Ask a question from expert

Project Report Assignment | Corporate Finance Assignment

12 Pages1720 Words90 Views

Added on 2020-05-28

Project Report Assignment | Corporate Finance Assignment

Added on 2020-05-28

BookmarkShareRelated Documents

Running Head: Corporate Finance1Project Report: Corporate Finance

Corporate Finance2Part 2: Company PerspectiveBackground:Woodside petroleum limited is an exploration and manufacturing company. This company is operating its business in Australian market. Woodside petroleum has the largest share in the gas and oil exploration industry of Australia. Head office of this company is situated is at Perth in Australia. This company has registered its stock in stock exchange of Australia. The main operations of this company are to exploration and deliver the oil and gas products in the Australian market. Various mines are owned by the company in Australia itself (Home, 2018). This company has most of the natural gas projects in Australia. 13.5% share of oil and gas exploration industry is held by Woodside petroleum limited only. This market share is the highest in the Australian market. Oil and gas exploration industry of Australia is one of the largest industries in ASX. This industry contributes 2.58% in the total GDP of the country. The current reports and the future trends of oil and gas exploration industry of Australia explains that the company has faced few losses in last year due to natural and environment factor and future trend explains that the firms in oil and gas industry must run the business though concerning about natural aspects (Annual report, 2018). The main key opportunity of Woodside petroleum limited is high technology of whichwould assist the organization to grab more market share. Through the help of technology, international project could also be owned by the company and the mission of the company could be accomplished. On the other hand, huge competition at international level is the mainthreat of the company and the bad relations of the company with its stakeholders would also impact over the performance of the company. Thus the company is required to manage the threats by identifying and taking a better step at fair time.Cash conversion cycle:Cash conversion cycle (CCC) is a financial analysis process which is used by the companies, management and the professionals to evaluate the cash turnover of the company. It directly impacts over the liquidity and working capital management position of the company. Cash conversion cycle calculations express about the total time in which the cash

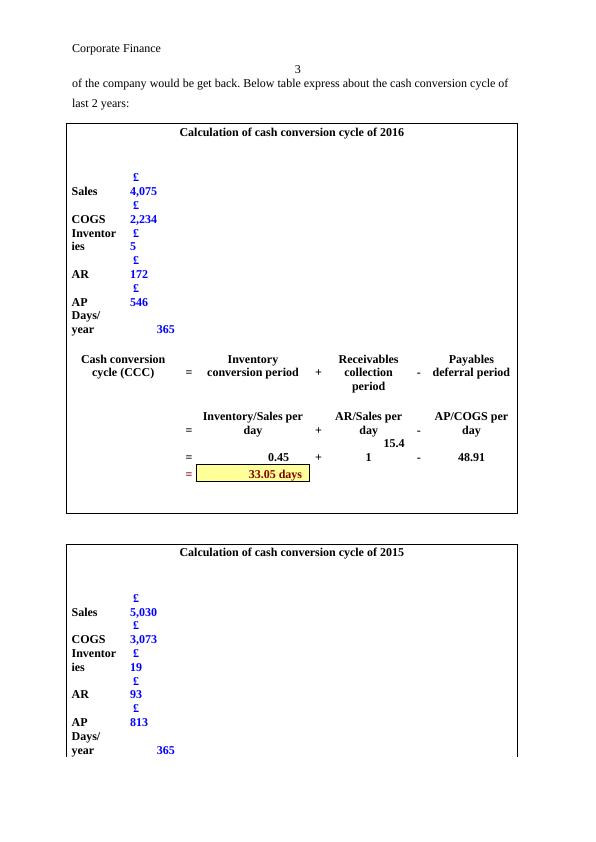

Corporate Finance3of the company would be get back. Below table express about the cash conversion cycle of last 2 years:Calculation of cash conversion cycle of 2016Sales £ 4,075 COGS £ 2,234 Inventories £ 5 AR £ 172 AP £ 546 Days/year365Cash conversioncycle (CCC)=Inventoryconversion period+Receivablescollectionperiod-Payablesdeferral period=Inventory/Sales perday+AR/Sales perday-AP/COGS perday= 0.45 + 15.41 -48.91 = 33.05 daysCalculation of cash conversion cycle of 2015Sales £ 5,030 COGS £ 3,073 Inventories £ 19 AR £ 93 AP £ 813 Days/year365

Corporate Finance4Cash conversioncycle (CCC)=Inventoryconversion period+Receivablescollectionperiod-Payablesdeferral period=Inventory/Sales perday+AR/Sales perday-AP/COGS perday=1.38 + 6.75 - 59.00 = - 50.87 (Arnold, 2013)The above table of cash conversion cycle expresses about the total days which would be required by the company to get back the total investment cash for operations and daily activities. The CCC of 2015 was -50.87 days and in 2016, it was -33.05 days. This explains that the average receivable collection days have been enhanced in 2016. Though, the current CCC position of the company expresses that the current working capital position of the company is in negative. It expresses that the current asset of the company is quite lower than the current liabilities of the company. Though, the cash turnover of the company is quite higher and explains that the good position could be maintained by the company. Short term and long term debt financing:In addition, financing options have been evaluated which had been opted by the company to raise its short term and long term funds. For short term financing, accounting payable is the most used source for the company. The current payables of the company are $ 546. On the other hand, for long term financing, interest bearing liability is the most used source for the company. The current interest bearing liability of the company is $ 4897. At the same time, total short term debt of the company is $ 963 and total long term liabilities of the company are $ 8128 (Brealey, Myers and Marcus, 2007). It explains that the long term as well as short term, both financing sources have been used by the company to manage its performance and the position in the market. Further, it also explains that the debt financing sources have been used by the company to reduce the level of the cost of the company. Bond valuation:

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Finance Assignment- Woodside Petroleum Ltdlg...

|5

|809

|52

FIN203 Corporate Finance Assignment | Woodside Petroleum Ltdlg...

|11

|2049

|76

Analysis of Woodside Petroleum Limitedlg...

|10

|3720

|85

Financial Analysis of Santos Limited: Comparative Analysis with Woodside Petroleumlg...

|14

|2058

|4

Financial Performance of Santos Limited and Woodside Petroleumlg...

|9

|1786

|4

Capital Structure Analysis for Woodside Petroleum Ltdlg...

|15

|4437

|323