HA3042 Taxation Law Assignment - Financial Year 2019-20

VerifiedAdded on 2023/01/11

|9

|2147

|43

Homework Assignment

AI Summary

This assignment solution addresses two key taxation scenarios. The first question focuses on the deductibility of expenses for a hospitality business, specifically analyzing whether replacing a commercial kitchen constitutes a deductible capital work expenditure or a repair. It references relevant Australian Taxation Office (ATO) guidelines and rulings. The second question calculates the tax liability of an individual involved in a musical instrument business and teaching, encompassing income from sales, salary, dividends, and interest, considering relevant sections of the Income Tax Assessment Act 1997 and ATO guidelines. The solution details the calculation of taxable income and the application of marginal tax rates and Medicare levy, providing a comprehensive breakdown of each income component and deduction.

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

QUESTION 1..................................................................................................................................1

Deductibility/ Non deductibility of Taxable income...................................................................1

QUESTION 2..................................................................................................................................3

Tax liability of Tom for the year 2019-20...................................................................................3

REFERENCES................................................................................................................................7

TABLE OF CONTENTS................................................................................................................2

QUESTION 1..................................................................................................................................1

Deductibility/ Non deductibility of Taxable income...................................................................1

QUESTION 2..................................................................................................................................3

Tax liability of Tom for the year 2019-20...................................................................................3

REFERENCES................................................................................................................................7

QUESTION 1

Deductibility/ Non deductibility of Taxable income

In this question Francis is experienced working businessman in hospitality industry for

number of years. Commercial kitchen in restaurant were in poor condition. He is planning to

replace whole commercial kitchen which will be costing $23000. Cost of the repairing and

kitchen appliances will be $4900, however some parts are not available in market anymore as

appliances are obsolete and old. Francis decides of replacing commercial kitchen with new

modern appliances as there are new appliance in market having better features and the durability.

Since Francis is running restaurant business and kitchen in the restaurant is considered as

part of the commercial properties that is used for producing assessable income. There are

provisions regarding the amount and nature of expenses that could be claimed under the

deductions (Aquilina, 2019). For claiming the deduction it is essential to identify the nature of

transaction that whether it is a deductible regular expense of capital expenditure. Replacing

whole commercial kitchen will be classified as capital work expenditure.

Tax payer can claim deduction for the capital expenditures incurred for producing assessable

income such as building and structural improvements are written off as capital expenditures. Any

individual could claim deduction for building, extensions or the improvements, alteration to

building including leasehold improvements and such other. if it is not possible to reliably

determine the cost of construction, estimate from independent qualified person. Australian

taxation office allows the publicans and hoteliers & publicans for claiming capital allowances for

wear and tear over the time of building and depreciation of plant and equipments over time.

There are many publican that lose significant amount of money and many dollars for the tax

deductions as not effectively accounting for removal and disposal of the building & assets when

the properties are upgraded

People are claiming deductions over the renovation of properties and commercial premises.

In the hospitality industry kitchen is considered as the part of income producing unit. The assets

used in kitchen are capital assets therefore the tax deductions are available to the businessman in

the form of depreciation (McGregor-Lowndes and Hannah, 2017). Australian taxation office

provides for owners of the income producing properties for claiming deductions of natural wear

and tear which occurs to the building or commercial premises. Depreciation on structure of

building through capital work deductions.

1

Deductibility/ Non deductibility of Taxable income

In this question Francis is experienced working businessman in hospitality industry for

number of years. Commercial kitchen in restaurant were in poor condition. He is planning to

replace whole commercial kitchen which will be costing $23000. Cost of the repairing and

kitchen appliances will be $4900, however some parts are not available in market anymore as

appliances are obsolete and old. Francis decides of replacing commercial kitchen with new

modern appliances as there are new appliance in market having better features and the durability.

Since Francis is running restaurant business and kitchen in the restaurant is considered as

part of the commercial properties that is used for producing assessable income. There are

provisions regarding the amount and nature of expenses that could be claimed under the

deductions (Aquilina, 2019). For claiming the deduction it is essential to identify the nature of

transaction that whether it is a deductible regular expense of capital expenditure. Replacing

whole commercial kitchen will be classified as capital work expenditure.

