Investor Perception of Auditor's Fraud Detection Abilities

VerifiedAdded on 2023/01/20

|21

|3489

|83

Report

AI Summary

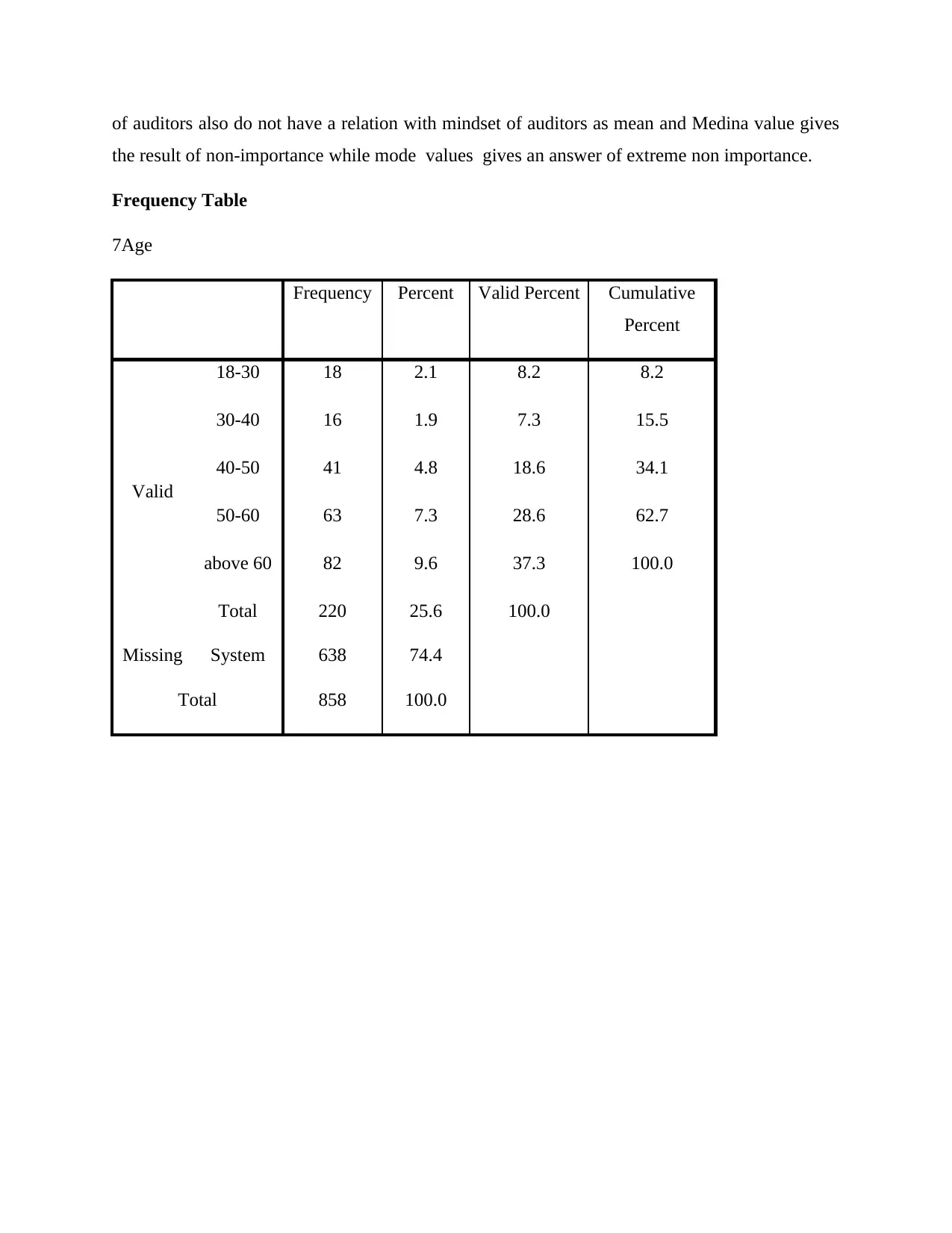

