Investment Appraisal, Valuation, and Financial Analysis Assignment

VerifiedAdded on 2022/08/01

|10

|3130

|46

Homework Assignment

AI Summary

This finance assignment solution provides a comprehensive analysis of investment appraisal techniques, valuation methods, and financial analysis. It begins by explaining the use of cash flows over profit in investment decisions, followed by a detailed explanation of relevant and irrelevant cash flows, and the importance of considering inflation. The assignment then delves into the computation of beta and weighted average cost of capital (WACC), including a terminal value calculation. Further, the solution explores economic value, adjusted book value, and various valuation ratios such as EV/EBITDA, price-to-earnings, and price-to-cash-flow ratios, providing detailed calculations and explanations for each. The solution also examines 'make or buy' decisions and how to determine the relevant costs for manufacturing or outsourcing.

Ans 1

(a) Most, if not all finance managers and decision makers use cash flows, instead of profit of a

project for the investment appraisal. Cash flows means the amount of cash that the project

has been able to generate for the entity, whereas, profit refers to the amount that the entity

has earned from the project, whether or not the same has been realised in cash.

Since capital investment required in making a project is huge, management is interested in

the cash that it would be able to generate from the project, before investing in the project.

Cash flows from the project are then used to compute payback period of the project, net

present value of the project.

The major reason for not using profit number for such analysis, could be, profit can be

misleading in scenarios, where the entity has not been able to convert the same in cash and

also, profit is generally impacted by various non-cash expenses such as depreciation, which

should not be considered in investment appraisal (Kengatharan L, 2017).

(b) Investment appraisal is an exercise, whose outcome is, whether or not an investment should

be made in the project being evaluated. In arriving at this answer, investment appraisers use

relevant cash flows from the project, relevant cash flows are the cash flows which would

affect the decision to invest or not to invest in the project. These are cash flows that will

occur to the entity in the future and are incremental in nature, i.e. these cash flows will not

occur if the project is not undertaken by the entity (Relevant cash flows of capital

budgeting).

Irrelevant cash flows, as the name suggests, are cash flows that are not impacted by the

project being undertaken by the management. These are cash flows (both inflows and

outflows), that occur irrespective of the project being undertaken.

(c) Investment appraisal process involves forecasting the revenue and cost relevant to the

project over the useful life of the project, the useful life could be 5 years or 10 or in certain

cases, it could also be 15 years or beyond.

Since the appraisers are required to forecast the cash flows that project would be able to

generate in the future, they are very well required to consider inflation in their analysis.

Inflation will affect both the cost and revenue of the products planned to be manufactured

by the entity, but the degree of impact on both cost and revenue could differ significantly.

(d) ‘Make or buy decision’ involves choosing between manufacturing a product or outsourcing

the production to a third party and procuring the material from the third party.

This decision is driven by the relevant cost for manufacturing the component inhouse or the

landed cost of procuring it from outside. Relevant cost in this case, is the direct cost of

manufacturing the component inhouse, i.e. the cost which is directly attributable to

(a) Most, if not all finance managers and decision makers use cash flows, instead of profit of a

project for the investment appraisal. Cash flows means the amount of cash that the project

has been able to generate for the entity, whereas, profit refers to the amount that the entity

has earned from the project, whether or not the same has been realised in cash.

Since capital investment required in making a project is huge, management is interested in

the cash that it would be able to generate from the project, before investing in the project.

Cash flows from the project are then used to compute payback period of the project, net

present value of the project.

The major reason for not using profit number for such analysis, could be, profit can be

misleading in scenarios, where the entity has not been able to convert the same in cash and

also, profit is generally impacted by various non-cash expenses such as depreciation, which

should not be considered in investment appraisal (Kengatharan L, 2017).

(b) Investment appraisal is an exercise, whose outcome is, whether or not an investment should

be made in the project being evaluated. In arriving at this answer, investment appraisers use

relevant cash flows from the project, relevant cash flows are the cash flows which would

affect the decision to invest or not to invest in the project. These are cash flows that will

occur to the entity in the future and are incremental in nature, i.e. these cash flows will not

occur if the project is not undertaken by the entity (Relevant cash flows of capital

budgeting).

Irrelevant cash flows, as the name suggests, are cash flows that are not impacted by the

project being undertaken by the management. These are cash flows (both inflows and

outflows), that occur irrespective of the project being undertaken.

(c) Investment appraisal process involves forecasting the revenue and cost relevant to the

project over the useful life of the project, the useful life could be 5 years or 10 or in certain

cases, it could also be 15 years or beyond.

Since the appraisers are required to forecast the cash flows that project would be able to

generate in the future, they are very well required to consider inflation in their analysis.

Inflation will affect both the cost and revenue of the products planned to be manufactured

by the entity, but the degree of impact on both cost and revenue could differ significantly.

(d) ‘Make or buy decision’ involves choosing between manufacturing a product or outsourcing

the production to a third party and procuring the material from the third party.

