Dividend Policy and Share Value

VerifiedAdded on 2020/04/29

|11

|3220

|486

AI Summary

The assignment examines the influence of dividend policies on a company's share value. It requires students to delve into various academic articles and publications, including those by Barman (2008), Bodie (2013), Bradford et al. (2013), Brealey et al. (2007), and others. Students must analyze the research findings presented in these papers to understand the relationship between dividend policies and share value.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Corporate Finance

1

Project report: Corporate finance

1

Project report: Corporate finance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Finance

2

Contents

Introduction.......................................................................................................................3

Analyze the dividend polices and analytical view............................................................3

Low dividend payout or high dividend payout.................................................................4

Analysis over dividend and share price relation...............................................................5

Analytical evidences.........................................................................................................6

Conclusion........................................................................................................................7

References.........................................................................................................................9

2

Contents

Introduction.......................................................................................................................3

Analyze the dividend polices and analytical view............................................................3

Low dividend payout or high dividend payout.................................................................4

Analysis over dividend and share price relation...............................................................5

Analytical evidences.........................................................................................................6

Conclusion........................................................................................................................7

References.........................................................................................................................9

Corporate Finance

3

Introduction:

Dividend payment strategy and share price of a company is directly related to each

other. If the company would offer high dividend payout or low dividend payout than it

directly affects the share price of a company. Mainly, both the policies which are high

dividend policies and low dividend policies make the different impact over the performance

and the stock price of a company. Companies’ take the help of various dividend policies to

make a better decision about how much dividend must be paid to the investors to keep them

satisfied and attract other investors to invest into the operations of the company (Zhang,

2012). Various dividend policies such as relevant theory, residual relevant theory, expectation

theory etc have been analyzed. Usually making a decision about the high or low dividend is

important for an organization. An organization is required to look over various factors and

then make a better decision about the dividends. In this report, various dividend policies of

the company have been analyzed and than a better decision have been made (FIRRER 2012).

Analyze the dividend polices and analytical view:

Dividend policies are mainly of two types which are relevant dividend polices and

irrelevant dividend policies. Relevant dividend policies depict that mainly investors look over

the market and dividend offered by the company to make a decision about the investment into

the company. Relevant dividend theories are bird in hand theory, expectation theory and

residual dividend theory whereas irrelevant theories are MM theory. Dividend relevant

theories brief that the tax and the transaction cost of the company are also applied and

considered while making the decision of the investment. Inflation rate do not exist in this

theory (Tucker, 2011). Bird in hand theory mainly considers that high dividend payout ratio

must be adopted by the company as it attracts the investors more due to the thought process

of the investors that they would be able to earn the more return from the stock of the

company.

Further, the residual dividend theory depict that the company must manage all the

expenditure, capital expenditure before distributing the divided amount to its shareholders.

This depict that the total amount of profit must be distributed to the shareholder but after

paying all the capital expenditure (DEEPTEE and ROSHAN, 2009). Expectation theory

states that long term interest rate depict about the short term performance of the company.

3

Introduction:

Dividend payment strategy and share price of a company is directly related to each

other. If the company would offer high dividend payout or low dividend payout than it

directly affects the share price of a company. Mainly, both the policies which are high

dividend policies and low dividend policies make the different impact over the performance

and the stock price of a company. Companies’ take the help of various dividend policies to

make a better decision about how much dividend must be paid to the investors to keep them

satisfied and attract other investors to invest into the operations of the company (Zhang,

2012). Various dividend policies such as relevant theory, residual relevant theory, expectation

theory etc have been analyzed. Usually making a decision about the high or low dividend is

important for an organization. An organization is required to look over various factors and

then make a better decision about the dividends. In this report, various dividend policies of

the company have been analyzed and than a better decision have been made (FIRRER 2012).

