Project Planning and Budgeting: Financial Analysis and Cost Management

VerifiedAdded on 2021/06/14

|19

|4051

|91

Project

AI Summary

This project planning and budgeting assignment analyzes the financial aspects of the St. Dismas Assisted Living Facility, including a 20-year forecast of sales, cash flow, and profit and loss. It details the initial start-up costs for a 450-bed rehabilitation hospital, estimating costs between $8,500,000 and $11,000,000. The financial analysis reveals that the company incurs losses in the first two years, followed by linear profit growth. The assignment breaks down cost management planning, including fixed and average monthly costs, start-up expenses, and assets. Revenue projections are provided. The project also addresses quality management planning, emphasizing the cost of quality, including prevention, appraisal, and nonconformance costs, and utilizing tools like reducing balance depreciation and breakeven analysis to ensure the budget's feasibility.

Running head: PROJECT PLANNING AND BUDGETING

Project Planning and Budgeting

Name of Student:

Name of University:

Author’s Note:

Project Planning and Budgeting

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PROJECT PLANNING AND BUDGETING

Table of Contents

Cost Management Planning.............................................................................................................2

Quality Management Planning........................................................................................................5

References........................................................................................................................................8

List of Appendix..............................................................................................................................0

Table of Contents

Cost Management Planning.............................................................................................................2

Quality Management Planning........................................................................................................5

References........................................................................................................................................8

List of Appendix..............................................................................................................................0