Tax payer can claim deduction for the capital expenditures incurred for producing assessable

income such as building and structural improvements are written off as capital expenditures. Any

individual could claim deduction for building, extensions or the improvements, alteration to

building including leasehold improvements and such other. if it is not possible to reliably

determine the cost of construction, estimate from independent qualified person. Australian

taxation office allows the publicans and hoteliers & publicans for claiming capital allowances for

wear and tear over the time of building and depreciation of plant and equipments over time.

There are many publican that lose significant amount of money and many dollars for the tax

deductions as not effectively accounting for removal and disposal of the building & assets when

the properties are upgraded

People are claiming deductions over the renovation of properties and commercial premises.

In the hospitality industry kitchen is considered as the part of income producing unit. The assets

used in kitchen are capital assets therefore the tax deductions are available to the businessman in

the form of depreciation (McGregor-Lowndes and Hannah, 2017). Australian taxation office

provides for owners of the income producing properties for claiming deductions of natural wear

and tear which occurs to the building or commercial premises. Depreciation on structure of

building through capital work deductions.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital work deduction on structural assets like kitchen equipments, walls, roof tiles are not

affected by legislative changes and could be claimed by owners of income producing properties.

The deductions make around 85%-90 % of depreciation claim. When the structural assets are

removed there could be depreciation deduction available. Process called scrapping is often

applied that allows the investors in claiming deduction in year when items are actually removed.

As per the taxation office item for which immediate claims could be made are repairs to

investment properties for making good or identifying damages, defects or deterioration of

property. Management & maintenance cost like corporate fees, advertising, cleaning, land tax,

council rates etc.

Any major renovation in the commercial building such as restaurants, hotels etc of

bathroom, kitchen are classified under capital improvements by ATO and such expenditures are

claimed under capital work deductions. The expenditure could not be claimed in year in which

they are incurred. Deductions expenses incurred in renovating/ buildings and depreciation are

deducted over number of years.

Expenditures that are made on the property are allowed for deduction. Repairs carried out by

the taxpayers should directly relate to wear& tear or the damages occurred due to use of property

for producing assessable income. Repairs usually involve renewals or replacement of the broken

or worn out part. The repairs are considered of capital nature and no deduction is allowed when

the entire structure of the property is being replaced like building kitchen, cupboard, refrigerators

and such other things. Renovations, extensions, improvements and the alterations. Initial repairs

expenses for remedying the defects, deterioration or damage which existed at date of acquiring

the property (Capital Works deduction, 2019). Capital work deduction is available for such

expenditures and repairs. Capital nature expenses will be forming part of cost base of property

while measuring capital gains tax. Examples of repairs include replacement of broken windows,

repairing of electrical appliances, maintaining plumbing etc. Deduction is available if it is related

for producing assessable income.

In this case replacing the kitchen is considered part of the income producing property which

is restaurant. Replacing the kitchen is counted as capital works deductions under division 43 of

Income Tax Assessment Act, 1997. Expenditures incurred for capital works are not allowed for

deduction under one income year. However repairs on kitchen appliances during the income year

2

affected by legislative changes and could be claimed by owners of income producing properties.

The deductions make around 85%-90 % of depreciation claim. When the structural assets are

removed there could be depreciation deduction available. Process called scrapping is often

applied that allows the investors in claiming deduction in year when items are actually removed.

As per the taxation office item for which immediate claims could be made are repairs to

investment properties for making good or identifying damages, defects or deterioration of

property. Management & maintenance cost like corporate fees, advertising, cleaning, land tax,

council rates etc.

Any major renovation in the commercial building such as restaurants, hotels etc of

bathroom, kitchen are classified under capital improvements by ATO and such expenditures are

claimed under capital work deductions. The expenditure could not be claimed in year in which

they are incurred. Deductions expenses incurred in renovating/ buildings and depreciation are

deducted over number of years.