Analyze the dividend polices and analytical view:

Dividend policies are mainly of two types which are relevant dividend polices and

irrelevant dividend policies. Relevant dividend policies depict that mainly investors look over

the market and dividend offered by the company to make a decision about the investment into

the company. Relevant dividend theories are bird in hand theory, expectation theory and

residual dividend theory whereas irrelevant theories are MM theory. Dividend relevant

theories brief that the tax and the transaction cost of the company are also applied and

considered while making the decision of the investment. Inflation rate do not exist in this

theory (Tucker, 2011). Bird in hand theory mainly considers that high dividend payout ratio

must be adopted by the company as it attracts the investors more due to the thought process

of the investors that they would be able to earn the more return from the stock of the

company.

Further, the residual dividend theory depict that the company must manage all the

expenditure, capital expenditure before distributing the divided amount to its shareholders.

This depict that the total amount of profit must be distributed to the shareholder but after

paying all the capital expenditure (DEEPTEE and ROSHAN, 2009). Expectation theory

states that long term interest rate depict about the short term performance of the company.

Corporate Finance

4

Further, it has been found that all of these theories depict the company to take the use of all

the net profit to attract the investors (Davies and Crawford, 2011).

Further, irrelevant dividend policies have been analyzed. It depict that mainly

investors do not look over the market and dividend offered by the company to make a

decision about the investment into the company whereas they analyze the financial

performance and stability of the company (Breuer, Rieger and Soypak, 2014). Miller and

Modigliani have invested this approach. They have analyzed through this research that it is

not necessary for the investors of a market to consider the dividend payout of the company

(Masum, 2014).

They have also approached that the dividend payout of a company could never be

enough to analyze about the stability and performance of the company. This theory also

briefs that the tax and the transaction cost of the company are also not applied and do not

considered while making the decision about the investment (CORRERIA, 2013). This theory

mainly considers that it is not required for an organization to deliver high dividend to the

investor because this could not depict about the performance of the company (Travlos,

Trigeorgis and Vafeas, 2015).

The hypothesis of dividend theory depict that various factors are there which makes

an impact over the management and organization choice about the dividends. Leverages, debt

constraints, capital rules impairment, cash availability and investment opportunities in front

of the company (Barman, 2008). For instance, if the company has a great investment

opportunity and for that company wants to raise the fund than company could retain some

amount of dividend for further use and it would impact over the dividend policies of the

companies.

Further, according to the study of Brealey, Myers and Marcus, (2007), it has been

found that the factors are quite important for an investors as well as organization to

understand. Many times, the dividend is lowered by the company to raise the profits of the

company through some other ways. Investors must look over these points and make a

decision accordingly (Bradford, Chen and Zhu, 2013). It would also help the company to

maintain the stock price.

Though, from various studies and the reports of the analyst, it has been analyzed that

the investors are not well informed and do not have enough knowledge to analyze and

4

Further, it has been found that all of these theories depict the company to take the use of all

the net profit to attract the investors (Davies and Crawford, 2011).

Further, irrelevant dividend policies have been analyzed. It depict that mainly

investors do not look over the market and dividend offered by the company to make a

decision about the investment into the company whereas they analyze the financial

performance and stability of the company (Breuer, Rieger and Soypak, 2014). Miller and

Modigliani have invested this approach. They have analyzed through this research that it is

not necessary for the investors of a market to consider the dividend payout of the company

(Masum, 2014).

They have also approached that the dividend payout of a company could never be

enough to analyze about the stability and performance of the company. This theory also

briefs that the tax and the transaction cost of the company are also not applied and do not

considered while making the decision about the investment (CORRERIA, 2013). This theory

mainly considers that it is not required for an organization to deliver high dividend to the

investor because this could not depict about the performance of the company (Travlos,

Trigeorgis and Vafeas, 2015).

The hypothesis of dividend theory depict that various factors are there which makes

an impact over the management and organization choice about the dividends. Leverages, debt

constraints, capital rules impairment, cash availability and investment opportunities in front

of the company (Barman, 2008). For instance, if the company has a great investment

opportunity and for that company wants to raise the fund than company could retain some

amount of dividend for further use and it would impact over the dividend policies of the

companies.

