Risk Management Model for Desklib - Analysis of CAPM, Systematic Risk, Alpha, Validity of Model, Sharpe Measure and Treynor Measure

VerifiedAdded on 2022/11/14

|12

|2237

|330

AI Summary

The Risk Management Model for Desklib includes analysis of CAPM, Systematic Risk, Alpha, Validity of Model, Sharpe Measure and Treynor Measure. It covers portfolio return, required rate of return, and risk adjusted performance of assets. The report also provides insights on the interpretation of R2 and the comparison among the results.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Risk Management Model

1

Project Report: Risk Management Model

1

Project Report: Risk Management Model

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Risk Management Model

2

Contents

Task 1................................................................................................................................3

a) CAPM.......................................................................................................................3

b) Portfolio Return........................................................................................................3

Task 2................................................................................................................................3

Systematic risk..............................................................................................................3

Alpha.............................................................................................................................4

Validity of model..........................................................................................................4

Interpretation of R2.......................................................................................................6

Required rate of return..................................................................................................6

Task 3................................................................................................................................7

Sharpe measure and Treynor Measure of single asset..................................................7

Sharpe measure and Treynor Measure of portfolio asset.............................................8

Comparison among the results......................................................................................9

References:.....................................................................................................................10

Appendix.........................................................................................................................11

2

Contents

Task 1................................................................................................................................3

a) CAPM.......................................................................................................................3

b) Portfolio Return........................................................................................................3

Task 2................................................................................................................................3

Systematic risk..............................................................................................................3

Alpha.............................................................................................................................4

Validity of model..........................................................................................................4

Interpretation of R2.......................................................................................................6

Required rate of return..................................................................................................6

Task 3................................................................................................................................7

Sharpe measure and Treynor Measure of single asset..................................................7

Sharpe measure and Treynor Measure of portfolio asset.............................................8

Comparison among the results......................................................................................9

References:.....................................................................................................................10

Appendix.........................................................................................................................11

Risk Management Model

3

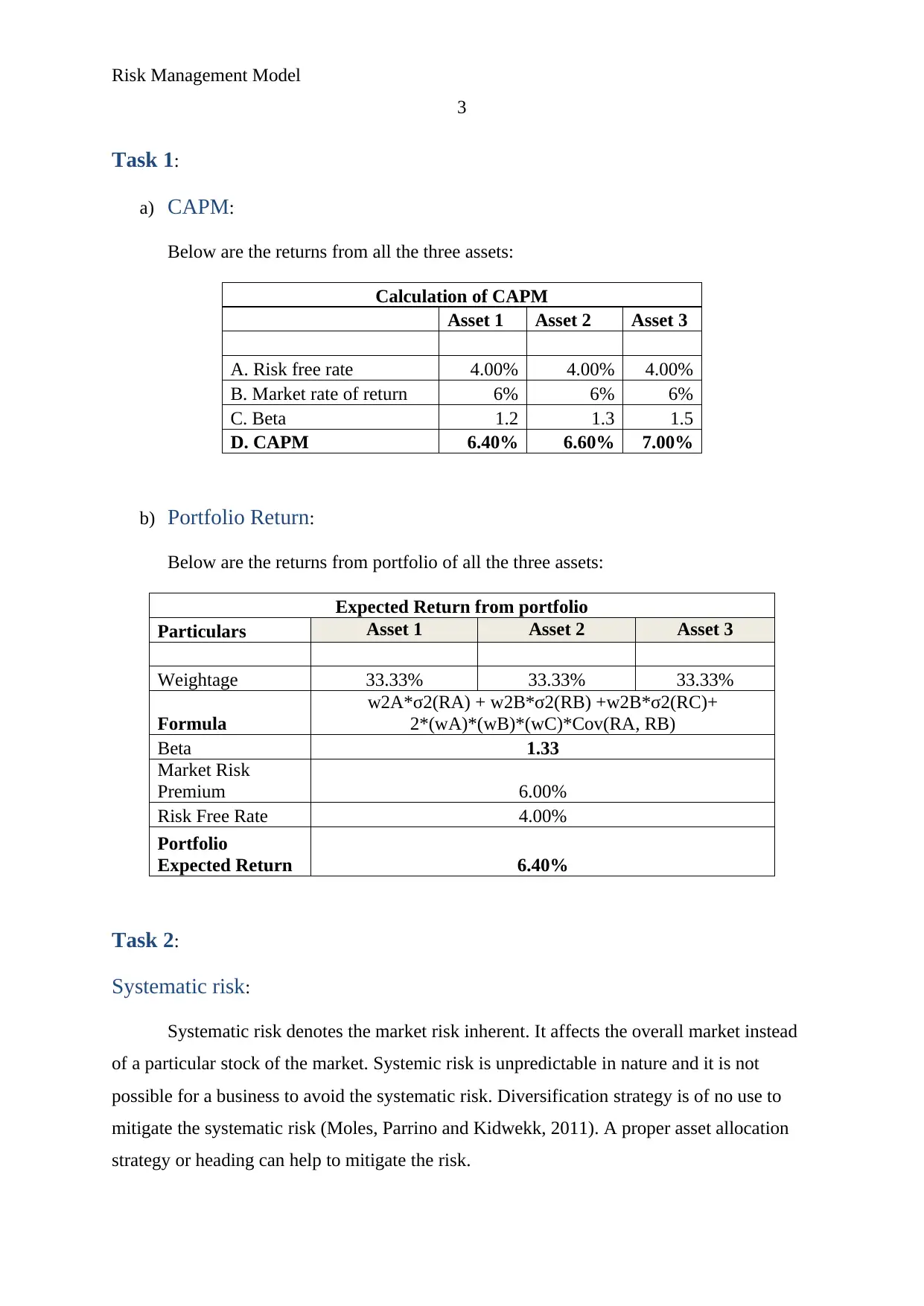

Task 1:

a) CAPM:

Below are the returns from all the three assets:

Calculation of CAPM

Asset 1 Asset 2 Asset 3

A. Risk free rate 4.00% 4.00% 4.00%

B. Market rate of return 6% 6% 6%

C. Beta 1.2 1.3 1.5

D. CAPM 6.40% 6.60% 7.00%

b) Portfolio Return:

Below are the returns from portfolio of all the three assets:

Expected Return from portfolio

Particulars Asset 1 Asset 2 Asset 3

Weightage 33.33% 33.33% 33.33%

Formula

w2A*σ2(RA) + w2B*σ2(RB) +w2B*σ2(RC)+

2*(wA)*(wB)*(wC)*Cov(RA, RB)

Beta 1.33

Market Risk

Premium 6.00%

Risk Free Rate 4.00%

Portfolio

Expected Return 6.40%

Task 2:

Systematic risk:

Systematic risk denotes the market risk inherent. It affects the overall market instead

of a particular stock of the market. Systemic risk is unpredictable in nature and it is not

possible for a business to avoid the systematic risk. Diversification strategy is of no use to

mitigate the systematic risk (Moles, Parrino and Kidwekk, 2011). A proper asset allocation

strategy or heading can help to mitigate the risk.

