Detailed Analysis and Project Report on Cost and Control Job Costing

VerifiedAdded on 2020/04/01

|17

|1831

|37

Project

AI Summary

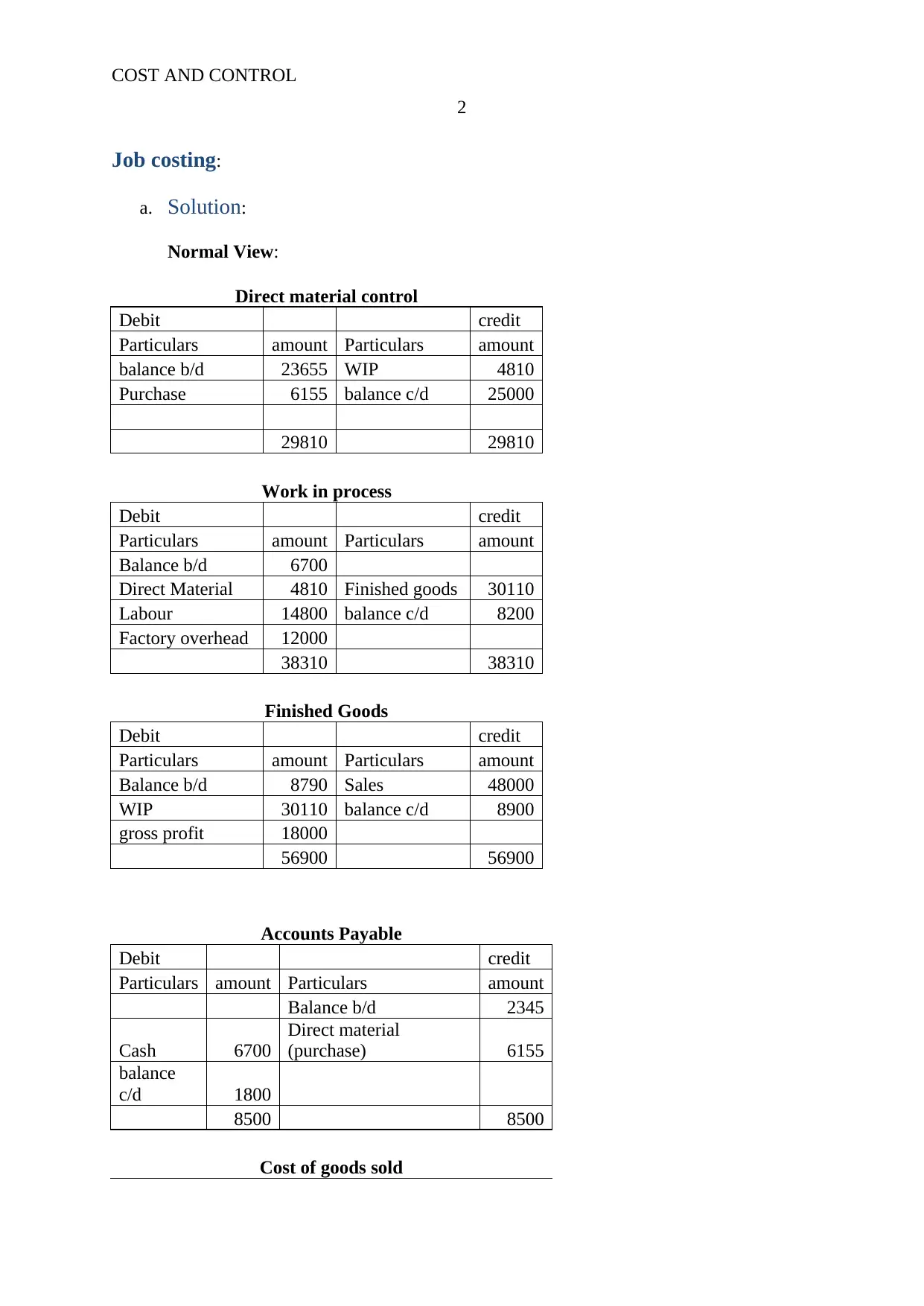

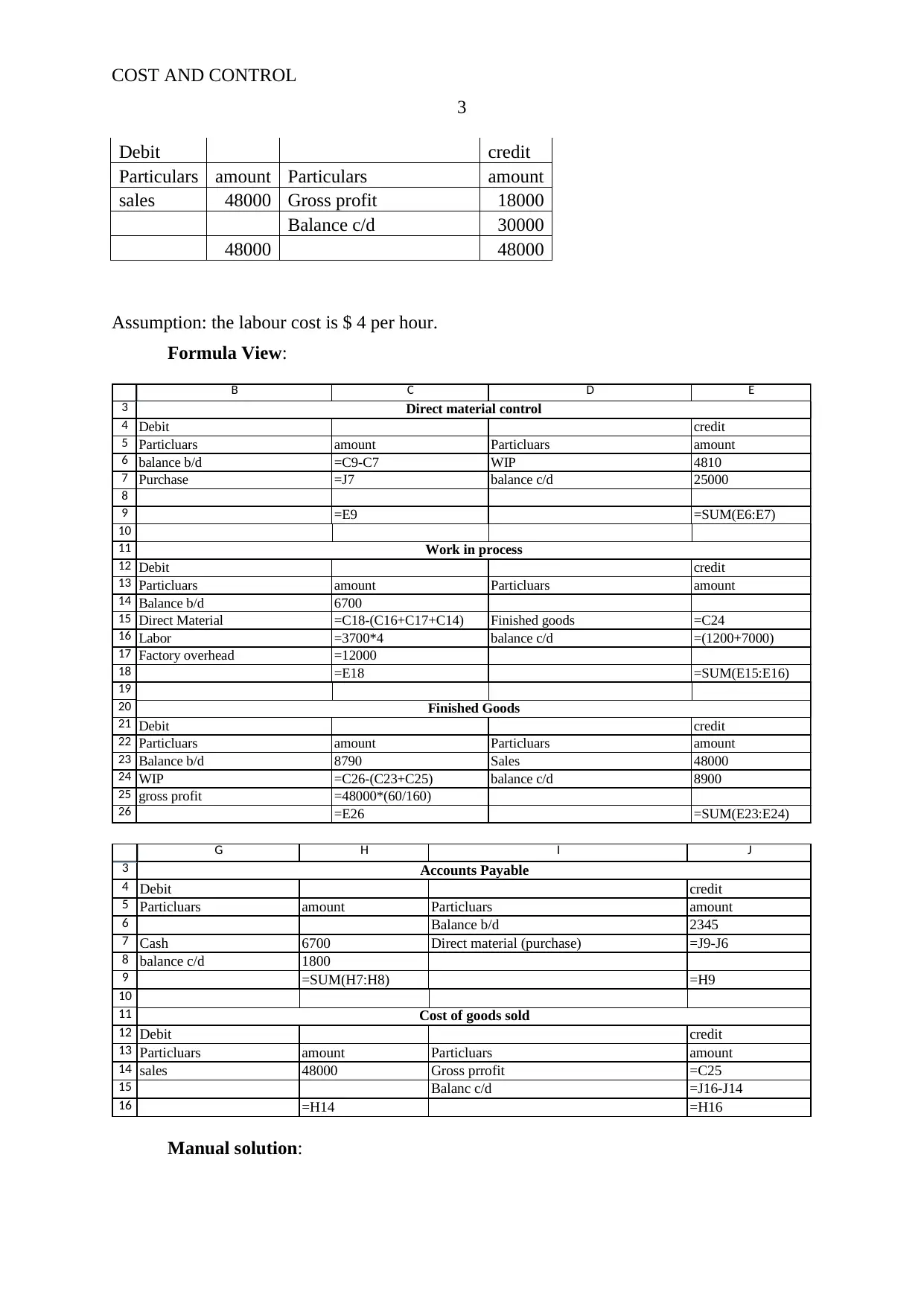

