Ratio Analysis for Elegant Sdn Bhd: Performance Evaluation for 2016-2017

VerifiedAdded on 2023/06/03

|11

|1576

|341

AI Summary

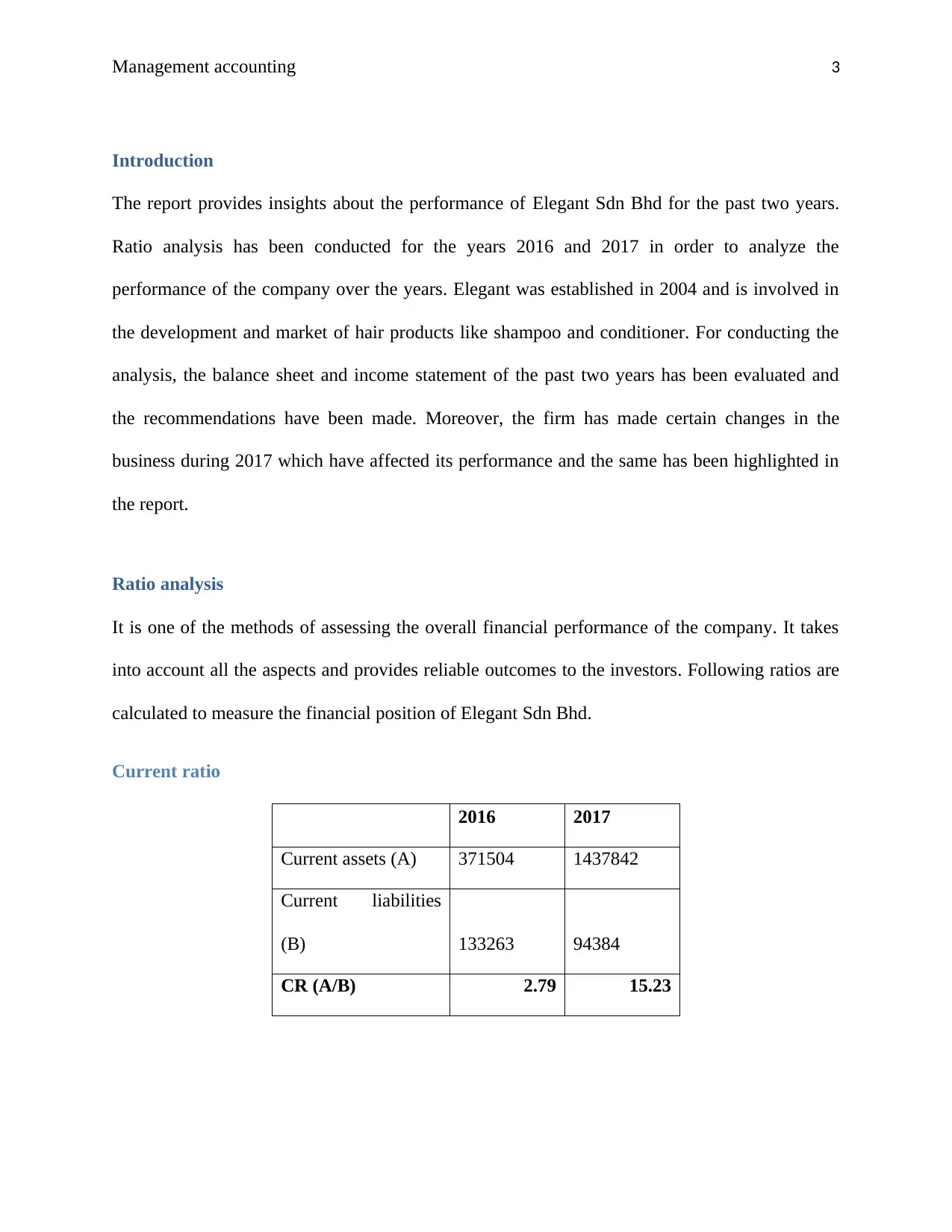

