ACC00712 Essay: Qualitative Characteristics of Accounting Info

VerifiedAdded on 2023/03/23

|10

|2320

|71

Essay

AI Summary

This essay discusses the concept of revaluation with regard to Telstra's land and highlights the qualitative characteristics of financial information, including understandability, comparability, relevance, and faithful representation, based on the Australian Accounting Standards Board (AASB) framework. It analyzes the annual report of Abacus Property Group, identifying key fundamental characteristics such as understandability, comparability, faithful representation, reliability, and relevance. The essay also explores the reaction of investors and the security market to company disclosures, particularly concerning earnings and share prices, and concludes that good accounting information must possess these characteristics to achieve its intended goals. Desklib provides a platform for students to access similar solved assignments and past papers.

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 1

STUDENT NAME:

STUDENT ID NO.:

UNIT NAME:

UNIT CODE:

TUTOR’S NAME:

ASSIGNMENT

NO.:

ASSIGNMENT

TITLE:

DUE DATE:

DATE

SUBMITTED:

Declaration:

I have read and understand the Rules Relating to Awards (Rule 3 Section 18 –

Academic Misconduct Including Plagiarism) as contained in the SCU Policy

Library. I understand the penalties that apply for plagiarism and agree to be bound

by these rules. The work I am submitting electronically is entirely my own work.

Signed:

(name)

Date:

STUDENT NAME:

STUDENT ID NO.:

UNIT NAME:

UNIT CODE:

TUTOR’S NAME:

ASSIGNMENT

NO.:

ASSIGNMENT

TITLE:

DUE DATE:

DATE

SUBMITTED:

Declaration:

I have read and understand the Rules Relating to Awards (Rule 3 Section 18 –

Academic Misconduct Including Plagiarism) as contained in the SCU Policy

Library. I understand the penalties that apply for plagiarism and agree to be bound

by these rules. The work I am submitting electronically is entirely my own work.

Signed:

(name)

Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 2

EXECUTIVE SUMMARY

The purpose of this essay is to discuss the concept of revaluation in regard to the Telstra’s land

which was revalued. The essay also highlights the qualitative characteristics of financial

information and discusses the understandability, comparability, relevance and faithful

representation.it also identify key fundamental characteristics in the annual report of Abacus

property group.

EXECUTIVE SUMMARY

The purpose of this essay is to discuss the concept of revaluation in regard to the Telstra’s land

which was revalued. The essay also highlights the qualitative characteristics of financial

information and discusses the understandability, comparability, relevance and faithful

representation.it also identify key fundamental characteristics in the annual report of Abacus

property group.

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 3

Table of Contents

1.0 PART 1...................................................................................................................................................4

1.1 INTRODUCTION.................................................................................................................................4

1.2 REVALUATION....................................................................................................................................4

2.0 PART 2...................................................................................................................................................4

2.1 AUSTRALIAN ACCOUNTING STANDARDS BOARD (AASB)...................................................................4

2.2 QUALITATIVE CHARACTERISTICS OF FINANCIAL INFORMATION........................................................5

2.2.1UNDERSTANDABILITY..................................................................................................................5

2.2.2 RELEVANCE.................................................................................................................................5

2.2.3 COMPAREABILITY.......................................................................................................................5

2.2.4 RELIABILITY.................................................................................................................................6

2.2.5 FAITHFUL REPRESENTATION.......................................................................................................6

2.3 PRUDENCE CONCEPT.............................................................................................................................6

3.0 PART 3...................................................................................................................................................7

3.1 ABACUS PROPERTY GROUP ANNUAL 2017/2018 ANNUAL REPORT FEATURES.................................7

3.1.1 UNDERSTANDABILITY.................................................................................................................7

3.1.2 COMPAREABILITY.......................................................................................................................7

3.1.3 FAITHFUL REPRESENTATION.......................................................................................................8

3.1.4 RELIABILITY.................................................................................................................................8

3.1.5 RELEVANCE.................................................................................................................................8

3.2 PRUDENCE CONCEPT.........................................................................................................................8

4.0 PART 4...................................................................................................................................................9

4.1 REACTION OF INVESTORS AND SECURITY MARKET...........................................................................9

