Accounting Report: ASIC Role, Wesfarmers Impairment and Compliance

VerifiedAdded on 2021/05/31

|11

|1795

|121

Report

AI Summary

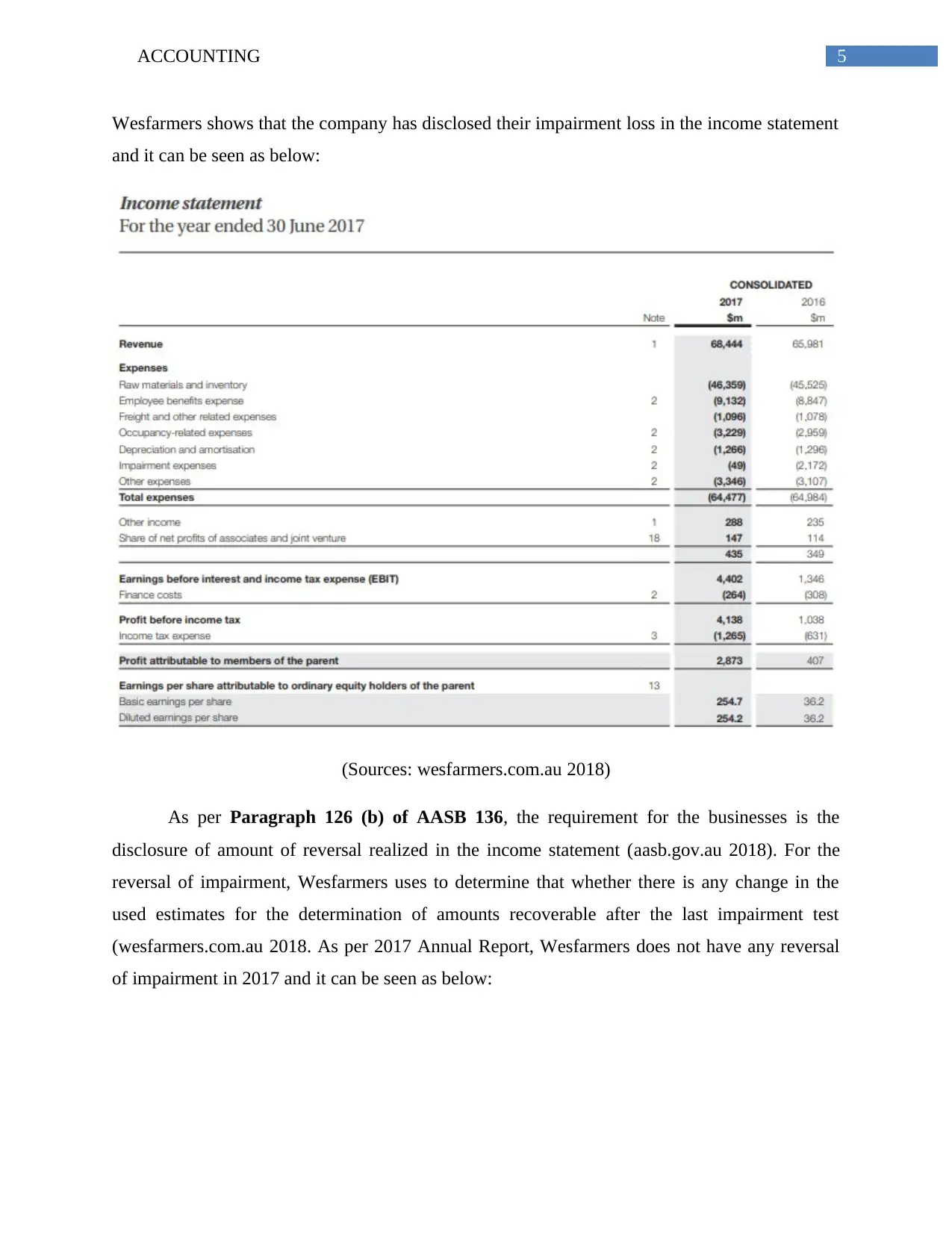

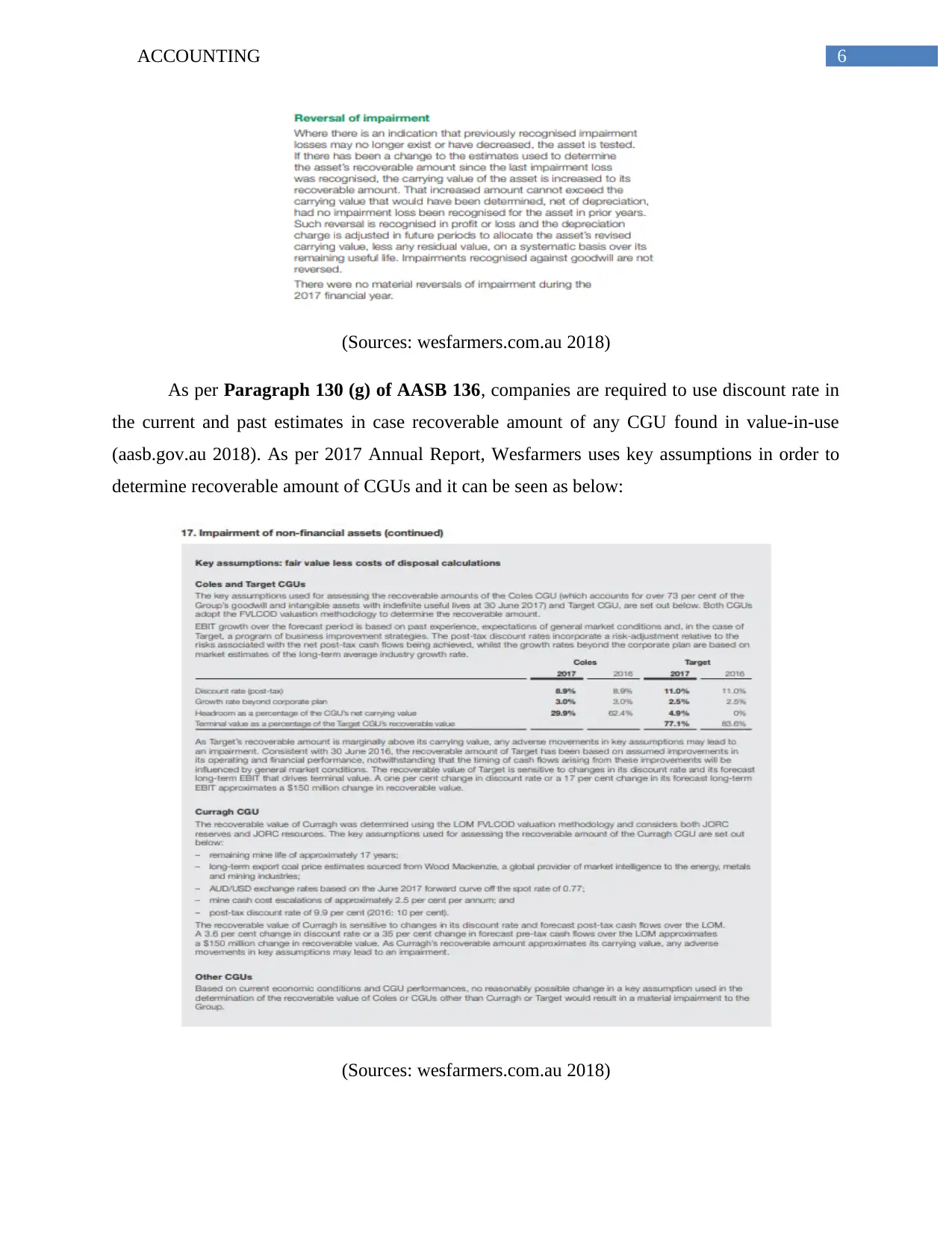

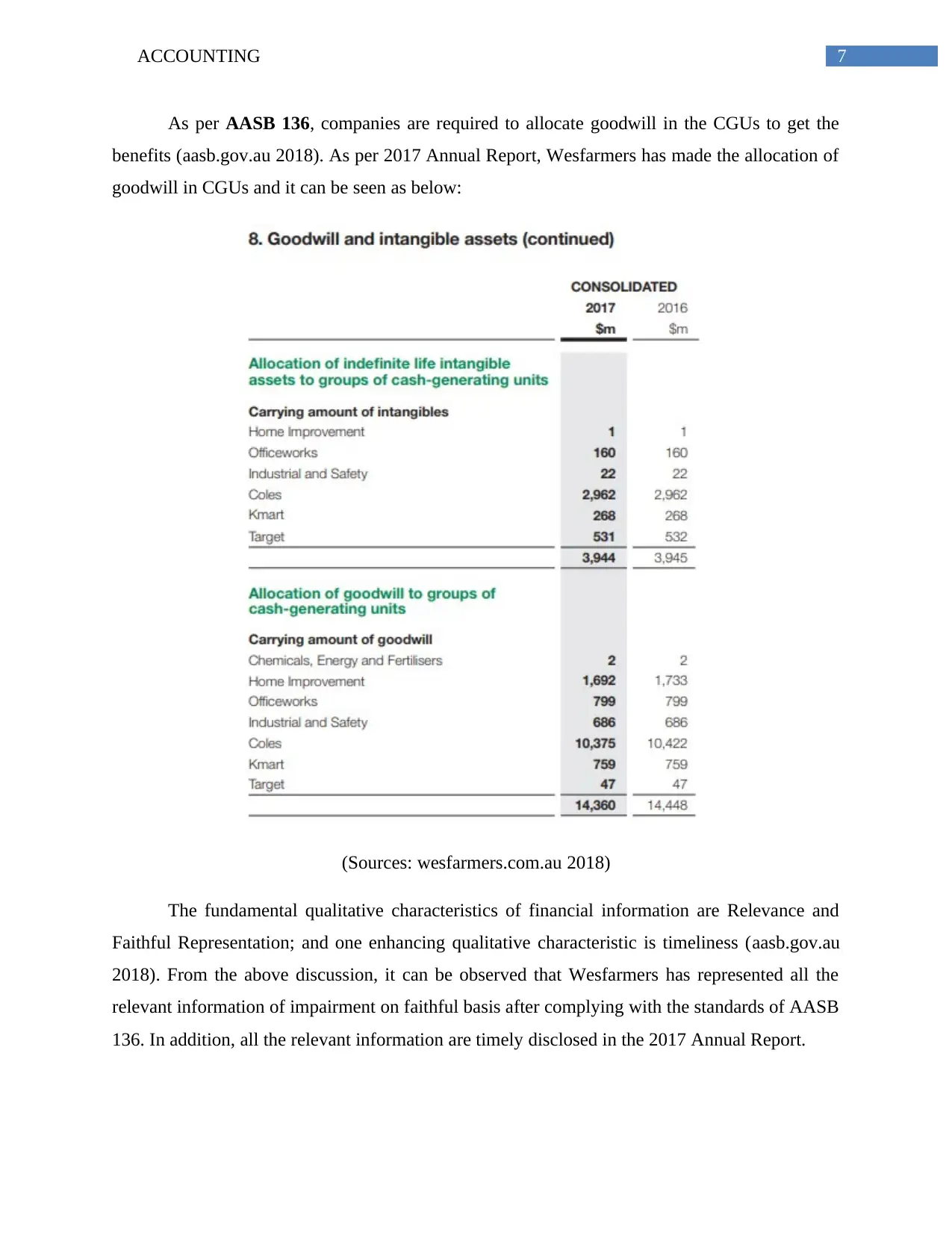

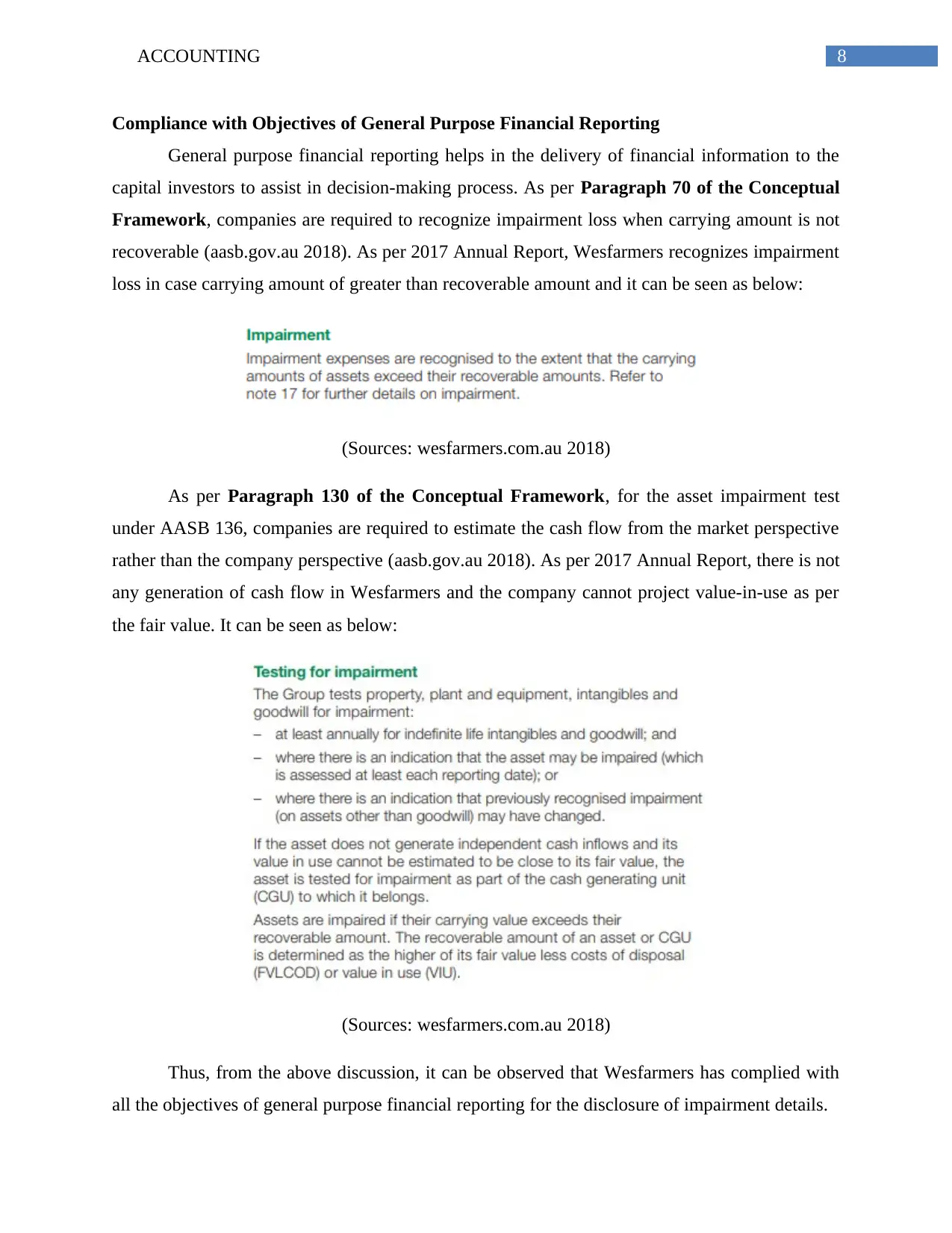

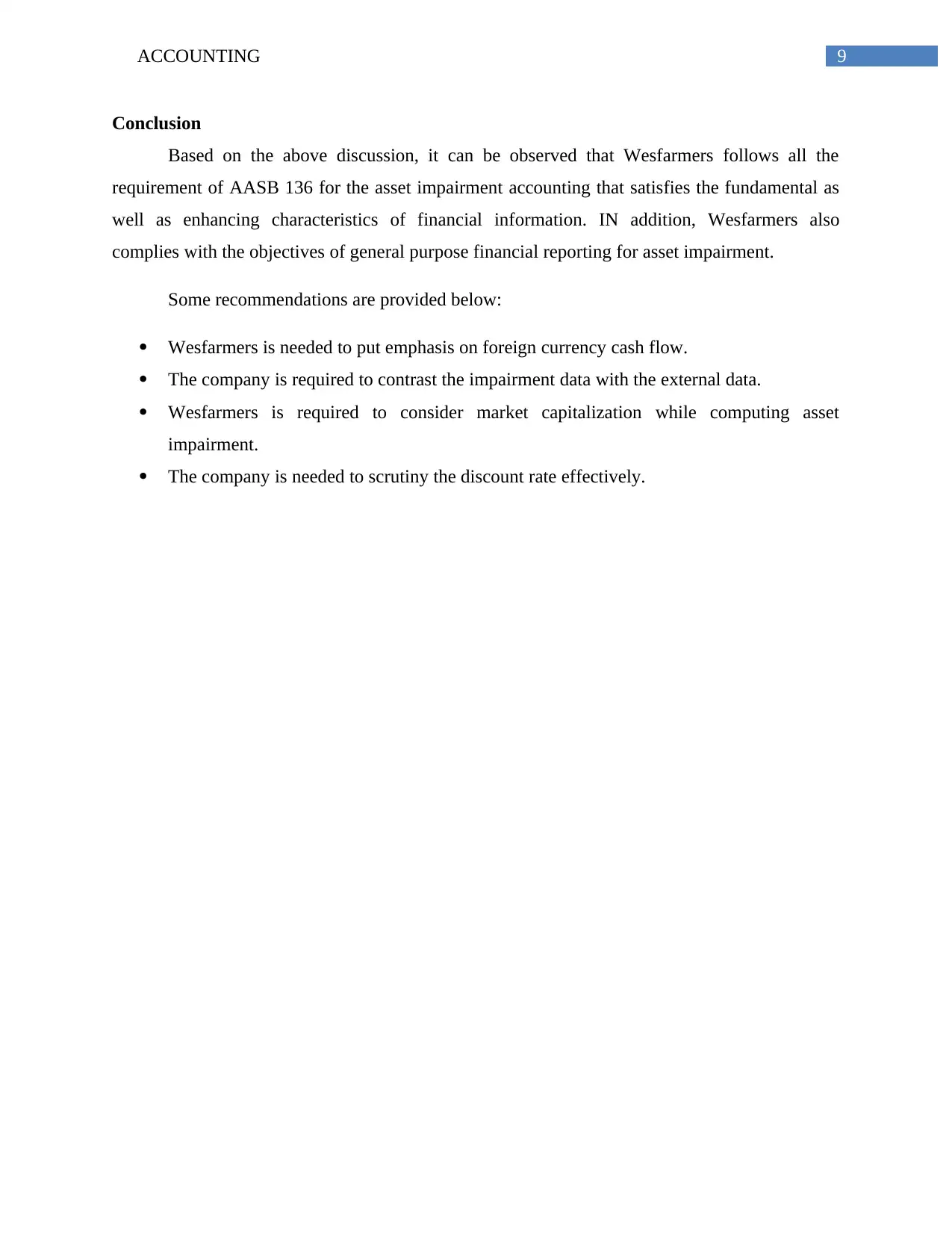

This report provides a comprehensive analysis of impairment write-downs, focusing on Wesfarmers Limited, a prominent company in the Australian retail industry. It begins by examining the role of the Australian Securities and Investment Commission (ASIC) as a corporate regulator, highlighting its responsibilities in promoting market confidence, ensuring market efficiency, and improving financial reporting quality. The report then delves into the specifics of impairment write-downs within Wesfarmers, including the assets tested, such as property, plant, and equipment (PPE), trade receivables, and goodwill, along with the amounts of impairment losses. It then assesses Wesfarmers' compliance with the qualitative characteristics of financial information, specifically relevance, faithful representation, and timeliness, as outlined in AASB 136. Finally, the report evaluates Wesfarmers' adherence to the objectives of general purpose financial reporting, focusing on the recognition of impairment losses and the estimation of cash flows. The report concludes with recommendations for Wesfarmers to enhance its impairment accounting practices, such as emphasizing foreign currency cash flow and considering market capitalization.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.