2PROJECT PLANNING AND BUDGETING

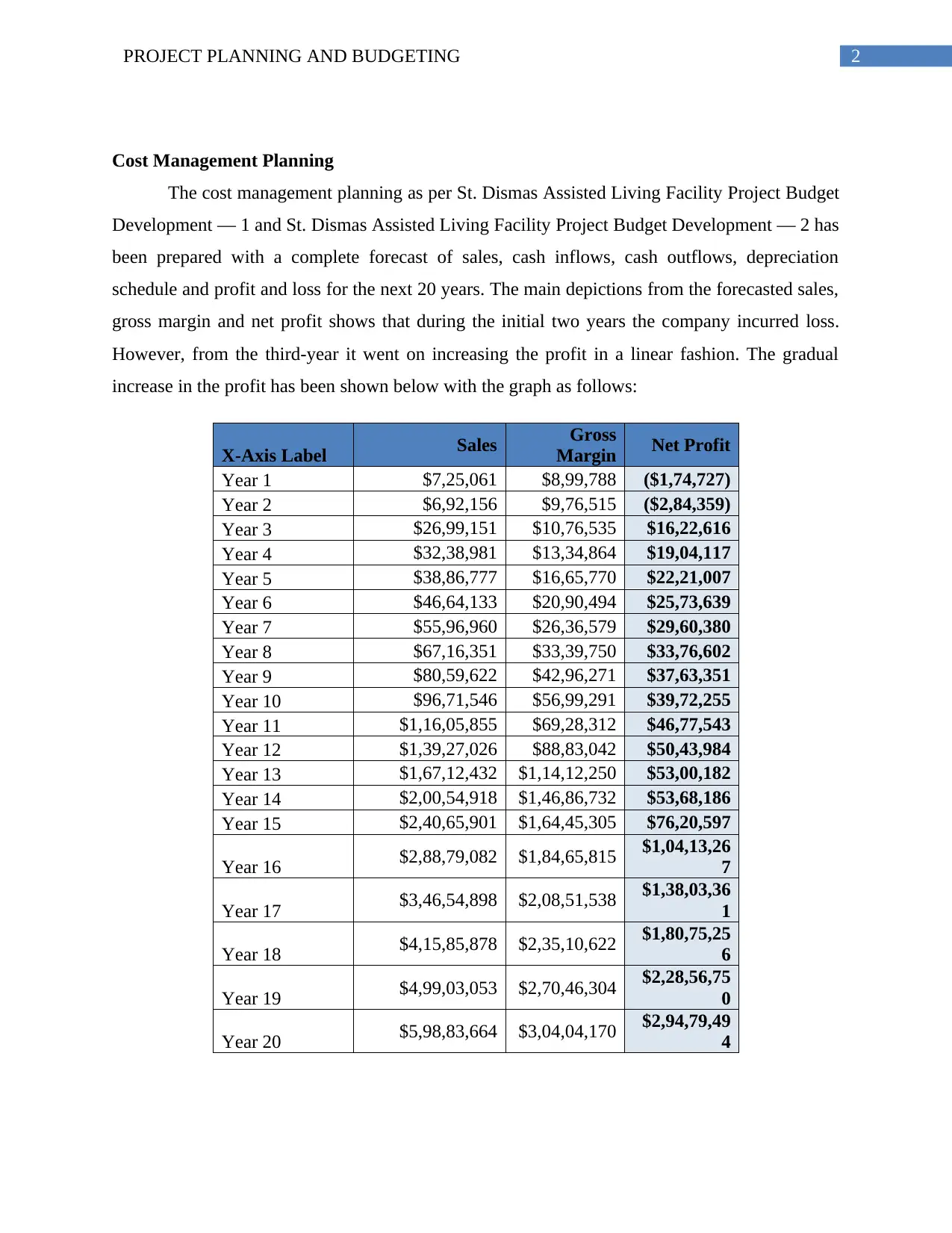

Cost Management Planning

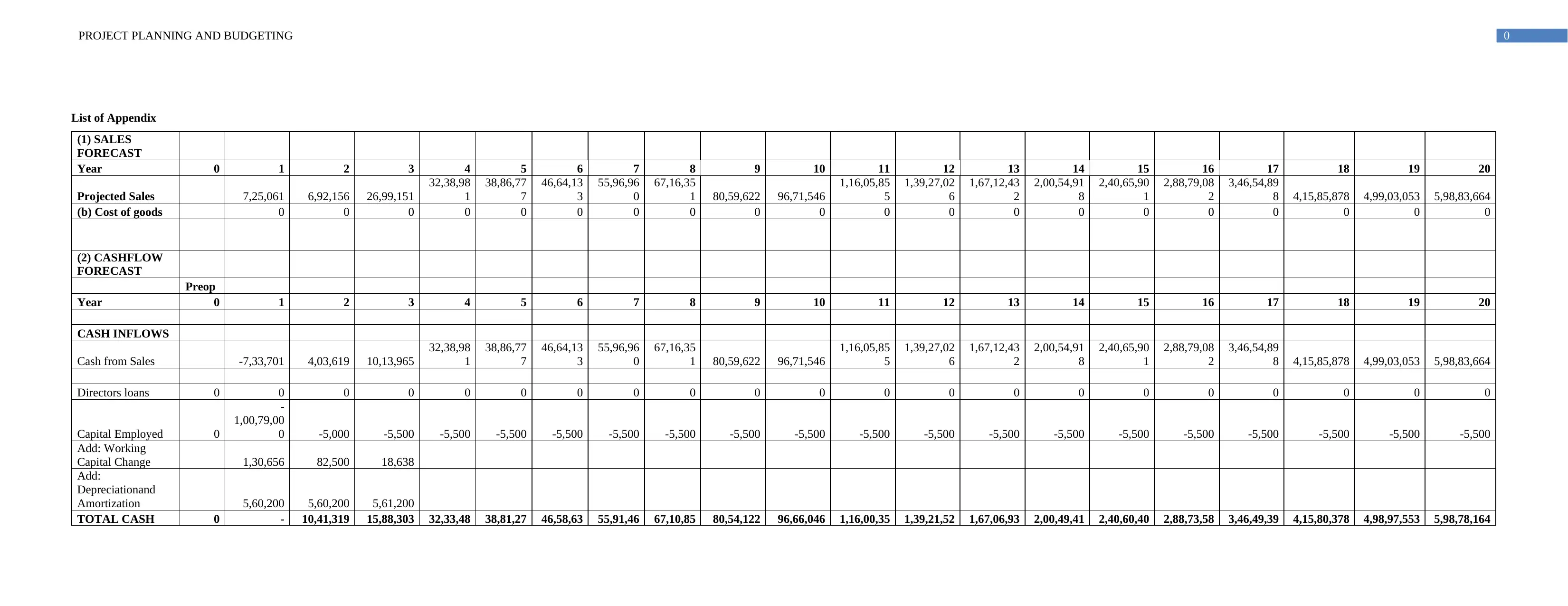

The cost management planning as per St. Dismas Assisted Living Facility Project Budget

Development — 1 and St. Dismas Assisted Living Facility Project Budget Development — 2 has

been prepared with a complete forecast of sales, cash inflows, cash outflows, depreciation

schedule and profit and loss for the next 20 years. The main depictions from the forecasted sales,

gross margin and net profit shows that during the initial two years the company incurred loss.

However, from the third-year it went on increasing the profit in a linear fashion. The gradual

increase in the profit has been shown below with the graph as follows:

X-Axis Label Sales Gross

Margin Net Profit

Year 1 $7,25,061 $8,99,788 ($1,74,727)

Year 2 $6,92,156 $9,76,515 ($2,84,359)

Year 3 $26,99,151 $10,76,535 $16,22,616

Year 4 $32,38,981 $13,34,864 $19,04,117

Year 5 $38,86,777 $16,65,770 $22,21,007

Year 6 $46,64,133 $20,90,494 $25,73,639

Year 7 $55,96,960 $26,36,579 $29,60,380

Year 8 $67,16,351 $33,39,750 $33,76,602

Year 9 $80,59,622 $42,96,271 $37,63,351

Year 10 $96,71,546 $56,99,291 $39,72,255

Year 11 $1,16,05,855 $69,28,312 $46,77,543

Year 12 $1,39,27,026 $88,83,042 $50,43,984

Year 13 $1,67,12,432 $1,14,12,250 $53,00,182

Year 14 $2,00,54,918 $1,46,86,732 $53,68,186

Year 15 $2,40,65,901 $1,64,45,305 $76,20,597

Year 16 $2,88,79,082 $1,84,65,815 $1,04,13,26

7

Year 17 $3,46,54,898 $2,08,51,538 $1,38,03,36

1

Year 18 $4,15,85,878 $2,35,10,622 $1,80,75,25

6

Year 19 $4,99,03,053 $2,70,46,304 $2,28,56,75

0

Year 20 $5,98,83,664 $3,04,04,170 $2,94,79,49

4

Cost Management Planning

The cost management planning as per St. Dismas Assisted Living Facility Project Budget

Development — 1 and St. Dismas Assisted Living Facility Project Budget Development — 2 has

been prepared with a complete forecast of sales, cash inflows, cash outflows, depreciation

schedule and profit and loss for the next 20 years. The main depictions from the forecasted sales,

gross margin and net profit shows that during the initial two years the company incurred loss.

However, from the third-year it went on increasing the profit in a linear fashion. The gradual

increase in the profit has been shown below with the graph as follows:

X-Axis Label Sales Gross

Margin Net Profit

Year 1 $7,25,061 $8,99,788 ($1,74,727)

Year 2 $6,92,156 $9,76,515 ($2,84,359)

Year 3 $26,99,151 $10,76,535 $16,22,616

Year 4 $32,38,981 $13,34,864 $19,04,117

Year 5 $38,86,777 $16,65,770 $22,21,007

Year 6 $46,64,133 $20,90,494 $25,73,639

Year 7 $55,96,960 $26,36,579 $29,60,380

Year 8 $67,16,351 $33,39,750 $33,76,602

Year 9 $80,59,622 $42,96,271 $37,63,351

Year 10 $96,71,546 $56,99,291 $39,72,255

Year 11 $1,16,05,855 $69,28,312 $46,77,543

Year 12 $1,39,27,026 $88,83,042 $50,43,984

Year 13 $1,67,12,432 $1,14,12,250 $53,00,182

Year 14 $2,00,54,918 $1,46,86,732 $53,68,186

Year 15 $2,40,65,901 $1,64,45,305 $76,20,597

Year 16 $2,88,79,082 $1,84,65,815 $1,04,13,26

7

Year 17 $3,46,54,898 $2,08,51,538 $1,38,03,36

1

Year 18 $4,15,85,878 $2,35,10,622 $1,80,75,25

6

Year 19 $4,99,03,053 $2,70,46,304 $2,28,56,75

0

Year 20 $5,98,83,664 $3,04,04,170 $2,94,79,49

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PROJECT PLANNING AND BUDGETING

Figure: Increasing net profit, gross profit and sales revenue over the next 20 years

(Source: As created by the author)

The initial start-up cost has considered 450 – bed rehabilitation hospital and the Manistee

mission has ensured that entire projects cost is between $8,500,000 and $11,000,000 for the

facility construction. The main depictions of the financial has been able to state that St. Dismas

Medical Center will be able to maintain a steady inflow of cash which is evident with $ -

