Cost Accounting Homework: Financial, Cost, and Profit Analysis

VerifiedAdded on 2020/04/07

|13

|2454

|500

Homework Assignment

AI Summary

This homework assignment solution provides a detailed analysis of various cost accounting problems. It begins with a process costing problem, calculating equivalent units, cost per unit, and the cost of goods transferred out and ending work-in-process inventory. The solution then addresses financial, environmental, social, and economic issues related to a spice processing company's expansion, evaluating cost-benefit analyses and risk factors. It also includes a cost behavior analysis using the high-low method and least squares regression, along with a break-even analysis and margin of safety calculations. Furthermore, the assignment explores absorption and variable costing methods, comparing income statements under both approaches. Finally, it presents an activity-based costing analysis, comparing it to traditional costing and evaluating product profitability and pricing strategies, with a memo summarizing the findings and recommendations.

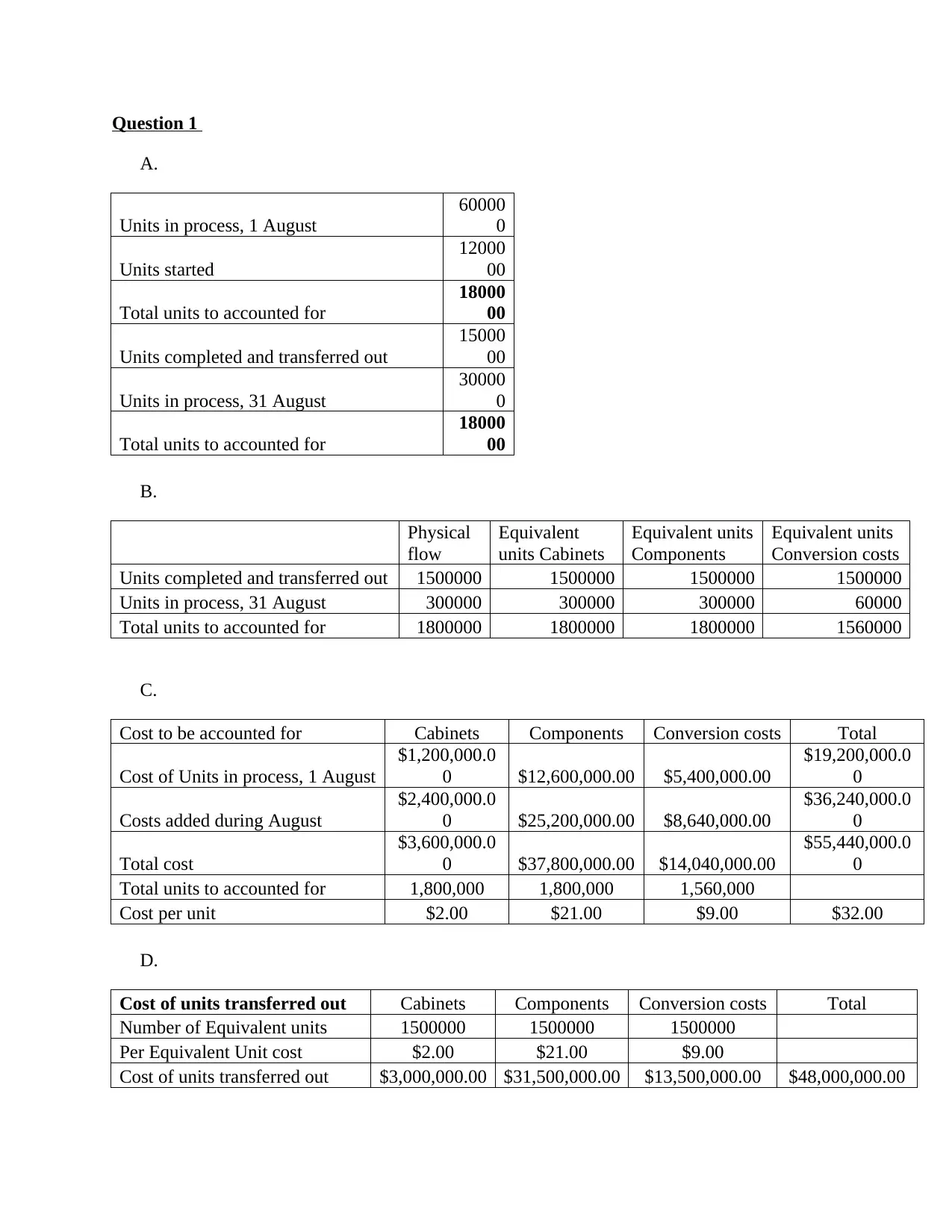

Question 1

A.

Units in process, 1 August

60000

0

Units started

12000

00

Total units to accounted for

18000

00

Units completed and transferred out

15000

00

Units in process, 31 August

30000

0

Total units to accounted for

18000

00

B.

Physical

flow

Equivalent

units Cabinets

Equivalent units

Components

Equivalent units

Conversion costs

Units completed and transferred out 1500000 1500000 1500000 1500000

Units in process, 31 August 300000 300000 300000 60000

Total units to accounted for 1800000 1800000 1800000 1560000

C.

Cost to be accounted for Cabinets Components Conversion costs Total

Cost of Units in process, 1 August

$1,200,000.0

0 $12,600,000.00 $5,400,000.00

$19,200,000.0

0

Costs added during August

$2,400,000.0

0 $25,200,000.00 $8,640,000.00

$36,240,000.0

0

Total cost

$3,600,000.0

0 $37,800,000.00 $14,040,000.00

$55,440,000.0

0

Total units to accounted for 1,800,000 1,800,000 1,560,000

Cost per unit $2.00 $21.00 $9.00 $32.00

D.

Cost of units transferred out Cabinets Components Conversion costs Total

Number of Equivalent units 1500000 1500000 1500000

Per Equivalent Unit cost $2.00 $21.00 $9.00

Cost of units transferred out $3,000,000.00 $31,500,000.00 $13,500,000.00 $48,000,000.00

A.

Units in process, 1 August

60000

0

Units started

12000

00

Total units to accounted for

18000

00

Units completed and transferred out

15000

00

Units in process, 31 August

30000

0

Total units to accounted for

18000

00

B.

Physical

flow

Equivalent

units Cabinets

Equivalent units

Components

Equivalent units

Conversion costs

Units completed and transferred out 1500000 1500000 1500000 1500000

Units in process, 31 August 300000 300000 300000 60000

Total units to accounted for 1800000 1800000 1800000 1560000

C.

Cost to be accounted for Cabinets Components Conversion costs Total

Cost of Units in process, 1 August

$1,200,000.0

0 $12,600,000.00 $5,400,000.00

$19,200,000.0

0

Costs added during August

$2,400,000.0

0 $25,200,000.00 $8,640,000.00

$36,240,000.0

0

Total cost

$3,600,000.0

0 $37,800,000.00 $14,040,000.00

$55,440,000.0

0

Total units to accounted for 1,800,000 1,800,000 1,560,000

Cost per unit $2.00 $21.00 $9.00 $32.00

D.

Cost of units transferred out Cabinets Components Conversion costs Total

Number of Equivalent units 1500000 1500000 1500000

Per Equivalent Unit cost $2.00 $21.00 $9.00

Cost of units transferred out $3,000,000.00 $31,500,000.00 $13,500,000.00 $48,000,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of ending WIP inventory Cabinets Components Conversion costs Total

Number of Equivalent units 300000 300000 60000

Per Equivalent Unit cost $2.00 $21.00 $9.00

Cost of units transferred out $600,000.00 $6,300,000.00 $540,000.00 $7,440,000.00

E.

Cost to be accounted for

Cost of Units in process, 1 August $ 19,200,000.00

Costs added during August $ 36,240,000.00

Total cost to be accounted for $ 55,440,000.00

Cost accounted for

Cost of units transferred out $ 48,000,000.00

cost of ending WIP inventory $ 7,440,000.00

Total Cost accounted for $ 55,440,000.00

Question 2

A.

