Project Methodologies

Added on 2023-01-19

29 Pages3173 Words50 Views

PROJECT METHODOLOGIES

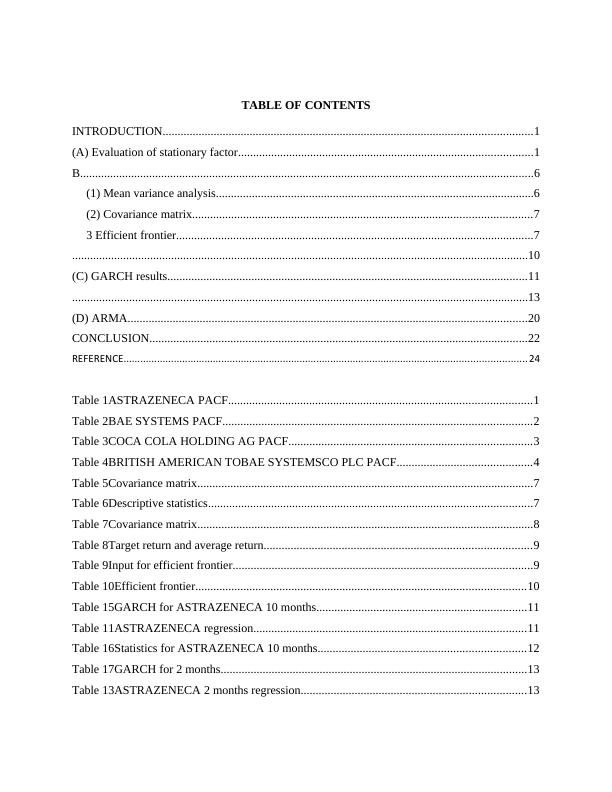

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

(A) Evaluation of stationary factor..................................................................................................1

B.......................................................................................................................................................6

(1) Mean variance analysis..........................................................................................................6

(2) Covariance matrix.................................................................................................................7

3 Efficient frontier.......................................................................................................................7

........................................................................................................................................................10

(C) GARCH results........................................................................................................................11

........................................................................................................................................................13

(D) ARMA.....................................................................................................................................20

CONCLUSION..............................................................................................................................22

REFERENCE................................................................................................................................................24

Table 1ASTRAZENECA PACF.....................................................................................................1

Table 2BAE SYSTEMS PACF.......................................................................................................2

Table 3COCA COLA HOLDING AG PACF.................................................................................3

Table 4BRITISH AMERICAN TOBAE SYSTEMSCO PLC PACF.............................................4

Table 5Covariance matrix................................................................................................................7

Table 6Descriptive statistics............................................................................................................7

Table 7Covariance matrix................................................................................................................8

Table 8Target return and average return.........................................................................................9

Table 9Input for efficient frontier....................................................................................................9

Table 10Efficient frontier..............................................................................................................10

Table 15GARCH for ASTRAZENECA 10 months......................................................................11

Table 11ASTRAZENECA regression...........................................................................................11

Table 16Statistics for ASTRAZENECA 10 months.....................................................................12

Table 17GARCH for 2 months......................................................................................................13

Table 13ASTRAZENECA 2 months regression...........................................................................13