5.1 CONCLUSION.........................................................................................................................................9

6.0 REFERENCES........................................................................................................................................10

7.0 APPENDICES.........................................................................................................................................12

7.1 APPENDIX I: ABACUS 2017 TOTAL ASSETS.......................................................................................12

7.2 APPENDIX II: ABACUS 2018 TOTAL ASSETS......................................................................................12

Table of Contents

1.0 PART 1...................................................................................................................................................4

1.1 INTRODUCTION.................................................................................................................................4

1.2 REVALUATION....................................................................................................................................4

2.0 PART 2...................................................................................................................................................4

2.1 AUSTRALIAN ACCOUNTING STANDARDS BOARD (AASB)...................................................................4

2.2 QUALITATIVE CHARACTERISTICS OF FINANCIAL INFORMATION........................................................5

2.2.1UNDERSTANDABILITY..................................................................................................................5

2.2.2 RELEVANCE.................................................................................................................................5

2.2.3 COMPAREABILITY.......................................................................................................................5

2.2.4 RELIABILITY.................................................................................................................................6

2.2.5 FAITHFUL REPRESENTATION.......................................................................................................6

2.3 PRUDENCE CONCEPT.............................................................................................................................6

3.0 PART 3...................................................................................................................................................7

3.1 ABACUS PROPERTY GROUP ANNUAL 2017/2018 ANNUAL REPORT FEATURES.................................7

3.1.1 UNDERSTANDABILITY.................................................................................................................7

3.1.2 COMPAREABILITY.......................................................................................................................7

3.1.3 FAITHFUL REPRESENTATION.......................................................................................................8

3.1.4 RELIABILITY.................................................................................................................................8

3.1.5 RELEVANCE.................................................................................................................................8

3.2 PRUDENCE CONCEPT.........................................................................................................................8

4.0 PART 4...................................................................................................................................................9

4.1 REACTION OF INVESTORS AND SECURITY MARKET...........................................................................9

5.1 CONCLUSION.........................................................................................................................................9

6.0 REFERENCES........................................................................................................................................10

7.0 APPENDICES.........................................................................................................................................12

7.1 APPENDIX I: ABACUS 2017 TOTAL ASSETS.......................................................................................12

7.2 APPENDIX II: ABACUS 2018 TOTAL ASSETS......................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 4

1.0 PART 1.

1.1 INTRODUCTION

Abacus property group is a diversified group that carries out its operations majorly in Australia.

Its securities are traded in the Australian security exchange.it was listed in the security exchange

in November 2002 and its total market capital base was $2.4 billion at 30th June 2017 and $2.7

billion as at 30th June 2018.its main business is the investment property. They acquire property

assets and making sure that this asset is effectively managed to generate more returns and grow.

1.2 REVALUATION

It is right for the accountants of Telstra to revalue land since the market values of fixed assets

like land keeps on changing from time to time due to appreciation in their values AASB QC5.

This asset should therefore be revalued each year by various accountants of various companies

so as to ascertain their true book values as at that period. Revaluation of these assets will assist

the company to establish their true asset base based on the true carrying amount of asset

revalued. This concept of revaluation is in line with AASB paragraph 81 on revaluation and

restatement of asset. Revaluing land means presenting true information in the financial statement

and therefore it is in line with faithful representation under AASB QC12-QC16.

2.0 PART 2.

2.1 AUSTRALIAN ACCOUNTING STANDARDS BOARD (AASB).

The Australian accounting standards board(AASB) is enforcing the standards of international

accounting standards board (IASB) for reporting and presentation of the accounting information.

Some sections of the current Australian conceptual framework contain some qualitative

characteristics of financial information, definition and recognition of some items in the financial

statements (Wagenhofer, 2009, pg. 76). To differentiate Australian framework from the

international framework, prefix “Aus” is used followed by the number of IASB paragraph and

the decimal.

2.2 QUALITATIVE CHARACTERISTICS OF FINANCIAL INFORMATION

2.2.1UNDERSTANDABILITY

Understandability is an essential feature of an accounting information as it should be prepared

bearing in mind the needs of the users as per the requirement of AASB paragraph QC30 – QC32.

