Bond Valuation: Calculating Price and Yield to Maturity (YTM)

VerifiedAdded on 2022/08/29

|7

|1676

|14

Homework Assignment

AI Summary

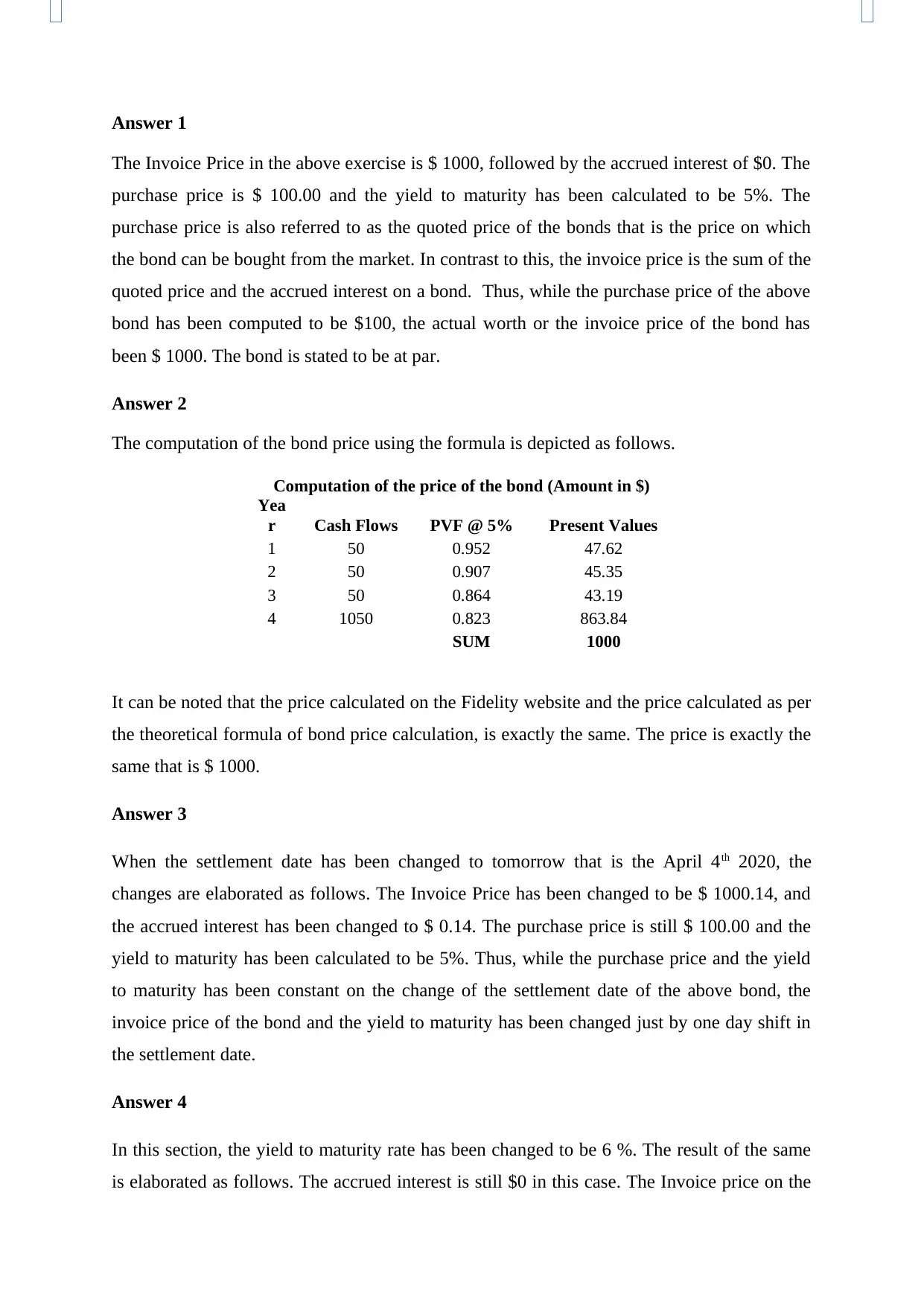

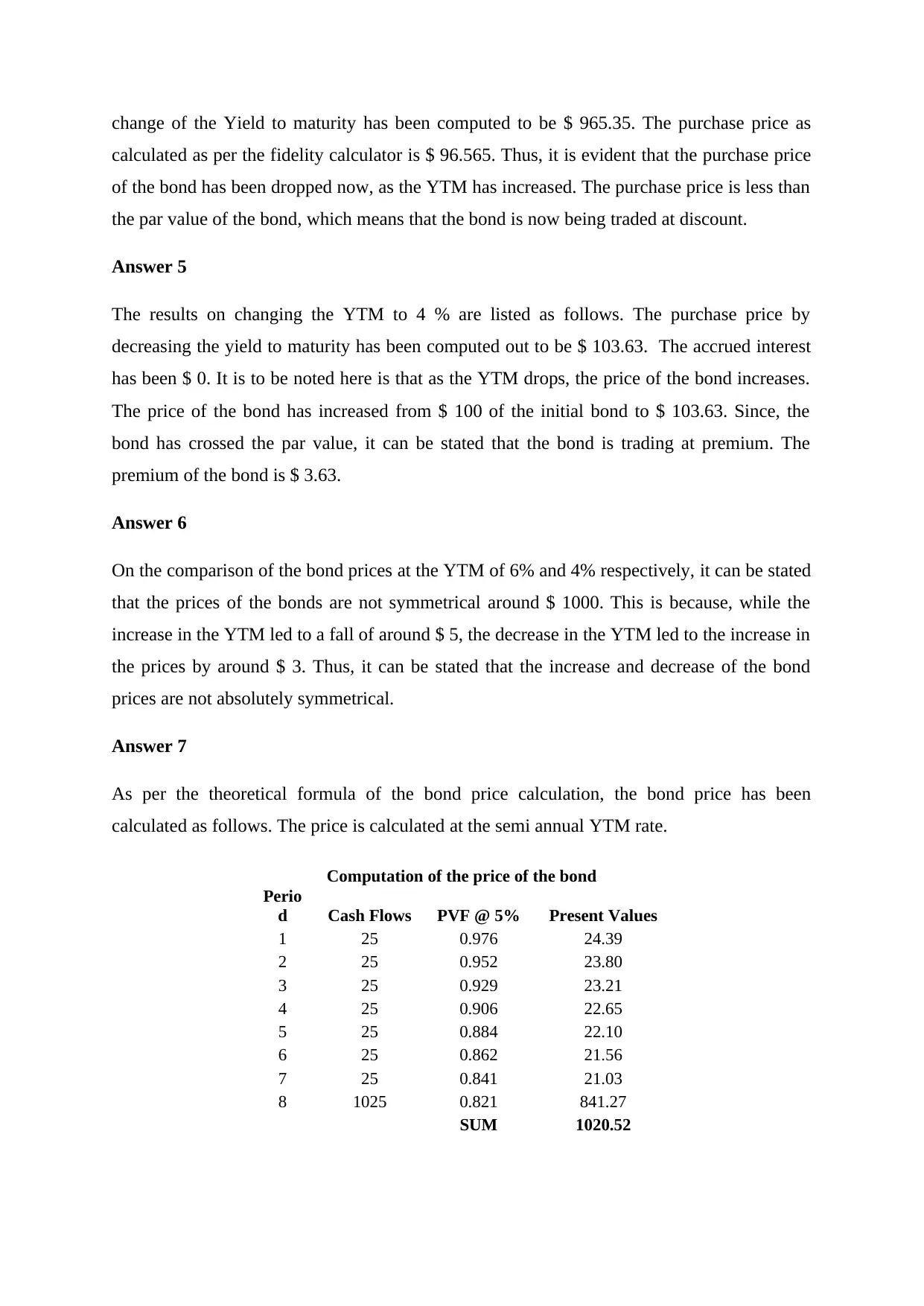

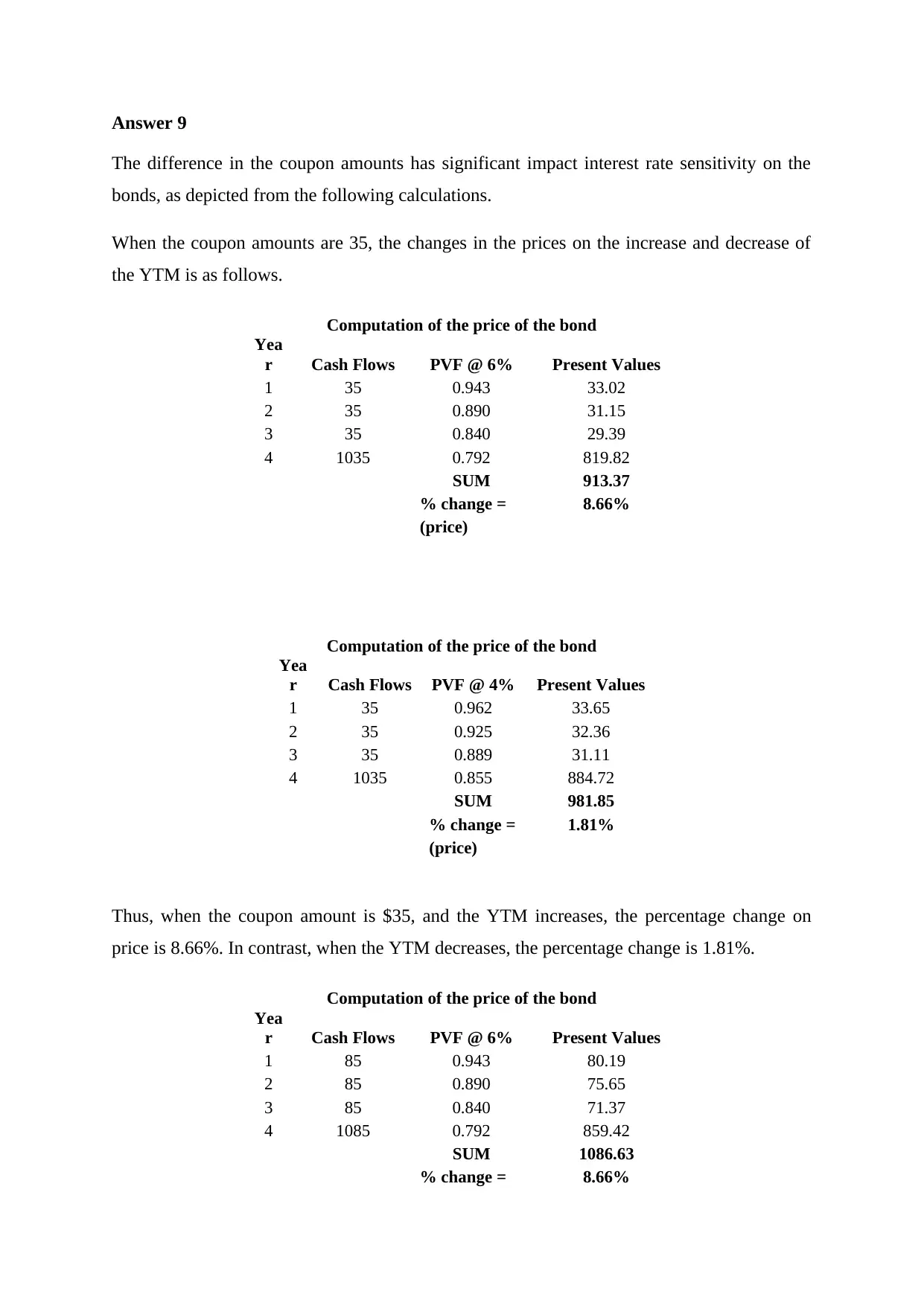

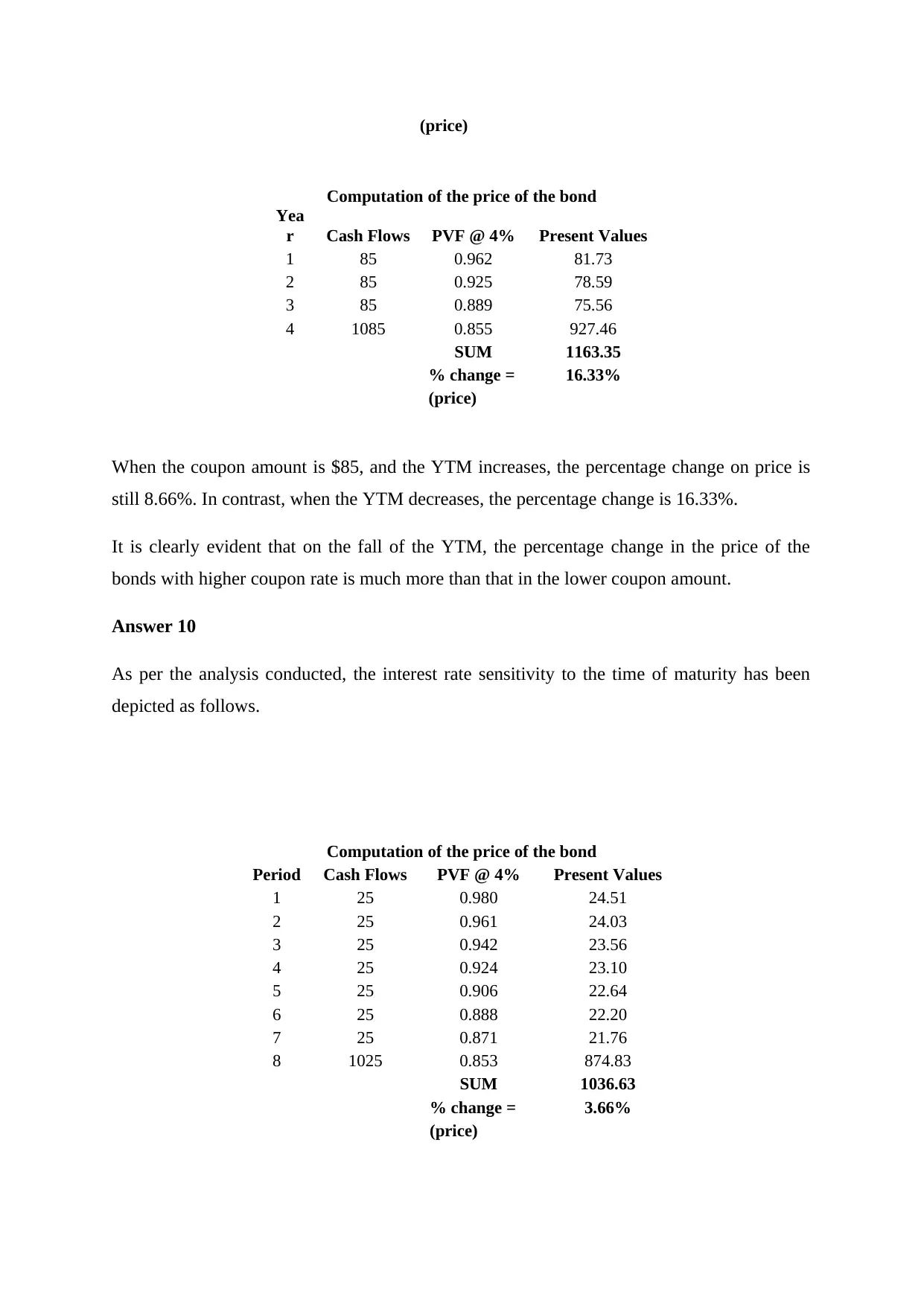

