Strategic Analysis of Financial Performance: Project Report

VerifiedAdded on 2020/05/16

|42

|13724

|303

Project

AI Summary

This project report presents a critical analysis of corporate financial and operating positions, employing both traditional and contemporary financial analysis methods. It begins with an introduction to financial statements and their importance in business decision-making, covering the statement of financial performance, position, cash flows, and equity changes. The report then delves into traditional methods, including horizontal and vertical analysis, and ratio analysis, evaluating their strengths and limitations. Horizontal analysis assesses financial data over time, while vertical analysis uses a comparative approach. The report also explores contemporary methods such as the Capital Asset Pricing Model (CAPM), the Dividend Growth Model (DGM), and the Efficient Market Hypothesis (EMH). The study examines the financial performance of Tate & Lyle and Wolseley using these methods, offering insights into their profitability, liquidity, solvency, and efficiency. The report concludes by emphasizing the importance of selecting financial evaluation techniques that align with an organization's specific needs and objectives, providing a comprehensive overview of financial analysis methodologies.

Running Head: Strategic Analysis

1

Project Report: Strategic Analysis

1

Project Report: Strategic Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Analysis

2

Contents

Introduction.................................................................................................................... 3

Critical review of financial analysis’s traditional methods..............................................4

Horizontal analysis......................................................................................................4

Vertical analysis.......................................................................................................... 6

Traditional ratio analysis.............................................................................................8

Contemporary methods of financial analysis................................................................10

Capital asset pricing model.......................................................................................11

Dividend growth model.............................................................................................12

Effective market hypothesis......................................................................................13

Conclusion.....................................................................................................................13

References.................................................................................................................... 15

Appendix....................................................................................................................... 17

2

Contents

Introduction.................................................................................................................... 3

Critical review of financial analysis’s traditional methods..............................................4

Horizontal analysis......................................................................................................4

Vertical analysis.......................................................................................................... 6

Traditional ratio analysis.............................................................................................8

Contemporary methods of financial analysis................................................................10

Capital asset pricing model.......................................................................................11

Dividend growth model.............................................................................................12

Effective market hypothesis......................................................................................13

Conclusion.....................................................................................................................13

References.................................................................................................................... 15

Appendix....................................................................................................................... 17

Strategic Analysis

3

Introduction:

This report has been described about the critically analyse of the financial and

operating position of corporations which is shepherding by the different traditional and

contemporary methods. Financial statement is apprehended four vital business actions:

Forecasting, Capitalising, funding and operation. To make Effective economic decisions,

financial statement analysis is the effective process by reviewing and analysing financial

statements. Financial statement consists of the statement of financial performance,

statement of financial position, statement of cash flows, and statement of changes in

equity. Financial statement analysis has described a technique or way which involved

identifying the risks, evaluating the performance, financial condition, and forthcoming

predictions of the corporation. Actually, this analysis has been used by the multiplicity of

interested party, as per investors of all categories, the supervision authority, and mainly the

management of the company. Usually, to analyse the financial statements, most popular

two types of method has been used. One is called Traditional Methods and another is

called Contemporary methods. The Most common process for financial statements

analysis is been the practise the numerous of ratios. Mainly, the Ratios are using to

compute the comparative dimensions of the individual amount in kin to a different.

Principally, Ratios are easily compared to the same ratio which is calculated for the

prior period, otherwise established of the average for the industry. It helps to measure

that company is carrying out their activities according the expectations or not. The

ratios change of the figure can take the attention of the commentator. Other method is

to calculation is horizontal and vertical analysis1. Horizontal analysis is judge by the

financial information which is presented sequence of reporting periods. Vertical

analysis has been done of the financial statement analysis followed by the comparative.

It describes like every item of the financial statement is listed as a percentage of

another item. In the contemporary methods, CAPM is very popular for analysis the risk

1 Charles H Gibson. Financial reporting and analysis. South-Western Cengage Learning,

2011.

3

Introduction:

This report has been described about the critically analyse of the financial and

operating position of corporations which is shepherding by the different traditional and

contemporary methods. Financial statement is apprehended four vital business actions:

Forecasting, Capitalising, funding and operation. To make Effective economic decisions,

financial statement analysis is the effective process by reviewing and analysing financial

statements. Financial statement consists of the statement of financial performance,

statement of financial position, statement of cash flows, and statement of changes in

equity. Financial statement analysis has described a technique or way which involved

identifying the risks, evaluating the performance, financial condition, and forthcoming

predictions of the corporation. Actually, this analysis has been used by the multiplicity of

interested party, as per investors of all categories, the supervision authority, and mainly the

management of the company. Usually, to analyse the financial statements, most popular

two types of method has been used. One is called Traditional Methods and another is

called Contemporary methods. The Most common process for financial statements

analysis is been the practise the numerous of ratios. Mainly, the Ratios are using to

compute the comparative dimensions of the individual amount in kin to a different.

Principally, Ratios are easily compared to the same ratio which is calculated for the

prior period, otherwise established of the average for the industry. It helps to measure

that company is carrying out their activities according the expectations or not. The

ratios change of the figure can take the attention of the commentator. Other method is

to calculation is horizontal and vertical analysis1. Horizontal analysis is judge by the

financial information which is presented sequence of reporting periods. Vertical

analysis has been done of the financial statement analysis followed by the comparative.

It describes like every item of the financial statement is listed as a percentage of

another item. In the contemporary methods, CAPM is very popular for analysis the risk

1 Charles H Gibson. Financial reporting and analysis. South-Western Cengage Learning,

2011.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Analysis

4

effectively. DGM shows that how to grow the company dividends2. It grows the

perpetuity basis or different rates. And the last but not the list is EMH which idea is

partly established by the Eugene Fama in the 1960s.

