Assignment on Diploma in Business 2022

VerifiedAdded on 2022/02/28

|9

|3335

|28

Assignment

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

i

ASSIGNMENT 01 FRONT SHEET

Qualification BTEC Level 4 HND Diploma in Business

Unit number and title Unit 5: Accounting Principles

Submission date 08/02/2022 Date received (1st Submission)

Re-submission date Date received (2nd Submission)

Student Name Vu Dang Quang Huy Student ID GBH210803

Class No. GBH1013 Assessor Name Le Thi Yen Oanh

Student declaration

I certify that the assignment submission is entirely my own work and I fully understand the consequences of plagiarism.

I understand that making a false declaration is a form of malpractice.

Student Signature

Grading Grid

P1 P2 M1 D1

ASSIGNMENT 01 FRONT SHEET

Qualification BTEC Level 4 HND Diploma in Business

Unit number and title Unit 5: Accounting Principles

Submission date 08/02/2022 Date received (1st Submission)

Re-submission date Date received (2nd Submission)

Student Name Vu Dang Quang Huy Student ID GBH210803

Class No. GBH1013 Assessor Name Le Thi Yen Oanh

Student declaration

I certify that the assignment submission is entirely my own work and I fully understand the consequences of plagiarism.

I understand that making a false declaration is a form of malpractice.

Student Signature

Grading Grid

P1 P2 M1 D1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Summative Feedbacks Resubmission Feedbacks

Grade: Assessor Signature: Date:

Internal Verifier’s Comments:

Grade: Assessor Signature: Date:

Internal Verifier’s Comments:

Introduction

As a Graduate Trainee of PricewaterhouseCoopers Vietnam, this report will analyse the role of

accounting in an organisation and evaluate roles and responsibilities of the accounting function.

1. The accounting function in an organisation

Definition: Accounting is the process of recording financial transactions related to a company.

The accounting process that involves summarizing, analyzing, and reporting these transactions to

supervisors, regulators, and tax collectors (INVESTOPEDIA, n.d.).

Purpose of the accounting: According to Indeed Editorial Team (2021), all businesses use

accounting to report, track, execute, and forecast financial transactions. The main duties of

accountants are to store and analyze financial information and monitor monetary transactions.

Accounting is used to prepare financial statements for a company's employees, management, and

investors. Accountants also have the function of ensuring the payment of funds inside and

outside the company. Besides, the purpose of accounting is to gather and report financial

information about a company's performance, financial condition, and cash flows

(ACCOUNTINGTOOLS, 2021).

The main users of accounting information: According to Javed (2021), there are mainly two

types of users of accounting information

Internal users:

1. Management: uses accounting information to evaluate and analyze the financial

performance and financial position of the organization, in order to make important

decisions and take appropriate actions to improve the business performance.

profitability, financial position and cash flow.

2. Owners: the owners invests capital to establish and operate the business with the

primary goal of earning profit. They need accurate financial information to know

what they have gained or lost over a particular period of time. On the basis of

accounting information, they decide on future actions such as expansion or

contraction of the business

External users:

1. Lenders: are individuals or financial institutions that typically lend money to

businesses and earn interest income. They need accounting information to evaluate

both the financial performance and financial position of the business and have

reasonable assurance that the entity to which they are lending money will be able to

repay their principal. as well as paying interest on that money.

As a Graduate Trainee of PricewaterhouseCoopers Vietnam, this report will analyse the role of

accounting in an organisation and evaluate roles and responsibilities of the accounting function.

1. The accounting function in an organisation

Definition: Accounting is the process of recording financial transactions related to a company.

The accounting process that involves summarizing, analyzing, and reporting these transactions to

supervisors, regulators, and tax collectors (INVESTOPEDIA, n.d.).

Purpose of the accounting: According to Indeed Editorial Team (2021), all businesses use

accounting to report, track, execute, and forecast financial transactions. The main duties of

accountants are to store and analyze financial information and monitor monetary transactions.

Accounting is used to prepare financial statements for a company's employees, management, and

investors. Accountants also have the function of ensuring the payment of funds inside and

outside the company. Besides, the purpose of accounting is to gather and report financial

information about a company's performance, financial condition, and cash flows

(ACCOUNTINGTOOLS, 2021).