1,01,21,845 in the first year, $ 10,41,319 in the second year, $ 15,88,303 in the third year, $

32,33,481 in the fourth year and so on. The estimation of total monthly cost is depicted to be $

376657. The company brick above the start of expenses has been listed below as follows:

Start-up Requirements

Start-up Expenses

Fixed Costs Particulars Amount ($)

Premises (RENT & RATES) $0

Salaries and Wages $3,76,657

Interest on loan 8% $0

Employee Benefits $82,865

Figure: Increasing net profit, gross profit and sales revenue over the next 20 years

(Source: As created by the author)

The initial start-up cost has considered 450 – bed rehabilitation hospital and the Manistee

mission has ensured that entire projects cost is between $8,500,000 and $11,000,000 for the

facility construction. The main depictions of the financial has been able to state that St. Dismas

Medical Center will be able to maintain a steady inflow of cash which is evident with $ -

1,01,21,845 in the first year, $ 10,41,319 in the second year, $ 15,88,303 in the third year, $

32,33,481 in the fourth year and so on. The estimation of total monthly cost is depicted to be $

376657. The company brick above the start of expenses has been listed below as follows:

Start-up Requirements

Start-up Expenses

Fixed Costs Particulars Amount ($)

Premises (RENT & RATES) $0

Salaries and Wages $3,76,657

Interest on loan 8% $0

Employee Benefits $82,865

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

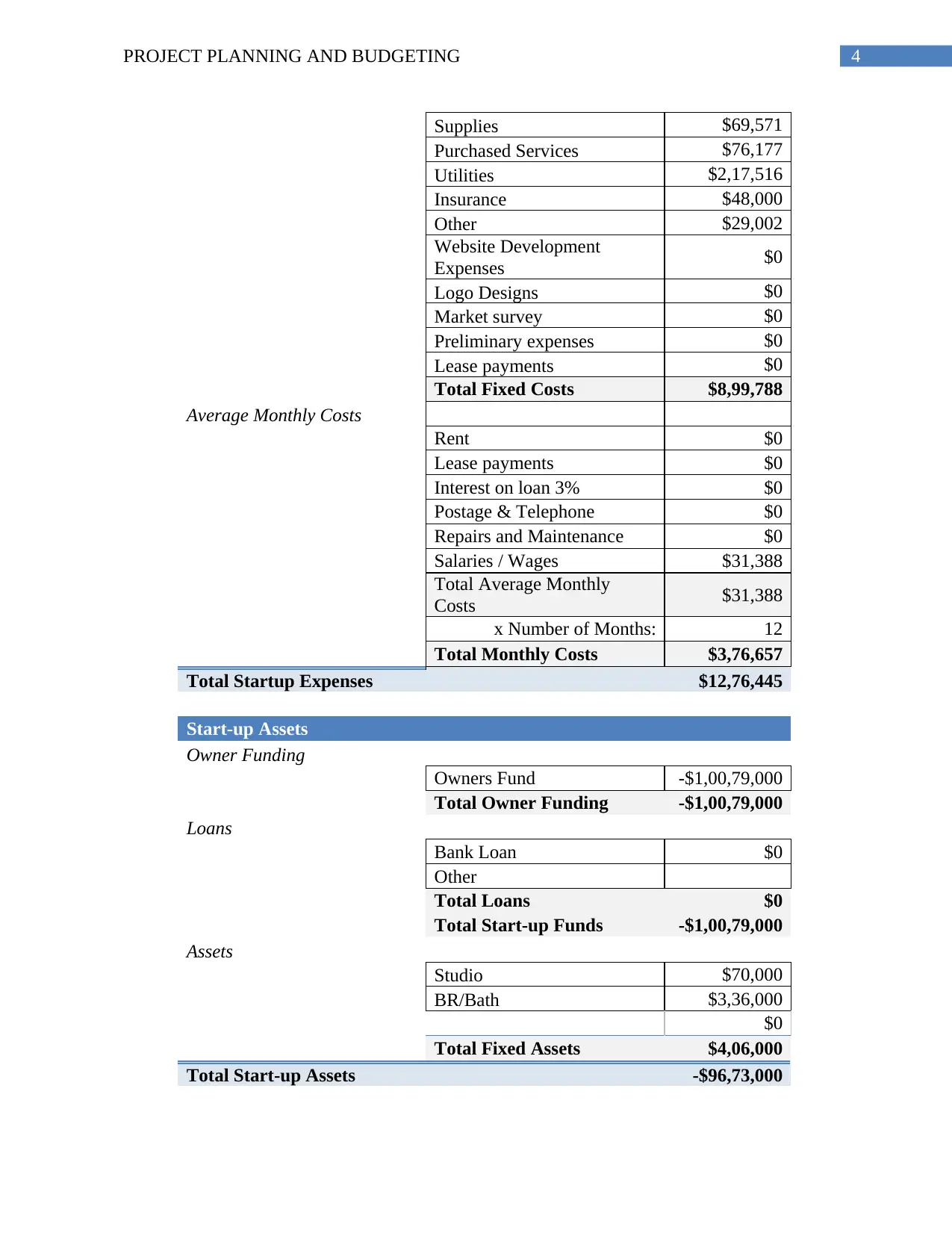

4PROJECT PLANNING AND BUDGETING

Supplies $69,571

Purchased Services $76,177

Utilities $2,17,516

Insurance $48,000

Other $29,002

Website Development

Expenses $0

Logo Designs $0

Market survey $0

Preliminary expenses $0

Lease payments $0

Total Fixed Costs $8,99,788

Average Monthly Costs

Rent $0

Lease payments $0

Interest on loan 3% $0

Postage & Telephone $0

Repairs and Maintenance $0

Salaries / Wages $31,388

Total Average Monthly

Costs $31,388

x Number of Months: 12

Total Monthly Costs $3,76,657

Total Startup Expenses $12,76,445

Start-up Assets

Owner Funding

Owners Fund -$1,00,79,000

Total Owner Funding -$1,00,79,000

Loans

Bank Loan $0

Other

Total Loans $0

Total Start-up Funds -$1,00,79,000

Assets

Studio $70,000

BR/Bath $3,36,000

$0

Total Fixed Assets $4,06,000

Total Start-up Assets -$96,73,000

Supplies $69,571

Purchased Services $76,177

Utilities $2,17,516

Insurance $48,000

Other $29,002

Website Development

Expenses $0

Logo Designs $0

Market survey $0

Preliminary expenses $0

Lease payments $0

Total Fixed Costs $8,99,788

Average Monthly Costs

Rent $0

Lease payments $0

Interest on loan 3% $0

Postage & Telephone $0

Repairs and Maintenance $0

Salaries / Wages $31,388

Total Average Monthly

Costs $31,388

x Number of Months: 12

Total Monthly Costs $3,76,657

Total Startup Expenses $12,76,445

Start-up Assets

Owner Funding

Owners Fund -$1,00,79,000

Total Owner Funding -$1,00,79,000

Loans

Bank Loan $0

Other

Total Loans $0

Total Start-up Funds -$1,00,79,000

Assets

Studio $70,000

BR/Bath $3,36,000

$0

Total Fixed Assets $4,06,000

Total Start-up Assets -$96,73,000

5PROJECT PLANNING AND BUDGETING

The company has identified the increasing nature of expenses in terms of salaries and