They should be prepared in the most understandable manner and in a way that can be easily

comprehended by the users of such information.in this feature, users of the accounting

1.0 PART 1.

1.1 INTRODUCTION

Abacus property group is a diversified group that carries out its operations majorly in Australia.

Its securities are traded in the Australian security exchange.it was listed in the security exchange

in November 2002 and its total market capital base was $2.4 billion at 30th June 2017 and $2.7

billion as at 30th June 2018.its main business is the investment property. They acquire property

assets and making sure that this asset is effectively managed to generate more returns and grow.

1.2 REVALUATION

It is right for the accountants of Telstra to revalue land since the market values of fixed assets

like land keeps on changing from time to time due to appreciation in their values AASB QC5.

This asset should therefore be revalued each year by various accountants of various companies

so as to ascertain their true book values as at that period. Revaluation of these assets will assist

the company to establish their true asset base based on the true carrying amount of asset

revalued. This concept of revaluation is in line with AASB paragraph 81 on revaluation and

restatement of asset. Revaluing land means presenting true information in the financial statement

and therefore it is in line with faithful representation under AASB QC12-QC16.

2.0 PART 2.

2.1 AUSTRALIAN ACCOUNTING STANDARDS BOARD (AASB).

The Australian accounting standards board(AASB) is enforcing the standards of international

accounting standards board (IASB) for reporting and presentation of the accounting information.

Some sections of the current Australian conceptual framework contain some qualitative

characteristics of financial information, definition and recognition of some items in the financial

statements (Wagenhofer, 2009, pg. 76). To differentiate Australian framework from the

international framework, prefix “Aus” is used followed by the number of IASB paragraph and

the decimal.

2.2 QUALITATIVE CHARACTERISTICS OF FINANCIAL INFORMATION

2.2.1UNDERSTANDABILITY

Understandability is an essential feature of an accounting information as it should be prepared

bearing in mind the needs of the users as per the requirement of AASB paragraph QC30 – QC32.

They should be prepared in the most understandable manner and in a way that can be easily

comprehended by the users of such information.in this feature, users of the accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 5

information are assumed to possess some skills to read and understand well the accounting

reports and obtain relevant information suitable to their needs.

2.2.2 RELEVANCE

Relevance of the accounting information simply means that the accounting information

presented in the annual reports of the company should be useful to the decision making process

of the intended users of such information. This same function of the information plays a key role

in projection of the future concerning the way that the company can structure itself or the results

of its budgeted program (AASB paragraph QC5 – QC10). The information concerning the state of

the company at a particular point in time and its previous performance is used to project the

future position of the company and other users need like dividend payout ratio, salaries and

wages, share prices and the company’s solvency state.

2.2.3 COMPAREABILITY

Comparability means that the accounting information presentation should be in form that can be

easily compared with the statements of the same firm in the same industry. It also means that,

users of the information should be able to make comparisons of the company’s performance

from one year to the next and identify some changes and trends in such reports. Therefore, this

quality needs preparers of financial statements to present financial reports of the same nature and

effect in the same and consistent manner for the company and different entities (AASB paragraphs

QC20 – QC25).

2.2.4 RELIABILITY

Reliability of an accounting information means that the information contained in the statements

does not contain errors and biasness and can be utilized by various users to provide key

information that they need from them.an accounting information may be relevant but not reliable

or its recognition may be misleading (Shortridge & Smith, 2009, pg. 11). For instance, the value

of the claim for damages which is under a legal action may be disputed and therefore it will not

be in order for the company to recognize this value in its full amount in the statement of financial

position as it will portray a wrong information to the users.

2.2.5 FAITHFUL REPRESENTATION

Faithfull representation of accounting information means that the financial information should

represent transaction events faithfully according to AASB QC12-QC16. For instance, the

statement of financial position should represent faithfully the elements such as assets, liabilities

information are assumed to possess some skills to read and understand well the accounting

reports and obtain relevant information suitable to their needs.