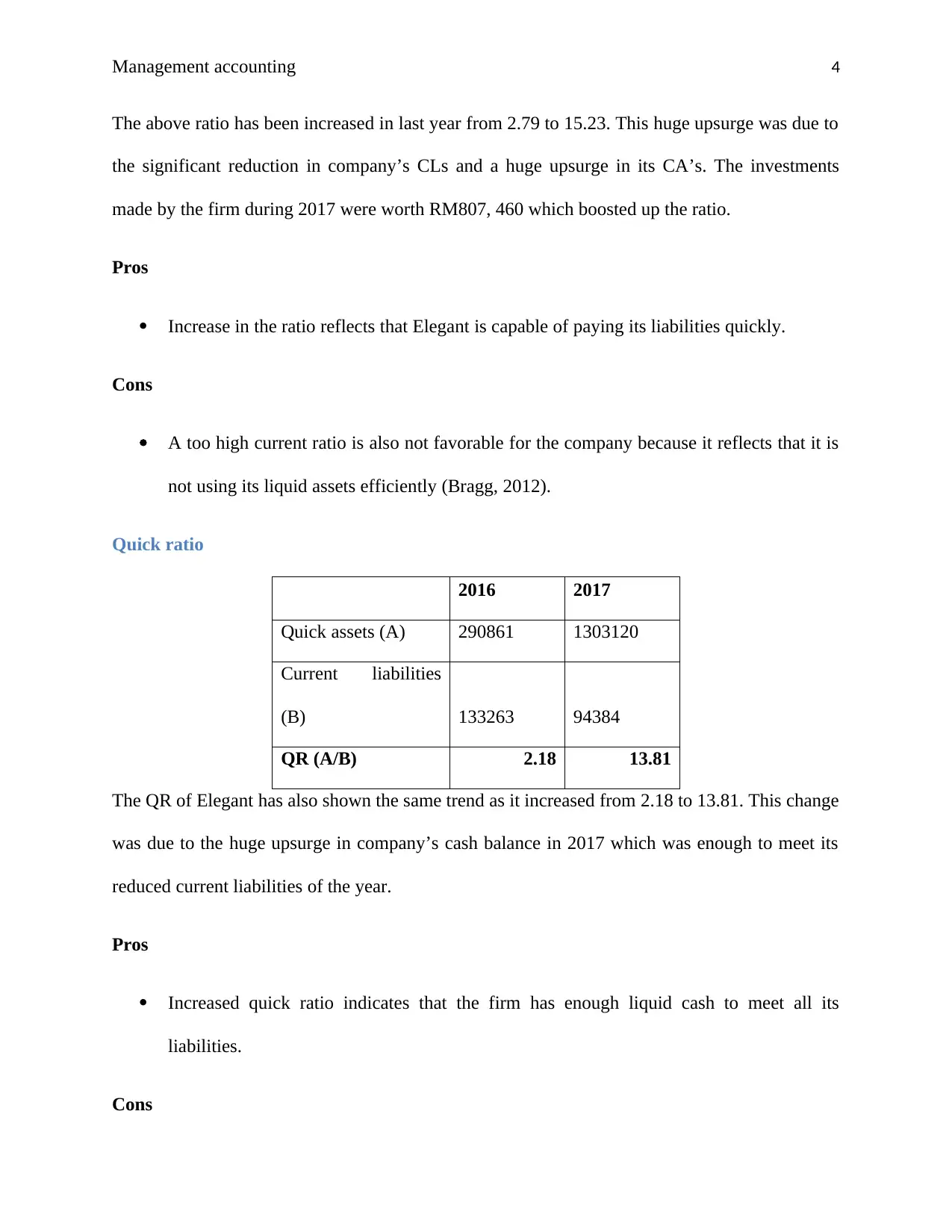

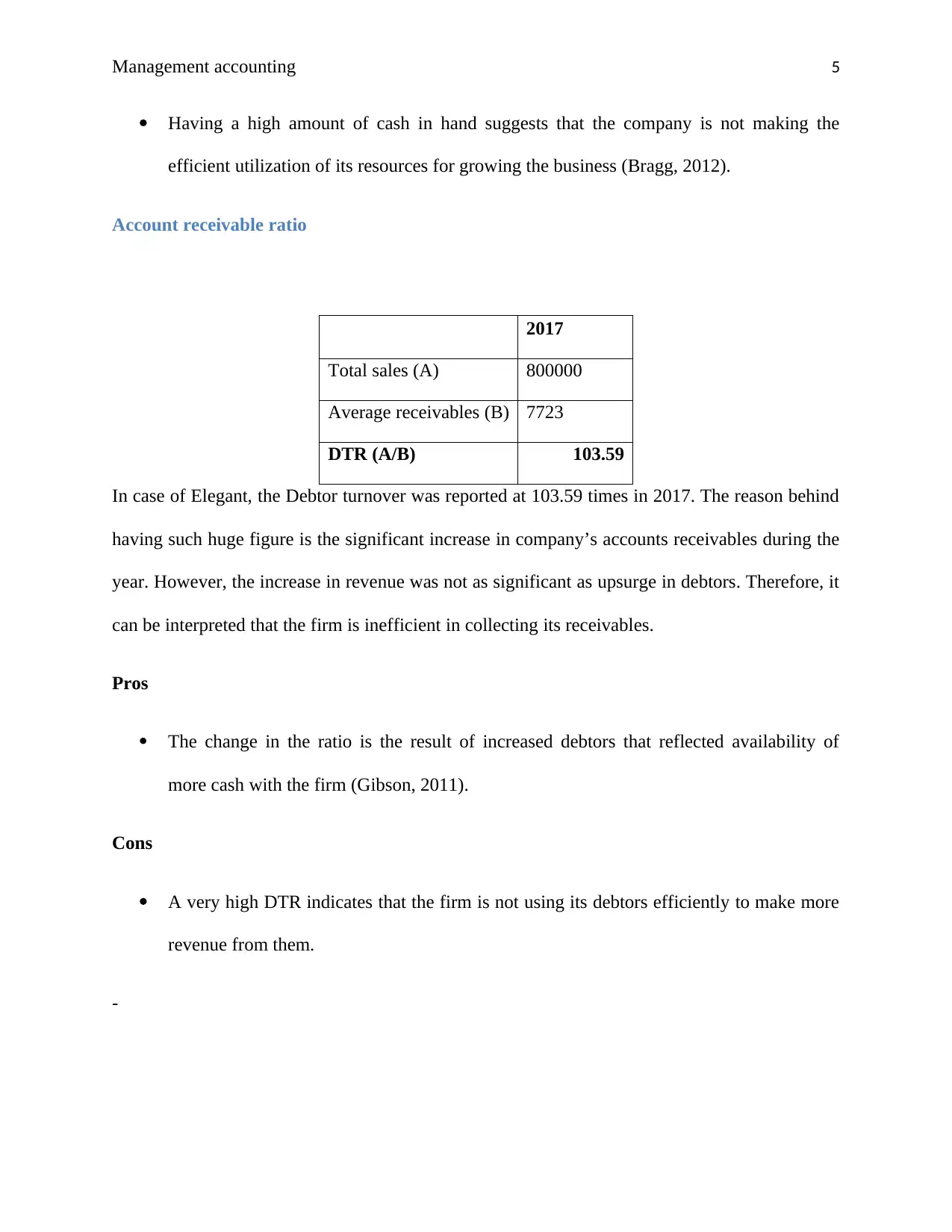

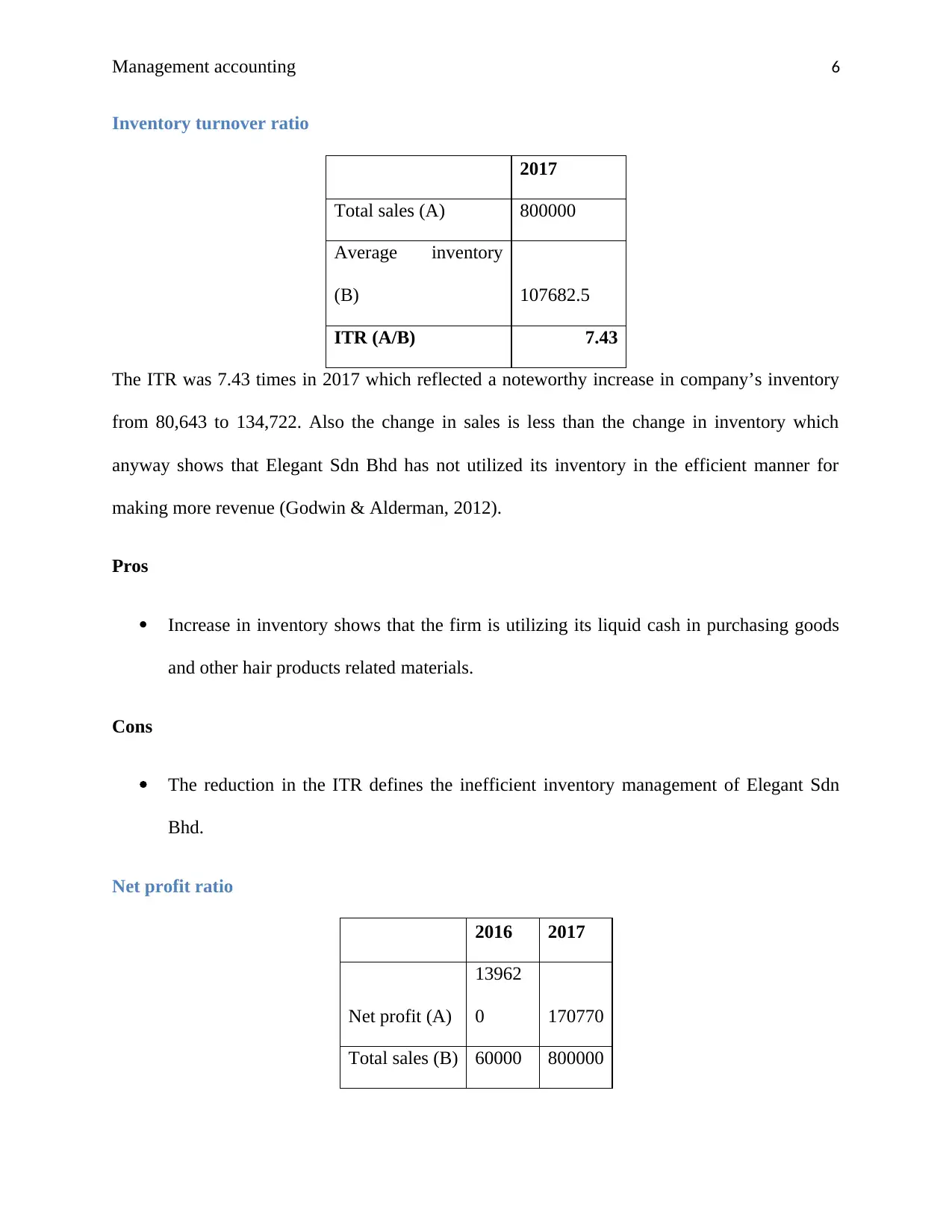

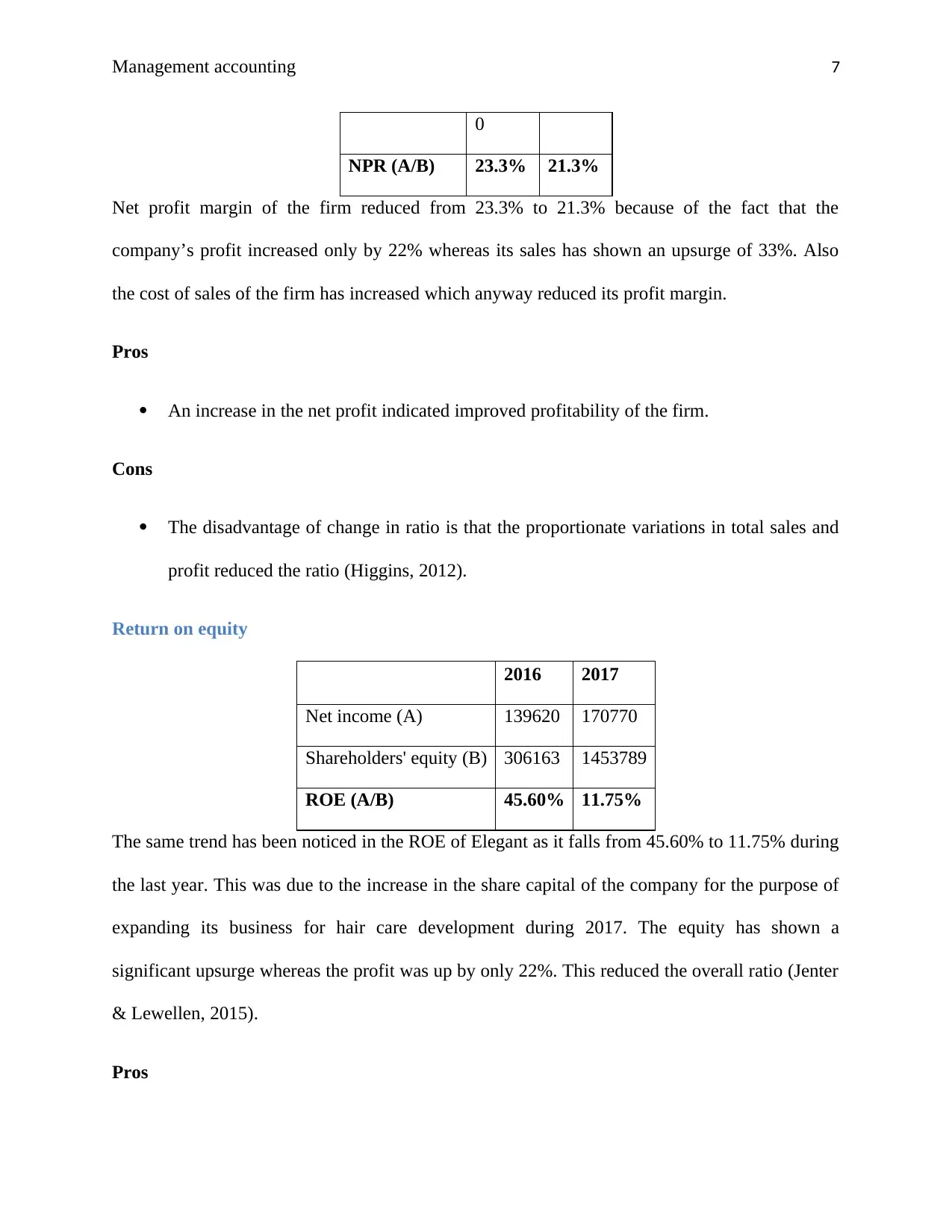

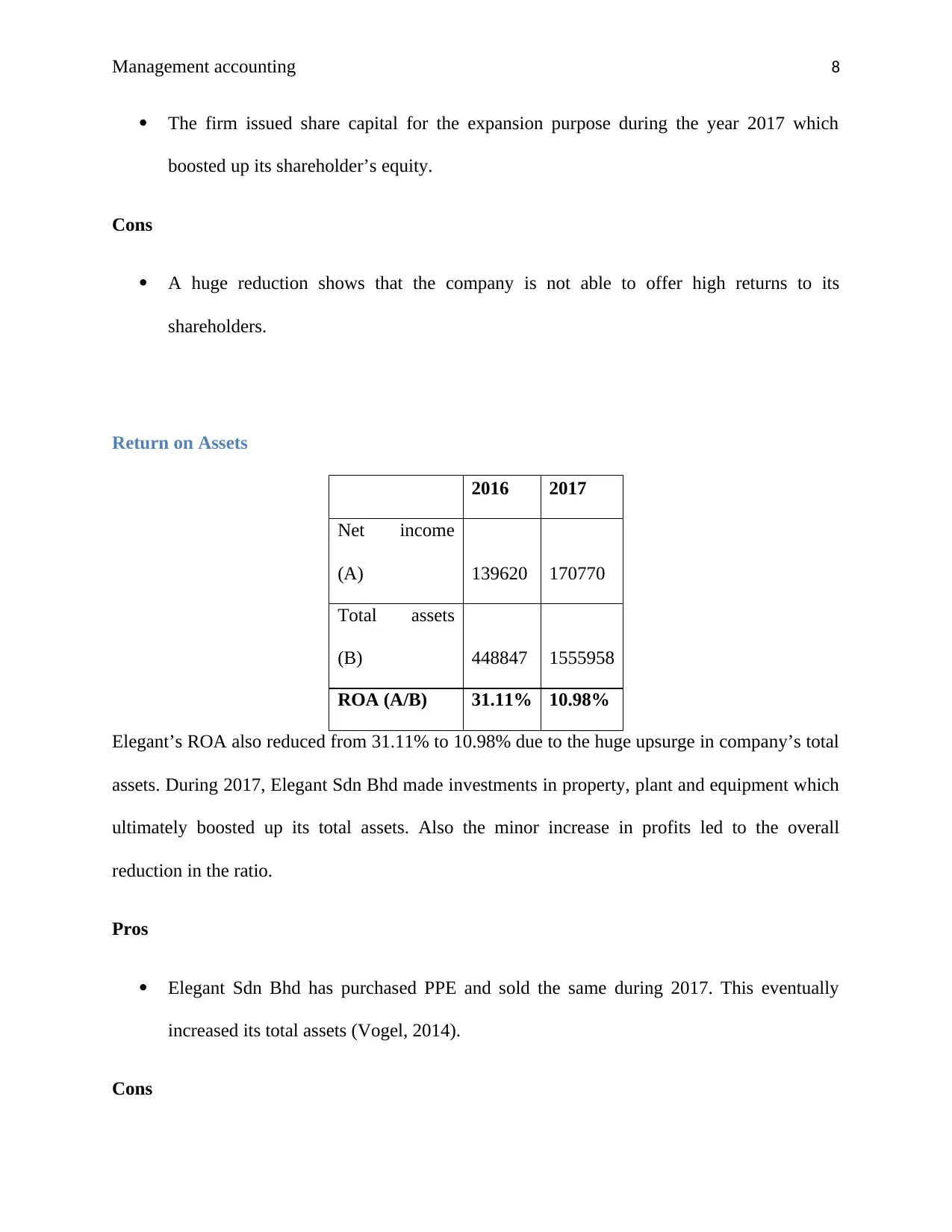

This report provides insights about the performance of Elegant Sdn Bhd for the past two years through ratio analysis. The report evaluates the financial position of the company through various ratios like current ratio, quick ratio, account receivable ratio, inventory turnover ratio, net profit ratio, return on equity, return on assets, and debt/equity ratio. The report concludes with recommendations for the company to improve its profitability and efficiency position.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.