The main users of accounting information: According to Javed (2021), there are mainly two

types of users of accounting information

Internal users:

1. Management: uses accounting information to evaluate and analyze the financial

performance and financial position of the organization, in order to make important

decisions and take appropriate actions to improve the business performance.

profitability, financial position and cash flow.

2. Owners: the owners invests capital to establish and operate the business with the

primary goal of earning profit. They need accurate financial information to know

what they have gained or lost over a particular period of time. On the basis of

accounting information, they decide on future actions such as expansion or

contraction of the business

External users:

1. Lenders: are individuals or financial institutions that typically lend money to

businesses and earn interest income. They need accounting information to evaluate

both the financial performance and financial position of the business and have

reasonable assurance that the entity to which they are lending money will be able to

repay their principal. as well as paying interest on that money.

revenue, expenditure, profit of a business to satisfy their expectations and wants when

investing in a business.

- Organization: Accountants track income and expenditure, ensure regulatory compliance,

and provide investors, management and governments with quantitative financial

information that can be used to make business decisions. Besides, accounting helps

evaluate business performance, helps create budgets and future forecasts, helps prepare

financial statements (Woods, 2019). As a result, it helps businesses keep their business

running.

2. The context and purpose of financial and management accounting

The roles and importance of accounting as an information system:

According to Balignot (2020), accounting is an information system that provides stakeholders

with reports on the economic and state of the company. Financial transactions within the

company are handled through accounting. Accounting includes the process of identification, the

process of measurement and the process of reporting to produce financial statements. The

accounting information system collects data in the form of transactions occurring within the

company such as purchases, sales transactions, cash disbursements and cash receipts.

Accounting information within the company is needed by both internal parties and external

parties (Balignot, 2020). The purpose of an accounting information system is to collect, process

and report information related to the financial aspects of a company's business. Therefore,

accounting plays an essential role as an information system in business.

Financial accounting and management accounting in terms of purpose and scope:

Financial accounting:

- Purpose: is the original form of accounting that records business transactions and

aggregates data into reports, which are presented to users to make rationally financial

decisions. Financial accounting emphasizes giving a true and fair view of a

company's financial position to different parties (S, 2021).

- Scope: The scope of financial accounting includes recording transactions,

summarising information, analysing information, reporting information and

presenting it for both internal and external users (Financial Yard, n.d.).

Management accounting:

- Purpose: is a new field of accounting that studies management aspects. It involves

providing financial data to a company's management so that they can make sound

economic decisions (S, 2021). Furthermore, Management accounting assists

management in planning, directing, and controlling the functions and areas of

investing in a business.

- Organization: Accountants track income and expenditure, ensure regulatory compliance,

and provide investors, management and governments with quantitative financial

information that can be used to make business decisions. Besides, accounting helps

evaluate business performance, helps create budgets and future forecasts, helps prepare

financial statements (Woods, 2019). As a result, it helps businesses keep their business

running.

2. The context and purpose of financial and management accounting

The roles and importance of accounting as an information system:

According to Balignot (2020), accounting is an information system that provides stakeholders

with reports on the economic and state of the company. Financial transactions within the

company are handled through accounting. Accounting includes the process of identification, the

process of measurement and the process of reporting to produce financial statements. The

accounting information system collects data in the form of transactions occurring within the

company such as purchases, sales transactions, cash disbursements and cash receipts.

Accounting information within the company is needed by both internal parties and external

parties (Balignot, 2020). The purpose of an accounting information system is to collect, process

and report information related to the financial aspects of a company's business. Therefore,

accounting plays an essential role as an information system in business.

Financial accounting and management accounting in terms of purpose and scope:

Financial accounting:

- Purpose: is the original form of accounting that records business transactions and

aggregates data into reports, which are presented to users to make rationally financial

decisions. Financial accounting emphasizes giving a true and fair view of a

company's financial position to different parties (S, 2021).

- Scope: The scope of financial accounting includes recording transactions,

summarising information, analysing information, reporting information and

presenting it for both internal and external users (Financial Yard, n.d.).

