Shell Investment Analysis

VerifiedAdded on 2020/05/28

|12

|1720

|90

AI Summary

The assignment delves into a comprehensive analysis of investment opportunities within Royal Dutch Shell. It examines the company's financial performance, specifically focusing on key metrics such as net present value (NPV) and internal rate of return (IRR). The report aims to determine the viability and profitability of potential investments in Shell, providing insights for decision-making regarding resource allocation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Corporate Finance

1

Project Report: Corporate Finance

1

Project Report: Corporate Finance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Finance

2

Part 2: Company Perspective

Background:

Woodside petroleum limited is an exploration and manufacturing company. This

company is operating its business in Australian market. Woodside petroleum has the largest

share in the gas and oil exploration industry of Australia. Head office of this company is

situated is at Perth in Australia. This company has registered its stock in stock exchange of

Australia. The main operations of this company are to exploration and deliver the oil and gas

products in the Australian market. Various mines are owned by the company in Australia

itself (Home, 2018). This company has most of the natural gas projects in Australia. 13.5%

share of oil and gas exploration industry is held by Woodside petroleum limited only. This

market share is the highest in the Australian market.

Oil and gas exploration industry of Australia is one of the largest industries in ASX.

This industry contributes 2.58% in the total GDP of the country. The current reports and the

future trends of oil and gas exploration industry of Australia explains that the company has

faced few losses in last year due to natural and environment factor and future trend explains

that the firms in oil and gas industry must run the business though concerning about natural

aspects (Annual report, 2018).

The main key opportunity of Woodside petroleum limited is high technology of which

would assist the organization to grab more market share. Through the help of technology,

international project could also be owned by the company and the mission of the company

could be accomplished. On the other hand, huge competition at international level is the main

threat of the company and the bad relations of the company with its stakeholders would also

impact over the performance of the company. Thus the company is required to manage the

threats by identifying and taking a better step at fair time.

Cash conversion cycle:

Cash conversion cycle (CCC) is a financial analysis process which is used by the

companies, management and the professionals to evaluate the cash turnover of the company.

It directly impacts over the liquidity and working capital management position of the

company. Cash conversion cycle calculations express about the total time in which the cash

2

Part 2: Company Perspective

Background:

Woodside petroleum limited is an exploration and manufacturing company. This

company is operating its business in Australian market. Woodside petroleum has the largest

share in the gas and oil exploration industry of Australia. Head office of this company is

situated is at Perth in Australia. This company has registered its stock in stock exchange of

Australia. The main operations of this company are to exploration and deliver the oil and gas

products in the Australian market. Various mines are owned by the company in Australia

itself (Home, 2018). This company has most of the natural gas projects in Australia. 13.5%

share of oil and gas exploration industry is held by Woodside petroleum limited only. This

market share is the highest in the Australian market.

Oil and gas exploration industry of Australia is one of the largest industries in ASX.

This industry contributes 2.58% in the total GDP of the country. The current reports and the

future trends of oil and gas exploration industry of Australia explains that the company has

faced few losses in last year due to natural and environment factor and future trend explains

that the firms in oil and gas industry must run the business though concerning about natural

aspects (Annual report, 2018).

The main key opportunity of Woodside petroleum limited is high technology of which

would assist the organization to grab more market share. Through the help of technology,

international project could also be owned by the company and the mission of the company

could be accomplished. On the other hand, huge competition at international level is the main

threat of the company and the bad relations of the company with its stakeholders would also

impact over the performance of the company. Thus the company is required to manage the

threats by identifying and taking a better step at fair time.

Cash conversion cycle:

Cash conversion cycle (CCC) is a financial analysis process which is used by the

companies, management and the professionals to evaluate the cash turnover of the company.

It directly impacts over the liquidity and working capital management position of the

company. Cash conversion cycle calculations express about the total time in which the cash

Corporate Finance

3

of the company would be get back. Below table express about the cash conversion cycle of

last 2 years:

Calculation of cash conversion cycle of 2016

Sales

£

4,075

COGS

£

2,234

Inventor

ies

£

5

AR

£

172

AP

£

546

Days/

year 365

Cash conversion

cycle (CCC) =

Inventory

conversion period +

Receivables

collection

period

-

Payables

deferral period

=

Inventory/Sales per

day +

AR/Sales per

day -

AP/COGS per

day

= 0.45 +

15.4

1 - 48.91

= 33.05 days

Calculation of cash conversion cycle of 2015

Sales

£

5,030

COGS

£

3,073

Inventor

ies

£

19

AR

£

93

AP

£

813

Days/

year 365

3

of the company would be get back. Below table express about the cash conversion cycle of

last 2 years:

Calculation of cash conversion cycle of 2016

Sales

£

4,075

COGS

£

2,234

Inventor

ies

£

5

AR

£

172

AP

£

546

Days/

year 365

Cash conversion

cycle (CCC) =

Inventory

conversion period +

Receivables

collection

period

-

Payables

deferral period

=

Inventory/Sales per

day +

AR/Sales per

day -

AP/COGS per

day

= 0.45 +

15.4

1 - 48.91

= 33.05 days

Calculation of cash conversion cycle of 2015

Sales

£

5,030

COGS

£

3,073

Inventor

ies

£

19

AR

£

93

AP

£

813

Days/

year 365

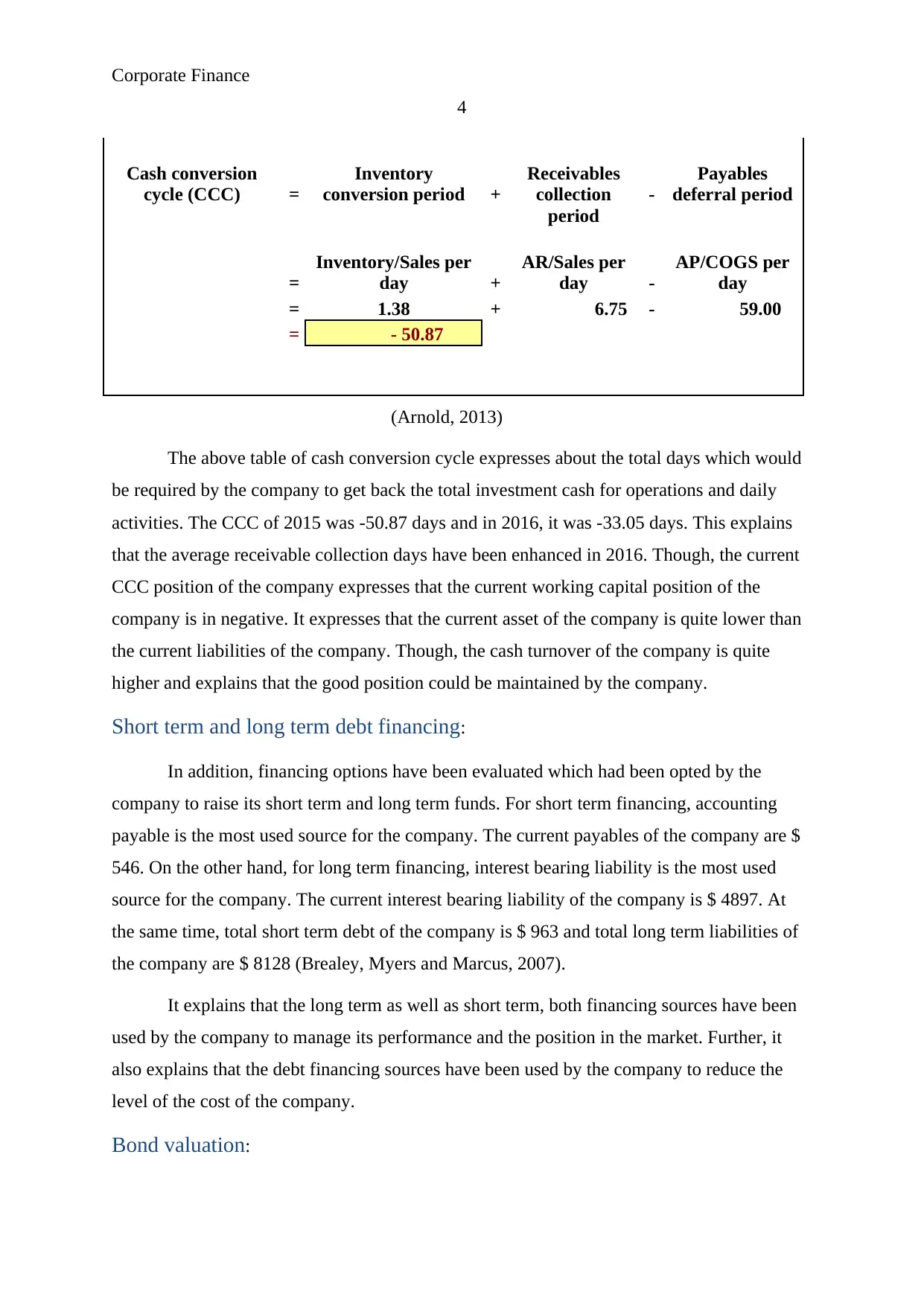

Corporate Finance

4

Cash conversion

cycle (CCC) =

Inventory

conversion period +

Receivables

collection

period

-

Payables

deferral period

=

Inventory/Sales per

day +

AR/Sales per

day -

AP/COGS per

day

= 1.38 + 6.75 - 59.00

= - 50.87

(Arnold, 2013)

The above table of cash conversion cycle expresses about the total days which would

be required by the company to get back the total investment cash for operations and daily

activities. The CCC of 2015 was -50.87 days and in 2016, it was -33.05 days. This explains

that the average receivable collection days have been enhanced in 2016. Though, the current

CCC position of the company expresses that the current working capital position of the

company is in negative. It expresses that the current asset of the company is quite lower than

the current liabilities of the company. Though, the cash turnover of the company is quite

higher and explains that the good position could be maintained by the company.

