QAB105 Quantitative Analysis for Business: A Detailed Report, 2018

VerifiedAdded on 2023/06/03

|8

|1139

|173

Report

AI Summary

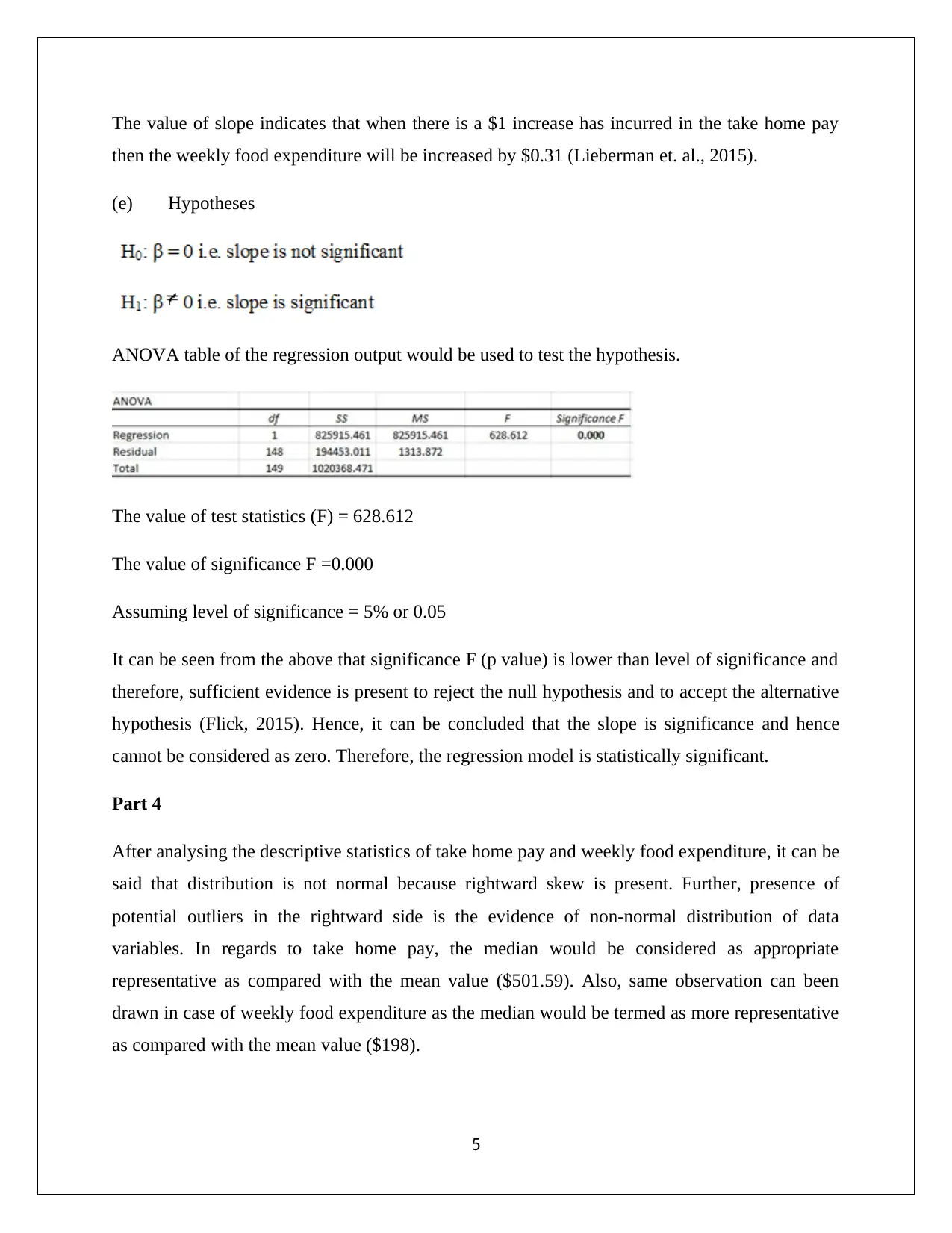

This report presents a quantitative analysis of business data, focusing on the relationship between take-home pay and weekly food expenditure. The analysis employs stratified random sampling and addresses potential data collection issues. Descriptive statistics, including histograms and numerical summaries, reveal a positive skew in the data. Regression analysis indicates a strong positive correlation between the variables, with a correlation coefficient of 0.90. The regression equation (y = 40.86 + 0.31x) suggests that for every $1 increase in take-home pay, weekly food expenditure increases by $0.31. Hypothesis testing confirms the statistical significance of the regression model. The report concludes that the variables are strongly correlated, validating the understanding that food expenditure is a function of income. Desklib offers a variety of similar solved assignments and past papers for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.