Management accounting:

- Purpose: is a new field of accounting that studies management aspects. It involves

providing financial data to a company's management so that they can make sound

economic decisions (S, 2021). Furthermore, Management accounting assists

management in planning, directing, and controlling the functions and areas of

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

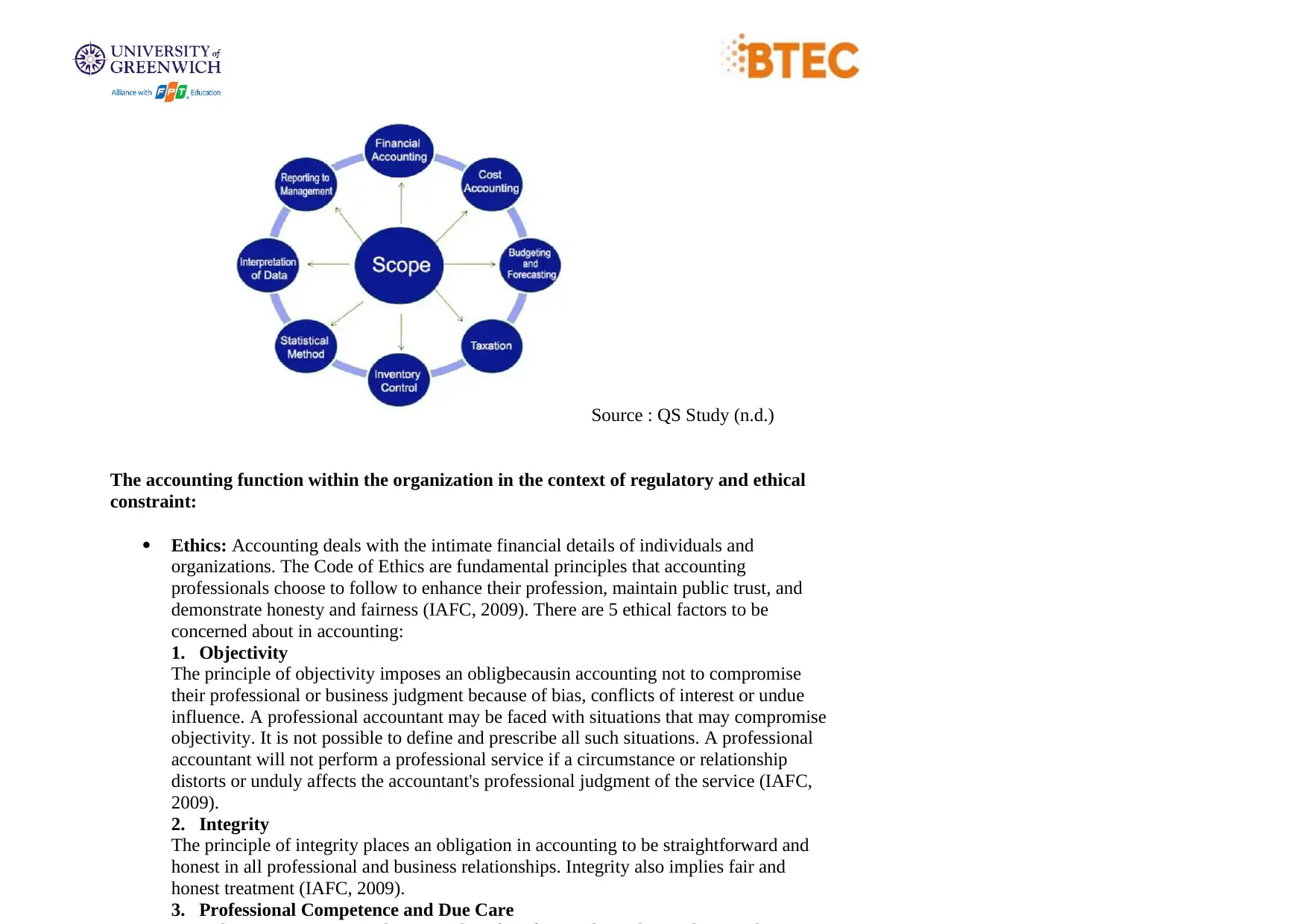

Source : QS Study (n.d.)

The accounting function within the organization in the context of regulatory and ethical

constraint:

Ethics: Accounting deals with the intimate financial details of individuals and

organizations. The Code of Ethics are fundamental principles that accounting

professionals choose to follow to enhance their profession, maintain public trust, and

demonstrate honesty and fairness (IAFC, 2009). There are 5 ethical factors to be

concerned about in accounting:

1. Objectivity

The principle of objectivity imposes an obligbecausin accounting not to compromise

their professional or business judgment because of bias, conflicts of interest or undue

influence. A professional accountant may be faced with situations that may compromise

objectivity. It is not possible to define and prescribe all such situations. A professional

accountant will not perform a professional service if a circumstance or relationship

distorts or unduly affects the accountant's professional judgment of the service (IAFC,

2009).