Short term and long term debt financing:

In addition, financing options have been evaluated which had been opted by the

company to raise its short term and long term funds. For short term financing, accounting

payable is the most used source for the company. The current payables of the company are $

546. On the other hand, for long term financing, interest bearing liability is the most used

source for the company. The current interest bearing liability of the company is $ 4897. At

the same time, total short term debt of the company is $ 963 and total long term liabilities of

the company are $ 8128 (Brealey, Myers and Marcus, 2007).

It explains that the long term as well as short term, both financing sources have been

used by the company to manage its performance and the position in the market. Further, it

also explains that the debt financing sources have been used by the company to reduce the

level of the cost of the company.

Bond valuation:

4

Cash conversion

cycle (CCC) =

Inventory

conversion period +

Receivables

collection

period

-

Payables

deferral period

=

Inventory/Sales per

day +

AR/Sales per

day -

AP/COGS per

day

= 1.38 + 6.75 - 59.00

= - 50.87

(Arnold, 2013)

The above table of cash conversion cycle expresses about the total days which would

be required by the company to get back the total investment cash for operations and daily

activities. The CCC of 2015 was -50.87 days and in 2016, it was -33.05 days. This explains

that the average receivable collection days have been enhanced in 2016. Though, the current

CCC position of the company expresses that the current working capital position of the

company is in negative. It expresses that the current asset of the company is quite lower than

the current liabilities of the company. Though, the cash turnover of the company is quite

higher and explains that the good position could be maintained by the company.

Short term and long term debt financing:

In addition, financing options have been evaluated which had been opted by the

company to raise its short term and long term funds. For short term financing, accounting

payable is the most used source for the company. The current payables of the company are $

546. On the other hand, for long term financing, interest bearing liability is the most used

source for the company. The current interest bearing liability of the company is $ 4897. At

the same time, total short term debt of the company is $ 963 and total long term liabilities of

the company are $ 8128 (Brealey, Myers and Marcus, 2007).

It explains that the long term as well as short term, both financing sources have been

used by the company to manage its performance and the position in the market. Further, it

also explains that the debt financing sources have been used by the company to reduce the

level of the cost of the company.

Bond valuation:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Finance

5

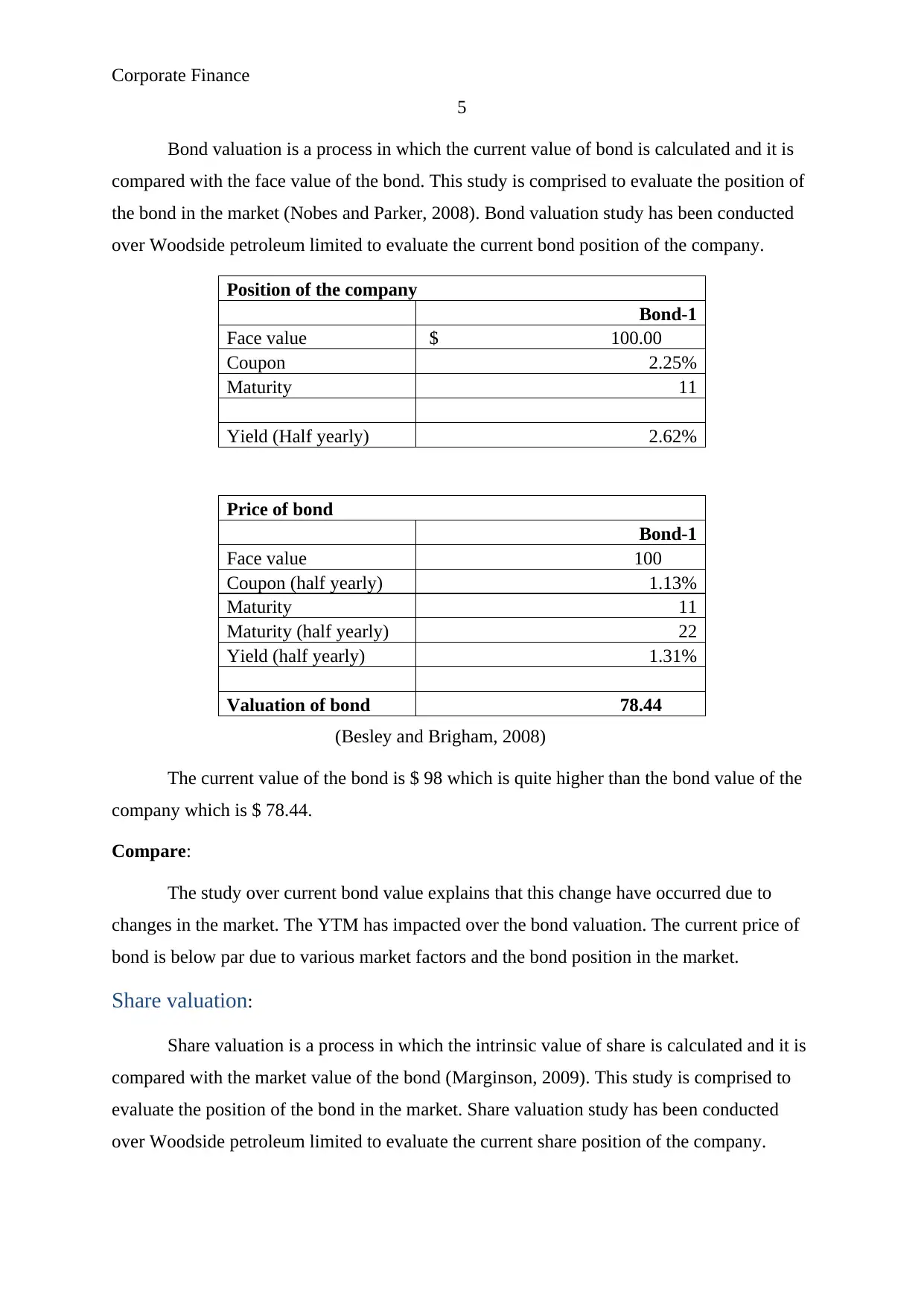

Bond valuation is a process in which the current value of bond is calculated and it is

compared with the face value of the bond. This study is comprised to evaluate the position of

the bond in the market (Nobes and Parker, 2008). Bond valuation study has been conducted

over Woodside petroleum limited to evaluate the current bond position of the company.

Position of the company

Bond-1

Face value $ 100.00

Coupon 2.25%

Maturity 11

Yield (Half yearly) 2.62%

Price of bond

Bond-1

Face value 100

Coupon (half yearly) 1.13%

Maturity 11

Maturity (half yearly) 22

Yield (half yearly) 1.31%

Valuation of bond 78.44

(Besley and Brigham, 2008)

The current value of the bond is $ 98 which is quite higher than the bond value of the

company which is $ 78.44.

Compare:

The study over current bond value explains that this change have occurred due to

changes in the market. The YTM has impacted over the bond valuation. The current price of

bond is below par due to various market factors and the bond position in the market.

Share valuation:

Share valuation is a process in which the intrinsic value of share is calculated and it is

compared with the market value of the bond (Marginson, 2009). This study is comprised to

evaluate the position of the bond in the market. Share valuation study has been conducted

over Woodside petroleum limited to evaluate the current share position of the company.

5

Bond valuation is a process in which the current value of bond is calculated and it is

compared with the face value of the bond. This study is comprised to evaluate the position of

the bond in the market (Nobes and Parker, 2008). Bond valuation study has been conducted

over Woodside petroleum limited to evaluate the current bond position of the company.

Position of the company

Bond-1

Face value $ 100.00

Coupon 2.25%

Maturity 11

Yield (Half yearly) 2.62%

Price of bond

Bond-1

Face value 100

Coupon (half yearly) 1.13%

Maturity 11

Maturity (half yearly) 22

Yield (half yearly) 1.31%

Valuation of bond 78.44

(Besley and Brigham, 2008)

The current value of the bond is $ 98 which is quite higher than the bond value of the

company which is $ 78.44.