Financial issues

Cost of setting up of the factory at in the East Asia for making preliminary processing of spices

is $1.2 million. The company needs to take consideration required cost, available funding options

and cost of funding.

The company is having the benefit of $0.22 per kilogram of spice processing in East Asia in

comparison of Gold Coast because processing cost at Gold Coast is $0.33 per kilogram and

processing cost in the proposed setup is $0.11 per kilogram.

Environmental issues

Current facility of the company is meeting governmental environmental standards but the

company is having some problems due to complaints of neighbors, this can be reduced by

implementing a new facility which will inure running cost of $17500 and implementation cost of

$29000.

Social issues

The company is paying only $3 per hour to the employees however due to long hour work in the

comical fumes employees may get problems in their lungs. Hence company should either make

some provisions for retrenchment compensation for medical expenses of employees or to give

them basic health related facilities or provide them periodic medical compensation.

Number of Equivalent units 300000 300000 60000

Per Equivalent Unit cost $2.00 $21.00 $9.00

Cost of units transferred out $600,000.00 $6,300,000.00 $540,000.00 $7,440,000.00

E.

Cost to be accounted for

Cost of Units in process, 1 August $ 19,200,000.00

Costs added during August $ 36,240,000.00

Total cost to be accounted for $ 55,440,000.00

Cost accounted for

Cost of units transferred out $ 48,000,000.00

cost of ending WIP inventory $ 7,440,000.00

Total Cost accounted for $ 55,440,000.00

Question 2

A.

Financial issues

Cost of setting up of the factory at in the East Asia for making preliminary processing of spices

is $1.2 million. The company needs to take consideration required cost, available funding options

and cost of funding.

The company is having the benefit of $0.22 per kilogram of spice processing in East Asia in

comparison of Gold Coast because processing cost at Gold Coast is $0.33 per kilogram and

processing cost in the proposed setup is $0.11 per kilogram.

Environmental issues

Current facility of the company is meeting governmental environmental standards but the

company is having some problems due to complaints of neighbors, this can be reduced by

implementing a new facility which will inure running cost of $17500 and implementation cost of

$29000.

Social issues

The company is paying only $3 per hour to the employees however due to long hour work in the

comical fumes employees may get problems in their lungs. Hence company should either make

some provisions for retrenchment compensation for medical expenses of employees or to give

them basic health related facilities or provide them periodic medical compensation.

The company is having some problem with the 12 staff members of production wing this

problem can be reduced by either incurring cost of $285000 as redundancy cost or $43000 cost

for a mediator between staff and management. The company should also consider idf these 12

staff members will be retrenched with dissatisfaction then it will impact company’s social and

environmental report.

Economic issues

Company’s quality manager is expected to have reputation enhancement due to the implication

of new facility for the filtering system.

B.

In addition to above, specified factors company should also consider following factors,

Quality of product emerged from pre-processing either at Gold Coast or at East Asia will remain

same hence company should not consider quality factors.

Import export rules and other governmental and political rules will impact the transfer cost of

pre-processed spices from East Asia to Gold Coast. In addition, to transfer cost, it will also

impact other things like quantity etc.

The company should also consider the wrong stories published by the local newspaper which

incurs a reputational loss for the company.

Question 3

A.

problem can be reduced by either incurring cost of $285000 as redundancy cost or $43000 cost

for a mediator between staff and management. The company should also consider idf these 12

staff members will be retrenched with dissatisfaction then it will impact company’s social and

environmental report.

Economic issues

Company’s quality manager is expected to have reputation enhancement due to the implication

of new facility for the filtering system.

B.

In addition to above, specified factors company should also consider following factors,

Quality of product emerged from pre-processing either at Gold Coast or at East Asia will remain

same hence company should not consider quality factors.

Import export rules and other governmental and political rules will impact the transfer cost of

pre-processed spices from East Asia to Gold Coast. In addition, to transfer cost, it will also

impact other things like quantity etc.

The company should also consider the wrong stories published by the local newspaper which

incurs a reputational loss for the company.