Critical review of financial analysis’s traditional methods:

Financial analysis could be done through traditional as well as contemporary

methods. Following study explains about the traditional method of the company and its

critical evaluation:

Horizontal analysis:

Horizontal analysis or trend analysis is a financial tool which is used to evaluate a

financial statement data in excess of certain period of time. The purpose of the calculation is

to evaluate the increase or the decrease and mainly used in intra company comparison. The

changes of the amount are easily identified and it is the most advantage in this financial

tools. . But, sometimes difficulties create to do the calculations3. As an example, there is no

value an asset item has in the previous year but value is created in the next year, so the

problem is percentage don’t calculated. On the other hand, the negative figures give the

impression in the previous years and a positive figure exists the following year, but the

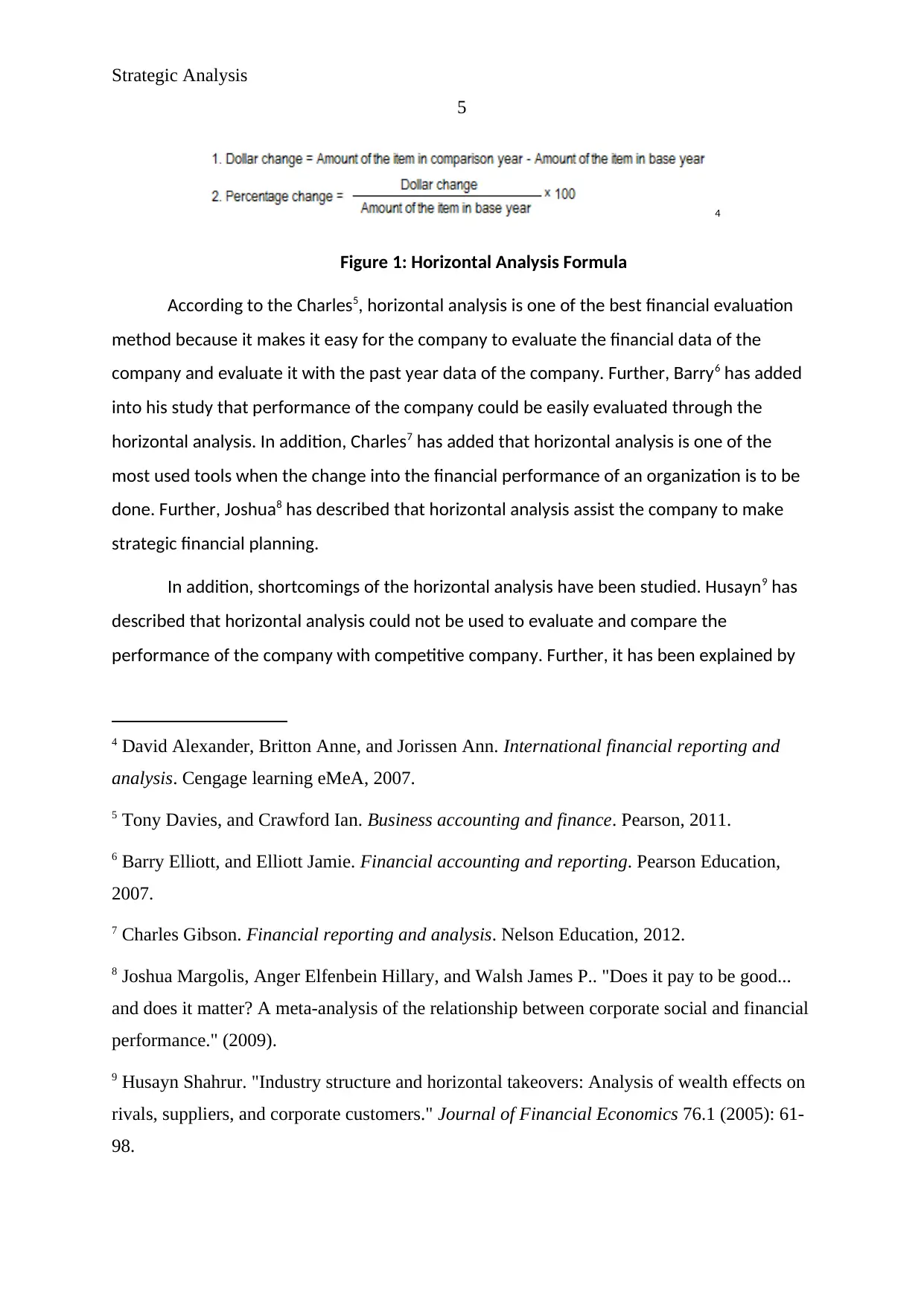

percentage change cannot figure. The following is the formula of horizontal analysis:

2 Tony Davies, and Crawford Ian. Business accounting and finance. Pearson, 2011.

3 Charles H Gibson. Financial reporting and analysis. South-Western Cengage Learning,

2011.

4

effectively. DGM shows that how to grow the company dividends2. It grows the

perpetuity basis or different rates. And the last but not the list is EMH which idea is

partly established by the Eugene Fama in the 1960s.

Critical review of financial analysis’s traditional methods:

Financial analysis could be done through traditional as well as contemporary

methods. Following study explains about the traditional method of the company and its

critical evaluation:

Horizontal analysis:

Horizontal analysis or trend analysis is a financial tool which is used to evaluate a

financial statement data in excess of certain period of time. The purpose of the calculation is

to evaluate the increase or the decrease and mainly used in intra company comparison. The

changes of the amount are easily identified and it is the most advantage in this financial

tools. . But, sometimes difficulties create to do the calculations3. As an example, there is no

value an asset item has in the previous year but value is created in the next year, so the

problem is percentage don’t calculated. On the other hand, the negative figures give the

impression in the previous years and a positive figure exists the following year, but the

percentage change cannot figure. The following is the formula of horizontal analysis:

2 Tony Davies, and Crawford Ian. Business accounting and finance. Pearson, 2011.

3 Charles H Gibson. Financial reporting and analysis. South-Western Cengage Learning,

2011.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Analysis

5

4

Figure 1: Horizontal Analysis Formula

According to the Charles5, horizontal analysis is one of the best financial evaluation

method because it makes it easy for the company to evaluate the financial data of the

company and evaluate it with the past year data of the company. Further, Barry6 has added

into his study that performance of the company could be easily evaluated through the

horizontal analysis. In addition, Charles7 has added that horizontal analysis is one of the

most used tools when the change into the financial performance of an organization is to be

done. Further, Joshua8 has described that horizontal analysis assist the company to make

strategic financial planning.