Expenditures that are made on the property are allowed for deduction. Repairs carried out by

the taxpayers should directly relate to wear& tear or the damages occurred due to use of property

for producing assessable income. Repairs usually involve renewals or replacement of the broken

or worn out part. The repairs are considered of capital nature and no deduction is allowed when

the entire structure of the property is being replaced like building kitchen, cupboard, refrigerators

and such other things. Renovations, extensions, improvements and the alterations. Initial repairs

expenses for remedying the defects, deterioration or damage which existed at date of acquiring

the property (Capital Works deduction, 2019). Capital work deduction is available for such

expenditures and repairs. Capital nature expenses will be forming part of cost base of property

while measuring capital gains tax. Examples of repairs include replacement of broken windows,

repairing of electrical appliances, maintaining plumbing etc. Deduction is available if it is related

for producing assessable income.

In this case replacing the kitchen is considered part of the income producing property which

is restaurant. Replacing the kitchen is counted as capital works deductions under division 43 of

Income Tax Assessment Act, 1997. Expenditures incurred for capital works are not allowed for

deduction under one income year. However repairs on kitchen appliances during the income year

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are not considered as capital expenses as they are carried out due to normal wear and tear of the

appliances.

Replacing the whole kitchen will considered under capital improvements for producing

assessable income as per the guidelines provided by the ATO. Therefore as per the Section 43 of

ITAA replacing whole kitchen will be counted as capital works and deduction will be available

in the form of deduction over useful life. However the repairs expenses of $4900 could be

claimed as deduction in the year in which they are incurred. The repairs are deductible as per the

provisions of Section 25 of ITAA, 1997 as it is made to the kitchen appliance that is mainly used

for producing the assessed for that period. Taxation Ruling 2007/9 provides for capital

expenditures over hotels and restaurants (ITAA, 1997. 2019). On the other if only repairs were

made in the whole kitchen in place of renovation or replacement whole expenditure would have

been considered as repairs and deduction would have been claimed under section 25 of the act.

QUESTION 2

Tom owns a business named Tom’s Band in Sydney selling musical instruments. He also

gives guitar teaching classes on casual basis at Guitar school in Sydney that is local musical

college. Tom has incurred transactions for the income year and based on these taxable receipts of

Tom are to be calculated for the financial year 2019-20.