Further, according to the study of Brealey, Myers and Marcus, (2007), it has been

found that the factors are quite important for an investors as well as organization to

understand. Many times, the dividend is lowered by the company to raise the profits of the

company through some other ways. Investors must look over these points and make a

decision accordingly (Bradford, Chen and Zhu, 2013). It would also help the company to

maintain the stock price.

Though, from various studies and the reports of the analyst, it has been analyzed that

the investors are not well informed and do not have enough knowledge to analyze and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Finance

5

evaluate the performance of the company (Bodie, 2013). They only analyze the current

performance and the position of the company which could only be analyzed through the

current market share price of the company (STEEN et al, 2012).

Thus through this analysis, it has been analyzed that the company’s are required to

announce the dividend to set the performance and position into the current market so that the

investors could get attract towards the company and make high investment into the company.

Cash dividends are bit essential for the company to become more competitive and enhance

the market price of the stock of the company (CORRERIA et al, 2013).

Factors for low dividend payout or high dividend payout:

Dividend payout is the value which evaluates the total dividend paid out by the

company to its investors on the basis of the net profit of the company. Dividend payout of a

company mainly depends over the policies of the company (Breuer, Rieger and Soypak,

2014). If the company follows the policy of the relevant policies than the dividend payout of

the company would be higher whereas if the company would follow the policies of the

irrelevant policies than the dividend payout of the company would be lower or nil. The

formulas of dividend payout are as follows:

=Total annual dividend of the company / diluted earnings per share (Davies and Crawford,

2011).

There are various factors which affect the lower dividend payout as well as higher

dividend payout of a company such as the industry norms, investment opportunity, cash

position in the company, competitor’s position, profit position of the company, economical

position etc. A company is required to make the decision about dividend payout after

considering all the above given factors. Such as if the economical position is not good than

must company must retain the profit and use it for further operations of the company rather

than dividing it into the shareholders of the company.

Low dividend payout ratio depict that the comapny would offer a lower % of the total

net profit to the investors and will retain the extra amount for the further investment in the

company so that the company do not require to raise the funds from the external sources.

Low dividend payout ratio is not in the favour of the company according to the various

analyst of the company (Barman, 2008). At the same time, high dividend payout ratio depict

that the comapny would offer a higher % of the total net profit to the investors so that the

5

evaluate the performance of the company (Bodie, 2013). They only analyze the current

performance and the position of the company which could only be analyzed through the

current market share price of the company (STEEN et al, 2012).

Thus through this analysis, it has been analyzed that the company’s are required to

announce the dividend to set the performance and position into the current market so that the

investors could get attract towards the company and make high investment into the company.

Cash dividends are bit essential for the company to become more competitive and enhance

the market price of the stock of the company (CORRERIA et al, 2013).

Factors for low dividend payout or high dividend payout:

Dividend payout is the value which evaluates the total dividend paid out by the

company to its investors on the basis of the net profit of the company. Dividend payout of a

company mainly depends over the policies of the company (Breuer, Rieger and Soypak,

2014). If the company follows the policy of the relevant policies than the dividend payout of

the company would be higher whereas if the company would follow the policies of the

irrelevant policies than the dividend payout of the company would be lower or nil. The

formulas of dividend payout are as follows:

=Total annual dividend of the company / diluted earnings per share (Davies and Crawford,

2011).

There are various factors which affect the lower dividend payout as well as higher

dividend payout of a company such as the industry norms, investment opportunity, cash

position in the company, competitor’s position, profit position of the company, economical

position etc. A company is required to make the decision about dividend payout after

considering all the above given factors. Such as if the economical position is not good than

must company must retain the profit and use it for further operations of the company rather

than dividing it into the shareholders of the company.

Low dividend payout ratio depict that the comapny would offer a lower % of the total

net profit to the investors and will retain the extra amount for the further investment in the

company so that the company do not require to raise the funds from the external sources.

