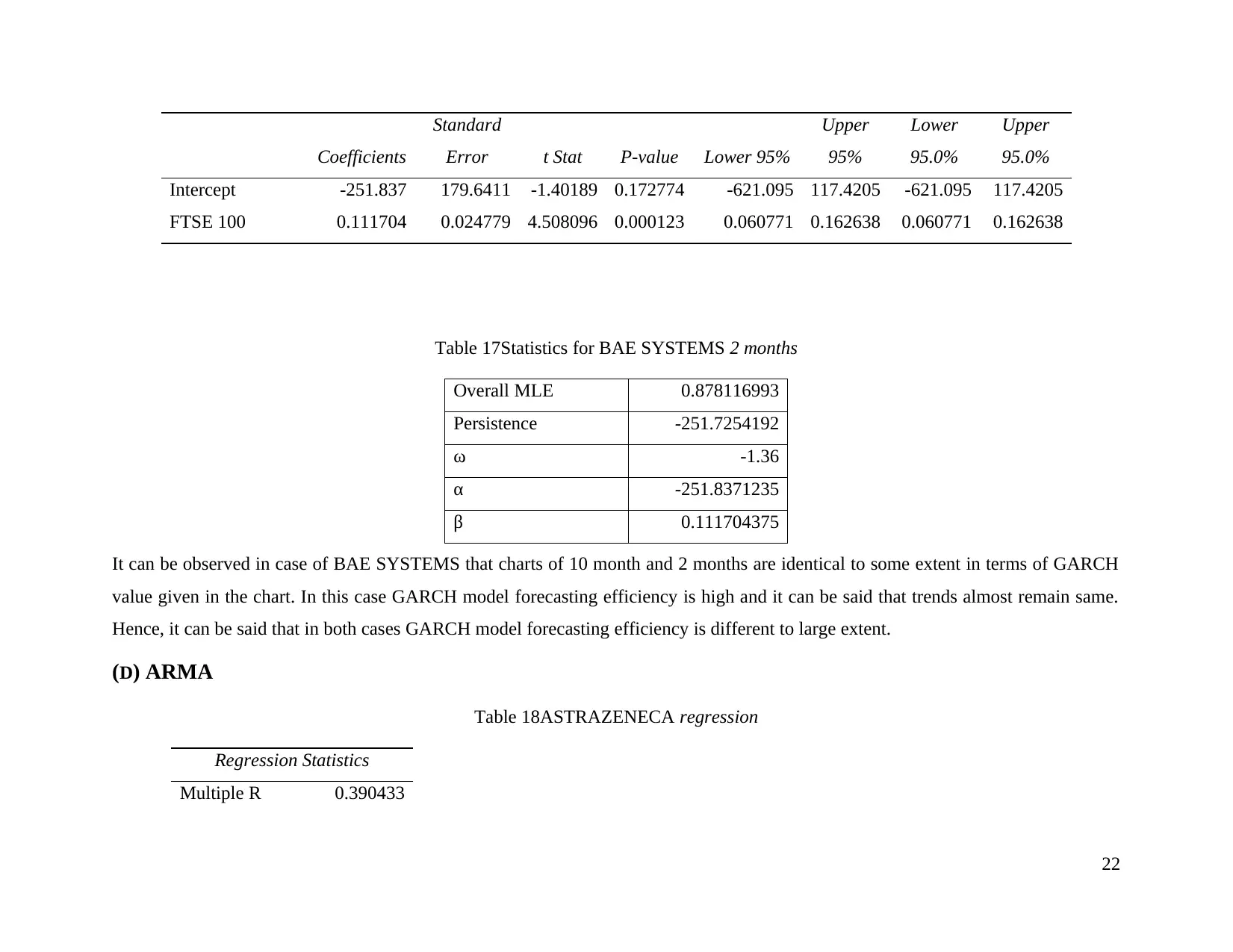

Intercept -251.837 179.6411 -1.40189 0.172774 -621.095 117.4205 -621.095 117.4205

FTSE 100 0.111704 0.024779 4.508096 0.000123 0.060771 0.162638 0.060771 0.162638

Table 17Statistics for BAE SYSTEMS 2 months

Overall MLE 0.878116993

Persistence -251.7254192

ω -1.36

α -251.8371235

β 0.111704375

It can be observed in case of BAE SYSTEMS that charts of 10 month and 2 months are identical to some extent in terms of GARCH

value given in the chart. In this case GARCH model forecasting efficiency is high and it can be said that trends almost remain same.

