Financial Analysis Project

VerifiedAdded on 2020/04/07

|14

|3286

|61

AI Summary

This assignment delves into the analysis of a financial project. It requires students to calculate key metrics such as the payback period and Accounting Rate of Return (ARR) using present value calculations at a 12% discount rate. The assignment provides step-by-step solutions for cash flow projections, ARR calculation, and payback period determination. It also includes a detailed explanation of the project's financial feasibility based on these calculated metrics.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting for business

1

Project Report: Accounting for business

1

Project Report: Accounting for business

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting for business

2

Executive summary

This description has been equipped to investigate 2 investment proposals. In this

paper, restaurant and new machineries, both investments have been analyzed. For it, various

techniques have been investigated according to the investment proposals. This report

expresses the reader about the diverse techniques that could be used to examine both the

investment proposal of the company. In this report paper, various aspects such as purpose of

the investment and the report, scope of the investment and the report, limitations etc have

been analyzed. Further, scope of investment and nature of investments also have been

examined. Further, investment opportunity of restaurant and new machineries has been

analyzed. Lastly, both the investment has been compared to find the better proposals of the

investment.

2

Executive summary

This description has been equipped to investigate 2 investment proposals. In this

paper, restaurant and new machineries, both investments have been analyzed. For it, various

techniques have been investigated according to the investment proposals. This report

expresses the reader about the diverse techniques that could be used to examine both the

investment proposal of the company. In this report paper, various aspects such as purpose of

the investment and the report, scope of the investment and the report, limitations etc have

been analyzed. Further, scope of investment and nature of investments also have been

examined. Further, investment opportunity of restaurant and new machineries has been

analyzed. Lastly, both the investment has been compared to find the better proposals of the

investment.

Accounting for business

3

Introduction:

The specified case study represent that 2 investment suggestions have been accessible

by the marketing student, Mark and Paul. They have briefed both the orders in front of many

people to make some investment into the opportunities and improve the value of invested

money. In this case study paper, different methods and equipment have been contested to

investigate and compare the best investment proposal into given proposals by the Mark and

Paul. Capital budgeting techniques and tools have been used in this report to analyze the first

investment proposal and budgeting techniques and tools have been used in this report for the

second proposal proposed by Mark and Paul (Garrison et al, 2010). This case study depict

that, the major aphorism of this report paper is to examine the best venture opportunity which

would present the people who has invested their amount, more return and the suggestion of

the asset would be striking for the people. More, various limitations and scopes are situated

of both the investment with the nature of the investment. Through this report, it has been

found that the opportunities and the nature of the business are more striking and these

opportunities make it a profitable deal for the investors as the investment would be higher.

Nature and scope of investment:

Investments are the amount which is proposed by an individual, government or a firm

into some financial securities or business proposals from their savings to encourage the value

of the savings amount. The investment is a back bone of every organization. If an

organization do not get any investment from the market then it becomes quite tough for the

organization to run the business (Brewer, Garrison and Noreen, 2005). The nature of the

investment is viable in nature and at the same time, the scope of investment is quite wider.

The investment opportunity must be analyzed by the investor before investing the amount in

that so that a better result could be got.

First Investment opportunity:

Mark and Paul, the marketing student of a university has proposed two investment

opportunity to invest and enhance the value of the money. First opportunity offered by them

is the investment into a new business, restaurant. In the case study, various revenues and

expenditure have been described by them which are required to start the business. Through

the case study, it has been found that the return from this technique could be investigated

3

Introduction:

The specified case study represent that 2 investment suggestions have been accessible

by the marketing student, Mark and Paul. They have briefed both the orders in front of many

people to make some investment into the opportunities and improve the value of invested

money. In this case study paper, different methods and equipment have been contested to

investigate and compare the best investment proposal into given proposals by the Mark and

Paul. Capital budgeting techniques and tools have been used in this report to analyze the first

investment proposal and budgeting techniques and tools have been used in this report for the

second proposal proposed by Mark and Paul (Garrison et al, 2010). This case study depict

that, the major aphorism of this report paper is to examine the best venture opportunity which

would present the people who has invested their amount, more return and the suggestion of

the asset would be striking for the people. More, various limitations and scopes are situated

of both the investment with the nature of the investment. Through this report, it has been

found that the opportunities and the nature of the business are more striking and these

opportunities make it a profitable deal for the investors as the investment would be higher.

Nature and scope of investment:

Investments are the amount which is proposed by an individual, government or a firm

into some financial securities or business proposals from their savings to encourage the value

of the savings amount. The investment is a back bone of every organization. If an

organization do not get any investment from the market then it becomes quite tough for the

organization to run the business (Brewer, Garrison and Noreen, 2005). The nature of the

investment is viable in nature and at the same time, the scope of investment is quite wider.

The investment opportunity must be analyzed by the investor before investing the amount in

that so that a better result could be got.

First Investment opportunity:

Mark and Paul, the marketing student of a university has proposed two investment

opportunity to invest and enhance the value of the money. First opportunity offered by them

is the investment into a new business, restaurant. In the case study, various revenues and

expenditure have been described by them which are required to start the business. Through

the case study, it has been found that the return from this technique could be investigated

Accounting for business

4

through the technique of budgeting report. Following are the details which have been given

by the Mark and Paul for this investment is:

Restaurant Purchase and Expenses

Machinery/ equipment $ 1,10,000

Furniture (tables and chairs) $ 30,000

Vehicle (Deliveries) $ 43,000

Utensils (cups, plates) $ 18,000

Produce (for 1 week) $ 10,000

Drinks (For 1 month) $ 20,000

Jun-01 Bank $ 80,000

Purchase of $10,000 for a week from June 1 and the amount of purchase

would be given to suppliers from 1 august.

Purchase of $ 20,000 for 1 month from July-1 and the amount

of purchase would be given to suppliers periodically which is as

follows:

10% in current month

45% in second month

45% in third month

Labour

Number of casual labour 3

Working in a day (hours) 6 hours

In a week (days) 6 days

Rate

$ 23 per

hour

Drawings

$ 10000 each per

month

Overhead $ 5,000

Sales

20000 meals in first month

18000 meals in second month

18000 meals in third month

22000 in forth month

Average selling price $ 45

4

through the technique of budgeting report. Following are the details which have been given

by the Mark and Paul for this investment is:

Restaurant Purchase and Expenses

Machinery/ equipment $ 1,10,000

Furniture (tables and chairs) $ 30,000

Vehicle (Deliveries) $ 43,000

Utensils (cups, plates) $ 18,000

Produce (for 1 week) $ 10,000

Drinks (For 1 month) $ 20,000

Jun-01 Bank $ 80,000

Purchase of $10,000 for a week from June 1 and the amount of purchase

would be given to suppliers from 1 august.