This decision is driven by the relevant cost for manufacturing the component inhouse or the

landed cost of procuring it from outside. Relevant cost in this case, is the direct cost of

manufacturing the component inhouse, i.e. the cost which is directly attributable to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

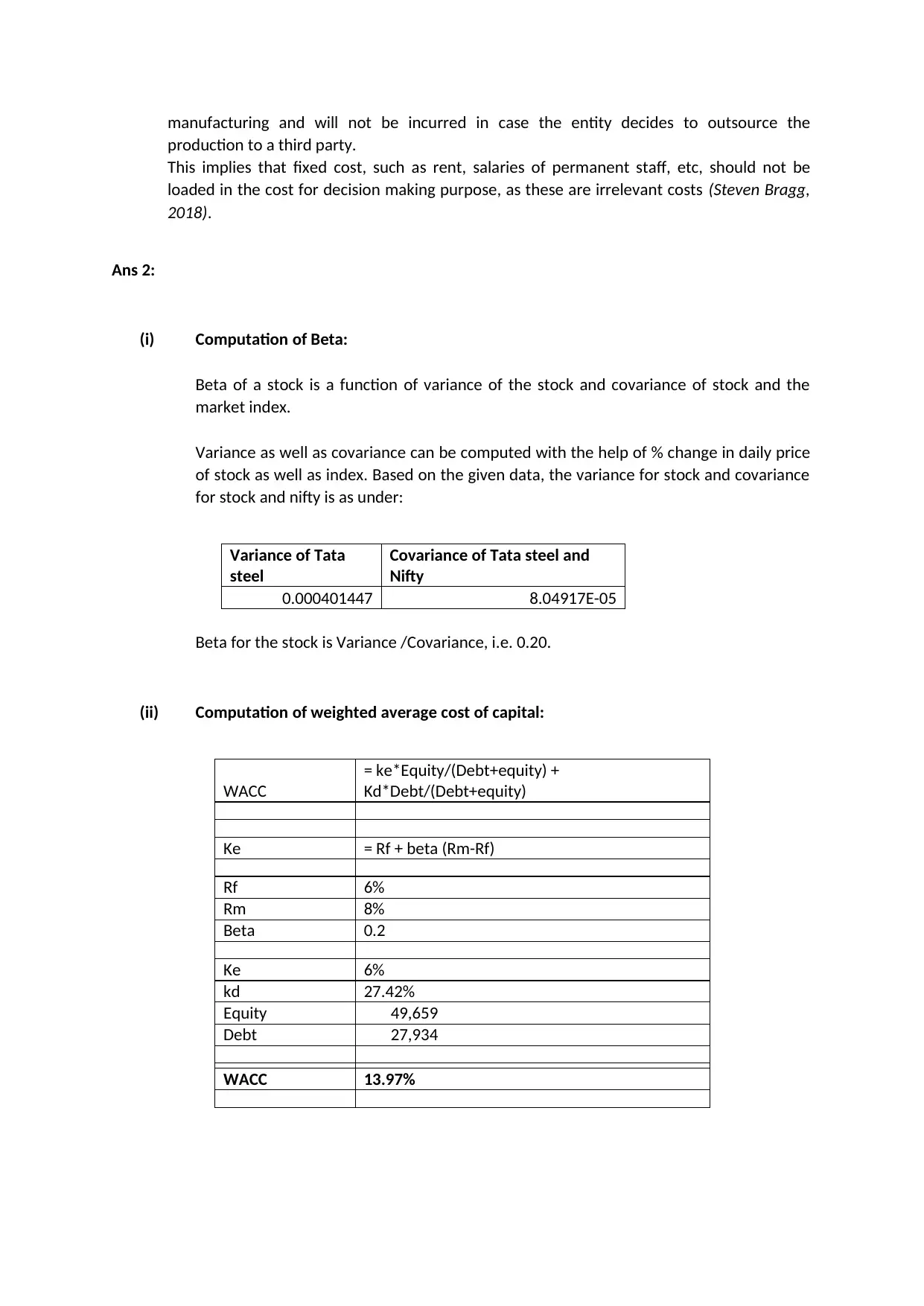

manufacturing and will not be incurred in case the entity decides to outsource the

production to a third party.

This implies that fixed cost, such as rent, salaries of permanent staff, etc, should not be

loaded in the cost for decision making purpose, as these are irrelevant costs (Steven Bragg,

2018).

Ans 2:

(i) Computation of Beta:

Beta of a stock is a function of variance of the stock and covariance of stock and the

market index.

Variance as well as covariance can be computed with the help of % change in daily price

of stock as well as index. Based on the given data, the variance for stock and covariance

for stock and nifty is as under:

Variance of Tata

steel

Covariance of Tata steel and

Nifty

0.000401447 8.04917E-05

Beta for the stock is Variance /Covariance, i.e. 0.20.

(ii) Computation of weighted average cost of capital:

WACC

= ke*Equity/(Debt+equity) +

Kd*Debt/(Debt+equity)

Ke = Rf + beta (Rm-Rf)

Rf 6%

Rm 8%

Beta 0.2

Ke 6%

kd 27.42%

Equity 49,659

Debt 27,934

WACC 13.97%

production to a third party.

This implies that fixed cost, such as rent, salaries of permanent staff, etc, should not be

loaded in the cost for decision making purpose, as these are irrelevant costs (Steven Bragg,

2018).

Ans 2:

(i) Computation of Beta:

Beta of a stock is a function of variance of the stock and covariance of stock and the

market index.

Variance as well as covariance can be computed with the help of % change in daily price

of stock as well as index. Based on the given data, the variance for stock and covariance

for stock and nifty is as under:

Variance of Tata

steel

Covariance of Tata steel and

Nifty

0.000401447 8.04917E-05

Beta for the stock is Variance /Covariance, i.e. 0.20.