wages, employee benefits, supplies, purchase services and other expenses. In addition to this, the

fixed assets are considered with the studio and BR/Bath. Some of the main contributing items for

the cost management planning is depicted with increasing revenue in terms of service revenue

studios, one-bedroom, additional person revenue and ancillary revenue. Some of the important

highlights of the revenue earnings is seen with increasing revenue budget with $ 2,56,662 in the

first year, $ 4,14,012 in the second year, $ 4,30,572 in third year, $ 5,29,604 in the fourth year, $

6,51,412 in the fifth year and so on. The total service revenue of the company has shown massive

increase from the fourth year itself. The different nature of depictions made in the revenue

budget and expected budget has been conducive in addressing to the growing business as a result

of strategic objectives.

Quality Management Planning

The project has considered cost of quality having a vital role in the project quality

management. The prevention, detection and dealing with the defects is identified with main form

of quality initiative to achieve best costing principles. The conformation of the cost is the main

effort directed to keep the inaccurate cost constant fall into the category of revenue budget. In

order to ensure cost of conformance is sustained in the report, prevention cost and appraisal cost

has been considered to be the main factor by ensuring quality management (Renedo et al., 2015).

The prevention cost is included the activities which are seen to be specifically designed for

preventing poor quality of the services. In this case, the quality of services has been ensured with

better quality of service revenue studios, bedroom and additional rooms. This will ensure that St.

Dismas Assisted Living Facility is able to generate a sustained service revenue from its

operations. Henceforth, the prevention costs are considered with those activities whose main

intention is seen with reducing the total number of defects. Appraisal cost is another area of

quality aspect which has been able to ensure that the areas of faulty service is identified from

beforehand and before it reaches to the customer. Significantly better approach has been

identified with asking the employees about their own quality control approach and what do they

expect to get a desired service. The project has also considered the quality aspect with

consideration of nonconformance costs. These areas of costs take place as defects are produced

The company has identified the increasing nature of expenses in terms of salaries and

wages, employee benefits, supplies, purchase services and other expenses. In addition to this, the

fixed assets are considered with the studio and BR/Bath. Some of the main contributing items for

the cost management planning is depicted with increasing revenue in terms of service revenue

studios, one-bedroom, additional person revenue and ancillary revenue. Some of the important

highlights of the revenue earnings is seen with increasing revenue budget with $ 2,56,662 in the

first year, $ 4,14,012 in the second year, $ 4,30,572 in third year, $ 5,29,604 in the fourth year, $

6,51,412 in the fifth year and so on. The total service revenue of the company has shown massive

increase from the fourth year itself. The different nature of depictions made in the revenue

budget and expected budget has been conducive in addressing to the growing business as a result

of strategic objectives.

Quality Management Planning

The project has considered cost of quality having a vital role in the project quality

management. The prevention, detection and dealing with the defects is identified with main form

of quality initiative to achieve best costing principles. The conformation of the cost is the main

effort directed to keep the inaccurate cost constant fall into the category of revenue budget. In

order to ensure cost of conformance is sustained in the report, prevention cost and appraisal cost

has been considered to be the main factor by ensuring quality management (Renedo et al., 2015).

The prevention cost is included the activities which are seen to be specifically designed for

preventing poor quality of the services. In this case, the quality of services has been ensured with

better quality of service revenue studios, bedroom and additional rooms. This will ensure that St.

Dismas Assisted Living Facility is able to generate a sustained service revenue from its

operations. Henceforth, the prevention costs are considered with those activities whose main

intention is seen with reducing the total number of defects. Appraisal cost is another area of

quality aspect which has been able to ensure that the areas of faulty service is identified from

beforehand and before it reaches to the customer. Significantly better approach has been

identified with asking the employees about their own quality control approach and what do they

expect to get a desired service. The project has also considered the quality aspect with

consideration of nonconformance costs. These areas of costs take place as defects are produced

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PROJECT PLANNING AND BUDGETING