Tax liability of Tom for the year 2019-20

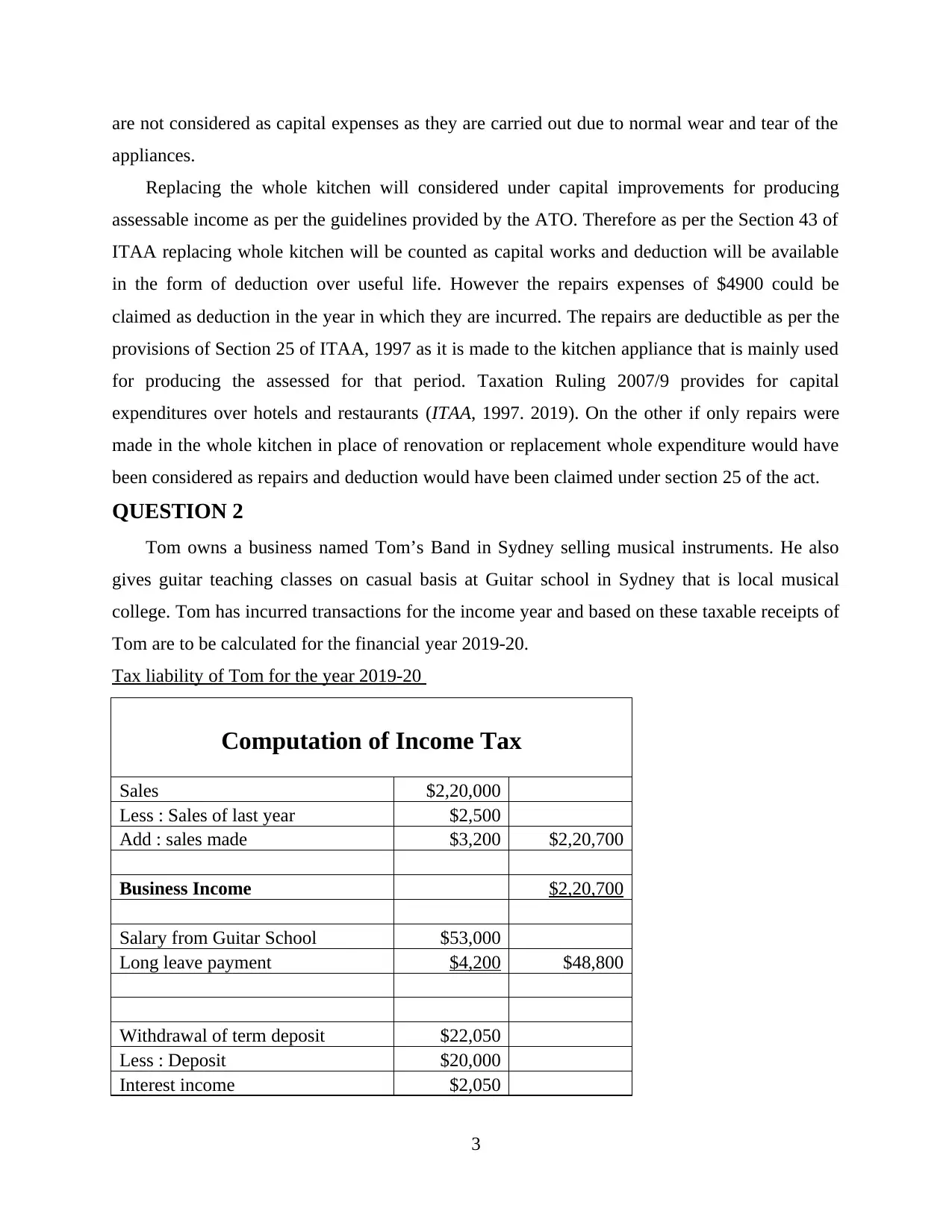

Computation of Income Tax

Sales $2,20,000

Less : Sales of last year $2,500

Add : sales made $3,200 $2,20,700

Business Income $2,20,700

Salary from Guitar School $53,000

Long leave payment $4,200 $48,800

Withdrawal of term deposit $22,050

Less : Deposit $20,000

Interest income $2,050

3

appliances.

Replacing the whole kitchen will considered under capital improvements for producing

assessable income as per the guidelines provided by the ATO. Therefore as per the Section 43 of

ITAA replacing whole kitchen will be counted as capital works and deduction will be available

in the form of deduction over useful life. However the repairs expenses of $4900 could be

claimed as deduction in the year in which they are incurred. The repairs are deductible as per the

provisions of Section 25 of ITAA, 1997 as it is made to the kitchen appliance that is mainly used

for producing the assessed for that period. Taxation Ruling 2007/9 provides for capital

expenditures over hotels and restaurants (ITAA, 1997. 2019). On the other if only repairs were

made in the whole kitchen in place of renovation or replacement whole expenditure would have

been considered as repairs and deduction would have been claimed under section 25 of the act.

QUESTION 2

Tom owns a business named Tom’s Band in Sydney selling musical instruments. He also

gives guitar teaching classes on casual basis at Guitar school in Sydney that is local musical

college. Tom has incurred transactions for the income year and based on these taxable receipts of

Tom are to be calculated for the financial year 2019-20.

