Capital Markets and Investment Report

VerifiedAdded on 2020/02/05

|14

|4926

|90

Report

AI Summary

This report analyzes a diversified investment portfolio designed for a risk-averse investor. The portfolio includes bonds, equities, mutual funds, fixed interest securities, and gold. The report evaluates the portfolio's performance using various investment theories and models, including the efficient market hypothesis (EMH), the capital asset pricing model (CAPM), and modern portfolio theory (MPT). The rationale behind the asset allocation is explained, considering the risk profile of the investor and market conditions. The report also discusses different investment styles and their relevance to the portfolio. Finally, the report concludes by assessing the portfolio's overall performance in terms of risk and return, comparing it to the FTSE 100 index. The analysis shows that the portfolio is expected to generate a return of 13.14%, which is close to the annual return of the FTSE 100 index.

CAPITAL MARKETS AND

INVESTMENT

1

INVESTMENT

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

RATIONALE FOR THE CHOICE OF THE PORTFOLIO.................................................................3

EVALUATION, EXAMINATION AND APPLICATION OF THE INVESTMENT THEORIES

AND MODELS....................................................................................................................................7

3.1 Efficient market hypothesis theory............................................................................................8

3.2 Capital assets pricing model......................................................................................................8

3.3 Modern portfolio theory.............................................................................................................9

3.4 Investment styles........................................................................................................................9

CONCLUSION BASED ON PORTFOLIO PERFORMANCE........................................................10

REFERENCES...................................................................................................................................12

2

INTRODUCTION................................................................................................................................3

RATIONALE FOR THE CHOICE OF THE PORTFOLIO.................................................................3

EVALUATION, EXAMINATION AND APPLICATION OF THE INVESTMENT THEORIES

AND MODELS....................................................................................................................................7

3.1 Efficient market hypothesis theory............................................................................................8

3.2 Capital assets pricing model......................................................................................................8

3.3 Modern portfolio theory.............................................................................................................9

3.4 Investment styles........................................................................................................................9

CONCLUSION BASED ON PORTFOLIO PERFORMANCE........................................................10

REFERENCES...................................................................................................................................12

2

INTRODUCTION

In the current age, companies started operating in the domestic as well as overseas. It attracts

investors to invest their money in the profitable companies so as to get maximum return. However,

the different level of risk and reward on different nature of securities make it essential for the

investors to make rational and informed investment decisions after carrying out an in-depth

analysis. The present project report aims at creating a portfolio comprising minimum of 5 product

or assets for the purpose of diversification and risk minimizing. Moreover, the report will also

present a critical evaluation of various theories of investment like modern portfolio theory, efficient

market hypothesis, capital assets pricing model and others. Lastly, the designed portfolio will be

evaluated in terms of both the risk and return so as to satisfy the investor return expectations.

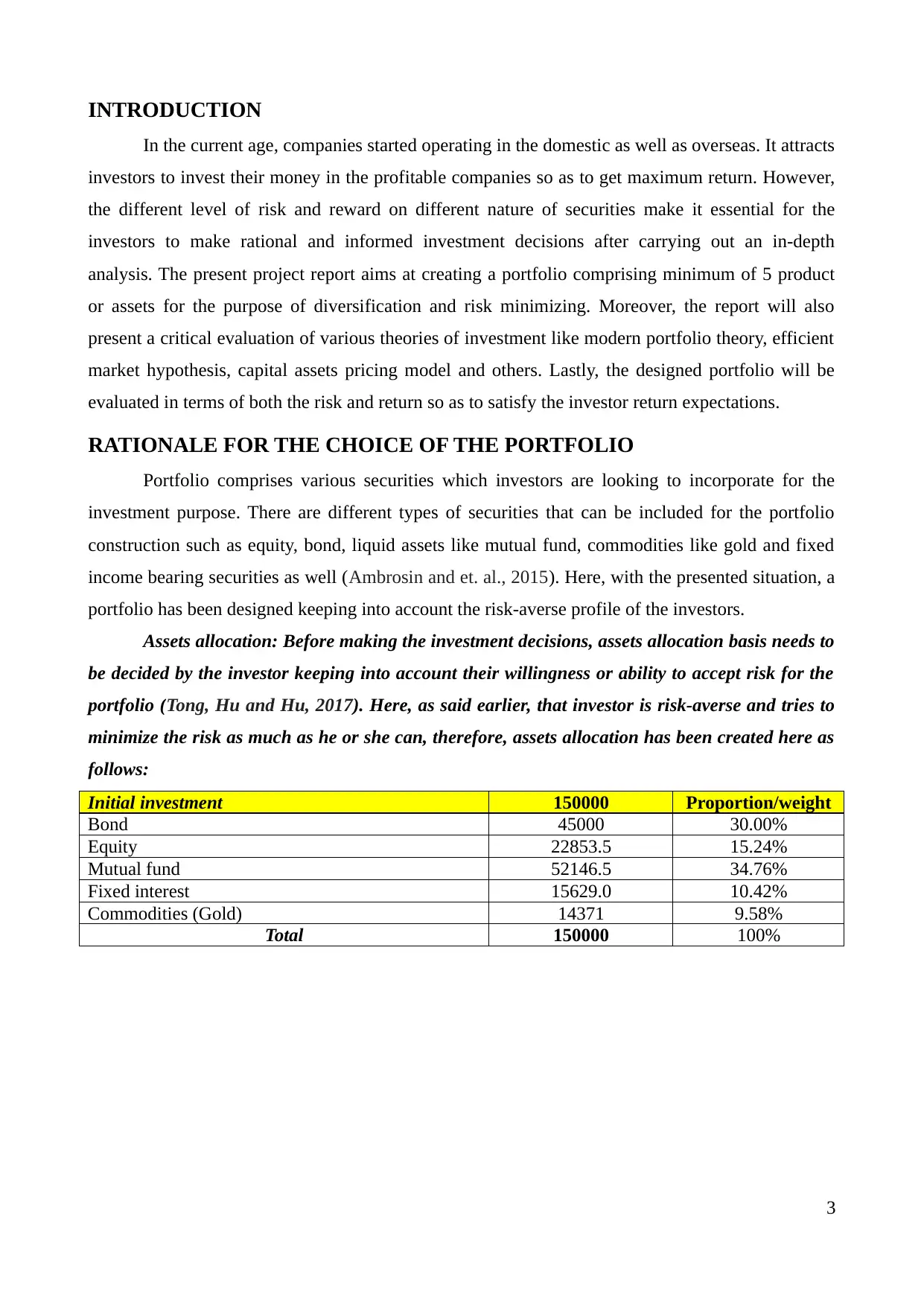

RATIONALE FOR THE CHOICE OF THE PORTFOLIO

Portfolio comprises various securities which investors are looking to incorporate for the

investment purpose. There are different types of securities that can be included for the portfolio

construction such as equity, bond, liquid assets like mutual fund, commodities like gold and fixed

income bearing securities as well (Ambrosin and et. al., 2015). Here, with the presented situation, a

portfolio has been designed keeping into account the risk-averse profile of the investors.

Assets allocation: Before making the investment decisions, assets allocation basis needs to

be decided by the investor keeping into account their willingness or ability to accept risk for the

portfolio (Tong, Hu and Hu, 2017). Here, as said earlier, that investor is risk-averse and tries to

minimize the risk as much as he or she can, therefore, assets allocation has been created here as

follows:

Initial investment 150000 Proportion/weight

Bond 45000 30.00%

Equity 22853.5 15.24%

Mutual fund 52146.5 34.76%

Fixed interest 15629.0 10.42%

Commodities (Gold) 14371 9.58%

Total 150000 100%

3

In the current age, companies started operating in the domestic as well as overseas. It attracts

investors to invest their money in the profitable companies so as to get maximum return. However,

the different level of risk and reward on different nature of securities make it essential for the

investors to make rational and informed investment decisions after carrying out an in-depth

analysis. The present project report aims at creating a portfolio comprising minimum of 5 product

or assets for the purpose of diversification and risk minimizing. Moreover, the report will also

present a critical evaluation of various theories of investment like modern portfolio theory, efficient

market hypothesis, capital assets pricing model and others. Lastly, the designed portfolio will be

evaluated in terms of both the risk and return so as to satisfy the investor return expectations.