(ii) Computation of weighted average cost of capital:

WACC

= ke*Equity/(Debt+equity) +

Kd*Debt/(Debt+equity)

Ke = Rf + beta (Rm-Rf)

Rf 6%

Rm 8%

Beta 0.2

Ke 6%

kd 27.42%

Equity 49,659

Debt 27,934

WACC 13.97%

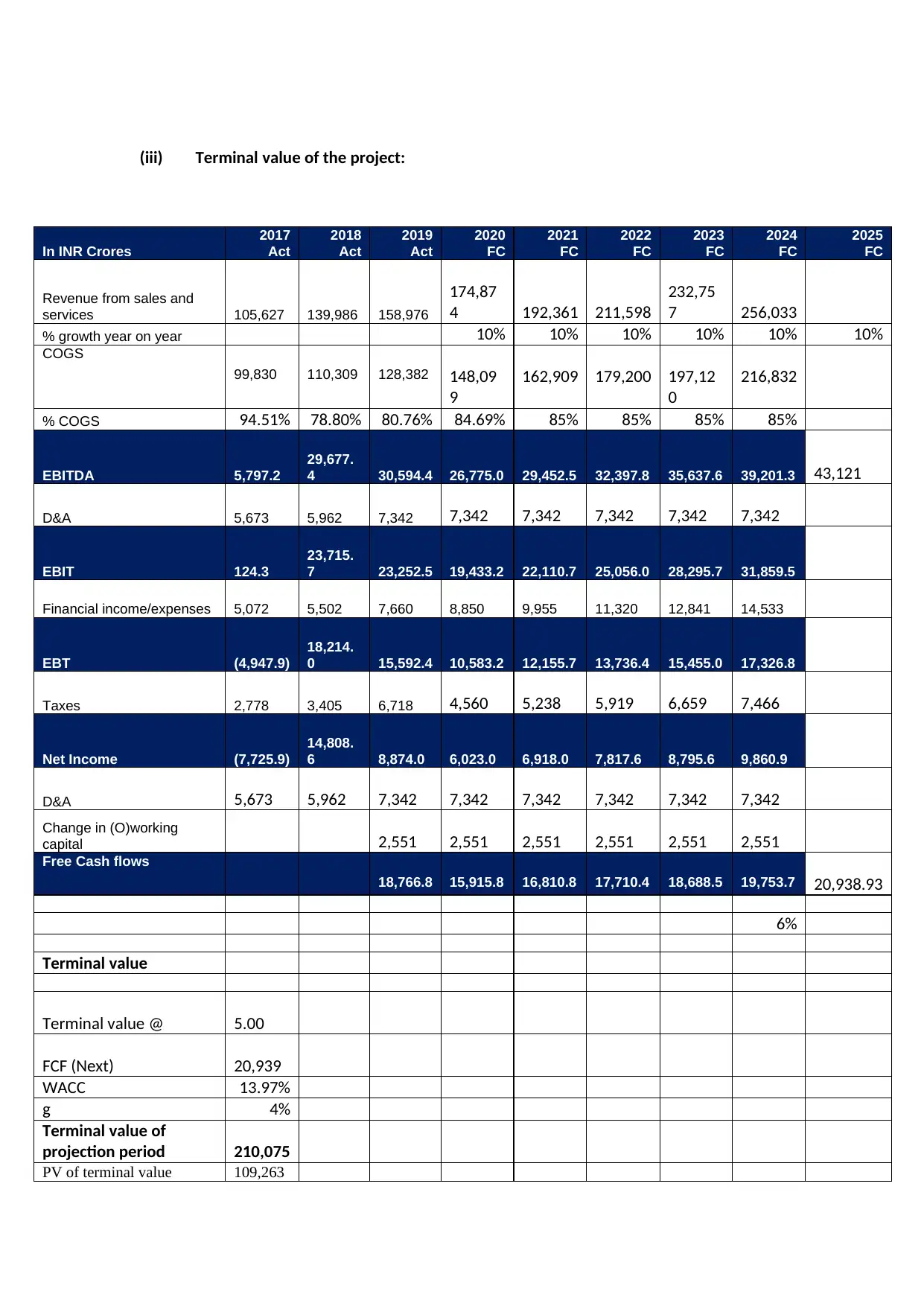

(iii) Terminal value of the project:

In INR Crores

2017

Act

2018

Act

2019

Act

2020

FC

2021

FC

2022

FC

2023

FC

2024

FC

2025

FC

Revenue from sales and

services 105,627 139,986 158,976

174,87

4 192,361 211,598

232,75

7 256,033

% growth year on year 10% 10% 10% 10% 10% 10%

COGS

99,830 110,309 128,382 148,09

9

162,909 179,200 197,12

0

216,832

% COGS 94.51% 78.80% 80.76% 84.69% 85% 85% 85% 85%

EBITDA 5,797.2

29,677.

4 30,594.4 26,775.0 29,452.5 32,397.8 35,637.6 39,201.3 43,121

D&A 5,673 5,962 7,342 7,342 7,342 7,342 7,342 7,342

EBIT 124.3

23,715.

7 23,252.5 19,433.2 22,110.7 25,056.0 28,295.7 31,859.5

Financial income/expenses 5,072 5,502 7,660 8,850 9,955 11,320 12,841 14,533

EBT (4,947.9)

18,214.