In addition, shortcomings of the horizontal analysis have been studied. Husayn9 has

described that horizontal analysis could not be used to evaluate and compare the

performance of the company with competitive company. Further, it has been explained by

4 David Alexander, Britton Anne, and Jorissen Ann. International financial reporting and

analysis. Cengage learning eMeA, 2007.

5 Tony Davies, and Crawford Ian. Business accounting and finance. Pearson, 2011.

6 Barry Elliott, and Elliott Jamie. Financial accounting and reporting. Pearson Education,

2007.

7 Charles Gibson. Financial reporting and analysis. Nelson Education, 2012.

8 Joshua Margolis, Anger Elfenbein Hillary, and Walsh James P.. "Does it pay to be good...

and does it matter? A meta-analysis of the relationship between corporate social and financial

performance." (2009).

9 Husayn Shahrur. "Industry structure and horizontal takeovers: Analysis of wealth effects on

rivals, suppliers, and corporate customers." Journal of Financial Economics 76.1 (2005): 61-

98.

5

4

Figure 1: Horizontal Analysis Formula

According to the Charles5, horizontal analysis is one of the best financial evaluation

method because it makes it easy for the company to evaluate the financial data of the

company and evaluate it with the past year data of the company. Further, Barry6 has added

into his study that performance of the company could be easily evaluated through the

horizontal analysis. In addition, Charles7 has added that horizontal analysis is one of the

most used tools when the change into the financial performance of an organization is to be

done. Further, Joshua8 has described that horizontal analysis assist the company to make

strategic financial planning.

In addition, shortcomings of the horizontal analysis have been studied. Husayn9 has

described that horizontal analysis could not be used to evaluate and compare the

performance of the company with competitive company. Further, it has been explained by

4 David Alexander, Britton Anne, and Jorissen Ann. International financial reporting and

analysis. Cengage learning eMeA, 2007.

5 Tony Davies, and Crawford Ian. Business accounting and finance. Pearson, 2011.

6 Barry Elliott, and Elliott Jamie. Financial accounting and reporting. Pearson Education,

2007.

7 Charles Gibson. Financial reporting and analysis. Nelson Education, 2012.

8 Joshua Margolis, Anger Elfenbein Hillary, and Walsh James P.. "Does it pay to be good...

and does it matter? A meta-analysis of the relationship between corporate social and financial

performance." (2009).

9 Husayn Shahrur. "Industry structure and horizontal takeovers: Analysis of wealth effects on

rivals, suppliers, and corporate customers." Journal of Financial Economics 76.1 (2005): 61-

98.

Strategic Analysis

6

David10 that it is tough to choose the base year for the horizontal analysis study. More, it has

been said that the various assumptions are required to be made for this study.

The study of horizontal analysis has been done on Tate and Lyle & Wolseley and it

has been found that the financial performance of Tate and Lyle plc has been worst in 2016

in comparison of last 5 years. Currently, the gross profit of the company has been lowered

by 5.25% and the net profit of the company has been lowered by 47.25%. Company is

required to focus on this point.

On the other hand, the study of horizontal analysis has been done on Wolseley and it

has been found that the financial performance of Wolseley plc has been better in 2016 in

comparison of last 5 years. Currently, the gross profit of the company has been enhanced by

10.33% and the net profit of the company has been enhanced by 1056.14%. Company is

required to manage the same level.

Vertical analysis:

Vertical analysis is a financial tool which is used to evaluate a financial statement

data in excess of certain period of time. The purpose of the calculation is to evaluate the

competition level of the company in the industry and the changes into the financial

performance of the company from last year11. The changes of the amount are easily

identified and it is the most advantage in this financial tools. . But, sometimes difficulties

create to do the calculations. As an example, there is an expense which has not been

occurred in a company but has taken place into other company, so the problem occurs while

evaluating the data. The following is the formula of vertical analysis:

10 David Alexander, Britton Anne, and Jorissen Ann. International financial reporting and

analysis. Cengage learning eMeA, 2007.

11 Charles H Gibson. Financial reporting and analysis. South-Western Cengage Learning,

2011.

6

David10 that it is tough to choose the base year for the horizontal analysis study. More, it has

been said that the various assumptions are required to be made for this study.

The study of horizontal analysis has been done on Tate and Lyle & Wolseley and it

has been found that the financial performance of Tate and Lyle plc has been worst in 2016

in comparison of last 5 years. Currently, the gross profit of the company has been lowered

by 5.25% and the net profit of the company has been lowered by 47.25%. Company is

required to focus on this point.

On the other hand, the study of horizontal analysis has been done on Wolseley and it

has been found that the financial performance of Wolseley plc has been better in 2016 in

comparison of last 5 years. Currently, the gross profit of the company has been enhanced by

10.33% and the net profit of the company has been enhanced by 1056.14%. Company is

required to manage the same level.

Vertical analysis:

Vertical analysis is a financial tool which is used to evaluate a financial statement

data in excess of certain period of time. The purpose of the calculation is to evaluate the

competition level of the company in the industry and the changes into the financial

performance of the company from last year11. The changes of the amount are easily

identified and it is the most advantage in this financial tools. . But, sometimes difficulties

create to do the calculations. As an example, there is an expense which has not been

occurred in a company but has taken place into other company, so the problem occurs while

evaluating the data. The following is the formula of vertical analysis:

10 David Alexander, Britton Anne, and Jorissen Ann. International financial reporting and

analysis. Cengage learning eMeA, 2007.