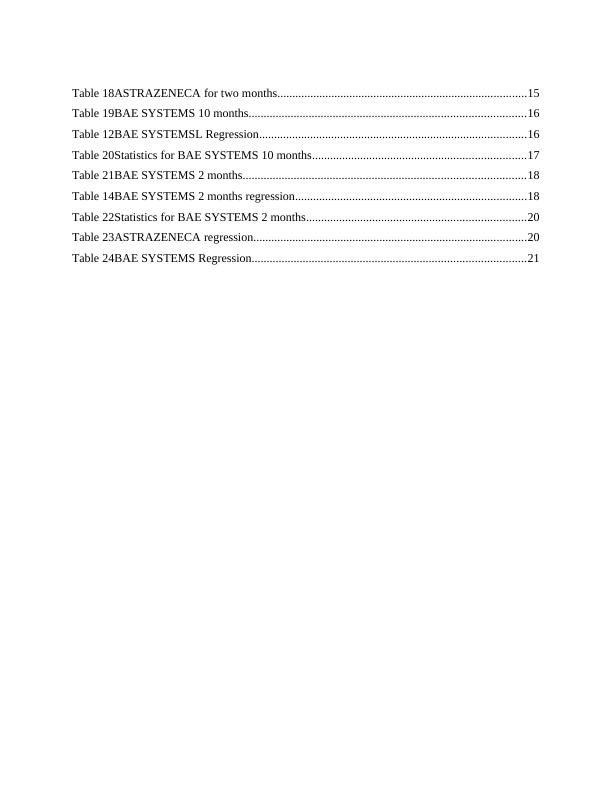

INTRODUCTION...........................................................................................................................1

(A) Evaluation of stationary factor..................................................................................................1

B.......................................................................................................................................................6

(1) Mean variance analysis..........................................................................................................6

(2) Covariance matrix.................................................................................................................7

3 Efficient frontier.......................................................................................................................7

........................................................................................................................................................10

(C) GARCH results........................................................................................................................11

........................................................................................................................................................13

(D) ARMA.....................................................................................................................................20

CONCLUSION..............................................................................................................................22

REFERENCE................................................................................................................................................24

Table 1ASTRAZENECA PACF.....................................................................................................1

Table 2BAE SYSTEMS PACF.......................................................................................................2

Table 3COCA COLA HOLDING AG PACF.................................................................................3

Table 4BRITISH AMERICAN TOBAE SYSTEMSCO PLC PACF.............................................4

Table 5Covariance matrix................................................................................................................7

Table 6Descriptive statistics............................................................................................................7

Table 7Covariance matrix................................................................................................................8

Table 8Target return and average return.........................................................................................9

Table 9Input for efficient frontier....................................................................................................9

Table 10Efficient frontier..............................................................................................................10

Table 15GARCH for ASTRAZENECA 10 months......................................................................11

Table 11ASTRAZENECA regression...........................................................................................11

Table 16Statistics for ASTRAZENECA 10 months.....................................................................12

Table 17GARCH for 2 months......................................................................................................13

Table 13ASTRAZENECA 2 months regression...........................................................................13

Table 18ASTRAZENECA for two months...................................................................................15

Table 19BAE SYSTEMS 10 months............................................................................................16

Table 12BAE SYSTEMSL Regression.........................................................................................16

Table 20Statistics for BAE SYSTEMS 10 months.......................................................................17

Table 21BAE SYSTEMS 2 months..............................................................................................18

Table 14BAE SYSTEMS 2 months regression.............................................................................18

Table 22Statistics for BAE SYSTEMS 2 months.........................................................................20

Table 23ASTRAZENECA regression...........................................................................................20

Table 24BAE SYSTEMS Regression...........................................................................................21

Table 19BAE SYSTEMS 10 months............................................................................................16

Table 12BAE SYSTEMSL Regression.........................................................................................16

Table 20Statistics for BAE SYSTEMS 10 months.......................................................................17

Table 21BAE SYSTEMS 2 months..............................................................................................18

Table 14BAE SYSTEMS 2 months regression.............................................................................18

Table 22Statistics for BAE SYSTEMS 2 months.........................................................................20

Table 23ASTRAZENECA regression...........................................................................................20

Table 24BAE SYSTEMS Regression...........................................................................................21