Tax liability of Tom for the year 2019-20

Computation of Income Tax

Sales $2,20,000

Less : Sales of last year $2,500

Add : sales made $3,200 $2,20,700

Business Income $2,20,700

Salary from Guitar School $53,000

Long leave payment $4,200 $48,800

Withdrawal of term deposit $22,050

Less : Deposit $20,000

Interest income $2,050

3

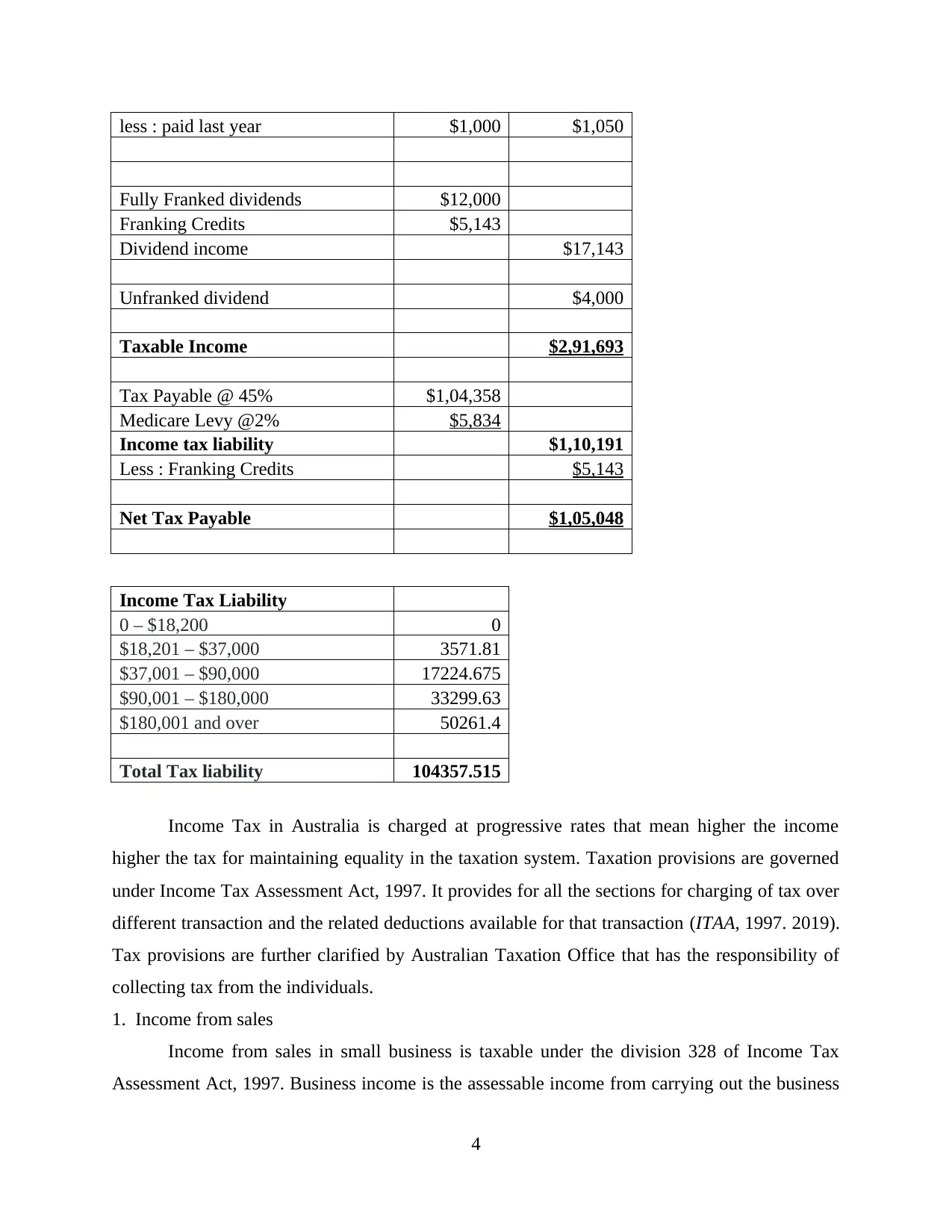

less : paid last year $1,000 $1,050

Fully Franked dividends $12,000

Franking Credits $5,143

Dividend income $17,143

Unfranked dividend $4,000

Taxable Income $2,91,693

Tax Payable @ 45% $1,04,358

Medicare Levy @2% $5,834

Income tax liability $1,10,191

Less : Franking Credits $5,143

Net Tax Payable $1,05,048

Income Tax Liability

0 – $18,200 0

$18,201 – $37,000 3571.81

$37,001 – $90,000 17224.675

$90,001 – $180,000 33299.63

$180,001 and over 50261.4

Total Tax liability 104357.515

Income Tax in Australia is charged at progressive rates that mean higher the income

higher the tax for maintaining equality in the taxation system. Taxation provisions are governed

under Income Tax Assessment Act, 1997. It provides for all the sections for charging of tax over

different transaction and the related deductions available for that transaction (ITAA, 1997. 2019).