Low dividend payout ratio is not in the favour of the company according to the various

analyst of the company (Barman, 2008). At the same time, high dividend payout ratio depict

that the comapny would offer a higher % of the total net profit to the investors so that the

Corporate Finance

6

company. This % would be higher than the affordability of the company. High dividend

payout ratio is not in the favour of the company according to the various analyst of the

company as this assist the company to face various risks in the market (Brealey, Myers and

Marcus, 2007).

A company must consider the high dividend payout ratio only if the market position

of the company is well and good and company could enhance the profit at any time and the

funds could also be raised by the company from market easily (Shao, Kwo and Guedhami,

2013). So, the management accountant must make the decision of lower dividend policies

and higher dividend policies accordingly. Mainly, it is considered that higher dividend profit

is the best option as investor got some money periodically in terms of dividend which makes

them attract.

Analysis over dividend and share price relation:

Dividend payment and share price of the company is direct related to each other.

Mainly, the share price of a company is affected due to the dividend price although the

dividend history and other related factors also make an affect over these values. If the

dividend offered by the company gets reduced than it directly affect the share price of the

company. Companies’ take the help of various dividend policies to make a better decision

about how much dividend must be paid to the investors to keep them satisfy and attract other

investors to invest into the operations of the company. Basically, it becomes bit tough for the

company to make these decisions.

Market psychology is an outcome of various analysts’ report collectively that depict

that basically the share price of a company depends over the total stock of the company

which has been issues and fluctuations which could take place into the security market or the

economical condition of the company. Naser, Nuseibeh and Rashed, (2013) have expressed

that an investor always wants to earn more profits from the market and enhance the worth of

the invested amount. So he or she tries to invest into that security from where they could earn

more profits.

Bodie, (2013) has expressed in their study that dividend psychology has also been

studied and it has been analyzed that it depicts that the many companies always offer the

same dividend with a good dividend payout ratio so that the expectation of the investors

enhances from the market and they expect that each company would offer them that much of

6

company. This % would be higher than the affordability of the company. High dividend

payout ratio is not in the favour of the company according to the various analyst of the

company as this assist the company to face various risks in the market (Brealey, Myers and

Marcus, 2007).

A company must consider the high dividend payout ratio only if the market position

of the company is well and good and company could enhance the profit at any time and the

funds could also be raised by the company from market easily (Shao, Kwo and Guedhami,

2013). So, the management accountant must make the decision of lower dividend policies

and higher dividend policies accordingly. Mainly, it is considered that higher dividend profit

is the best option as investor got some money periodically in terms of dividend which makes

them attract.

Analysis over dividend and share price relation:

Dividend payment and share price of the company is direct related to each other.

Mainly, the share price of a company is affected due to the dividend price although the

dividend history and other related factors also make an affect over these values. If the

dividend offered by the company gets reduced than it directly affect the share price of the

company. Companies’ take the help of various dividend policies to make a better decision

about how much dividend must be paid to the investors to keep them satisfy and attract other

investors to invest into the operations of the company. Basically, it becomes bit tough for the

company to make these decisions.

Market psychology is an outcome of various analysts’ report collectively that depict

that basically the share price of a company depends over the total stock of the company

which has been issues and fluctuations which could take place into the security market or the

economical condition of the company. Naser, Nuseibeh and Rashed, (2013) have expressed

that an investor always wants to earn more profits from the market and enhance the worth of

the invested amount. So he or she tries to invest into that security from where they could earn

more profits.

Bodie, (2013) has expressed in their study that dividend psychology has also been

studied and it has been analyzed that it depicts that the many companies always offer the

same dividend with a good dividend payout ratio so that the expectation of the investors

enhances from the market and they expect that each company would offer them that much of

Corporate Finance

7

dividend. Thanatawee (2013) says that this creates a positive relationship among the dividend

and share price of the company. As due to the dividend, the investors would be attracted more

towards the company and then the demand and supply of the stock in the market would

enhance and through it the share price of the company would also increase.