RATIONALE FOR THE CHOICE OF THE PORTFOLIO

Portfolio comprises various securities which investors are looking to incorporate for the

investment purpose. There are different types of securities that can be included for the portfolio

construction such as equity, bond, liquid assets like mutual fund, commodities like gold and fixed

income bearing securities as well (Ambrosin and et. al., 2015). Here, with the presented situation, a

portfolio has been designed keeping into account the risk-averse profile of the investors.

Assets allocation: Before making the investment decisions, assets allocation basis needs to

be decided by the investor keeping into account their willingness or ability to accept risk for the

portfolio (Tong, Hu and Hu, 2017). Here, as said earlier, that investor is risk-averse and tries to

minimize the risk as much as he or she can, therefore, assets allocation has been created here as

follows:

Initial investment 150000 Proportion/weight

Bond 45000 30.00%

Equity 22853.5 15.24%

Mutual fund 52146.5 34.76%

Fixed interest 15629.0 10.42%

Commodities (Gold) 14371 9.58%

Total 150000 100%

3

You're viewing a preview

Unlock full access by subscribing today!

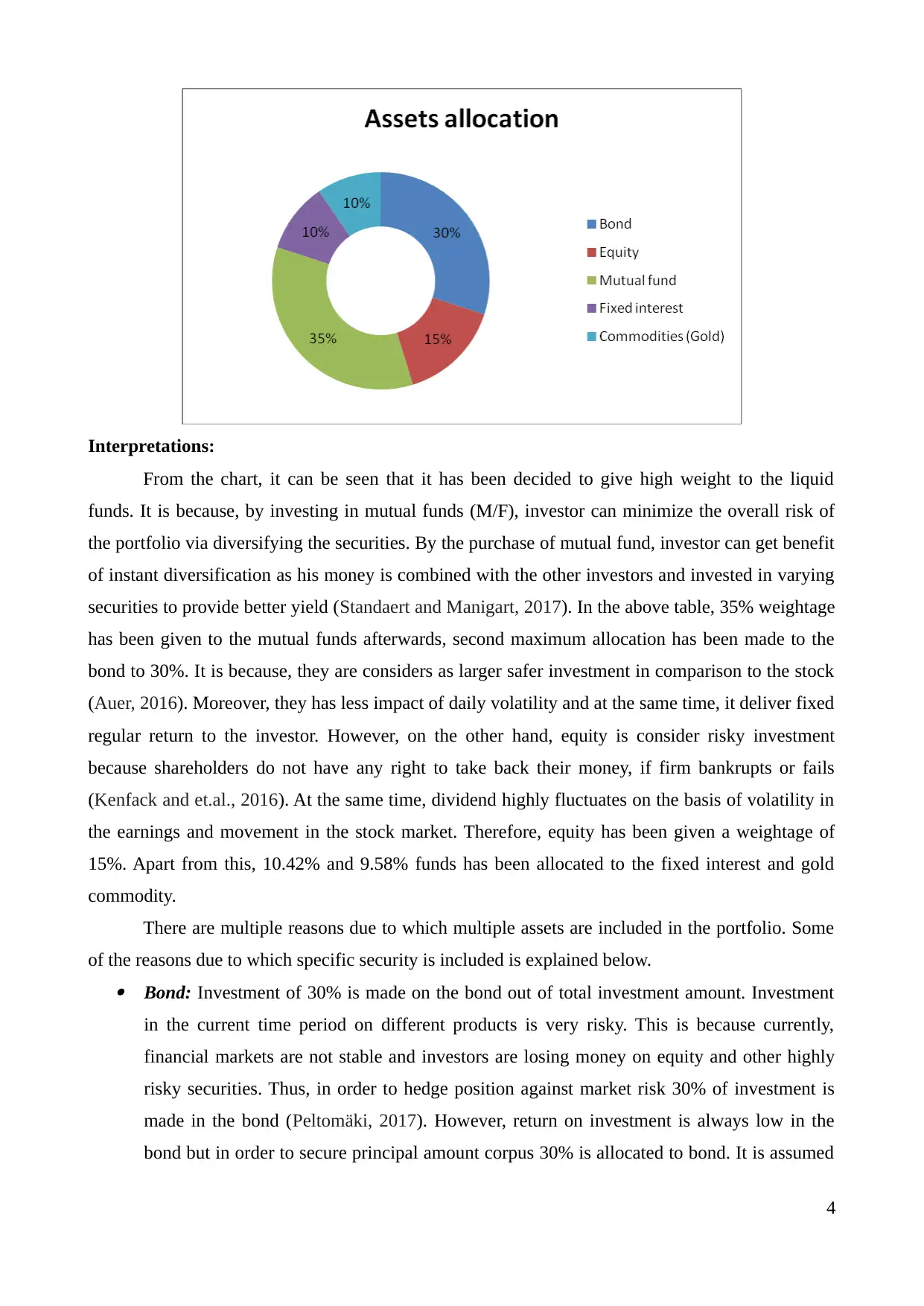

Interpretations:

From the chart, it can be seen that it has been decided to give high weight to the liquid

funds. It is because, by investing in mutual funds (M/F), investor can minimize the overall risk of

the portfolio via diversifying the securities. By the purchase of mutual fund, investor can get benefit

of instant diversification as his money is combined with the other investors and invested in varying

securities to provide better yield (Standaert and Manigart, 2017). In the above table, 35% weightage

has been given to the mutual funds afterwards, second maximum allocation has been made to the

bond to 30%. It is because, they are considers as larger safer investment in comparison to the stock

(Auer, 2016). Moreover, they has less impact of daily volatility and at the same time, it deliver fixed

regular return to the investor. However, on the other hand, equity is consider risky investment

because shareholders do not have any right to take back their money, if firm bankrupts or fails

(Kenfack and et.al., 2016). At the same time, dividend highly fluctuates on the basis of volatility in

the earnings and movement in the stock market. Therefore, equity has been given a weightage of

15%. Apart from this, 10.42% and 9.58% funds has been allocated to the fixed interest and gold

commodity.

There are multiple reasons due to which multiple assets are included in the portfolio. Some

of the reasons due to which specific security is included is explained below. Bond: Investment of 30% is made on the bond out of total investment amount. Investment

in the current time period on different products is very risky. This is because currently,

financial markets are not stable and investors are losing money on equity and other highly

risky securities. Thus, in order to hedge position against market risk 30% of investment is

made in the bond (Peltomäki, 2017). However, return on investment is always low in the

bond but in order to secure principal amount corpus 30% is allocated to bond. It is assumed

4

From the chart, it can be seen that it has been decided to give high weight to the liquid

funds. It is because, by investing in mutual funds (M/F), investor can minimize the overall risk of

the portfolio via diversifying the securities. By the purchase of mutual fund, investor can get benefit

of instant diversification as his money is combined with the other investors and invested in varying

securities to provide better yield (Standaert and Manigart, 2017). In the above table, 35% weightage

has been given to the mutual funds afterwards, second maximum allocation has been made to the

bond to 30%. It is because, they are considers as larger safer investment in comparison to the stock

(Auer, 2016). Moreover, they has less impact of daily volatility and at the same time, it deliver fixed

regular return to the investor. However, on the other hand, equity is consider risky investment

because shareholders do not have any right to take back their money, if firm bankrupts or fails

(Kenfack and et.al., 2016). At the same time, dividend highly fluctuates on the basis of volatility in

the earnings and movement in the stock market. Therefore, equity has been given a weightage of

15%. Apart from this, 10.42% and 9.58% funds has been allocated to the fixed interest and gold

commodity.

There are multiple reasons due to which multiple assets are included in the portfolio. Some

of the reasons due to which specific security is included is explained below. Bond: Investment of 30% is made on the bond out of total investment amount. Investment

in the current time period on different products is very risky. This is because currently,

financial markets are not stable and investors are losing money on equity and other highly

risky securities. Thus, in order to hedge position against market risk 30% of investment is

made in the bond (Peltomäki, 2017). However, return on investment is always low in the

bond but in order to secure principal amount corpus 30% is allocated to bond. It is assumed

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that investor is risk averse in nature and market is unstable due to which investment must be

secured. It can be noted that in case of most of stocks beta value is much higher and is above

0.70. In case of some stocks it can be observed that beta value exceed 1. This clearly shows

that in case stock market will be bearish investor will lose huge amount of money on the

invested amount.