Compare:

The study over current bond value explains that this change have occurred due to

changes in the market. The YTM has impacted over the bond valuation. The current price of

bond is below par due to various market factors and the bond position in the market.

Share valuation:

Share valuation is a process in which the intrinsic value of share is calculated and it is

compared with the market value of the bond (Marginson, 2009). This study is comprised to

evaluate the position of the bond in the market. Share valuation study has been conducted

over Woodside petroleum limited to evaluate the current share position of the company.

Corporate Finance

6

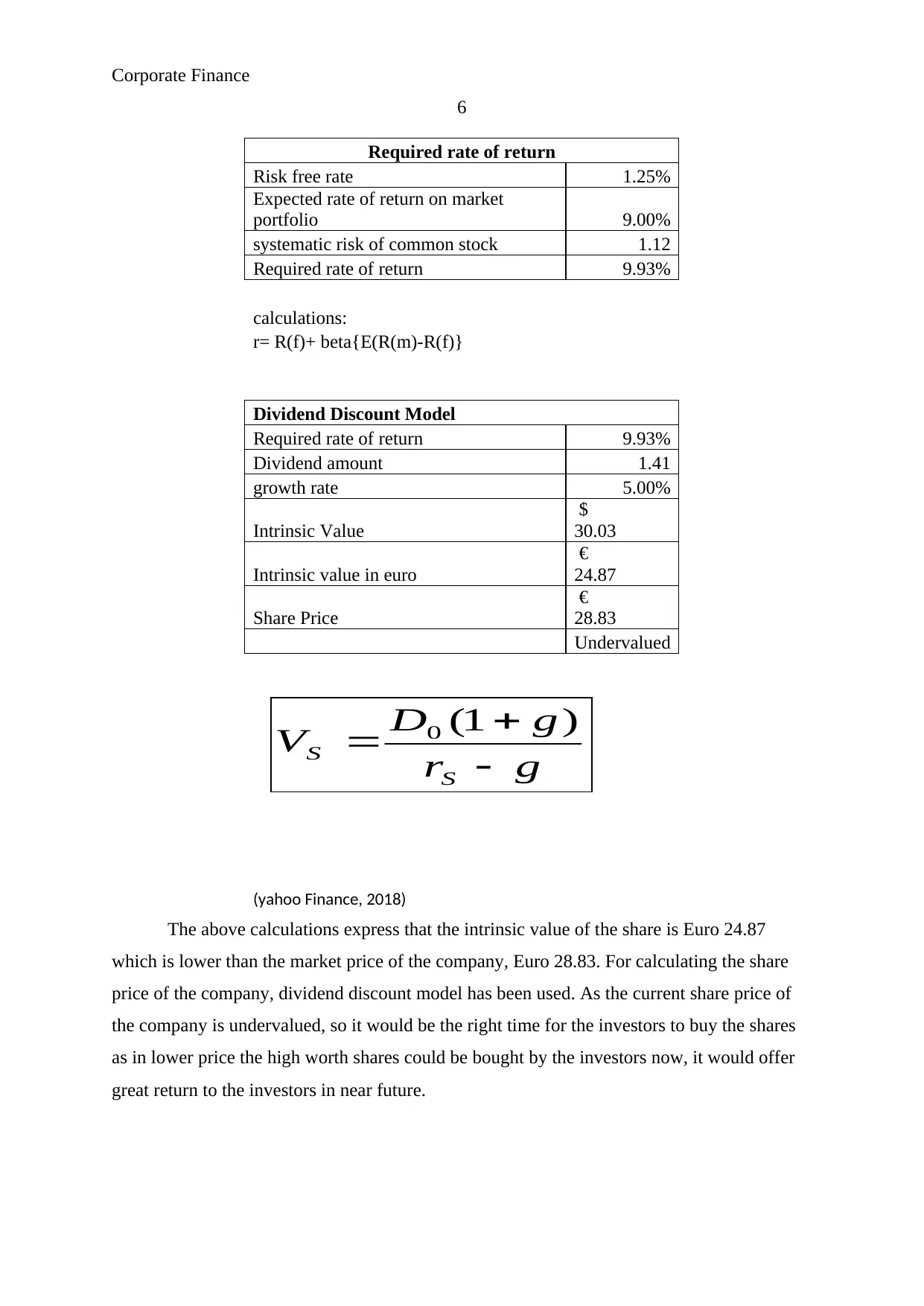

Required rate of return

Risk free rate 1.25%

Expected rate of return on market

portfolio 9.00%

systematic risk of common stock 1.12

Required rate of return 9.93%

calculations:

r= R(f)+ beta{E(R(m)-R(f)}

Dividend Discount Model

Required rate of return 9.93%

Dividend amount 1.41

growth rate 5.00%

Intrinsic Value

$

30.03

Intrinsic value in euro

€

24.87

Share Price

€

28.83

Undervalued

(yahoo Finance, 2018)

The above calculations express that the intrinsic value of the share is Euro 24.87

which is lower than the market price of the company, Euro 28.83. For calculating the share

price of the company, dividend discount model has been used. As the current share price of

the company is undervalued, so it would be the right time for the investors to buy the shares

as in lower price the high worth shares could be bought by the investors now, it would offer

great return to the investors in near future.

gr

gD

V

S

S

)1(0

6

Required rate of return

Risk free rate 1.25%

Expected rate of return on market

portfolio 9.00%

systematic risk of common stock 1.12

Required rate of return 9.93%

calculations:

r= R(f)+ beta{E(R(m)-R(f)}

Dividend Discount Model

Required rate of return 9.93%

Dividend amount 1.41

growth rate 5.00%

Intrinsic Value

$

30.03

Intrinsic value in euro

€

24.87

Share Price

€

28.83

Undervalued

(yahoo Finance, 2018)

The above calculations express that the intrinsic value of the share is Euro 24.87

which is lower than the market price of the company, Euro 28.83. For calculating the share

price of the company, dividend discount model has been used. As the current share price of

the company is undervalued, so it would be the right time for the investors to buy the shares

as in lower price the high worth shares could be bought by the investors now, it would offer

great return to the investors in near future.