Question 3

A.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

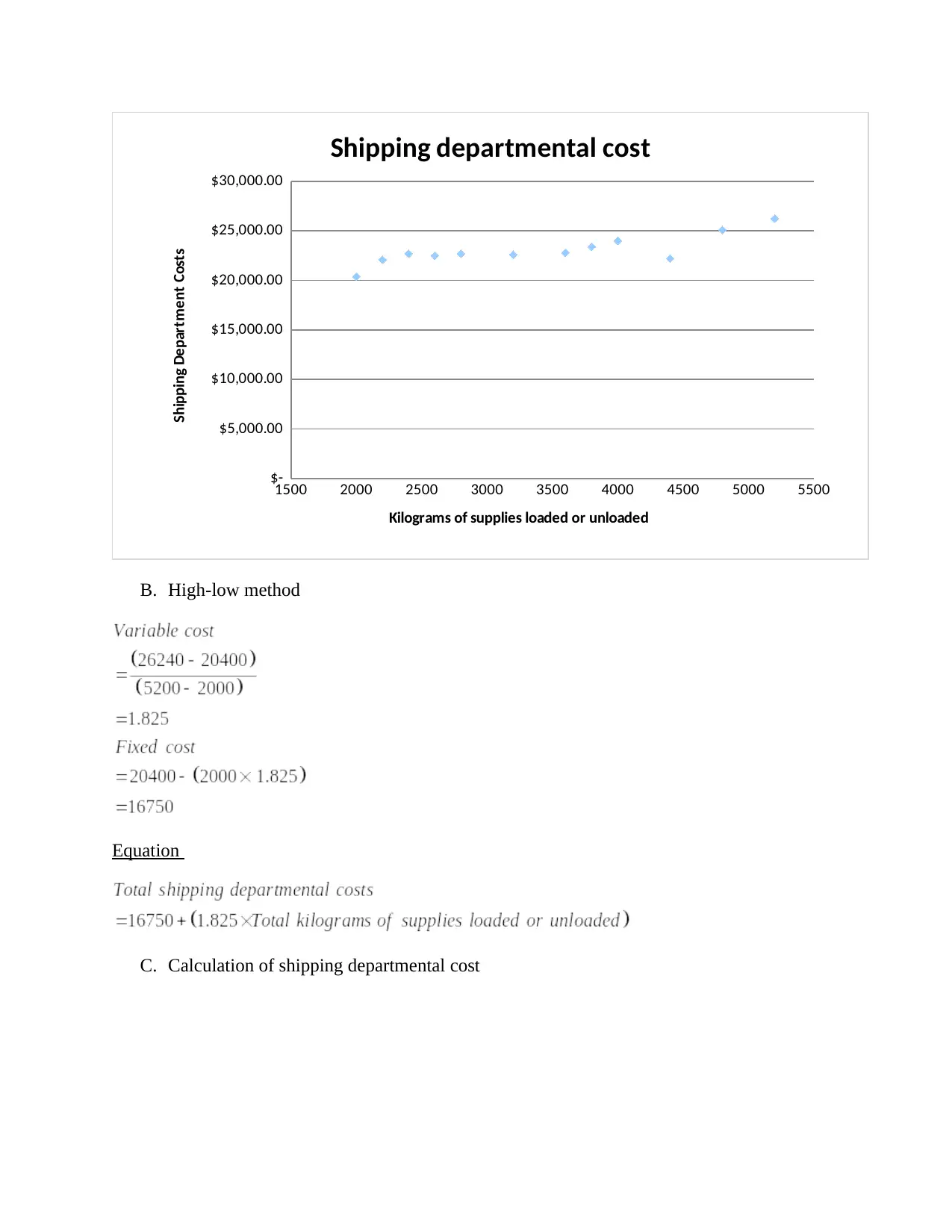

1500 2000 2500 3000 3500 4000 4500 5000 5500

$-

$5,000.00

$10,000.00

$15,000.00

$20,000.00

$25,000.00

$30,000.00

Shipping departmental cost

Kilograms of supplies loaded or unloaded

Shipping Department Costs

B. High-low method

Equation

C. Calculation of shipping departmental cost

$-

$5,000.00

$10,000.00

$15,000.00

$20,000.00

$25,000.00

$30,000.00

Shipping departmental cost

Kilograms of supplies loaded or unloaded

Shipping Department Costs

B. High-low method

Equation

C. Calculation of shipping departmental cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

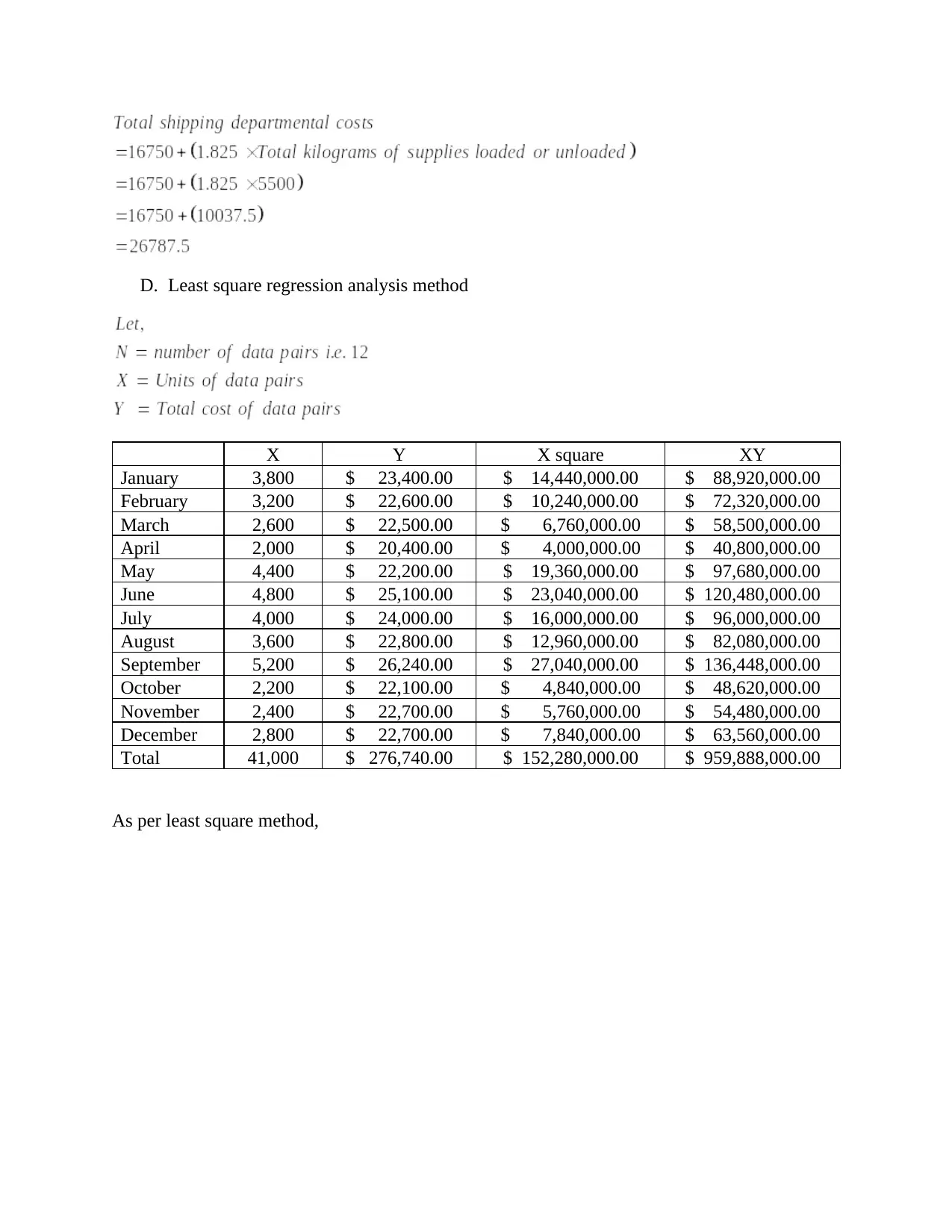

D. Least square regression analysis method

X Y X square XY

January 3,800 $ 23,400.00 $ 14,440,000.00 $ 88,920,000.00

February 3,200 $ 22,600.00 $ 10,240,000.00 $ 72,320,000.00

March 2,600 $ 22,500.00 $ 6,760,000.00 $ 58,500,000.00

April 2,000 $ 20,400.00 $ 4,000,000.00 $ 40,800,000.00

May 4,400 $ 22,200.00 $ 19,360,000.00 $ 97,680,000.00

June 4,800 $ 25,100.00 $ 23,040,000.00 $ 120,480,000.00

July 4,000 $ 24,000.00 $ 16,000,000.00 $ 96,000,000.00

August 3,600 $ 22,800.00 $ 12,960,000.00 $ 82,080,000.00

September 5,200 $ 26,240.00 $ 27,040,000.00 $ 136,448,000.00

October 2,200 $ 22,100.00 $ 4,840,000.00 $ 48,620,000.00

November 2,400 $ 22,700.00 $ 5,760,000.00 $ 54,480,000.00

December 2,800 $ 22,700.00 $ 7,840,000.00 $ 63,560,000.00

Total 41,000 $ 276,740.00 $ 152,280,000.00 $ 959,888,000.00

As per least square method,

X Y X square XY

January 3,800 $ 23,400.00 $ 14,440,000.00 $ 88,920,000.00

February 3,200 $ 22,600.00 $ 10,240,000.00 $ 72,320,000.00

March 2,600 $ 22,500.00 $ 6,760,000.00 $ 58,500,000.00

April 2,000 $ 20,400.00 $ 4,000,000.00 $ 40,800,000.00

May 4,400 $ 22,200.00 $ 19,360,000.00 $ 97,680,000.00

June 4,800 $ 25,100.00 $ 23,040,000.00 $ 120,480,000.00

July 4,000 $ 24,000.00 $ 16,000,000.00 $ 96,000,000.00

August 3,600 $ 22,800.00 $ 12,960,000.00 $ 82,080,000.00

September 5,200 $ 26,240.00 $ 27,040,000.00 $ 136,448,000.00

October 2,200 $ 22,100.00 $ 4,840,000.00 $ 48,620,000.00

November 2,400 $ 22,700.00 $ 5,760,000.00 $ 54,480,000.00

December 2,800 $ 22,700.00 $ 7,840,000.00 $ 63,560,000.00

Total 41,000 $ 276,740.00 $ 152,280,000.00 $ 959,888,000.00

As per least square method,

E. Equation

F. Calculation of shipping departmental cost

G. Cost predictions estimated under high low method and a regression method is different

because these methods consider different data. The high low method takes into account

only data values showing highest and lowest volume (Bamber et al., 2008) but regression

method takes into account all data values.

Moreover, the comparison between these two methods concludes that regression method

is better than the high low method because regression method takes into account all data

values, in turn, it is likely to give precise results.