Purchase of $ 20,000 for 1 month from July-1 and the amount

of purchase would be given to suppliers periodically which is as

follows:

10% in current month

45% in second month

45% in third month

Labour

Number of casual labour 3

Working in a day (hours) 6 hours

In a week (days) 6 days

Rate

$ 23 per

hour

Drawings

$ 10000 each per

month

Overhead $ 5,000

Sales

20000 meals in first month

18000 meals in second month

18000 meals in third month

22000 in forth month

Average selling price $ 45

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting for business

5

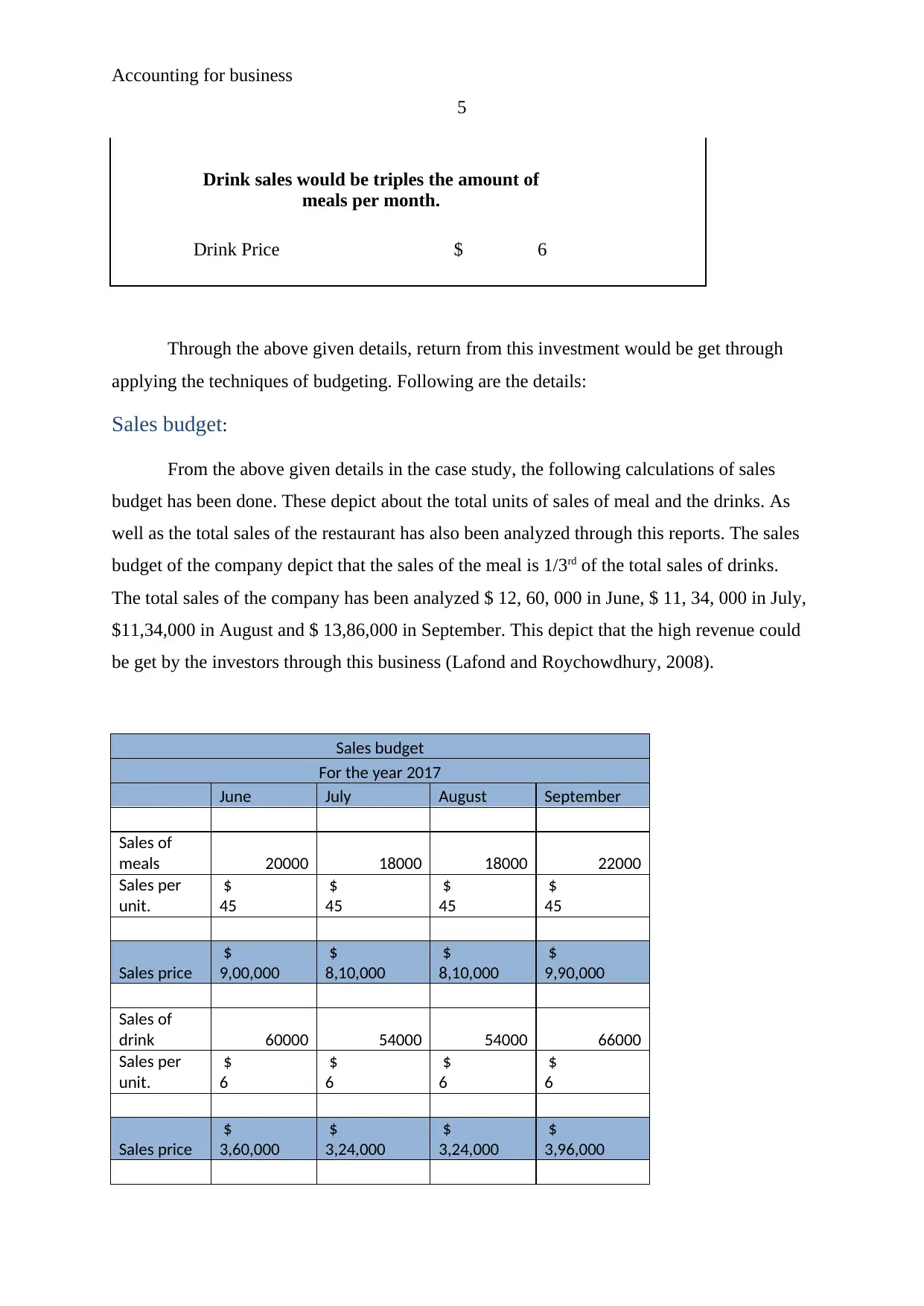

Drink sales would be triples the amount of

meals per month.

Drink Price $ 6

Through the above given details, return from this investment would be get through

applying the techniques of budgeting. Following are the details:

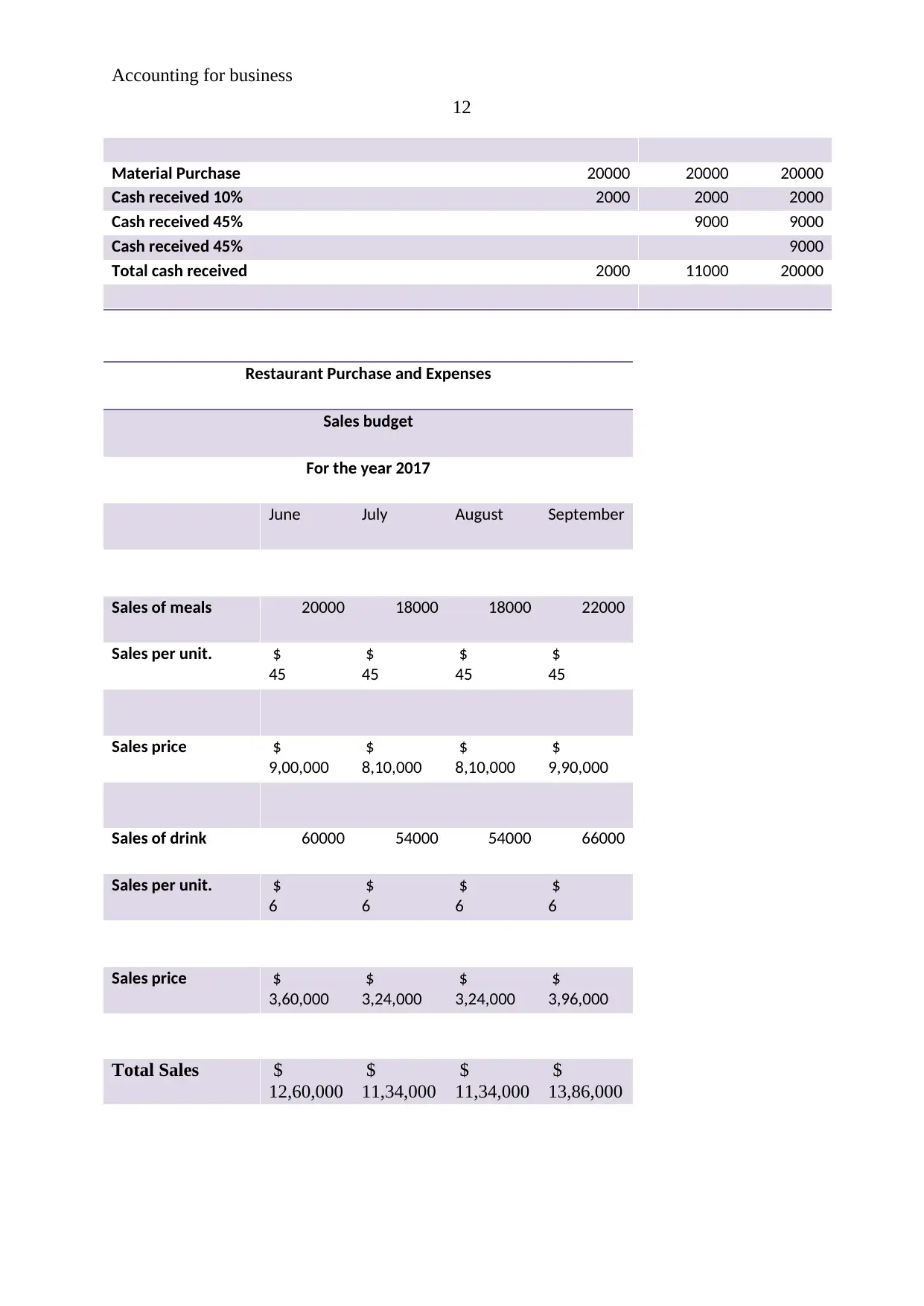

Sales budget:

From the above given details in the case study, the following calculations of sales

budget has been done. These depict about the total units of sales of meal and the drinks. As

well as the total sales of the restaurant has also been analyzed through this reports. The sales

budget of the company depict that the sales of the meal is 1/3rd of the total sales of drinks.