gr

gD

V

S

S

)1(0

Corporate Finance

7

Part 3: Capital Budgeting

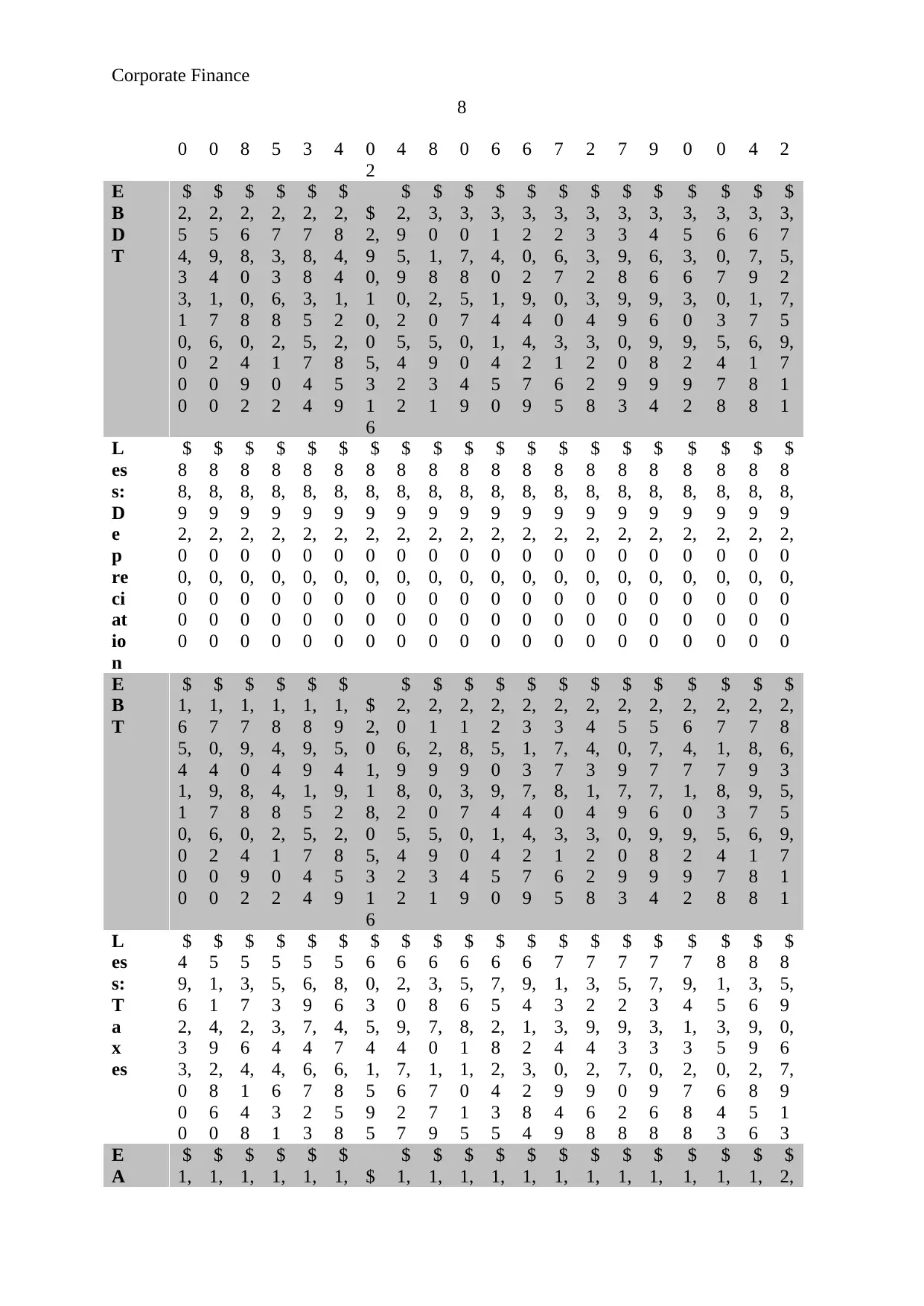

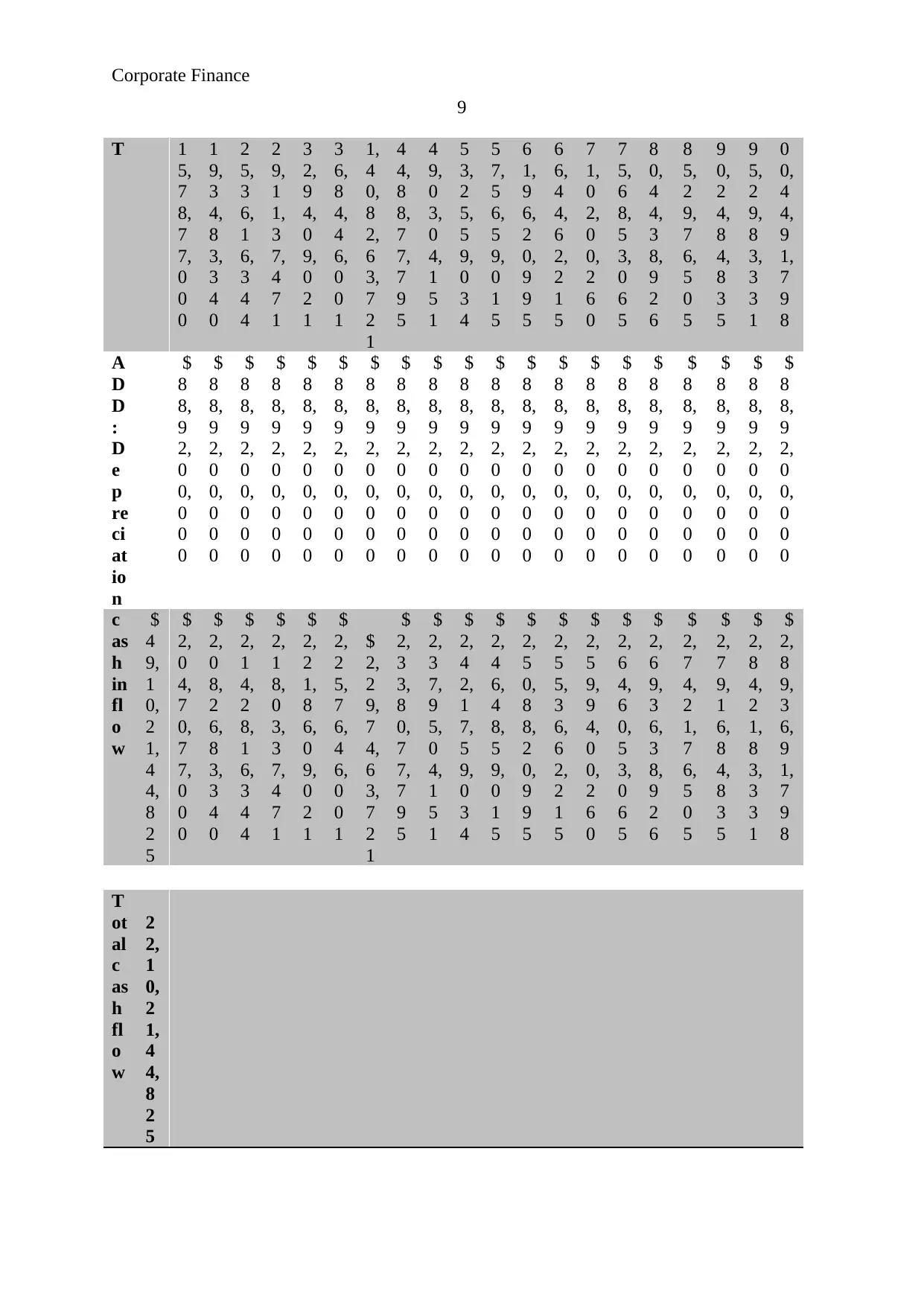

Free cash flows:

Free cash flows brief about the total cash inflow of a company (Phillips and

Stawarski, 2016). Following is the free cash flow of investment opportunity of Shell:

Project A

Y

e

a

r

1

Y

e

a

r

2

Y

e

a

r

3

Y

e

a

r

4

Y

e

a

r

5

Y

e

a

r

6

Y

e

a

r

7

Y

e

a

r

8

Y

e

a

r

9

Y

e

a

r

1

0

Y

e

a

r

1

1

Y

e

a

r

1

2

Y

e

a

r

1

3

Y

e

a

r

1

4

Y

e

a

r

1

5

Y

e

a

r

1

6

Y

e

a

r

1

7

Y

e

a

r

1

8

Y

e

a

r

1

9

Y

e

a

r

2

0

I

ni

ti

al

O

ut

la

y

$

2

7,

0

0,

0

0,

0

0,

0

0

0

R

e

v

e

n

u

es

$

3,

6

3,

3

3,

0

0,

0

0

0

$

3,

7

0,

5

9,

6

6,

0

0

0

$

3,

7

8,

0

0,

8

5,

3

2

0

$

3,

8

5,

5

6,

8

7,

0

2

6

$

3,

9

3,

2

8,

0

0,

7

6

7

$

4,

0

1,

1

4,

5

6,

7

8

2

$

4,

0

9,

1

6,

8

5,

9

1

8

$

4,

1

7,

3

5,

1

9,

6

3

6

$

4,

2

5,

6

9,

9

0,

0

2

9

$

4,

3

4,

2

1,

2

9,

8

3

0

$

4,

4

2,

8

9,

7

2,

4

2

6

$

4,

5

1,

7

5,

5

1,

8

7

5

$

4,

6

0,

7

9,

0

2,

9

1

2

$

4,

7

0,

0

0,

6

0,

9

7

0

$

4,

7

9,

4

0,

6

2,

1

9

0

$

4,

8

8,

9

9,

4

3,

4

3

4

$

4,

9

8,

7

7,

4

2,

3

0

2

$

5,

0

8,

7

4,

9

7,

1

4

8

$

5,

1

8,

9

2,

4

7,

0

9

1

$

5,

2

9,

3

0,

3

2,

0

3

3

E

x

p

e

n

se

s

$

1,

0

8,

9

9,

9

0,

0

0

$

1,

1

1,

1

7,

8

9,

8

0

$

1,

1

0,

0

0,

0

4,

8

2

$

1,

1

2,

2

0,

0

4,

9

2

$

1,

1

4,

4

4,

4

5,

0

2

$

1,

1

6,

7

3,

3

3,

9

2

$

1,

1

9,

0

6,

8

0,

6

$

1,

2

1,

4

4,

9

4,

2

1

$

1,

2

3,

8

7,

8

4,

0

9

$

1,

2

6,

3

5,

5

9,

7

8

$

1,

2

8,

8

8,

3

0,

9

7

$

1,

3

1,

4

6,

0

7,

5

9

$

1,

3

4,

0

8,

9

9,

7

4

$

1,

3

6,

7

7,

1

7,

7

4

$

1,

3

9,

5

0,

7

2,

0

9

$

1,

4

2,

2

9,

7

3,

5

3

$

1,

4

5,

1

4,

3

3,

0

1

$

1,

4

8,

0

4,

6

1,

6

7

$

1,

5

1,

0

0,

7

0,

9

0

$

1,

5

4,

0

2,

7

2,

3

2

7

Part 3: Capital Budgeting

Free cash flows:

Free cash flows brief about the total cash inflow of a company (Phillips and

Stawarski, 2016). Following is the free cash flow of investment opportunity of Shell:

Project A

Y

e

a

r

1

Y

e

a

r

2

Y

e

a

r

3

Y

e

a

r

4

Y

e

a

r

5

Y

e

a

r

6

Y

e

a

r

7

Y

e

a

r

8

Y

e

a

r

9

Y

e

a

r

1

0

Y

e

a

r

1

1

Y

e

a

r

1

2

Y

e

a

r

1

3

Y

e

a

r

1

4

Y

e

a

r

1

5

Y

e

a

r

1

6

Y

e

a

r

1

7

Y

e

a

r

1

8

Y

e

a

r

1

9

Y

e

a

r

2

0

I

ni

ti

al

O

ut

la

y

$

2

7,

0

0,

0

0,

0

0,

0

0

0

R

e

v

e

n

u

es

$

3,

6

3,

3

3,

0

0,

0

0

0

$

3,

7

0,

5

9,

6

6,

0

0

0

$

3,

7

8,

0

0,

8

5,

3

2

0

$

3,

8

5,

5

6,

8

7,

0

2

6

$

3,

9

3,

2

8,

0

0,

7

6

7

$

4,

0

1,

1

4,

5

6,

7

8

2

$

4,

0

9,

1

6,

8

5,

9

1

8

$

4,

1

7,

3

5,

1

9,

6

3

6

$

4,

2

5,

6

9,

9

0,

0

2

9

$

4,

3

4,

2

1,

2

9,

8

3

0

$

4,

4

2,

8

9,

7

2,

4

2

6

$

4,

5

1,

7

5,

5

1,

8

7

5

$

4,

6

0,

7

9,

0

2,

9

1

2

$

4,

7

0,

0

0,

6

0,

9

7

0

$

4,

7

9,

4

0,

6

2,

1

9

0

$

4,

8

8,

9

9,

4

3,

4

3

4

$

4,

9

8,

7

7,

4

2,

3

0

2

$

5,

0

8,

7

4,

9

7,

1

4

8

$

5,

1

8,

9

2,

4

7,

0

9

1

$

5,

2

9,

3

0,

3

2,

0

3

3

E

x

p

e

n

se

s

$

1,

0

8,

9

9,

9

0,

0

0

$

1,

1

1,

1

7,

8

9,

8

0

$

1,

1

0,

0

0,

0

4,

8

2

$

1,

1

2,

2

0,

0

4,

9

2

$

1,

1

4,

4

4,

4

5,

0

2

$

1,

1

6,

7

3,

3

3,

9

2

$

1,

1

9,

0

6,

8

0,

6

$

1,

2

1,

4

4,

9

4,

2

1

$

1,

2

3,

8

7,

8

4,

0

9

$

1,

2

6,

3

5,

5

9,

7

8

$

1,

2

8,

8

8,

3

0,

9

7

$

1,

3

1,

4

6,

0

7,

5

9

$

1,

3

4,

0

8,

9

9,

7

4

$

1,

3

6,

7

7,

1

7,

7

4

$

1,

3

9,

5

0,

7

2,

0

9

$

1,

4

2,

2

9,

7

3,

5

3

$

1,

4

5,

1

4,

3

3,

0

1

$

1,

4

8,

0

4,

6

1,

6

7

$

1,

5

1,

0

0,

7

0,

9

0

$

1,

5

4,

0

2,

7

2,

3

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Finance

8

0 0 8 5 3 4 0

2

4 8 0 6 6 7 2 7 9 0 0 4 2

E

B

D

T

$

2,

5

4,

3

3,

1

0,

0

0

0

$

2,

5

9,

4

1,

7

6,

2

0

0

$

2,

6

8,

0

0,

8

0,

4

9

2

$

2,

7

3,

3

6,

8

2,

1

0

2

$

2,

7

8,

8

3,

5

5,

7

4

4

$

2,

8

4,

4

1,

2

2,

8

5

9

$

2,

9

0,

1

0,

0

5,

3

1

6

$

2,

9

5,

9

0,

2

5,

4

2

2

$

3,

0

1,

8

2,

0

5,

9

3

1

$

3,

0

7,

8

5,

7

0,

0

4

9

$

3,

1

4,

0

1,

4

1,

4

5

0

$

3,

2

0,

2

9,

4

4,

2

7

9

$

3,

2

6,

7

0,

0

3,

1

6

5

$

3,

3

3,

2

3,

4

3,

2

2

8

$

3,

3

9,

8

9,

9

0,

0

9

3

$

3,

4

6,

6

9,

6

9,

8

9

4

$

3,

5

3,

6

3,

0

9,

2

9

2

$

3,

6

0,

7

0,

3

5,

4

7

8

$

3,

6

7,

9

1,

7

6,

1

8

8

$

3,

7

5,

2

7,

5

9,

7

1

1

L

es

s:

D

e

p

re

ci

at

io

n

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

E

B

T

$

1,

6

5,

4

1,

1

0,

0

0

0

$

1,

7

0,

4

9,

7

6,

2

0

0

$

1,

7

9,

0

8,

8

0,

4

9

2

$

1,

8

4,

4

4,

8

2,

1

0

2

$

1,

8

9,

9

1,

5

5,

7

4

4

$

1,

9

5,

4

9,

2

2,

8

5

9

$

2,

0

1,

1

8,

0

5,

3

1

6

$

2,

0

6,

9

8,

2

5,

4

2

2

$

2,

1

2,

9

0,

0

5,

9

3

1

$

2,

1

8,

9

3,

7

0,

0

4

9

$

2,

2

5,

0

9,

4

1,

4

5

0

$

2,

3

1,

3

7,

4

4,

2

7

9

$

2,

3

7,

7

8,

0

3,

1

6

5

$

2,

4

4,

3

1,

4

3,

2

2

8

$

2,

5

0,

9

7,

9

0,

0

9

3

$

2,

5

7,

7

7,

6

9,

8

9

4

$

2,

6

4,

7

1,

0

9,

2

9

2

$

2,

7

1,

7

8,

3

5,

4

7

8

$

2,

7

8,

9

9,

7

6,

1

8

8

$

2,

8

6,

3

5,

5

9,

7

1

1

L

es

s:

T

a

x

es

$

4

9,

6

2,

3

3,

0

0

0

$

5

1,

1

4,

9

2,

8

6

0

$

5

3,

7

2,

6

4,

1

4

8

$

5

5,

3

3,

4

4,

6

3

1

$

5

6,

9

7,

4

6,

7

2

3

$

5

8,

6

4,

7

6,

8

5

8

$

6

0,

3

5,

4

1,

5

9

5

$

6

2,

0

9,

4

7,

6

2

7

$

6

3,

8

7,

0

1,

7

7

9

$

6

5,

6

8,

1

1,

0

1

5

$

6

7,

5

2,

8

2,

4

3

5

$

6

9,

4

1,

2

3,

2

8

4

$

7

1,

3

3,

4

0,

9

4

9

$

7

3,

2

9,

4

2,

9

6

8

$

7

5,

2

9,

3

7,

0

2

8

$

7

7,

3

3,

3

0,

9

6

8

$

7

9,

4

1,

3

2,

7

8

8

$

8

1,

5

3,

5

0,

6

4

3

$

8

3,

6

9,

9

2,

8

5

6

$

8

5,

9

0,

6

7,

9

1

3

E

A

$

1,

$

1,

$

1,

$

1,

$

1,

$

1, $

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

2,

8

0 0 8 5 3 4 0

2

4 8 0 6 6 7 2 7 9 0 0 4 2

E

B

D

T

$

2,

5

4,

3

3,

1

0,

0

0

0

$

2,

5

9,

4

1,

7

6,

2

0

0

$

2,

6

8,

0

0,

8

0,

4

9

2

$

2,

7

3,

3

6,

8

2,

1

0

2

$

2,

7

8,

8

3,

5

5,

7

4

4

$

2,

8

4,

4

1,

2

2,

8

5

9

$

2,

9

0,

1

0,

0

5,

3

1

6

$

2,

9

5,

9

0,

2

5,

4

2

2

$

3,

0

1,

8

2,

0

5,

9

3

1

$

3,

0

7,

8

5,

7

0,

0

4

9

$

3,

1

4,

0

1,

4

1,

4

5

0

$

3,

2

0,

2

9,

4

4,

2

7

9

$

3,

2

6,

7

0,

0

3,

1

6

5

$

3,

3

3,

2

3,

4

3,

2

2

8

$

3,

3

9,

8

9,

9

0,

0

9

3

$

3,

4

6,

6

9,

6

9,

8

9

4

$

3,

5

3,

6

3,

0

9,

2

9

2

$

3,

6

0,

7

0,

3

5,

4

7

8

$

3,

6

7,

9

1,

7

6,

1

8

8

$

3,

7

5,

2

7,

5

9,

7

1

1

L

es

s:

D

e

p

re

ci

at

io

n

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

E

B

T

$

1,

6

5,

4

1,

1

0,

0

0

0

$

1,

7

0,

4

9,

7

6,

2

0

0

$

1,

7

9,

0

8,

8

0,

4

9

2

$

1,

8

4,

4

4,

8

2,

1

0

2

$

1,

8

9,

9

1,

5

5,

7

4

4

$

1,

9

5,

4

9,

2

2,

8

5

9

$

2,

0

1,

1

8,

0

5,

3

1

6

$

2,

0

6,

9

8,

2

5,

4

2

2

$

2,

1

2,

9

0,

0

5,

9

3

1

$

2,

1

8,

9

3,

7

0,

0

4

9

$

2,

2

5,

0

9,

4

1,

4

5

0

$

2,

3

1,

3

7,

4

4,

2

7

9

$

2,

3

7,

7

8,

0

3,

1

6

5

$

2,

4

4,

3

1,

4

3,

2

2

8

$

2,

5

0,

9

7,

9

0,

0

9

3

$

2,

5

7,

7

7,

6

9,

8

9

4

$

2,

6

4,

7

1,

0

9,

2

9

2

$

2,

7

1,

7

8,

3

5,

4

7

8

$

2,

7

8,

9

9,

7

6,

1

8

8

$

2,

8

6,

3

5,

5

9,

7

1

1

L

es

s:

T

a

x

es

$

4

9,

6

2,

3

3,

0

0

0

$

5

1,

1

4,

9

2,

8

6

0

$

5

3,

7

2,

6

4,

1

4

8

$

5

5,

3

3,

4

4,

6

3

1

$

5

6,

9

7,

4

6,

7

2

3

$

5

8,

6

4,

7

6,

8

5

8

$

6

0,

3

5,

4

1,

5

9

5

$

6

2,

0

9,

4

7,

6

2

7

$

6

3,

8

7,

0

1,

7

7

9

$

6

5,

6

8,

1

1,

0

1

5

$

6

7,

5

2,

8

2,

4

3

5

$

6

9,

4

1,

2

3,

2

8

4

$

7

1,

3

3,

4

0,

9

4

9

$

7

3,

2

9,

4

2,

9

6

8

$

7

5,

2

9,

3

7,

0

2

8

$

7

7,

3

3,

3

0,

9

6

8

$

7

9,

4

1,

3

2,

7

8

8

$

8

1,

5

3,

5

0,

6

4

3

$

8

3,

6

9,

9

2,

8

5

6

$

8

5,

9

0,

6

7,

9

1

3

E

A

$

1,

$

1,

$

1,

$

1,

$

1,

$

1, $

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

1,

$

2,

Corporate Finance

9

T 1

5,

7

8,

7

7,

0

0

0

1

9,

3

4,

8

3,

3

4

0

2

5,

3

6,

1

6,

3

4

4

2

9,

1

1,

3

7,

4

7

1

3

2,

9

4,

0

9,

0

2

1

3

6,

8

4,

4

6,

0

0

1

1,

4

0,

8

2,

6

3,

7

2

1

4

4,

8

8,

7

7,

7

9

5

4

9,

0

3,

0

4,

1

5

1

5

3,

2

5,

5

9,

0

3

4

5

7,

5

6,

5

9,

0

1

5

6

1,

9

6,

2

0,

9

9

5

6

6,

4

4,

6

2,

2

1

5

7

1,

0

2,

0

0,

2

6

0

7

5,

6

8,

5

3,

0

6

5

8

0,

4

4,

3

8,

9

2

6

8

5,

2

9,

7

6,

5

0

5

9

0,

2

4,

8

4,

8

3

5

9

5,

2

9,

8

3,

3

3

1

0

0,

4

4,

9

1,

7

9

8

A

D

D

:

D

e

p

re

ci

at

io

n

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

c

as

h

in

fl

o

w

$

4

9,

1

0,

2

1,

4

4,

8

2

5

$

2,

0

4,

7

0,

7

7,

0

0

0

$

2,

0

8,

2

6,

8

3,

3

4

0

$

2,

1

4,

2

8,

1

6,

3

4

4

$

2,

1

8,

0

3,

3

7,

4

7

1

$

2,

2

1,

8

6,

0

9,

0

2

1

$

2,

2

5,

7

6,

4

6,

0

0

1

$

2,

2

9,

7

4,

6

3,

7

2

1

$

2,

3

3,

8

0,

7

7,

7

9

5

$

2,

3

7,

9

5,

0

4,

1

5

1

$

2,

4

2,

1

7,

5

9,

0

3

4

$

2,

4

6,

4

8,

5

9,

0

1

5

$

2,

5

0,

8

8,

2

0,

9

9

5

$

2,

5

5,

3

6,

6

2,

2

1

5

$

2,

5

9,

9

4,

0

0,

2

6

0

$

2,

6

4,

6

0,

5

3,

0

6

5

$

2,

6

9,

3

6,

3

8,

9

2

6

$

2,

7

4,

2

1,

7

6,

5

0

5

$

2,

7

9,

1

6,

8

4,

8

3

5

$

2,

8

4,

2

1,

8

3,

3

3

1

$

2,

8

9,

3

6,

9

1,

7

9

8

T

ot

al

c

as

h

fl

o

w

2

2,

1

0,

2

1,

4

4,

8

2

5

9

T 1

5,

7

8,

7

7,

0

0

0

1

9,

3

4,

8

3,

3

4

0

2

5,

3

6,

1

6,

3

4

4

2

9,

1

1,

3

7,

4

7

1

3

2,

9

4,

0

9,

0

2

1

3

6,

8

4,

4

6,

0

0

1

1,

4

0,

8

2,

6

3,

7

2

1

4

4,

8

8,

7

7,

7

9

5

4

9,

0

3,

0

4,

1

5

1

5

3,

2

5,

5

9,

0

3

4

5

7,

5

6,

5

9,

0

1

5

6

1,

9

6,

2

0,

9

9

5

6

6,

4

4,

6

2,

2

1

5

7

1,

0

2,

0

0,

2

6

0

7

5,

6

8,

5

3,

0

6

5

8

0,

4

4,

3

8,

9

2

6

8

5,

2

9,

7

6,

5

0

5

9

0,

2

4,

8

4,

8

3

5

9

5,

2

9,

8

3,

3

3

1

0

0,

4

4,

9

1,

7

9

8

A

D

D

:

D

e

p

re

ci

at

io

n

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

$

8

8,

9

2,

0

0,

0

0

0

c

as

h

in

fl

o

w

$

4

9,

1

0,

2

1,

4

4,

8

2

5

$

2,

0

4,

7

0,

7

7,

0

0

0

$

2,

0

8,

2

6,

8

3,

3

4

0

$

2,

1

4,

2

8,

1

6,

3

4

4

$

2,

1

8,

0

3,

3

7,

4

7

1

$

2,

2

1,

8

6,

0

9,

0

2

1

$

2,

2

5,

7

6,

4

6,

0

0

1

$

2,

2

9,

7

4,

6

3,

7

2

1

$

2,

3

3,

8

0,

7

7,

7

9

5

$

2,

3

7,

9

5,

0

4,

1

5

1

$

2,

4

2,

1

7,

5

9,

0

3

4

$

2,

4

6,

4

8,

5

9,

0

1

5

$

2,

5

0,

8

8,

2

0,

9

9

5

$

2,

5

5,

3

6,

6

2,

2

1

5

$

2,

5

9,

9

4,

0

0,

2

6

0

$

2,

6

4,

6

0,

5

3,

0

6

5

$

2,

6

9,

3

6,

3

8,

9

2

6

$

2,

7

4,

2

1,

7

6,

5

0

5

$

2,

7

9,

1

6,

8

4,

8

3

5

$

2,

8

4,

2

1,

8

3,

3

3

1

$

2,

8

9,

3

6,

9

1,

7

9

8

T

ot

al

c

as

h

fl

o

w

2

2,

1

0,

2

1,

4

4,

8

2

5

Corporate Finance

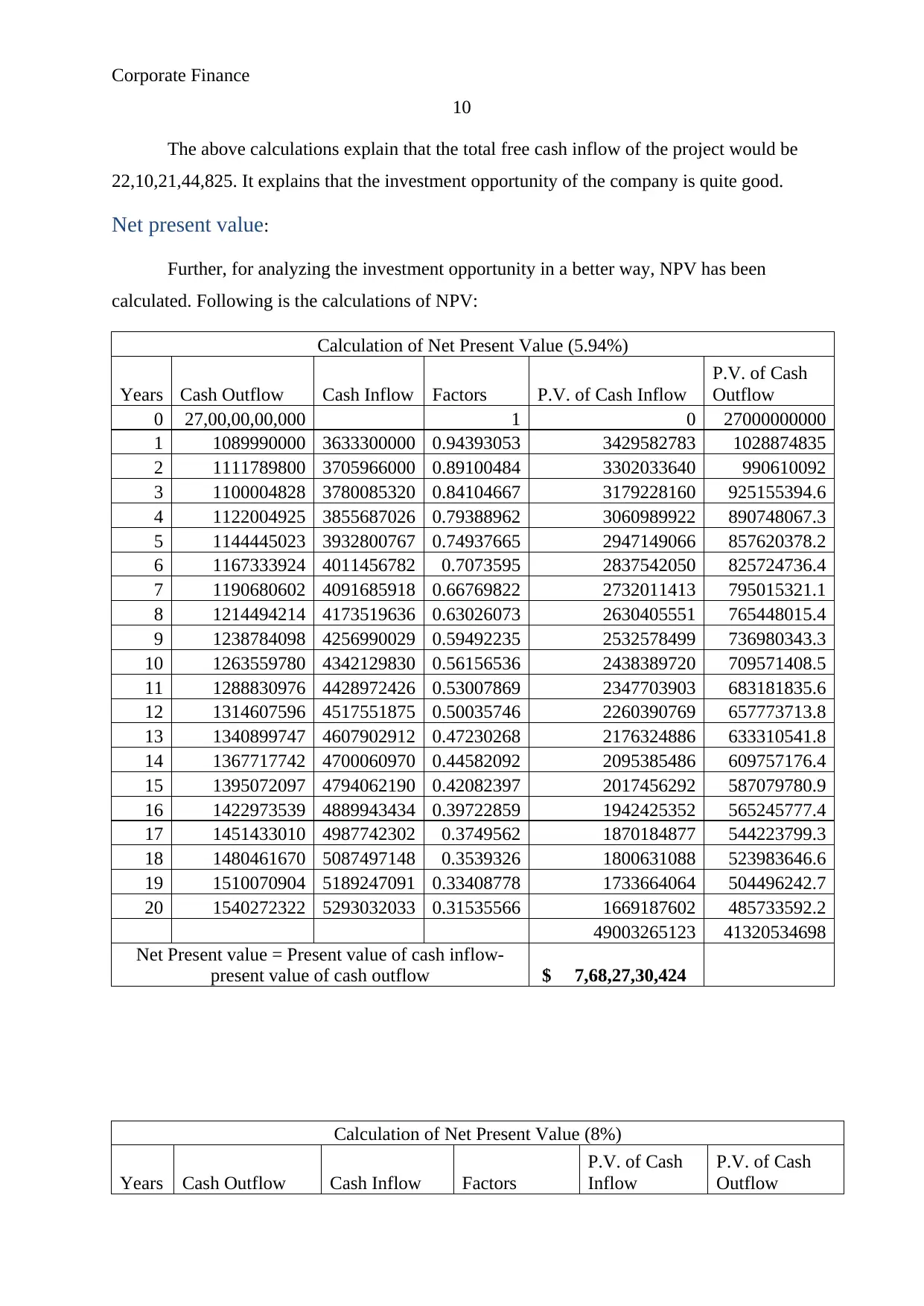

10

The above calculations explain that the total free cash inflow of the project would be

22,10,21,44,825. It explains that the investment opportunity of the company is quite good.

Net present value:

Further, for analyzing the investment opportunity in a better way, NPV has been

calculated. Following is the calculations of NPV:

Calculation of Net Present Value (5.94%)

Years Cash Outflow Cash Inflow Factors P.V. of Cash Inflow

P.V. of Cash

Outflow

0 27,00,00,00,000 1 0 27000000000

1 1089990000 3633300000 0.94393053 3429582783 1028874835

2 1111789800 3705966000 0.89100484 3302033640 990610092

3 1100004828 3780085320 0.84104667 3179228160 925155394.6

4 1122004925 3855687026 0.79388962 3060989922 890748067.3

5 1144445023 3932800767 0.74937665 2947149066 857620378.2

6 1167333924 4011456782 0.7073595 2837542050 825724736.4

7 1190680602 4091685918 0.66769822 2732011413 795015321.1

8 1214494214 4173519636 0.63026073 2630405551 765448015.4

9 1238784098 4256990029 0.59492235 2532578499 736980343.3

10 1263559780 4342129830 0.56156536 2438389720 709571408.5

11 1288830976 4428972426 0.53007869 2347703903 683181835.6

12 1314607596 4517551875 0.50035746 2260390769 657773713.8

13 1340899747 4607902912 0.47230268 2176324886 633310541.8

14 1367717742 4700060970 0.44582092 2095385486 609757176.4

15 1395072097 4794062190 0.42082397 2017456292 587079780.9

16 1422973539 4889943434 0.39722859 1942425352 565245777.4

17 1451433010 4987742302 0.3749562 1870184877 544223799.3

18 1480461670 5087497148 0.3539326 1800631088 523983646.6

19 1510070904 5189247091 0.33408778 1733664064 504496242.7

20 1540272322 5293032033 0.31535566 1669187602 485733592.2

49003265123 41320534698

Net Present value = Present value of cash inflow-

present value of cash outflow $ 7,68,27,30,424

Calculation of Net Present Value (8%)

Years Cash Outflow Cash Inflow Factors

P.V. of Cash

Inflow

P.V. of Cash

Outflow

10

The above calculations explain that the total free cash inflow of the project would be

22,10,21,44,825. It explains that the investment opportunity of the company is quite good.

Net present value:

Further, for analyzing the investment opportunity in a better way, NPV has been

calculated. Following is the calculations of NPV:

Calculation of Net Present Value (5.94%)

Years Cash Outflow Cash Inflow Factors P.V. of Cash Inflow

P.V. of Cash

Outflow

0 27,00,00,00,000 1 0 27000000000

1 1089990000 3633300000 0.94393053 3429582783 1028874835

2 1111789800 3705966000 0.89100484 3302033640 990610092

3 1100004828 3780085320 0.84104667 3179228160 925155394.6

4 1122004925 3855687026 0.79388962 3060989922 890748067.3

5 1144445023 3932800767 0.74937665 2947149066 857620378.2

6 1167333924 4011456782 0.7073595 2837542050 825724736.4

7 1190680602 4091685918 0.66769822 2732011413 795015321.1

8 1214494214 4173519636 0.63026073 2630405551 765448015.4

9 1238784098 4256990029 0.59492235 2532578499 736980343.3

10 1263559780 4342129830 0.56156536 2438389720 709571408.5

11 1288830976 4428972426 0.53007869 2347703903 683181835.6

12 1314607596 4517551875 0.50035746 2260390769 657773713.8

13 1340899747 4607902912 0.47230268 2176324886 633310541.8

14 1367717742 4700060970 0.44582092 2095385486 609757176.4

15 1395072097 4794062190 0.42082397 2017456292 587079780.9

16 1422973539 4889943434 0.39722859 1942425352 565245777.4

17 1451433010 4987742302 0.3749562 1870184877 544223799.3

18 1480461670 5087497148 0.3539326 1800631088 523983646.6

19 1510070904 5189247091 0.33408778 1733664064 504496242.7

20 1540272322 5293032033 0.31535566 1669187602 485733592.2

49003265123 41320534698

Net Present value = Present value of cash inflow-

present value of cash outflow $ 7,68,27,30,424

Calculation of Net Present Value (8%)