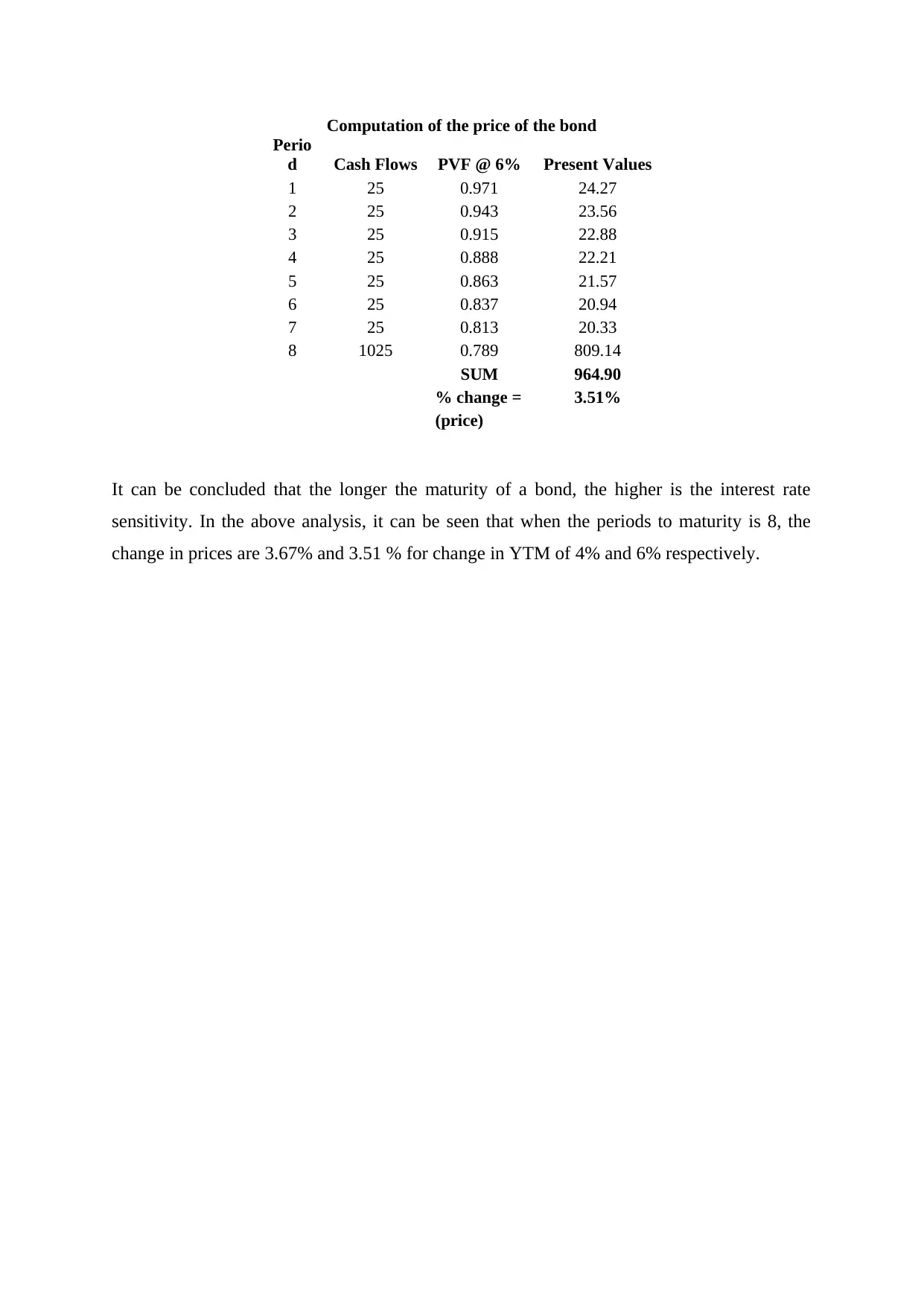

This assignment solution provides a comprehensive analysis of bond valuation and yield to maturity (YTM) using a price/yield calculator. It begins by determining the invoice price, accrued interest, purchase price, and yield to maturity for a bond at par. The solution then calculates the bond price using the present value formula, comparing it with the calculator's result. Further analysis explores the impact of changing the settlement date and the yield to maturity on the bond's invoice and purchase prices, highlighting scenarios where the bond trades at a discount or premium. The assignment also examines the symmetry of bond prices around par value with varying YTMs and calculates bond prices with semi-annual coupon payments. Finally, it investigates the inverse relationship between bond prices and market interest rates, the interest rate sensitivity with varying coupon amounts, and the effect of time to maturity on interest rate sensitivity, illustrating how longer maturities increase sensitivity. This document is available on Desklib, a platform offering a wide range of study tools and solved assignments for students.