The total sales of the company has been analyzed $ 12, 60, 000 in June, $ 11, 34, 000 in July,

$11,34,000 in August and $ 13,86,000 in September. This depict that the high revenue could

be get by the investors through this business (Lafond and Roychowdhury, 2008).

Sales budget

For the year 2017

June July August September

Sales of

meals 20000 18000 18000 22000

Sales per

unit.

$

45

$

45

$

45

$

45

Sales price

$

9,00,000

$

8,10,000

$

8,10,000

$

9,90,000

Sales of

drink 60000 54000 54000 66000

Sales per

unit.

$

6

$

6

$

6

$

6

Sales price

$

3,60,000

$

3,24,000

$

3,24,000

$

3,96,000

5

Drink sales would be triples the amount of

meals per month.

Drink Price $ 6

Through the above given details, return from this investment would be get through

applying the techniques of budgeting. Following are the details:

Sales budget:

From the above given details in the case study, the following calculations of sales

budget has been done. These depict about the total units of sales of meal and the drinks. As

well as the total sales of the restaurant has also been analyzed through this reports. The sales

budget of the company depict that the sales of the meal is 1/3rd of the total sales of drinks.

The total sales of the company has been analyzed $ 12, 60, 000 in June, $ 11, 34, 000 in July,

$11,34,000 in August and $ 13,86,000 in September. This depict that the high revenue could

be get by the investors through this business (Lafond and Roychowdhury, 2008).

Sales budget

For the year 2017

June July August September

Sales of

meals 20000 18000 18000 22000

Sales per

unit.

$

45

$

45

$

45

$

45

Sales price

$

9,00,000

$

8,10,000

$

8,10,000

$

9,90,000

Sales of

drink 60000 54000 54000 66000

Sales per

unit.

