University Finance: Options, Futures, and Risk Management Assignment

VerifiedAdded on 2022/11/01

|11

|966

|434

Homework Assignment

AI Summary

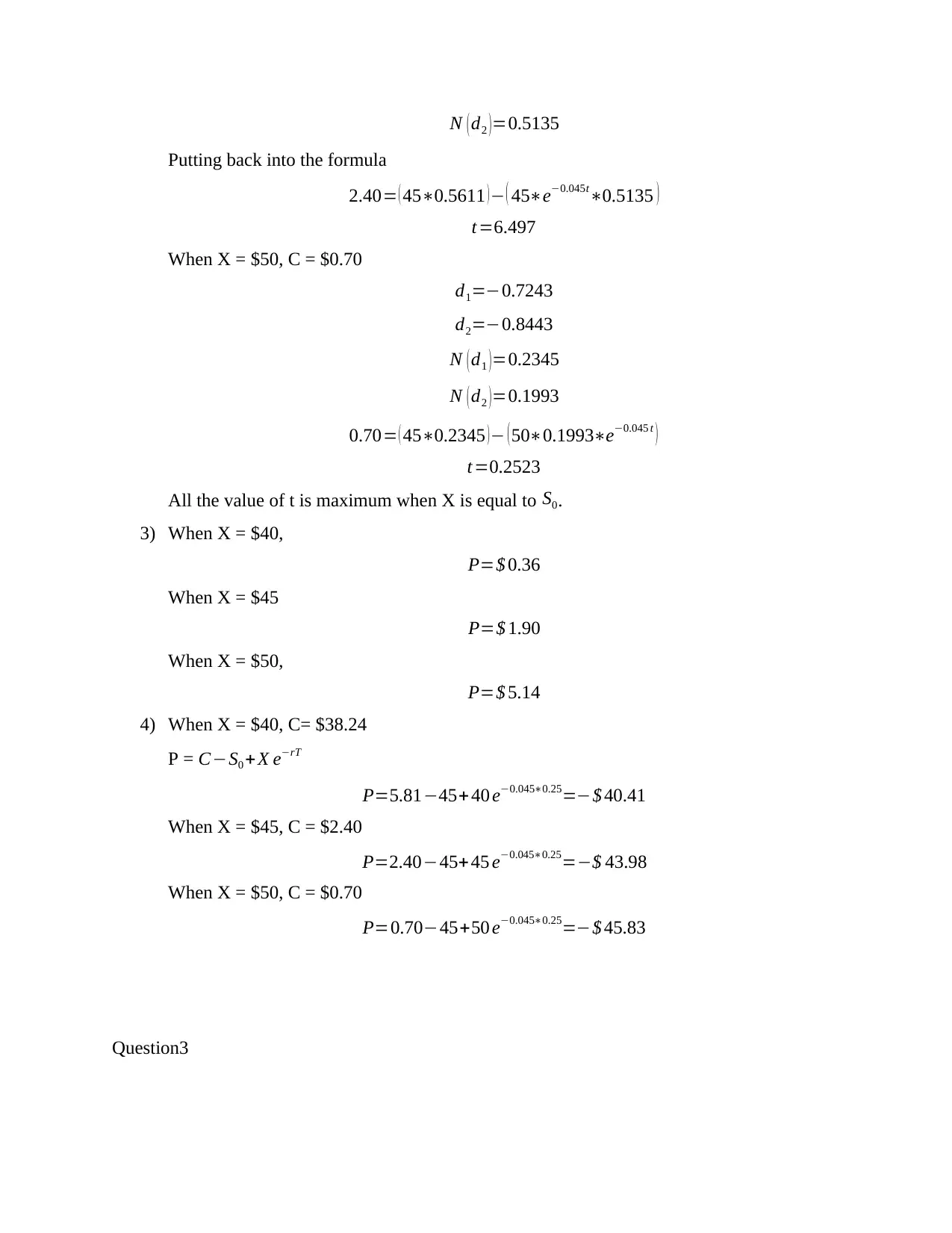

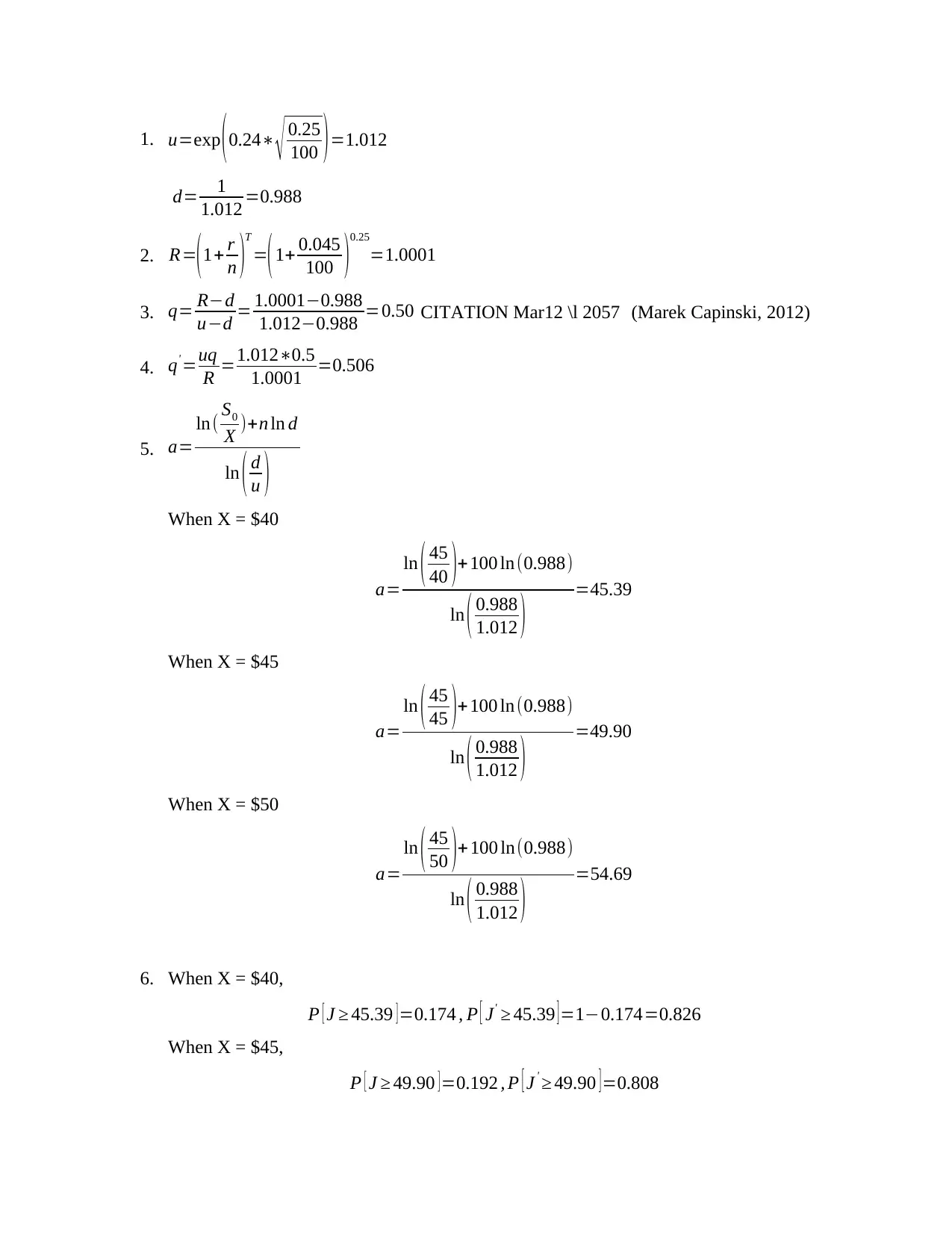

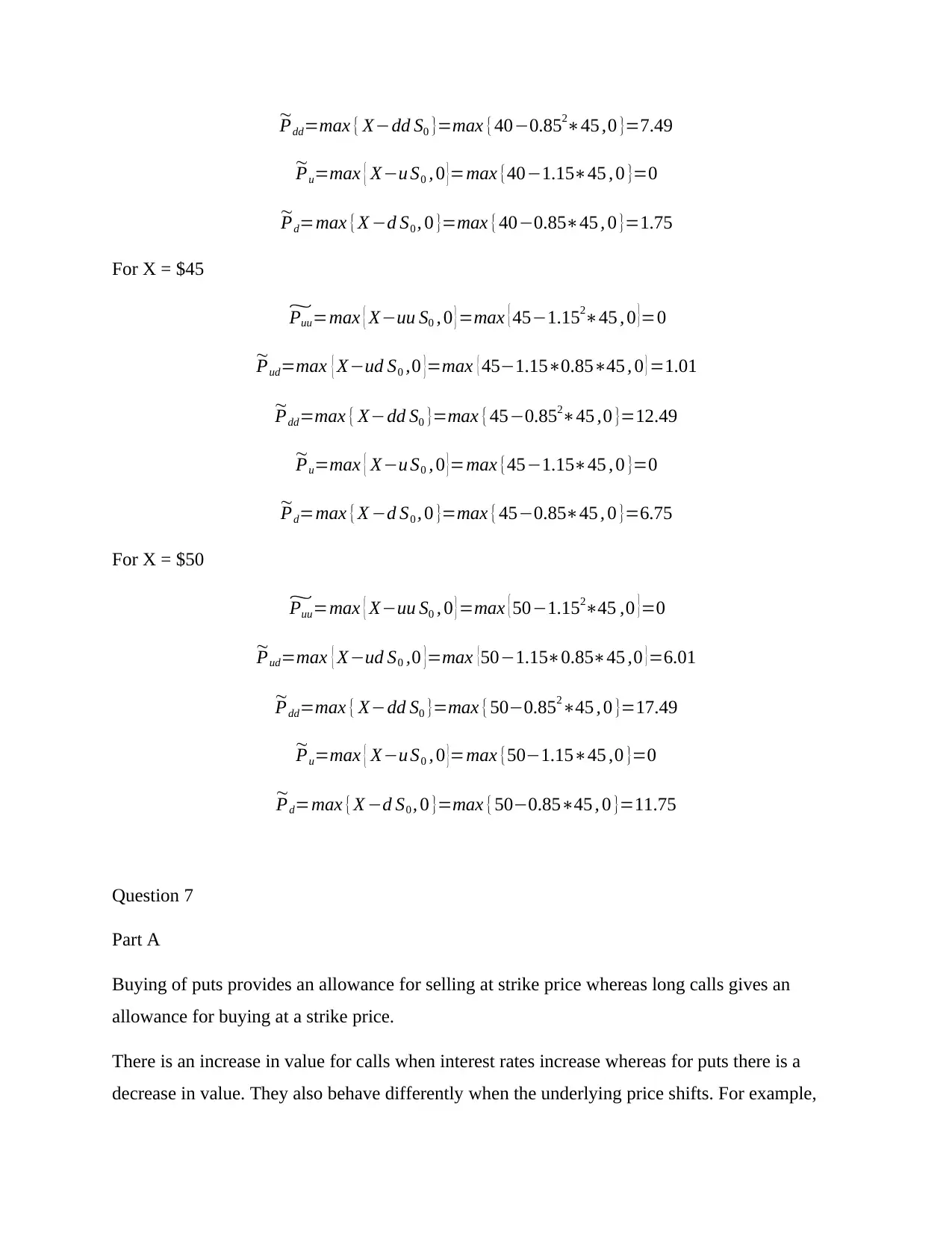

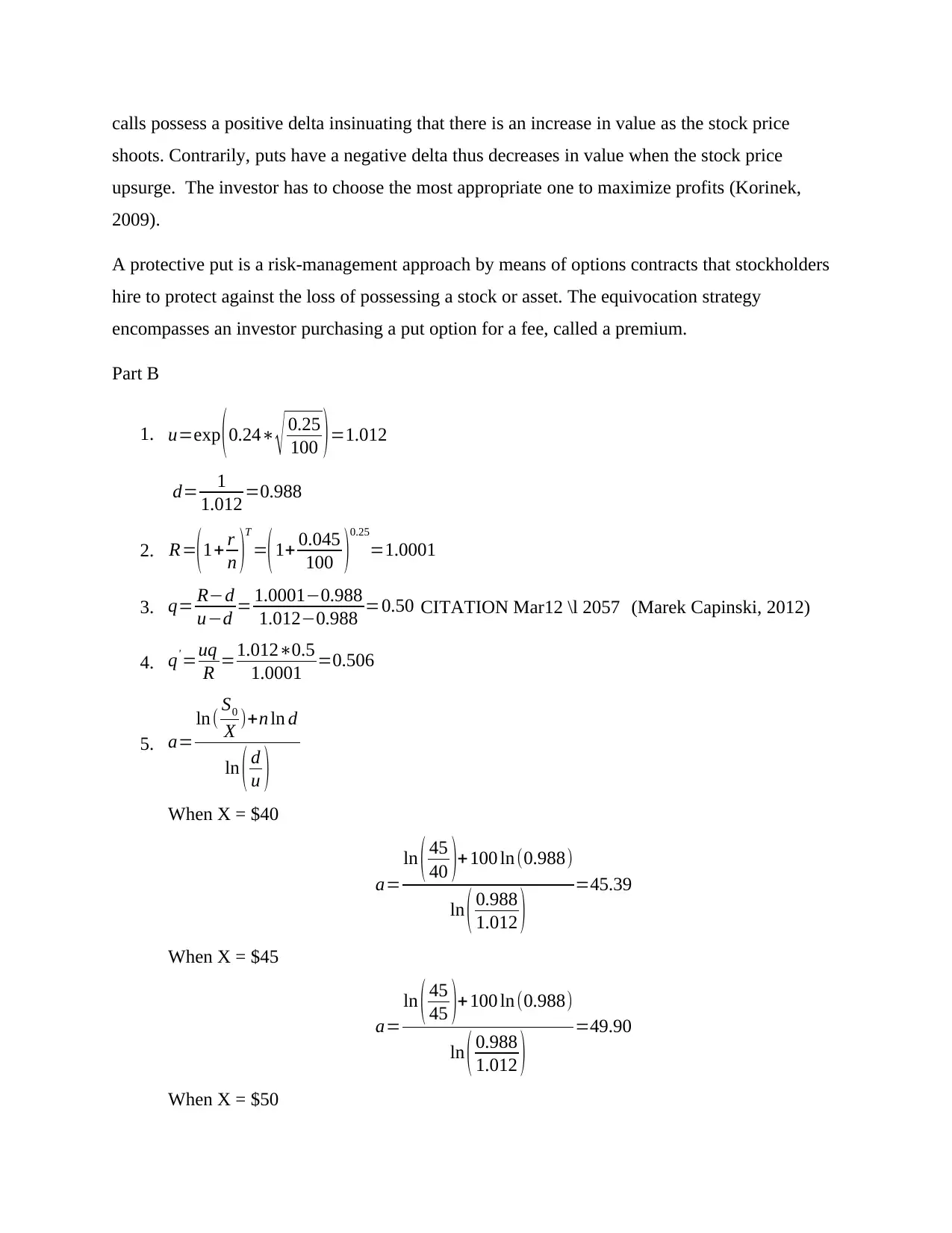

This assignment delves into the intricacies of options, futures, and risk management, covering several key areas. It begins with a simulation of stock prices using Brownian motion, exploring the impact of volatility and risk-free interest rates. The assignment then proceeds to calculate European call option prices using the Black-Scholes-Merton model and other methods, comparing their results and methodologies. Furthermore, it investigates the concept of the volatility smile, analyzing its implications for implied volatility and moneyness. The assignment also explores the differences between put and call options, including their delta and how they respond to changes in interest rates and underlying asset prices. Finally, it examines protective put strategies and calculates breakeven points and potential profits for various scenarios. The student provides detailed calculations, formulas, and interpretations throughout the assignment, demonstrating a strong understanding of the subject matter and the application of financial models. Excel simulations are included to support the analysis.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.