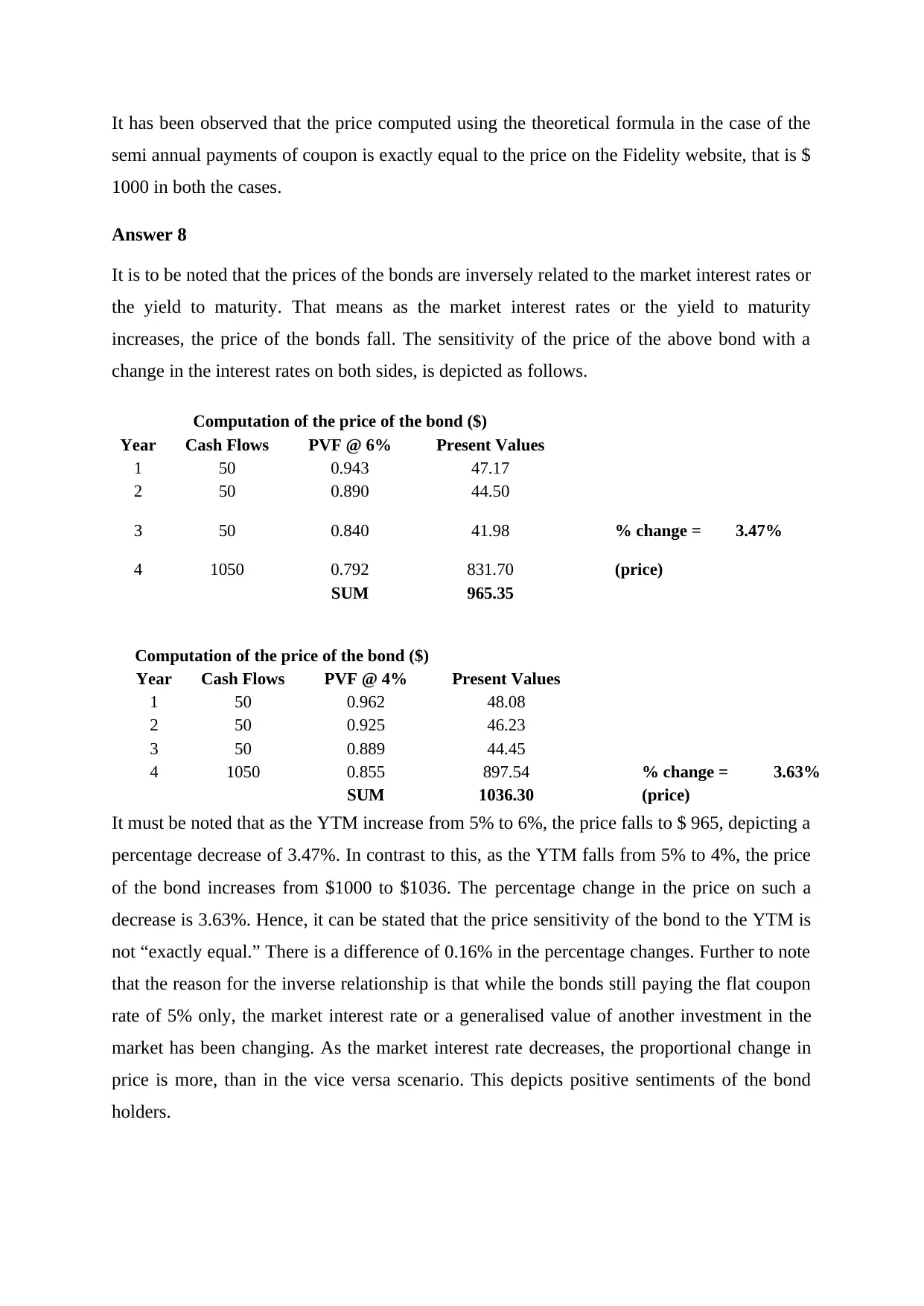

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.