11 Charles H Gibson. Financial reporting and analysis. South-Western Cengage Learning,

2011.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Analysis

7

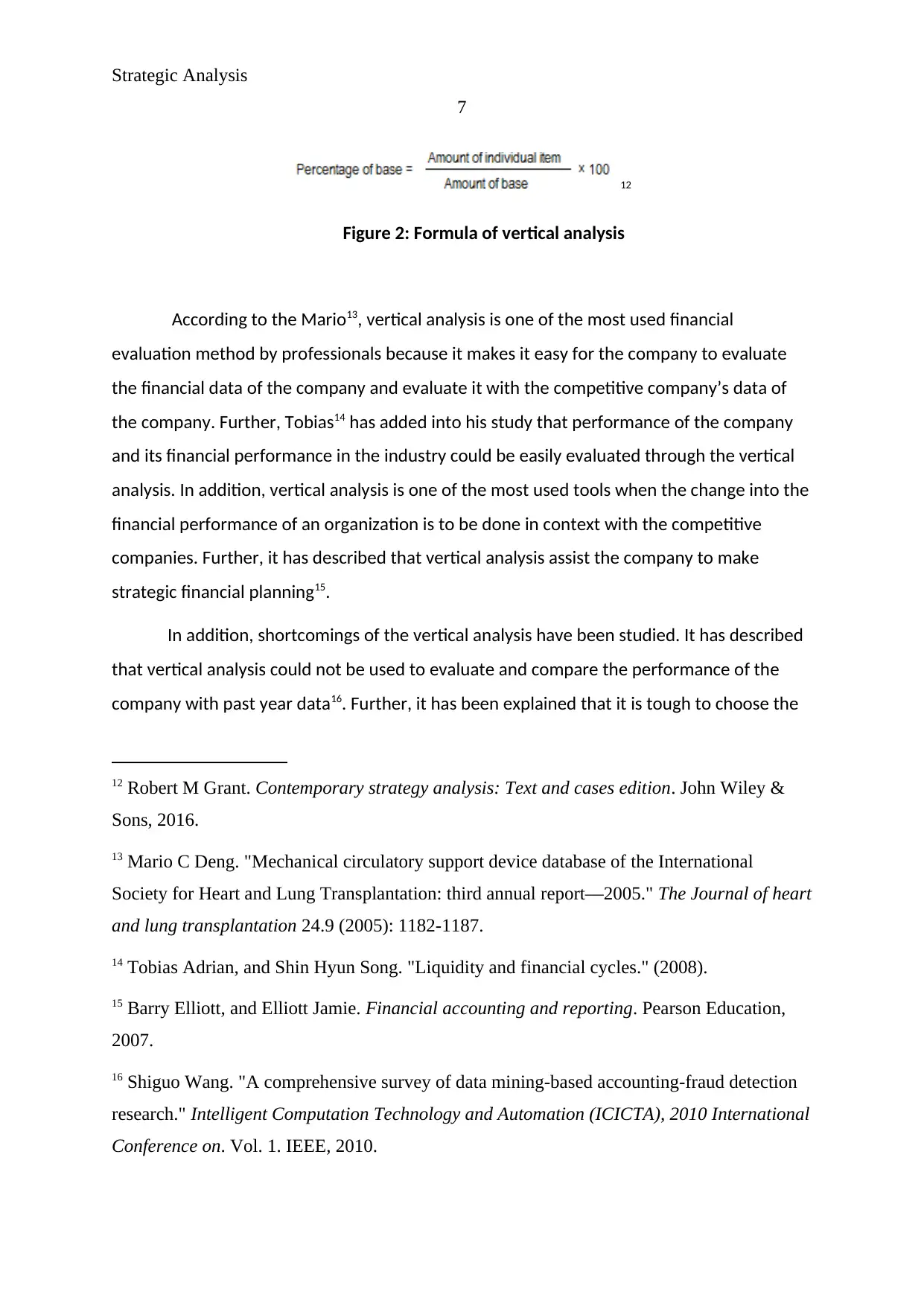

12

Figure 2: Formula of vertical analysis

According to the Mario13, vertical analysis is one of the most used financial

evaluation method by professionals because it makes it easy for the company to evaluate

the financial data of the company and evaluate it with the competitive company’s data of

the company. Further, Tobias14 has added into his study that performance of the company

and its financial performance in the industry could be easily evaluated through the vertical

analysis. In addition, vertical analysis is one of the most used tools when the change into the

financial performance of an organization is to be done in context with the competitive

companies. Further, it has described that vertical analysis assist the company to make

strategic financial planning15.

In addition, shortcomings of the vertical analysis have been studied. It has described

that vertical analysis could not be used to evaluate and compare the performance of the

company with past year data16. Further, it has been explained that it is tough to choose the

12 Robert M Grant. Contemporary strategy analysis: Text and cases edition. John Wiley &

Sons, 2016.

13 Mario C Deng. "Mechanical circulatory support device database of the International

Society for Heart and Lung Transplantation: third annual report—2005." The Journal of heart

and lung transplantation 24.9 (2005): 1182-1187.

14 Tobias Adrian, and Shin Hyun Song. "Liquidity and financial cycles." (2008).

15 Barry Elliott, and Elliott Jamie. Financial accounting and reporting. Pearson Education,

2007.

16 Shiguo Wang. "A comprehensive survey of data mining-based accounting-fraud detection

research." Intelligent Computation Technology and Automation (ICICTA), 2010 International

Conference on. Vol. 1. IEEE, 2010.

7

12

Figure 2: Formula of vertical analysis

According to the Mario13, vertical analysis is one of the most used financial

evaluation method by professionals because it makes it easy for the company to evaluate

the financial data of the company and evaluate it with the competitive company’s data of

the company. Further, Tobias14 has added into his study that performance of the company

and its financial performance in the industry could be easily evaluated through the vertical

analysis. In addition, vertical analysis is one of the most used tools when the change into the

financial performance of an organization is to be done in context with the competitive

companies. Further, it has described that vertical analysis assist the company to make

strategic financial planning15.