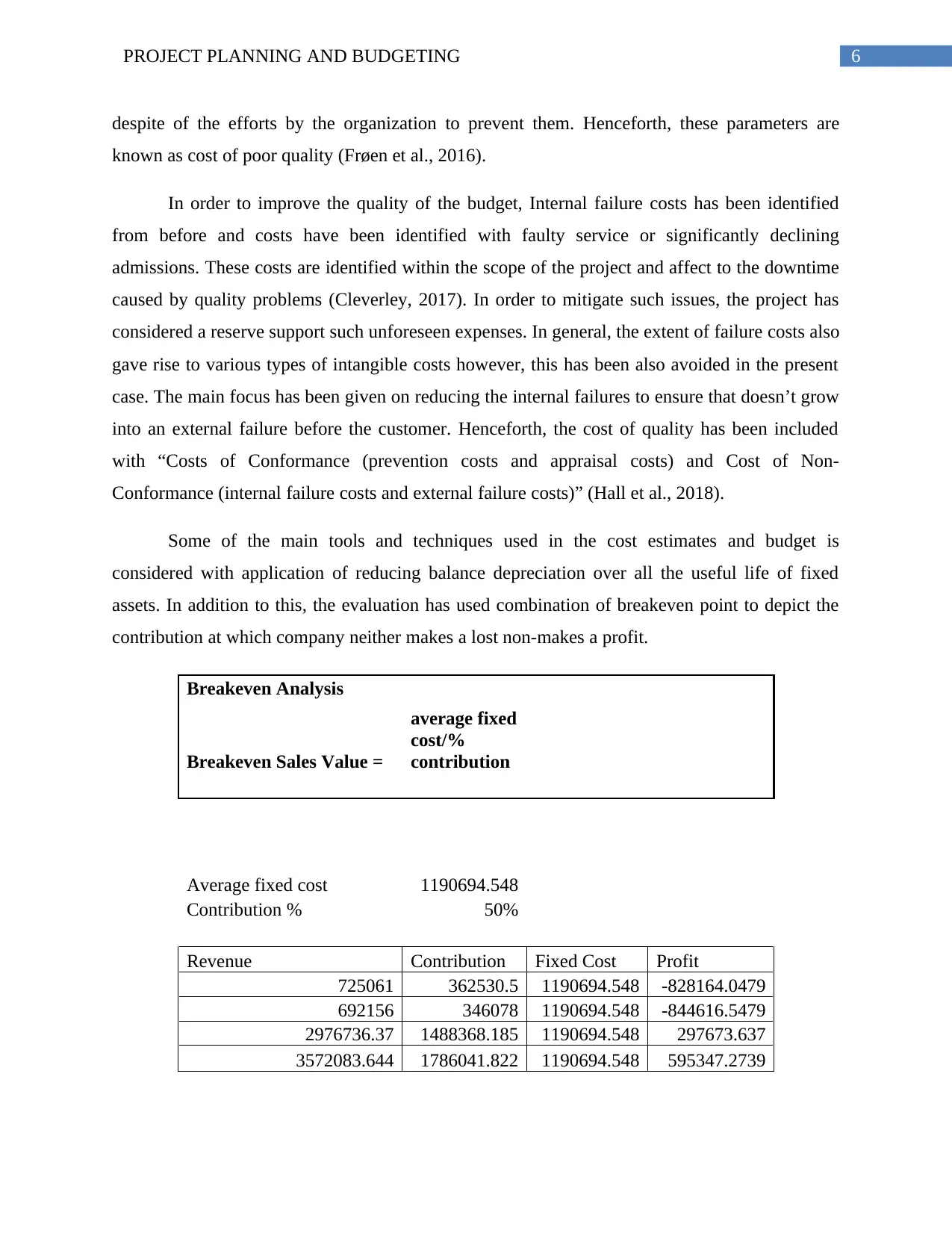

despite of the efforts by the organization to prevent them. Henceforth, these parameters are

known as cost of poor quality (Frøen et al., 2016).

In order to improve the quality of the budget, Internal failure costs has been identified

from before and costs have been identified with faulty service or significantly declining

admissions. These costs are identified within the scope of the project and affect to the downtime

caused by quality problems (Cleverley, 2017). In order to mitigate such issues, the project has

considered a reserve support such unforeseen expenses. In general, the extent of failure costs also

gave rise to various types of intangible costs however, this has been also avoided in the present

case. The main focus has been given on reducing the internal failures to ensure that doesn’t grow

into an external failure before the customer. Henceforth, the cost of quality has been included

with “Costs of Conformance (prevention costs and appraisal costs) and Cost of Non-

Conformance (internal failure costs and external failure costs)” (Hall et al., 2018).

Some of the main tools and techniques used in the cost estimates and budget is

considered with application of reducing balance depreciation over all the useful life of fixed

assets. In addition to this, the evaluation has used combination of breakeven point to depict the

contribution at which company neither makes a lost non-makes a profit.

Breakeven Analysis

Breakeven Sales Value =

average fixed

cost/%

contribution

Average fixed cost 1190694.548

Contribution % 50%

Revenue Contribution Fixed Cost Profit

725061 362530.5 1190694.548 -828164.0479

692156 346078 1190694.548 -844616.5479

2976736.37 1488368.185 1190694.548 297673.637

3572083.644 1786041.822 1190694.548 595347.2739

despite of the efforts by the organization to prevent them. Henceforth, these parameters are

known as cost of poor quality (Frøen et al., 2016).

In order to improve the quality of the budget, Internal failure costs has been identified

from before and costs have been identified with faulty service or significantly declining

admissions. These costs are identified within the scope of the project and affect to the downtime

caused by quality problems (Cleverley, 2017). In order to mitigate such issues, the project has

considered a reserve support such unforeseen expenses. In general, the extent of failure costs also

gave rise to various types of intangible costs however, this has been also avoided in the present

case. The main focus has been given on reducing the internal failures to ensure that doesn’t grow

into an external failure before the customer. Henceforth, the cost of quality has been included

with “Costs of Conformance (prevention costs and appraisal costs) and Cost of Non-

Conformance (internal failure costs and external failure costs)” (Hall et al., 2018).

Some of the main tools and techniques used in the cost estimates and budget is

considered with application of reducing balance depreciation over all the useful life of fixed

assets. In addition to this, the evaluation has used combination of breakeven point to depict the

contribution at which company neither makes a lost non-makes a profit.

Breakeven Analysis

Breakeven Sales Value =

average fixed

cost/%

contribution

Average fixed cost 1190694.548

Contribution % 50%

Revenue Contribution Fixed Cost Profit

725061 362530.5 1190694.548 -828164.0479

692156 346078 1190694.548 -844616.5479

2976736.37 1488368.185 1190694.548 297673.637

3572083.644 1786041.822 1190694.548 595347.2739

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PROJECT PLANNING AND BUDGETING

Some of the other application of quality management tools in the report has been evident

with using bar graphs to show the overall increase in revenue, gross margin and net profit. The

feasibility of the budget plan is evident with increasing nature of sales and net profit over a

timeline of 20 years. This is the main rationale for proceeding with the present financial plan

(White et al., 2016).

Some of the other application of quality management tools in the report has been evident

with using bar graphs to show the overall increase in revenue, gross margin and net profit. The

feasibility of the budget plan is evident with increasing nature of sales and net profit over a

timeline of 20 years. This is the main rationale for proceeding with the present financial plan

(White et al., 2016).

8PROJECT PLANNING AND BUDGETING

References

Cleverley, W. O. (2017). Essentials of health care finance. Jones & Bartlett Learning.

Frøen, J. F., Friberg, I. K., Lawn, J. E., Bhutta, Z. A., Pattinson, R. C., Allanson, E. R., ... &

Kinney, M. V. (2016). Stillbirths: progress and unfinished business. The

Lancet, 387(10018), 574-586.

Hall, M. A., Orentlicher, D., Bobinski, M. A., Bagley, N., & Cohen, I. G. (2018). Health care

law and ethics. Wolters Kluwer Law & Business.

