Foreign Exchange Hedging Strategies

VerifiedAdded on 2021/02/22

|8

|1720

|69

AI Summary

This assignment provides a thorough evaluation of different foreign exchange hedging methods, focusing on the money market hedge and historical simulation method. It discusses the advantages and disadvantages of each approach, recommending the money market hedge as more suitable due to its flexibility and customization options. The study emphasizes the importance of hedging in minimizing foreign exchange losses and making effective investment decisions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Project

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

Calculation of value at risk for using both Variance-Covariance and Historical Simulation

method:........................................................................................................................................3

Hedging Strategies

Comparing Costs and Benefits of different Hedging Strategies 6

Recommendation:........................................................................................................................7

CONCLUSION................................................................................................................................7

INTRODUCTION...........................................................................................................................3

Calculation of value at risk for using both Variance-Covariance and Historical Simulation

method:........................................................................................................................................3

Hedging Strategies

Comparing Costs and Benefits of different Hedging Strategies 6

Recommendation:........................................................................................................................7

CONCLUSION................................................................................................................................7

INTRODUCTION

Analysing investment risk is vital for assessing the viability of investment. There are

numerous kind of formulas and scientific or technical methods which helps in evaluation of the

investment proposals (Narayanaswamy, Jayram and Yoong, 2012). This study contains practical

sum of value of risk applying Variance-Covariance and Historical Simulation method, and

evaluates hedging strategies. Report also provides comparison of hedging strategies and

demonstrate the relationship of the payoff and profit of different hedging strategies.

TASK 1

Calculation of value at risk for using both Variance-Covariance and Historical Simulation

method:

Variance-Covariance: The technique of variance-covariance is a quantitative technique for

calculating value at risk. Due to the current presumptions it makes, an individual need distinct

data than all the other techniques to do it again (Variance-Covariance, 2019). The technique of

variance-covariance allows using of covariance such as volatilities and correlations of risk

variables and capital values inclinations with regard to such risk variables with the objective of

calculating the risk valuation. This technique leads straight to the final outcome, i.e. the valuation

at stake of the portfolio; there is no data about business situations. Throughout the whole

measurement, the variance-covariance technique uses linear equations of the risk variables

themselves, sometimes disregarding the drift. Some of the assumption it makes are:

The technique of variance-covariance believes that somehow the earnings of a inventory

portfolio are evenly distributed across the average of a ordinary or bell-shaped allocation

of probability.

Although returns are circulated in an ordinary or bell curve configuration, company need

to have the returns within standard deviation. For the most exchanged stocks, these could

be searched or calculated.

A simplifying aspect of this technique is that shares, generally triggered by certain inter-

nal factor, may generally move forwards and backwards with each other. That implies

company need the covariance of yields against many shares for all the equities in an in-

vestment.

Analysing investment risk is vital for assessing the viability of investment. There are

numerous kind of formulas and scientific or technical methods which helps in evaluation of the

investment proposals (Narayanaswamy, Jayram and Yoong, 2012). This study contains practical

sum of value of risk applying Variance-Covariance and Historical Simulation method, and

evaluates hedging strategies. Report also provides comparison of hedging strategies and

demonstrate the relationship of the payoff and profit of different hedging strategies.

TASK 1

Calculation of value at risk for using both Variance-Covariance and Historical Simulation

method:

Variance-Covariance: The technique of variance-covariance is a quantitative technique for

calculating value at risk. Due to the current presumptions it makes, an individual need distinct

data than all the other techniques to do it again (Variance-Covariance, 2019). The technique of

variance-covariance allows using of covariance such as volatilities and correlations of risk

variables and capital values inclinations with regard to such risk variables with the objective of

calculating the risk valuation. This technique leads straight to the final outcome, i.e. the valuation

at stake of the portfolio; there is no data about business situations. Throughout the whole

measurement, the variance-covariance technique uses linear equations of the risk variables

themselves, sometimes disregarding the drift. Some of the assumption it makes are:

The technique of variance-covariance believes that somehow the earnings of a inventory

portfolio are evenly distributed across the average of a ordinary or bell-shaped allocation

of probability.