In addition, shortcomings of the vertical analysis have been studied. It has described

that vertical analysis could not be used to evaluate and compare the performance of the

company with past year data16. Further, it has been explained that it is tough to choose the

12 Robert M Grant. Contemporary strategy analysis: Text and cases edition. John Wiley &

Sons, 2016.

13 Mario C Deng. "Mechanical circulatory support device database of the International

Society for Heart and Lung Transplantation: third annual report—2005." The Journal of heart

and lung transplantation 24.9 (2005): 1182-1187.

14 Tobias Adrian, and Shin Hyun Song. "Liquidity and financial cycles." (2008).

15 Barry Elliott, and Elliott Jamie. Financial accounting and reporting. Pearson Education,

2007.

16 Shiguo Wang. "A comprehensive survey of data mining-based accounting-fraud detection

research." Intelligent Computation Technology and Automation (ICICTA), 2010 International

Conference on. Vol. 1. IEEE, 2010.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Analysis

8

competition company as the operations are quite different of each company. More, it has

been said that the various assumptions are required to be made for this study17.

The study of vertical analysis has been done on Tate and Lyle & Wolseley and it has

been found that the financial performance, income and expenses have not been managed

by the company in a better way. The gross profit and net profit of the company has been

lesser in comparison with last year’s data. Further, the balance sheet of the company

explains about the negative changes into the current assets, total debts etc of the company.

On the other hand, the study of vertical analysis has been done on Wolseley and it

has been found that the financial performance, income and expenses have been managed

by the company in a better way. The gross profit and net profit of the company has been

better in last year’s data. Further, the balance sheet of the company explains about the

positive changes into the total assets, liabilities and equity of the company.

Traditional ratio analysis:

Traditional ratio analysis is a financial tool which is used to evaluate a financial

statement data in terms of other financial figures of the company. The purpose of the

calculation is to evaluate the competition, liquidity, stability, profitability etc level of the

company in the industry and the changes into the financial performance of the company

from last year. The changes of the amount could be easily identified through this tool. But,

sometimes difficulties create to do the calculations. The following is the formula of few parts

of traditional ratio analysis:

Profitability

Net margin

Net

profit/revenues

Return on equity Net profit/Equity18

17 Mario C Deng. "Mechanical circulatory support device database of the International

Society for Heart and Lung Transplantation: third annual report—2005." The Journal of heart

and lung transplantation 24.9 (2005): 1182-1187.

18 Tobias Adrian, and Shin Hyun Song. "Liquidity and financial cycles." (2008).

8

competition company as the operations are quite different of each company. More, it has

been said that the various assumptions are required to be made for this study17.

The study of vertical analysis has been done on Tate and Lyle & Wolseley and it has

been found that the financial performance, income and expenses have not been managed

by the company in a better way. The gross profit and net profit of the company has been

lesser in comparison with last year’s data. Further, the balance sheet of the company

explains about the negative changes into the current assets, total debts etc of the company.

On the other hand, the study of vertical analysis has been done on Wolseley and it

has been found that the financial performance, income and expenses have been managed

by the company in a better way. The gross profit and net profit of the company has been

better in last year’s data. Further, the balance sheet of the company explains about the

positive changes into the total assets, liabilities and equity of the company.

Traditional ratio analysis:

Traditional ratio analysis is a financial tool which is used to evaluate a financial

statement data in terms of other financial figures of the company. The purpose of the

calculation is to evaluate the competition, liquidity, stability, profitability etc level of the

company in the industry and the changes into the financial performance of the company

from last year. The changes of the amount could be easily identified through this tool. But,

sometimes difficulties create to do the calculations. The following is the formula of few parts

of traditional ratio analysis:

Profitability

Net margin

Net

profit/revenues

Return on equity Net profit/Equity18

17 Mario C Deng. "Mechanical circulatory support device database of the International

Society for Heart and Lung Transplantation: third annual report—2005." The Journal of heart

and lung transplantation 24.9 (2005): 1182-1187.