Hence, it can be said that in both cases GARCH model forecasting efficiency is different to large extent.

(D) ARMA

Table 18ASTRAZENECA regression

Regression Statistics

Multiple R 0.390433

22

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -251.837 179.6411 -1.40189 0.172774 -621.095 117.4205 -621.095 117.4205

FTSE 100 0.111704 0.024779 4.508096 0.000123 0.060771 0.162638 0.060771 0.162638

Table 17Statistics for BAE SYSTEMS 2 months

Overall MLE 0.878116993

Persistence -251.7254192

ω -1.36

α -251.8371235

β 0.111704375

It can be observed in case of BAE SYSTEMS that charts of 10 month and 2 months are identical to some extent in terms of GARCH

value given in the chart. In this case GARCH model forecasting efficiency is high and it can be said that trends almost remain same.

Hence, it can be said that in both cases GARCH model forecasting efficiency is different to large extent.

(D) ARMA

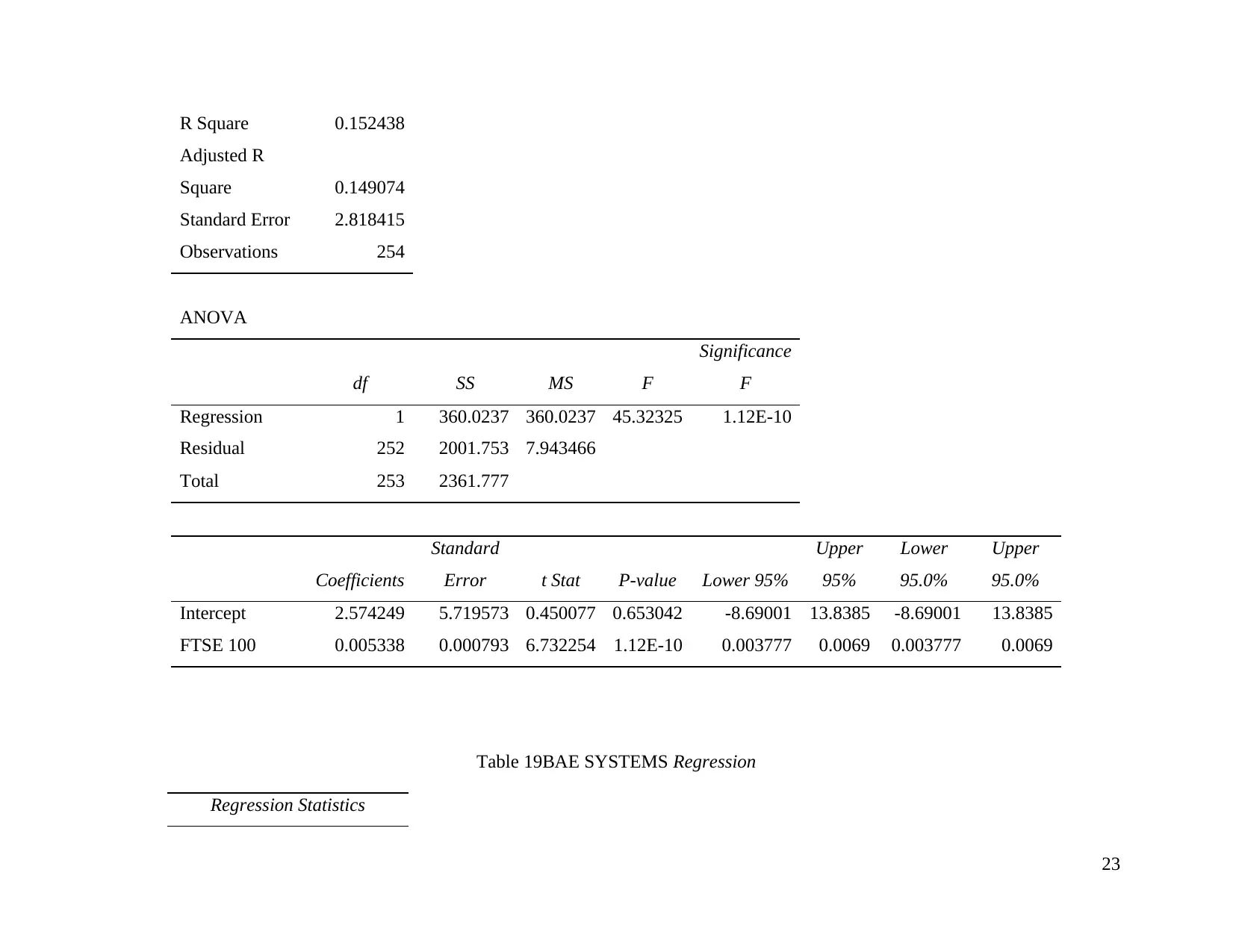

Table 18ASTRAZENECA regression

Regression Statistics

Multiple R 0.390433

22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

R Square 0.152438

Adjusted R

Square 0.149074

Standard Error 2.818415

Observations 254

ANOVA

df SS MS F

Significance

F

Regression 1 360.0237 360.0237 45.32325 1.12E-10

Residual 252 2001.753 7.943466

Total 253 2361.777

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 2.574249 5.719573 0.450077 0.653042 -8.69001 13.8385 -8.69001 13.8385