Through it and through the market analysis, it has been found that dividend

declaration affects the stock price of a company at huge level (Bradford et al, 2013). At the

time of delivering the dividend, the share price of the company get fluctuate rapidly and the

main reason behind enhancing and decreasing the stock price of the company is its dividend

payout value. Baker and Weigand, (2015) have expressed that through the dividend and stock

price of the company have positive relations with each other so the company is required to

offer a good dividend to the investors to make a good position in the market and enhance the

market price of the security.

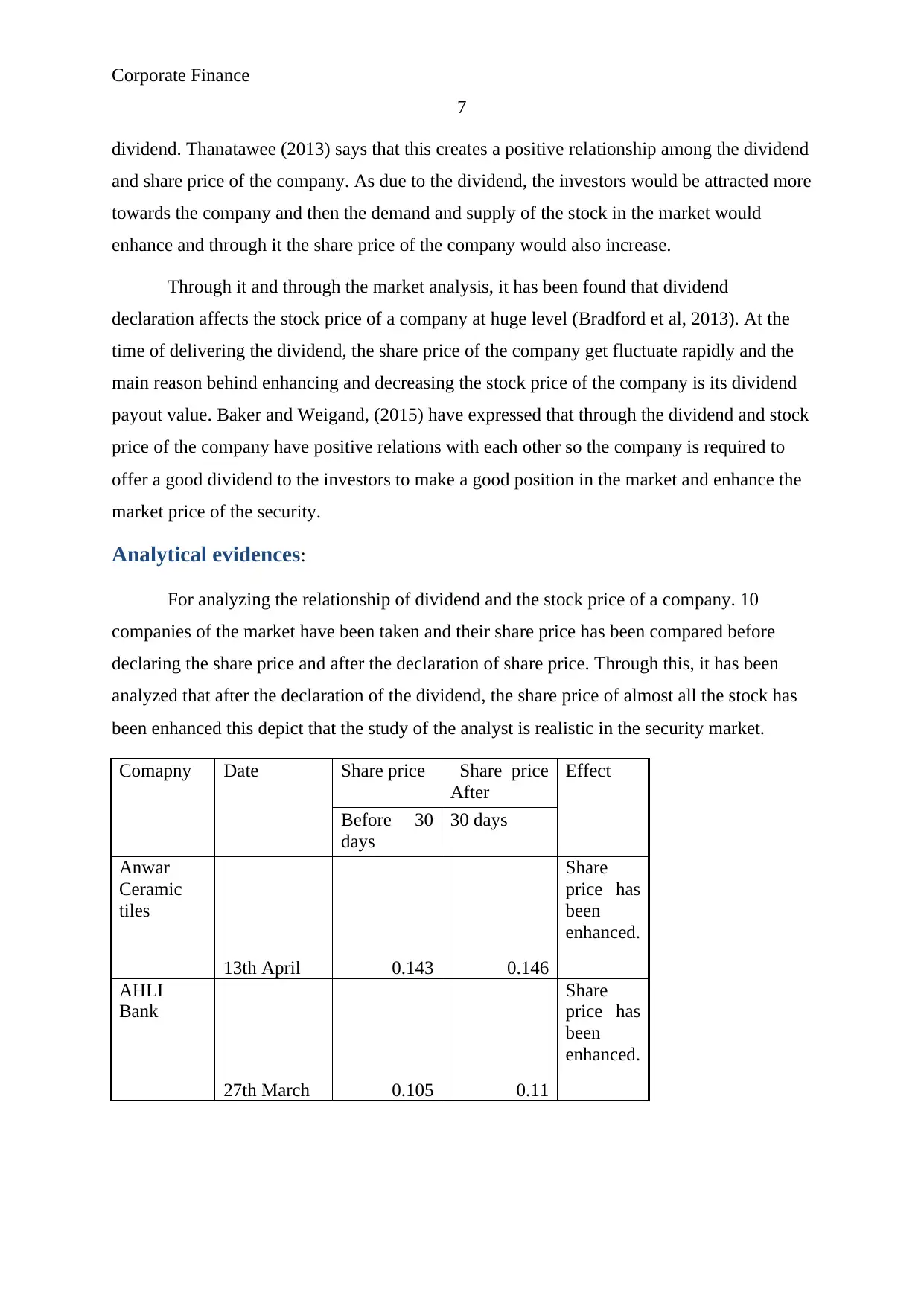

Analytical evidences:

For analyzing the relationship of dividend and the stock price of a company. 10

companies of the market have been taken and their share price has been compared before

declaring the share price and after the declaration of share price. Through this, it has been

analyzed that after the declaration of the dividend, the share price of almost all the stock has

been enhanced this depict that the study of the analyst is realistic in the security market.

Comapny Date Share price Share price

After

Effect

Before 30

days

30 days

Anwar

Ceramic

tiles

13th April 0.143 0.146

Share

price has

been

enhanced.

AHLI

Bank

27th March 0.105 0.11

Share

price has

been

enhanced.

7

dividend. Thanatawee (2013) says that this creates a positive relationship among the dividend

and share price of the company. As due to the dividend, the investors would be attracted more

towards the company and then the demand and supply of the stock in the market would

enhance and through it the share price of the company would also increase.

Through it and through the market analysis, it has been found that dividend

declaration affects the stock price of a company at huge level (Bradford et al, 2013). At the

time of delivering the dividend, the share price of the company get fluctuate rapidly and the

main reason behind enhancing and decreasing the stock price of the company is its dividend

payout value. Baker and Weigand, (2015) have expressed that through the dividend and stock

price of the company have positive relations with each other so the company is required to

offer a good dividend to the investors to make a good position in the market and enhance the

market price of the security.

Analytical evidences:

For analyzing the relationship of dividend and the stock price of a company. 10

companies of the market have been taken and their share price has been compared before

declaring the share price and after the declaration of share price. Through this, it has been

analyzed that after the declaration of the dividend, the share price of almost all the stock has

been enhanced this depict that the study of the analyst is realistic in the security market.

Comapny Date Share price Share price

After

Effect

Before 30

days

30 days

Anwar

Ceramic

tiles

13th April 0.143 0.146

Share

price has

been

enhanced.

AHLI

Bank

27th March 0.105 0.11

Share

price has

been

enhanced.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Finance

8

Madina

Investment

28th June 0.38 0.39

Share

price has

been

enhanced.

ACWA

Power

Barka

18th June 0.78 0.752

Share

price has

been

reduced.

Bank

Dhofar

27th March 0.198 0.202

Share

price has

been

enhanced.

Majan

college

29th Nov 0.42 0.46

Share

price has

been

enhanced.

Batinah

power

11th June 1.125 1.125

Share

price is

similar.

Madina

Takaful

27th March 0.105 0.109

Share

price has

been

enhanced.

Buriami

Hotel

18th June 0.93 0.98

Share

price has

been

enhanced.

Omannia

financial

securities

21st March 0.253 0.276

Share

price has

been

enhanced.

The above calculation and analysis over the above companies express that the Anwar

ceramic tiles, AHLI bank, Medina Investment, Bank Dhofar, Majan college, Madina Takaful,

Buriami Hotel and Omannia financial securities depict that the stock price of these securities

8

Madina

Investment

28th June 0.38 0.39

Share

price has

been

enhanced.

ACWA

Power

Barka

18th June 0.78 0.752

Share

price has

been

reduced.

Bank

Dhofar

27th March 0.198 0.202

Share

price has

been

enhanced.

Majan

college

29th Nov 0.42 0.46

Share

price has

been

enhanced.

Batinah

power

11th June 1.125 1.125

Share

price is

similar.

Madina

Takaful

27th March 0.105 0.109

Share

price has

been

enhanced.

Buriami

Hotel

18th June 0.93 0.98

Share

price has

been

enhanced.

Omannia

financial

securities

21st March 0.253 0.276

Share

price has

been

enhanced.