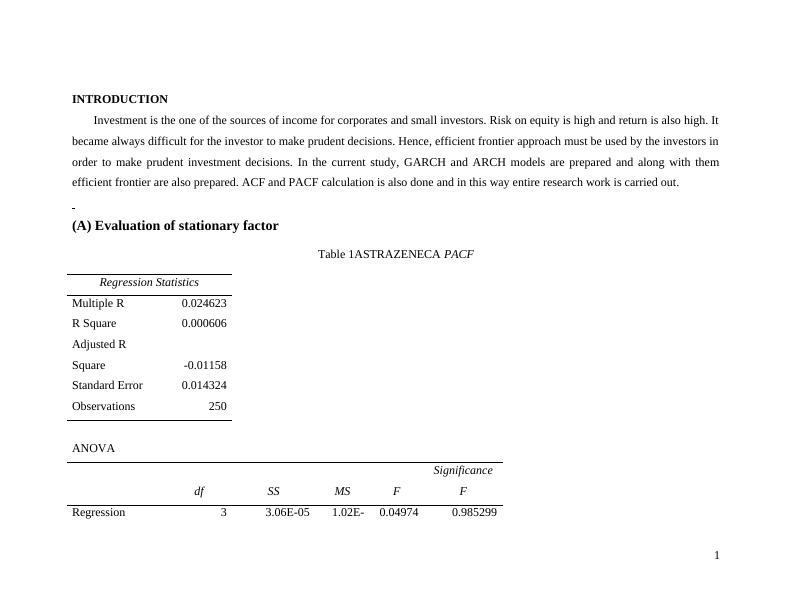

INTRODUCTION

Investment is the one of the sources of income for corporates and small investors. Risk on equity is high and return is also high. It

became always difficult for the investor to make prudent decisions. Hence, efficient frontier approach must be used by the investors in

order to make prudent investment decisions. In the current study, GARCH and ARCH models are prepared and along with them

efficient frontier are also prepared. ACF and PACF calculation is also done and in this way entire research work is carried out.

(A) Evaluation of stationary factor

Table 1ASTRAZENECA PACF

Regression Statistics

Multiple R 0.024623

R Square 0.000606

Adjusted R

Square -0.01158

Standard Error 0.014324

Observations 250

ANOVA

df SS MS F

Significance

F

Regression 3 3.06E-05 1.02E- 0.04974 0.985299

1

Investment is the one of the sources of income for corporates and small investors. Risk on equity is high and return is also high. It

became always difficult for the investor to make prudent decisions. Hence, efficient frontier approach must be used by the investors in

order to make prudent investment decisions. In the current study, GARCH and ARCH models are prepared and along with them

efficient frontier are also prepared. ACF and PACF calculation is also done and in this way entire research work is carried out.

(A) Evaluation of stationary factor

Table 1ASTRAZENECA PACF

Regression Statistics

Multiple R 0.024623

R Square 0.000606

Adjusted R

Square -0.01158

Standard Error 0.014324

Observations 250

ANOVA

df SS MS F

Significance

F

Regression 3 3.06E-05 1.02E- 0.04974 0.985299

1

05 4

Residual 246 0.050471

0.00020

5

Total 249 0.050502

Coefficient

s

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0.000596 0.000909

0.65583

8

0.51254

1 -0.00119 0.002386 -0.00119 0.002386

Lag 2 0.023965 0.063764 0.37583

0.70736

7 -0.10163 0.149559 -0.10163 0.149559

Lag 3 -0.00472 0.063757 -0.0741

0.94099

3 -0.1303 0.120855 -0.1303 0.120855

Lag 4 -0.0036 0.062989 -0.05708

0.95453

1 -0.12766 0.120471 -0.12766 0.120471

Table 2BAE SYSTEMS PACF

Regression Statistics

Multiple R 0.115003739

R Square 0.01322586

Adjusted R

Square 0.001192029

2

Residual 246 0.050471

0.00020

5

Total 249 0.050502

Coefficient

s

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0.000596 0.000909

0.65583

8

0.51254

1 -0.00119 0.002386 -0.00119 0.002386

Lag 2 0.023965 0.063764 0.37583

0.70736

7 -0.10163 0.149559 -0.10163 0.149559

Lag 3 -0.00472 0.063757 -0.0741

0.94099

3 -0.1303 0.120855 -0.1303 0.120855

Lag 4 -0.0036 0.062989 -0.05708

0.95453

1 -0.12766 0.120471 -0.12766 0.120471

Table 2BAE SYSTEMS PACF

Regression Statistics

Multiple R 0.115003739

R Square 0.01322586

Adjusted R

Square 0.001192029

2

Standard Error 0.014060995

Observations 250

ANOVA

df SS MS F

Significance

F

Regression 3 0.000652 0.000217 1.099056 0.350169

Residual 246 0.048637 0.000198

Total 249 0.049289

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0.000380909 0.00089 0.427991 0.669032 -0.00137 0.002134 -0.00137 0.002134