3

Task 1:

a) CAPM:

Below are the returns from all the three assets:

Calculation of CAPM

Asset 1 Asset 2 Asset 3

A. Risk free rate 4.00% 4.00% 4.00%

B. Market rate of return 6% 6% 6%

C. Beta 1.2 1.3 1.5

D. CAPM 6.40% 6.60% 7.00%

b) Portfolio Return:

Below are the returns from portfolio of all the three assets:

Expected Return from portfolio

Particulars Asset 1 Asset 2 Asset 3

Weightage 33.33% 33.33% 33.33%

Formula

w2A*σ2(RA) + w2B*σ2(RB) +w2B*σ2(RC)+

2*(wA)*(wB)*(wC)*Cov(RA, RB)

Beta 1.33

Market Risk

Premium 6.00%

Risk Free Rate 4.00%

Portfolio

Expected Return 6.40%

Task 2:

Systematic risk:

Systematic risk denotes the market risk inherent. It affects the overall market instead

of a particular stock of the market. Systemic risk is unpredictable in nature and it is not

possible for a business to avoid the systematic risk. Diversification strategy is of no use to

mitigate the systematic risk (Moles, Parrino and Kidwekk, 2011). A proper asset allocation

strategy or heading can help to mitigate the risk.

Risk Management Model

4

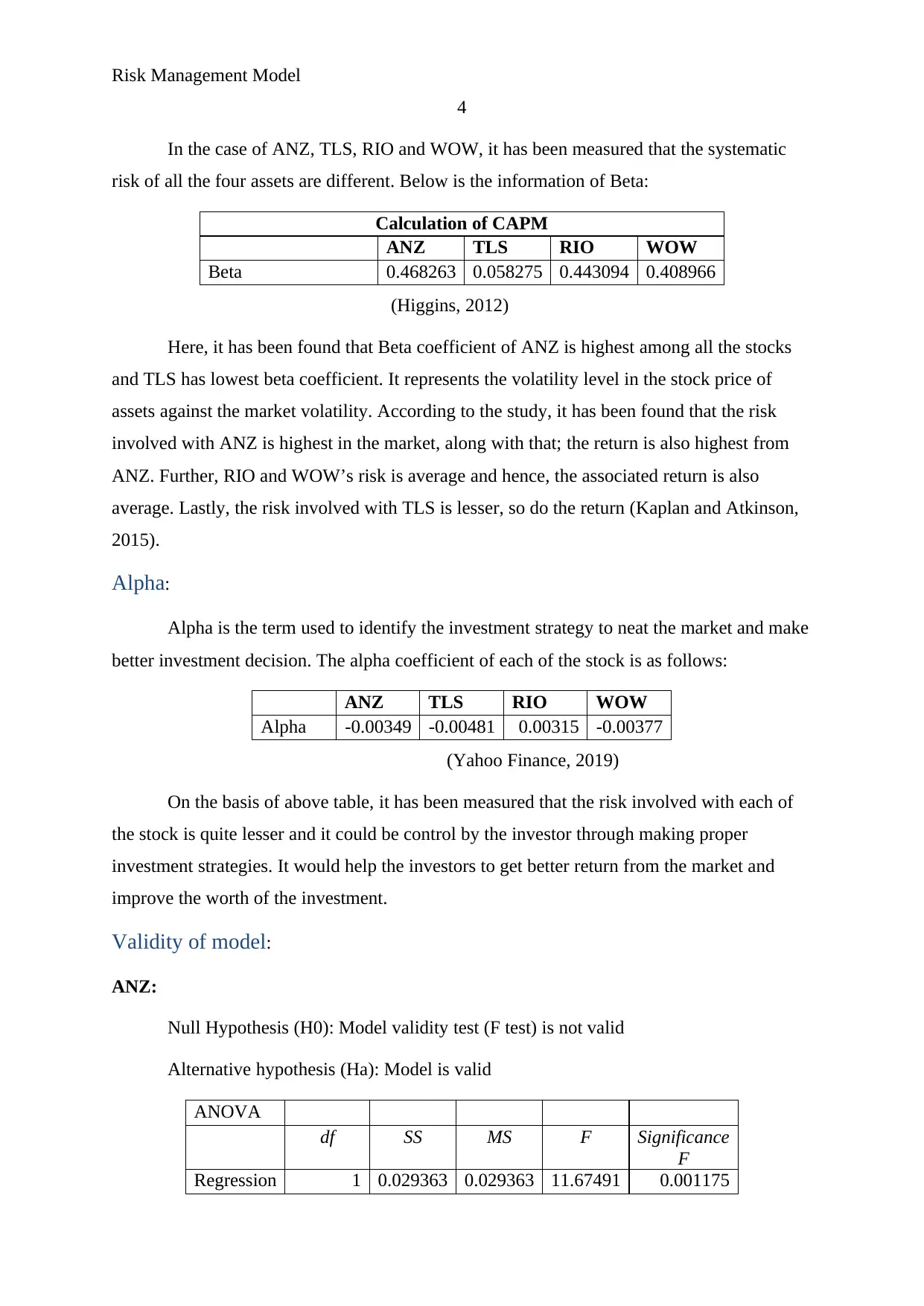

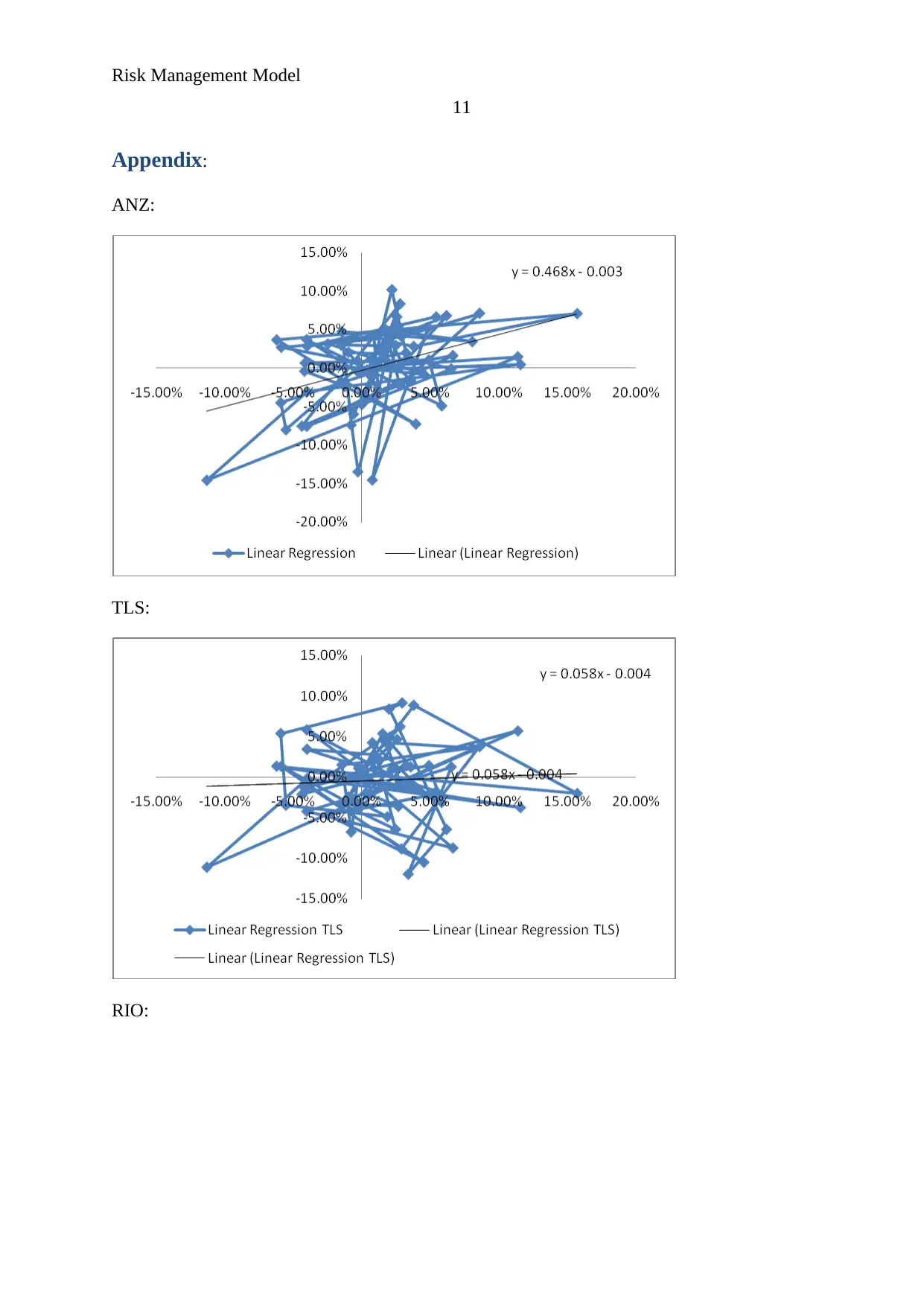

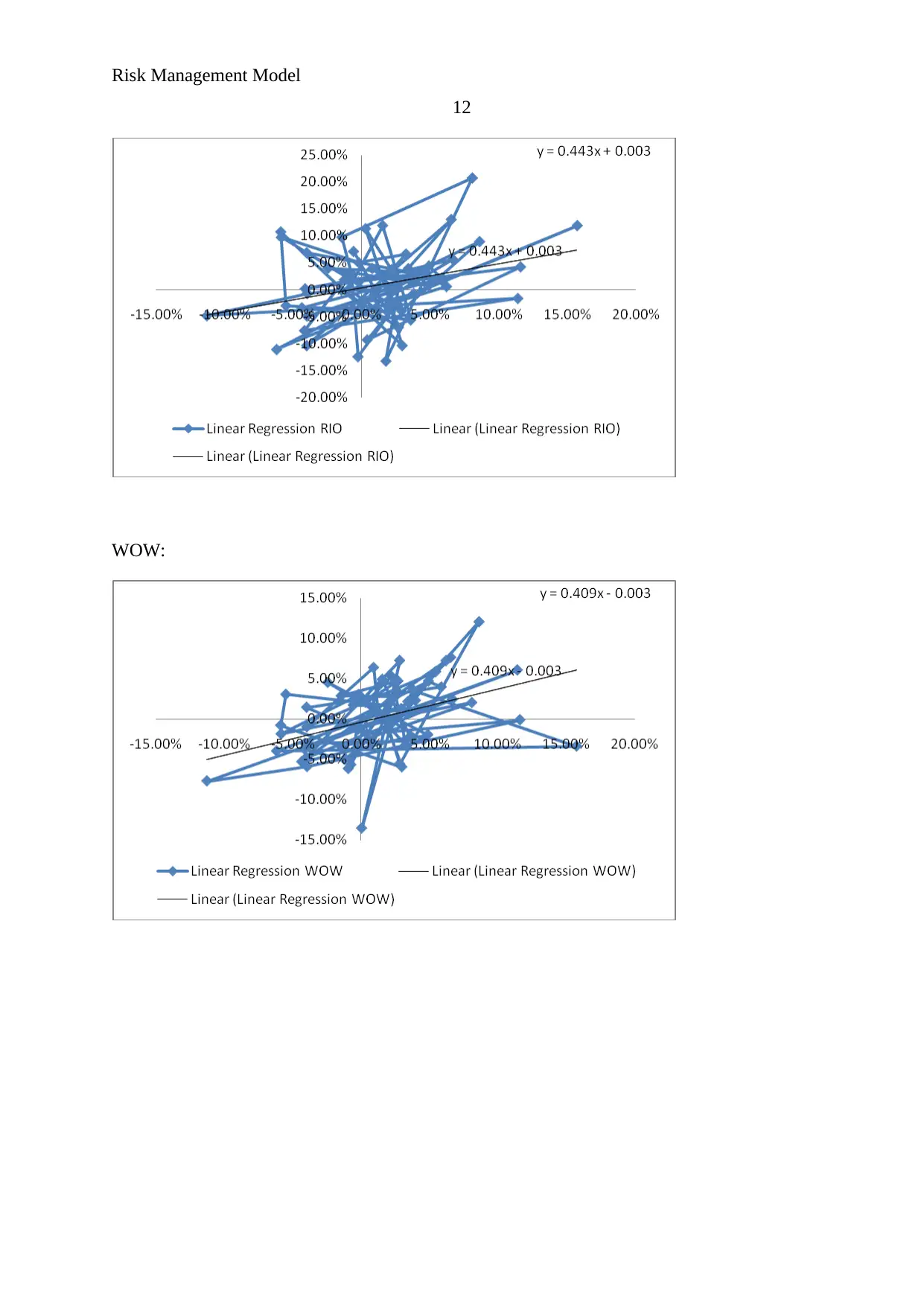

In the case of ANZ, TLS, RIO and WOW, it has been measured that the systematic

risk of all the four assets are different. Below is the information of Beta:

Calculation of CAPM

ANZ TLS RIO WOW

Beta 0.468263 0.058275 0.443094 0.408966

(Higgins, 2012)

Here, it has been found that Beta coefficient of ANZ is highest among all the stocks

and TLS has lowest beta coefficient. It represents the volatility level in the stock price of

assets against the market volatility. According to the study, it has been found that the risk

involved with ANZ is highest in the market, along with that; the return is also highest from

ANZ. Further, RIO and WOW’s risk is average and hence, the associated return is also

average. Lastly, the risk involved with TLS is lesser, so do the return (Kaplan and Atkinson,

2015).