0 15,592.4 10,583.2 12,155.7 13,736.4 15,455.0 17,326.8

Taxes 2,778 3,405 6,718 4,560 5,238 5,919 6,659 7,466

Net Income (7,725.9)

14,808.

6 8,874.0 6,023.0 6,918.0 7,817.6 8,795.6 9,860.9

D&A 5,673 5,962 7,342 7,342 7,342 7,342 7,342 7,342

Change in (O)working

capital 2,551 2,551 2,551 2,551 2,551 2,551

Free Cash flows

18,766.8 15,915.8 16,810.8 17,710.4 18,688.5 19,753.7 20,938.93

6%

Terminal value

Terminal value @ 5.00

FCF (Next) 20,939

WACC 13.97%

g 4%

Terminal value of

projection period 210,075

PV of terminal value 109,263

In INR Crores

2017

Act

2018

Act

2019

Act

2020

FC

2021

FC

2022

FC

2023

FC

2024

FC

2025

FC

Revenue from sales and

services 105,627 139,986 158,976

174,87

4 192,361 211,598

232,75

7 256,033

% growth year on year 10% 10% 10% 10% 10% 10%

COGS

99,830 110,309 128,382 148,09

9

162,909 179,200 197,12

0

216,832

% COGS 94.51% 78.80% 80.76% 84.69% 85% 85% 85% 85%

EBITDA 5,797.2

29,677.

4 30,594.4 26,775.0 29,452.5 32,397.8 35,637.6 39,201.3 43,121

D&A 5,673 5,962 7,342 7,342 7,342 7,342 7,342 7,342

EBIT 124.3

23,715.

7 23,252.5 19,433.2 22,110.7 25,056.0 28,295.7 31,859.5

Financial income/expenses 5,072 5,502 7,660 8,850 9,955 11,320 12,841 14,533

EBT (4,947.9)

18,214.

0 15,592.4 10,583.2 12,155.7 13,736.4 15,455.0 17,326.8

Taxes 2,778 3,405 6,718 4,560 5,238 5,919 6,659 7,466

Net Income (7,725.9)

14,808.