Lag 2 0.113199299 0.063782 1.774779 0.077171 -0.01243 0.238828 -0.01243 0.238828

Lag 3 0.007945121 0.064332 0.123502 0.901811 -0.11877 0.134657 -0.11877 0.134657

Lag 4

-

0.017024478 0.064132 -0.26546 0.790876 -0.14334 0.109293 -0.14334 0.109293

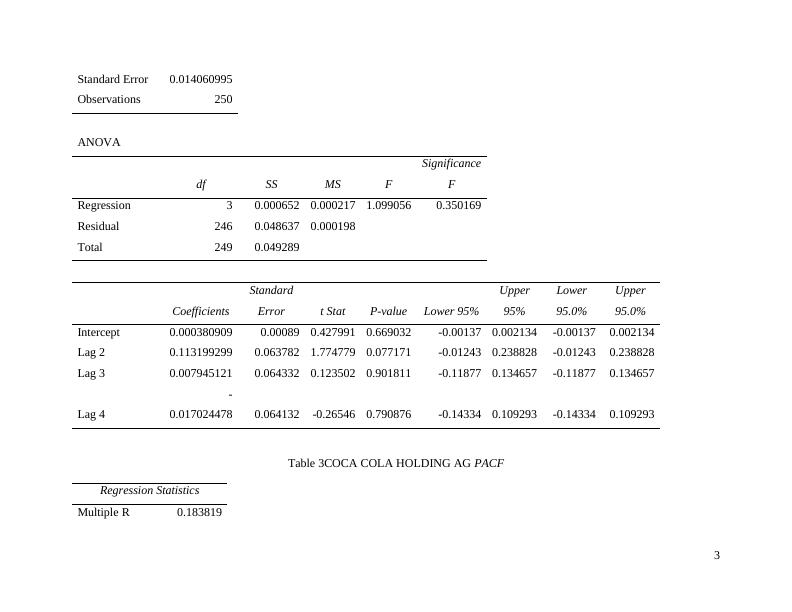

Table 3COCA COLA HOLDING AG PACF

Regression Statistics

Multiple R 0.183819

3

Observations 250

ANOVA

df SS MS F

Significance

F

Regression 3 0.000652 0.000217 1.099056 0.350169

Residual 246 0.048637 0.000198

Total 249 0.049289

Coefficients

Standard

Error t Stat P-value Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 0.000380909 0.00089 0.427991 0.669032 -0.00137 0.002134 -0.00137 0.002134

Lag 2 0.113199299 0.063782 1.774779 0.077171 -0.01243 0.238828 -0.01243 0.238828

Lag 3 0.007945121 0.064332 0.123502 0.901811 -0.11877 0.134657 -0.11877 0.134657

Lag 4

-

0.017024478 0.064132 -0.26546 0.790876 -0.14334 0.109293 -0.14334 0.109293

Table 3COCA COLA HOLDING AG PACF

Regression Statistics

Multiple R 0.183819

3

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Anova Assignment | Answerslg...

|22

|2126

|25

Regression Analysis of Relationship between Annual Income and Credit Card Chargeslg...

|7

|1017

|404

SEO Suggestions for Desklib Online Librarylg...

|4

|530

|447

Analysis of Click Sales Datalg...

|11

|1213

|79

Statistics - Desklib Online Library for Study Materiallg...

|8

|726

|67

Business Statisticslg...

|5

|454

|43