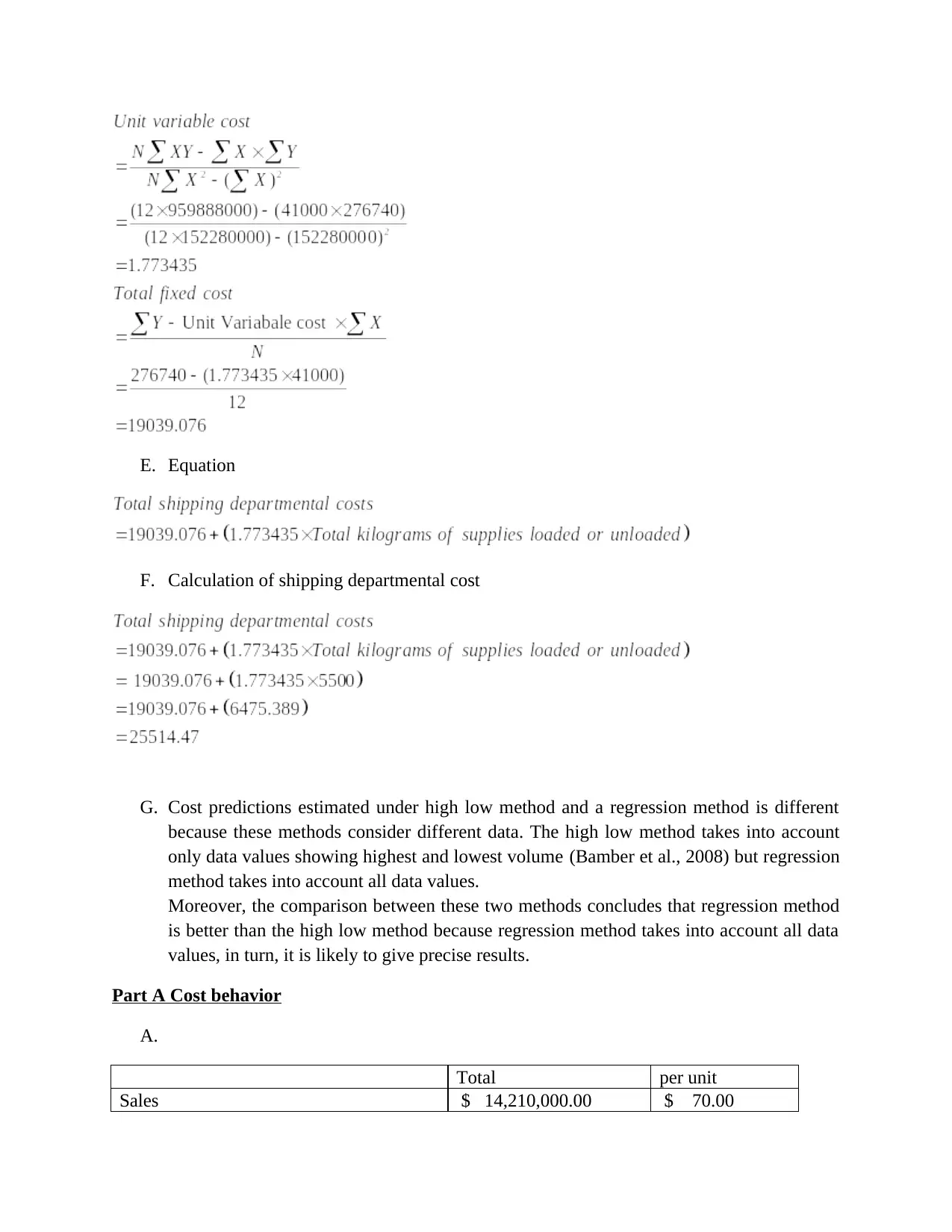

Part A Cost behavior

A.

Total per unit

Sales $ 14,210,000.00 $ 70.00

F. Calculation of shipping departmental cost

G. Cost predictions estimated under high low method and a regression method is different

because these methods consider different data. The high low method takes into account

only data values showing highest and lowest volume (Bamber et al., 2008) but regression

method takes into account all data values.

Moreover, the comparison between these two methods concludes that regression method

is better than the high low method because regression method takes into account all data

values, in turn, it is likely to give precise results.

Part A Cost behavior

A.

Total per unit

Sales $ 14,210,000.00 $ 70.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable cost $ 8,120,000.00 $ 40.00

Fixed cost $ 4,945,000.00

Contribution per unit (Sales-variable cost) $ 30.00

Break even number of units (Fixed cost/ contribution per unit) 164833.33

Contribution margin ratio (contribution/ sales) 42.86%

Break even sales revenue (fixed cost/ contribution margin ratio) $ 11,538,333.33

B.

Present Proposed

Sales $ 14,210,000.00 $ 15,210,000.00

Total variable cost $ 8,120,000.00 $ 8,691,428.57

Contribution $ 6,090,000.00 $ 6,518,571.43

Fixed cost $ 4,945,000.00 $ 5,195,000.00

Operating income $ 1,145,000.00 $ 1,323,571.43

Increase in operating income $ 178,571.43

% increase in operating income 15.60%

C. If sales revenue will increase by $1,500,000 then variable cost will also increase by

57.14% of $1,500,000 i.e. $857,142.86. In turn, the contribution will increase by

$642,157.14. Fixed cost will remain fixed hence operating income will increase by

$642,157.14.

D.

Sales $ 14,210,000.00

Less: Break even sales revenue $ 11,538,333.33

Margin of safety $ 2,671,666.67

E.

Contribution margin $ 6,090,000.00

Operating income $ 1,145,000.00

Operating leverage (contribution margin/ Operating income) 5.318777293

Contribution margin after increase in sale (6090000*1.08) $ 6,577,200.00

Operating income (operating leverage*Contribution margin after increase in sale) $ 1,236,600.00

Increase in operating income (1236600-1145000) $ 91,600.00

Part B Income statements under absorption costing and variable costing

Fixed cost $ 4,945,000.00

Contribution per unit (Sales-variable cost) $ 30.00

Break even number of units (Fixed cost/ contribution per unit) 164833.33

Contribution margin ratio (contribution/ sales) 42.86%

Break even sales revenue (fixed cost/ contribution margin ratio) $ 11,538,333.33

B.

Present Proposed

Sales $ 14,210,000.00 $ 15,210,000.00

Total variable cost $ 8,120,000.00 $ 8,691,428.57

Contribution $ 6,090,000.00 $ 6,518,571.43

Fixed cost $ 4,945,000.00 $ 5,195,000.00

Operating income $ 1,145,000.00 $ 1,323,571.43

Increase in operating income $ 178,571.43

% increase in operating income 15.60%

C. If sales revenue will increase by $1,500,000 then variable cost will also increase by

57.14% of $1,500,000 i.e. $857,142.86. In turn, the contribution will increase by

$642,157.14. Fixed cost will remain fixed hence operating income will increase by

$642,157.14.

D.

Sales $ 14,210,000.00

Less: Break even sales revenue $ 11,538,333.33

Margin of safety $ 2,671,666.67

E.

Contribution margin $ 6,090,000.00

Operating income $ 1,145,000.00

Operating leverage (contribution margin/ Operating income) 5.318777293

Contribution margin after increase in sale (6090000*1.08) $ 6,577,200.00

Operating income (operating leverage*Contribution margin after increase in sale) $ 1,236,600.00

Increase in operating income (1236600-1145000) $ 91,600.00

Part B Income statements under absorption costing and variable costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