Years Cash Outflow Cash Inflow Factors

P.V. of Cash

Inflow

P.V. of Cash

Outflow

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Finance

11

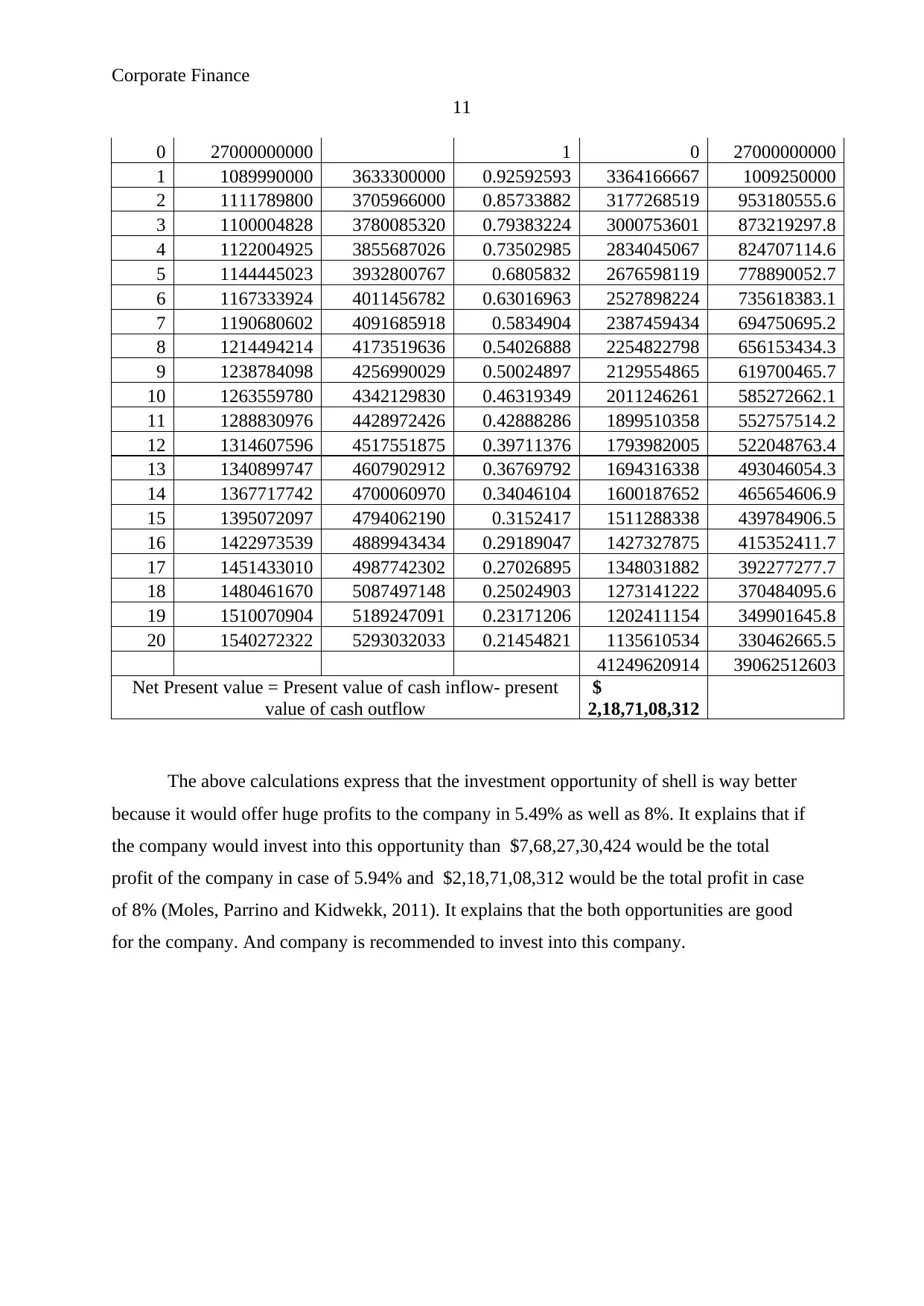

0 27000000000 1 0 27000000000

1 1089990000 3633300000 0.92592593 3364166667 1009250000

2 1111789800 3705966000 0.85733882 3177268519 953180555.6

3 1100004828 3780085320 0.79383224 3000753601 873219297.8

4 1122004925 3855687026 0.73502985 2834045067 824707114.6

5 1144445023 3932800767 0.6805832 2676598119 778890052.7

6 1167333924 4011456782 0.63016963 2527898224 735618383.1

7 1190680602 4091685918 0.5834904 2387459434 694750695.2

8 1214494214 4173519636 0.54026888 2254822798 656153434.3

9 1238784098 4256990029 0.50024897 2129554865 619700465.7

10 1263559780 4342129830 0.46319349 2011246261 585272662.1

11 1288830976 4428972426 0.42888286 1899510358 552757514.2

12 1314607596 4517551875 0.39711376 1793982005 522048763.4

13 1340899747 4607902912 0.36769792 1694316338 493046054.3

14 1367717742 4700060970 0.34046104 1600187652 465654606.9

15 1395072097 4794062190 0.3152417 1511288338 439784906.5

16 1422973539 4889943434 0.29189047 1427327875 415352411.7

17 1451433010 4987742302 0.27026895 1348031882 392277277.7

18 1480461670 5087497148 0.25024903 1273141222 370484095.6

19 1510070904 5189247091 0.23171206 1202411154 349901645.8

20 1540272322 5293032033 0.21454821 1135610534 330462665.5

41249620914 39062512603

Net Present value = Present value of cash inflow- present

value of cash outflow

$

2,18,71,08,312

The above calculations express that the investment opportunity of shell is way better

because it would offer huge profits to the company in 5.49% as well as 8%. It explains that if

the company would invest into this opportunity than $7,68,27,30,424 would be the total

profit of the company in case of 5.94% and $2,18,71,08,312 would be the total profit in case

of 8% (Moles, Parrino and Kidwekk, 2011). It explains that the both opportunities are good

for the company. And company is recommended to invest into this company.

11

0 27000000000 1 0 27000000000

1 1089990000 3633300000 0.92592593 3364166667 1009250000

2 1111789800 3705966000 0.85733882 3177268519 953180555.6

3 1100004828 3780085320 0.79383224 3000753601 873219297.8

4 1122004925 3855687026 0.73502985 2834045067 824707114.6

5 1144445023 3932800767 0.6805832 2676598119 778890052.7

6 1167333924 4011456782 0.63016963 2527898224 735618383.1

7 1190680602 4091685918 0.5834904 2387459434 694750695.2

8 1214494214 4173519636 0.54026888 2254822798 656153434.3

9 1238784098 4256990029 0.50024897 2129554865 619700465.7

10 1263559780 4342129830 0.46319349 2011246261 585272662.1

11 1288830976 4428972426 0.42888286 1899510358 552757514.2

12 1314607596 4517551875 0.39711376 1793982005 522048763.4

13 1340899747 4607902912 0.36769792 1694316338 493046054.3

14 1367717742 4700060970 0.34046104 1600187652 465654606.9

15 1395072097 4794062190 0.3152417 1511288338 439784906.5

16 1422973539 4889943434 0.29189047 1427327875 415352411.7

17 1451433010 4987742302 0.27026895 1348031882 392277277.7

18 1480461670 5087497148 0.25024903 1273141222 370484095.6

19 1510070904 5189247091 0.23171206 1202411154 349901645.8

20 1540272322 5293032033 0.21454821 1135610534 330462665.5

41249620914 39062512603

Net Present value = Present value of cash inflow- present

value of cash outflow

$

2,18,71,08,312

The above calculations express that the investment opportunity of shell is way better

because it would offer huge profits to the company in 5.49% as well as 8%. It explains that if

the company would invest into this opportunity than $7,68,27,30,424 would be the total

profit of the company in case of 5.94% and $2,18,71,08,312 would be the total profit in case

of 8% (Moles, Parrino and Kidwekk, 2011). It explains that the both opportunities are good

for the company. And company is recommended to invest into this company.

Corporate Finance

12

References:

Annual Report. Woodside petroleum limited. Available at

http://www.woodside.com.au/Investors-Media/announcements/Documents/

01.03.2017%20Annual%20Report%202016.pdf [Accessed on 12th Jan 2018].

Arnold, G., 2013. Corporate financial management. Pearson Higher Ed.

Besley, S. and Brigham, E.F., 2008. Essentials of managerial finance. Thomson South-

Western.

Brealey, R., Myers, S.C. and Marcus, A.J., 2007. FundamentalsofCorporate Finance. Mc

Graw Hill, New York.

Home. 2018. Woodside petroleum limited. Available at

http://www.woodside.com.au/Pages/home.aspx [Accessed on 12th Jan 2018].

Marginson, D.E., 2009. Beyond the budgetary control system: towards a two-tiered process

of management control. Management Accounting Research, 10(3), pp.203-230.

Moles, P. Parrino, R and Kidwekk, D,.2011. Corporate finance, European edition, John

Wiley &sons, United Kingdom

Nobes, C. and Parker, R.H., 2008. Comparative international accounting. Pearson Education.

Phillips, P.P. and Stawarski, C.A. 2016. Data Collection: Planning for and Collecting All

Types of Data. John Wiley & Sons.

Yahoo Finance. 2018. Royal Dutch Shell plc. Available at

https://au.finance.yahoo.com/quote/RDSA.AS?p=RDSA.AS [Accessed on 12th Jan 2018].

12

References:

Annual Report. Woodside petroleum limited. Available at

http://www.woodside.com.au/Investors-Media/announcements/Documents/

01.03.2017%20Annual%20Report%202016.pdf [Accessed on 12th Jan 2018].

Arnold, G., 2013. Corporate financial management. Pearson Higher Ed.

Besley, S. and Brigham, E.F., 2008. Essentials of managerial finance. Thomson South-

Western.

Brealey, R., Myers, S.C. and Marcus, A.J., 2007. FundamentalsofCorporate Finance. Mc

Graw Hill, New York.

Home. 2018. Woodside petroleum limited. Available at

http://www.woodside.com.au/Pages/home.aspx [Accessed on 12th Jan 2018].

Marginson, D.E., 2009. Beyond the budgetary control system: towards a two-tiered process

of management control. Management Accounting Research, 10(3), pp.203-230.

Moles, P. Parrino, R and Kidwekk, D,.2011. Corporate finance, European edition, John

Wiley &sons, United Kingdom

Nobes, C. and Parker, R.H., 2008. Comparative international accounting. Pearson Education.

Phillips, P.P. and Stawarski, C.A. 2016. Data Collection: Planning for and Collecting All

Types of Data. John Wiley & Sons.

Yahoo Finance. 2018. Royal Dutch Shell plc. Available at

https://au.finance.yahoo.com/quote/RDSA.AS?p=RDSA.AS [Accessed on 12th Jan 2018].

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.