Renedo, A., Marston, C. A., Spyridonidis, D., & Barlow, J. (2015). Patient and Public

Involvement in Healthcare Quality Improvement: How organizations can help patients

and professionals to collaborate. Public Management Review, 17(1), 17-34.

White, K. M., Dudley-Brown, S., & Terhaar, M. F. (Eds.). (2016). Translation of evidence into

nursing and health care. Springer Publishing Company.

References

Cleverley, W. O. (2017). Essentials of health care finance. Jones & Bartlett Learning.

Frøen, J. F., Friberg, I. K., Lawn, J. E., Bhutta, Z. A., Pattinson, R. C., Allanson, E. R., ... &

Kinney, M. V. (2016). Stillbirths: progress and unfinished business. The

Lancet, 387(10018), 574-586.

Hall, M. A., Orentlicher, D., Bobinski, M. A., Bagley, N., & Cohen, I. G. (2018). Health care

law and ethics. Wolters Kluwer Law & Business.

Renedo, A., Marston, C. A., Spyridonidis, D., & Barlow, J. (2015). Patient and Public

Involvement in Healthcare Quality Improvement: How organizations can help patients

and professionals to collaborate. Public Management Review, 17(1), 17-34.

White, K. M., Dudley-Brown, S., & Terhaar, M. F. (Eds.). (2016). Translation of evidence into

nursing and health care. Springer Publishing Company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0PROJECT PLANNING AND BUDGETING

List of Appendix

(1) SALES

FORECAST

Year 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Projected Sales 7,25,061 6,92,156 26,99,151

32,38,98

1

38,86,77

7

46,64,13

3

55,96,96

0

67,16,35

1 80,59,622 96,71,546

1,16,05,85

5

1,39,27,02

6

1,67,12,43

2

2,00,54,91

8

2,40,65,90

1

2,88,79,08

2

3,46,54,89

8 4,15,85,878 4,99,03,053 5,98,83,664

(b) Cost of goods 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

(2) CASHFLOW

FORECAST

Preop

Year 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

CASH INFLOWS

Cash from Sales -7,33,701 4,03,619 10,13,965

32,38,98

1

38,86,77

7

46,64,13

3

55,96,96

0

67,16,35

1 80,59,622 96,71,546

1,16,05,85

5

1,39,27,02

6

1,67,12,43

2

2,00,54,91

8

2,40,65,90

1

2,88,79,08

2

3,46,54,89

8 4,15,85,878 4,99,03,053 5,98,83,664

Directors loans 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Capital Employed 0

-

1,00,79,00

0 -5,000 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500

Add: Working

Capital Change 1,30,656 82,500 18,638

Add:

Depreciationand

Amortization 5,60,200 5,60,200 5,61,200

TOTAL CASH 0 - 10,41,319 15,88,303 32,33,48 38,81,27 46,58,63 55,91,46 67,10,85 80,54,122 96,66,046 1,16,00,35 1,39,21,52 1,67,06,93 2,00,49,41 2,40,60,40 2,88,73,58 3,46,49,39 4,15,80,378 4,98,97,553 5,98,78,164

List of Appendix

(1) SALES

FORECAST

Year 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Projected Sales 7,25,061 6,92,156 26,99,151

32,38,98

1

38,86,77

7

46,64,13

3

55,96,96

0

67,16,35

1 80,59,622 96,71,546

1,16,05,85

5

1,39,27,02

6

1,67,12,43

2

2,00,54,91

8

2,40,65,90

1

2,88,79,08

2

3,46,54,89

8 4,15,85,878 4,99,03,053 5,98,83,664

(b) Cost of goods 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

(2) CASHFLOW

FORECAST

Preop

Year 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

CASH INFLOWS

Cash from Sales -7,33,701 4,03,619 10,13,965

32,38,98

1

38,86,77

7

46,64,13

3

55,96,96

0

67,16,35

1 80,59,622 96,71,546

1,16,05,85

5

1,39,27,02

6

1,67,12,43

2

2,00,54,91

8

2,40,65,90

1

2,88,79,08

2

3,46,54,89

8 4,15,85,878 4,99,03,053 5,98,83,664

Directors loans 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Capital Employed 0

-

1,00,79,00

0 -5,000 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500 -5,500

Add: Working

Capital Change 1,30,656 82,500 18,638

Add:

Depreciationand

Amortization 5,60,200 5,60,200 5,61,200

TOTAL CASH 0 - 10,41,319 15,88,303 32,33,48 38,81,27 46,58,63 55,91,46 67,10,85 80,54,122 96,66,046 1,16,00,35 1,39,21,52 1,67,06,93 2,00,49,41 2,40,60,40 2,88,73,58 3,46,49,39 4,15,80,378 4,98,97,553 5,98,78,164

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PROJECT PLANNING AND BUDGETING