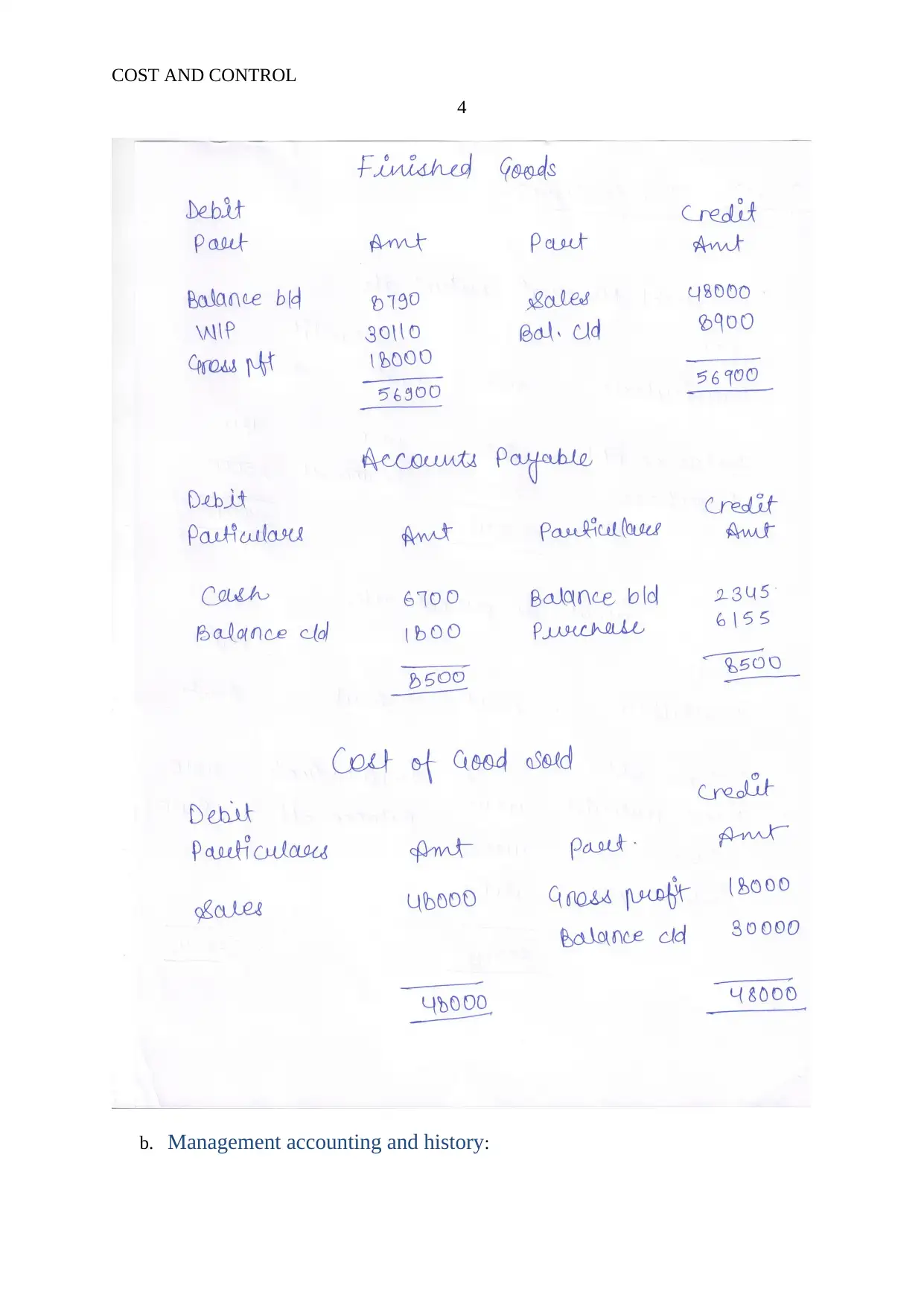

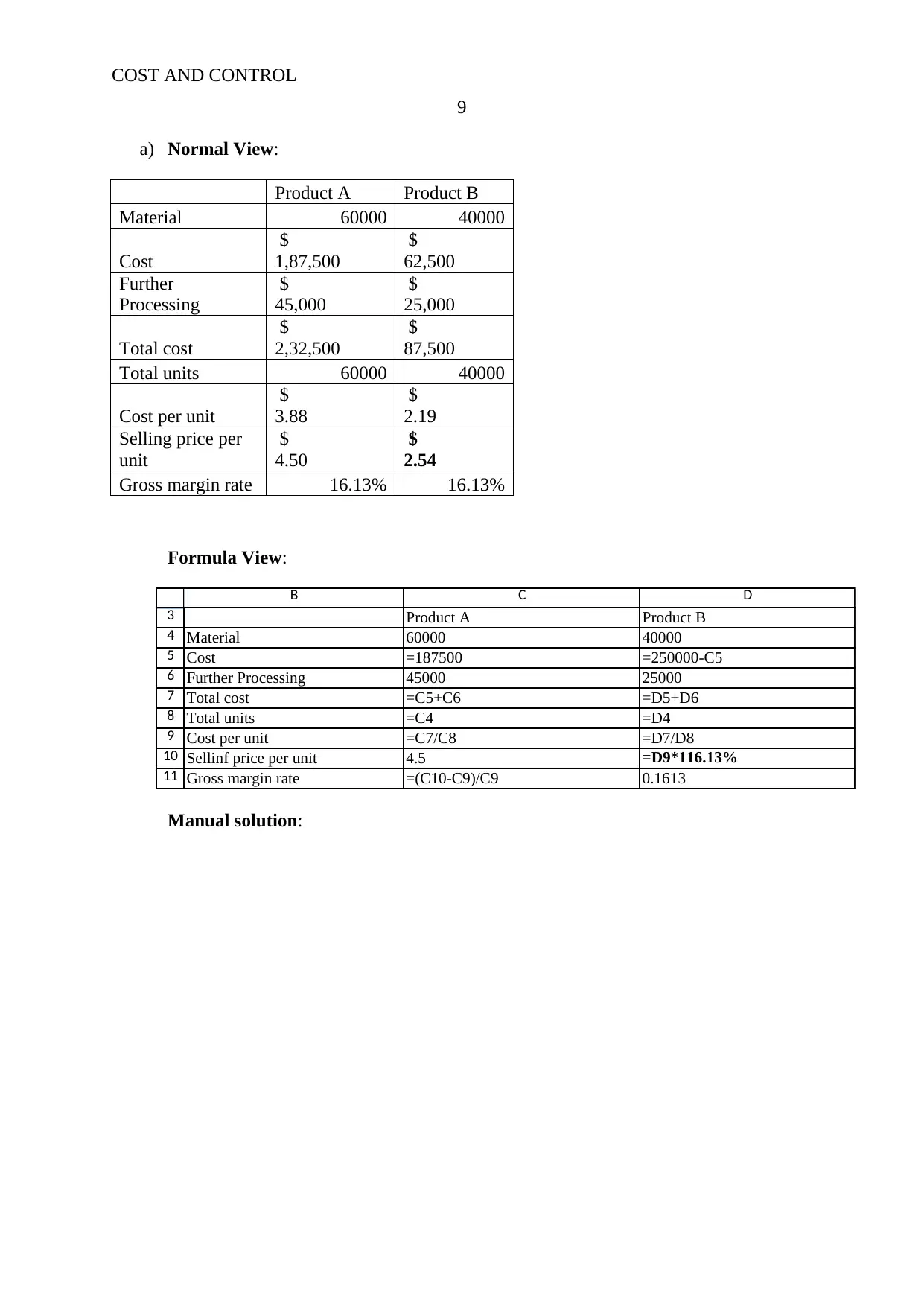

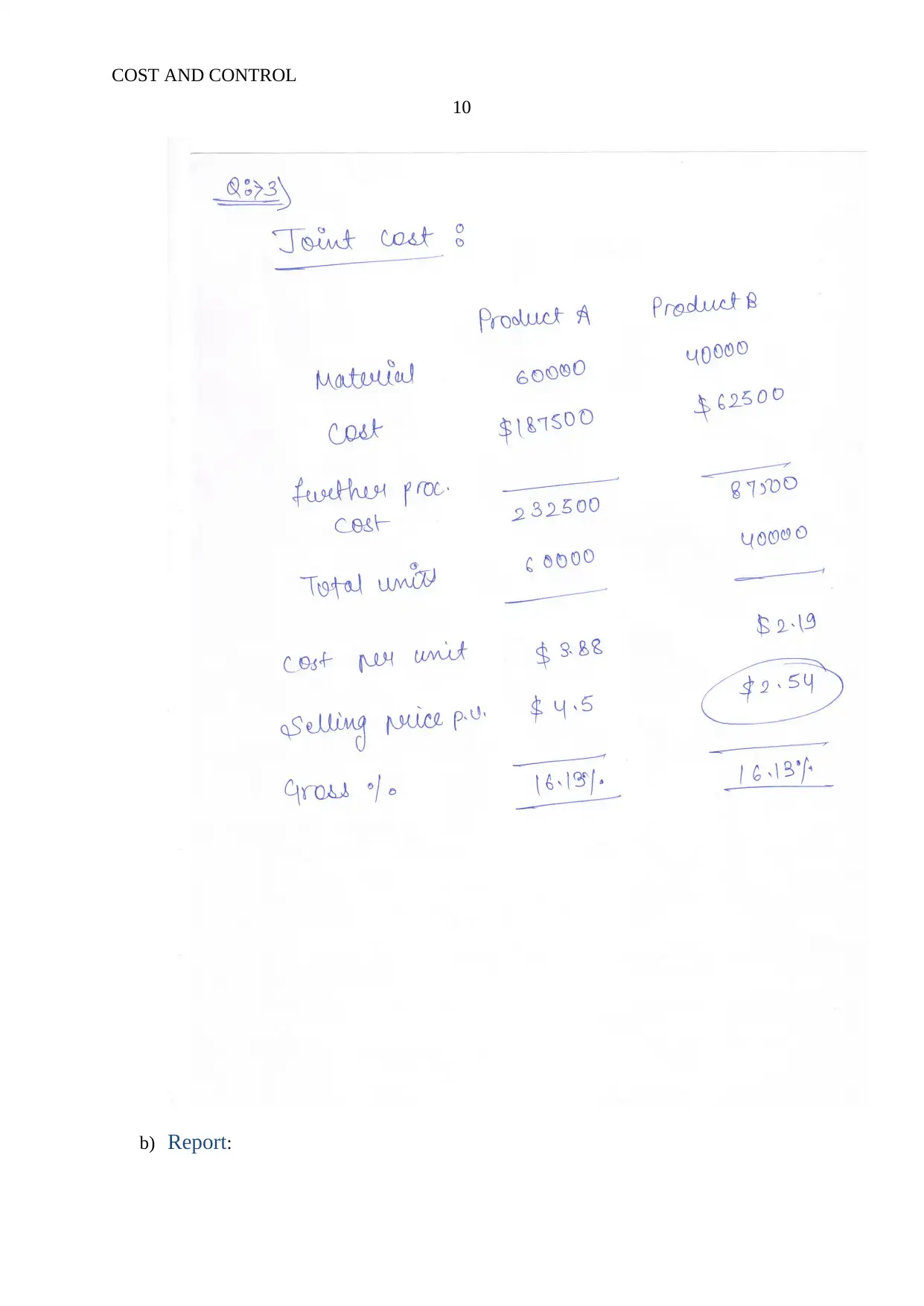

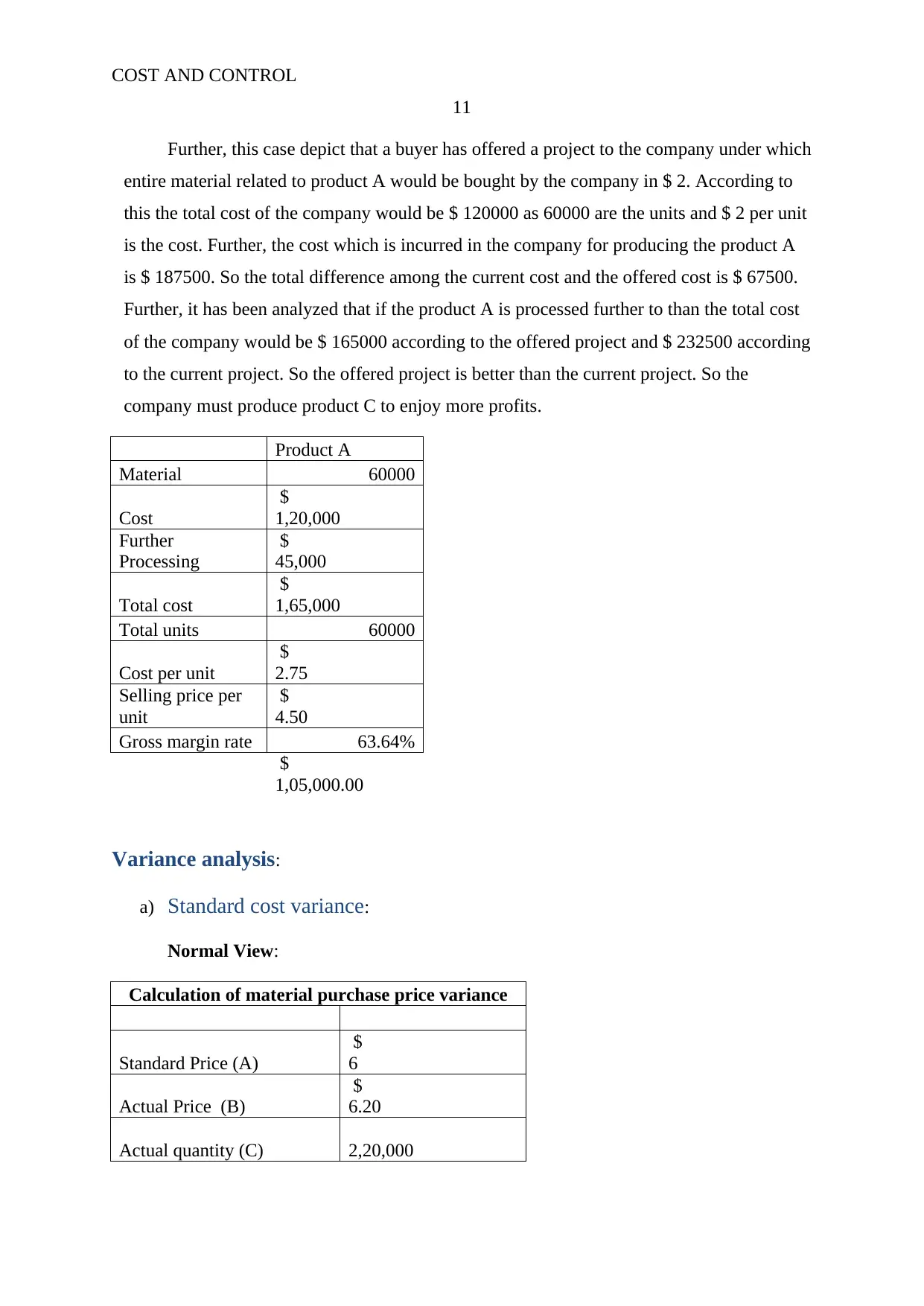

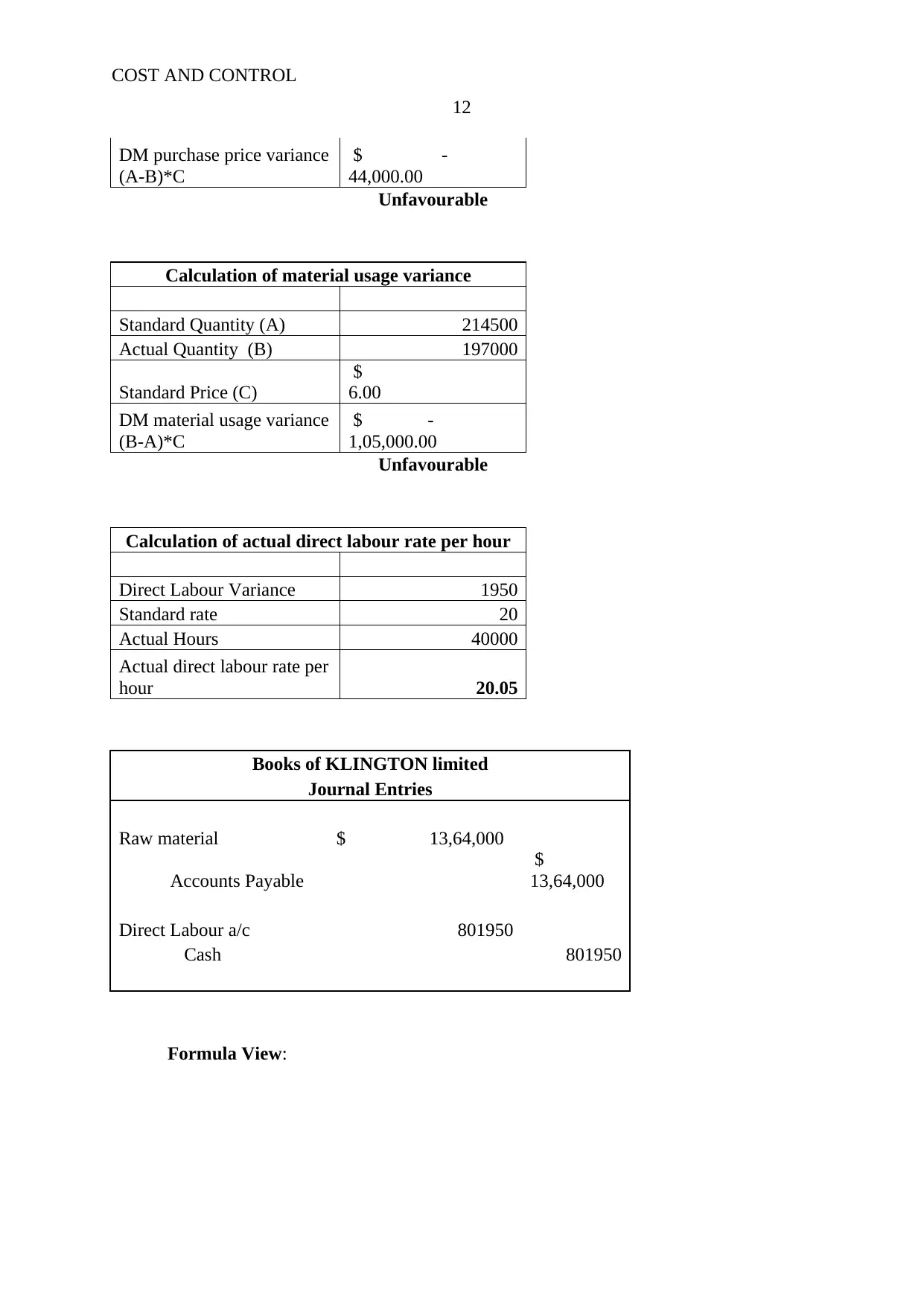

This project report delves into cost control and job costing, encompassing various financial analyses and techniques. The report begins with a normal view analysis of direct material control, work in process, and finished goods, along with journal entries and accounts payable. It then explores process costing, providing production reports for different processes. The project also includes a decision-making analysis for joint costing, comparing different scenarios and recommending the best course of action. Furthermore, the report covers variance analysis, including material purchase price and usage variances, and actual direct labor rate calculations. Finally, it presents a financial model for forecasting income statements, including sales projections, cost of goods sold, and profit analysis, along with a discussion on the political process. The project utilizes normal view, formula view, and manual solution approaches to provide a comprehensive understanding of the concepts.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.