FTSE 100 0.005338 0.000793 6.732254 1.12E-10 0.003777 0.0069 0.003777 0.0069

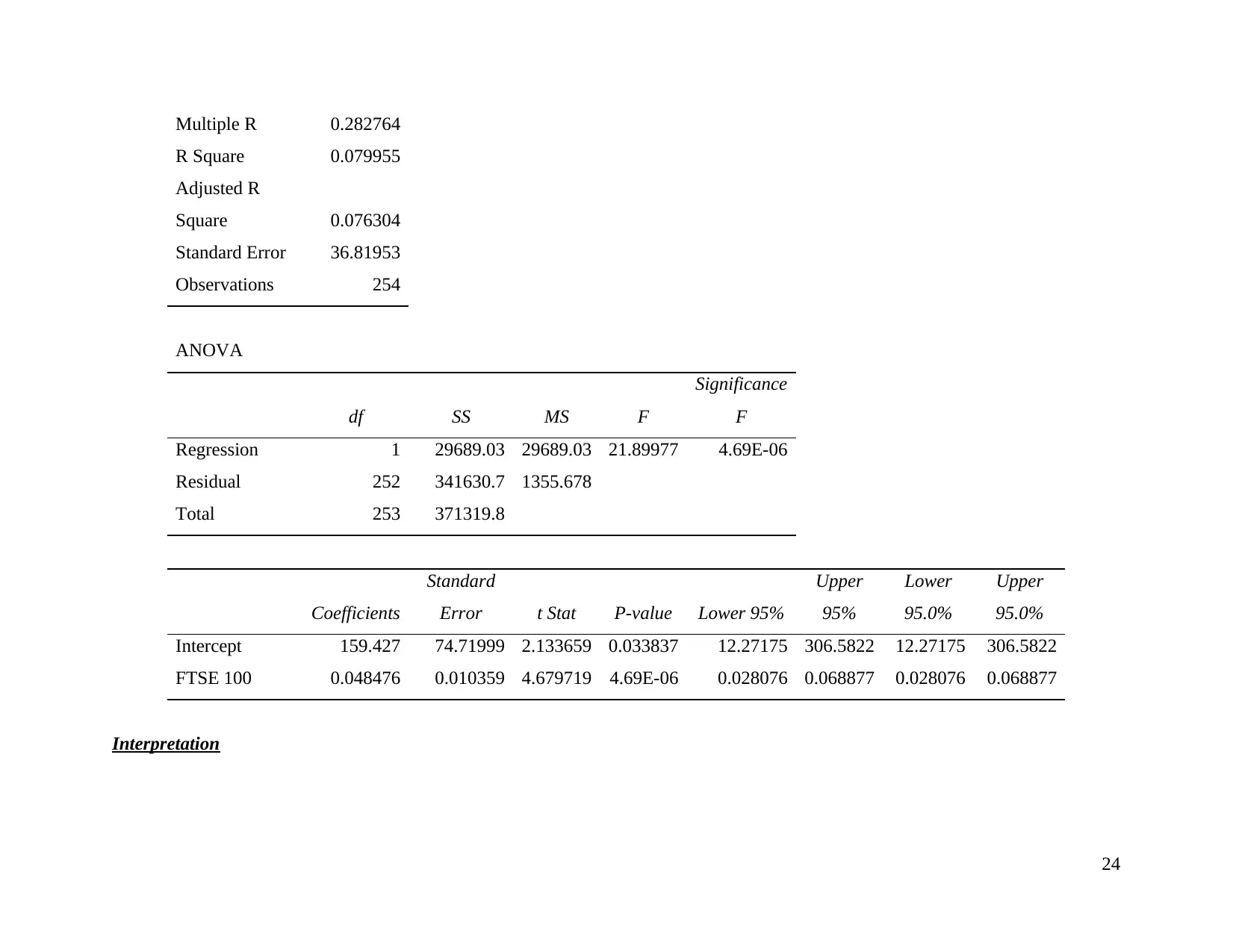

Table 19BAE SYSTEMS Regression

Regression Statistics

23

Adjusted R

Square 0.149074

Standard Error 2.818415

Observations 254

ANOVA

df SS MS F

Significance

F

Regression 1 360.0237 360.0237 45.32325 1.12E-10

Residual 252 2001.753 7.943466

Total 253 2361.777

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 2.574249 5.719573 0.450077 0.653042 -8.69001 13.8385 -8.69001 13.8385

FTSE 100 0.005338 0.000793 6.732254 1.12E-10 0.003777 0.0069 0.003777 0.0069

Table 19BAE SYSTEMS Regression

Regression Statistics

23

Multiple R 0.282764

R Square 0.079955

Adjusted R

Square 0.076304

Standard Error 36.81953

Observations 254

ANOVA

df SS MS F

Significance

F

Regression 1 29689.03 29689.03 21.89977 4.69E-06

Residual 252 341630.7 1355.678

Total 253 371319.8

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 159.427 74.71999 2.133659 0.033837 12.27175 306.5822 12.27175 306.5822

FTSE 100 0.048476 0.010359 4.679719 4.69E-06 0.028076 0.068877 0.028076 0.068877

Interpretation

24

R Square 0.079955

Adjusted R

Square 0.076304

Standard Error 36.81953

Observations 254

ANOVA

df SS MS F

Significance

F

Regression 1 29689.03 29689.03 21.89977 4.69E-06

Residual 252 341630.7 1355.678

Total 253 371319.8

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 159.427 74.71999 2.133659 0.033837 12.27175 306.5822 12.27175 306.5822

FTSE 100 0.048476 0.010359 4.679719 4.69E-06 0.028076 0.068877 0.028076 0.068877

Interpretation

24

Sum of square for ASTRAZENECA is 422905.3296 and same in case of BAE SYSTEMS is 59420723. It can be said that

variance is high in case of both firms and this means that shares are fluctuating at rapid pace which means that there is high risk

profile of both firms shares. BAE SYSTEMS shares are highly volatile then ASTRAZENECA shares.

CONCLUSION