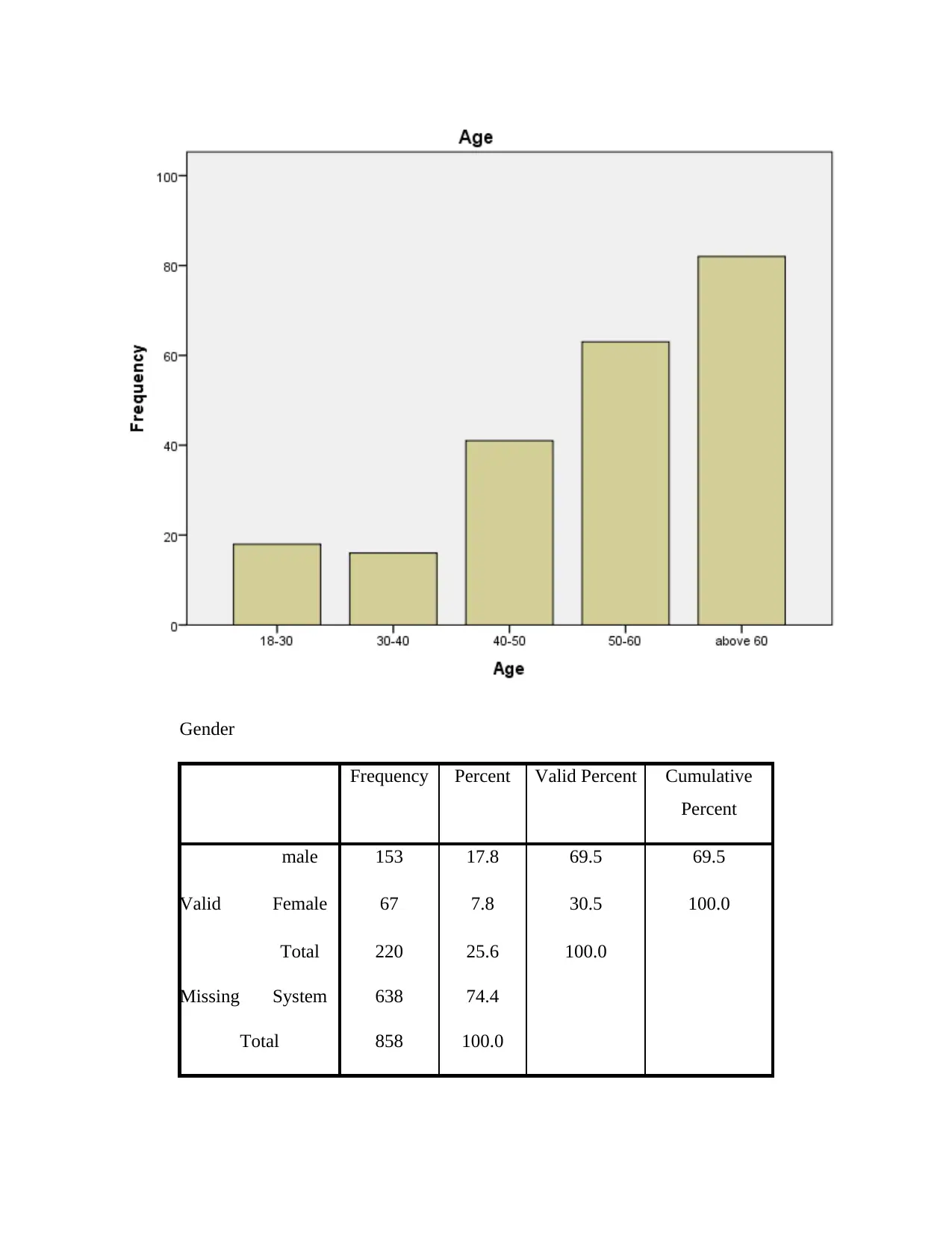

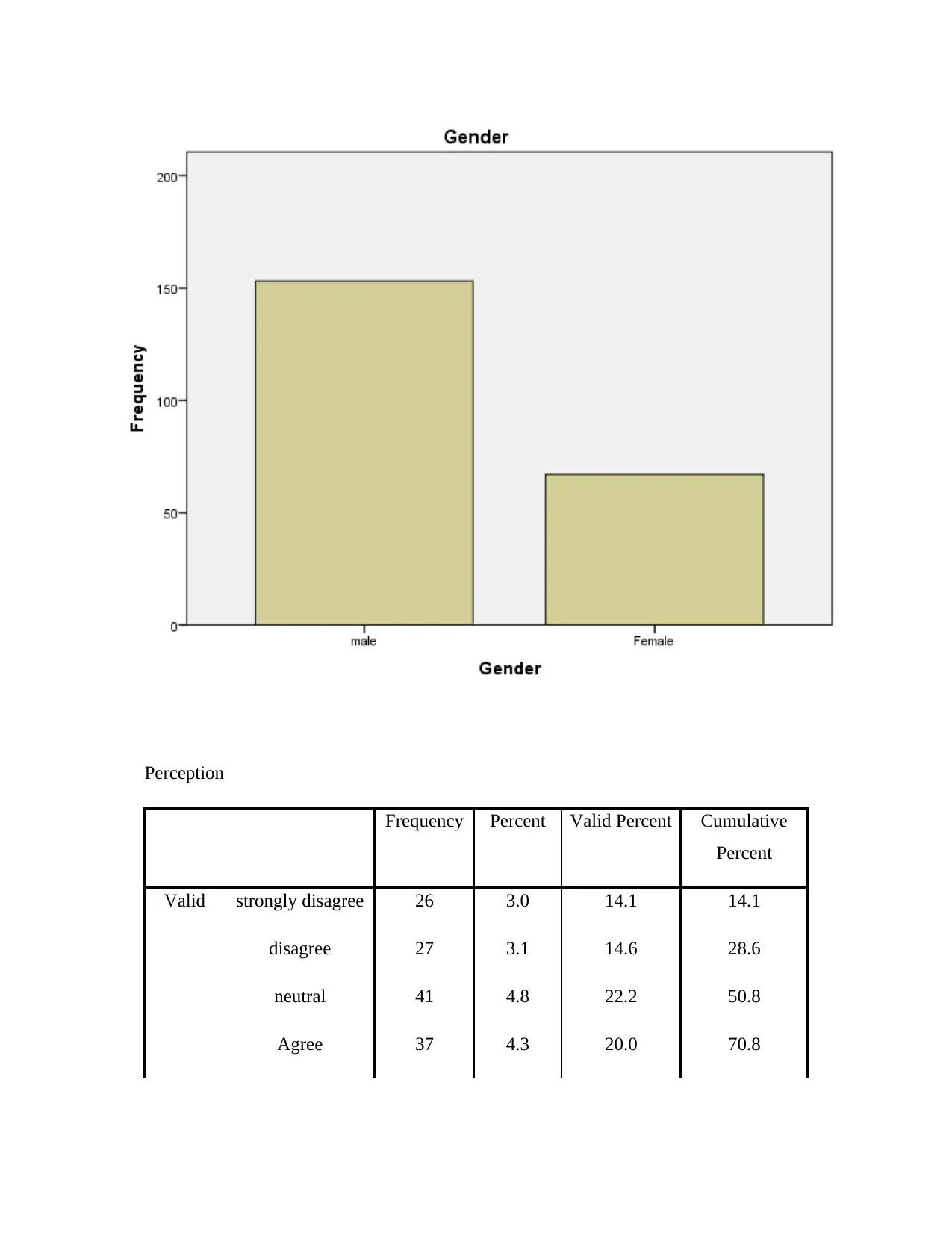

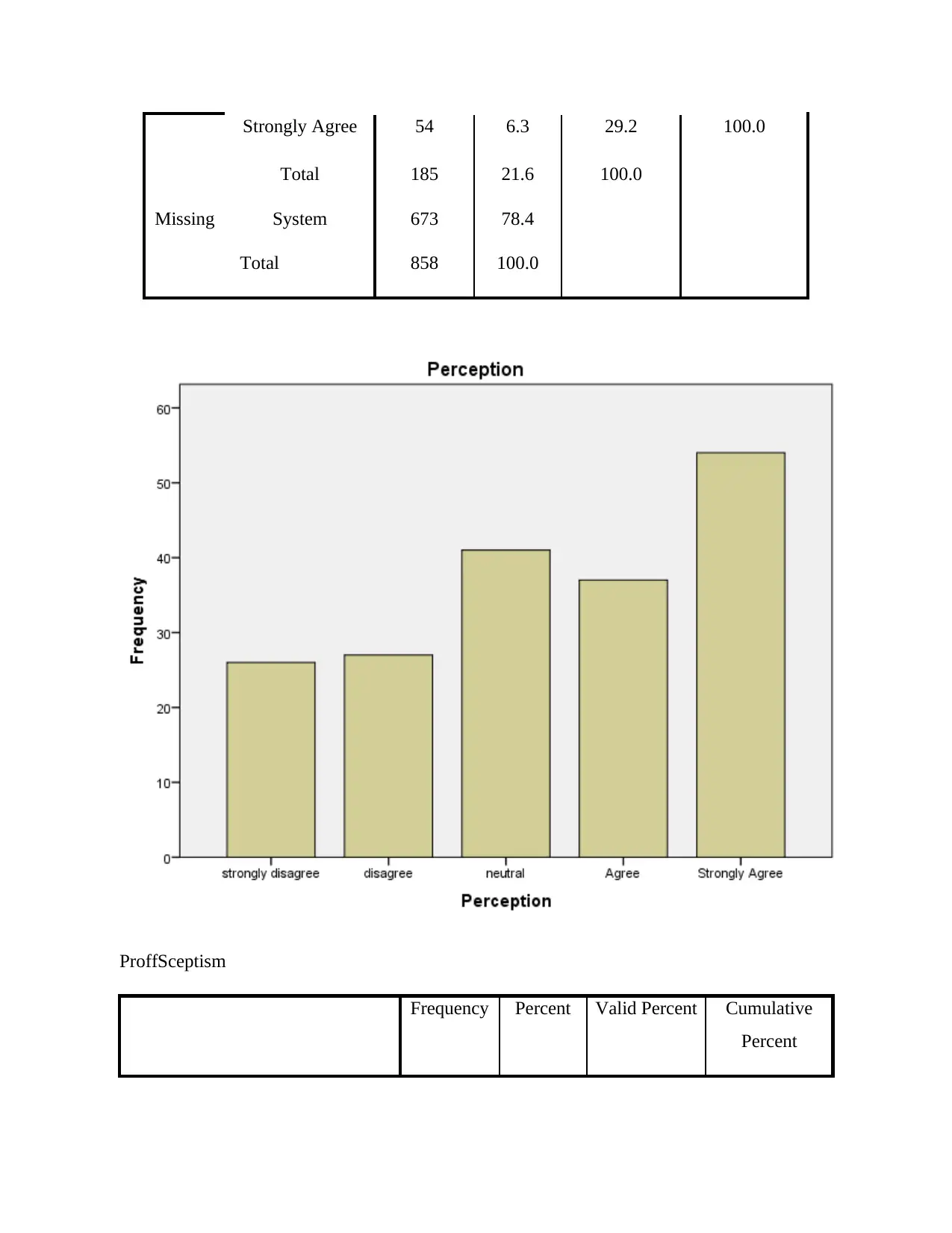

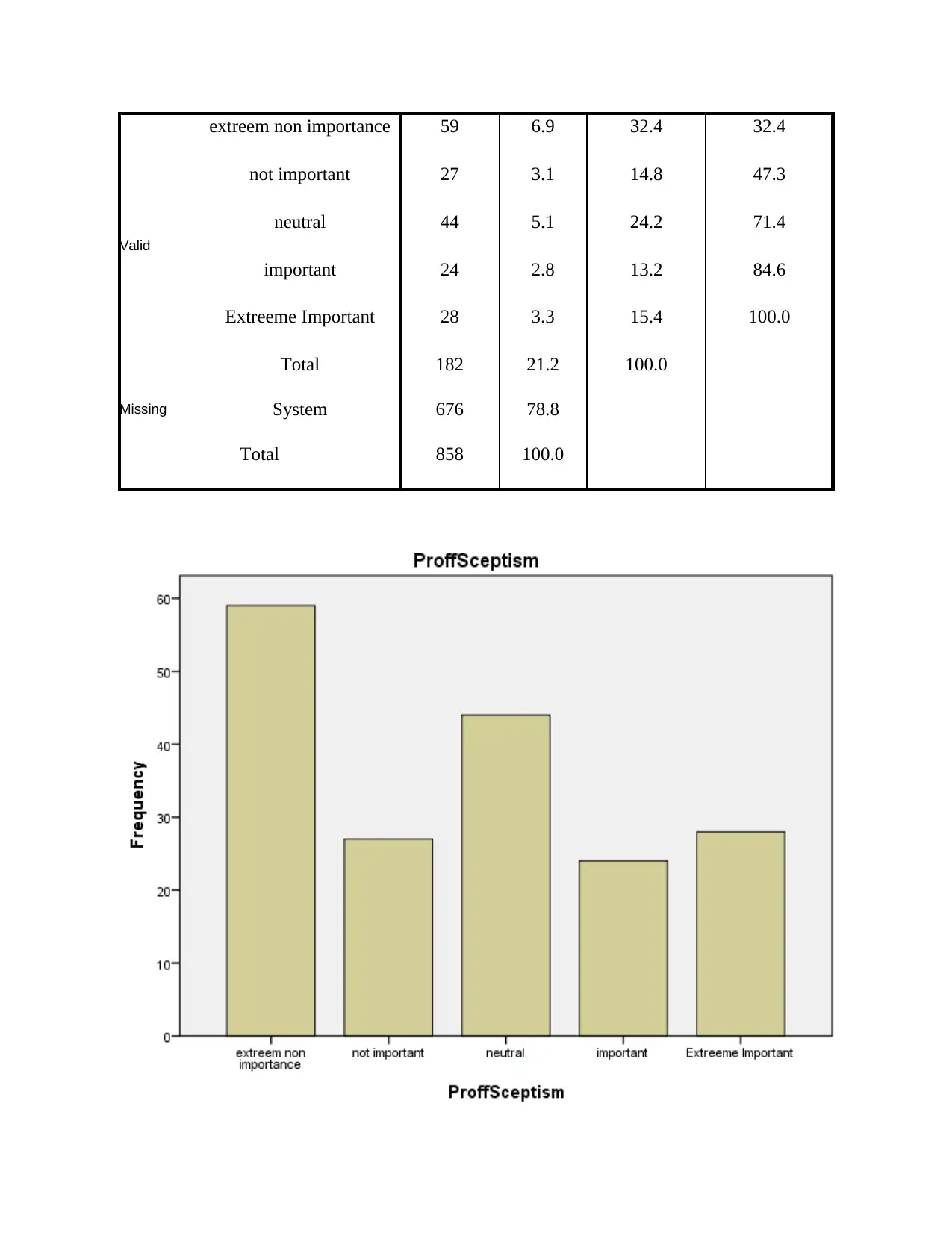

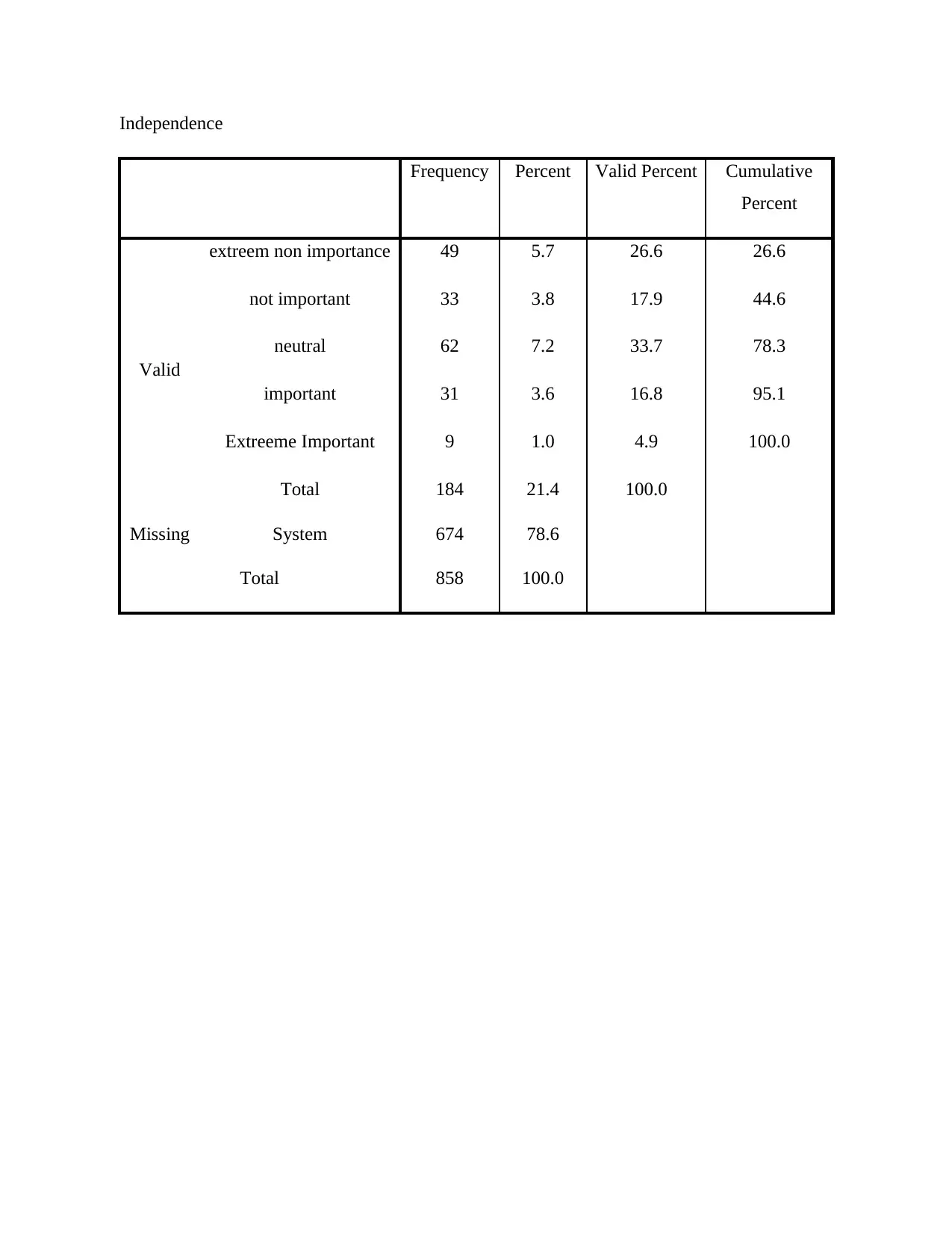