6 8,874.0 6,023.0 6,918.0 7,817.6 8,795.6 9,860.9

D&A 5,673 5,962 7,342 7,342 7,342 7,342 7,342 7,342

Change in (O)working

capital 2,551 2,551 2,551 2,551 2,551 2,551

Free Cash flows

18,766.8 15,915.8 16,810.8 17,710.4 18,688.5 19,753.7 20,938.93

6%

Terminal value

Terminal value @ 5.00

FCF (Next) 20,939

WACC 13.97%

g 4%

Terminal value of

projection period 210,075

PV of terminal value 109,263

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

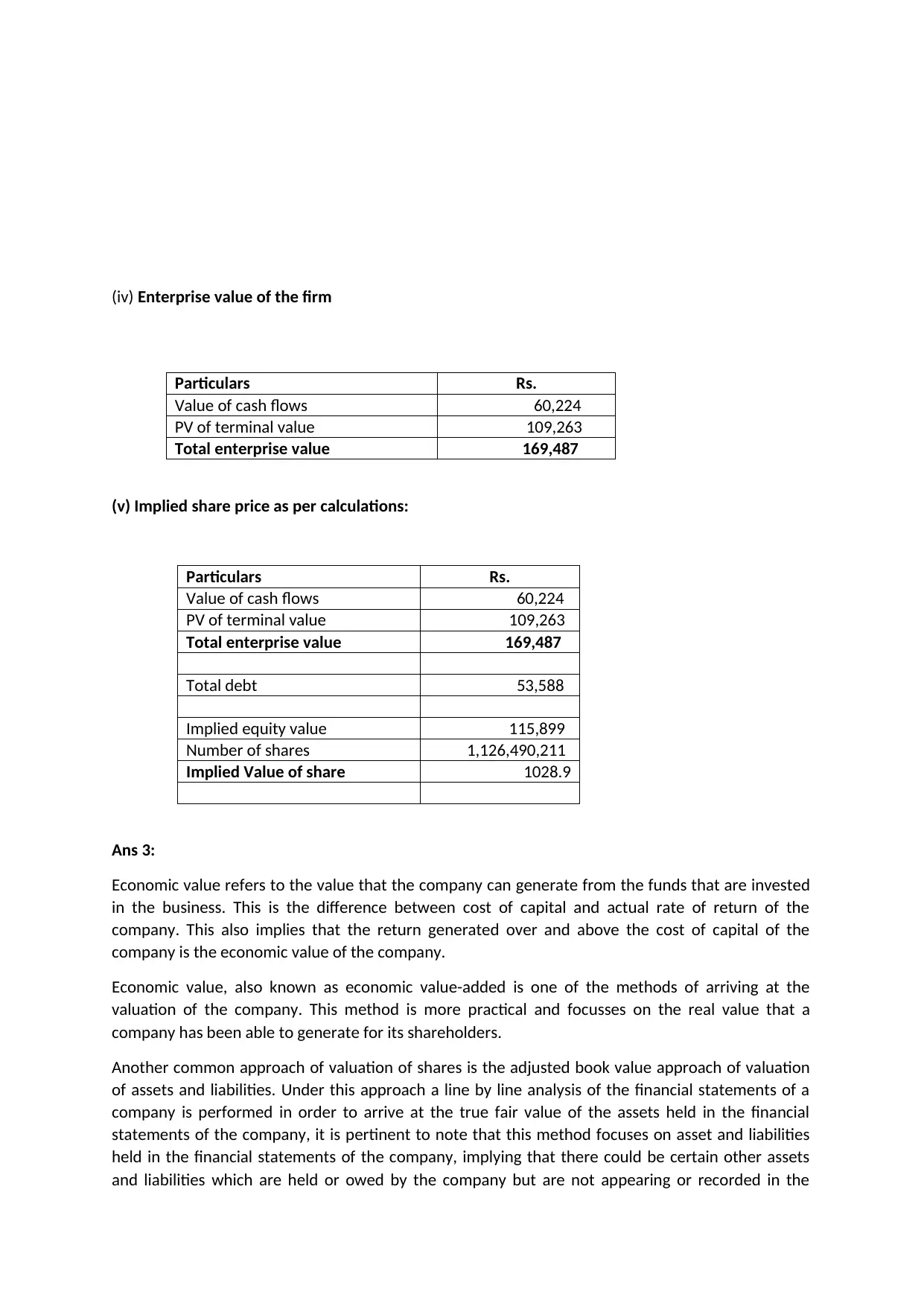

(iv) Enterprise value of the firm

(v) Implied share price as per calculations:

Particulars Rs.

Value of cash flows 60,224

PV of terminal value 109,263

Total enterprise value 169,487

Total debt 53,588

Implied equity value 115,899

Number of shares 1,126,490,211

Implied Value of share 1028.9

Ans 3:

Economic value refers to the value that the company can generate from the funds that are invested

in the business. This is the difference between cost of capital and actual rate of return of the

company. This also implies that the return generated over and above the cost of capital of the

company is the economic value of the company.

Economic value, also known as economic value-added is one of the methods of arriving at the

valuation of the company. This method is more practical and focusses on the real value that a

company has been able to generate for its shareholders.

Another common approach of valuation of shares is the adjusted book value approach of valuation

of assets and liabilities. Under this approach a line by line analysis of the financial statements of a

company is performed in order to arrive at the true fair value of the assets held in the financial

statements of the company, it is pertinent to note that this method focuses on asset and liabilities

held in the financial statements of the company, implying that there could be certain other assets

and liabilities which are held or owed by the company but are not appearing or recorded in the

Particulars Rs.

Value of cash flows 60,224

PV of terminal value 109,263

Total enterprise value 169,487

(v) Implied share price as per calculations:

Particulars Rs.

Value of cash flows 60,224

PV of terminal value 109,263

Total enterprise value 169,487

Total debt 53,588

Implied equity value 115,899

Number of shares 1,126,490,211

Implied Value of share 1028.9

Ans 3:

Economic value refers to the value that the company can generate from the funds that are invested

in the business. This is the difference between cost of capital and actual rate of return of the

company. This also implies that the return generated over and above the cost of capital of the

company is the economic value of the company.

Economic value, also known as economic value-added is one of the methods of arriving at the

valuation of the company. This method is more practical and focusses on the real value that a

company has been able to generate for its shareholders.

Another common approach of valuation of shares is the adjusted book value approach of valuation

of assets and liabilities. Under this approach a line by line analysis of the financial statements of a

company is performed in order to arrive at the true fair value of the assets held in the financial

statements of the company, it is pertinent to note that this method focuses on asset and liabilities

held in the financial statements of the company, implying that there could be certain other assets

and liabilities which are held or owed by the company but are not appearing or recorded in the

Particulars Rs.

Value of cash flows 60,224

PV of terminal value 109,263

Total enterprise value 169,487

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial statements of the company, such as self-developed intangible assets, like Goodwill,

contingent liabilities.

Thus, the value driven by the adjusted book value approach may be under or over-stated as it might

not capture all the assets held by the company, i.e. skipping the assets which are not recorded.

In order to compute the valuation of Reliance using the adjusted book value approach, various

assets held by the company, majorly in the following categories, are required to be valued at fair

value:

i. Property plant and equipment –

It is presently recorded at INR 1,94,895 Crores, whereas the fair value of the assets in

this category could be significantly different than their book value, as the book value is

the value at which these were purchased, as reduced by depreciation and amortisation

over the period, fair value on the other hand, will be driven by the market forces and

market prices of the assets in discussion.

ii. Intangible assets:

The book value of 8,293 Crores of intangible assets, is reflecting the cost less

accumulated depreciation on such assets, and is not reflective of the real market value

of the assets on the date of valuation.

These two items, along with Capital work in progress, will be the major reason for the difference

between adjusted book value and book value. Similarly there could be certain other assets and

liabilities, which are recorded in the books of accounts, at values different to their current market

value, those assets will also be required to be revalued to reflect the fair market value as on the date

of valuation.

In order to compute the Economic value for Reliance there are various adjustments that are

required to be made in the numbers published in the financial statements of the company, those

adjustments include:

1. In the general expenses of 1,453 crores incurred by the company in the year 2019,

Identifying the expenses that have been incurred on training and R&D, as these expenses are

required to be considered as an investment in the business and same should not be

deducted to compute the actual return that has been generated by the business.

This school of though doesn’t consider the amount incurred on training and R&D as expense

and rather it is considered as an investment in the business and net investment is increased

by such amount.

Thus, the net investment in business by Reliance, will be further increased by the amount

spent by it on training and R&D related areas.

contingent liabilities.