Equity: Investment of 15.24% is made in the equity which is the small percentage of the

invested corpus. Equity is assumed as one of the risky and highly return generated

investment avenue. There are multiple reasons due to which equity is included in the

portfolio and its proportion is kept low in the portfolio. Equity is included in the portfolio

because only by keeping debt in the portfolio sufficient amount of return cannot be

generated on the invested amount (Guerrien, 2011). It can be observed that most of the firms

that are constitutes of the FTSE index have high beta value and due to this reason few firms

are taken in the portfolio. In order to elevate profitability in the portfolio low proportion of

amount is allocated to equity. It is ensured while selecting firms that they have moderate or

high beta value with strong finance fundamentals in the current time period. Software and

tourism are the two industries that are growing at rapid rate in the UK. Thus, due to this

reason two firms namely Intercontinental hotel and Sage group as well as Associated British

foods are included in the portfolio. There is great demand of cars in UK and its economy is

coming on growth track. Due to this reason it is expected that in the upcoming time period

demand of cars increased. Thus, Admiral Group is included in the portfolio. It can be said

that equity portfolio is well diversified and firms are prudently selected in same on the basis

of growth prospective that are present in the specific industry. Reasons for selection of firm

is given below:

1. Associated British foods (ABF)- Associated British foods is a public limited company which is

mainly in food processing retail industry, founded in 1935. There headquarters are Weston Center.

This firm mainly supply food and ingredients. There revenue is 13399 million euro in 2016. Return

of 19.42% and there beta are 1.15.

2. Admiral group (ADM)- It is a motor insurance company with its headquarter in Cardiff, Wales.

Its total revenue is 1016.8 million euro and there operating income is 289.8 million euro and there

net income is 214.1 million in 2016. This company have there return is 7.71% and there beta is

0.637.

3. Baratt Development- It is operating in the home construction business. With elevation in

economic growth of the UK demand for homes will increases in the upcoming time period. Hence,

it is expected that firm will earn good amount of return in the upcoming time period. This company

5

secured. It can be noted that in case of most of stocks beta value is much higher and is above

0.70. In case of some stocks it can be observed that beta value exceed 1. This clearly shows

that in case stock market will be bearish investor will lose huge amount of money on the

invested amount.

Equity: Investment of 15.24% is made in the equity which is the small percentage of the

invested corpus. Equity is assumed as one of the risky and highly return generated

investment avenue. There are multiple reasons due to which equity is included in the

portfolio and its proportion is kept low in the portfolio. Equity is included in the portfolio

because only by keeping debt in the portfolio sufficient amount of return cannot be

generated on the invested amount (Guerrien, 2011). It can be observed that most of the firms

that are constitutes of the FTSE index have high beta value and due to this reason few firms

are taken in the portfolio. In order to elevate profitability in the portfolio low proportion of

amount is allocated to equity. It is ensured while selecting firms that they have moderate or

high beta value with strong finance fundamentals in the current time period. Software and

tourism are the two industries that are growing at rapid rate in the UK. Thus, due to this

reason two firms namely Intercontinental hotel and Sage group as well as Associated British

foods are included in the portfolio. There is great demand of cars in UK and its economy is

coming on growth track. Due to this reason it is expected that in the upcoming time period

demand of cars increased. Thus, Admiral Group is included in the portfolio. It can be said

that equity portfolio is well diversified and firms are prudently selected in same on the basis

of growth prospective that are present in the specific industry. Reasons for selection of firm

is given below:

1. Associated British foods (ABF)- Associated British foods is a public limited company which is

mainly in food processing retail industry, founded in 1935. There headquarters are Weston Center.

This firm mainly supply food and ingredients. There revenue is 13399 million euro in 2016. Return

of 19.42% and there beta are 1.15.

2. Admiral group (ADM)- It is a motor insurance company with its headquarter in Cardiff, Wales.

Its total revenue is 1016.8 million euro and there operating income is 289.8 million euro and there

net income is 214.1 million in 2016. This company have there return is 7.71% and there beta is

0.637.

3. Baratt Development- It is operating in the home construction business. With elevation in

economic growth of the UK demand for homes will increases in the upcoming time period. Hence,

it is expected that firm will earn good amount of return in the upcoming time period. This company

5

have return is 12.51% and there beta is 0.6483. Hence, mentioned firm is included in the portfolio.

4. Intercontinental hotels- It is a British multinational hotels, company headquarter in Den-ham,

UK. It is founded in 2003. It provide hospitality problems. Its total revenue is 1715 million dollar in

2016 and operating income is 707 million dollar in 2016 and its net income is 417 million dollar in

2016. Intercontinental hotels is taken in portfolio as it is working in the tourism industry. Return of

33.85% generated and there beta are 0.9699. Thus, by considering past performance of stock,

anticipated high growth of industry and high beta value it is expected that good amount of return

can be generated by the mentioned firm. Due to this reason mentioned firm is included in the

portfolio.

5. Sage group- It is commonly known as Sage, it is a public limited company, which is software

industry. There headquarters in Newcastle upon Type, England, UK. There revenue is 1569.1

million euro and operating income is 427 million euro in 2016. Beta value is 1.1388 and there

return is 5.91%. So that this firm, included in the portfolio. Mutual fund: Mutual fund is also selected in the portfolio and its proportion in same is kept

at 34.76%. As mentioned above investor wants to minimize risk and due to this reason

investment of mention percentage is made in the mutual fund. It must be noted that when

investment is made on the debt funds then it means that 10% to 20% is made in equity out of

entire corpus that is invested in the debt scheme (Auer, 2016).. Thus, with risk management

moderate return is also earned on the debt funds. Due to this reason substantial portion of

investment is made in the mutual fund scheme. By doing so it is ensured that risk will be

minimum and moderate risk will be earned on the investment. Thus, portion of 34.76% is

allocated to mutual fund scheme in the portfolio. Fixed interest: After making investment in all securities remaining amount is invested in the

bank product at interest rate of 2.50%. Investment in the saving account is not exposed to

market risk and due to this reason it can be said that it is wise decision to make investment

in bank product.

Commodity: Investment in gold is made because it is observed that when investment in

shares declined received proceeds are invested in safe heaven which is gold. Thus,

9.58% of portfolio is invested in the gold (Tong, Hu and Hu, 2017). This is done to

ensure that in case decline will be observed in the FTSE then in that case loss faced on

equity will be offset by gain that is made on gold.