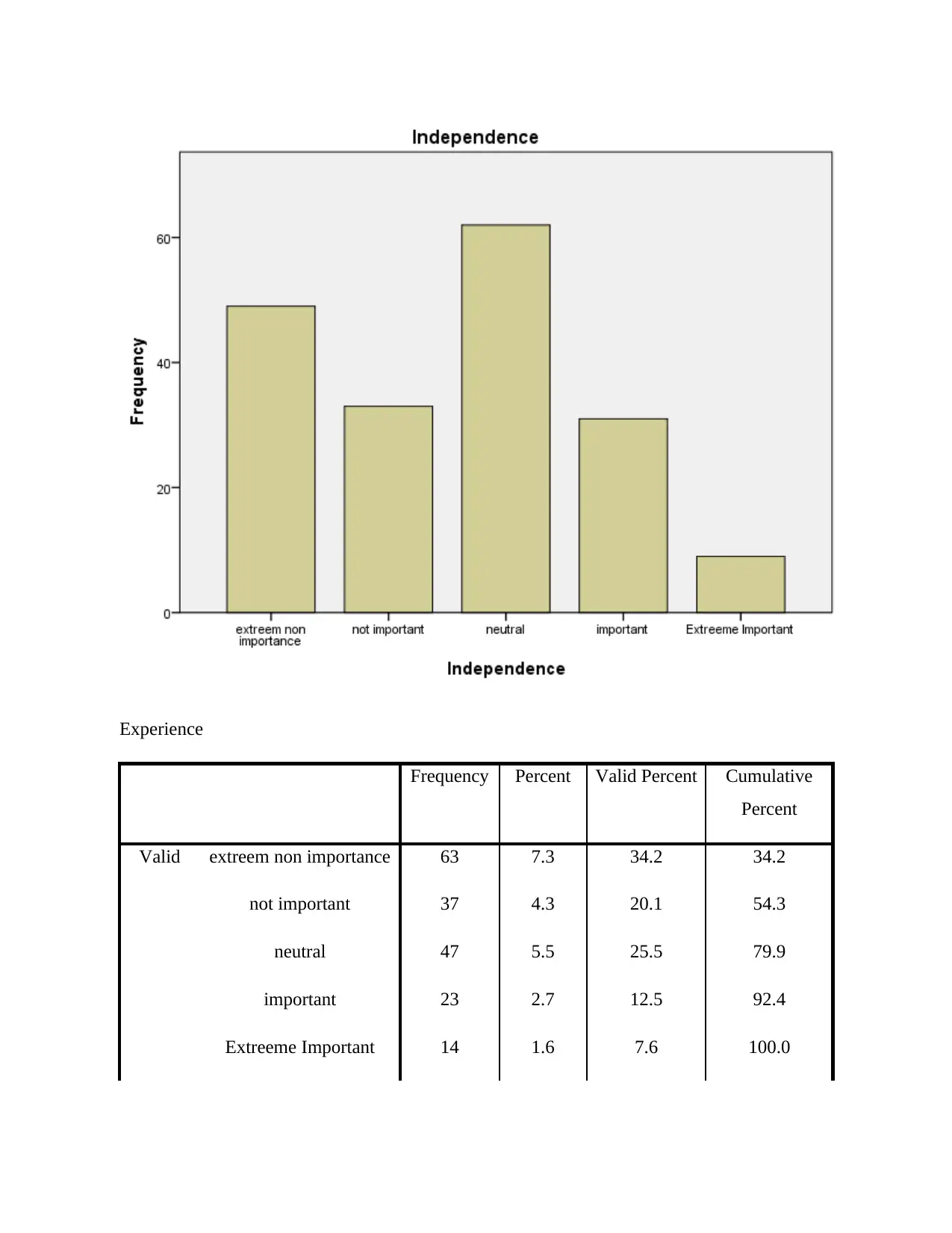

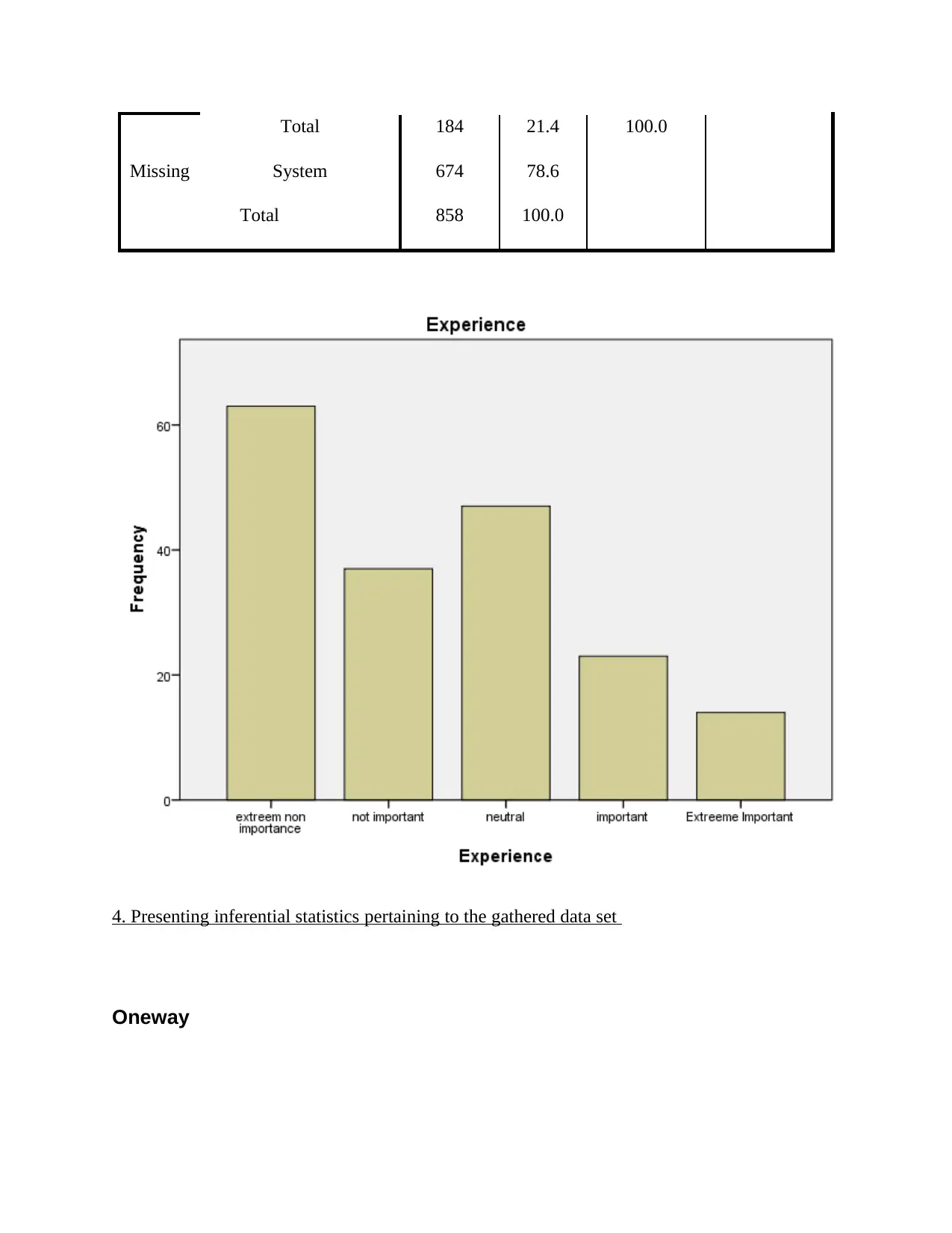

This report presents a quantitative data analysis exploring the relationship between auditor characteristics and investor perception of fraud detection. The study examines the impact of auditor independence, professional skepticism, and experience on investor views. Descriptive statistics summarize the data set, including mean, median, and mode for key variables. Inferential statistics, including ANOVA and post-hoc tests, are used to test the hypotheses. The analysis reveals that investor perception varies significantly with professional skepticism but not with auditor independence or experience. The report also identifies limitations of the data and references literature to support the methodologies used. Overall, the report provides a comprehensive analysis of the factors influencing investor perception of auditor fraud detection capabilities, offering valuable insights into the financial auditing process and its impact on investor confidence.

1 out of 21

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.