18 Tobias Adrian, and Shin Hyun Song. "Liquidity and financial cycles." (2008).

Strategic Analysis

9

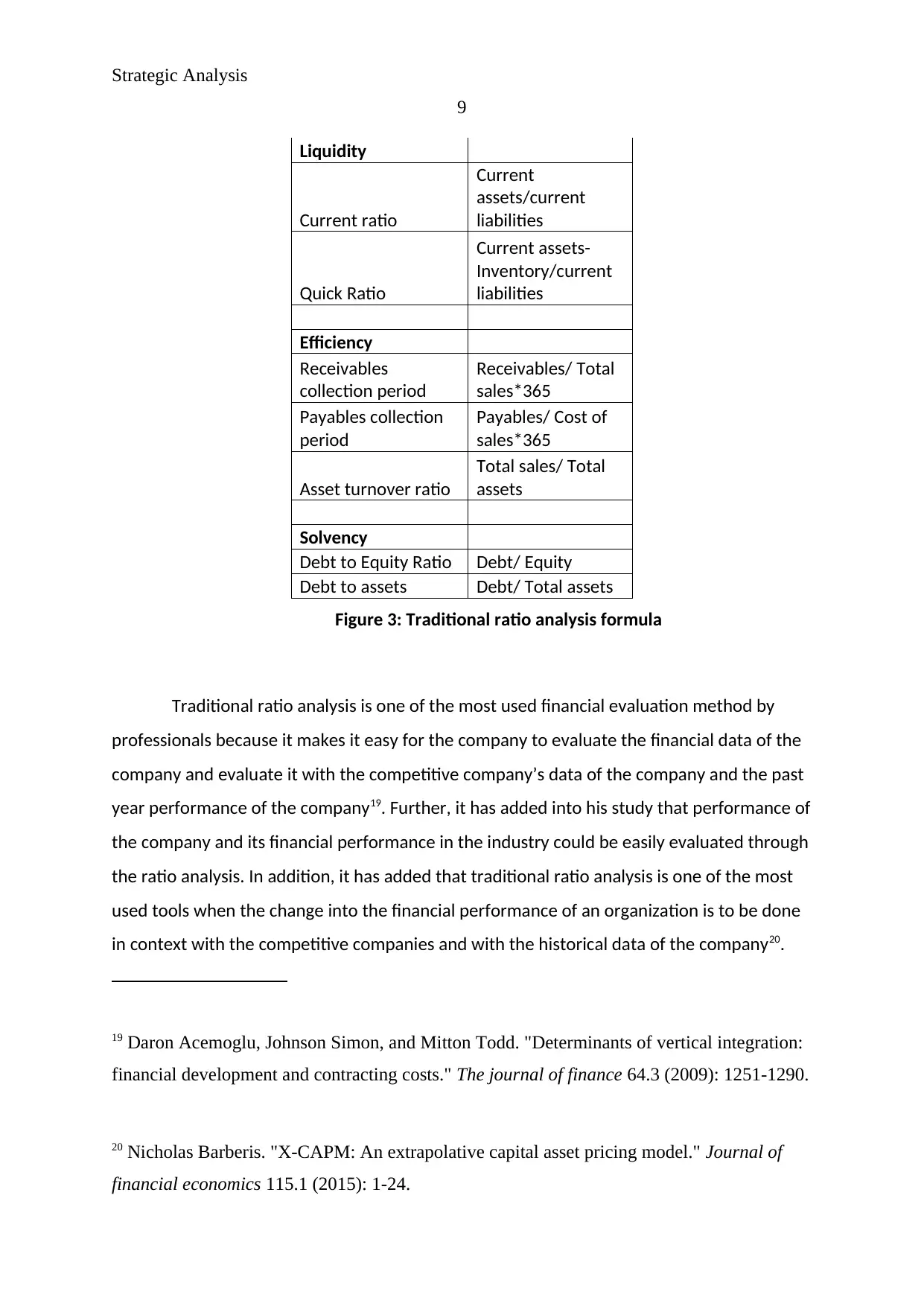

Liquidity

Current ratio

Current

assets/current

liabilities

Quick Ratio

Current assets-

Inventory/current

liabilities

Efficiency

Receivables

collection period

Receivables/ Total

sales*365

Payables collection

period

Payables/ Cost of

sales*365

Asset turnover ratio

Total sales/ Total

assets

Solvency

Debt to Equity Ratio Debt/ Equity

Debt to assets Debt/ Total assets

Figure 3: Traditional ratio analysis formula

Traditional ratio analysis is one of the most used financial evaluation method by

professionals because it makes it easy for the company to evaluate the financial data of the

company and evaluate it with the competitive company’s data of the company and the past

year performance of the company19. Further, it has added into his study that performance of

the company and its financial performance in the industry could be easily evaluated through

the ratio analysis. In addition, it has added that traditional ratio analysis is one of the most

used tools when the change into the financial performance of an organization is to be done

in context with the competitive companies and with the historical data of the company20.

19 Daron Acemoglu, Johnson Simon, and Mitton Todd. "Determinants of vertical integration:

financial development and contracting costs." The journal of finance 64.3 (2009): 1251-1290.

20 Nicholas Barberis. "X-CAPM: An extrapolative capital asset pricing model." Journal of

financial economics 115.1 (2015): 1-24.

9

Liquidity

Current ratio

Current

assets/current

liabilities

Quick Ratio

Current assets-

Inventory/current

liabilities

Efficiency

Receivables

collection period

Receivables/ Total

sales*365

Payables collection

period

Payables/ Cost of

sales*365

Asset turnover ratio

Total sales/ Total

assets

Solvency

Debt to Equity Ratio Debt/ Equity

Debt to assets Debt/ Total assets

Figure 3: Traditional ratio analysis formula

Traditional ratio analysis is one of the most used financial evaluation method by

professionals because it makes it easy for the company to evaluate the financial data of the

company and evaluate it with the competitive company’s data of the company and the past

year performance of the company19. Further, it has added into his study that performance of

the company and its financial performance in the industry could be easily evaluated through

the ratio analysis. In addition, it has added that traditional ratio analysis is one of the most

used tools when the change into the financial performance of an organization is to be done

in context with the competitive companies and with the historical data of the company20.

19 Daron Acemoglu, Johnson Simon, and Mitton Todd. "Determinants of vertical integration:

financial development and contracting costs." The journal of finance 64.3 (2009): 1251-1290.

20 Nicholas Barberis. "X-CAPM: An extrapolative capital asset pricing model." Journal of

financial economics 115.1 (2015): 1-24.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Strategic Analysis

10

Further, it has described that traditional ratio analysis assist the company to make strategic

financial planning.

In addition, shortcomings of the ratio analysis have been studied. It has described

that ratio analysis study is based on various assumptions. Further, it has been explained that

it is tough to compare the data with the competitive companies21. Further, the different

level of ratios is set by the company according to its nature and policies22.

The study of traditional ratio analysis has been done on Tate and Lyle and it has been

found that the profitability level, liquidity level, solvency level and efficiency level have been

managed by the company in a better way. The profitability level of the company is

impressive on the other hand, liquidity position explains to reduce the level of current

assets. Further, the efficiency and solvency of the company explains about the good position

of the company.

On the other hand, the study of traditional ratio analysis has been done on Wolseley

and it has been found that the profitability level, liquidity level, solvency level and efficiency

level have been managed by the company in a better way. The profitability level of the

company is quite impressive. On the other hand, liquidity position explains to reduce the

level of current assets. Further, the efficiency and solvency of the company explains about

the few changes into the policies and capital structure of the company.

The above study of traditional method of financial evaluation technique expresses

that all the techniques have some pros as well as some cons. An organization should choose

the financial evaluation technique according to its nature, needs and objectives.

Contemporary methods of financial analysis:

21 Daron Acemoglu, Johnson Simon, and Mitton Todd. "Determinants of vertical integration:

financial development and contracting costs." The journal of finance 64.3 (2009): 1251-1290.