2. Integrity

The principle of integrity places an obligation in accounting to be straightforward and

honest in all professional and business relationships. Integrity also implies fair and

honest treatment (IAFC, 2009).

3. Professional Competence and Due Care

The accounting function within the organization in the context of regulatory and ethical

constraint:

Ethics: Accounting deals with the intimate financial details of individuals and

organizations. The Code of Ethics are fundamental principles that accounting

professionals choose to follow to enhance their profession, maintain public trust, and

demonstrate honesty and fairness (IAFC, 2009). There are 5 ethical factors to be

concerned about in accounting:

1. Objectivity

The principle of objectivity imposes an obligbecausin accounting not to compromise

their professional or business judgment because of bias, conflicts of interest or undue

influence. A professional accountant may be faced with situations that may compromise

objectivity. It is not possible to define and prescribe all such situations. A professional

accountant will not perform a professional service if a circumstance or relationship

distorts or unduly affects the accountant's professional judgment of the service (IAFC,

2009).

2. Integrity

The principle of integrity places an obligation in accounting to be straightforward and

honest in all professional and business relationships. Integrity also implies fair and

honest treatment (IAFC, 2009).

3. Professional Competence and Due Care

According to IAFC (2009), the Confidentiality Principle imposes an obligation in

accounting to refrain from:

(a) Disclosure to outside company or organization using confidential information

obtained as a result of professional and business relationships without appropriate and

specific authority or unless authorized or legal or professional obligation to disclose.

(b) Use confidential information obtained from professional and business relationships

for their own personal benefit or the benefit of third parties.

A professional accountant must maintain confidentiality, even in a social setting, alert to

the possibility of accidental disclosure, especially to a close business associate or a close

member or directly in the family. A professional accountant must also maintain the

confidentiality of information disclosed by a potential client or employer (IAFC, 2009).

5. Professional Behavior

The principle of professional behavior places an obligation in accounting to comply with

relevant laws and regulations and to avoid any action known or ought to be known by

professional accountants that could discredit the profession. This includes actions that a

reasonable and informed third party, taking into account all specific facts and

circumstances available to the professional accountant at that time, might conclude to

affect negatively for the reputation of the profession (IAFC, 2009).

Principles:

1. Cost

According to ACCOUNTINGTOOLS (2021), this is the concept that business should

only recognize assets, liabilities, and investments in equity at the original purchase price.

This principle is becoming less and less effective as a range of accounting standards are

geared towards adjusting assets and liabilities to their fair values.

2. Matching

The matching principle aims to adjust revenues and costs. Expenses must be recognized

in the period in which revenue is earned from them. In the same way, revenue must be

recognized in the period in which the costs incurred to earn them are recognised. The

matching principle is actually the result of applying the concept of accumulation

(ACCOUNTINGVERSE, n.d.).

3. Revenue Recognition

Revenue should be recognized on a company's income statement when it is earned. As a

result, a company will report some revenue on its income statement before customers

pay for goods or services they have received. In the case of cash sales, revenue will be

reported when the customer pays for their merchandise. If the customer pays in advance,

the revenue will be reported after receipt of the money (ACCOUNTINGCOACH, n.d.).

4. Full Disclosure

accounting to refrain from:

(a) Disclosure to outside company or organization using confidential information

obtained as a result of professional and business relationships without appropriate and

specific authority or unless authorized or legal or professional obligation to disclose.

(b) Use confidential information obtained from professional and business relationships

for their own personal benefit or the benefit of third parties.

A professional accountant must maintain confidentiality, even in a social setting, alert to

the possibility of accidental disclosure, especially to a close business associate or a close

member or directly in the family. A professional accountant must also maintain the

confidentiality of information disclosed by a potential client or employer (IAFC, 2009).

5. Professional Behavior

The principle of professional behavior places an obligation in accounting to comply with

relevant laws and regulations and to avoid any action known or ought to be known by

professional accountants that could discredit the profession. This includes actions that a

reasonable and informed third party, taking into account all specific facts and

circumstances available to the professional accountant at that time, might conclude to

affect negatively for the reputation of the profession (IAFC, 2009).

