Quantitative Finance and Financial Market Assignment - Course Code XYZ

VerifiedAdded on 2023/06/08

|26

|5367

|155

Homework Assignment

AI Summary

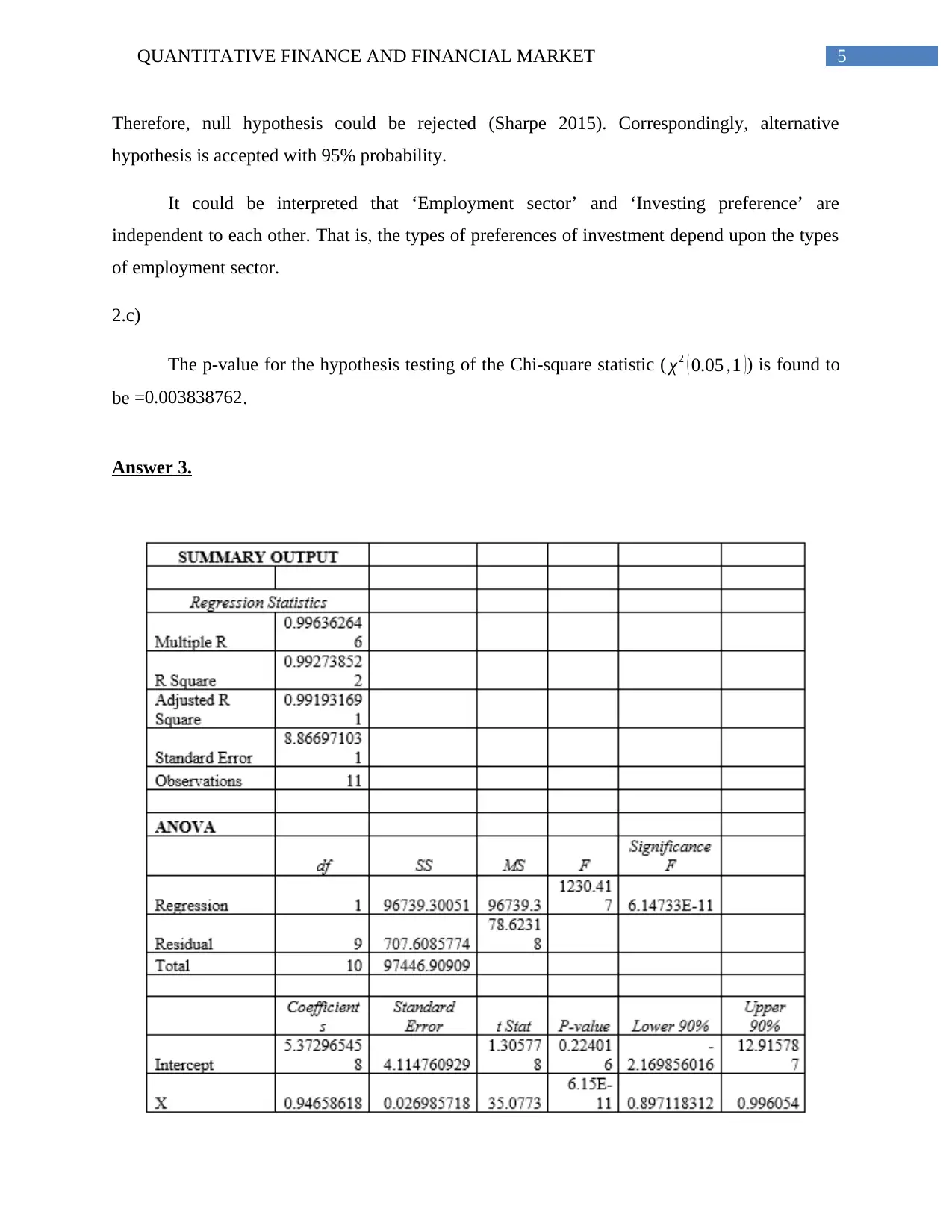

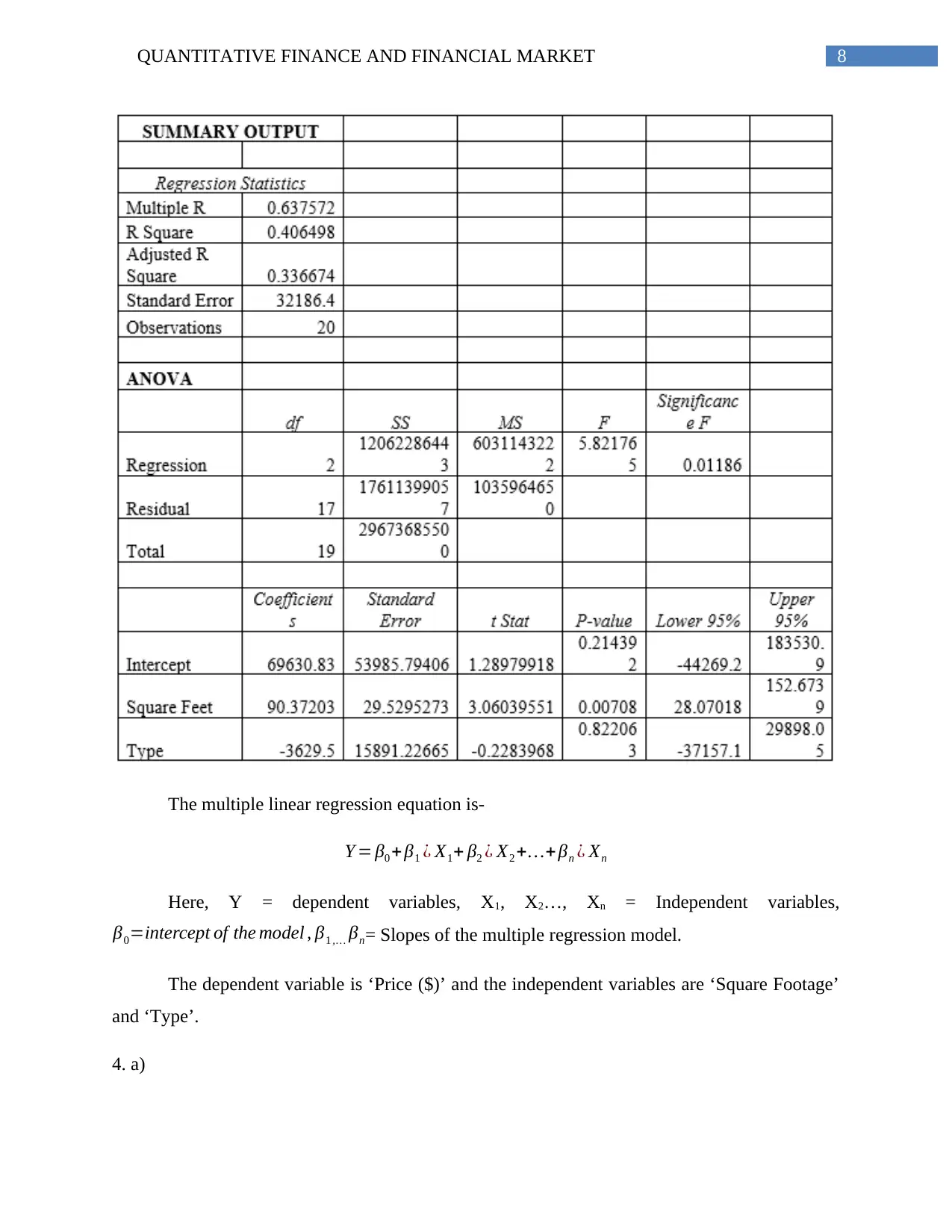

This assignment solution addresses several key concepts in quantitative finance and financial markets. It begins with a two-sample t-test to compare median incomes of men and women, followed by a Chi-square test to analyze the association between employment sector and investment preferences. The solution then delves into regression analysis, including least squares regression to predict account balances and multiple linear regression to predict housing prices based on square footage and type. Furthermore, the assignment includes time series analysis using dummy variables to forecast client generation and concludes with portfolio optimization, calculating expected returns and standard deviations for various stock combinations to construct an efficient frontier. The solution demonstrates the application of statistical methods to real-world financial scenarios, offering insights into market analysis, investment strategies, and risk management.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.