2.2.2 RELEVANCE

Relevance of the accounting information simply means that the accounting information

presented in the annual reports of the company should be useful to the decision making process

of the intended users of such information. This same function of the information plays a key role

in projection of the future concerning the way that the company can structure itself or the results

of its budgeted program (AASB paragraph QC5 – QC10). The information concerning the state of

the company at a particular point in time and its previous performance is used to project the

future position of the company and other users need like dividend payout ratio, salaries and

wages, share prices and the company’s solvency state.

2.2.3 COMPAREABILITY

Comparability means that the accounting information presentation should be in form that can be

easily compared with the statements of the same firm in the same industry. It also means that,

users of the information should be able to make comparisons of the company’s performance

from one year to the next and identify some changes and trends in such reports. Therefore, this

quality needs preparers of financial statements to present financial reports of the same nature and

effect in the same and consistent manner for the company and different entities (AASB paragraphs

QC20 – QC25).

2.2.4 RELIABILITY

Reliability of an accounting information means that the information contained in the statements

does not contain errors and biasness and can be utilized by various users to provide key

information that they need from them.an accounting information may be relevant but not reliable

or its recognition may be misleading (Shortridge & Smith, 2009, pg. 11). For instance, the value

of the claim for damages which is under a legal action may be disputed and therefore it will not

be in order for the company to recognize this value in its full amount in the statement of financial

position as it will portray a wrong information to the users.

2.2.5 FAITHFUL REPRESENTATION

Faithfull representation of accounting information means that the financial information should

represent transaction events faithfully according to AASB QC12-QC16. For instance, the

statement of financial position should represent faithfully the elements such as assets, liabilities

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 6

and equity of the company as at the reporting period and should meet the criteria set to be used in

the recognition. It is advisable that the companies should recognize elements of the financial

statement and provide necessary disclosures concerning the risks of possible errors around such

recognition.

3.0 PART 3

3.1 ABACUS PROPERTY GROUP ANNUAL 2017/2018 ANNUAL REPORT

FEATURES

3.1.1 UNDERSTANDABILITY

Fundamental qualitative characteristics of a good accounting information has been portrayed in

various aspects of the 2017 and 2018 annual reports of abacus property group. Understandability

feature has been clearly demonstrated since the annual reports of this company can be easily read

and understood by the user (AASB paragraphs QC30 – QC32).it display all elements of the

financial statement in a logical and easy to read manner. For instance, the income statement of

abacus property group clearly lists all the revenues and expenses in a very clear manner.

Common user of this information will be able to know that the group made a net profit after tax

of $292088000 and $246958000 in 2017 and 2018 respectively. The user can therefore make

appropriate decision based on this understanding. Abacus group comprise of AGHL, AT, AGPL,

AIT, ASPT and ASOL group which jointly form abacus property group. The statement of

comprehensive income has clearly lists various incomes that are attributable to each group. This

enhances the understandability of this information who want to know the income of each group

(Kirschenheiter &Ramakrishna, 2010).

3.1.2 COMPAREABILITY

Comparability feature is clearly portrayed in these annual reports as they relate to the same

period of time, that is 30th June of 2017 and 2018.this will enhance the comparison of various

elements of the reports that relate to the same period of time. The income statement also gives a

net profit after tax of $292088000 and $246958000 in 2017 and 2018 respectively. The user will

therefore be able to do simple comparisons of these two profits and make relevant investment

decision regarding to the company. Comparison on various incomes of a particular group for

each year can be clearly drawn from the statement of comprehensive income since the statement

list the income for each particular group. The annual report of abacus group is easily comparable

across years (Cascino & Gassen, 2010).

and equity of the company as at the reporting period and should meet the criteria set to be used in

the recognition. It is advisable that the companies should recognize elements of the financial

statement and provide necessary disclosures concerning the risks of possible errors around such

recognition.

3.0 PART 3

3.1 ABACUS PROPERTY GROUP ANNUAL 2017/2018 ANNUAL REPORT

FEATURES

3.1.1 UNDERSTANDABILITY

Fundamental qualitative characteristics of a good accounting information has been portrayed in

various aspects of the 2017 and 2018 annual reports of abacus property group. Understandability

feature has been clearly demonstrated since the annual reports of this company can be easily read

and understood by the user (AASB paragraphs QC30 – QC32).it display all elements of the

financial statement in a logical and easy to read manner. For instance, the income statement of

abacus property group clearly lists all the revenues and expenses in a very clear manner.