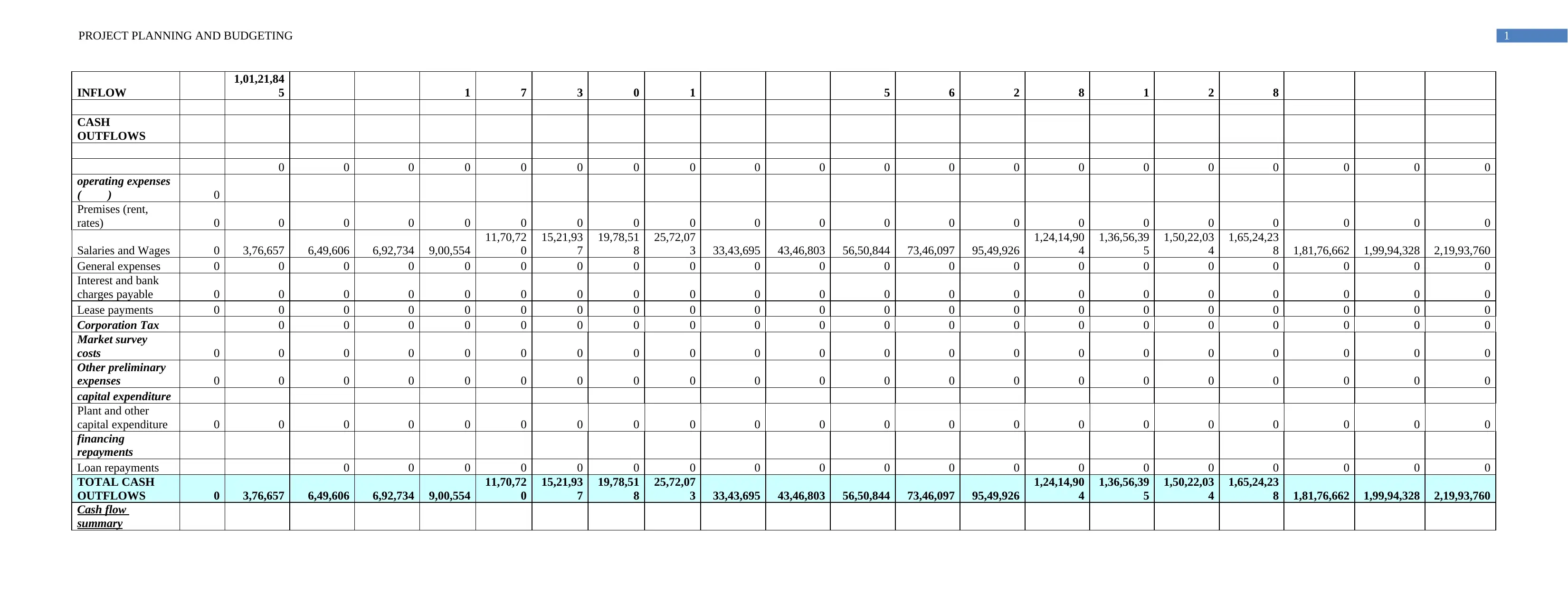

INFLOW

1,01,21,84

5 1 7 3 0 1 5 6 2 8 1 2 8

CASH

OUTFLOWS

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

operating expenses

( ) 0

Premises (rent,

rates) 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Salaries and Wages 0 3,76,657 6,49,606 6,92,734 9,00,554

11,70,72

0

15,21,93

7

19,78,51

8

25,72,07

3 33,43,695 43,46,803 56,50,844 73,46,097 95,49,926

1,24,14,90

4

1,36,56,39

5

1,50,22,03

4

1,65,24,23

8 1,81,76,662 1,99,94,328 2,19,93,760

General expenses 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Interest and bank

charges payable 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Lease payments 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Corporation Tax 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Market survey

costs 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Other preliminary

expenses 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

capital expenditure

Plant and other

capital expenditure 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

financing

repayments

Loan repayments 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

TOTAL CASH

OUTFLOWS 0 3,76,657 6,49,606 6,92,734 9,00,554

11,70,72

0

15,21,93

7

19,78,51

8

25,72,07

3 33,43,695 43,46,803 56,50,844 73,46,097 95,49,926

1,24,14,90

4

1,36,56,39

5

1,50,22,03

4

1,65,24,23

8 1,81,76,662 1,99,94,328 2,19,93,760

Cash flow

summary

INFLOW

1,01,21,84

5 1 7 3 0 1 5 6 2 8 1 2 8

CASH

OUTFLOWS

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

operating expenses

( ) 0

Premises (rent,

rates) 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Salaries and Wages 0 3,76,657 6,49,606 6,92,734 9,00,554

11,70,72

0

15,21,93

7

19,78,51

8

25,72,07

3 33,43,695 43,46,803 56,50,844 73,46,097 95,49,926

1,24,14,90

4

1,36,56,39

5

1,50,22,03

4

1,65,24,23

8 1,81,76,662 1,99,94,328 2,19,93,760

General expenses 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Interest and bank

charges payable 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Lease payments 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Corporation Tax 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Market survey