The above calculation and analysis over the above companies express that the Anwar

ceramic tiles, AHLI bank, Medina Investment, Bank Dhofar, Majan college, Madina Takaful,

Buriami Hotel and Omannia financial securities depict that the stock price of these securities

Corporate Finance

9

has been enhanced after announcing the dividend. This has taken place due to the high

dividend payout ratio. The dividend announcement has attracted the investors to invest into

the company. Further, the stock price of the ACWA power Barka has been reduced due to

lower dividend payout ratio. And the share price of Batinah Power has become same even

after announcing the dividend due to the fact that the dividend offered by the company was

average. Through this study, it has been found that if the normal or good dividend is offered

by the company to its investors then the demand of the stock enhances into the market and it

directly make an impact over the share price of the company (Hillier, Grinblatt and Titman,

2011).

Conclusion:

To conclude, organizations must look over the analysis and market situation as well as

the nature of the investors before announcing the dividend so that the investors could get

attract towards the company and company become able to get more dividend from the

market. Cash dividends are bit essential for the company to become more competitive and

enhance the market price of the stock of the company.

Neither the higher dividend payout ratio nor the lower dividend payout ratio is in the

favour of the company as both of these would raise the different issues in front of the

company. Through this, it is suggested to the manager of the company to evaluate the

dividend payout ratio according to the nature of the company and economical condition of the

country.

9

has been enhanced after announcing the dividend. This has taken place due to the high

dividend payout ratio. The dividend announcement has attracted the investors to invest into

the company. Further, the stock price of the ACWA power Barka has been reduced due to

lower dividend payout ratio. And the share price of Batinah Power has become same even

after announcing the dividend due to the fact that the dividend offered by the company was

average. Through this study, it has been found that if the normal or good dividend is offered

by the company to its investors then the demand of the stock enhances into the market and it

directly make an impact over the share price of the company (Hillier, Grinblatt and Titman,

2011).

Conclusion:

To conclude, organizations must look over the analysis and market situation as well as

the nature of the investors before announcing the dividend so that the investors could get

attract towards the company and company become able to get more dividend from the

market. Cash dividends are bit essential for the company to become more competitive and

enhance the market price of the stock of the company.

Neither the higher dividend payout ratio nor the lower dividend payout ratio is in the

favour of the company as both of these would raise the different issues in front of the

company. Through this, it is suggested to the manager of the company to evaluate the

dividend payout ratio according to the nature of the company and economical condition of the

country.

Corporate Finance

10

References:

Baker, H.K. and Weigand, R., 2015. Corporate dividend policy revisited. Managerial

Finance, 41(2), pp.126-144.

Barman, G.P., 2008. An evaluation of how dividend policies impact on the share value of

selected companies.

Bodie, Z., 2013. Investments. McGraw-Hill.

Bradford, W., Chen, C. and Zhu, S., 2013. Cash dividend policy, corporate pyramids, and

ownership structure: Evidence from China. International Review of Economics &

Finance, 27, pp.445-464.

Brealey, R., Myers, S.C. and Marcus, A.J., 2007. FundamentalsofCorporate Finance. Mc

Graw Hill, New York.

Breuer, W., Rieger, M.O. and Soypak, K.C., 2014. The behavioral foundations of corporate

dividend policy a cross-country analysis. Journal of Banking & Finance, 42, pp.247-265.

CORREIA, C. et al. 2013. Financial Management. 7th Edition. Cape Town: Juta

andCompany Ltd.2.

Davies, T. and Crawford, I., 2011. Business accounting and finance. Pearson.

DEEPTEE, P. and ROSHAN, B. 2009. Signaling Power of Dividends on firms futureProfits

A Literature Review. Evergreen Energy- Interdisciplinary Journal, pp.1-9.

FIRER, C. et al. 2012. Fundamentals of Corporate Finance. 5th Edition.Berkshire.McGraw-

Hill Companies, Inc.

Hillier, D., Grinblatt, M. and Titman, S., 2011. Financial markets and corporate strategy.

McGraw Hill.