Principles:

1. Cost

According to ACCOUNTINGTOOLS (2021), this is the concept that business should

only recognize assets, liabilities, and investments in equity at the original purchase price.

This principle is becoming less and less effective as a range of accounting standards are

geared towards adjusting assets and liabilities to their fair values.

2. Matching

The matching principle aims to adjust revenues and costs. Expenses must be recognized

in the period in which revenue is earned from them. In the same way, revenue must be

recognized in the period in which the costs incurred to earn them are recognised. The

matching principle is actually the result of applying the concept of accumulation

(ACCOUNTINGVERSE, n.d.).

3. Revenue Recognition

Revenue should be recognized on a company's income statement when it is earned. As a

result, a company will report some revenue on its income statement before customers

pay for goods or services they have received. In the case of cash sales, revenue will be

reported when the customer pays for their merchandise. If the customer pays in advance,

the revenue will be reported after receipt of the money (ACCOUNTINGCOACH, n.d.).

4. Full Disclosure

significantly reduce the time it takes to close issue financial statements. It is helpful to

discuss with the company's auditors what constitutes a material item, so that there are no

problems with these items when the financial statements are audited

(ACCOUNTINGTOOLS, 2021).

2. Conservatism

The conservative principle is the general concept of recognizing expenses and liabilities

as soon as possible when the outcome is uncertain, but only recognizing revenues and

assets when they are guaranteed to be received. As a conservative rule, if they are

uncertain about incurring a loss, they should be inclined to record a loss. Conversely, if

they are uncertain about recording the gain, they should not record the gain

(ACCOUNTINGTOOLS, 2021).

Assumptions

1. Going-Concerns

The going concern principle is the assumption that an entity will continue in business for

the foreseeable future. On the contrary, this means that the entity will not be forced to

suspend operations and liquidate its assets in the near term at potentially very low prices.

By making this assumption, the accountant can delay the recognition of certain expenses

until a later period, when the entity is considered to be still in business and using its

assets efficiently possible (ACCOUNTINGTOOLS, 2021).

2. Monetary Unit

The monetary unit state that only record business transactions that can be expressed in a

currency. As a result, a company cannot record non-quantifiable items such as the skill

level of its employees, the quality of customer service, or the ingenuity of its technical

staff. The monetary unit principle also assumes that the value of the currency in which

transactions are recorded remains relatively stable over time (ACCOUNTINGTOOLS,

2021).

3. Business entity

The concept of a business entity stipulates that transactions involving a business must be

recorded separately from those of owners or other businesses. Doing so requires the use

of separate books of accounts for the organization, which completely excludes the assets

and liabilities of any other entity or of its owners. Without this concept, the records of

multiple entities would be mixed together, making it difficult to distinguish the financial

or taxable results of a business (ACCOUNTINGTOOLS, 2021).

4. Time Period

The time period principle is the concept that a business must report the financial results

of its activities over a standard period of time, usually monthly, quarterly, or annually.

Once the duration of each reporting period is established, use the guidelines of Generally

discuss with the company's auditors what constitutes a material item, so that there are no

problems with these items when the financial statements are audited

(ACCOUNTINGTOOLS, 2021).

2. Conservatism

The conservative principle is the general concept of recognizing expenses and liabilities

as soon as possible when the outcome is uncertain, but only recognizing revenues and

assets when they are guaranteed to be received. As a conservative rule, if they are

uncertain about incurring a loss, they should be inclined to record a loss. Conversely, if

they are uncertain about recording the gain, they should not record the gain

(ACCOUNTINGTOOLS, 2021).

Assumptions

1. Going-Concerns

The going concern principle is the assumption that an entity will continue in business for

the foreseeable future. On the contrary, this means that the entity will not be forced to

suspend operations and liquidate its assets in the near term at potentially very low prices.

By making this assumption, the accountant can delay the recognition of certain expenses

until a later period, when the entity is considered to be still in business and using its

assets efficiently possible (ACCOUNTINGTOOLS, 2021).

2. Monetary Unit

The monetary unit state that only record business transactions that can be expressed in a

currency. As a result, a company cannot record non-quantifiable items such as the skill

level of its employees, the quality of customer service, or the ingenuity of its technical

staff. The monetary unit principle also assumes that the value of the currency in which

transactions are recorded remains relatively stable over time (ACCOUNTINGTOOLS,

2021).