Common user of this information will be able to know that the group made a net profit after tax

of $292088000 and $246958000 in 2017 and 2018 respectively. The user can therefore make

appropriate decision based on this understanding. Abacus group comprise of AGHL, AT, AGPL,

AIT, ASPT and ASOL group which jointly form abacus property group. The statement of

comprehensive income has clearly lists various incomes that are attributable to each group. This

enhances the understandability of this information who want to know the income of each group

(Kirschenheiter &Ramakrishna, 2010).

3.1.2 COMPAREABILITY

Comparability feature is clearly portrayed in these annual reports as they relate to the same

period of time, that is 30th June of 2017 and 2018.this will enhance the comparison of various

elements of the reports that relate to the same period of time. The income statement also gives a

net profit after tax of $292088000 and $246958000 in 2017 and 2018 respectively. The user will

therefore be able to do simple comparisons of these two profits and make relevant investment

decision regarding to the company. Comparison on various incomes of a particular group for

each year can be clearly drawn from the statement of comprehensive income since the statement

list the income for each particular group. The annual report of abacus group is easily comparable

across years (Cascino & Gassen, 2010).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 7

3.1.3 FAITHFUL REPRESENTATION

Quality of faithful representation has been clearly shown in the way the group has disclosed

various significant estimates and judgments with regard to treatment of accounting elements.it

has been disclosed that the financial asset is treated at the fair value through the profit and loss

on recognition (pg.42 of the 2018 annual report).

3.1.4 RELIABILITY

Reliability quality is shown in pg. 49 where the group has adequately shown the amount of total

facility loan and the unused amount at the reporting date. This information will assist the user of

this information in making key decision regarding the investment in the group.

3.1.5 RELEVANCE

Relevance quality has been clearly shown since the group has provided key financial information

consistently from year to year. This information will assist the user to judge and draw relevant

conclusion regarding the groups viability. Total equity has been shown to be $ 1,916,702,000

and $ 1,814,621,000 in 2018 and 2017 respectively. This can help the user project the total

equity for 2019 since it is shown to be on an upward trajectory.it is in line with AASB paragraph

QC6 – QC10

4.0 PART 4.

4.1 REACTION OF INVESTORS AND SECURITY MARKET

The security market will react to various disclosures regarding the company’s announcements on

their earnings. This is an announcement on the company’s performance and profitability levels

for a particular period. For the case of abacus group, it reported its performance annually of a

profit of $292088000 and $246958000 in 2017 and 2018 respectively. Profitability of the

company is shown in the income statement while the earnings are supposed to be adequately

announced for a company that is listed in the security market. This is in line with the quality of

relevance with regard to the predictability of the company’s performance.in the financial

statement of abacus property group pg.27, it is clearly shown that Basic and diluted earnings per

stapled security (cents) were 42.18 and 49.91 in 2018 and 2017 consecutively. This will make

and investor to know that the value decline in 2018 by 7.73. The information disclosed will make

the investors judge the possible levels of dividend expected from the company.

3.1.3 FAITHFUL REPRESENTATION

Quality of faithful representation has been clearly shown in the way the group has disclosed

various significant estimates and judgments with regard to treatment of accounting elements.it

has been disclosed that the financial asset is treated at the fair value through the profit and loss

on recognition (pg.42 of the 2018 annual report).

3.1.4 RELIABILITY

Reliability quality is shown in pg. 49 where the group has adequately shown the amount of total

facility loan and the unused amount at the reporting date. This information will assist the user of

this information in making key decision regarding the investment in the group.