Masum, A.A., 2014. Dividend policy and its impact on stock price–A study on commercial

banks listed in Dhaka stock exchange.

10

References:

Baker, H.K. and Weigand, R., 2015. Corporate dividend policy revisited. Managerial

Finance, 41(2), pp.126-144.

Barman, G.P., 2008. An evaluation of how dividend policies impact on the share value of

selected companies.

Bodie, Z., 2013. Investments. McGraw-Hill.

Bradford, W., Chen, C. and Zhu, S., 2013. Cash dividend policy, corporate pyramids, and

ownership structure: Evidence from China. International Review of Economics &

Finance, 27, pp.445-464.

Brealey, R., Myers, S.C. and Marcus, A.J., 2007. FundamentalsofCorporate Finance. Mc

Graw Hill, New York.

Breuer, W., Rieger, M.O. and Soypak, K.C., 2014. The behavioral foundations of corporate

dividend policy a cross-country analysis. Journal of Banking & Finance, 42, pp.247-265.

CORREIA, C. et al. 2013. Financial Management. 7th Edition. Cape Town: Juta

andCompany Ltd.2.

Davies, T. and Crawford, I., 2011. Business accounting and finance. Pearson.

DEEPTEE, P. and ROSHAN, B. 2009. Signaling Power of Dividends on firms futureProfits

A Literature Review. Evergreen Energy- Interdisciplinary Journal, pp.1-9.

FIRER, C. et al. 2012. Fundamentals of Corporate Finance. 5th Edition.Berkshire.McGraw-

Hill Companies, Inc.

Hillier, D., Grinblatt, M. and Titman, S., 2011. Financial markets and corporate strategy.

McGraw Hill.

Masum, A.A., 2014. Dividend policy and its impact on stock price–A study on commercial

banks listed in Dhaka stock exchange.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Finance

11

Naser, K., Nuseibeh, R. and Rashed, W., 2013. Managers' perception of dividend policy:

Evidence from companies listed on Abu Dhabi Securities Exchange. Issues in Business

Management and Economics, 1(1), pp.001-012.

Shao, L., Kwok, C.C. and Guedhami, O., 2013. DIVIDEND POLICY: BALANCING

SHAREHOLDERS'AND CREDITORS'INTERESTS. Journal of Financial Research, 36(1),

pp.43-66.

STEEN, E. et al. 2012. stakeholder conflicts and dividend

policy. Journal of Banking & Finance, 36 pp. 2852-2864

Thanatawee, Y., 2013. Ownership structure and dividend policy: Evidence from Thailand.

Travlos, N.G., Trigeorgis, L. and Vafeas, N., 2015. Shareholder wealth effects of dividend

policy changes in an emerging stock market: The case of Cyprus.

Tucker, J.W., 2011. Selection bias and econometric remedies in accounting and finance

research.

Zhang, D., 2012. Managerial dividend-paying incentives. Erasmus University Rotterdam.

11

Naser, K., Nuseibeh, R. and Rashed, W., 2013. Managers' perception of dividend policy:

Evidence from companies listed on Abu Dhabi Securities Exchange. Issues in Business

Management and Economics, 1(1), pp.001-012.

Shao, L., Kwok, C.C. and Guedhami, O., 2013. DIVIDEND POLICY: BALANCING

SHAREHOLDERS'AND CREDITORS'INTERESTS. Journal of Financial Research, 36(1),

pp.43-66.

STEEN, E. et al. 2012. stakeholder conflicts and dividend

policy. Journal of Banking & Finance, 36 pp. 2852-2864

Thanatawee, Y., 2013. Ownership structure and dividend policy: Evidence from Thailand.

Travlos, N.G., Trigeorgis, L. and Vafeas, N., 2015. Shareholder wealth effects of dividend

policy changes in an emerging stock market: The case of Cyprus.

Tucker, J.W., 2011. Selection bias and econometric remedies in accounting and finance

research.

Zhang, D., 2012. Managerial dividend-paying incentives. Erasmus University Rotterdam.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.