$

6

$

6

$

6

$

6

Sales price

$

3,60,000

$

3,24,000

$

3,24,000

$

3,96,000

Accounting for business

6

Total Sales

$

12,60,000

$

11,34,000

$

11,34,000

$

13,86,000

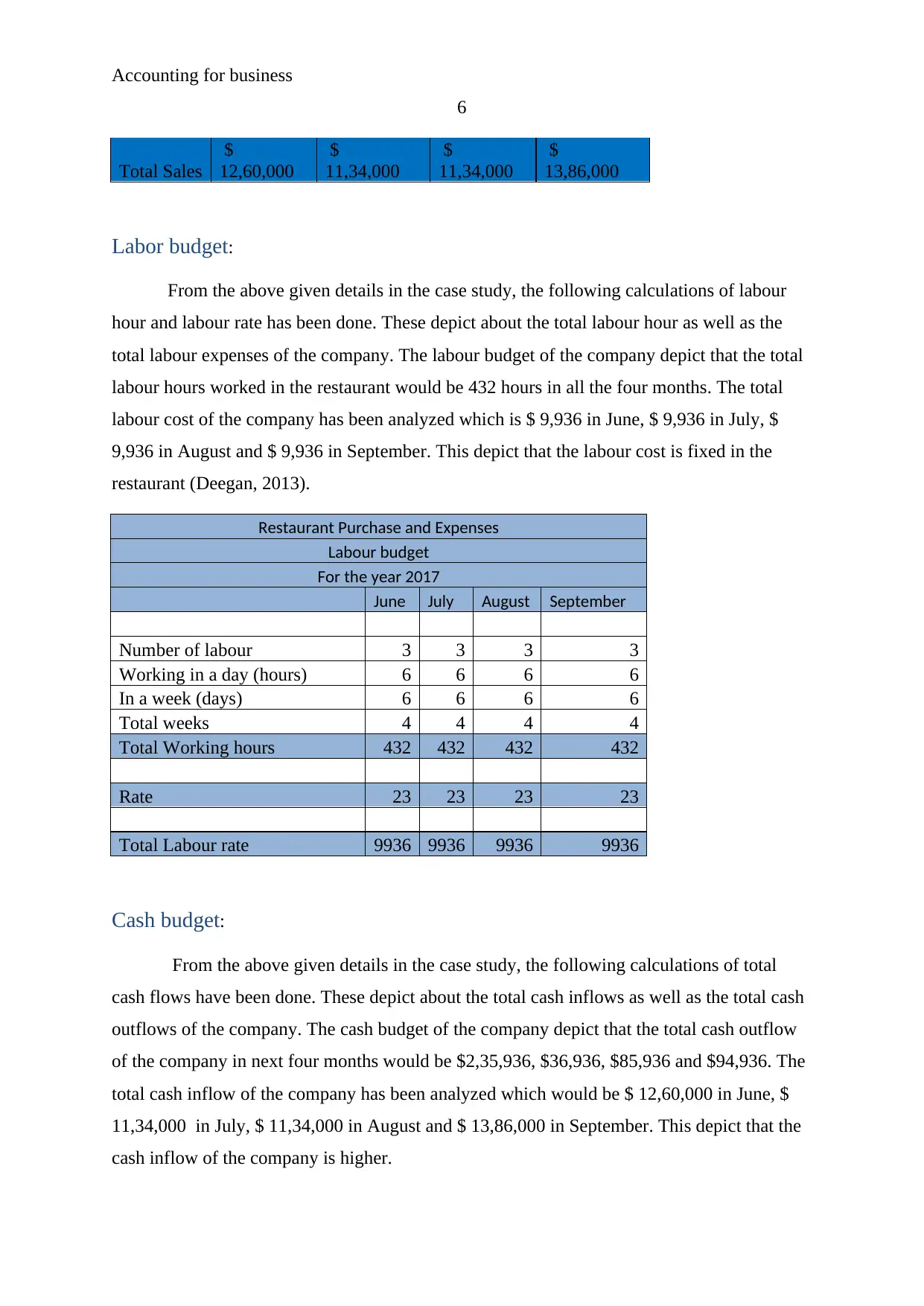

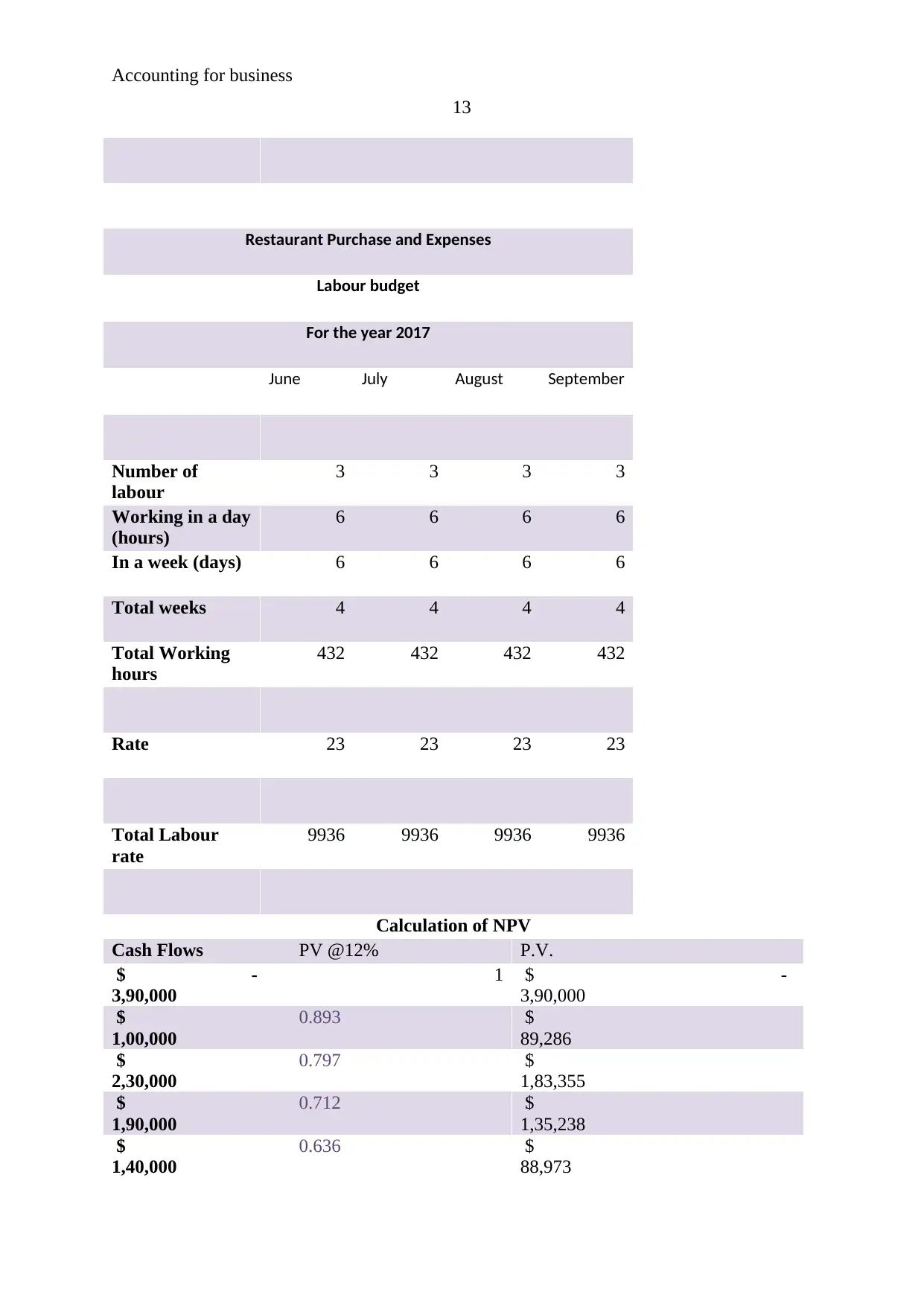

Labor budget:

From the above given details in the case study, the following calculations of labour

hour and labour rate has been done. These depict about the total labour hour as well as the

total labour expenses of the company. The labour budget of the company depict that the total

labour hours worked in the restaurant would be 432 hours in all the four months. The total

labour cost of the company has been analyzed which is $ 9,936 in June, $ 9,936 in July, $

9,936 in August and $ 9,936 in September. This depict that the labour cost is fixed in the

restaurant (Deegan, 2013).