Alpha:

Alpha is the term used to identify the investment strategy to neat the market and make

better investment decision. The alpha coefficient of each of the stock is as follows:

ANZ TLS RIO WOW

Alpha -0.00349 -0.00481 0.00315 -0.00377

(Yahoo Finance, 2019)

On the basis of above table, it has been measured that the risk involved with each of

the stock is quite lesser and it could be control by the investor through making proper

investment strategies. It would help the investors to get better return from the market and

improve the worth of the investment.

Validity of model:

ANZ:

Null Hypothesis (H0): Model validity test (F test) is not valid

Alternative hypothesis (Ha): Model is valid

ANOVA

df SS MS F Significance

F

Regression 1 0.029363 0.029363 11.67491 0.001175

4

In the case of ANZ, TLS, RIO and WOW, it has been measured that the systematic

risk of all the four assets are different. Below is the information of Beta:

Calculation of CAPM

ANZ TLS RIO WOW

Beta 0.468263 0.058275 0.443094 0.408966

(Higgins, 2012)

Here, it has been found that Beta coefficient of ANZ is highest among all the stocks

and TLS has lowest beta coefficient. It represents the volatility level in the stock price of

assets against the market volatility. According to the study, it has been found that the risk

involved with ANZ is highest in the market, along with that; the return is also highest from

ANZ. Further, RIO and WOW’s risk is average and hence, the associated return is also

average. Lastly, the risk involved with TLS is lesser, so do the return (Kaplan and Atkinson,

2015).

Alpha:

Alpha is the term used to identify the investment strategy to neat the market and make

better investment decision. The alpha coefficient of each of the stock is as follows:

ANZ TLS RIO WOW

Alpha -0.00349 -0.00481 0.00315 -0.00377

(Yahoo Finance, 2019)

On the basis of above table, it has been measured that the risk involved with each of

the stock is quite lesser and it could be control by the investor through making proper

investment strategies. It would help the investors to get better return from the market and

improve the worth of the investment.

Validity of model:

ANZ:

Null Hypothesis (H0): Model validity test (F test) is not valid

Alternative hypothesis (Ha): Model is valid

ANOVA

df SS MS F Significance

F

Regression 1 0.029363 0.029363 11.67491 0.001175

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Risk Management Model

5

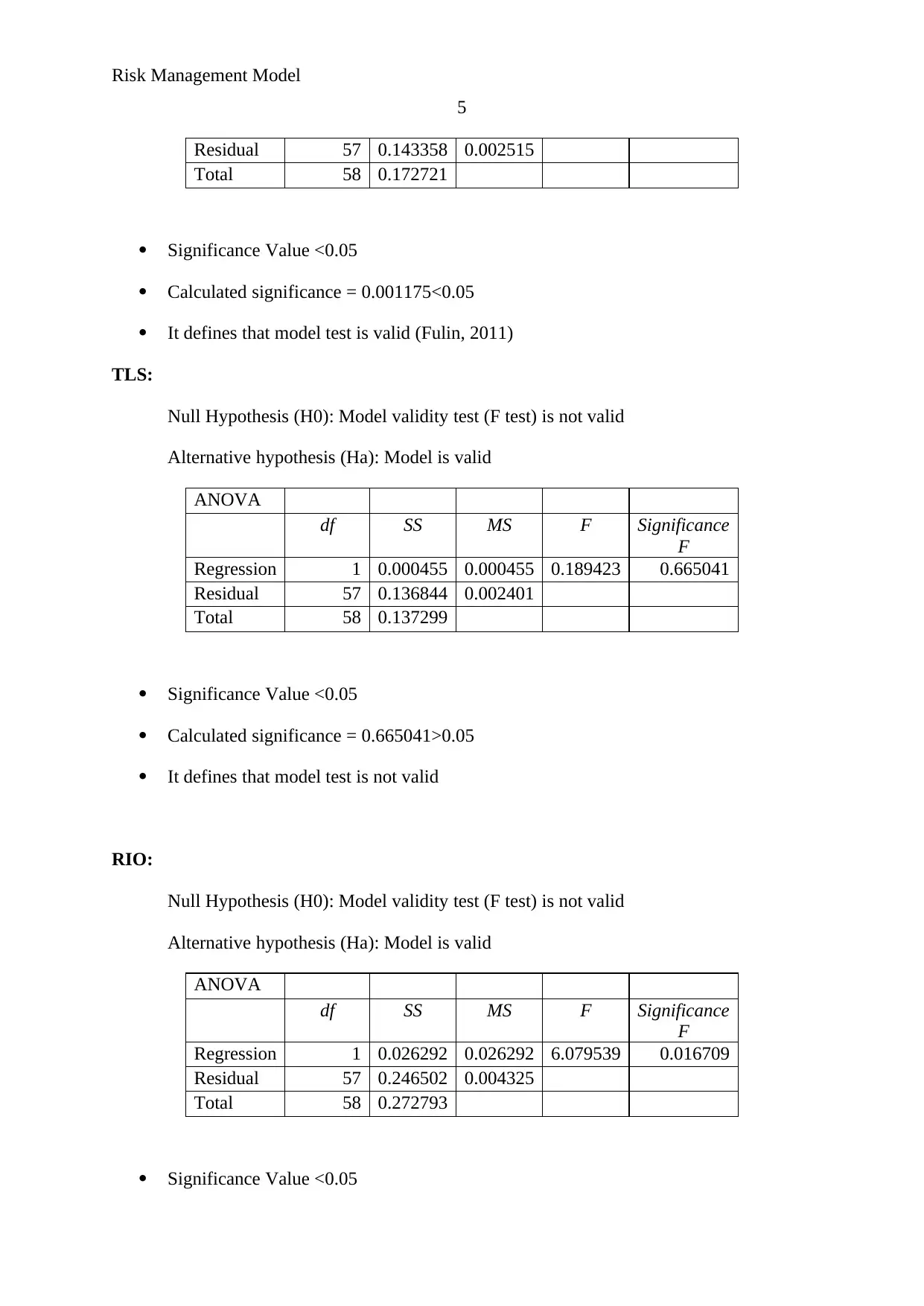

Residual 57 0.143358 0.002515

Total 58 0.172721

Significance Value <0.05

Calculated significance = 0.001175<0.05

It defines that model test is valid (Fulin, 2011)

TLS:

Null Hypothesis (H0): Model validity test (F test) is not valid

Alternative hypothesis (Ha): Model is valid

ANOVA

df SS MS F Significance

F

Regression 1 0.000455 0.000455 0.189423 0.665041

Residual 57 0.136844 0.002401

Total 58 0.137299

Significance Value <0.05

Calculated significance = 0.665041>0.05

It defines that model test is not valid

RIO:

Null Hypothesis (H0): Model validity test (F test) is not valid

Alternative hypothesis (Ha): Model is valid

ANOVA

df SS MS F Significance

F

Regression 1 0.026292 0.026292 6.079539 0.016709

Residual 57 0.246502 0.004325

Total 58 0.272793

Significance Value <0.05

5

Residual 57 0.143358 0.002515

Total 58 0.172721

Significance Value <0.05

Calculated significance = 0.001175<0.05

It defines that model test is valid (Fulin, 2011)

TLS:

Null Hypothesis (H0): Model validity test (F test) is not valid

Alternative hypothesis (Ha): Model is valid

ANOVA

df SS MS F Significance

F

Regression 1 0.000455 0.000455 0.189423 0.665041

Residual 57 0.136844 0.002401

Total 58 0.137299

Significance Value <0.05

Calculated significance = 0.665041>0.05

It defines that model test is not valid

RIO:

Null Hypothesis (H0): Model validity test (F test) is not valid

Alternative hypothesis (Ha): Model is valid

ANOVA

df SS MS F Significance

F

Regression 1 0.026292 0.026292 6.079539 0.016709

Residual 57 0.246502 0.004325

Total 58 0.272793

Significance Value <0.05

Risk Management Model

6

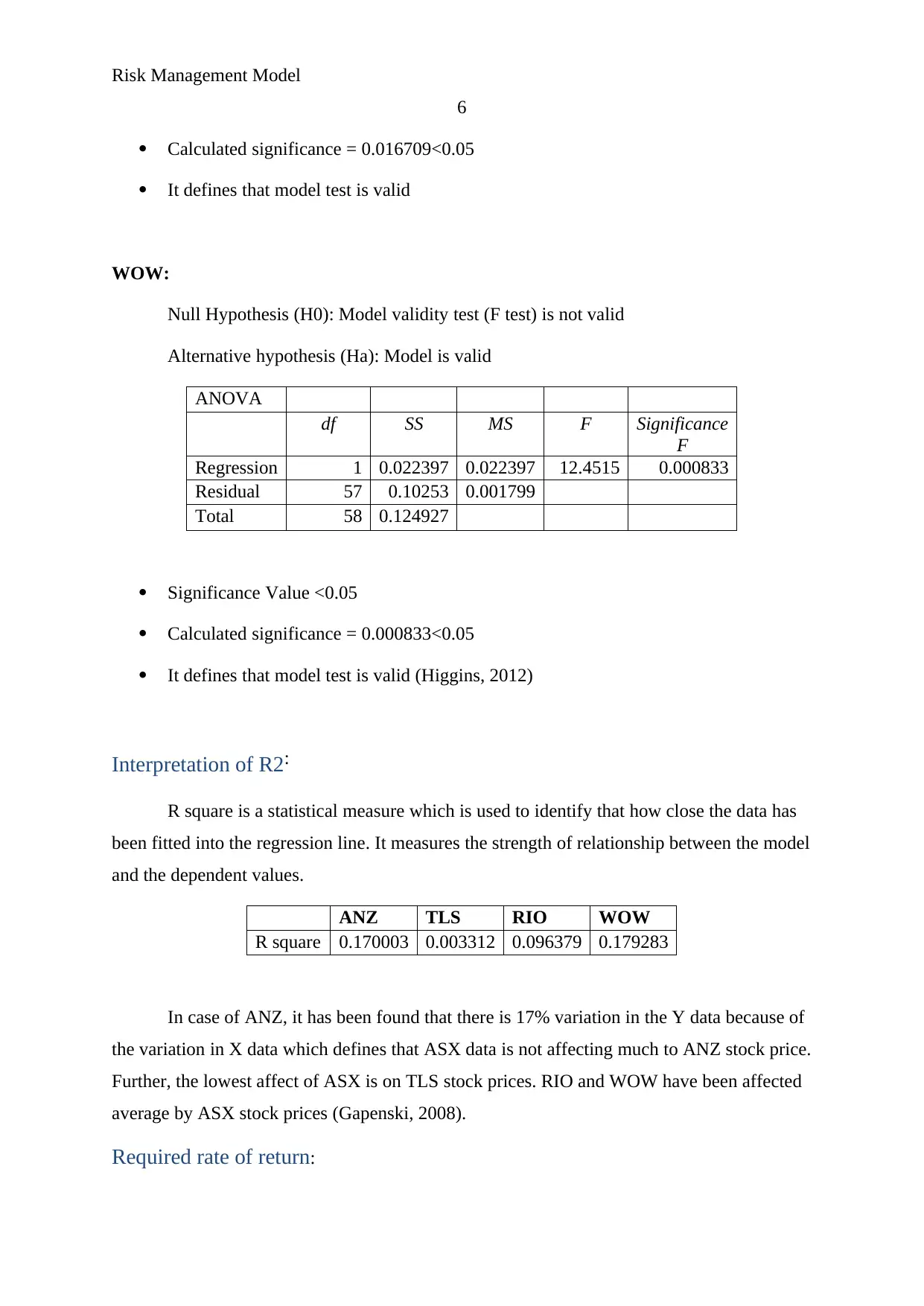

Calculated significance = 0.016709<0.05

It defines that model test is valid

WOW:

Null Hypothesis (H0): Model validity test (F test) is not valid

Alternative hypothesis (Ha): Model is valid

ANOVA

df SS MS F Significance

F

Regression 1 0.022397 0.022397 12.4515 0.000833

Residual 57 0.10253 0.001799

Total 58 0.124927

Significance Value <0.05

Calculated significance = 0.000833<0.05

It defines that model test is valid (Higgins, 2012)

Interpretation of R2:

R square is a statistical measure which is used to identify that how close the data has

been fitted into the regression line. It measures the strength of relationship between the model

and the dependent values.

ANZ TLS RIO WOW

R square 0.170003 0.003312 0.096379 0.179283

In case of ANZ, it has been found that there is 17% variation in the Y data because of

the variation in X data which defines that ASX data is not affecting much to ANZ stock price.

Further, the lowest affect of ASX is on TLS stock prices. RIO and WOW have been affected

average by ASX stock prices (Gapenski, 2008).

Required rate of return:

6

Calculated significance = 0.016709<0.05

It defines that model test is valid

WOW:

Null Hypothesis (H0): Model validity test (F test) is not valid

Alternative hypothesis (Ha): Model is valid

ANOVA

df SS MS F Significance

F

Regression 1 0.022397 0.022397 12.4515 0.000833

Residual 57 0.10253 0.001799

Total 58 0.124927

Significance Value <0.05

Calculated significance = 0.000833<0.05

It defines that model test is valid (Higgins, 2012)

Interpretation of R2:

R square is a statistical measure which is used to identify that how close the data has

been fitted into the regression line. It measures the strength of relationship between the model

and the dependent values.

ANZ TLS RIO WOW

R square 0.170003 0.003312 0.096379 0.179283

In case of ANZ, it has been found that there is 17% variation in the Y data because of

the variation in X data which defines that ASX data is not affecting much to ANZ stock price.

Further, the lowest affect of ASX is on TLS stock prices. RIO and WOW have been affected

average by ASX stock prices (Gapenski, 2008).