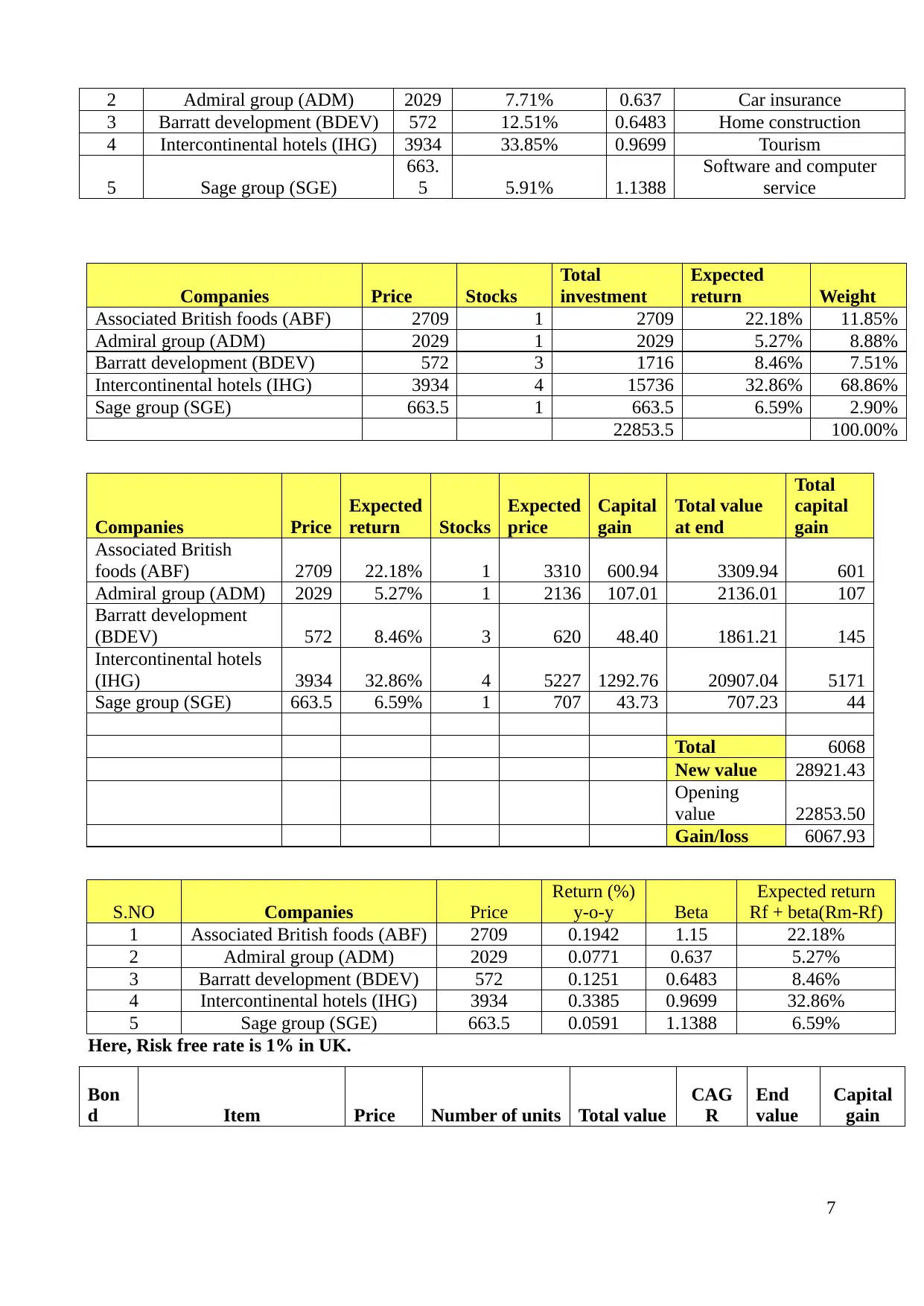

S.NO Companies Price

Return (%) y-o-

y Beta Industry

1

Associated British foods

(ABF) 2709 19.42% 1.15 Tourism

6

4. Intercontinental hotels- It is a British multinational hotels, company headquarter in Den-ham,

UK. It is founded in 2003. It provide hospitality problems. Its total revenue is 1715 million dollar in

2016 and operating income is 707 million dollar in 2016 and its net income is 417 million dollar in

2016. Intercontinental hotels is taken in portfolio as it is working in the tourism industry. Return of

33.85% generated and there beta are 0.9699. Thus, by considering past performance of stock,

anticipated high growth of industry and high beta value it is expected that good amount of return

can be generated by the mentioned firm. Due to this reason mentioned firm is included in the

portfolio.

5. Sage group- It is commonly known as Sage, it is a public limited company, which is software

industry. There headquarters in Newcastle upon Type, England, UK. There revenue is 1569.1

million euro and operating income is 427 million euro in 2016. Beta value is 1.1388 and there

return is 5.91%. So that this firm, included in the portfolio. Mutual fund: Mutual fund is also selected in the portfolio and its proportion in same is kept

at 34.76%. As mentioned above investor wants to minimize risk and due to this reason

investment of mention percentage is made in the mutual fund. It must be noted that when

investment is made on the debt funds then it means that 10% to 20% is made in equity out of

entire corpus that is invested in the debt scheme (Auer, 2016).. Thus, with risk management

moderate return is also earned on the debt funds. Due to this reason substantial portion of

investment is made in the mutual fund scheme. By doing so it is ensured that risk will be

minimum and moderate risk will be earned on the investment. Thus, portion of 34.76% is

allocated to mutual fund scheme in the portfolio. Fixed interest: After making investment in all securities remaining amount is invested in the

bank product at interest rate of 2.50%. Investment in the saving account is not exposed to

market risk and due to this reason it can be said that it is wise decision to make investment

in bank product.

Commodity: Investment in gold is made because it is observed that when investment in

shares declined received proceeds are invested in safe heaven which is gold. Thus,

9.58% of portfolio is invested in the gold (Tong, Hu and Hu, 2017). This is done to

ensure that in case decline will be observed in the FTSE then in that case loss faced on

equity will be offset by gain that is made on gold.

S.NO Companies Price

Return (%) y-o-

y Beta Industry

1

Associated British foods

(ABF) 2709 19.42% 1.15 Tourism

6

You're viewing a preview

Unlock full access by subscribing today!

2 Admiral group (ADM) 2029 7.71% 0.637 Car insurance

3 Barratt development (BDEV) 572 12.51% 0.6483 Home construction

4 Intercontinental hotels (IHG) 3934 33.85% 0.9699 Tourism

5 Sage group (SGE)

663.

5 5.91% 1.1388

Software and computer

service

Companies Price Stocks

Total

investment

Expected

return Weight

Associated British foods (ABF) 2709 1 2709 22.18% 11.85%

Admiral group (ADM) 2029 1 2029 5.27% 8.88%

Barratt development (BDEV) 572 3 1716 8.46% 7.51%

Intercontinental hotels (IHG) 3934 4 15736 32.86% 68.86%

Sage group (SGE) 663.5 1 663.5 6.59% 2.90%

22853.5 100.00%

Companies Price

Expected

return Stocks

Expected

price

Capital

gain

Total value

at end

Total

capital

gain

Associated British

foods (ABF) 2709 22.18% 1 3310 600.94 3309.94 601

Admiral group (ADM) 2029 5.27% 1 2136 107.01 2136.01 107

Barratt development

(BDEV) 572 8.46% 3 620 48.40 1861.21 145

Intercontinental hotels

(IHG) 3934 32.86% 4 5227 1292.76 20907.04 5171

Sage group (SGE) 663.5 6.59% 1 707 43.73 707.23 44

Total 6068

New value 28921.43

Opening

value 22853.50

Gain/loss 6067.93

S.NO Companies Price

Return (%)

y-o-y Beta

Expected return

Rf + beta(Rm-Rf)

1 Associated British foods (ABF) 2709 0.1942 1.15 22.18%

2 Admiral group (ADM) 2029 0.0771 0.637 5.27%

3 Barratt development (BDEV) 572 0.1251 0.6483 8.46%

4 Intercontinental hotels (IHG) 3934 0.3385 0.9699 32.86%

5 Sage group (SGE) 663.5 0.0591 1.1388 6.59%

Here, Risk free rate is 1% in UK.

Bon

d Item Price Number of units Total value

CAG

R

End

value

Capital

gain

7

3 Barratt development (BDEV) 572 12.51% 0.6483 Home construction

4 Intercontinental hotels (IHG) 3934 33.85% 0.9699 Tourism

5 Sage group (SGE)

663.

5 5.91% 1.1388

Software and computer

service

Companies Price Stocks

Total

investment

Expected

return Weight

Associated British foods (ABF) 2709 1 2709 22.18% 11.85%

Admiral group (ADM) 2029 1 2029 5.27% 8.88%

Barratt development (BDEV) 572 3 1716 8.46% 7.51%

Intercontinental hotels (IHG) 3934 4 15736 32.86% 68.86%

Sage group (SGE) 663.5 1 663.5 6.59% 2.90%

22853.5 100.00%

Companies Price

Expected

return Stocks

Expected

price

Capital

gain

Total value

at end

Total

capital

gain

Associated British

foods (ABF) 2709 22.18% 1 3310 600.94 3309.94 601

Admiral group (ADM) 2029 5.27% 1 2136 107.01 2136.01 107

Barratt development

(BDEV) 572 8.46% 3 620 48.40 1861.21 145

Intercontinental hotels

(IHG) 3934 32.86% 4 5227 1292.76 20907.04 5171

Sage group (SGE) 663.5 6.59% 1 707 43.73 707.23 44

Total 6068

New value 28921.43

Opening

value 22853.50

Gain/loss 6067.93

S.NO Companies Price

Return (%)

y-o-y Beta

Expected return

Rf + beta(Rm-Rf)

1 Associated British foods (ABF) 2709 0.1942 1.15 22.18%

2 Admiral group (ADM) 2029 0.0771 0.637 5.27%

3 Barratt development (BDEV) 572 0.1251 0.6483 8.46%

4 Intercontinental hotels (IHG) 3934 0.3385 0.9699 32.86%

5 Sage group (SGE) 663.5 0.0591 1.1388 6.59%

Here, Risk free rate is 1% in UK.