3. Business entity

The concept of a business entity stipulates that transactions involving a business must be

recorded separately from those of owners or other businesses. Doing so requires the use

of separate books of accounts for the organization, which completely excludes the assets

and liabilities of any other entity or of its owners. Without this concept, the records of

multiple entities would be mixed together, making it difficult to distinguish the financial

or taxable results of a business (ACCOUNTINGTOOLS, 2021).

4. Time Period

The time period principle is the concept that a business must report the financial results

of its activities over a standard period of time, usually monthly, quarterly, or annually.

Once the duration of each reporting period is established, use the guidelines of Generally

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

repreping financial data coming in and out of a business, allowing both company

managers and outside investors to understand a company's health and provide make

informed decisions.

Conclusion

This report explains the roles and purpose of accounting in an organization and the

concepts of accounting regulations and principles as well as ethics in accounting.

References

ACCOUNTINGCOACH, n.d. Introduction to Accounting Principles. [Online]

Available at: https://www.accountingcoach.com/accounting-principles/explanation

[Accessed 16 01 2022].

AccountingTools, 2021. Basic accounting principles. [Online]

Available at: https://www.accountingtools.com/articles/2017/5/15/basic-accounting-principles

[Accessed 16 01 2022].

ACCOUNTINGTOOLS, 2021. Business entity concept. [Online]

Available at: https://www.accountingtools.com/articles/what-is-the-business-entity-concept.html

[Accessed 17 01 2022].

ACCOUNTINGTOOLS, 2021. Conservatism principle definition. [Online]

Available at: https://www.accountingtools.com/articles/2017/5/14/the-conservatism-principle

[Accessed 17 01 2022].

ACCOUNTINGTOOLS, 2021. Materiality principle definition. [Online]

Available at: https://www.accountingtools.com/articles/2017/5/14/the-materiality-principle

[Accessed 17 01 2022].

ACCOUNTINGTOOLS, 2021. The going concern principle. [Online]

Available at: https://www.accountingtools.com/articles/2017/5/14/the-going-concern-principle

[Accessed 17 01 2022].

ACCOUNTINGTOOLS, 2021. The monetary unit principle. [Online]

Available at: https://www.accountingtools.com/articles/2017/5/15/the-monetary-unit-principle

[Accessed 17 01 2022].

ACCOUNTINGTOOLS, 2021. The purpose of accounting. [Online]

Available at: https://www.accountingtools.com/articles/what-is-the-purpose-of-accounting.html

[Accessed 14 01 2022].

ACCOUNTINGTOOLS, 2021. The time period principle. [Online]

Available at: https://www.accountingtools.com/articles/2017/5/15/the-time-period-

principle#:~:text=The%20time%20period%20principle%20is,monthly%2C%20quarterly%2C%

managers and outside investors to understand a company's health and provide make

informed decisions.

Conclusion

This report explains the roles and purpose of accounting in an organization and the

concepts of accounting regulations and principles as well as ethics in accounting.

References

ACCOUNTINGCOACH, n.d. Introduction to Accounting Principles. [Online]

Available at: https://www.accountingcoach.com/accounting-principles/explanation

[Accessed 16 01 2022].

AccountingTools, 2021. Basic accounting principles. [Online]

Available at: https://www.accountingtools.com/articles/2017/5/15/basic-accounting-principles

[Accessed 16 01 2022].

ACCOUNTINGTOOLS, 2021. Business entity concept. [Online]

Available at: https://www.accountingtools.com/articles/what-is-the-business-entity-concept.html

[Accessed 17 01 2022].

ACCOUNTINGTOOLS, 2021. Conservatism principle definition. [Online]

Available at: https://www.accountingtools.com/articles/2017/5/14/the-conservatism-principle

[Accessed 17 01 2022].

ACCOUNTINGTOOLS, 2021. Materiality principle definition. [Online]

Available at: https://www.accountingtools.com/articles/2017/5/14/the-materiality-principle

[Accessed 17 01 2022].

ACCOUNTINGTOOLS, 2021. The going concern principle. [Online]

Available at: https://www.accountingtools.com/articles/2017/5/14/the-going-concern-principle

[Accessed 17 01 2022].

ACCOUNTINGTOOLS, 2021. The monetary unit principle. [Online]

Available at: https://www.accountingtools.com/articles/2017/5/15/the-monetary-unit-principle

[Accessed 17 01 2022].

