Financial Management Assignment (Semester 2, 2019): Finance Topics

VerifiedAdded on 2022/11/16

|8

|1465

|240

Homework Assignment

AI Summary

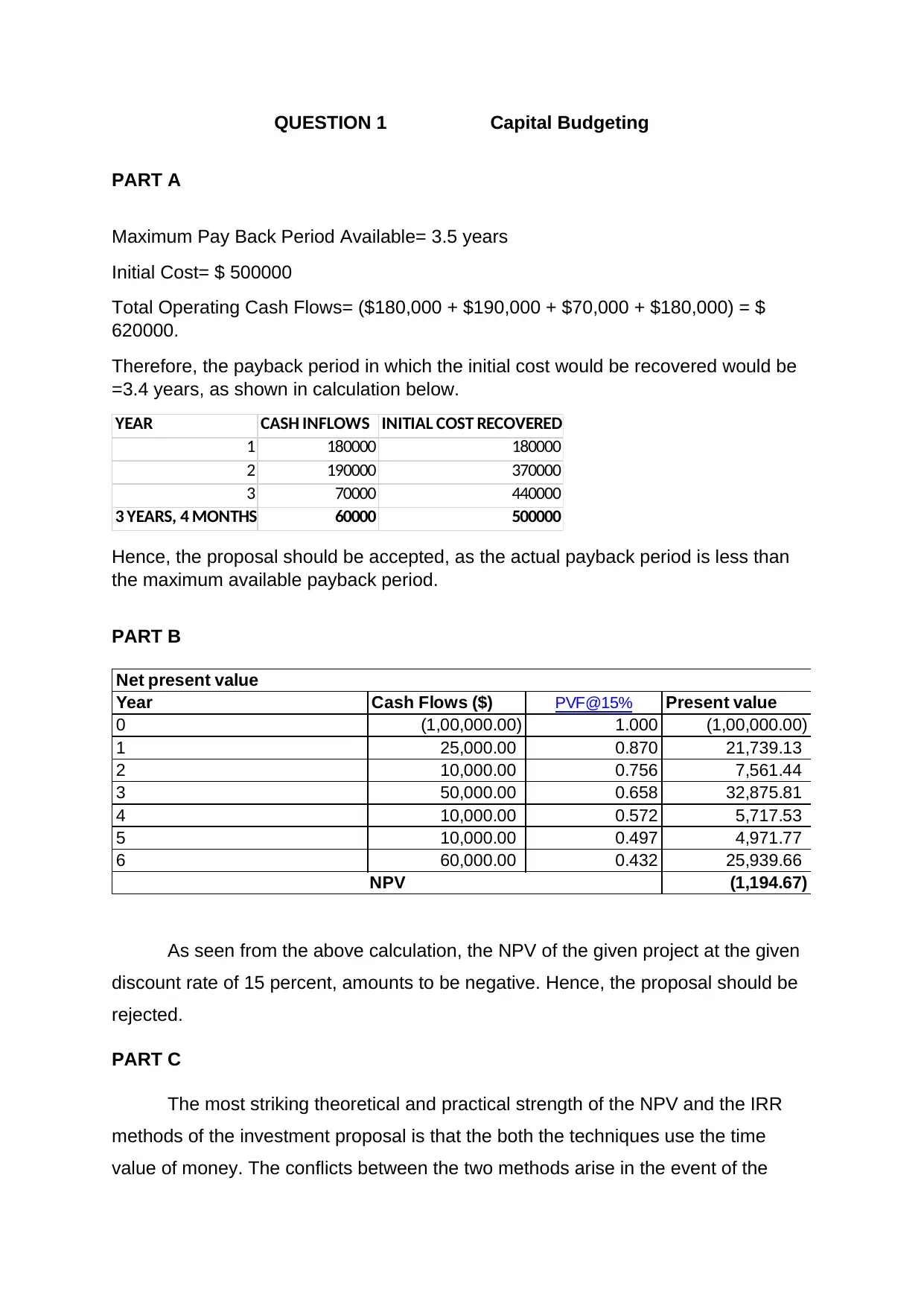

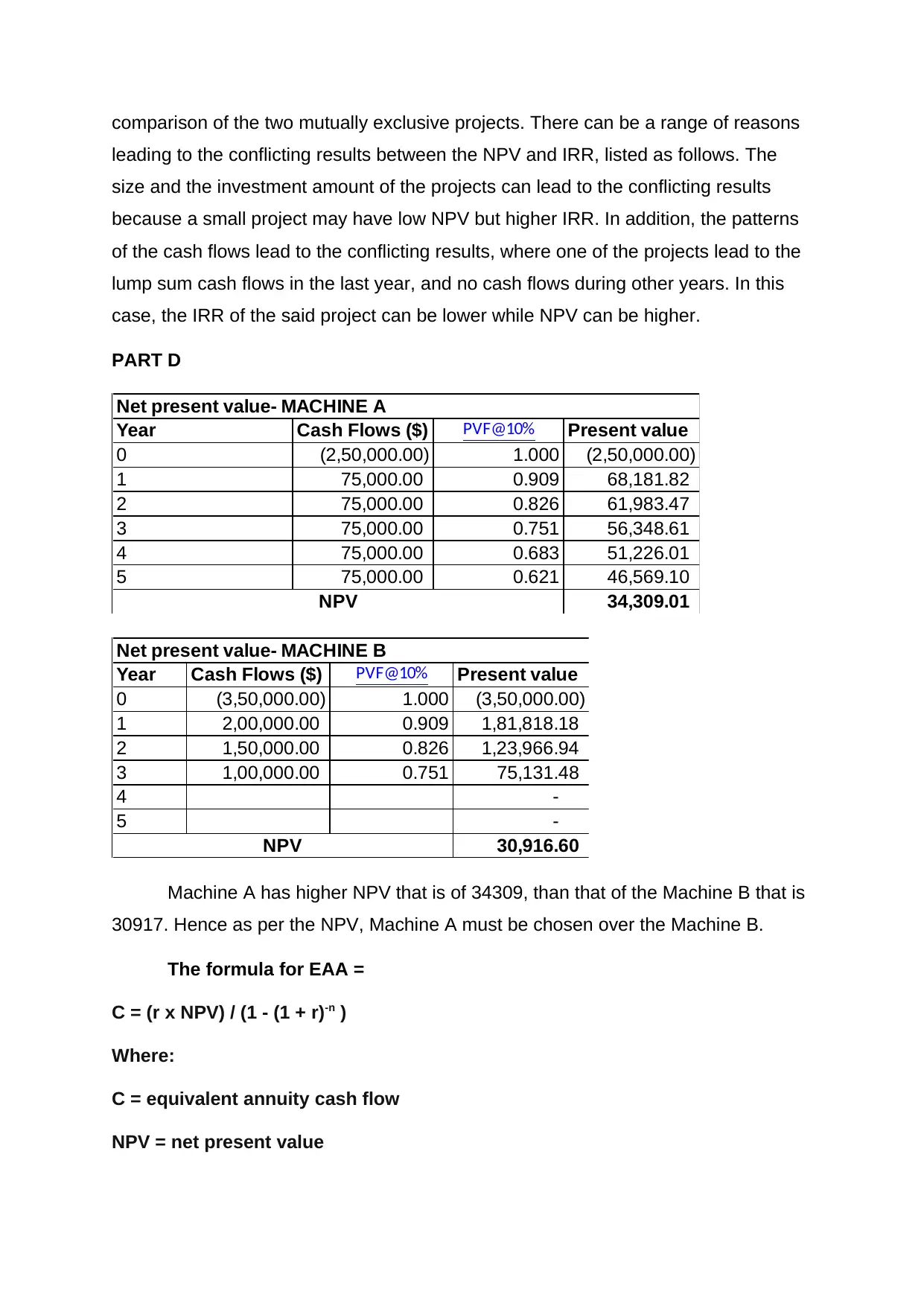

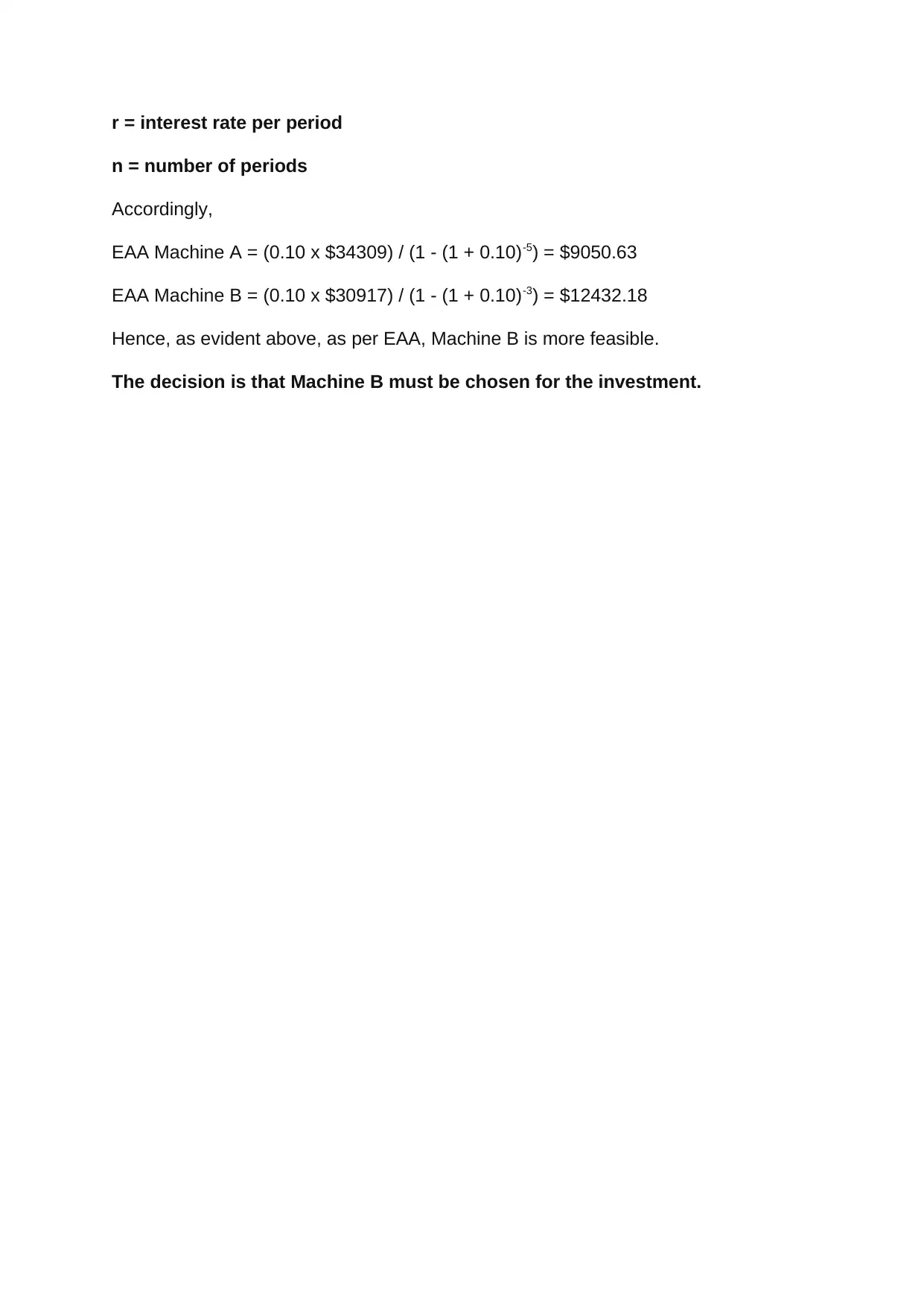