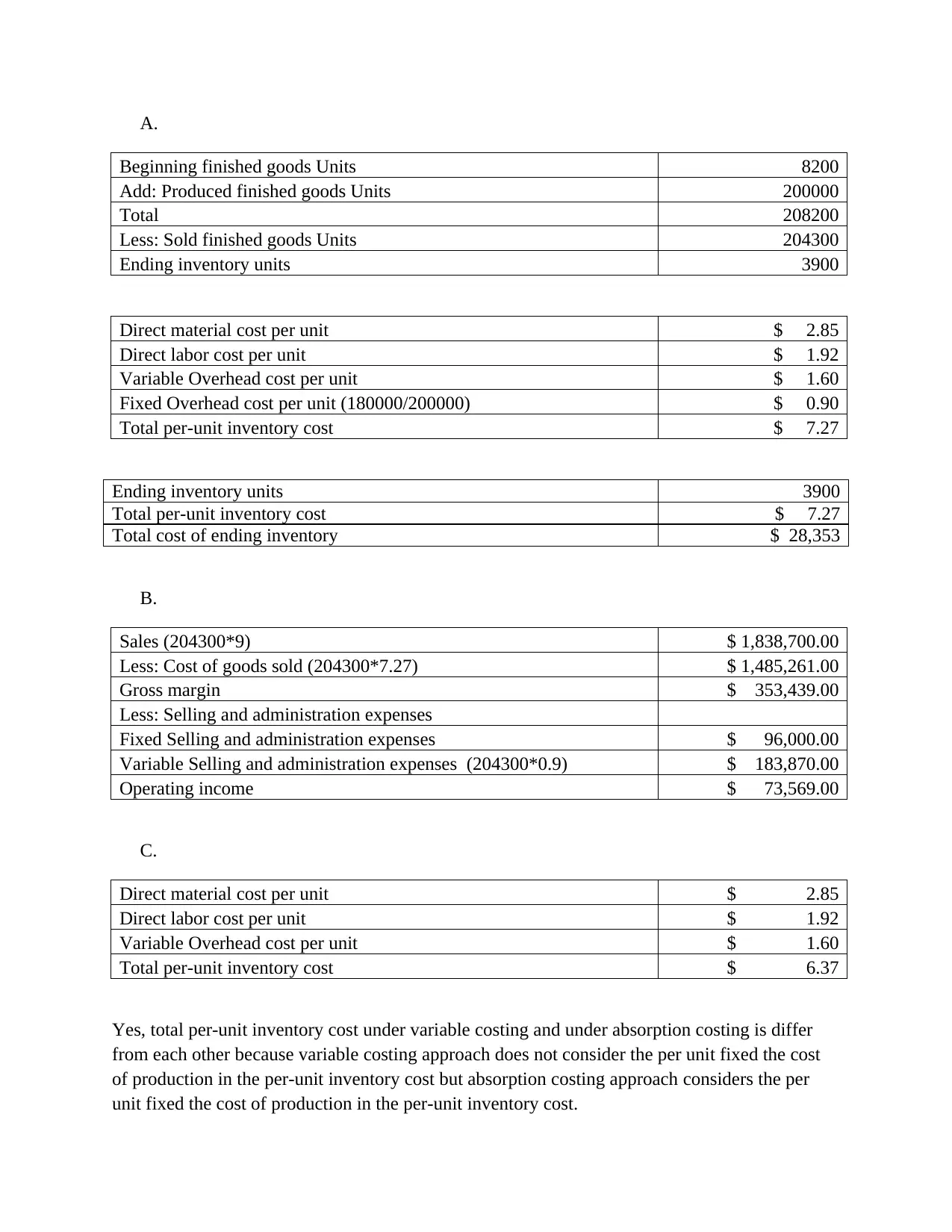

A.

Beginning finished goods Units 8200

Add: Produced finished goods Units 200000

Total 208200

Less: Sold finished goods Units 204300

Ending inventory units 3900

Direct material cost per unit $ 2.85

Direct labor cost per unit $ 1.92

Variable Overhead cost per unit $ 1.60

Fixed Overhead cost per unit (180000/200000) $ 0.90

Total per-unit inventory cost $ 7.27

Ending inventory units 3900

Total per-unit inventory cost $ 7.27

Total cost of ending inventory $ 28,353

B.

Sales (204300*9) $ 1,838,700.00

Less: Cost of goods sold (204300*7.27) $ 1,485,261.00

Gross margin $ 353,439.00

Less: Selling and administration expenses

Fixed Selling and administration expenses $ 96,000.00

Variable Selling and administration expenses (204300*0.9) $ 183,870.00

Operating income $ 73,569.00

C.

Direct material cost per unit $ 2.85

Direct labor cost per unit $ 1.92

Variable Overhead cost per unit $ 1.60

Total per-unit inventory cost $ 6.37

Yes, total per-unit inventory cost under variable costing and under absorption costing is differ

from each other because variable costing approach does not consider the per unit fixed the cost

of production in the per-unit inventory cost but absorption costing approach considers the per

unit fixed the cost of production in the per-unit inventory cost.

Beginning finished goods Units 8200

Add: Produced finished goods Units 200000

Total 208200

Less: Sold finished goods Units 204300

Ending inventory units 3900

Direct material cost per unit $ 2.85

Direct labor cost per unit $ 1.92

Variable Overhead cost per unit $ 1.60

Fixed Overhead cost per unit (180000/200000) $ 0.90

Total per-unit inventory cost $ 7.27

Ending inventory units 3900

Total per-unit inventory cost $ 7.27

Total cost of ending inventory $ 28,353

B.

Sales (204300*9) $ 1,838,700.00

Less: Cost of goods sold (204300*7.27) $ 1,485,261.00

Gross margin $ 353,439.00

Less: Selling and administration expenses

Fixed Selling and administration expenses $ 96,000.00

Variable Selling and administration expenses (204300*0.9) $ 183,870.00

Operating income $ 73,569.00

C.

Direct material cost per unit $ 2.85

Direct labor cost per unit $ 1.92

Variable Overhead cost per unit $ 1.60

Total per-unit inventory cost $ 6.37

Yes, total per-unit inventory cost under variable costing and under absorption costing is differ

from each other because variable costing approach does not consider the per unit fixed the cost

of production in the per-unit inventory cost but absorption costing approach considers the per

unit fixed the cost of production in the per-unit inventory cost.