costs 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Other preliminary

expenses 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

capital expenditure

Plant and other

capital expenditure 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

financing

repayments

Loan repayments 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

TOTAL CASH

OUTFLOWS 0 3,76,657 6,49,606 6,92,734 9,00,554

11,70,72

0

15,21,93

7

19,78,51

8

25,72,07

3 33,43,695 43,46,803 56,50,844 73,46,097 95,49,926

1,24,14,90

4

1,36,56,39

5

1,50,22,03

4

1,65,24,23

8 1,81,76,662 1,99,94,328 2,19,93,760

Cash flow

summary

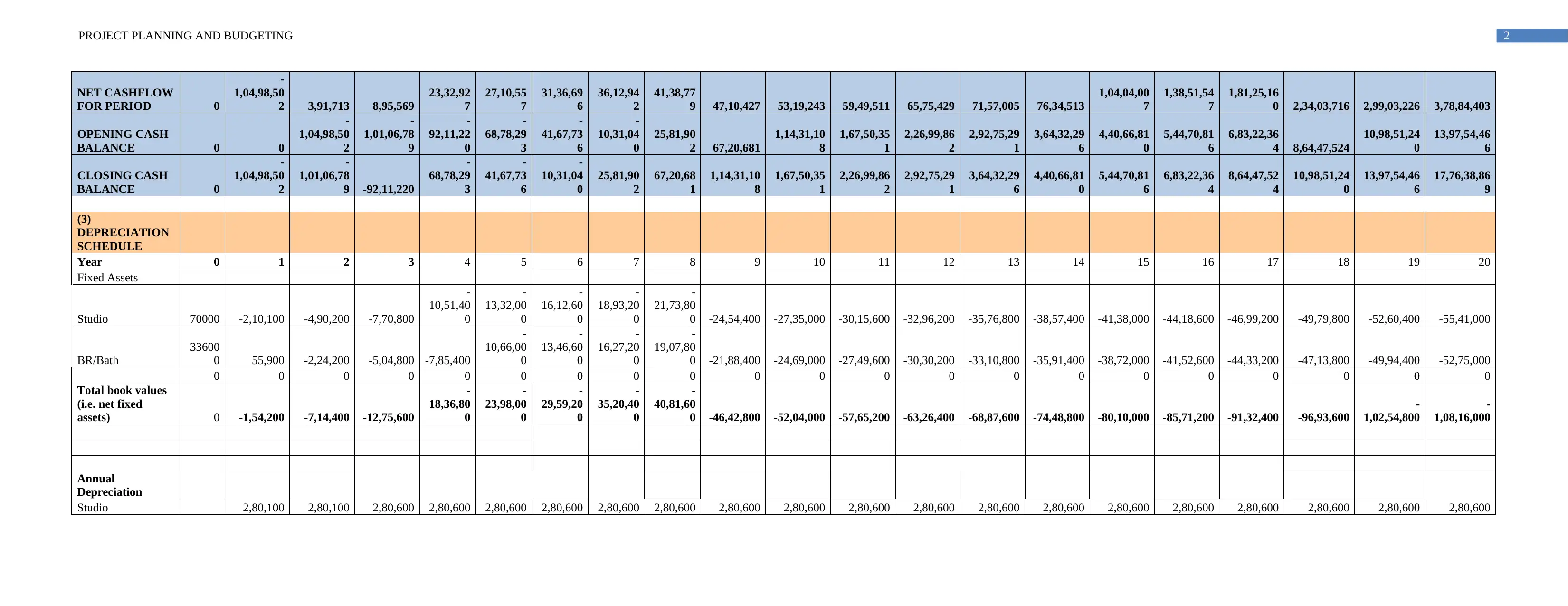

2PROJECT PLANNING AND BUDGETING

NET CASHFLOW

FOR PERIOD 0

-

1,04,98,50

2 3,91,713 8,95,569

23,32,92

7

27,10,55

7

31,36,69

6

36,12,94

2

41,38,77

9 47,10,427 53,19,243 59,49,511 65,75,429 71,57,005 76,34,513

1,04,04,00

7

1,38,51,54

7

1,81,25,16

0 2,34,03,716 2,99,03,226 3,78,84,403

OPENING CASH

BALANCE 0 0

-

1,04,98,50

2

-

1,01,06,78

9

-

92,11,22

0

-

68,78,29

3

-

41,67,73

6

-

10,31,04

0

25,81,90

2 67,20,681

1,14,31,10

8

1,67,50,35

1

2,26,99,86

2

2,92,75,29

1

3,64,32,29

6

4,40,66,81

0

5,44,70,81

6

6,83,22,36

4 8,64,47,524

10,98,51,24

0

13,97,54,46

6

CLOSING CASH

BALANCE 0

-

1,04,98,50

2

-

1,01,06,78

9 -92,11,220

-

68,78,29

3

-

41,67,73

6

-

10,31,04

0

25,81,90

2

67,20,68

1

1,14,31,10

8

1,67,50,35

1

2,26,99,86

2

2,92,75,29

1

3,64,32,29

6

4,40,66,81

0

5,44,70,81

6

6,83,22,36

4

8,64,47,52

4

10,98,51,24

0

13,97,54,46

6

17,76,38,86

9

(3)

DEPRECIATION

SCHEDULE

Year 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Fixed Assets

Studio 70000 -2,10,100 -4,90,200 -7,70,800

-

10,51,40

0

-

13,32,00

0

-

16,12,60

0

-

18,93,20

0

-

21,73,80

0 -24,54,400 -27,35,000 -30,15,600 -32,96,200 -35,76,800 -38,57,400 -41,38,000 -44,18,600 -46,99,200 -49,79,800 -52,60,400 -55,41,000

BR/Bath

33600

0 55,900 -2,24,200 -5,04,800 -7,85,400

-

10,66,00

0

-

13,46,60

0

-

16,27,20

0

-

19,07,80

0 -21,88,400 -24,69,000 -27,49,600 -30,30,200 -33,10,800 -35,91,400 -38,72,000 -41,52,600 -44,33,200 -47,13,800 -49,94,400 -52,75,000

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Total book values

(i.e. net fixed

assets) 0 -1,54,200 -7,14,400 -12,75,600

-

18,36,80

0

-

23,98,00

0

-

29,59,20

0

-

35,20,40

0

-

40,81,60

0 -46,42,800 -52,04,000 -57,65,200 -63,26,400 -68,87,600 -74,48,800 -80,10,000 -85,71,200 -91,32,400 -96,93,600

-

1,02,54,800

-

1,08,16,000

Annual

Depreciation

Studio 2,80,100 2,80,100 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600

NET CASHFLOW

FOR PERIOD 0

-

1,04,98,50

2 3,91,713 8,95,569

23,32,92

7

27,10,55

7

31,36,69

6

36,12,94

2

41,38,77

9 47,10,427 53,19,243 59,49,511 65,75,429 71,57,005 76,34,513

1,04,04,00

7

1,38,51,54

7

1,81,25,16

0 2,34,03,716 2,99,03,226 3,78,84,403

OPENING CASH

BALANCE 0 0

-

1,04,98,50

2

-

1,01,06,78

9

-

92,11,22

0

-

68,78,29

3

-

41,67,73

6

-

10,31,04

0

25,81,90

2 67,20,681

1,14,31,10

8

1,67,50,35

1

2,26,99,86

2

2,92,75,29

1

3,64,32,29

6

4,40,66,81

0

5,44,70,81

6

6,83,22,36

4 8,64,47,524

10,98,51,24

0

13,97,54,46

6

CLOSING CASH

BALANCE 0

-

1,04,98,50

2

-

1,01,06,78

9 -92,11,220

-

68,78,29

3

-

41,67,73

6

-

10,31,04

0

25,81,90

2

67,20,68

1

1,14,31,10

8

1,67,50,35

1

2,26,99,86

2

2,92,75,29

1

3,64,32,29

6

4,40,66,81

0

5,44,70,81

6

6,83,22,36

4

8,64,47,52

4

10,98,51,24

0

13,97,54,46

6

17,76,38,86

9

(3)

DEPRECIATION

SCHEDULE

Year 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Fixed Assets

Studio 70000 -2,10,100 -4,90,200 -7,70,800

-

10,51,40

0

-

13,32,00

0

-

16,12,60

0

-

18,93,20

0

-

21,73,80

0 -24,54,400 -27,35,000 -30,15,600 -32,96,200 -35,76,800 -38,57,400 -41,38,000 -44,18,600 -46,99,200 -49,79,800 -52,60,400 -55,41,000

BR/Bath

33600

0 55,900 -2,24,200 -5,04,800 -7,85,400

-

10,66,00

0

-

13,46,60

0

-

16,27,20

0

-

19,07,80

0 -21,88,400 -24,69,000 -27,49,600 -30,30,200 -33,10,800 -35,91,400 -38,72,000 -41,52,600 -44,33,200 -47,13,800 -49,94,400 -52,75,000

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Total book values

(i.e. net fixed

assets) 0 -1,54,200 -7,14,400 -12,75,600

-

18,36,80

0

-

23,98,00

0

-

29,59,20

0

-

35,20,40

0

-

40,81,60

0 -46,42,800 -52,04,000 -57,65,200 -63,26,400 -68,87,600 -74,48,800 -80,10,000 -85,71,200 -91,32,400 -96,93,600

-

1,02,54,800

-

1,08,16,000

Annual

Depreciation

Studio 2,80,100 2,80,100 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600 2,80,600

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.