Tax provisions are further clarified by Australian Taxation Office that has the responsibility of

collecting tax from the individuals.

1. Income from sales

Income from sales in small business is taxable under the division 328 of Income Tax

Assessment Act, 1997. Business income is the assessable income from carrying out the business

4

Fully Franked dividends $12,000

Franking Credits $5,143

Dividend income $17,143

Unfranked dividend $4,000

Taxable Income $2,91,693

Tax Payable @ 45% $1,04,358

Medicare Levy @2% $5,834

Income tax liability $1,10,191

Less : Franking Credits $5,143

Net Tax Payable $1,05,048

Income Tax Liability

0 – $18,200 0

$18,201 – $37,000 3571.81

$37,001 – $90,000 17224.675

$90,001 – $180,000 33299.63

$180,001 and over 50261.4

Total Tax liability 104357.515

Income Tax in Australia is charged at progressive rates that mean higher the income

higher the tax for maintaining equality in the taxation system. Taxation provisions are governed

under Income Tax Assessment Act, 1997. It provides for all the sections for charging of tax over

different transaction and the related deductions available for that transaction (ITAA, 1997. 2019).

Tax provisions are further clarified by Australian Taxation Office that has the responsibility of

collecting tax from the individuals.

1. Income from sales

Income from sales in small business is taxable under the division 328 of Income Tax

Assessment Act, 1997. Business income is the assessable income from carrying out the business

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

during the year. it also includes the capital gain, income from personal services and deduction

are also there for the work related expenses for the business carried out by the tax payer. Sales

include $2500 that would have been recorded in the year it has been earned and therefore the tax

would have already been paid (Hockridge, 2018). Due to this it is deducting from sales of current

year. Similarly sales made in current year are included in the year they are earned and not the

year in which payments are received. Therefore the sales of $3200 in included in sales for

current year.

2. Long service leave

Long service leave is allowed to employees who have been working for long period of

time in Australia. This entitlement differs in every state of Australia. the leave pay rate should be

as per the normal routine working hours worked out by the employee. Employers are required to

withhold tax for long leave under section 83 of ITAA,1997. Therefore the tax will be paid in

year the leave is taken that is following year.

3. Tom has withdrawn capital deposits

ITAA, 1997 do not provides for tax on the withdrawal of capital deposits from the banks.

however as per the guidelines given by the ATO it could be identified clearly that indivisual is

required to pay tax over the interest income earned from any deposit. The interest earned by Tom

is reinvested in deposits on which also interest is received this year. As per ITAA, 1997 Tom is

liable to pay tax over interest that is earned in present year as tax over $1000 is already paid in

last year.

4. Fully Franked Dividends

Dividends in Australia are taxed by assessing that shareholder is resident of Australia.

Division 220 of ITAA provides for dividends. Tax payer is allowed for franking tax offset for

tax that has already been paid by the company on their income. Franking tax offset covert partly

or whole tax payable on dividends. On fully franked dividends individual is allowed to claim

offset for the credits that have been already paid by the company on dividends (Hoppe, 2020).

Franking credits of $5143 are allowed for offset from the total dividends that are received by

Tom in the current year.

5. Unfranked dividends

Unfranked dividends do not have credits attached to it. When unfranked dividends are

received individual is require to pay tax return over it. Section 802 of ITAA, 1997 provides for

5

are also there for the work related expenses for the business carried out by the tax payer. Sales

include $2500 that would have been recorded in the year it has been earned and therefore the tax

would have already been paid (Hockridge, 2018). Due to this it is deducting from sales of current

year. Similarly sales made in current year are included in the year they are earned and not the

year in which payments are received. Therefore the sales of $3200 in included in sales for

current year.