22 Eugene F Fama, and French Kenneth R.. "The value premium and the CAPM." The

Journal of Finance 61.5 (2006): 2163-2185.

10

Further, it has described that traditional ratio analysis assist the company to make strategic

financial planning.

In addition, shortcomings of the ratio analysis have been studied. It has described

that ratio analysis study is based on various assumptions. Further, it has been explained that

it is tough to compare the data with the competitive companies21. Further, the different

level of ratios is set by the company according to its nature and policies22.

The study of traditional ratio analysis has been done on Tate and Lyle and it has been

found that the profitability level, liquidity level, solvency level and efficiency level have been

managed by the company in a better way. The profitability level of the company is

impressive on the other hand, liquidity position explains to reduce the level of current

assets. Further, the efficiency and solvency of the company explains about the good position

of the company.

On the other hand, the study of traditional ratio analysis has been done on Wolseley

and it has been found that the profitability level, liquidity level, solvency level and efficiency

level have been managed by the company in a better way. The profitability level of the

company is quite impressive. On the other hand, liquidity position explains to reduce the

level of current assets. Further, the efficiency and solvency of the company explains about

the few changes into the policies and capital structure of the company.

The above study of traditional method of financial evaluation technique expresses

that all the techniques have some pros as well as some cons. An organization should choose

the financial evaluation technique according to its nature, needs and objectives.

Contemporary methods of financial analysis:

21 Daron Acemoglu, Johnson Simon, and Mitton Todd. "Determinants of vertical integration:

financial development and contracting costs." The journal of finance 64.3 (2009): 1251-1290.

22 Eugene F Fama, and French Kenneth R.. "The value premium and the CAPM." The

Journal of Finance 61.5 (2006): 2163-2185.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strategic Analysis

11

Financial analysis could be done through traditional as well as contemporary

methods. Following study explains about the contemporary method of the company and its

critical evaluation:

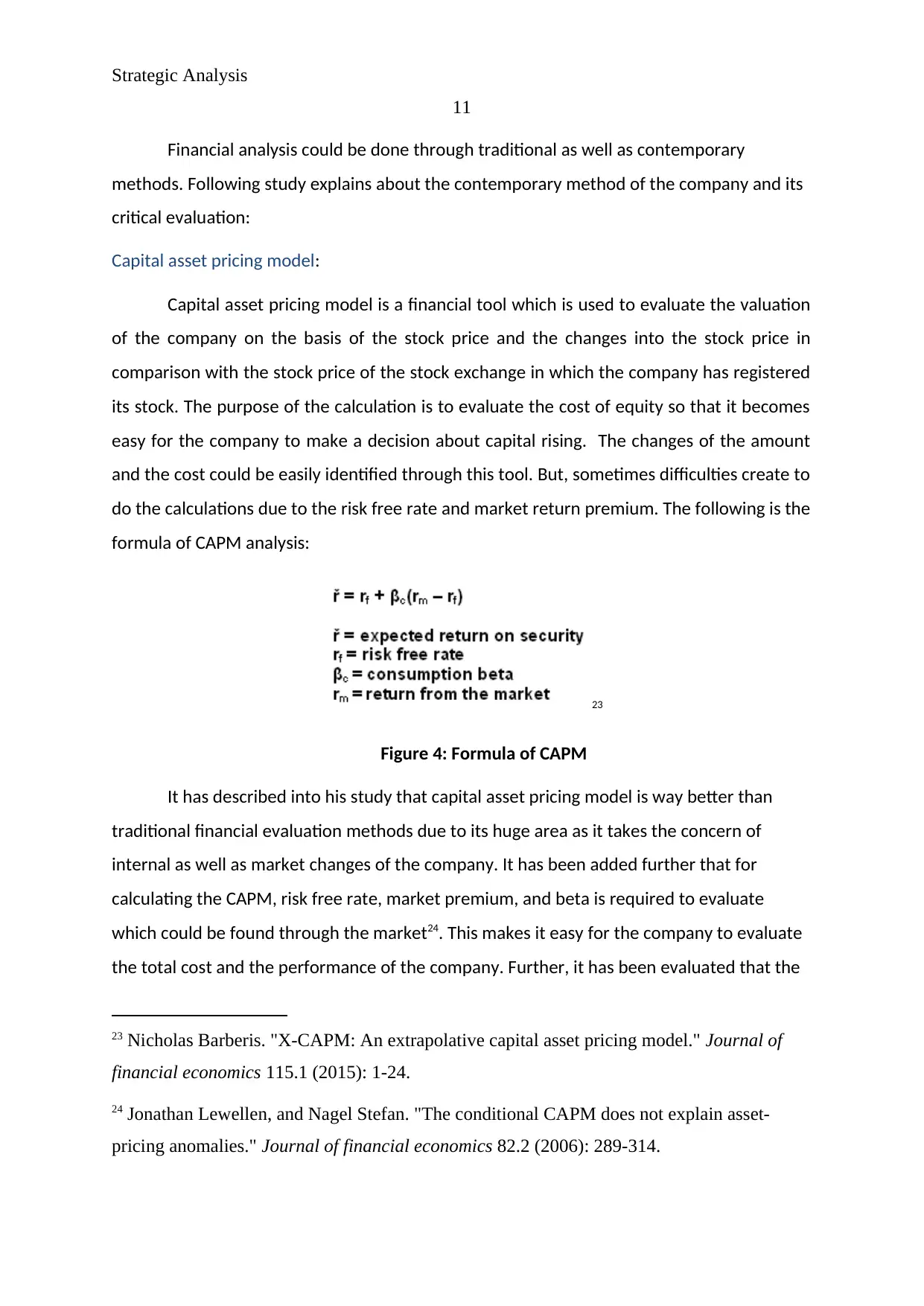

Capital asset pricing model:

Capital asset pricing model is a financial tool which is used to evaluate the valuation

of the company on the basis of the stock price and the changes into the stock price in

comparison with the stock price of the stock exchange in which the company has registered

its stock. The purpose of the calculation is to evaluate the cost of equity so that it becomes

easy for the company to make a decision about capital rising. The changes of the amount

and the cost could be easily identified through this tool. But, sometimes difficulties create to

do the calculations due to the risk free rate and market return premium. The following is the

formula of CAPM analysis:

23

Figure 4: Formula of CAPM

It has described into his study that capital asset pricing model is way better than

traditional financial evaluation methods due to its huge area as it takes the concern of

internal as well as market changes of the company. It has been added further that for

calculating the CAPM, risk free rate, market premium, and beta is required to evaluate

which could be found through the market24. This makes it easy for the company to evaluate

the total cost and the performance of the company. Further, it has been evaluated that the

23 Nicholas Barberis. "X-CAPM: An extrapolative capital asset pricing model." Journal of

financial economics 115.1 (2015): 1-24.