Thus, the value driven by the adjusted book value approach may be under or over-stated as it might

not capture all the assets held by the company, i.e. skipping the assets which are not recorded.

In order to compute the valuation of Reliance using the adjusted book value approach, various

assets held by the company, majorly in the following categories, are required to be valued at fair

value:

i. Property plant and equipment –

It is presently recorded at INR 1,94,895 Crores, whereas the fair value of the assets in

this category could be significantly different than their book value, as the book value is

the value at which these were purchased, as reduced by depreciation and amortisation

over the period, fair value on the other hand, will be driven by the market forces and

market prices of the assets in discussion.

ii. Intangible assets:

The book value of 8,293 Crores of intangible assets, is reflecting the cost less

accumulated depreciation on such assets, and is not reflective of the real market value

of the assets on the date of valuation.

These two items, along with Capital work in progress, will be the major reason for the difference

between adjusted book value and book value. Similarly there could be certain other assets and

liabilities, which are recorded in the books of accounts, at values different to their current market

value, those assets will also be required to be revalued to reflect the fair market value as on the date

of valuation.

In order to compute the Economic value for Reliance there are various adjustments that are

required to be made in the numbers published in the financial statements of the company, those

adjustments include:

1. In the general expenses of 1,453 crores incurred by the company in the year 2019,

Identifying the expenses that have been incurred on training and R&D, as these expenses are

required to be considered as an investment in the business and same should not be

deducted to compute the actual return that has been generated by the business.

This school of though doesn’t consider the amount incurred on training and R&D as expense

and rather it is considered as an investment in the business and net investment is increased

by such amount.

Thus, the net investment in business by Reliance, will be further increased by the amount

spent by it on training and R&D related areas.

2. For the leased assets in the balance sheet of the Company, amounting to INR 317 Crores as

on 31st March, 2019, the company needs to derive the fair value of such assets, as those

assets have contributed to the return generated by the company and hence, the fair value of

these assets should be considered in computing the actual return on assets of the company.

These assets are in the nature of plant and machinery and ships, which have been used in

generating the return from business and thus, based on the economic value school of

thought, to arrive at actual return generated on assets, the fair value of such assets are

required to be computed and considered in the computation of economic value.

3. The company needs to eliminate the impact of any unusual income that is considered in the

EBIT of the company, so as to be able to compute the actual return generated on total

assets. Actual return is the normal return that the company would earn in the normal course

of business.

4. The company should adjust the net investment made in the business, to reflect the net asset

values of the assets employed in the business, assuming that straight line method of

depreciation is deployed by the company, i.e. the depreciation charged on diminishing

balance method, needs to be adjusted to straight line method, so as to be able to compute

the book value accordingly.

b.

i. EV/EBITDA:

Enterprise value of a company is the value that the equity of the company would fetch in the

market, which is also known as market capitalisation of the company, added with debt,

minority interest and preferred share, the amount so derived is reduced by total cash and

cash equivalent and marketable securities.

Market capitalisation of reliance as on 31st March, 2019 is INR 863,996 Cr. (Annual report, 2019)

Gross Debt held by the company as on 31st March, 2019 is INR 287,505 Cr. (Annual report, 2019)

Less: Cash and cash equivalents as on 31st March, 2019 is INR 133,027 Cr. (Annual report, 2019)

Thus, the enterprise value of Reliance as on 31st March, 2019 is INR 1,018,474 Cr.

EBITDA of the company is 76,780 Crores (66,222 Cr + 10,558 Crores) (Annual report, 2019)

EV/EBITDA = 1,018,474/76,780 = 13.27

ii. Price to earnings ratio:

P/E ratio = Current share price/Earning per share

Current share price of reliance as on 31st March, 2019 is 1370. (Yahoo Finance)

EPS is INR 66.8 (Annual report, 2019)

on 31st March, 2019, the company needs to derive the fair value of such assets, as those

assets have contributed to the return generated by the company and hence, the fair value of

these assets should be considered in computing the actual return on assets of the company.

These assets are in the nature of plant and machinery and ships, which have been used in

generating the return from business and thus, based on the economic value school of

thought, to arrive at actual return generated on assets, the fair value of such assets are

required to be computed and considered in the computation of economic value.

3. The company needs to eliminate the impact of any unusual income that is considered in the

EBIT of the company, so as to be able to compute the actual return generated on total

assets. Actual return is the normal return that the company would earn in the normal course

of business.

4. The company should adjust the net investment made in the business, to reflect the net asset

values of the assets employed in the business, assuming that straight line method of

depreciation is deployed by the company, i.e. the depreciation charged on diminishing

balance method, needs to be adjusted to straight line method, so as to be able to compute

the book value accordingly.

b.

i. EV/EBITDA:

Enterprise value of a company is the value that the equity of the company would fetch in the

market, which is also known as market capitalisation of the company, added with debt,

minority interest and preferred share, the amount so derived is reduced by total cash and

cash equivalent and marketable securities.

Market capitalisation of reliance as on 31st March, 2019 is INR 863,996 Cr. (Annual report, 2019)

Gross Debt held by the company as on 31st March, 2019 is INR 287,505 Cr. (Annual report, 2019)

Less: Cash and cash equivalents as on 31st March, 2019 is INR 133,027 Cr. (Annual report, 2019)

Thus, the enterprise value of Reliance as on 31st March, 2019 is INR 1,018,474 Cr.