2. Long service leave

Long service leave is allowed to employees who have been working for long period of

time in Australia. This entitlement differs in every state of Australia. the leave pay rate should be

as per the normal routine working hours worked out by the employee. Employers are required to

withhold tax for long leave under section 83 of ITAA,1997. Therefore the tax will be paid in

year the leave is taken that is following year.

3. Tom has withdrawn capital deposits

ITAA, 1997 do not provides for tax on the withdrawal of capital deposits from the banks.

however as per the guidelines given by the ATO it could be identified clearly that indivisual is

required to pay tax over the interest income earned from any deposit. The interest earned by Tom

is reinvested in deposits on which also interest is received this year. As per ITAA, 1997 Tom is

liable to pay tax over interest that is earned in present year as tax over $1000 is already paid in

last year.

4. Fully Franked Dividends

Dividends in Australia are taxed by assessing that shareholder is resident of Australia.

Division 220 of ITAA provides for dividends. Tax payer is allowed for franking tax offset for

tax that has already been paid by the company on their income. Franking tax offset covert partly

or whole tax payable on dividends. On fully franked dividends individual is allowed to claim

offset for the credits that have been already paid by the company on dividends (Hoppe, 2020).

Franking credits of $5143 are allowed for offset from the total dividends that are received by

Tom in the current year.

5. Unfranked dividends

Unfranked dividends do not have credits attached to it. When unfranked dividends are

received individual is require to pay tax return over it. Section 802 of ITAA, 1997 provides for

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

unfranked dividend distribution. Tom is required to pay tax over the unfranked dividends

received.

6. Tax liability

Tax liability is calculated at the marginal rates that are applicable over the taxable income of

Tom. Tom is required to pay marginal tax rate of 45% on taxable income and Medicare levy of

2% on the taxable income. Net tax payable by Tom for the financial year 2019-20 is $105048.

6

received.

6. Tax liability

Tax liability is calculated at the marginal rates that are applicable over the taxable income of

Tom. Tom is required to pay marginal tax rate of 45% on taxable income and Medicare levy of

2% on the taxable income. Net tax payable by Tom for the financial year 2019-20 is $105048.

6

REFERENCES

Books and Journals

Aquilina, J., 2019, November. Reforming and realigning Division 855 of the Income Tax

Assessment Act 1997 to give better effect to its policy objectives. In Australian Tax

Forum (Vol. 34, No. 1).

McGregor-Lowndes, M. and Hannah, F.M., 2017. ACPNS Legal Case Notes Series: 2017-5

Glasby & Ors as Trustees Of The BCS Foundation v Attorney General of New South

Wales.

Loiacono, R. and Mortimer, C., 2017. Retrospective Tax Law: Has Pandora's Box Opened Never

to Be Shut Again. Ejtr. 15. p.105.

Hockridge, P., 2018. Alienation of income and. Tax Specialist. 22(1). p.30.

Hoppe, T., 2020. Tax Complexity in Australia–A Survey-Based Comparison to the OECD

Average.

Online

ITAA, 1997. 2019. [Online]. Available through :

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/ >.

Capital Works deduction. 2019. [Online]. Available through :

<https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-allowances/capital-

work >.

7

Books and Journals

Aquilina, J., 2019, November. Reforming and realigning Division 855 of the Income Tax

Assessment Act 1997 to give better effect to its policy objectives. In Australian Tax

Forum (Vol. 34, No. 1).

McGregor-Lowndes, M. and Hannah, F.M., 2017. ACPNS Legal Case Notes Series: 2017-5

Glasby & Ors as Trustees Of The BCS Foundation v Attorney General of New South

Wales.

Loiacono, R. and Mortimer, C., 2017. Retrospective Tax Law: Has Pandora's Box Opened Never

to Be Shut Again. Ejtr. 15. p.105.

Hockridge, P., 2018. Alienation of income and. Tax Specialist. 22(1). p.30.

Hoppe, T., 2020. Tax Complexity in Australia–A Survey-Based Comparison to the OECD

Average.

Online

ITAA, 1997. 2019. [Online]. Available through :

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/ >.

Capital Works deduction. 2019. [Online]. Available through :

<https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-allowances/capital-

work >.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.