24 Jonathan Lewellen, and Nagel Stefan. "The conditional CAPM does not explain asset-

pricing anomalies." Journal of financial economics 82.2 (2006): 289-314.

11

Financial analysis could be done through traditional as well as contemporary

methods. Following study explains about the contemporary method of the company and its

critical evaluation:

Capital asset pricing model:

Capital asset pricing model is a financial tool which is used to evaluate the valuation

of the company on the basis of the stock price and the changes into the stock price in

comparison with the stock price of the stock exchange in which the company has registered

its stock. The purpose of the calculation is to evaluate the cost of equity so that it becomes

easy for the company to make a decision about capital rising. The changes of the amount

and the cost could be easily identified through this tool. But, sometimes difficulties create to

do the calculations due to the risk free rate and market return premium. The following is the

formula of CAPM analysis:

23

Figure 4: Formula of CAPM

It has described into his study that capital asset pricing model is way better than

traditional financial evaluation methods due to its huge area as it takes the concern of

internal as well as market changes of the company. It has been added further that for

calculating the CAPM, risk free rate, market premium, and beta is required to evaluate

which could be found through the market24. This makes it easy for the company to evaluate

the total cost and the performance of the company. Further, it has been evaluated that the

23 Nicholas Barberis. "X-CAPM: An extrapolative capital asset pricing model." Journal of

financial economics 115.1 (2015): 1-24.

24 Jonathan Lewellen, and Nagel Stefan. "The conditional CAPM does not explain asset-

pricing anomalies." Journal of financial economics 82.2 (2006): 289-314.

Strategic Analysis

12

CAPM does not based on the assumptions25. Always real values are taken to evaluate the

performance and the required rate of return of the company. Further, on the basis of

required rate of return, it becomes easy for the investors to make a decision about the

investment or divestment from the stock of the company26. Thus it could be said that this

option is way better than traditional methods of financial analysis.

Dividend growth model:

Dividend growth model is a financial tool which is used to evaluate the valuation of

the stock price of the company and the changes into the stock price (face value and market

value). This model could be conducted through the help of dividend payment, dividend

growth rate and the cost of equity. The purpose of the calculation is to evaluate the value of

the shares so that it becomes easy for the investors to make a decision about investment in

the company. The changes of the amount and the value of shares could be easily identified

through this tool. But, sometimes difficulties create to do the calculations due to the growth

%. The following is the formula of dividend growth model analysis:

Gordon Growth Model: stock price = (dividend payment in the next period) / (cost

of equity - dividend growth rate) 27

It has described into his study that dividend growth model is way better than

traditional financial evaluation methods due to its huge area as it takes the concern of

internal as well as market changes of the company28. It has been added further that for

calculating the DGM, dividend payment, growth rate, and cost of equity is required to

evaluate which could be found through the market. This makes it easy for the investors to

25 Eugene F Fama, and French Kenneth R.. "The value premium and the CAPM." The

Journal of Finance 61.5 (2006): 2163-2185.

26 Roelinka Broekhuizen. "Optimizing oral nutritional drink supplementation in patients with

chronic obstructive pulmonary disease." British journal of nutrition 93.6 (2005): 965-971.

27 E. F. M. Wouters et al. "Airway biology." Thorax 60.6 (2005): 480-487.

28 Paul Barnes. "Dividend Growth Model." Wiley Encyclopedia of Management. 2009.

12

CAPM does not based on the assumptions25. Always real values are taken to evaluate the

performance and the required rate of return of the company. Further, on the basis of

required rate of return, it becomes easy for the investors to make a decision about the

investment or divestment from the stock of the company26. Thus it could be said that this

option is way better than traditional methods of financial analysis.

Dividend growth model:

Dividend growth model is a financial tool which is used to evaluate the valuation of

the stock price of the company and the changes into the stock price (face value and market

value). This model could be conducted through the help of dividend payment, dividend

growth rate and the cost of equity. The purpose of the calculation is to evaluate the value of

the shares so that it becomes easy for the investors to make a decision about investment in

the company. The changes of the amount and the value of shares could be easily identified

through this tool. But, sometimes difficulties create to do the calculations due to the growth

%. The following is the formula of dividend growth model analysis:

Gordon Growth Model: stock price = (dividend payment in the next period) / (cost

of equity - dividend growth rate) 27

It has described into his study that dividend growth model is way better than

traditional financial evaluation methods due to its huge area as it takes the concern of

internal as well as market changes of the company28. It has been added further that for

calculating the DGM, dividend payment, growth rate, and cost of equity is required to

evaluate which could be found through the market. This makes it easy for the investors to

25 Eugene F Fama, and French Kenneth R.. "The value premium and the CAPM." The

Journal of Finance 61.5 (2006): 2163-2185.

26 Roelinka Broekhuizen. "Optimizing oral nutritional drink supplementation in patients with

chronic obstructive pulmonary disease." British journal of nutrition 93.6 (2005): 965-971.

27 E. F. M. Wouters et al. "Airway biology." Thorax 60.6 (2005): 480-487.

28 Paul Barnes. "Dividend Growth Model." Wiley Encyclopedia of Management. 2009.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 42

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.