Ask a question from expert

Quantitative finance Assignment Solved

12 Pages1287 Words138 Views

Added on 2021-02-20

Quantitative finance Assignment Solved

Added on 2021-02-20

BookmarkShareRelated Documents

QUANTITATIVE FINANCE PROJECT1

TABLE OF CONTENTSTASK A...........................................................................................................................................1Discussing CAPM theory and related literature..........................................................................1TASK B...........................................................................................................................................1(1) Regression analysis to compute beta.....................................................................................1(2) T test......................................................................................................................................3(3) CAPM analysis......................................................................................................................5(4) CAPM and sensitivity to industry change.............................................................................6TASK C...........................................................................................................................................6(1) Fixed and random effects......................................................................................................6(2) Model for panel data regression analysis..............................................................................7REFERENCES..............................................................................................................................................12Figure 1GSK and FTSE regression.................................................................................................1Figure 2HIK and FTSE regression..................................................................................................2Figure 3IAG and FTSE regression..................................................................................................2Figure 4 IHG and FTSE regression.................................................................................................3Figure 5FTSE and GSK T test.........................................................................................................3Figure 6FTSE and HSK T test.........................................................................................................4Figure 7FTSE and IAG T test..........................................................................................................4Figure 8FTSE and IHG T test..........................................................................................................5Figure 9CAPM for GSK,HIK,IAG and IHG...................................................................................5Figure 10Hausman test for GSK and FTSE....................................................................................7Figure 11Panel regression for FTSE and GSK................................................................................8Figure 12Hausman test for HIK and FTSE.....................................................................................8Figure 13Panel regression for HIK and FTSE.................................................................................9Figure 14Hausman test for IAG and FTSE.....................................................................................9Figure 15Panel regression..............................................................................................................10Figure 16Hausman test for IHG and FTSE...................................................................................10

Figure 17Panel regression..............................................................................................................11

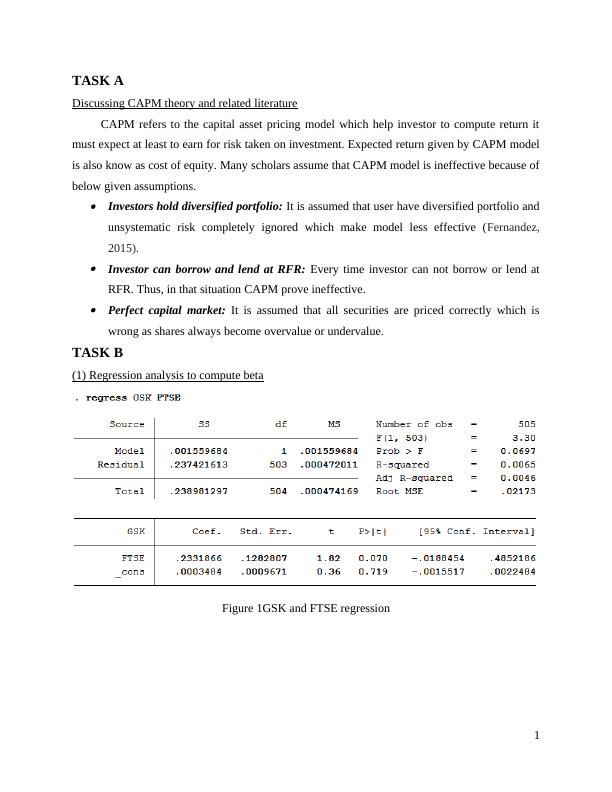

TASK ADiscussing CAPM theory and related literatureCAPM refers to the capital asset pricing model which help investor to compute return itmust expect at least to earn for risk taken on investment. Expected return given by CAPM modelis also know as cost of equity. Many scholars assume that CAPM model is ineffective because ofbelow given assumptions.Investors hold diversified portfolio: It is assumed that user have diversified portfolio andunsystematic risk completely ignored which make model less effective (Fernandez,2015).Investor can borrow and lend at RFR: Every time investor can not borrow or lend atRFR. Thus, in that situation CAPM prove ineffective.Perfect capital market: It is assumed that all securities are priced correctly which iswrong as shares always become overvalue or undervalue.TASK B(1) Regression analysis to compute betaFigure 1GSK and FTSE regression1

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Testing the CAPM Theory Using Time Series Regression Analysislg...

|18

|3072

|254

INVESTMENT ANALYSIS TABLE OF CONTENTSlg...

|15

|714

|74

Assignment On Excess Market Returnlg...

|6

|643

|19

(PDF) A Study on Multiple Linear Regression Analysislg...

|15

|2850

|227

CAPM Analysis of the Capital Asset Pricinglg...

|14

|3300

|18

Statistics Group Assignmentlg...

|10

|1019

|132