Restaurant Purchase and Expenses

Labour budget

For the year 2017

June July August September

Number of labour 3 3 3 3

Working in a day (hours) 6 6 6 6

In a week (days) 6 6 6 6

Total weeks 4 4 4 4

Total Working hours 432 432 432 432

Rate 23 23 23 23

Total Labour rate 9936 9936 9936 9936

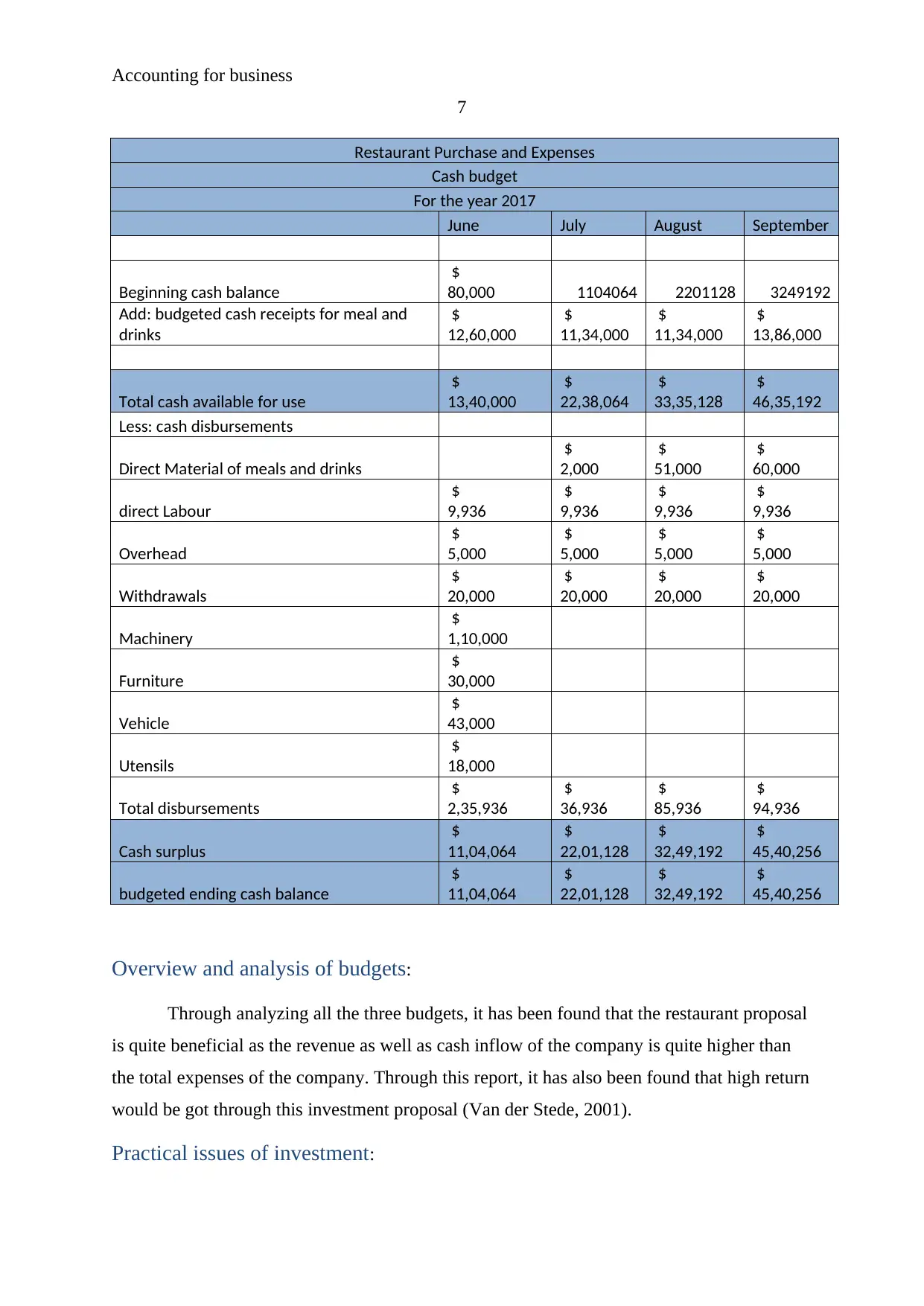

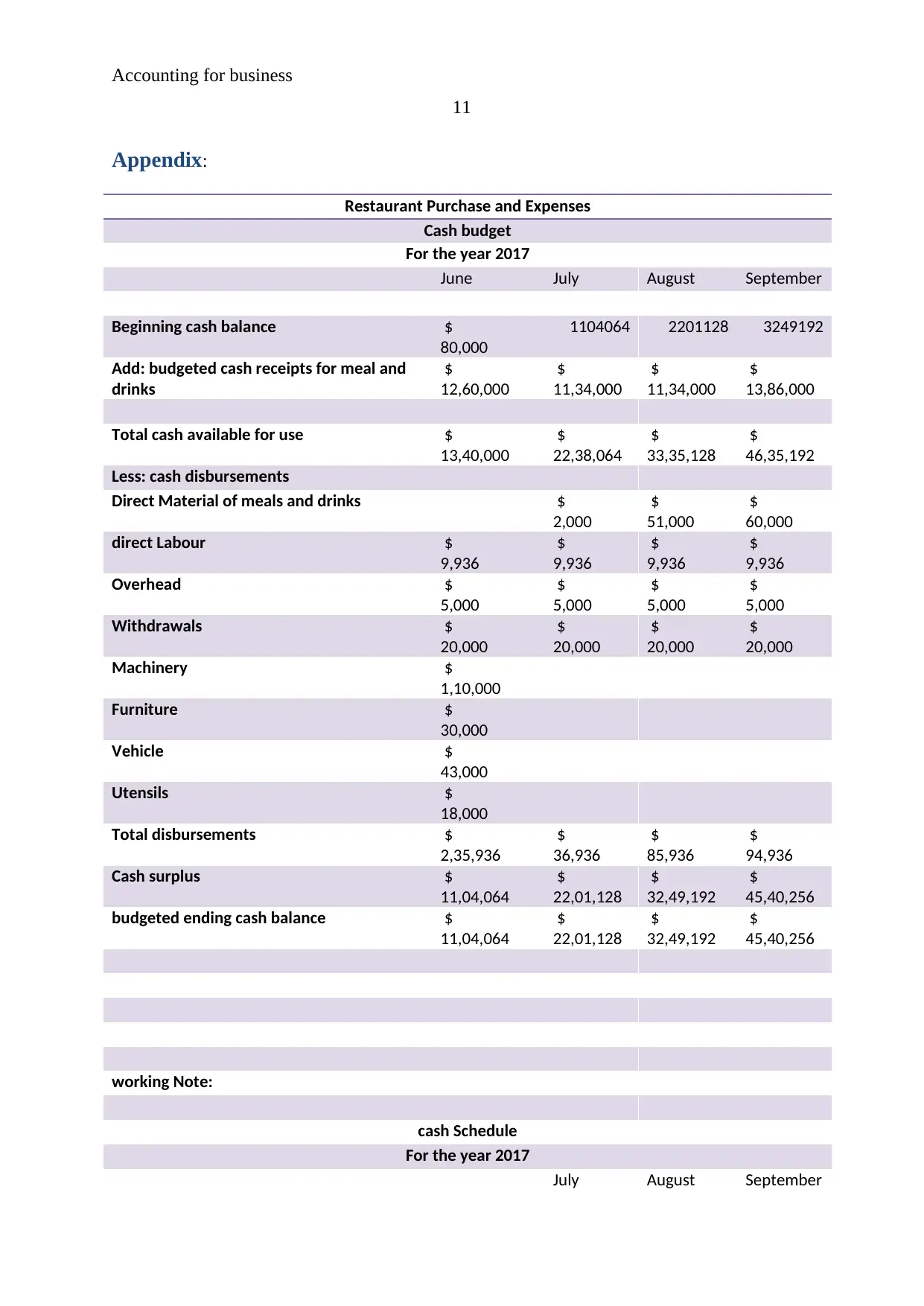

Cash budget:

From the above given details in the case study, the following calculations of total

cash flows have been done. These depict about the total cash inflows as well as the total cash

outflows of the company. The cash budget of the company depict that the total cash outflow

of the company in next four months would be $2,35,936, $36,936, $85,936 and $94,936. The

total cash inflow of the company has been analyzed which would be $ 12,60,000 in June, $

11,34,000 in July, $ 11,34,000 in August and $ 13,86,000 in September. This depict that the

cash inflow of the company is higher.

6

Total Sales

$

12,60,000

$

11,34,000

$

11,34,000

$

13,86,000

Labor budget:

From the above given details in the case study, the following calculations of labour

hour and labour rate has been done. These depict about the total labour hour as well as the

total labour expenses of the company. The labour budget of the company depict that the total

labour hours worked in the restaurant would be 432 hours in all the four months. The total

labour cost of the company has been analyzed which is $ 9,936 in June, $ 9,936 in July, $

9,936 in August and $ 9,936 in September. This depict that the labour cost is fixed in the

restaurant (Deegan, 2013).

Restaurant Purchase and Expenses

Labour budget

For the year 2017

June July August September

Number of labour 3 3 3 3

Working in a day (hours) 6 6 6 6

In a week (days) 6 6 6 6

Total weeks 4 4 4 4

Total Working hours 432 432 432 432

Rate 23 23 23 23

Total Labour rate 9936 9936 9936 9936

Cash budget:

From the above given details in the case study, the following calculations of total

cash flows have been done. These depict about the total cash inflows as well as the total cash

outflows of the company. The cash budget of the company depict that the total cash outflow

of the company in next four months would be $2,35,936, $36,936, $85,936 and $94,936. The

total cash inflow of the company has been analyzed which would be $ 12,60,000 in June, $

11,34,000 in July, $ 11,34,000 in August and $ 13,86,000 in September. This depict that the

cash inflow of the company is higher.