On the BAE systemssis of above analysis, it is concluded that regression method is the one of best approach that is used to

compute beta and intercept values. Mentioned tool scope is wide in terms of its use in the business and management. It is also

concluded that modern portfolio theory assists to large extent to investors in terms of making sound investment decisions. By using

efficient frontier model, one can prepare portfolio in such a way which lead to reduced risk and higher return on investment. It is also

concluded that GARCH and ARCH model to large extent assist investor to evaluate trends and making investment decisions.

25

variance is high in case of both firms and this means that shares are fluctuating at rapid pace which means that there is high risk

profile of both firms shares. BAE SYSTEMS shares are highly volatile then ASTRAZENECA shares.

CONCLUSION

On the BAE systemssis of above analysis, it is concluded that regression method is the one of best approach that is used to

compute beta and intercept values. Mentioned tool scope is wide in terms of its use in the business and management. It is also

concluded that modern portfolio theory assists to large extent to investors in terms of making sound investment decisions. By using

efficient frontier model, one can prepare portfolio in such a way which lead to reduced risk and higher return on investment. It is also

concluded that GARCH and ARCH model to large extent assist investor to evaluate trends and making investment decisions.

25

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCE

Books and journals

Modern portfolio theory efficient and optimal portfolios., 2019. [Online]. Available through:<

https://thismatter.com/money/investments/modern-portfolio-theory.htm>.

26

Books and journals

Modern portfolio theory efficient and optimal portfolios., 2019. [Online]. Available through:<

https://thismatter.com/money/investments/modern-portfolio-theory.htm>.

26

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.