Financial Reporting: Mortgage Requirements and Investment Analysis

VerifiedAdded on 2023/01/19

|9

|1858

|37

Report

AI Summary

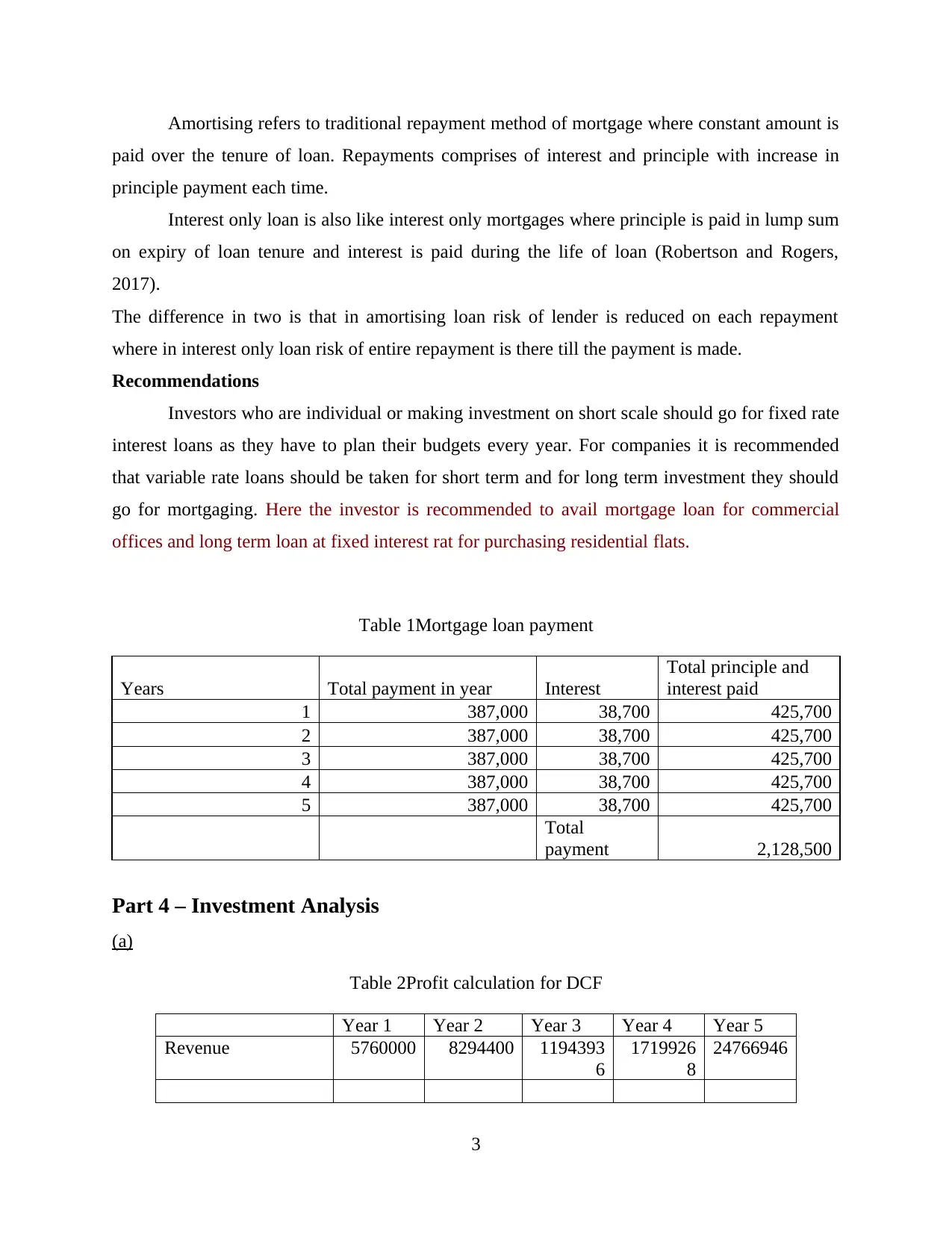

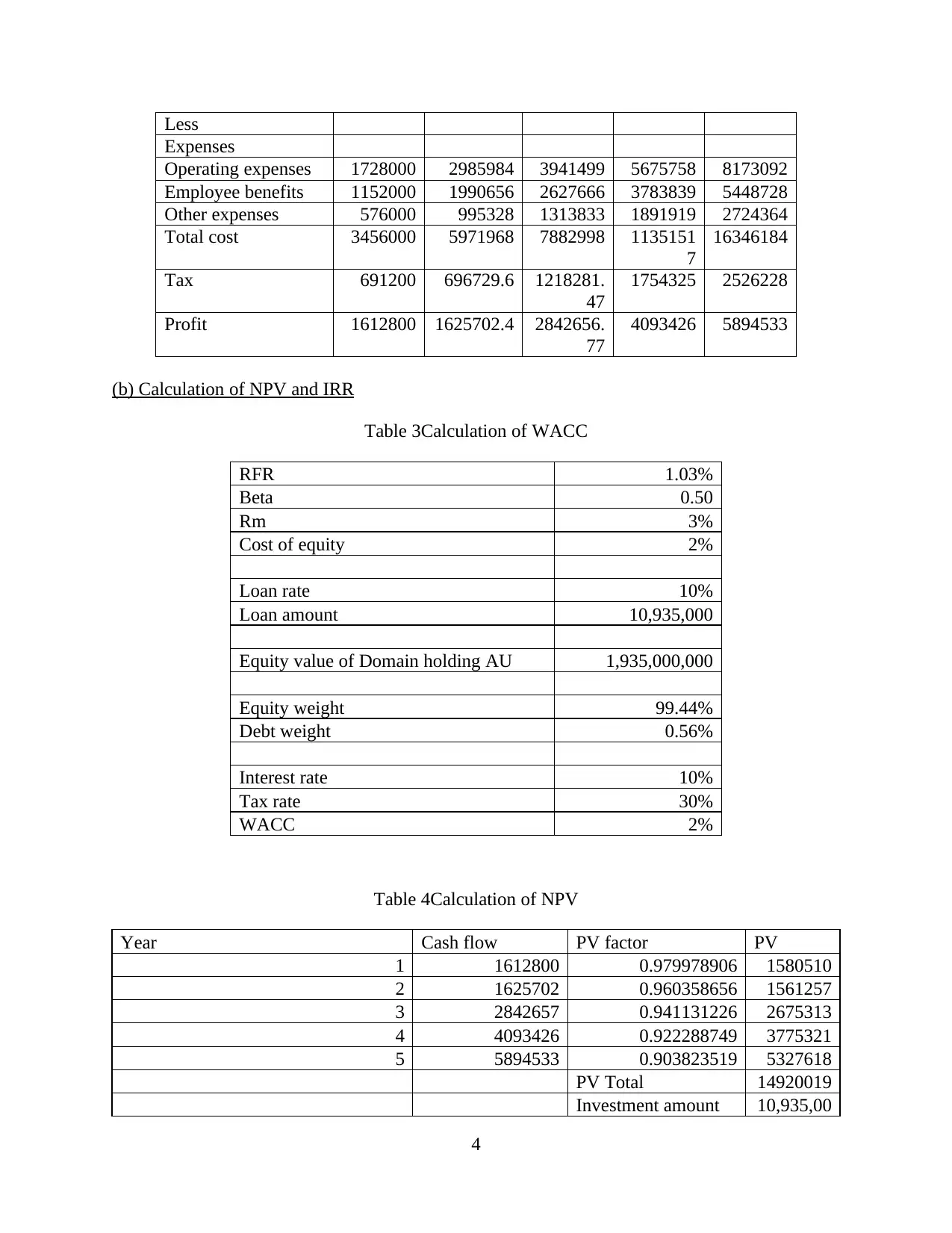

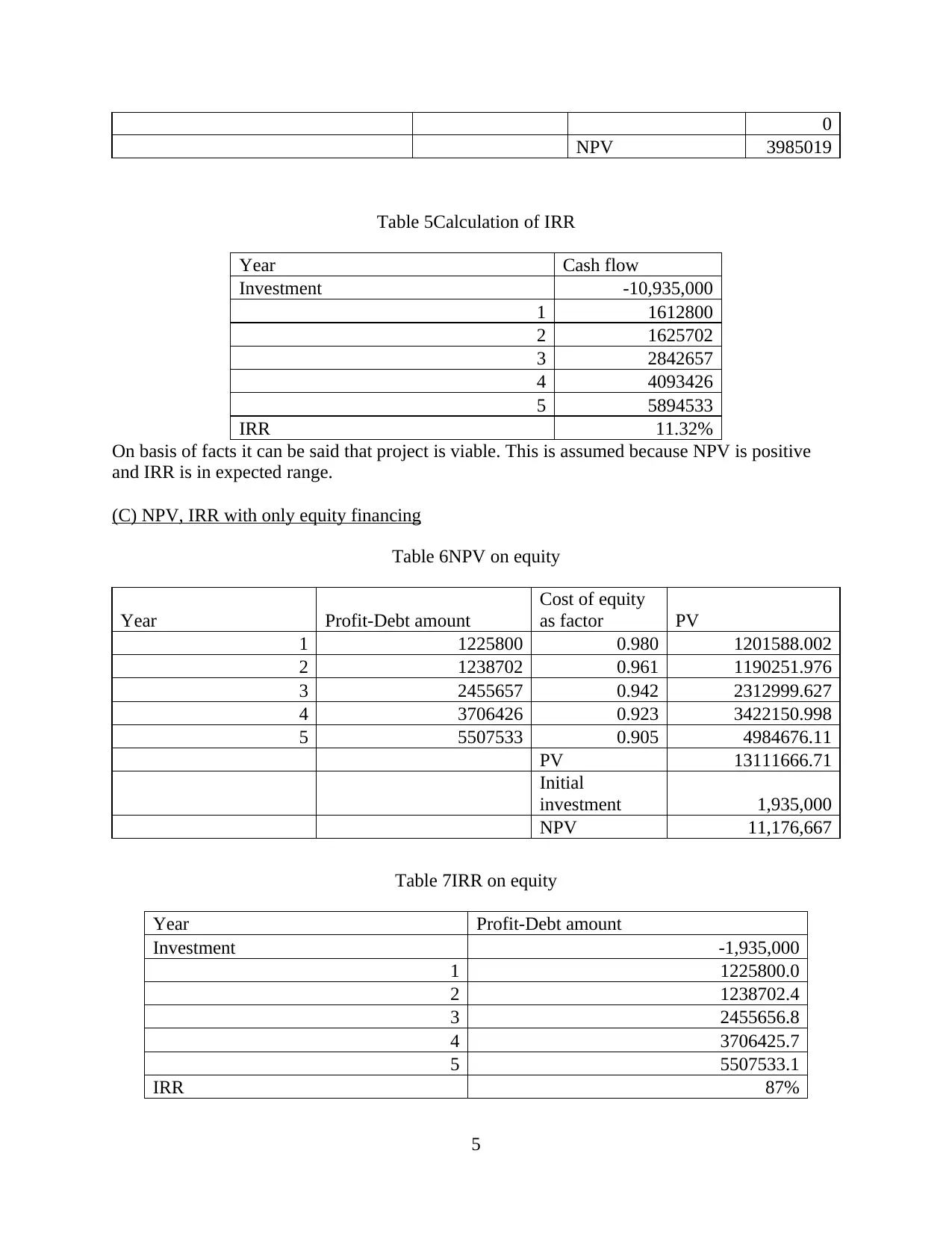

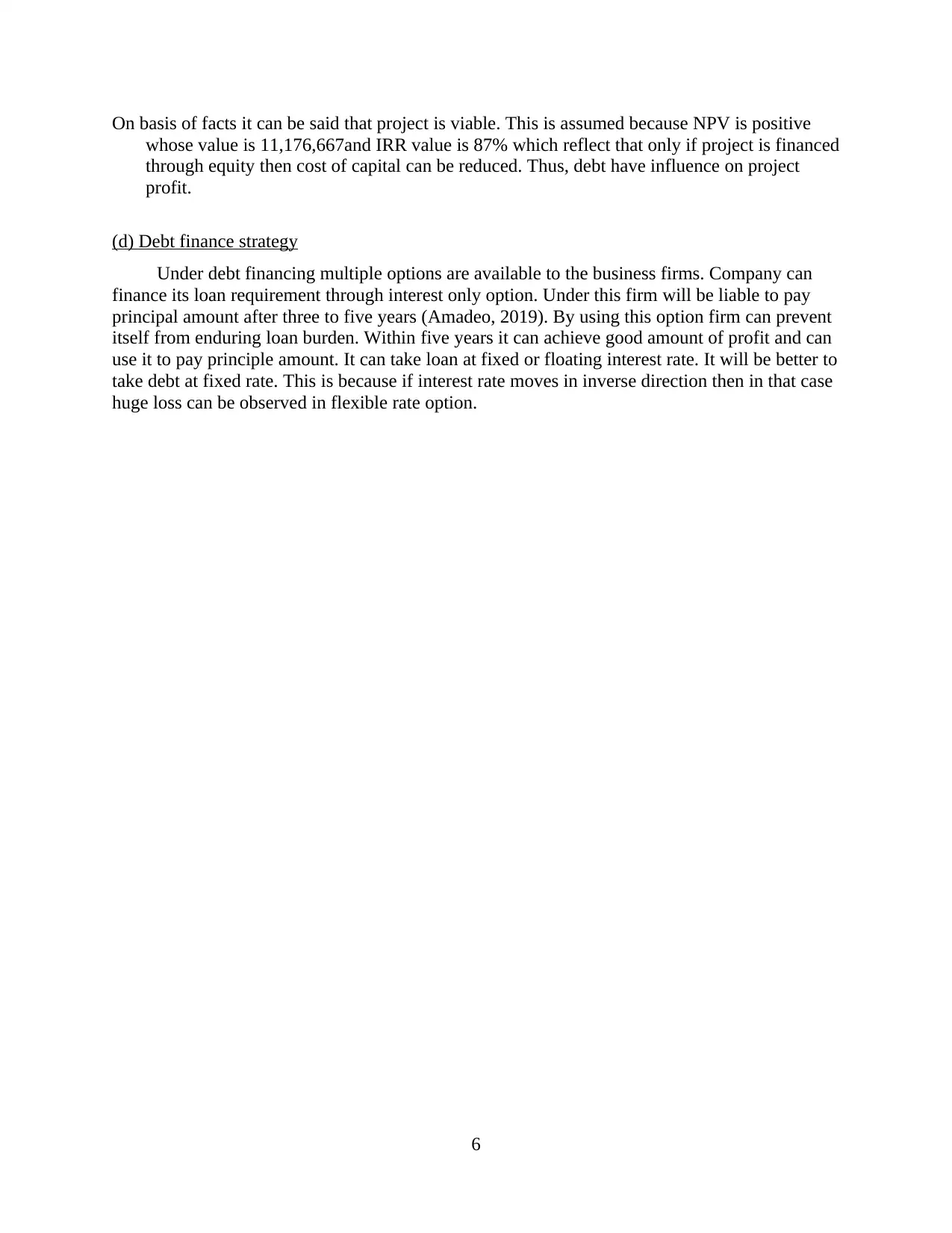

This report presents a financial analysis of income property investments, examining the property market, mortgage requirements, and various investment strategies. The introduction defines income property and its benefits, followed by an overview of the property market, highlighting trends and the growth of REITs. The report then explores mortgage requirements, including different loan options like fixed and variable interest rates, amortizing loans, and interest-only loans, with recommendations for investors. Part 4 focuses on investment analysis, including profit calculations, NPV and IRR calculations, and an analysis of equity financing. The report concludes with a discussion of debt financing strategies, offering insights into interest-only options and fixed versus floating interest rates, providing a comprehensive overview of financial reporting and investment decision-making in the real estate sector.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.