3.1.5 RELEVANCE

Relevance quality has been clearly shown since the group has provided key financial information

consistently from year to year. This information will assist the user to judge and draw relevant

conclusion regarding the groups viability. Total equity has been shown to be $ 1,916,702,000

and $ 1,814,621,000 in 2018 and 2017 respectively. This can help the user project the total

equity for 2019 since it is shown to be on an upward trajectory.it is in line with AASB paragraph

QC6 – QC10

4.0 PART 4.

4.1 REACTION OF INVESTORS AND SECURITY MARKET

The security market will react to various disclosures regarding the company’s announcements on

their earnings. This is an announcement on the company’s performance and profitability levels

for a particular period. For the case of abacus group, it reported its performance annually of a

profit of $292088000 and $246958000 in 2017 and 2018 respectively. Profitability of the

company is shown in the income statement while the earnings are supposed to be adequately

announced for a company that is listed in the security market. This is in line with the quality of

relevance with regard to the predictability of the company’s performance.in the financial

statement of abacus property group pg.27, it is clearly shown that Basic and diluted earnings per

stapled security (cents) were 42.18 and 49.91 in 2018 and 2017 consecutively. This will make

and investor to know that the value decline in 2018 by 7.73. The information disclosed will make

the investors judge the possible levels of dividend expected from the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 8

According to Cready and Gurun (2010), lower earning will will move market values higher and

Hussin et al. (2010) found out that low earnings of a company will leads to negative market

reaction. On disclosure of share price of the company, stock prices will will react positively or

negatively depending on the announcement.

5.1 CONCLUSION

In conclusion, good accounting information must contain the above characteristics for it to

achieve its intended goals so directed. Investors need to know the overall profitability of the

company while the security market would want to know the shares declared by the entity. All

these should be well covered if a financial report has all the necessary qualities of a good report.

6.0 REFERENCES.

AASB FRAMEWORK <https://www.aasb.gov.au/admin/file/content105/c9/Framework_07-

04_COMPjun14_07-14.pdf>

According to Cready and Gurun (2010), lower earning will will move market values higher and

Hussin et al. (2010) found out that low earnings of a company will leads to negative market

reaction. On disclosure of share price of the company, stock prices will will react positively or

negatively depending on the announcement.

5.1 CONCLUSION

In conclusion, good accounting information must contain the above characteristics for it to

achieve its intended goals so directed. Investors need to know the overall profitability of the

company while the security market would want to know the shares declared by the entity. All

these should be well covered if a financial report has all the necessary qualities of a good report.

6.0 REFERENCES.

AASB FRAMEWORK <https://www.aasb.gov.au/admin/file/content105/c9/Framework_07-

04_COMPjun14_07-14.pdf>

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 9

Abacus property group annual reports < http://www.annualreports.com/Company/abacus-

property-group>

Cascino, S. and Gassen, J., 2010. Mandatory IFRS adoption and accounting comparability (No.

2010-046). SFB 649 discussion paper.

Kirschenheiter, M. and Ramakrishnan, R.T., 2010, September. Prudence demands conservatism.

AAA.

Shortridge, R.T. and Smith, P.A., 2009. Understanding the changes in accounting

thought. Research in accounting regulation, 21(1), pp.11-18.

Wagenhofer, A., 2009. Global accounting standards: reality and ambitions. Accounting Research

Journal, 22(1), pp.68-80.

Abacus property group annual reports < http://www.annualreports.com/Company/abacus-

property-group>

Cascino, S. and Gassen, J., 2010. Mandatory IFRS adoption and accounting comparability (No.

2010-046). SFB 649 discussion paper.

Kirschenheiter, M. and Ramakrishnan, R.T., 2010, September. Prudence demands conservatism.

AAA.

Shortridge, R.T. and Smith, P.A., 2009. Understanding the changes in accounting

thought. Research in accounting regulation, 21(1), pp.11-18.

Wagenhofer, A., 2009. Global accounting standards: reality and ambitions. Accounting Research

Journal, 22(1), pp.68-80.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION 10