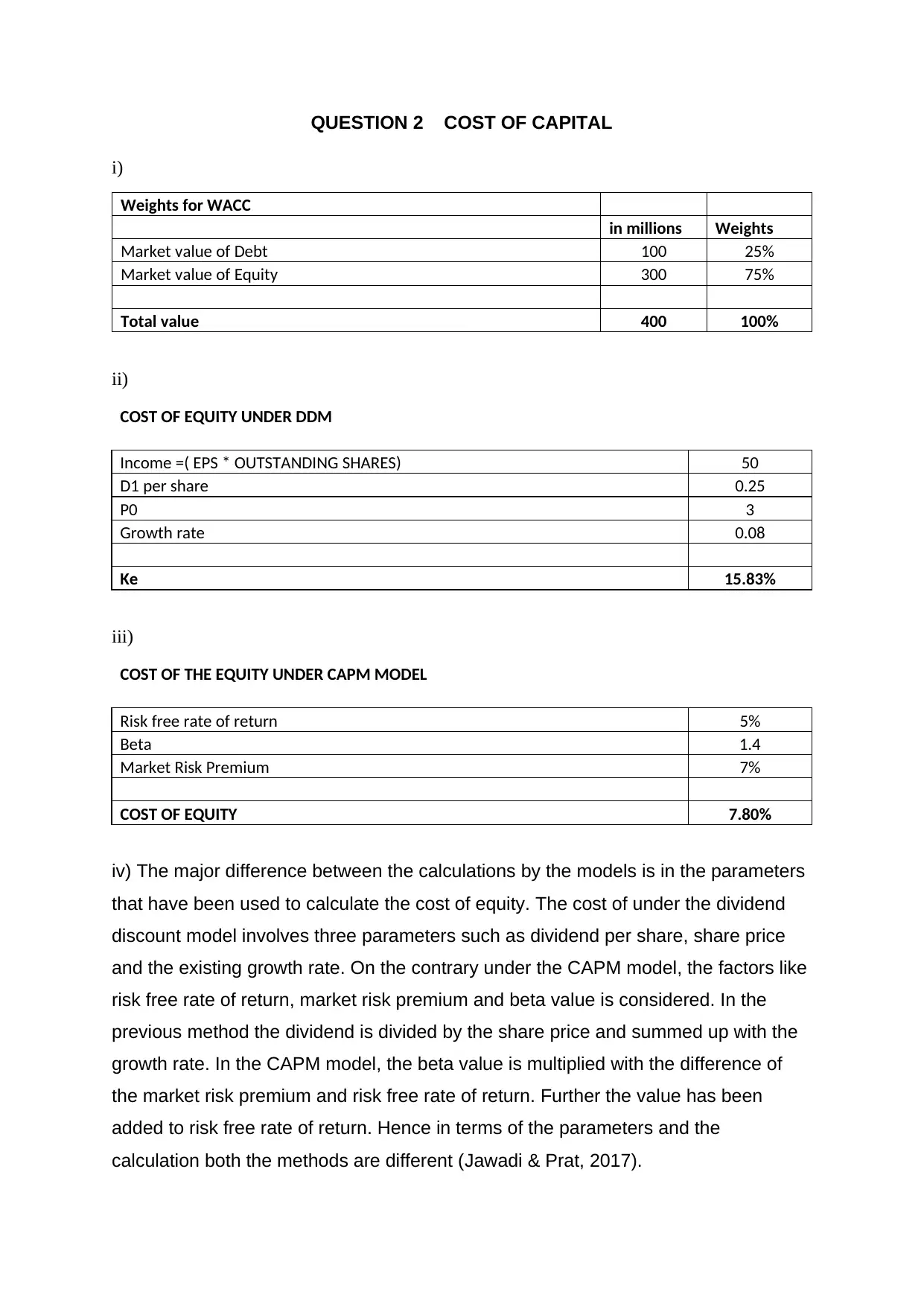

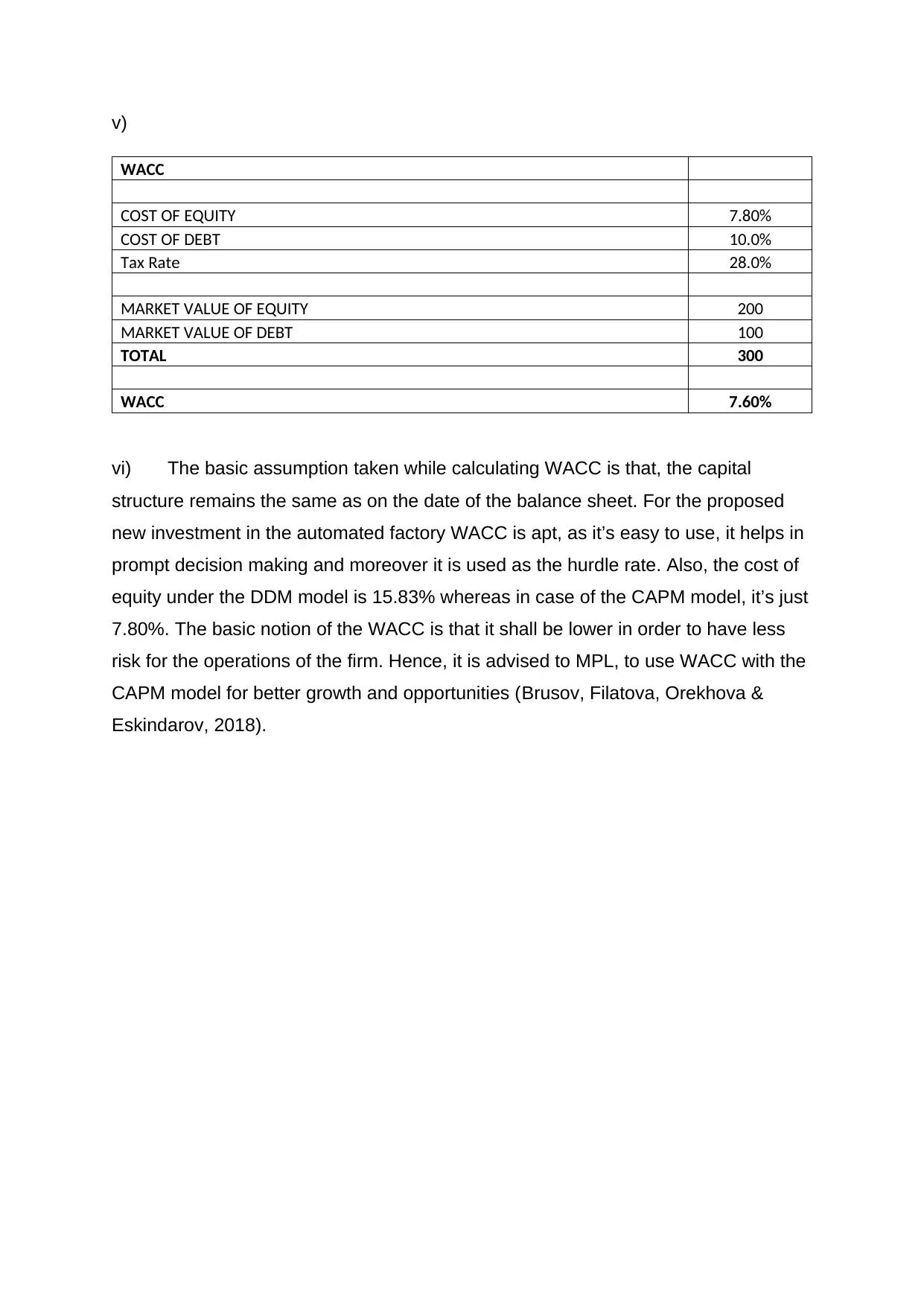

This finance assignment addresses key concepts in financial management, including capital budgeting, cost of capital, and risk and return analysis. The assignment begins with a capital budgeting section, evaluating a project's payback period and NPV, and discussing the strengths and weaknesses of NPV and IRR methods, and comparing the feasibility of different machines using NPV and EAA. The second section focuses on the cost of capital, calculating the weighted average cost of capital (WACC) using both DDM and CAPM models, and discussing the assumptions and implications of WACC. The final section delves into risk and return, valuing shares using Gordon's Growth Model, explaining diversification's role in risk reduction, contrasting beta and standard deviation, and calculating the cost of equity for ordinary and preference shares. The assignment demonstrates the application of financial principles and models to make informed investment and financial decisions.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.