Required rate of return:

Risk Management Model

7

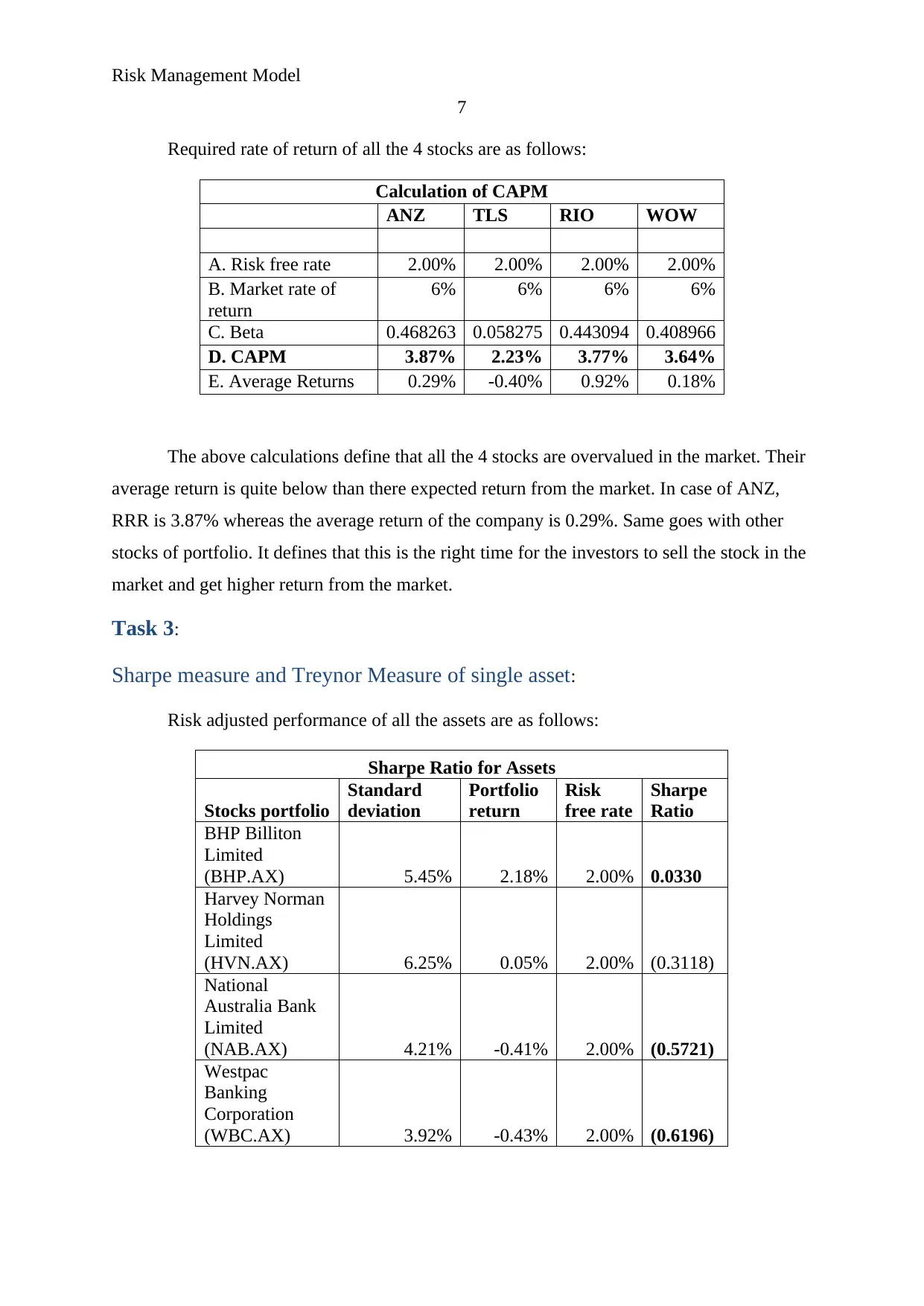

Required rate of return of all the 4 stocks are as follows:

Calculation of CAPM

ANZ TLS RIO WOW

A. Risk free rate 2.00% 2.00% 2.00% 2.00%

B. Market rate of

return

6% 6% 6% 6%

C. Beta 0.468263 0.058275 0.443094 0.408966

D. CAPM 3.87% 2.23% 3.77% 3.64%

E. Average Returns 0.29% -0.40% 0.92% 0.18%

The above calculations define that all the 4 stocks are overvalued in the market. Their

average return is quite below than there expected return from the market. In case of ANZ,

RRR is 3.87% whereas the average return of the company is 0.29%. Same goes with other

stocks of portfolio. It defines that this is the right time for the investors to sell the stock in the

market and get higher return from the market.

Task 3:

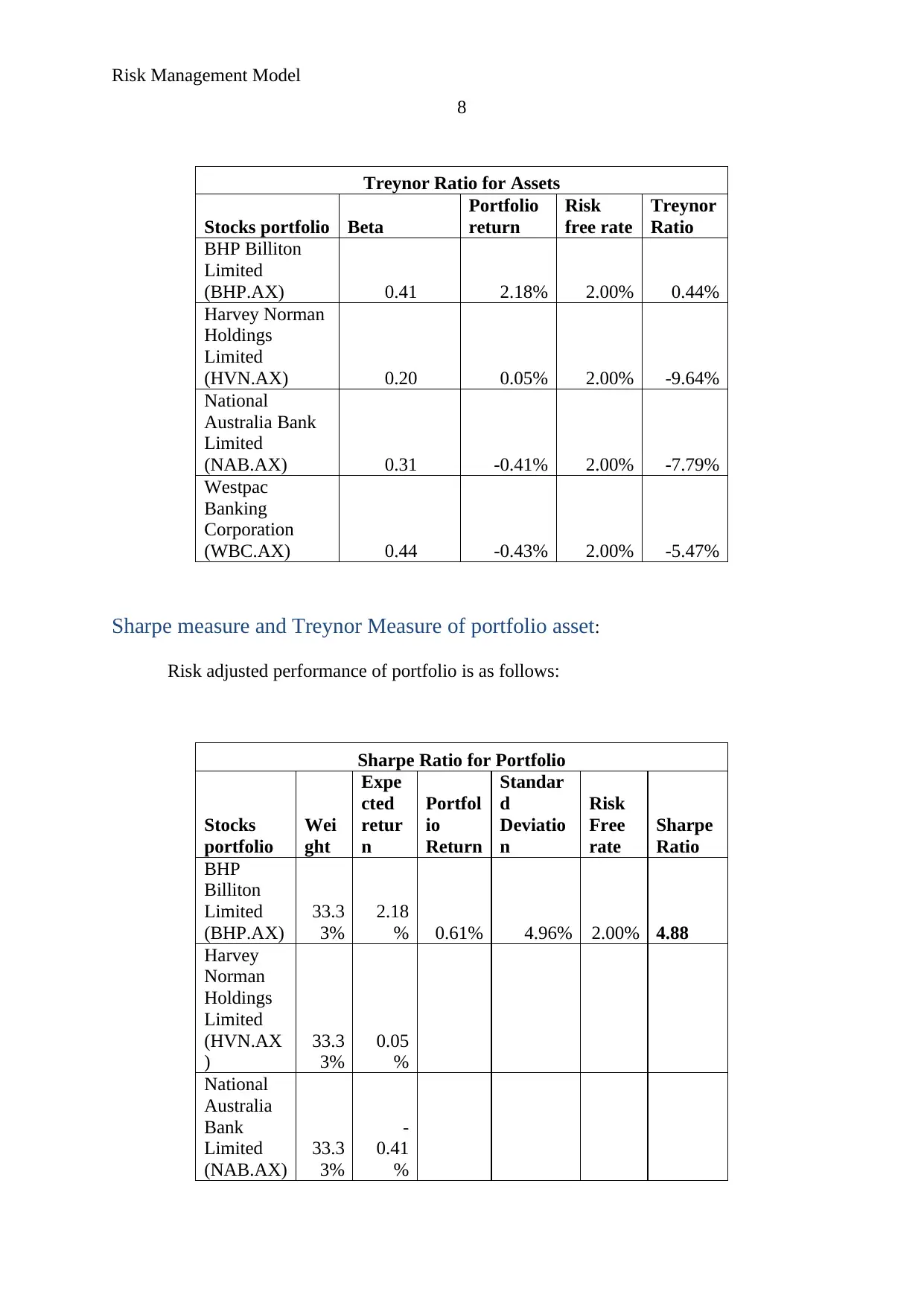

Sharpe measure and Treynor Measure of single asset:

Risk adjusted performance of all the assets are as follows:

Sharpe Ratio for Assets

Stocks portfolio

Standard

deviation

Portfolio

return

Risk

free rate

Sharpe

Ratio

BHP Billiton

Limited

(BHP.AX) 5.45% 2.18% 2.00% 0.0330

Harvey Norman

Holdings

Limited

(HVN.AX) 6.25% 0.05% 2.00% (0.3118)

National

Australia Bank

Limited

(NAB.AX) 4.21% -0.41% 2.00% (0.5721)

Westpac

Banking

Corporation

(WBC.AX) 3.92% -0.43% 2.00% (0.6196)

7

Required rate of return of all the 4 stocks are as follows:

Calculation of CAPM

ANZ TLS RIO WOW

A. Risk free rate 2.00% 2.00% 2.00% 2.00%

B. Market rate of

return

6% 6% 6% 6%

C. Beta 0.468263 0.058275 0.443094 0.408966

D. CAPM 3.87% 2.23% 3.77% 3.64%

E. Average Returns 0.29% -0.40% 0.92% 0.18%

The above calculations define that all the 4 stocks are overvalued in the market. Their

average return is quite below than there expected return from the market. In case of ANZ,

RRR is 3.87% whereas the average return of the company is 0.29%. Same goes with other

stocks of portfolio. It defines that this is the right time for the investors to sell the stock in the

market and get higher return from the market.

Task 3:

Sharpe measure and Treynor Measure of single asset:

Risk adjusted performance of all the assets are as follows:

Sharpe Ratio for Assets

Stocks portfolio

Standard

deviation

Portfolio

return

Risk

free rate

Sharpe

Ratio

BHP Billiton

Limited

(BHP.AX) 5.45% 2.18% 2.00% 0.0330

Harvey Norman

Holdings

Limited

(HVN.AX) 6.25% 0.05% 2.00% (0.3118)

National

Australia Bank

Limited

(NAB.AX) 4.21% -0.41% 2.00% (0.5721)

Westpac

Banking

Corporation

(WBC.AX) 3.92% -0.43% 2.00% (0.6196)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk Management Model

8

Treynor Ratio for Assets

Stocks portfolio Beta

Portfolio

return

Risk

free rate

Treynor

Ratio

BHP Billiton

Limited

(BHP.AX) 0.41 2.18% 2.00% 0.44%

Harvey Norman

Holdings

Limited

(HVN.AX) 0.20 0.05% 2.00% -9.64%

National

Australia Bank

Limited

(NAB.AX) 0.31 -0.41% 2.00% -7.79%

Westpac

Banking

Corporation

(WBC.AX) 0.44 -0.43% 2.00% -5.47%

Sharpe measure and Treynor Measure of portfolio asset:

Risk adjusted performance of portfolio is as follows:

Sharpe Ratio for Portfolio

Stocks

portfolio

Wei

ght

Expe

cted

retur

n

Portfol

io

Return

Standar

d

Deviatio

n

Risk

Free

rate

Sharpe

Ratio

BHP

Billiton

Limited

(BHP.AX)

33.3

3%

2.18

% 0.61% 4.96% 2.00% 4.88

Harvey

Norman

Holdings

Limited

(HVN.AX

)

33.3

3%

0.05

%

National

Australia

Bank

Limited

(NAB.AX)

33.3

3%

-

0.41

%

8

Treynor Ratio for Assets

Stocks portfolio Beta

Portfolio

return

Risk

free rate

Treynor

Ratio

BHP Billiton

Limited

(BHP.AX) 0.41 2.18% 2.00% 0.44%

Harvey Norman

Holdings

Limited

(HVN.AX) 0.20 0.05% 2.00% -9.64%

National

Australia Bank

Limited

(NAB.AX) 0.31 -0.41% 2.00% -7.79%

Westpac

Banking

Corporation

(WBC.AX) 0.44 -0.43% 2.00% -5.47%

Sharpe measure and Treynor Measure of portfolio asset:

Risk adjusted performance of portfolio is as follows:

Sharpe Ratio for Portfolio

Stocks

portfolio

Wei

ght

Expe

cted

retur

n

Portfol

io

Return

Standar

d

Deviatio

n

Risk

Free

rate

Sharpe

Ratio

BHP

Billiton

Limited

(BHP.AX)

33.3

3%

2.18

% 0.61% 4.96% 2.00% 4.88

Harvey

Norman

Holdings

Limited

(HVN.AX

)

33.3

3%

0.05

%

National

Australia

Bank

Limited

(NAB.AX)