Although returns are circulated in an ordinary or bell curve configuration, company need

to have the returns within standard deviation. For the most exchanged stocks, these could

be searched or calculated.

A simplifying aspect of this technique is that shares, generally triggered by certain inter-

nal factor, may generally move forwards and backwards with each other. That implies

company need the covariance of yields against many shares for all the equities in an in-

vestment.

Historical Simulation method: It is also one of the effective calculation techniques for

value-at-risk (VaR) that utilizes historical information to evaluate the effect of market

movements on a portfolio. Since historical simulation utilizes actual information, it can record

unforeseen events and inferences that a conceptual framework would not generally estimate.

Historically documented currency fluctuations are subject to an existing portfolio; this will be

used to produce a allocation of portfolio yields. No complex statistical ideas are needed to use

the historical method. However, you need excellent information and lots of it before the more

precise your assessment will be, the larger the information set company is going to work with.

This model could then be used with such a specified probability to determine the highest loss–

which is, the VaR. The Historical Simulations methodology's basic hypothesis is that company

base its outcomes on their portfolio's previous performance and assume that perhaps the previous

is a good measure of both the immediate future. Some major advantages are:

It does not utilize macroeconomic statements to model the VaR, it works better and espe-

cially when compared with techniques using the normal distribution hypothesis, since the

information on economic yields are thickly tailed.

It's also simpler to calculate and can empirically integrate correlations between assets.

Cost of capital is 12%.

Units 10000

Spread 2%

Variance Covariance

VaR = Value of Portfolio * Sd* Variance of

portfolio

200,000,000 *

2%*12%

= 480000

Calculating VaR Using Historical Simulation

For calculation purpose confidence level is taken at

99%

value-at-risk (VaR) that utilizes historical information to evaluate the effect of market

movements on a portfolio. Since historical simulation utilizes actual information, it can record

unforeseen events and inferences that a conceptual framework would not generally estimate.

Historically documented currency fluctuations are subject to an existing portfolio; this will be

used to produce a allocation of portfolio yields. No complex statistical ideas are needed to use

the historical method. However, you need excellent information and lots of it before the more

precise your assessment will be, the larger the information set company is going to work with.

This model could then be used with such a specified probability to determine the highest loss–

which is, the VaR. The Historical Simulations methodology's basic hypothesis is that company

base its outcomes on their portfolio's previous performance and assume that perhaps the previous

is a good measure of both the immediate future. Some major advantages are:

It does not utilize macroeconomic statements to model the VaR, it works better and espe-

cially when compared with techniques using the normal distribution hypothesis, since the

information on economic yields are thickly tailed.

It's also simpler to calculate and can empirically integrate correlations between assets.

Cost of capital is 12%.

Units 10000

Spread 2%

Variance Covariance

VaR = Value of Portfolio * Sd* Variance of

portfolio

200,000,000 *

2%*12%

= 480000

Calculating VaR Using Historical Simulation

For calculation purpose confidence level is taken at

99%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

.12 - .02 = 0.1

So results are above the confidence level investment portfolio

is viable.

Hedging Strategies

Currency Forwards:

A currency forward is one which is used in the foreign markets to lockdown the exchange rate

while completing a sale or purchase transaction. Settlement for this type of financial instrument

can be done either in cash or on a delivery basis. This is only possible when the option is

mutually acceptable and has been mentioned in the contract at the time it was signed by the

contractual parties. As a hedging mechanism, a currency forward would ensure that the British

Company as well as IntUSA would be safe from fluctuations occurring in the global exchange

rates. As a result, the risk of losing by one party at the expense of another would be greatly

minimised as on the time of payment only that rate would be taken into account which was

agreed upon between both the parties when they were signing the contract of Currency Forwards

(Di Nunno, Khedher and Vanmaele, 2015).

