Raising of Funds: Step Up Bonds vs Convertible Bonds

Assessment 2 for the Financial Accounting course at Queensland University of Technology is a business report on High PG Ltd, a production company with an average return on assets of 8.0%.

5 Pages1293 Words85 Views

Added on 2023-06-07

About This Document

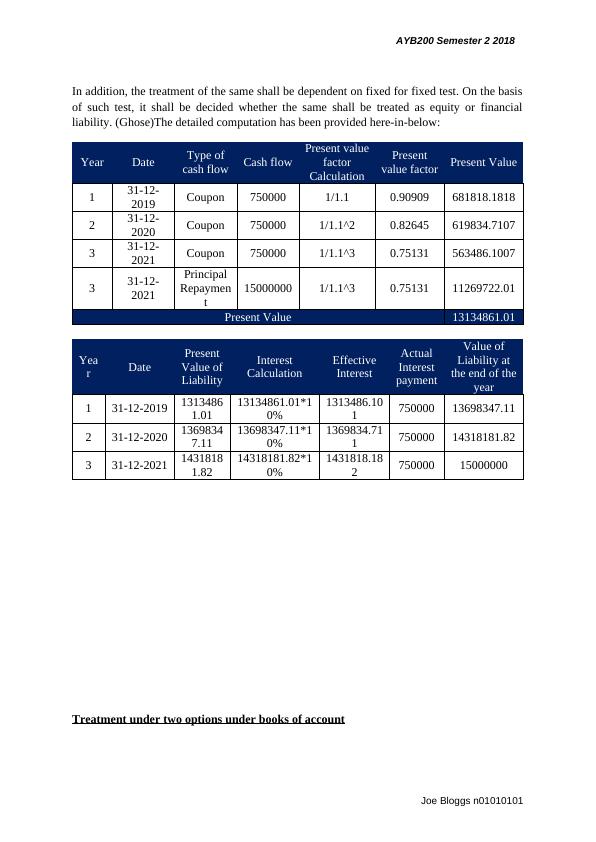

High PG Limited is proposing to acquire further funds from the market in the form of debts or convertible equity whichever is beneficial. Two options have been explored: (a) Raising funds through issue of step up bonds with interest rates or coupon rates of 8%, 10% and 12%. (b) Convertible bonds which are convertible into equity of 15 million shares at the end of 3 year from settlement date. The article discusses the accounting treatment and impact on balance sheet of both options.

Raising of Funds: Step Up Bonds vs Convertible Bonds

Assessment 2 for the Financial Accounting course at Queensland University of Technology is a business report on High PG Ltd, a production company with an average return on assets of 8.0%.

Added on 2023-06-07

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Analysis and Evaluation of Financing Options for Bayer: ACC7046 Financial Strategy

|10

|2718

|343

Financing Expansion Plans of Tuxedo Air with Bond Issue

|6

|750

|24

Financial Accounting Analysis of Organization

|13

|2141

|15

Accounting for Business: Income Recognition and Revenue Recognition

|8

|1319

|53

Financial Statement Analysis of Amani Gold Limited

|14

|4051

|220

Recommendation to the senior management of LMU Plc regarding investment appraisal

|8

|985

|57