Accounting for business

7

Restaurant Purchase and Expenses

Cash budget

For the year 2017

June July August September

Beginning cash balance

$

80,000 1104064 2201128 3249192

Add: budgeted cash receipts for meal and

drinks

$

12,60,000

$

11,34,000

$

11,34,000

$

13,86,000

Total cash available for use

$

13,40,000

$

22,38,064

$

33,35,128

$

46,35,192

Less: cash disbursements

Direct Material of meals and drinks

$

2,000

$

51,000

$

60,000

direct Labour

$

9,936

$

9,936

$

9,936

$

9,936

Overhead

$

5,000

$

5,000

$

5,000

$

5,000

Withdrawals

$

20,000

$

20,000

$

20,000

$

20,000

Machinery

$

1,10,000

Furniture

$

30,000

Vehicle

$

43,000

Utensils

$

18,000

Total disbursements

$

2,35,936

$

36,936

$

85,936

$

94,936

Cash surplus

$

11,04,064

$

22,01,128

$

32,49,192

$

45,40,256

budgeted ending cash balance

$

11,04,064

$

22,01,128

$

32,49,192

$

45,40,256

Overview and analysis of budgets:

Through analyzing all the three budgets, it has been found that the restaurant proposal

is quite beneficial as the revenue as well as cash inflow of the company is quite higher than

the total expenses of the company. Through this report, it has also been found that high return

would be got through this investment proposal (Van der Stede, 2001).

Practical issues of investment:

7

Restaurant Purchase and Expenses

Cash budget

For the year 2017

June July August September

Beginning cash balance

$

80,000 1104064 2201128 3249192

Add: budgeted cash receipts for meal and

drinks

$

12,60,000

$

11,34,000

$

11,34,000

$

13,86,000

Total cash available for use

$

13,40,000

$

22,38,064

$

33,35,128

$

46,35,192

Less: cash disbursements

Direct Material of meals and drinks

$

2,000

$

51,000

$

60,000

direct Labour

$

9,936

$

9,936

$

9,936

$

9,936

Overhead

$

5,000

$

5,000

$

5,000

$

5,000

Withdrawals

$

20,000

$

20,000

$

20,000

$

20,000

Machinery

$

1,10,000

Furniture

$

30,000

Vehicle

$

43,000

Utensils

$

18,000

Total disbursements

$

2,35,936

$

36,936

$

85,936

$

94,936

Cash surplus

$

11,04,064

$

22,01,128

$

32,49,192

$

45,40,256

budgeted ending cash balance

$

11,04,064

$

22,01,128

$

32,49,192

$

45,40,256

Overview and analysis of budgets:

Through analyzing all the three budgets, it has been found that the restaurant proposal

is quite beneficial as the revenue as well as cash inflow of the company is quite higher than

the total expenses of the company. Through this report, it has also been found that high return

would be got through this investment proposal (Van der Stede, 2001).

Practical issues of investment:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for business

8

Various practical issues could impact over an investment opportunity. Through this

report, it has been found that the market changes, new competitors in the market, already

existed players, changes in the economy etc could impact over the opportunity negatively

which would make the return negative (Nobes & Parker, 2008).

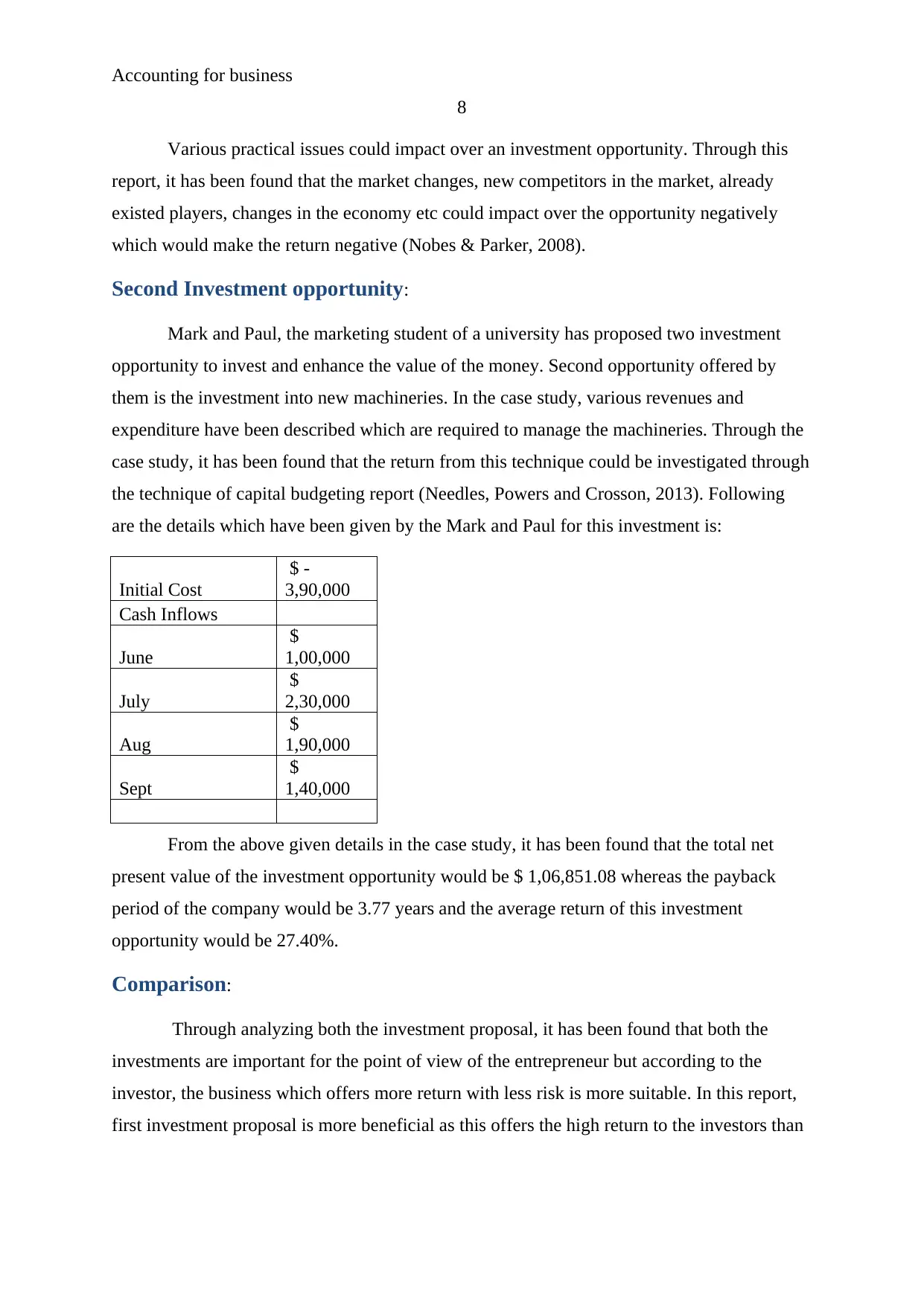

Second Investment opportunity:

Mark and Paul, the marketing student of a university has proposed two investment

opportunity to invest and enhance the value of the money. Second opportunity offered by

them is the investment into new machineries. In the case study, various revenues and

expenditure have been described which are required to manage the machineries. Through the

case study, it has been found that the return from this technique could be investigated through

the technique of capital budgeting report (Needles, Powers and Crosson, 2013). Following

are the details which have been given by the Mark and Paul for this investment is:

Initial Cost

$ -

3,90,000

Cash Inflows

June

$

1,00,000

July

$

2,30,000

Aug

$

1,90,000

Sept

$

1,40,000

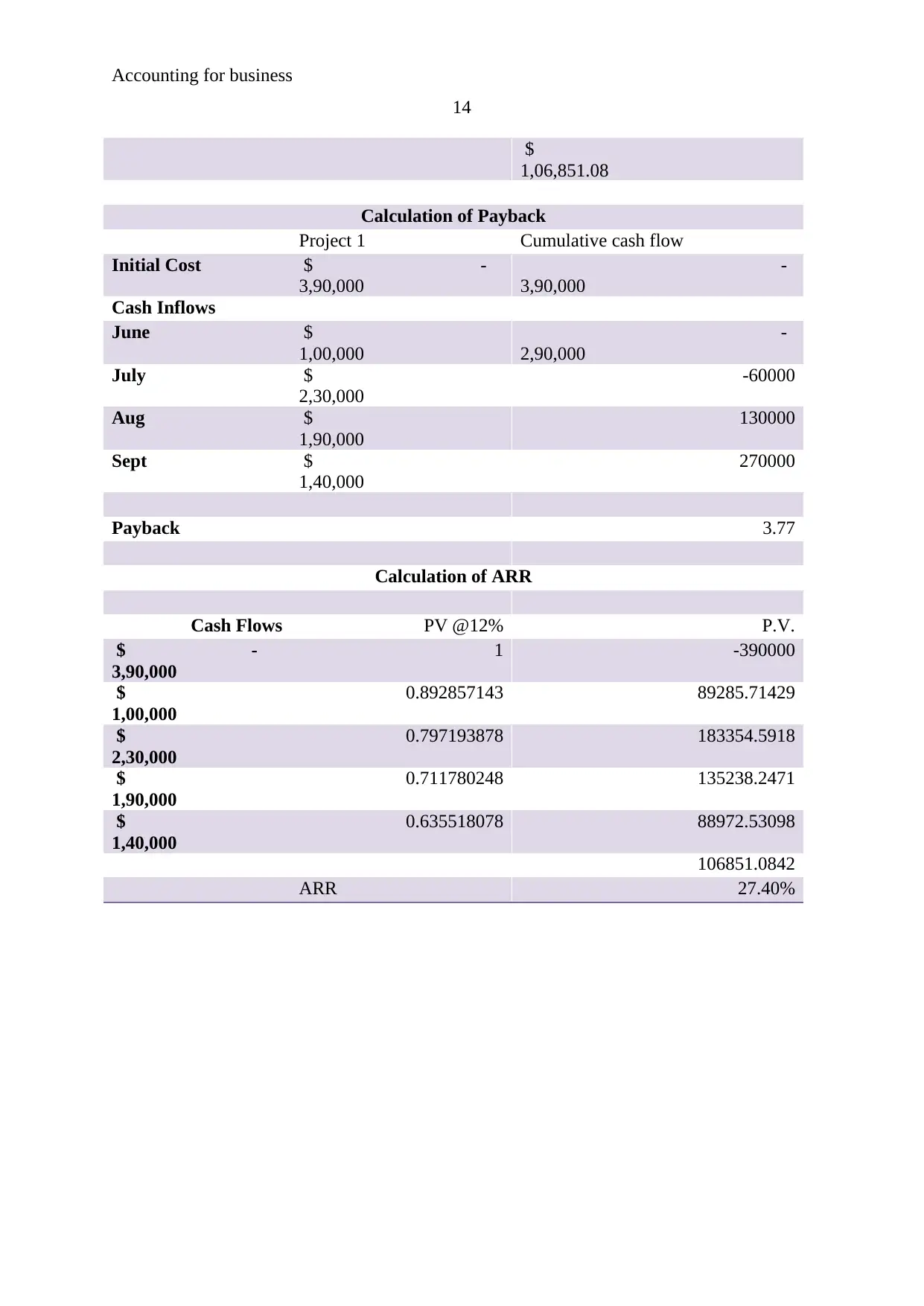

From the above given details in the case study, it has been found that the total net

present value of the investment opportunity would be $ 1,06,851.08 whereas the payback

period of the company would be 3.77 years and the average return of this investment

opportunity would be 27.40%.

Comparison:

Through analyzing both the investment proposal, it has been found that both the

investments are important for the point of view of the entrepreneur but according to the

investor, the business which offers more return with less risk is more suitable. In this report,

first investment proposal is more beneficial as this offers the high return to the investors than

8

Various practical issues could impact over an investment opportunity. Through this

report, it has been found that the market changes, new competitors in the market, already

existed players, changes in the economy etc could impact over the opportunity negatively

which would make the return negative (Nobes & Parker, 2008).

Second Investment opportunity:

Mark and Paul, the marketing student of a university has proposed two investment

opportunity to invest and enhance the value of the money. Second opportunity offered by

them is the investment into new machineries. In the case study, various revenues and

expenditure have been described which are required to manage the machineries. Through the

case study, it has been found that the return from this technique could be investigated through

the technique of capital budgeting report (Needles, Powers and Crosson, 2013). Following

are the details which have been given by the Mark and Paul for this investment is:

Initial Cost

$ -

3,90,000

Cash Inflows

June

$

1,00,000

July

$

2,30,000

Aug

$

1,90,000

Sept

$

1,40,000

From the above given details in the case study, it has been found that the total net

present value of the investment opportunity would be $ 1,06,851.08 whereas the payback

period of the company would be 3.77 years and the average return of this investment

opportunity would be 27.40%.

Comparison:

Through analyzing both the investment proposal, it has been found that both the

investments are important for the point of view of the entrepreneur but according to the

investor, the business which offers more return with less risk is more suitable. In this report,

first investment proposal is more beneficial as this offers the high return to the investors than

Accounting for business

9

the second proposal. So an investor is suggested to invest into the first proposal but if

investor doesn’t want to face any risk then second option is better (Bierman, 2010).

Conclusion:

Thus through this report, it could be concluded that both the opportunities offered by

Mark and Paul for investment are better in their own way. First opportunity offer high return

but at the same time, risk is also higher whereas in second opportunity, less risk is situated.

9

the second proposal. So an investor is suggested to invest into the first proposal but if

investor doesn’t want to face any risk then second option is better (Bierman, 2010).

Conclusion:

Thus through this report, it could be concluded that both the opportunities offered by

Mark and Paul for investment are better in their own way. First opportunity offer high return

but at the same time, risk is also higher whereas in second opportunity, less risk is situated.

Accounting for business

10

References:

Brewer, P.C., Garrison, R.H. and Noreen, E.W., (2005). Introduction to managerial

accounting. McGraw-Hill Irwin.

Bierman, H., (2010). An introduction to accounting and managerial finance: a merger of

equals. World Scientific.

Deegan, C., (2013). Financial accounting theory. McGraw-Hill Education Australia.

Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., (2010). Managerial

accounting. Issues in Accounting Education, (25(4), pp.79(2-793.

Lafond, R. and Roychowdhury, S., (2008). Managerial ownership and accounting

conservatism. Journal of accounting research, 46(1), pp.101-135.

Needles, B., Powers, M. and Crosson, S., (2013). Financial and managerial accounting.

Nelson Education.

Nobes, C. and Parker, R.H., (2008). Comparative international accounting. Pearson

Education.

Van der Stede, W.A., (2001). Measuring ‘tight budgetary control’. Management Accounting

Research, 1(2(1), pp.119-137.

10

References:

Brewer, P.C., Garrison, R.H. and Noreen, E.W., (2005). Introduction to managerial

accounting. McGraw-Hill Irwin.

Bierman, H., (2010). An introduction to accounting and managerial finance: a merger of

equals. World Scientific.