Bon

d Item Price Number of units Total value

CAG

R

End

value

Capital

gain

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

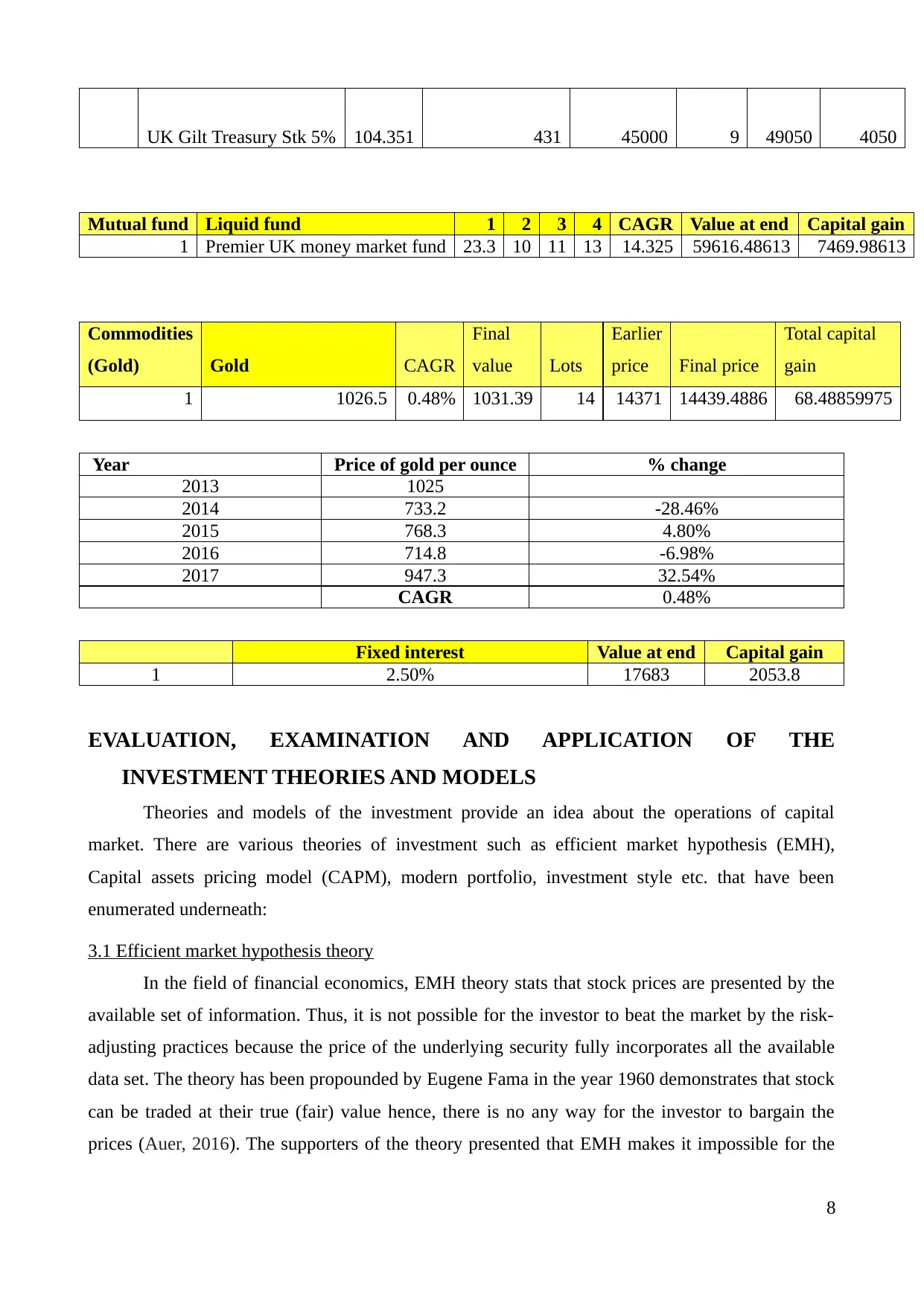

UK Gilt Treasury Stk 5% 104.351 431 45000 9 49050 4050

Mutual fund Liquid fund 1 2 3 4 CAGR Value at end Capital gain

1 Premier UK money market fund 23.3 10 11 13 14.325 59616.48613 7469.98613

Commodities

(Gold) Gold CAGR

Final

value Lots

Earlier

price Final price

Total capital

gain

1 1026.5 0.48% 1031.39 14 14371 14439.4886 68.48859975

Year Price of gold per ounce % change

2013 1025

2014 733.2 -28.46%

2015 768.3 4.80%

2016 714.8 -6.98%

2017 947.3 32.54%

CAGR 0.48%

Fixed interest Value at end Capital gain

1 2.50% 17683 2053.8

EVALUATION, EXAMINATION AND APPLICATION OF THE

INVESTMENT THEORIES AND MODELS

Theories and models of the investment provide an idea about the operations of capital

market. There are various theories of investment such as efficient market hypothesis (EMH),

Capital assets pricing model (CAPM), modern portfolio, investment style etc. that have been

enumerated underneath:

3.1 Efficient market hypothesis theory

In the field of financial economics, EMH theory stats that stock prices are presented by the

available set of information. Thus, it is not possible for the investor to beat the market by the risk-

adjusting practices because the price of the underlying security fully incorporates all the available

data set. The theory has been propounded by Eugene Fama in the year 1960 demonstrates that stock

can be traded at their true (fair) value hence, there is no any way for the investor to bargain the

prices (Auer, 2016). The supporters of the theory presented that EMH makes it impossible for the

8

Mutual fund Liquid fund 1 2 3 4 CAGR Value at end Capital gain

1 Premier UK money market fund 23.3 10 11 13 14.325 59616.48613 7469.98613

Commodities

(Gold) Gold CAGR

Final

value Lots

Earlier

price Final price

Total capital

gain

1 1026.5 0.48% 1031.39 14 14371 14439.4886 68.48859975

Year Price of gold per ounce % change

2013 1025

2014 733.2 -28.46%

2015 768.3 4.80%

2016 714.8 -6.98%

2017 947.3 32.54%

CAGR 0.48%

Fixed interest Value at end Capital gain

1 2.50% 17683 2053.8

EVALUATION, EXAMINATION AND APPLICATION OF THE

INVESTMENT THEORIES AND MODELS

Theories and models of the investment provide an idea about the operations of capital

market. There are various theories of investment such as efficient market hypothesis (EMH),

Capital assets pricing model (CAPM), modern portfolio, investment style etc. that have been

enumerated underneath:

3.1 Efficient market hypothesis theory

In the field of financial economics, EMH theory stats that stock prices are presented by the

available set of information. Thus, it is not possible for the investor to beat the market by the risk-

adjusting practices because the price of the underlying security fully incorporates all the available

data set. The theory has been propounded by Eugene Fama in the year 1960 demonstrates that stock

can be traded at their true (fair) value hence, there is no any way for the investor to bargain the

prices (Auer, 2016). The supporters of the theory presented that EMH makes it impossible for the

8

capital investors to either buy undervalued stock or dispose off their stock at the inflated prices.

Thus, it is pointless to find out the undervalued stock or forecast the future trend through technical

and fundamental analysis. However, the critics argued that as per the theory of EMH, investors only

look towards the historical prices, earnings and past track records, it is because, prices are heavily

influenced by the expectations of the users. Thus, it just simply states that past stock price has a

great impact on the future price (Guerrien, 2011).

