HA2011 Management Accounting Assignment

13 Pages3464 Words173 Views

Holmes Institute Sydney

Management Accounting (HA2011)

Added on 2020-05-28

HA2011 Management Accounting Assignment

Holmes Institute Sydney

Management Accounting (HA2011)

Added on 2020-05-28

ShareRelated Documents

Running Head: Management Accounting 1Project Report: Management Accounting

Management Accounting 2Executive SummaryThis report expresses about 2 cases in which first case express about the costing system of an organization and other case briefs about the budgeting methods of a production company. In first case, the total cost per cake has been evaluated and the bill of entire activities has also been prepared in this report to evaluate the total cost of the cake per unit. Product cost for Lamington has also been calculated and the extra cost details have been given accordingly.In second case, total cash inflows of the company has been measured according to the present plan of the club and the cash inflows according to the future plan of the club. New plan explain that the few changes in the fee structure of the club would make a change in the total cash inflow of the company.

Management Accounting 3ContentsExecutive Summary..........................................................................................................2Part A: Activity Based costing.........................................................................................4Introduction...................................................................................................................4Cost per unit of the company........................................................................................4Bill of activities.............................................................................................................6Product cost for lamington............................................................................................7Conclusion....................................................................................................................8Part B: Budgeting.............................................................................................................9Introduction...................................................................................................................9Improvement in the fee structure................................................................................10Assumptions...............................................................................................................11Evaluation...................................................................................................................12Conclusion..................................................................................................................12References.......................................................................................................................13

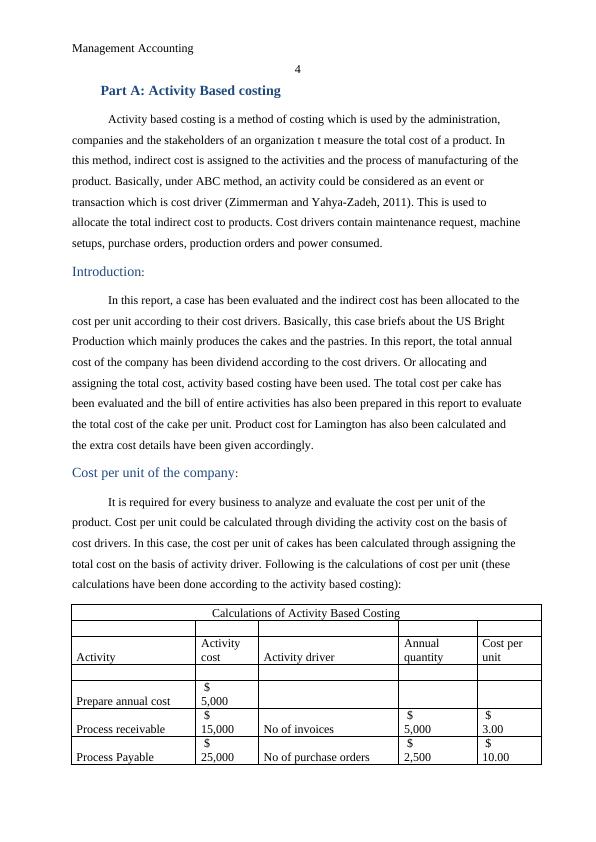

Management Accounting 4Part A: Activity Based costingActivity based costing is a method of costing which is used by the administration, companies and the stakeholders of an organization t measure the total cost of a product. In this method, indirect cost is assigned to the activities and the process of manufacturing of the product. Basically, under ABC method, an activity could be considered as an event or transaction which is cost driver (Zimmerman and Yahya-Zadeh, 2011). This is used to allocate the total indirect cost to products. Cost drivers contain maintenance request, machinesetups, purchase orders, production orders and power consumed. Introduction:In this report, a case has been evaluated and the indirect cost has been allocated to the cost per unit according to their cost drivers. Basically, this case briefs about the US Bright Production which mainly produces the cakes and the pastries. In this report, the total annual cost of the company has been dividend according to the cost drivers. Or allocating and assigning the total cost, activity based costing have been used. The total cost per cake has been evaluated and the bill of entire activities has also been prepared in this report to evaluatethe total cost of the cake per unit. Product cost for Lamington has also been calculated and the extra cost details have been given accordingly. Cost per unit of the company:It is required for every business to analyze and evaluate the cost per unit of the product. Cost per unit could be calculated through dividing the activity cost on the basis of cost drivers. In this case, the cost per unit of cakes has been calculated through assigning the total cost on the basis of activity driver. Following is the calculations of cost per unit (these calculations have been done according to the activity based costing):Calculations of Activity Based CostingActivityActivity costActivity driverAnnual quantityCost per unitPrepare annual cost $ 5,000 Process receivable $ 15,000 No of invoices $ 5,000 $ 3.00 Process Payable $ 25,000 No of purchase orders $ 2,500 $ 10.00

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

HA2011: Financial Management Assignmentlg...

|13

|3450

|83

HA2011 Report on Activity based Costing and Budgetinglg...

|11

|2233

|120

Management Accounting Assignment - (Solved)lg...

|10

|2211

|63

Management Accounting Report (Doc)lg...

|16

|2545

|62

HA2011 Activity based Costing and Budgeting Reportlg...

|11

|2248

|108

Activity Based-Costing Method - Assignmentlg...

|12

|3066

|30