Money Market:

Hedging through money market is a technique which locks in the value of foreign currency

transaction in terms of the company’s domestic currency. Thus, enabling the domestic business

entity to prevent or minimise the currency risk while undertaking an international transaction. If

InstUSA sells its 10,000 units at prevalent exchange rate of US$1 and pound sterling relative at

the time of signing the contract. It can execute its money market hedge in the following way:

a. Buying the current value of the foreign currency transaction amount at the spot rate.

b. Placing the foreign currency purchased on deposit and receiving interest until payment is

made.

c. Using the deposit to make the foreign currency payment.

Currency Options:

So results are above the confidence level investment portfolio

is viable.

Hedging Strategies

Currency Forwards:

A currency forward is one which is used in the foreign markets to lockdown the exchange rate

while completing a sale or purchase transaction. Settlement for this type of financial instrument

can be done either in cash or on a delivery basis. This is only possible when the option is

mutually acceptable and has been mentioned in the contract at the time it was signed by the

contractual parties. As a hedging mechanism, a currency forward would ensure that the British

Company as well as IntUSA would be safe from fluctuations occurring in the global exchange

rates. As a result, the risk of losing by one party at the expense of another would be greatly

minimised as on the time of payment only that rate would be taken into account which was

agreed upon between both the parties when they were signing the contract of Currency Forwards

(Di Nunno, Khedher and Vanmaele, 2015).

Money Market:

Hedging through money market is a technique which locks in the value of foreign currency

transaction in terms of the company’s domestic currency. Thus, enabling the domestic business

entity to prevent or minimise the currency risk while undertaking an international transaction. If

InstUSA sells its 10,000 units at prevalent exchange rate of US$1 and pound sterling relative at

the time of signing the contract. It can execute its money market hedge in the following way:

a. Buying the current value of the foreign currency transaction amount at the spot rate.

b. Placing the foreign currency purchased on deposit and receiving interest until payment is

made.

c. Using the deposit to make the foreign currency payment.

Currency Options:

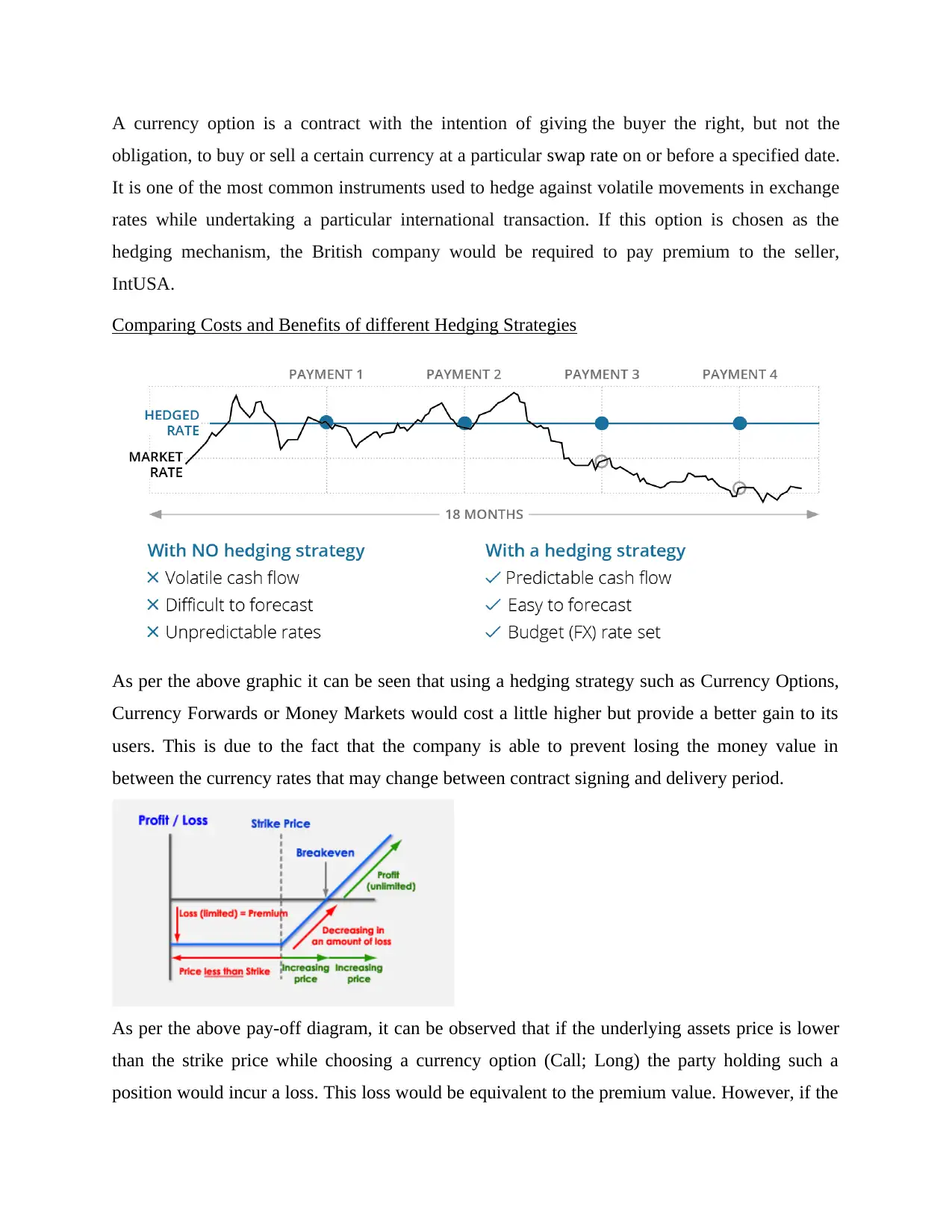

A currency option is a contract with the intention of giving the buyer the right, but not the

obligation, to buy or sell a certain currency at a particular swap rate on or before a specified date.

It is one of the most common instruments used to hedge against volatile movements in exchange

rates while undertaking a particular international transaction. If this option is chosen as the

hedging mechanism, the British company would be required to pay premium to the seller,

IntUSA.

Comparing Costs and Benefits of different Hedging Strategies

As per the above graphic it can be seen that using a hedging strategy such as Currency Options,

Currency Forwards or Money Markets would cost a little higher but provide a better gain to its

users. This is due to the fact that the company is able to prevent losing the money value in

between the currency rates that may change between contract signing and delivery period.

As per the above pay-off diagram, it can be observed that if the underlying assets price is lower

than the strike price while choosing a currency option (Call; Long) the party holding such a

position would incur a loss. This loss would be equivalent to the premium value. However, if the

obligation, to buy or sell a certain currency at a particular swap rate on or before a specified date.

It is one of the most common instruments used to hedge against volatile movements in exchange

rates while undertaking a particular international transaction. If this option is chosen as the

hedging mechanism, the British company would be required to pay premium to the seller,

IntUSA.

Comparing Costs and Benefits of different Hedging Strategies

As per the above graphic it can be seen that using a hedging strategy such as Currency Options,

Currency Forwards or Money Markets would cost a little higher but provide a better gain to its

users. This is due to the fact that the company is able to prevent losing the money value in

between the currency rates that may change between contract signing and delivery period.

As per the above pay-off diagram, it can be observed that if the underlying assets price is lower

than the strike price while choosing a currency option (Call; Long) the party holding such a

position would incur a loss. This loss would be equivalent to the premium value. However, if the

underlying asset price is greater than the strike price, the holder would experience a decline in its

losses as the price increases to the where it reaches the breakeven and beyond which the pay-off

for the holder would be in the form of higher profits. The opposite is true in the case of Put

Option holders.

Recommendation:

From above evaluation of different hedging strategies, it has been analysed that Money Market

hedge is more appropriate as it emphasises purely on current rates. It could be applied efficiently

in respect of currencies in which forward contracts are not effectively available like customised

investment portfolio (Krey and Riahi, 2013). This hedging method is also useful for a small

entity or business which does not have access to the currency forward market, as noted earlier.

The money market hedge can be customized to precise amounts and dates. Though this degree of

customization is also available in currency forwards, the forward market is not readily accessible

to everyone. The money market hedge is more complicated than regular currency forwards, since

it is a step-by-step deconstruction of the latter. It may therefore be suitable for hedging

occasional or one-off transactions, but as it involves a number of distinct steps, may be too

cumbersome for frequent transactions.