It has three forms, weak-form, semi-strong form and strong –form of efficiency. In the first,

future year’s prices cannot be forecasted using historical year’s prices and investor will not be able

to get an excess return through performing technical & fundamental analysis and various

investment strategies (Ang, 2011). However, in the semi-strong form, the prices of the stock fully

adjust the publically available data set. Lastly, in strong-form, price reflects all set of information

and it is often exists in the existence of legal barriers and trading legislations. The theory also has

been criticised due to information biasness (Baker and Riddick, 2013). Besides this, the joint

hypothesis problem presents that it is impossible to test the efficiency of the market. Moreover,

return can only be increased by taking more risk in such situation; expected return will be less in

comparison to other securities which holds more stability.

3.2 Capital assets pricing model

CAPM theory presents the relationship between the expected estimated return and the

systematic investment risk. The model is based on the following equation, stated below:

Expected return = risk free rate + beta ( market risk – risk free rate)

Here, beta is measurement to assess and evaluate the volatility in the market and its impact

on the return. 1 value of it state that stock price moves exact as per the market trends however,

value below 1 indicates less volatility in the market or vice-versa (Dhrymes, 2017). The idea behind

invention of CAPM model is that investors can be compensated in two ways that are risk and time

value of currency which is presented by the Rf. On the other side, difference between market and

risk free rate shows premium that is presented by the SML (security market line). SML indicates the

level of systematic risk on different types of securities along with the expected return. The theory

suggests investors that they can create a diversified portfolio by incorporating riskier assets with the

less risky securities so as to minimize the overall risk of the portfolio (Cao, Han and Wang, 2017).

Modern theories suggests that systematic risk can be mitigated by the help of diversification,

however, in the actual corporate scenario, it is founded that systematic risk cannot be eliminated by

any way therefore, CAPM model is often used by the investors to quantified and analyse such risk

in the portfolio. As per the theory, DCF method is considered as the best model for the evaluation of

9

Thus, it is pointless to find out the undervalued stock or forecast the future trend through technical

and fundamental analysis. However, the critics argued that as per the theory of EMH, investors only

look towards the historical prices, earnings and past track records, it is because, prices are heavily

influenced by the expectations of the users. Thus, it just simply states that past stock price has a

great impact on the future price (Guerrien, 2011).

It has three forms, weak-form, semi-strong form and strong –form of efficiency. In the first,

future year’s prices cannot be forecasted using historical year’s prices and investor will not be able

to get an excess return through performing technical & fundamental analysis and various

investment strategies (Ang, 2011). However, in the semi-strong form, the prices of the stock fully

adjust the publically available data set. Lastly, in strong-form, price reflects all set of information

and it is often exists in the existence of legal barriers and trading legislations. The theory also has

been criticised due to information biasness (Baker and Riddick, 2013). Besides this, the joint

hypothesis problem presents that it is impossible to test the efficiency of the market. Moreover,

return can only be increased by taking more risk in such situation; expected return will be less in

comparison to other securities which holds more stability.

3.2 Capital assets pricing model

CAPM theory presents the relationship between the expected estimated return and the

systematic investment risk. The model is based on the following equation, stated below:

Expected return = risk free rate + beta ( market risk – risk free rate)

Here, beta is measurement to assess and evaluate the volatility in the market and its impact

on the return. 1 value of it state that stock price moves exact as per the market trends however,

value below 1 indicates less volatility in the market or vice-versa (Dhrymes, 2017). The idea behind

invention of CAPM model is that investors can be compensated in two ways that are risk and time

value of currency which is presented by the Rf. On the other side, difference between market and

risk free rate shows premium that is presented by the SML (security market line). SML indicates the

level of systematic risk on different types of securities along with the expected return. The theory

suggests investors that they can create a diversified portfolio by incorporating riskier assets with the

less risky securities so as to minimize the overall risk of the portfolio (Cao, Han and Wang, 2017).

Modern theories suggests that systematic risk can be mitigated by the help of diversification,

however, in the actual corporate scenario, it is founded that systematic risk cannot be eliminated by

any way therefore, CAPM model is often used by the investors to quantified and analyse such risk

in the portfolio. As per the theory, DCF method is considered as the best model for the evaluation of

9

You're viewing a preview

Unlock full access by subscribing today!

risk and return, in which, future year cash flows are discounted at the WACC (KUEHN, Simutin

and Wang, 2017).

3.3 Modern portfolio theory

This theory is helpful for the investors to maximize their total expected return on the

portfolio by minimizing the risk inherited. MPT model suggests that it is impossible for the investor

to design an efficient frontier that will give greater yield at a given level of risk. The theory assumed

that investors have rationale behaviour and they are risk-averse also. This is the reason why they are

intended to minimize their total risk on the investment to get the expected yield. It is also referred as

the portfolio management theory which believes that efficient frontier can be designed to gain

maximum return at a given level of risk (Chen, 2016). Thus, here investors can put money in more

than one securities and thereby reap diversification benefits so as to minimize their risk on the

portfolio. In this, various components such as beta, alpha, r-squared, standard deviation and sharpe

ratio can be used for making an analysis of the risk-return relationship on different kind of securities

(Grasse, Whaley and Ihrke, 2016).

3.4 Investment styles

In accordance with this theory, active investors are those who need professional money

managers to carefully choose their securities, in contrast, passive management do not depends upon

the professional money managers for deciding the investment structure to gain maximum yield.

However, the second style is value or growth investing, in which, investors make decisions whether

they are interested in investing money in fastly and rapidly growing companies or underpriced

firms, for such purpose, they examine the financial metrics (Del Viva, Kasanen and Trigeorgis,

2017). The growth style showcase exceeding earnings, high return, greater profit margin whilst, in

contrast, value style focuses on acquisition of a firm at a good price therefore, they consider less

price to earning ration, greater dividend and low price to sales ratio.

Lastly, under the small or large cap, they measure company’s sizes which are measured in

the terms of market capitalization. It is computed by multiplying the total number of outstanding

shares with the price of the stock (Peltomäki, 2017). Some of the investors believe that small sized

companies have higher opportunities therefore; they put money in small cap firms to drive better

return. On the other hand, risk-averse investors are interested in their fund security by putting

money in large cap stocks because they are well-established and have strong competitive position.

Here, they expect moderate or slightly less return in comparison to the small caps.

CONCLUSION BASED ON PORTFOLIO PERFORMANCE

Securities Amount Income Capital gain Capital gain %

10

and Wang, 2017).

3.3 Modern portfolio theory

This theory is helpful for the investors to maximize their total expected return on the

portfolio by minimizing the risk inherited. MPT model suggests that it is impossible for the investor

to design an efficient frontier that will give greater yield at a given level of risk. The theory assumed

that investors have rationale behaviour and they are risk-averse also. This is the reason why they are

intended to minimize their total risk on the investment to get the expected yield. It is also referred as

the portfolio management theory which believes that efficient frontier can be designed to gain

maximum return at a given level of risk (Chen, 2016). Thus, here investors can put money in more

than one securities and thereby reap diversification benefits so as to minimize their risk on the

portfolio. In this, various components such as beta, alpha, r-squared, standard deviation and sharpe

ratio can be used for making an analysis of the risk-return relationship on different kind of securities

(Grasse, Whaley and Ihrke, 2016).

3.4 Investment styles

In accordance with this theory, active investors are those who need professional money

managers to carefully choose their securities, in contrast, passive management do not depends upon

the professional money managers for deciding the investment structure to gain maximum yield.

However, the second style is value or growth investing, in which, investors make decisions whether

they are interested in investing money in fastly and rapidly growing companies or underpriced

firms, for such purpose, they examine the financial metrics (Del Viva, Kasanen and Trigeorgis,

2017). The growth style showcase exceeding earnings, high return, greater profit margin whilst, in

contrast, value style focuses on acquisition of a firm at a good price therefore, they consider less

price to earning ration, greater dividend and low price to sales ratio.

Lastly, under the small or large cap, they measure company’s sizes which are measured in

the terms of market capitalization. It is computed by multiplying the total number of outstanding

shares with the price of the stock (Peltomäki, 2017). Some of the investors believe that small sized

companies have higher opportunities therefore; they put money in small cap firms to drive better

return. On the other hand, risk-averse investors are interested in their fund security by putting

money in large cap stocks because they are well-established and have strong competitive position.