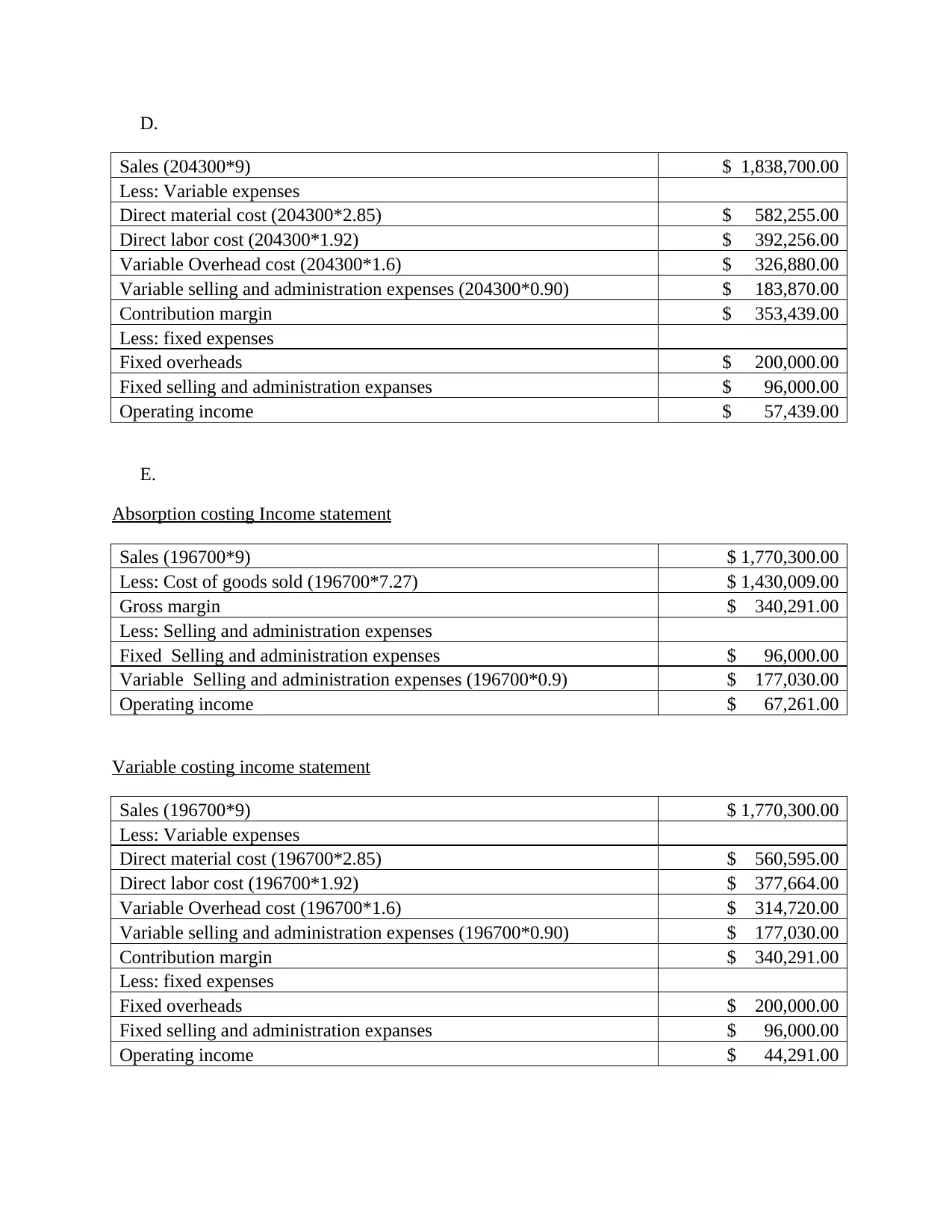

D.

Sales (204300*9) $ 1,838,700.00

Less: Variable expenses

Direct material cost (204300*2.85) $ 582,255.00

Direct labor cost (204300*1.92) $ 392,256.00

Variable Overhead cost (204300*1.6) $ 326,880.00

Variable selling and administration expenses (204300*0.90) $ 183,870.00

Contribution margin $ 353,439.00

Less: fixed expenses

Fixed overheads $ 200,000.00

Fixed selling and administration expanses $ 96,000.00

Operating income $ 57,439.00

E.

Absorption costing Income statement

Sales (196700*9) $ 1,770,300.00

Less: Cost of goods sold (196700*7.27) $ 1,430,009.00

Gross margin $ 340,291.00

Less: Selling and administration expenses

Fixed Selling and administration expenses $ 96,000.00

Variable Selling and administration expenses (196700*0.9) $ 177,030.00

Operating income $ 67,261.00

Variable costing income statement

Sales (196700*9) $ 1,770,300.00

Less: Variable expenses

Direct material cost (196700*2.85) $ 560,595.00

Direct labor cost (196700*1.92) $ 377,664.00

Variable Overhead cost (196700*1.6) $ 314,720.00

Variable selling and administration expenses (196700*0.90) $ 177,030.00

Contribution margin $ 340,291.00

Less: fixed expenses

Fixed overheads $ 200,000.00

Fixed selling and administration expanses $ 96,000.00

Operating income $ 44,291.00

Sales (204300*9) $ 1,838,700.00

Less: Variable expenses

Direct material cost (204300*2.85) $ 582,255.00

Direct labor cost (204300*1.92) $ 392,256.00

Variable Overhead cost (204300*1.6) $ 326,880.00

Variable selling and administration expenses (204300*0.90) $ 183,870.00

Contribution margin $ 353,439.00

Less: fixed expenses

Fixed overheads $ 200,000.00

Fixed selling and administration expanses $ 96,000.00

Operating income $ 57,439.00

E.

Absorption costing Income statement

Sales (196700*9) $ 1,770,300.00

Less: Cost of goods sold (196700*7.27) $ 1,430,009.00

Gross margin $ 340,291.00

Less: Selling and administration expenses

Fixed Selling and administration expenses $ 96,000.00

Variable Selling and administration expenses (196700*0.9) $ 177,030.00

Operating income $ 67,261.00

Variable costing income statement

Sales (196700*9) $ 1,770,300.00

Less: Variable expenses

Direct material cost (196700*2.85) $ 560,595.00

Direct labor cost (196700*1.92) $ 377,664.00

Variable Overhead cost (196700*1.6) $ 314,720.00

Variable selling and administration expenses (196700*0.90) $ 177,030.00

Contribution margin $ 340,291.00

Less: fixed expenses

Fixed overheads $ 200,000.00

Fixed selling and administration expanses $ 96,000.00

Operating income $ 44,291.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

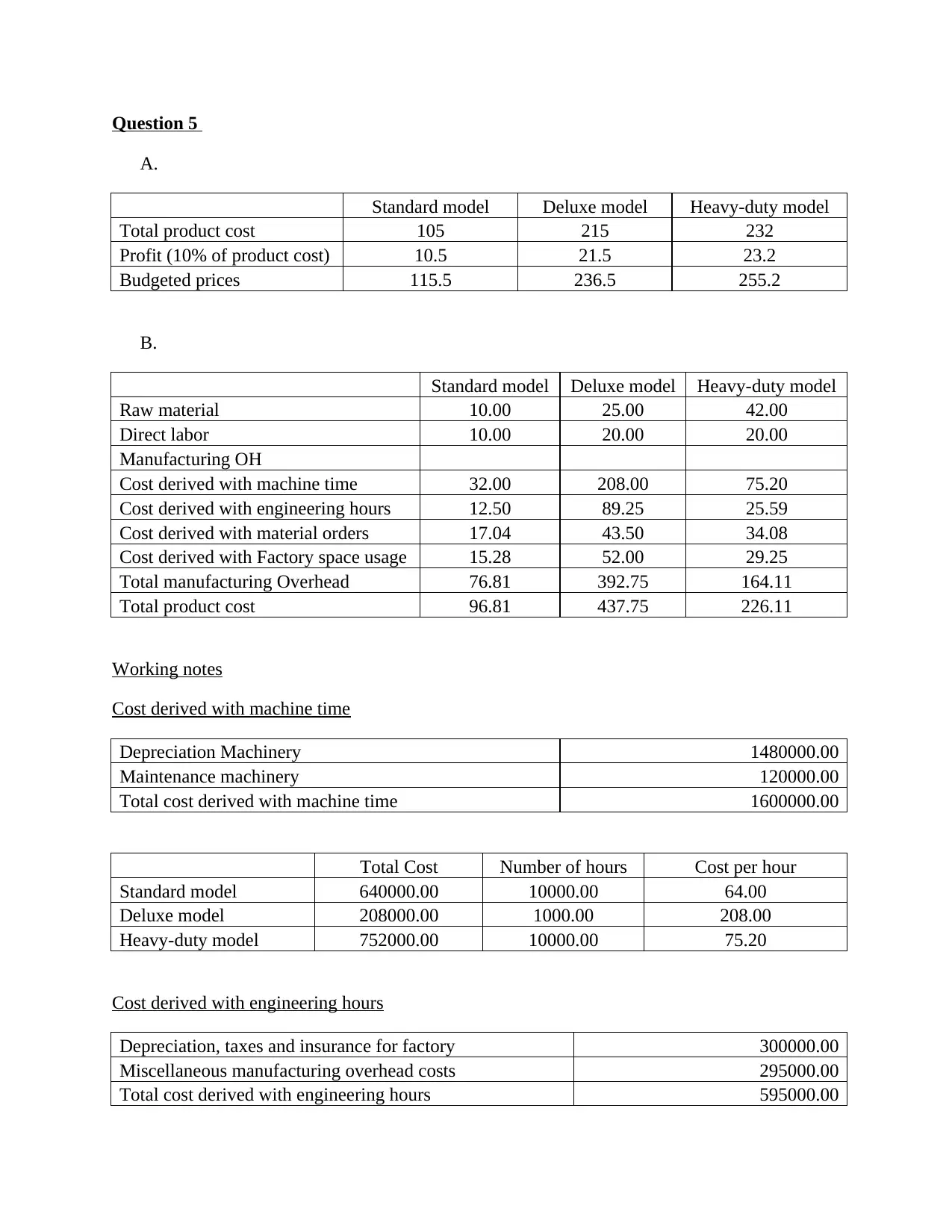

Question 5

A.