ACCOUNTINGTOOLS, 2021. The purpose of accounting. [Online]

Available at: https://www.accountingtools.com/articles/what-is-the-purpose-of-accounting.html

[Accessed 14 01 2022].

ACCOUNTINGTOOLS, 2021. The time period principle. [Online]

Available at: https://www.accountingtools.com/articles/2017/5/15/the-time-period-

principle#:~:text=The%20time%20period%20principle%20is,monthly%2C%20quarterly%2C%

Financial Yard, n.d. The Scope Of Financial Accounting. [Online]

Available at: https://financialyard.com/scope-of-financial-accounting/

[Accessed 15 01 2022].

IAFC, 2009. Code of Ethics for Professional. [Online]

Available at: https://www.ifac.org/system/files/publications/files/Code-of-

Ethics_July_2009_FINAL_02_23_10.pdf

[Accessed 16 01 2022].

Indeed Editorial Team, 2021. What Are the Functions of Accounting?. [Online]

Available at: https://www.indeed.com/career-advice/career-development/functions-of-

accounting

[Accessed 14 01 2022].

INVESTOPEDIA, n.d. Accounting. [Online]

Available at: https://www.investopedia.com/terms/a/accounting.asp

[Accessed 14 01 2021].

Javed, R., 2021. Users of accounting information. [Online]

Available at: https://www.accountingformanagement.org/users-of-accounting-information/

[Accessed 14 01 2022].

Kotler, 2012. Principles of Marketing, 14th edition. New York: Prentice Hall.

Kotler, P., Armstrong, G., Wong, V. & Saunders, J., 2008. Principles of Marketing - Fifth

European Edition. Essex: Prentice Hall.

QS Study, n.d. Scope of Management Accounting. [Online]

Available at: https://qsstudy.com/scope-field-management-accounting/

[Accessed 15 01 2022].

S, S., 2021. Difference Between Financial Accounting and Management Accounting. [Online]

Available at: https://keydifferences.com/difference-between-financial-accounting-and-

management-accounting.html

[Accessed 15 01 2022].

Woods, D., 2019. The Role of Accounting in Business and Why It’s Important. [Online]

Available at: https://www.pdr-cpa.com/knowledge-center/blog/role-of-accounting-in-

business#:~:text=Accounting%20plays%20a%20vital%20role,used%20in%20making%20busine

ss%20decisions.

[Accessed 17 01 2022].

Available at: https://financialyard.com/scope-of-financial-accounting/

[Accessed 15 01 2022].

IAFC, 2009. Code of Ethics for Professional. [Online]

Available at: https://www.ifac.org/system/files/publications/files/Code-of-

Ethics_July_2009_FINAL_02_23_10.pdf

[Accessed 16 01 2022].

Indeed Editorial Team, 2021. What Are the Functions of Accounting?. [Online]

Available at: https://www.indeed.com/career-advice/career-development/functions-of-

accounting

[Accessed 14 01 2022].

INVESTOPEDIA, n.d. Accounting. [Online]

Available at: https://www.investopedia.com/terms/a/accounting.asp

[Accessed 14 01 2021].

Javed, R., 2021. Users of accounting information. [Online]

Available at: https://www.accountingformanagement.org/users-of-accounting-information/

[Accessed 14 01 2022].

Kotler, 2012. Principles of Marketing, 14th edition. New York: Prentice Hall.

Kotler, P., Armstrong, G., Wong, V. & Saunders, J., 2008. Principles of Marketing - Fifth

European Edition. Essex: Prentice Hall.

QS Study, n.d. Scope of Management Accounting. [Online]

Available at: https://qsstudy.com/scope-field-management-accounting/

[Accessed 15 01 2022].

S, S., 2021. Difference Between Financial Accounting and Management Accounting. [Online]

Available at: https://keydifferences.com/difference-between-financial-accounting-and-

management-accounting.html

[Accessed 15 01 2022].

Woods, D., 2019. The Role of Accounting in Business and Why It’s Important. [Online]

Available at: https://www.pdr-cpa.com/knowledge-center/blog/role-of-accounting-in-

business#:~:text=Accounting%20plays%20a%20vital%20role,used%20in%20making%20busine

ss%20decisions.

[Accessed 17 01 2022].

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.