Here, they expect moderate or slightly less return in comparison to the small caps.

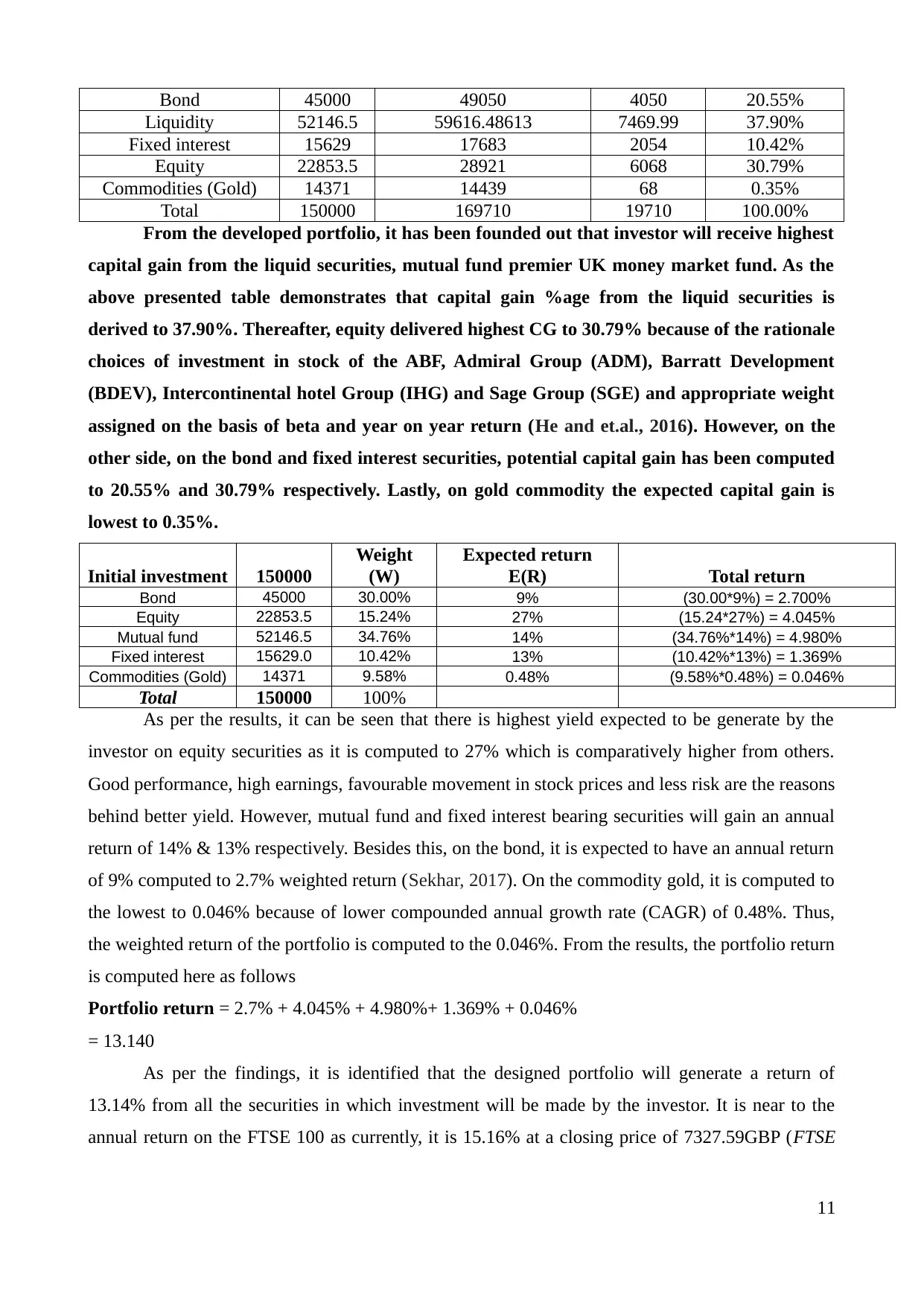

CONCLUSION BASED ON PORTFOLIO PERFORMANCE

Securities Amount Income Capital gain Capital gain %

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bond 45000 49050 4050 20.55%

Liquidity 52146.5 59616.48613 7469.99 37.90%

Fixed interest 15629 17683 2054 10.42%

Equity 22853.5 28921 6068 30.79%

Commodities (Gold) 14371 14439 68 0.35%

Total 150000 169710 19710 100.00%

From the developed portfolio, it has been founded out that investor will receive highest

capital gain from the liquid securities, mutual fund premier UK money market fund. As the

above presented table demonstrates that capital gain %age from the liquid securities is

derived to 37.90%. Thereafter, equity delivered highest CG to 30.79% because of the rationale

choices of investment in stock of the ABF, Admiral Group (ADM), Barratt Development

(BDEV), Intercontinental hotel Group (IHG) and Sage Group (SGE) and appropriate weight

assigned on the basis of beta and year on year return (He and et.al., 2016). However, on the

other side, on the bond and fixed interest securities, potential capital gain has been computed

to 20.55% and 30.79% respectively. Lastly, on gold commodity the expected capital gain is

lowest to 0.35%.

Initial investment 150000

Weight

(W)

Expected return

E(R) Total return

Bond 45000 30.00% 9% (30.00*9%) = 2.700%

Equity 22853.5 15.24% 27% (15.24*27%) = 4.045%

Mutual fund 52146.5 34.76% 14% (34.76%*14%) = 4.980%

Fixed interest 15629.0 10.42% 13% (10.42%*13%) = 1.369%

Commodities (Gold) 14371 9.58% 0.48% (9.58%*0.48%) = 0.046%

Total 150000 100%

As per the results, it can be seen that there is highest yield expected to be generate by the

investor on equity securities as it is computed to 27% which is comparatively higher from others.

Good performance, high earnings, favourable movement in stock prices and less risk are the reasons

behind better yield. However, mutual fund and fixed interest bearing securities will gain an annual

return of 14% & 13% respectively. Besides this, on the bond, it is expected to have an annual return

of 9% computed to 2.7% weighted return (Sekhar, 2017). On the commodity gold, it is computed to

the lowest to 0.046% because of lower compounded annual growth rate (CAGR) of 0.48%. Thus,

the weighted return of the portfolio is computed to the 0.046%. From the results, the portfolio return

is computed here as follows

Portfolio return = 2.7% + 4.045% + 4.980%+ 1.369% + 0.046%

= 13.140

As per the findings, it is identified that the designed portfolio will generate a return of

13.14% from all the securities in which investment will be made by the investor. It is near to the

annual return on the FTSE 100 as currently, it is 15.16% at a closing price of 7327.59GBP (FTSE

11

Liquidity 52146.5 59616.48613 7469.99 37.90%

Fixed interest 15629 17683 2054 10.42%

Equity 22853.5 28921 6068 30.79%

Commodities (Gold) 14371 14439 68 0.35%

Total 150000 169710 19710 100.00%

From the developed portfolio, it has been founded out that investor will receive highest

capital gain from the liquid securities, mutual fund premier UK money market fund. As the

above presented table demonstrates that capital gain %age from the liquid securities is

derived to 37.90%. Thereafter, equity delivered highest CG to 30.79% because of the rationale

choices of investment in stock of the ABF, Admiral Group (ADM), Barratt Development

(BDEV), Intercontinental hotel Group (IHG) and Sage Group (SGE) and appropriate weight

assigned on the basis of beta and year on year return (He and et.al., 2016). However, on the

other side, on the bond and fixed interest securities, potential capital gain has been computed

to 20.55% and 30.79% respectively. Lastly, on gold commodity the expected capital gain is

lowest to 0.35%.

Initial investment 150000

Weight

(W)

Expected return

E(R) Total return

Bond 45000 30.00% 9% (30.00*9%) = 2.700%

Equity 22853.5 15.24% 27% (15.24*27%) = 4.045%

Mutual fund 52146.5 34.76% 14% (34.76%*14%) = 4.980%

Fixed interest 15629.0 10.42% 13% (10.42%*13%) = 1.369%

Commodities (Gold) 14371 9.58% 0.48% (9.58%*0.48%) = 0.046%

Total 150000 100%

As per the results, it can be seen that there is highest yield expected to be generate by the

investor on equity securities as it is computed to 27% which is comparatively higher from others.