Standard model Deluxe model Heavy-duty model

Total product cost 105 215 232

Profit (10% of product cost) 10.5 21.5 23.2

Budgeted prices 115.5 236.5 255.2

B.

Standard model Deluxe model Heavy-duty model

Raw material 10.00 25.00 42.00

Direct labor 10.00 20.00 20.00

Manufacturing OH

Cost derived with machine time 32.00 208.00 75.20

Cost derived with engineering hours 12.50 89.25 25.59

Cost derived with material orders 17.04 43.50 34.08

Cost derived with Factory space usage 15.28 52.00 29.25

Total manufacturing Overhead 76.81 392.75 164.11

Total product cost 96.81 437.75 226.11

Working notes

Cost derived with machine time

Depreciation Machinery 1480000.00

Maintenance machinery 120000.00

Total cost derived with machine time 1600000.00

Total Cost Number of hours Cost per hour

Standard model 640000.00 10000.00 64.00

Deluxe model 208000.00 1000.00 208.00

Heavy-duty model 752000.00 10000.00 75.20

Cost derived with engineering hours

Depreciation, taxes and insurance for factory 300000.00

Miscellaneous manufacturing overhead costs 295000.00

Total cost derived with engineering hours 595000.00

A.

Standard model Deluxe model Heavy-duty model

Total product cost 105 215 232

Profit (10% of product cost) 10.5 21.5 23.2

Budgeted prices 115.5 236.5 255.2

B.

Standard model Deluxe model Heavy-duty model

Raw material 10.00 25.00 42.00

Direct labor 10.00 20.00 20.00

Manufacturing OH

Cost derived with machine time 32.00 208.00 75.20

Cost derived with engineering hours 12.50 89.25 25.59

Cost derived with material orders 17.04 43.50 34.08

Cost derived with Factory space usage 15.28 52.00 29.25

Total manufacturing Overhead 76.81 392.75 164.11

Total product cost 96.81 437.75 226.11

Working notes

Cost derived with machine time

Depreciation Machinery 1480000.00

Maintenance machinery 120000.00

Total cost derived with machine time 1600000.00

Total Cost Number of hours Cost per hour

Standard model 640000.00 10000.00 64.00

Deluxe model 208000.00 1000.00 208.00

Heavy-duty model 752000.00 10000.00 75.20

Cost derived with engineering hours

Depreciation, taxes and insurance for factory 300000.00

Miscellaneous manufacturing overhead costs 295000.00

Total cost derived with engineering hours 595000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

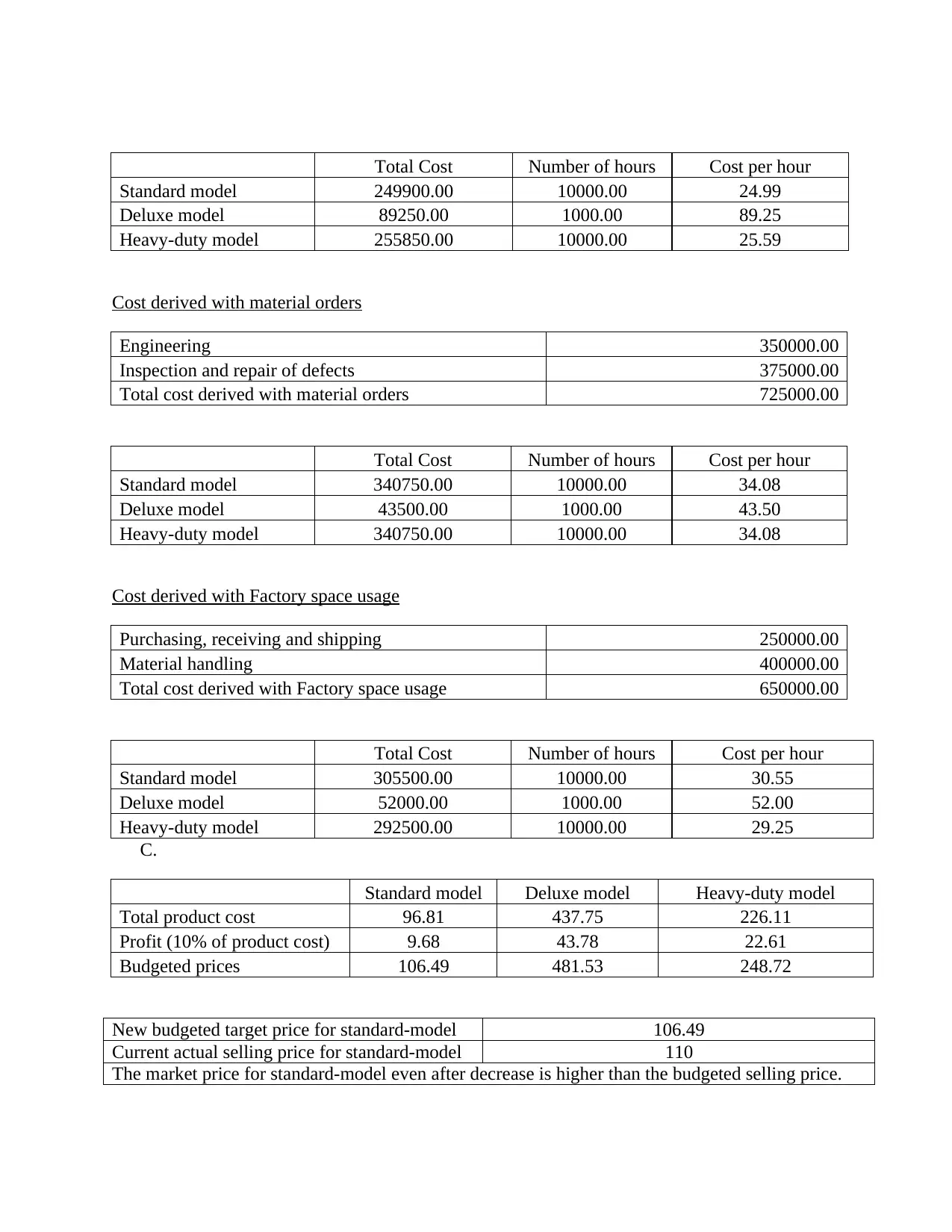

Total Cost Number of hours Cost per hour

Standard model 249900.00 10000.00 24.99

Deluxe model 89250.00 1000.00 89.25

Heavy-duty model 255850.00 10000.00 25.59

Cost derived with material orders

Engineering 350000.00

Inspection and repair of defects 375000.00

Total cost derived with material orders 725000.00

Total Cost Number of hours Cost per hour

Standard model 340750.00 10000.00 34.08

Deluxe model 43500.00 1000.00 43.50

Heavy-duty model 340750.00 10000.00 34.08

Cost derived with Factory space usage

Purchasing, receiving and shipping 250000.00

Material handling 400000.00

Total cost derived with Factory space usage 650000.00

Total Cost Number of hours Cost per hour

Standard model 305500.00 10000.00 30.55

Deluxe model 52000.00 1000.00 52.00

Heavy-duty model 292500.00 10000.00 29.25

C.

Standard model Deluxe model Heavy-duty model

Total product cost 96.81 437.75 226.11

Profit (10% of product cost) 9.68 43.78 22.61

Budgeted prices 106.49 481.53 248.72

New budgeted target price for standard-model 106.49

Current actual selling price for standard-model 110

The market price for standard-model even after decrease is higher than the budgeted selling price.