EBITDA of the company is 76,780 Crores (66,222 Cr + 10,558 Crores) (Annual report, 2019)

EV/EBITDA = 1,018,474/76,780 = 13.27

ii. Price to earnings ratio:

P/E ratio = Current share price/Earning per share

Current share price of reliance as on 31st March, 2019 is 1370. (Yahoo Finance)

EPS is INR 66.8 (Annual report, 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P/E Ratio = 1370/66.8 = 20.51

iii. Price to cash-flow ratio:

Price to cash flow ratio = Current share price/Cash flow share

Average Share price of reliance as on 31st March, 2019 is 1230 (Yahoo Finance)

The price used to compute this ratio is the three months average price, for period

beginning on 01st January, 2019 and ending on 31st March, 2019, to avoid one off

movement in prices at a particular date.

Operating cash flow per share is INR 67.30 (Annual report, 2019)

Price to cash flow Ratio = 1230/67.3 = 18.27

iv. Price to book ratio:

Book value of each share of Reliance as on 31st March, 2019 is 474.68 (Annual report,

2019)

Current share price of reliance as on 31st March, 2019 is 1370. (Yahoo Finance)

Price to book ratio = 1370/474.68 = 2.88.

This implies that the price of the share of the company is 2.88 times the book value of

the share of the company.

v. Each market multiple ratio computed above, has different significance in the valuation of

a company, for the purpose of investment.

Results of different multiple ratios computed above, vary significantly, based on the

parameter used for computation of such ratios. These ratios perse, doesn’t

communicate any significant message about the performance of the entity, rather,

these, when compared with similar ratios for other companies, provides a good

comparison base for different companies.

Economic value/EBITDA:

This ratio provides the number of times the economic value of an entity is, of the EBITDA

generated by the entity. This ratio is comparable across the industry with any other

company irrespective of the capital structure of the company, as computation of

economic value removes the effect of different capital structure and makes the ratio

comparable across companies.

iii. Price to cash-flow ratio:

Price to cash flow ratio = Current share price/Cash flow share

Average Share price of reliance as on 31st March, 2019 is 1230 (Yahoo Finance)

The price used to compute this ratio is the three months average price, for period

beginning on 01st January, 2019 and ending on 31st March, 2019, to avoid one off

movement in prices at a particular date.

Operating cash flow per share is INR 67.30 (Annual report, 2019)

Price to cash flow Ratio = 1230/67.3 = 18.27

iv. Price to book ratio:

Book value of each share of Reliance as on 31st March, 2019 is 474.68 (Annual report,

2019)

Current share price of reliance as on 31st March, 2019 is 1370. (Yahoo Finance)

Price to book ratio = 1370/474.68 = 2.88.

This implies that the price of the share of the company is 2.88 times the book value of

the share of the company.

v. Each market multiple ratio computed above, has different significance in the valuation of

a company, for the purpose of investment.

Results of different multiple ratios computed above, vary significantly, based on the

parameter used for computation of such ratios. These ratios perse, doesn’t

communicate any significant message about the performance of the entity, rather,

these, when compared with similar ratios for other companies, provides a good

comparison base for different companies.

Economic value/EBITDA:

This ratio provides the number of times the economic value of an entity is, of the EBITDA

generated by the entity. This ratio is comparable across the industry with any other

company irrespective of the capital structure of the company, as computation of

economic value removes the effect of different capital structure and makes the ratio

comparable across companies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price earnings ratio:

It is the most widely used ratio amongst the equity market analysts, to determine

whether the a share is undervalued, overvalued or at par valued, based on the industry

average P/E for the company.

Price earning ratio computes the multiple of EPS that price carries, so in case of Reliance,

P/E ratio is 20.51, implying that the price of Reliance’s share is 20.51 times the earnings

per share of the company.

To derive any meaningful message from this number, it needs to be compared with the

comparable companies’ P/E ratio as well as industry P/E ratio, this standalone number

perse has no or little relevance.

Price to cash flow ratio:

Another important multiple, being used by the analysts these days, is the price to cash

flow ratio, which computes the price as multiple of operating cash flow per share,

generated by the company.

This ratio is more relevant as it compares the prices to the cash generated by business

and not only to the earnings per share, which is driven by the profit generated by the

business, irrespective of whether the same is converted into cash or not.

Price to book ratio:

Price to book ratio is a traditional ratio, widely used by analysts to conclude whether a

share is trading overvalued, undervalued or at fair valued.

This ratio provides the comparison between the book value of the share and the market

value of the share (Tim Smith, 2019) .

Multiples are broadly of two types, i.e. Equity multiple and enterprise value multiple,

equity multiples are driven by the market price of the equity shared of the entity and

since, the market price doesn’t always fluctuate based on the performance of the

company, there could be a scenario, wherein the equity based multiple might change

without a significant change in the business performance of the company.

On the other hand, enterprise value related multiple enables the managers to compare

the companies irrespective of their capital structure, since, enterprise value of a

company eradicates the impact of capital composition of the company.

It is the most widely used ratio amongst the equity market analysts, to determine

whether the a share is undervalued, overvalued or at par valued, based on the industry

average P/E for the company.

Price earning ratio computes the multiple of EPS that price carries, so in case of Reliance,

P/E ratio is 20.51, implying that the price of Reliance’s share is 20.51 times the earnings

per share of the company.