CONCLUSION

From above study it has been articulated that adopting different methods can provide

easiness in conducting risk analysis. However, choosing most appropriate method and strategies

is a difficult task but a thoroughly evaluation of all aspects can make it simple. Mostly in foreign

contracts hedging is crucial as it assist in minimising foreign exchange losses. Hedging is vital

for preparing a effective portfolio and making an effective market and investment decision.

Companies specially conducts such king of analysis to ensure that their decisions are effective.

losses as the price increases to the where it reaches the breakeven and beyond which the pay-off

for the holder would be in the form of higher profits. The opposite is true in the case of Put

Option holders.

Recommendation:

From above evaluation of different hedging strategies, it has been analysed that Money Market

hedge is more appropriate as it emphasises purely on current rates. It could be applied efficiently

in respect of currencies in which forward contracts are not effectively available like customised

investment portfolio (Krey and Riahi, 2013). This hedging method is also useful for a small

entity or business which does not have access to the currency forward market, as noted earlier.

The money market hedge can be customized to precise amounts and dates. Though this degree of

customization is also available in currency forwards, the forward market is not readily accessible

to everyone. The money market hedge is more complicated than regular currency forwards, since

it is a step-by-step deconstruction of the latter. It may therefore be suitable for hedging

occasional or one-off transactions, but as it involves a number of distinct steps, may be too

cumbersome for frequent transactions.

CONCLUSION

From above study it has been articulated that adopting different methods can provide

easiness in conducting risk analysis. However, choosing most appropriate method and strategies

is a difficult task but a thoroughly evaluation of all aspects can make it simple. Mostly in foreign

contracts hedging is crucial as it assist in minimising foreign exchange losses. Hedging is vital

for preparing a effective portfolio and making an effective market and investment decision.

Companies specially conducts such king of analysis to ensure that their decisions are effective.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Narayanaswamy, B., Jayram, T.S. and Yoong, V.N., 2012, October. Hedging strategies for

renewable resource integration and uncertainty management in the smart grid. In 2012

3rd IEEE PES Innovative Smart Grid Technologies Europe (ISGT Europe) (pp. 1-8).

IEEE.

Di Nunno, G., Khedher, A. and Vanmaele, M., 2015. Robustness of quadratic hedging strategies

in finance via backward stochastic differential equations with jumps. Applied

Mathematics & Optimization, 72(3). pp. 353-389.

Krey, V. and Riahi, K., 2013. Risk hedging strategies under energy system and climate policy

uncertainties. In Handbook of Risk Management in Energy Production and Trading (pp.

435-474). Springer, Boston, MA.

Online

Variance-Covariance. 2019. [Online] Available through: <

https://link.springer.com/chapter/10.1057/9780230234758_20 >.

Historical Simulation method. 2019. [Online] Available through: <https://www.value-at-

risk.net/motivation-historical-simulation/>.

Books and Journals:

Narayanaswamy, B., Jayram, T.S. and Yoong, V.N., 2012, October. Hedging strategies for

renewable resource integration and uncertainty management in the smart grid. In 2012

3rd IEEE PES Innovative Smart Grid Technologies Europe (ISGT Europe) (pp. 1-8).

IEEE.

Di Nunno, G., Khedher, A. and Vanmaele, M., 2015. Robustness of quadratic hedging strategies

in finance via backward stochastic differential equations with jumps. Applied

Mathematics & Optimization, 72(3). pp. 353-389.

Krey, V. and Riahi, K., 2013. Risk hedging strategies under energy system and climate policy

uncertainties. In Handbook of Risk Management in Energy Production and Trading (pp.

435-474). Springer, Boston, MA.

Online

Variance-Covariance. 2019. [Online] Available through: <

https://link.springer.com/chapter/10.1057/9780230234758_20 >.

Historical Simulation method. 2019. [Online] Available through: <https://www.value-at-

risk.net/motivation-historical-simulation/>.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.