Good performance, high earnings, favourable movement in stock prices and less risk are the reasons

behind better yield. However, mutual fund and fixed interest bearing securities will gain an annual

return of 14% & 13% respectively. Besides this, on the bond, it is expected to have an annual return

of 9% computed to 2.7% weighted return (Sekhar, 2017). On the commodity gold, it is computed to

the lowest to 0.046% because of lower compounded annual growth rate (CAGR) of 0.48%. Thus,

the weighted return of the portfolio is computed to the 0.046%. From the results, the portfolio return

is computed here as follows

Portfolio return = 2.7% + 4.045% + 4.980%+ 1.369% + 0.046%

= 13.140

As per the findings, it is identified that the designed portfolio will generate a return of

13.14% from all the securities in which investment will be made by the investor. It is near to the

annual return on the FTSE 100 as currently, it is 15.16% at a closing price of 7327.59GBP (FTSE

11

100 Index’s share price, 2017). Hence, after evaluating the results, it becomes clear that the

designed portfolio will drive good return to the investor and drive good return for the risk taken by

investing the money.

12

designed portfolio will drive good return to the investor and drive good return for the risk taken by

investing the money.

12

You're viewing a preview

Unlock full access by subscribing today!

REFERENCES

Books and Journals

Ambrosin, and et. al., 2015. Advanced strategic management: A multi-perspective approach.

Palgrave Macmillan.

Auer, B.R., 2016. Do Socially Responsible Investment Policies Add or Destroy European Stock

Portfolio Value?. Journal of Business Ethics. 135(2). pp.381-397.

Baker, H.K. and Riddick, L.A., 2013. International finance: a survey. Oxford University Press.

Cao, J., Han, B. and Wang, Q., 2017. Institutional investment constraints and stock prices. Journal

of Financial and Quantitative Analysis. pp.1-25.

Chen, J.M., 2016. Modern Portfolio Theory. In Postmodern Portfolio Theory. Palgrave Macmillan

US. 12(3). pp.5-25.

Del Viva, L., Kasanen, E. and Trigeorgis, L., 2017. Real Options, Idiosyncratic Skewness, and

Diversification. Journal of Financial and Quantitative Analysis. 52(1). pp.215-241.

Dhrymes, P.J., 2017. Portfolio Theory: Origins, Markowitz and CAPM Based Selection.

In Portfolio Construction, Measurement, and Efficiency. Springer International Publishing.

10(2). pp. 39-48.

Grasse, N.J., Whaley, K.M. and Ihrke, D.M., 2016. Modern Portfolio Theory and Nonprofit Arts

Organizations: Identifying the Efficient Frontier. Nonprofit and Voluntary Sector

Quarterly. 45(4). pp.825-843.

He, K. and et.al., 2016. Multiscale dependence analysis and portfolio risk modeling for precious

metal markets. Resources Policy. 50(12). pp.224-233.

Kenfack, H. and et.al., 2016. The pricing of illiquidity risk on emerging stock exchange markets: A

portfolio panel data analysis. Journal of Economics and International Finance. 8(8). pp.127-

141.

KUEHN, L.A., Simutin, M. and Wang, J.J., 2017. A labor capital asset pricing model. The Journal

of Finance. 12(3). pp.16-39.

Peltomäki, J., 2017. Investment Styles and the Multifactor Analysis of Market Timing

Skill. International Journal of Managerial Finance. 13(1). pp.16-36.

Rutterford, J., 2016. Asset Allocation in Investment. Palgrave Macmillan US.

Sekhar, G.S., 2017. Portfolio Management. In The Management of Mutual Funds. Springer

International Publishing. 12(3). pp.133-148.

Standaert, T. and Manigart, S., 2017. Government as fund-of-fund and VC fund sponsors: effect on

employment in portfolio companies. Small Business Economics. 12(4). pp.1-17.

13

Books and Journals

Ambrosin, and et. al., 2015. Advanced strategic management: A multi-perspective approach.

Palgrave Macmillan.

Auer, B.R., 2016. Do Socially Responsible Investment Policies Add or Destroy European Stock

Portfolio Value?. Journal of Business Ethics. 135(2). pp.381-397.

Baker, H.K. and Riddick, L.A., 2013. International finance: a survey. Oxford University Press.

Cao, J., Han, B. and Wang, Q., 2017. Institutional investment constraints and stock prices. Journal

of Financial and Quantitative Analysis. pp.1-25.

Chen, J.M., 2016. Modern Portfolio Theory. In Postmodern Portfolio Theory. Palgrave Macmillan

US. 12(3). pp.5-25.

Del Viva, L., Kasanen, E. and Trigeorgis, L., 2017. Real Options, Idiosyncratic Skewness, and

Diversification. Journal of Financial and Quantitative Analysis. 52(1). pp.215-241.

Dhrymes, P.J., 2017. Portfolio Theory: Origins, Markowitz and CAPM Based Selection.

In Portfolio Construction, Measurement, and Efficiency. Springer International Publishing.

10(2). pp. 39-48.

Grasse, N.J., Whaley, K.M. and Ihrke, D.M., 2016. Modern Portfolio Theory and Nonprofit Arts

Organizations: Identifying the Efficient Frontier. Nonprofit and Voluntary Sector

Quarterly. 45(4). pp.825-843.

He, K. and et.al., 2016. Multiscale dependence analysis and portfolio risk modeling for precious

metal markets. Resources Policy. 50(12). pp.224-233.

Kenfack, H. and et.al., 2016. The pricing of illiquidity risk on emerging stock exchange markets: A

portfolio panel data analysis. Journal of Economics and International Finance. 8(8). pp.127-

141.

KUEHN, L.A., Simutin, M. and Wang, J.J., 2017. A labor capital asset pricing model. The Journal

of Finance. 12(3). pp.16-39.

Peltomäki, J., 2017. Investment Styles and the Multifactor Analysis of Market Timing

Skill. International Journal of Managerial Finance. 13(1). pp.16-36.

Rutterford, J., 2016. Asset Allocation in Investment. Palgrave Macmillan US.

Sekhar, G.S., 2017. Portfolio Management. In The Management of Mutual Funds. Springer

International Publishing. 12(3). pp.133-148.

Standaert, T. and Manigart, S., 2017. Government as fund-of-fund and VC fund sponsors: effect on

employment in portfolio companies. Small Business Economics. 12(4). pp.1-17.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tong, J., Hu, J. and Hu, J., 2017. Computing equilibrium prices for a capital asset pricing model

with heterogeneous beliefs and margin-requirement constraints. European Journal of

Operational Research. 256(1). pp.24-34.

Online

Ang, A., 2011. Review of the Efficient Market Theory and Evidence. [Online]. Accessed

Through:<https://www0.gsb.columbia.edu/faculty/aang/papers/EMH.pdf>: [Accessed on

17th April 2017].

FTSE 100 Index’s share price. 2017. [Online]. Available through: <

https://markets.ft.com/data/indices/tearsheet/summary?s=FTSE:FSI>. [Accessed on 17th

April 2017]

Guerrien, B., 2011. Efficient Market Hypothesis: What are we talking about?. [Online]. Accessed

Through:<http://www.paecon.net/PAEReview/issue56/GuerrienGun56.pdf>: [Accessed on

17th April 2017].

14

with heterogeneous beliefs and margin-requirement constraints. European Journal of

Operational Research. 256(1). pp.24-34.

Online

Ang, A., 2011. Review of the Efficient Market Theory and Evidence. [Online]. Accessed

Through:<https://www0.gsb.columbia.edu/faculty/aang/papers/EMH.pdf>: [Accessed on

17th April 2017].

FTSE 100 Index’s share price. 2017. [Online]. Available through: <

https://markets.ft.com/data/indices/tearsheet/summary?s=FTSE:FSI>. [Accessed on 17th

April 2017]

Guerrien, B., 2011. Efficient Market Hypothesis: What are we talking about?. [Online]. Accessed

Through:<http://www.paecon.net/PAEReview/issue56/GuerrienGun56.pdf>: [Accessed on

17th April 2017].

14

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.