33.3

3%

-

0.41

%

Risk Management Model

9

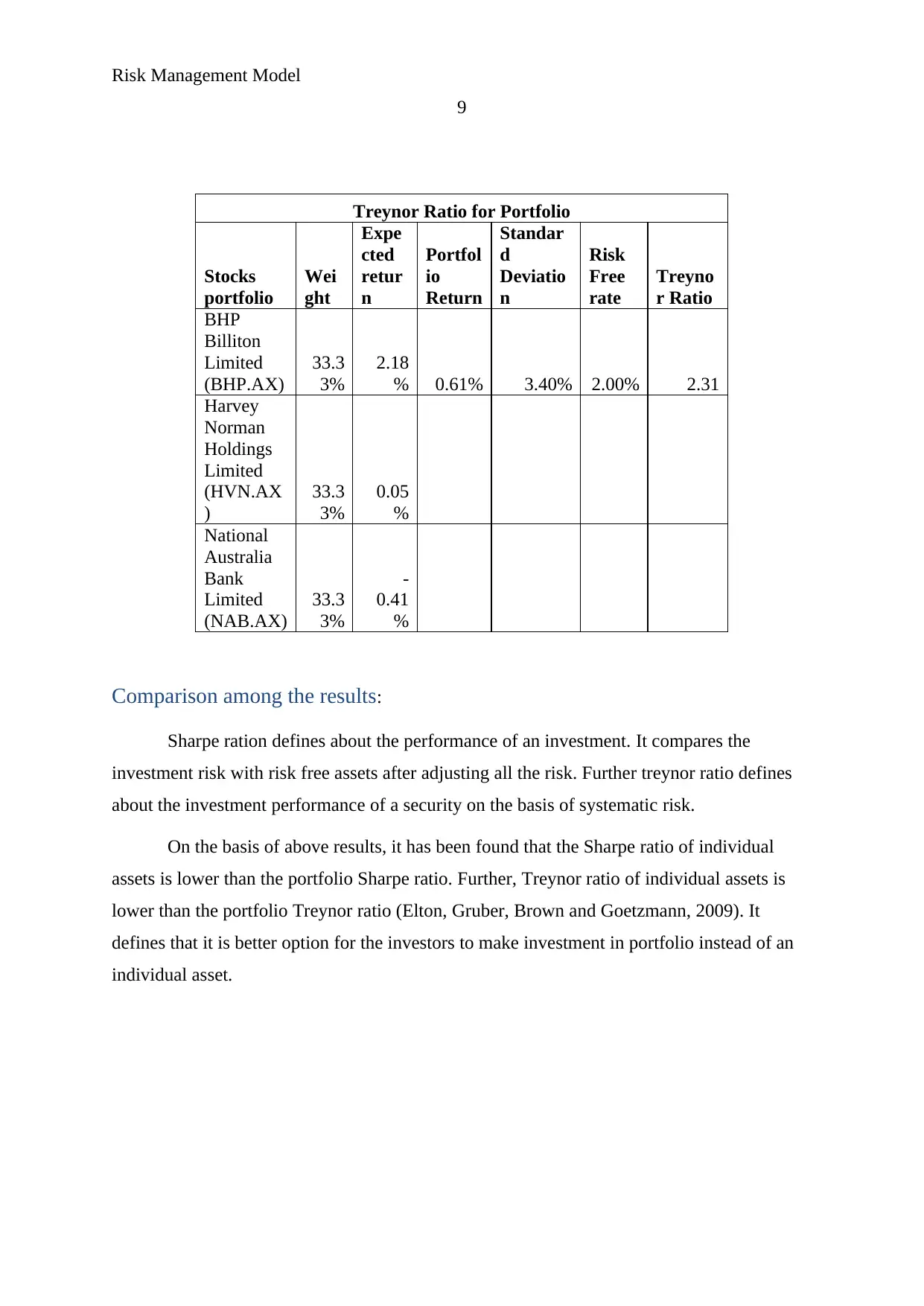

Treynor Ratio for Portfolio

Stocks

portfolio

Wei

ght

Expe

cted

retur

n

Portfol

io

Return

Standar

d

Deviatio

n

Risk

Free

rate

Treyno

r Ratio

BHP

Billiton

Limited

(BHP.AX)

33.3

3%

2.18

% 0.61% 3.40% 2.00% 2.31

Harvey

Norman

Holdings

Limited

(HVN.AX

)

33.3

3%

0.05

%

National

Australia

Bank

Limited

(NAB.AX)

33.3

3%

-

0.41

%

Comparison among the results:

Sharpe ration defines about the performance of an investment. It compares the

investment risk with risk free assets after adjusting all the risk. Further treynor ratio defines

about the investment performance of a security on the basis of systematic risk.

On the basis of above results, it has been found that the Sharpe ratio of individual

assets is lower than the portfolio Sharpe ratio. Further, Treynor ratio of individual assets is

lower than the portfolio Treynor ratio (Elton, Gruber, Brown and Goetzmann, 2009). It

defines that it is better option for the investors to make investment in portfolio instead of an

individual asset.

9

Treynor Ratio for Portfolio

Stocks

portfolio

Wei

ght

Expe

cted

retur

n

Portfol

io

Return

Standar

d

Deviatio

n

Risk

Free

rate

Treyno

r Ratio

BHP

Billiton

Limited

(BHP.AX)

33.3

3%

2.18

% 0.61% 3.40% 2.00% 2.31

Harvey

Norman

Holdings

Limited

(HVN.AX

)

33.3

3%

0.05

%

National

Australia

Bank

Limited

(NAB.AX)

33.3

3%

-

0.41

%

Comparison among the results:

Sharpe ration defines about the performance of an investment. It compares the

investment risk with risk free assets after adjusting all the risk. Further treynor ratio defines

about the investment performance of a security on the basis of systematic risk.

On the basis of above results, it has been found that the Sharpe ratio of individual

assets is lower than the portfolio Sharpe ratio. Further, Treynor ratio of individual assets is

lower than the portfolio Treynor ratio (Elton, Gruber, Brown and Goetzmann, 2009). It

defines that it is better option for the investors to make investment in portfolio instead of an

individual asset.

Risk Management Model

10

References:

Elton, E.J., Gruber, M.J., Brown, S.J., and Goetzmann, W.N. 2009. Modern Portfolio Theory

and Investment Analysis. John Wiley and Sons, United Kingdom.

Fulin, S. 2011. Preface by SHANG Fulin. Corporate Governance of Listed Companies in

China. OECD, 5, p.003.

Gapenski, L.C., 2008. Healthcare finance: an introduction to accounting and financial

management. Health Administration Press.

Higgins, R. C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Moles, P. Parrino, R and Kidwekk, D,.2011. Corporate finance, European edition, John

Wiley andsons, United Kingdom.

10

References:

Elton, E.J., Gruber, M.J., Brown, S.J., and Goetzmann, W.N. 2009. Modern Portfolio Theory

and Investment Analysis. John Wiley and Sons, United Kingdom.

Fulin, S. 2011. Preface by SHANG Fulin. Corporate Governance of Listed Companies in

China. OECD, 5, p.003.

Gapenski, L.C., 2008. Healthcare finance: an introduction to accounting and financial

management. Health Administration Press.

Higgins, R. C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Moles, P. Parrino, R and Kidwekk, D,.2011. Corporate finance, European edition, John

Wiley andsons, United Kingdom.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Risk Management Model

11

Appendix:

ANZ:

TLS:

RIO:

11

Appendix:

ANZ:

TLS:

RIO:

Risk Management Model

12

WOW:

12

WOW:

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.