Deegan, C., (2013). Financial accounting theory. McGraw-Hill Education Australia.

Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., (2010). Managerial

accounting. Issues in Accounting Education, (25(4), pp.79(2-793.

Lafond, R. and Roychowdhury, S., (2008). Managerial ownership and accounting

conservatism. Journal of accounting research, 46(1), pp.101-135.

Needles, B., Powers, M. and Crosson, S., (2013). Financial and managerial accounting.

Nelson Education.

Nobes, C. and Parker, R.H., (2008). Comparative international accounting. Pearson

Education.

Van der Stede, W.A., (2001). Measuring ‘tight budgetary control’. Management Accounting

Research, 1(2(1), pp.119-137.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting for business

11

Appendix:

Restaurant Purchase and Expenses

Cash budget

For the year 2017

June July August September

Beginning cash balance $

80,000

1104064 2201128 3249192

Add: budgeted cash receipts for meal and

drinks

$

12,60,000

$

11,34,000

$

11,34,000

$

13,86,000

Total cash available for use $

13,40,000

$

22,38,064

$

33,35,128

$

46,35,192

Less: cash disbursements

Direct Material of meals and drinks $

2,000

$

51,000

$

60,000

direct Labour $

9,936

$

9,936

$

9,936

$

9,936

Overhead $

5,000

$

5,000

$

5,000

$

5,000

Withdrawals $

20,000

$

20,000

$

20,000

$

20,000

Machinery $

1,10,000

Furniture $

30,000

Vehicle $

43,000

Utensils $

18,000

Total disbursements $

2,35,936

$

36,936

$

85,936

$

94,936

Cash surplus $

11,04,064

$

22,01,128

$

32,49,192

$

45,40,256

budgeted ending cash balance $

11,04,064

$

22,01,128

$

32,49,192

$

45,40,256

working Note:

cash Schedule

For the year 2017

July August September

11

Appendix:

Restaurant Purchase and Expenses

Cash budget

For the year 2017

June July August September

Beginning cash balance $

80,000

1104064 2201128 3249192

Add: budgeted cash receipts for meal and

drinks

$

12,60,000

$

11,34,000

$

11,34,000

$

13,86,000

Total cash available for use $

13,40,000

$

22,38,064

$

33,35,128

$

46,35,192

Less: cash disbursements

Direct Material of meals and drinks $

2,000

$

51,000

$

60,000

direct Labour $

9,936

$

9,936

$

9,936

$

9,936

Overhead $

5,000

$

5,000

$

5,000

$

5,000

Withdrawals $

20,000

$

20,000

$

20,000

$

20,000

Machinery $

1,10,000

Furniture $

30,000

Vehicle $

43,000

Utensils $

18,000

Total disbursements $

2,35,936

$

36,936

$

85,936

$

94,936

Cash surplus $

11,04,064

$

22,01,128

$

32,49,192

$

45,40,256

budgeted ending cash balance $

11,04,064

$

22,01,128

$

32,49,192

$

45,40,256

working Note:

cash Schedule

For the year 2017

July August September

Accounting for business

12

Material Purchase 20000 20000 20000

Cash received 10% 2000 2000 2000

Cash received 45% 9000 9000

Cash received 45% 9000

Total cash received 2000 11000 20000

Restaurant Purchase and Expenses

Sales budget

For the year 2017

June July August September

Sales of meals 20000 18000 18000 22000

Sales per unit. $

45

$

45

$

45

$

45

Sales price $

9,00,000

$

8,10,000

$

8,10,000

$

9,90,000

Sales of drink 60000 54000 54000 66000

Sales per unit. $

6

$

6

$

6

$

6

Sales price $

3,60,000

$

3,24,000

$

3,24,000

$

3,96,000

Total Sales $

12,60,000

$

11,34,000

$

11,34,000

$

13,86,000

12

Material Purchase 20000 20000 20000

Cash received 10% 2000 2000 2000

Cash received 45% 9000 9000

Cash received 45% 9000

Total cash received 2000 11000 20000

Restaurant Purchase and Expenses

Sales budget

For the year 2017

June July August September

Sales of meals 20000 18000 18000 22000

Sales per unit. $

45

$

45

$

45

$

45

Sales price $

9,00,000

$

8,10,000

$

8,10,000

$

9,90,000

Sales of drink 60000 54000 54000 66000

Sales per unit. $

6

$

6

$

6

$

6

Sales price $

3,60,000

$

3,24,000

$

3,24,000

$

3,96,000

Total Sales $

12,60,000

$

11,34,000

$

11,34,000

$

13,86,000

Accounting for business

13

Restaurant Purchase and Expenses

Labour budget

For the year 2017

June July August September

Number of

labour

3 3 3 3

Working in a day

(hours)

6 6 6 6

In a week (days) 6 6 6 6

Total weeks 4 4 4 4

Total Working

hours

432 432 432 432

Rate 23 23 23 23

Total Labour

rate

9936 9936 9936 9936

Calculation of NPV

Cash Flows PV @12% P.V.

$ -

3,90,000

1 $ -

3,90,000

$

1,00,000

0.893 $

89,286

$

2,30,000

0.797 $

1,83,355

$

1,90,000

0.712 $

1,35,238

$

1,40,000

0.636 $

88,973

13

Restaurant Purchase and Expenses

Labour budget

For the year 2017

June July August September

Number of

labour

3 3 3 3

Working in a day

(hours)

6 6 6 6

In a week (days) 6 6 6 6

Total weeks 4 4 4 4

Total Working

hours

432 432 432 432

Rate 23 23 23 23

Total Labour

rate

9936 9936 9936 9936

Calculation of NPV

Cash Flows PV @12% P.V.

$ -

3,90,000

1 $ -

3,90,000

$

1,00,000

0.893 $

89,286

$

2,30,000

0.797 $

1,83,355

$

1,90,000

0.712 $

1,35,238

$

1,40,000

0.636 $

88,973

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for business

14

$

1,06,851.08

Calculation of Payback

Project 1 Cumulative cash flow

Initial Cost $ -

3,90,000

-

3,90,000

Cash Inflows

June $

1,00,000

-

2,90,000

July $

2,30,000

-60000

Aug $

1,90,000

130000

Sept $

1,40,000

270000

Payback 3.77

Calculation of ARR

Cash Flows PV @12% P.V.

$ -

3,90,000

1 -390000

$

1,00,000

0.892857143 89285.71429

$

2,30,000

0.797193878 183354.5918

$

1,90,000

0.711780248 135238.2471

$

1,40,000

0.635518078 88972.53098

106851.0842

ARR 27.40%

14

$

1,06,851.08

Calculation of Payback

Project 1 Cumulative cash flow

Initial Cost $ -

3,90,000

-

3,90,000

Cash Inflows

June $

1,00,000

-

2,90,000

July $

2,30,000

-60000

Aug $

1,90,000

130000

Sept $

1,40,000

270000

Payback 3.77

Calculation of ARR

Cash Flows PV @12% P.V.

$ -

3,90,000

1 -390000

$

1,00,000

0.892857143 89285.71429

$

2,30,000

0.797193878 183354.5918

$

1,90,000

0.711780248 135238.2471

$

1,40,000

0.635518078 88972.53098

106851.0842

ARR 27.40%

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.