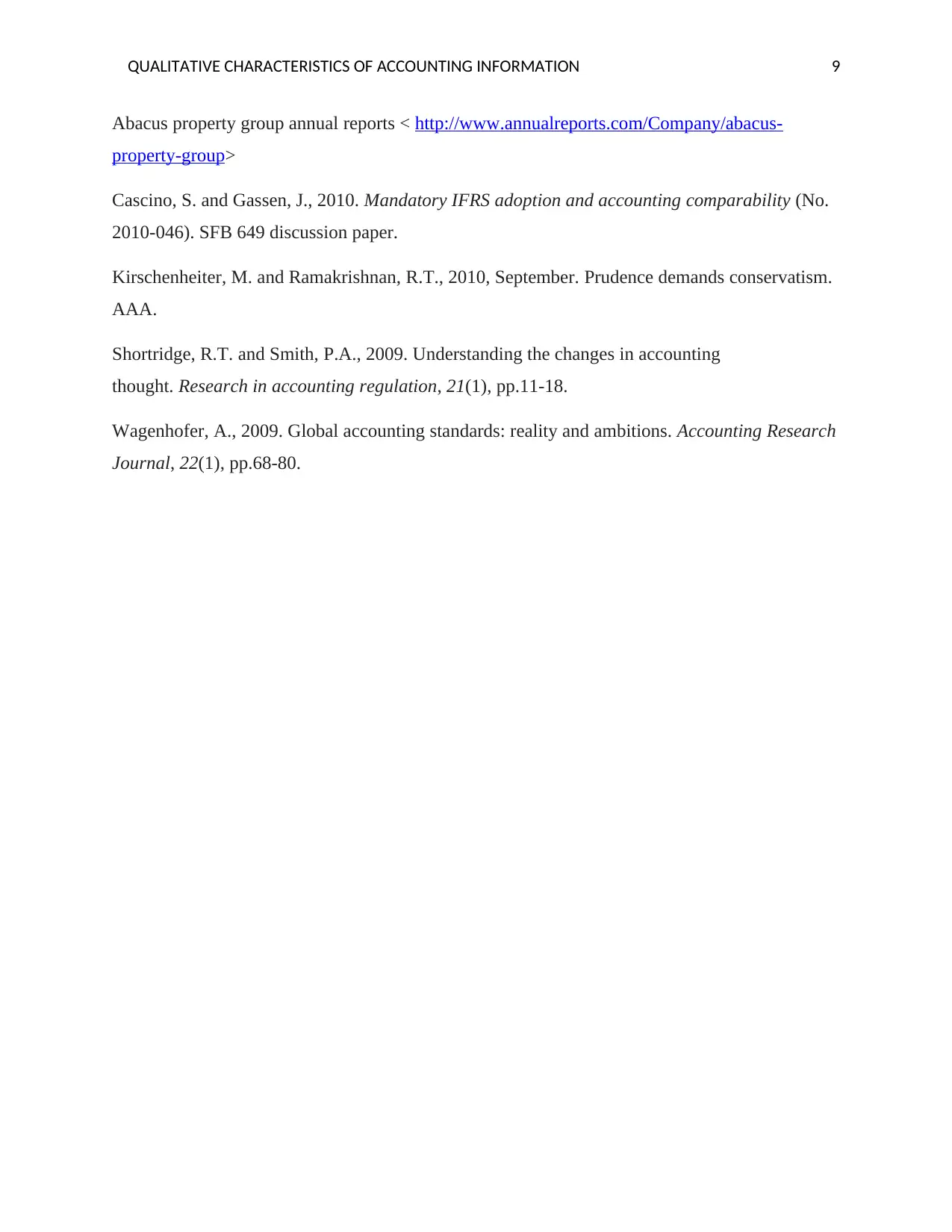

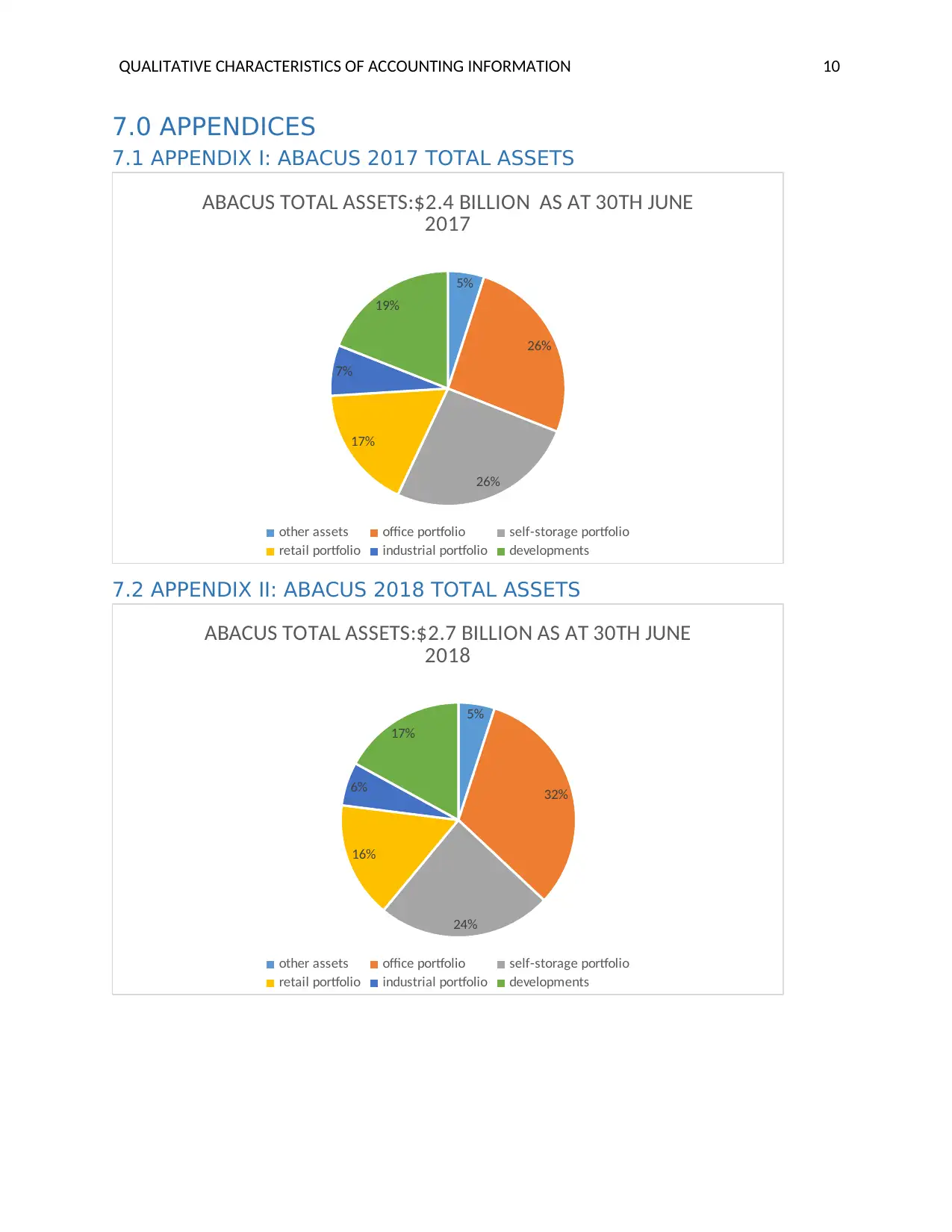

7.0 APPENDICES

7.1 APPENDIX I: ABACUS 2017 TOTAL ASSETS

5%

26%

26%

17%

7%

19%

ABACUS TOTAL ASSETS:$2.4 BILLION AS AT 30TH JUNE

2017

other assets office portfolio self-storage portfolio

retail portfolio industrial portfolio developments

7.2 APPENDIX II: ABACUS 2018 TOTAL ASSETS

5%

32%

24%

16%

6%

17%

ABACUS TOTAL ASSETS:$2.7 BILLION AS AT 30TH JUNE

2018

other assets office portfolio self-storage portfolio

retail portfolio industrial portfolio developments

7.0 APPENDICES

7.1 APPENDIX I: ABACUS 2017 TOTAL ASSETS

5%

26%

26%

17%

7%

19%

ABACUS TOTAL ASSETS:$2.4 BILLION AS AT 30TH JUNE

2017

other assets office portfolio self-storage portfolio

retail portfolio industrial portfolio developments

7.2 APPENDIX II: ABACUS 2018 TOTAL ASSETS

5%

32%

24%

16%

6%

17%

ABACUS TOTAL ASSETS:$2.7 BILLION AS AT 30TH JUNE

2018

other assets office portfolio self-storage portfolio

retail portfolio industrial portfolio developments

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.