To derive any meaningful message from this number, it needs to be compared with the

comparable companies’ P/E ratio as well as industry P/E ratio, this standalone number

perse has no or little relevance.

Price to cash flow ratio:

Another important multiple, being used by the analysts these days, is the price to cash

flow ratio, which computes the price as multiple of operating cash flow per share,

generated by the company.

This ratio is more relevant as it compares the prices to the cash generated by business

and not only to the earnings per share, which is driven by the profit generated by the

business, irrespective of whether the same is converted into cash or not.

Price to book ratio:

Price to book ratio is a traditional ratio, widely used by analysts to conclude whether a

share is trading overvalued, undervalued or at fair valued.

This ratio provides the comparison between the book value of the share and the market

value of the share (Tim Smith, 2019) .

Multiples are broadly of two types, i.e. Equity multiple and enterprise value multiple,

equity multiples are driven by the market price of the equity shared of the entity and

since, the market price doesn’t always fluctuate based on the performance of the

company, there could be a scenario, wherein the equity based multiple might change

without a significant change in the business performance of the company.

On the other hand, enterprise value related multiple enables the managers to compare

the companies irrespective of their capital structure, since, enterprise value of a

company eradicates the impact of capital composition of the company.

References:

Adam hayes 2020, Price-to-earnings ratio – P/E ratio, retrieved on 19/04/2020, retrieved

from https://www.investopedia.com/terms/p/price-earningsratio.asp

Annual report, 2019, Reliance industries limited, retrieved on 19/04/2020, retrieved from

https://www.ril.com/ar2018-19/ril-annual-report-2019.pdf.

CFI, Types of valuation multiples, Retrieved on 19/04/2020, retrieved from

https://corporatefinanceinstitute.com/resources/knowledge/valuation/types-of-

valuation-multiples/

Economic value added, (2019), retrieved on 19/04/2020, retrieved from

https://www.accountingtools.com/articles/2017/5/13/economic-value-added

Kengatharan L, 2017, Use of Capital Investment Appraisal Practices and Effectiveness of

Investment Decisions: A Study on Listed Manufacturing Companies in Sri Lanka,

retrieved on 19/04/2020, retrieved from

http://www.macrothink.org/journal/index.php/ajfa/article/download/12229/9813

Relevant cash flows of capital budgeting (XXXX), retrieved on 19/04/2020, retrieved from

https://accountantnextdoor.com/relevant-cash-flows-of-capital-budgeting/.

Steven Bragg, 2018, Make or Buy Analysis, retrieved on 19/04/2020, retrieved from

https://www.accountingtools.com/articles/make-or-buy-analysis.html

Tata steel, 2017, Financial information

Tata steel, 2018, Financial information

Tata steel, 2019, Financial information

Tim Smith, 2019, Multiples Approach, Retrieved on 19/04/2020, available at

https://www.investopedia.com/terms/m/multiplesapproach.asp

Yahoo finance, Reliance share price, retrieved on 19/04/2020, available at

https://in.finance.yahoo.com/quote/RELIANCE.NS/history?

period1=1546300800&period2=1553990400&interval=1d&filter=history&frequency

=1d

Will Kenton (2019), Price-to-Cash Flow Ratio – P/CF Definition, retrieved on 19/04/2020,

available at https://www.investopedia.com/terms/p/price-to-cash-flowratio.asp

Adam hayes 2020, Price-to-earnings ratio – P/E ratio, retrieved on 19/04/2020, retrieved

from https://www.investopedia.com/terms/p/price-earningsratio.asp

Annual report, 2019, Reliance industries limited, retrieved on 19/04/2020, retrieved from

https://www.ril.com/ar2018-19/ril-annual-report-2019.pdf.

CFI, Types of valuation multiples, Retrieved on 19/04/2020, retrieved from

https://corporatefinanceinstitute.com/resources/knowledge/valuation/types-of-

valuation-multiples/

Economic value added, (2019), retrieved on 19/04/2020, retrieved from

https://www.accountingtools.com/articles/2017/5/13/economic-value-added

Kengatharan L, 2017, Use of Capital Investment Appraisal Practices and Effectiveness of

Investment Decisions: A Study on Listed Manufacturing Companies in Sri Lanka,

retrieved on 19/04/2020, retrieved from

http://www.macrothink.org/journal/index.php/ajfa/article/download/12229/9813

Relevant cash flows of capital budgeting (XXXX), retrieved on 19/04/2020, retrieved from

https://accountantnextdoor.com/relevant-cash-flows-of-capital-budgeting/.

Steven Bragg, 2018, Make or Buy Analysis, retrieved on 19/04/2020, retrieved from

https://www.accountingtools.com/articles/make-or-buy-analysis.html

Tata steel, 2017, Financial information

Tata steel, 2018, Financial information

Tata steel, 2019, Financial information

Tim Smith, 2019, Multiples Approach, Retrieved on 19/04/2020, available at

https://www.investopedia.com/terms/m/multiplesapproach.asp

Yahoo finance, Reliance share price, retrieved on 19/04/2020, available at

https://in.finance.yahoo.com/quote/RELIANCE.NS/history?

period1=1546300800&period2=1553990400&interval=1d&filter=history&frequency

=1d

Will Kenton (2019), Price-to-Cash Flow Ratio – P/CF Definition, retrieved on 19/04/2020,

available at https://www.investopedia.com/terms/p/price-to-cash-flowratio.asp

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.