Standard model 249900.00 10000.00 24.99

Deluxe model 89250.00 1000.00 89.25

Heavy-duty model 255850.00 10000.00 25.59

Cost derived with material orders

Engineering 350000.00

Inspection and repair of defects 375000.00

Total cost derived with material orders 725000.00

Total Cost Number of hours Cost per hour

Standard model 340750.00 10000.00 34.08

Deluxe model 43500.00 1000.00 43.50

Heavy-duty model 340750.00 10000.00 34.08

Cost derived with Factory space usage

Purchasing, receiving and shipping 250000.00

Material handling 400000.00

Total cost derived with Factory space usage 650000.00

Total Cost Number of hours Cost per hour

Standard model 305500.00 10000.00 30.55

Deluxe model 52000.00 1000.00 52.00

Heavy-duty model 292500.00 10000.00 29.25

C.

Standard model Deluxe model Heavy-duty model

Total product cost 96.81 437.75 226.11

Profit (10% of product cost) 9.68 43.78 22.61

Budgeted prices 106.49 481.53 248.72

New budgeted target price for standard-model 106.49

Current actual selling price for standard-model 110

The market price for standard-model even after decrease is higher than the budgeted selling price.

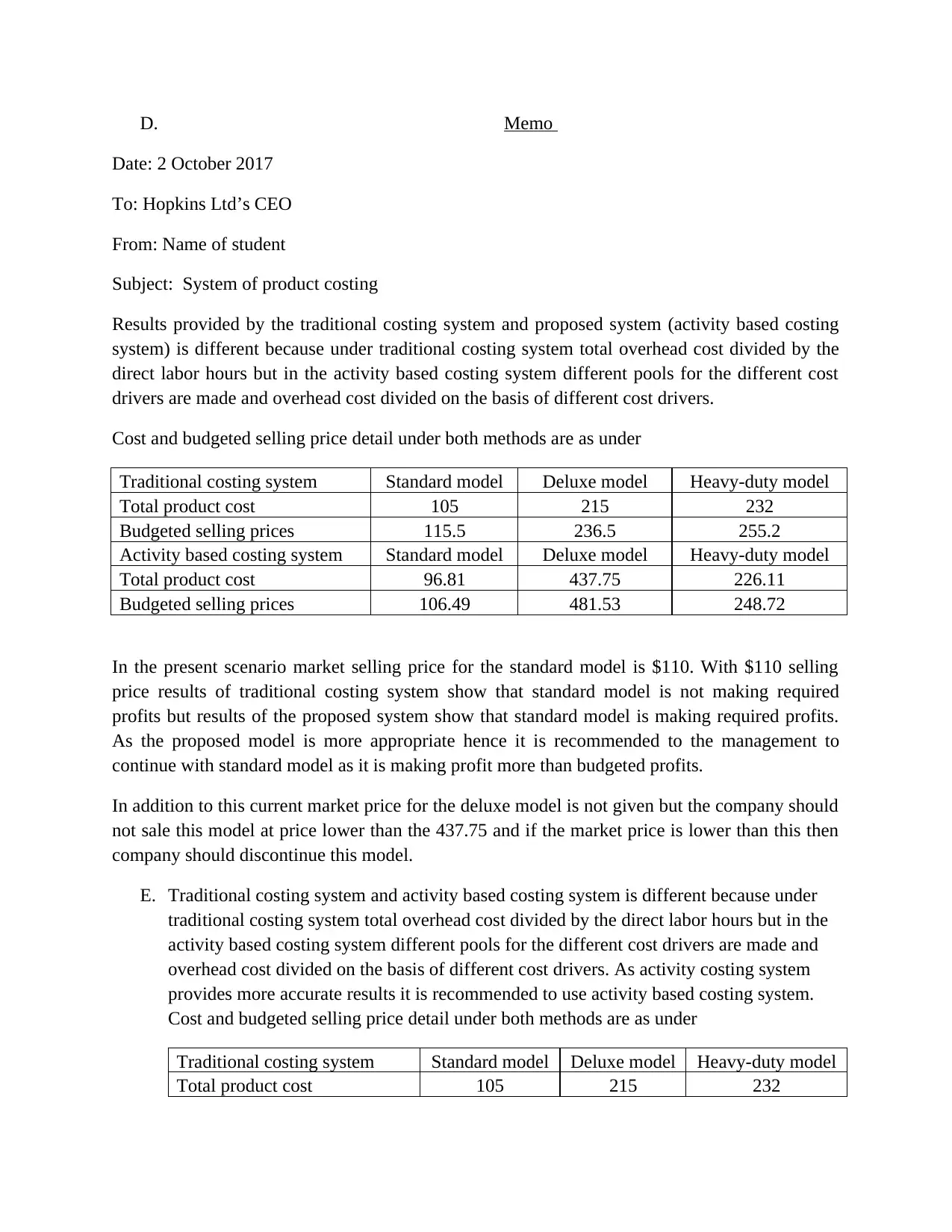

D. Memo

Date: 2 October 2017

To: Hopkins Ltd’s CEO

From: Name of student

Subject: System of product costing

Results provided by the traditional costing system and proposed system (activity based costing

system) is different because under traditional costing system total overhead cost divided by the

direct labor hours but in the activity based costing system different pools for the different cost

drivers are made and overhead cost divided on the basis of different cost drivers.

Cost and budgeted selling price detail under both methods are as under

Traditional costing system Standard model Deluxe model Heavy-duty model

Total product cost 105 215 232

Budgeted selling prices 115.5 236.5 255.2

Activity based costing system Standard model Deluxe model Heavy-duty model

Total product cost 96.81 437.75 226.11

Budgeted selling prices 106.49 481.53 248.72

In the present scenario market selling price for the standard model is $110. With $110 selling

price results of traditional costing system show that standard model is not making required

profits but results of the proposed system show that standard model is making required profits.

As the proposed model is more appropriate hence it is recommended to the management to

continue with standard model as it is making profit more than budgeted profits.

In addition to this current market price for the deluxe model is not given but the company should

not sale this model at price lower than the 437.75 and if the market price is lower than this then

company should discontinue this model.

E. Traditional costing system and activity based costing system is different because under

traditional costing system total overhead cost divided by the direct labor hours but in the

activity based costing system different pools for the different cost drivers are made and

overhead cost divided on the basis of different cost drivers. As activity costing system

provides more accurate results it is recommended to use activity based costing system.

Cost and budgeted selling price detail under both methods are as under

Traditional costing system Standard model Deluxe model Heavy-duty model

Total product cost 105 215 232

Date: 2 October 2017

To: Hopkins Ltd’s CEO

From: Name of student

Subject: System of product costing

Results provided by the traditional costing system and proposed system (activity based costing

system) is different because under traditional costing system total overhead cost divided by the

direct labor hours but in the activity based costing system different pools for the different cost

drivers are made and overhead cost divided on the basis of different cost drivers.

Cost and budgeted selling price detail under both methods are as under

Traditional costing system Standard model Deluxe model Heavy-duty model

Total product cost 105 215 232

Budgeted selling prices 115.5 236.5 255.2

Activity based costing system Standard model Deluxe model Heavy-duty model

Total product cost 96.81 437.75 226.11

Budgeted selling prices 106.49 481.53 248.72

In the present scenario market selling price for the standard model is $110. With $110 selling

price results of traditional costing system show that standard model is not making required

profits but results of the proposed system show that standard model is making required profits.

As the proposed model is more appropriate hence it is recommended to the management to

continue with standard model as it is making profit more than budgeted profits.

In addition to this current market price for the deluxe model is not given but the company should

not sale this model at price lower than the 437.75 and if the market price is lower than this then

company should discontinue this model.

E. Traditional costing system and activity based costing system is different because under

traditional costing system total overhead cost divided by the direct labor hours but in the

activity based costing system different pools for the different cost drivers are made and

overhead cost divided on the basis of different cost drivers. As activity costing system

provides more accurate results it is recommended to use activity based costing system.

Cost and budgeted selling price detail under both methods are as under

Traditional costing system Standard model Deluxe model Heavy-duty model

Total product cost 105 215 232

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.