Financial Analysis of ITV Plc: Ratio Analysis and Future Prospects

VerifiedAdded on 2023/06/14

|12

|2130

|117

Report

AI Summary

This report provides a comprehensive financial analysis of ITV Plc, a British media company, using ratio analysis to evaluate its financial performance from 2013 to 2016. The analysis covers profitability ratios (gross profit margin and operating profit margin), activity/efficiency ratios (trade receivable collection period and trade payable payments periods), and liquidity ratios (current ratio and acid test ratio). The report identifies both positive trends, such as revenue growth and effective liquidity, and areas for improvement, including a decreasing operating profit margin and acid test ratio. The analysis concludes that while ITV Plc is performing well financially, it needs to focus on improving profitability and liquidity through strategic adjustments in operating expenses and interest payments.

Running head: ACCOUNTS AND FINANCE

Accounts and Finance

Name of the Student

Name of the University

Author’s Note

Accounts and Finance

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTS AND FINANCE

Table of Contents

1) Introduction.................................................................................................................................2

1.1) Products and Size.................................................................................................................2

1.2) Place of Business..................................................................................................................2

1.3) Business Segment.................................................................................................................2

1.4) Future Prospects...................................................................................................................3

2) Ratio Analysis.............................................................................................................................3

2.1) Need For Ratio Analysis......................................................................................................3

2.2) Benefits of Ratio Analysis....................................................................................................3

2.3) Limitations of Ratio Analysis...............................................................................................4

2.4) Analysis of Financial Statements.........................................................................................4

3) Ratio Analysis.............................................................................................................................5

3.1) Profitability Ratio.................................................................................................................5

3.2) Activity/Efficiency Ratio.....................................................................................................6

3.3) Liquidity Ratio.....................................................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Appendix........................................................................................................................................11

Table of Contents

1) Introduction.................................................................................................................................2

1.1) Products and Size.................................................................................................................2

1.2) Place of Business..................................................................................................................2

1.3) Business Segment.................................................................................................................2

1.4) Future Prospects...................................................................................................................3

2) Ratio Analysis.............................................................................................................................3

2.1) Need For Ratio Analysis......................................................................................................3

2.2) Benefits of Ratio Analysis....................................................................................................3

2.3) Limitations of Ratio Analysis...............................................................................................4

2.4) Analysis of Financial Statements.........................................................................................4

3) Ratio Analysis.............................................................................................................................5

3.1) Profitability Ratio.................................................................................................................5

3.2) Activity/Efficiency Ratio.....................................................................................................6

3.3) Liquidity Ratio.....................................................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Appendix........................................................................................................................................11

2ACCOUNTS AND FINANCE

1) Introduction

1.1) Products and Size

ITV Plc is a British based media company. The major products of the company are

broadcasting and television production. More specifically, ITV Plc can be considered as an

integrated producer and broadcaster that create, owns and distributes different high-quality

content on various platforms globally (itvplc.com 2018).

It needs to be mention that ITV Plc is the largest company in United Kingdom (UK)

having the market share of 47.6% in TV advertising market. The number of registered user of

ITV Plc is 21 million. In 2017, the total revenue of ITV Plc was £3.132. Thus, all these aspects

state that ITV Plc is one of the biggest broadcast companies in UK (itvplc.com 2018).

1.2) Place of Business

It needs to be mentioned that the business operations of ITV Plc is mainly based on UK

as it is the largest commercial producer in UK. Apart from UK, the presence of ITV Plc can be

seen some major parts all over the world like America, Netherlands, Germany, France, Italy,

Australia and the Nordics (reuters.com 2018).

1.3) Business Segment

It can be observed that ITV Plc operates in two segments. They are Broadcast and Online

Segment; and ITV Studios Segment. The commercial family channels of UK operate in the

broadcast and online segment. The international content business of ITV Plc operates in the ITV

studio segment.

1) Introduction

1.1) Products and Size

ITV Plc is a British based media company. The major products of the company are

broadcasting and television production. More specifically, ITV Plc can be considered as an

integrated producer and broadcaster that create, owns and distributes different high-quality

content on various platforms globally (itvplc.com 2018).

It needs to be mention that ITV Plc is the largest company in United Kingdom (UK)

having the market share of 47.6% in TV advertising market. The number of registered user of

ITV Plc is 21 million. In 2017, the total revenue of ITV Plc was £3.132. Thus, all these aspects

state that ITV Plc is one of the biggest broadcast companies in UK (itvplc.com 2018).

1.2) Place of Business

It needs to be mentioned that the business operations of ITV Plc is mainly based on UK

as it is the largest commercial producer in UK. Apart from UK, the presence of ITV Plc can be

seen some major parts all over the world like America, Netherlands, Germany, France, Italy,

Australia and the Nordics (reuters.com 2018).

1.3) Business Segment

It can be observed that ITV Plc operates in two segments. They are Broadcast and Online

Segment; and ITV Studios Segment. The commercial family channels of UK operate in the

broadcast and online segment. The international content business of ITV Plc operates in the ITV

studio segment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTS AND FINANCE

1.4) Future Prospects

There has been expansion in the profit margin of ITV Plc for the last five years as

11.34% and 7.24% growth was there in net income and revenue respectively. At present, 13.45%

growth can be seen in the company. Thus, as per the forecast, it can be seen that the growth trend

will continue for future years and it will provide ITV Plc with the scope for business expansion

(simplywall.st 2018).

2) Ratio Analysis

2.1) Need For Ratio Analysis

Both the internal management and the external users use the results of ratio analysis for

the evaluation of the financial performance of the companies. Ratio analysis refers to the

quantitative analysis of financial information of the companies from the financial statements.

The main need for the use of ratio analysis is the analysis and evaluation of financial position of

the companies in the areas of profitability, efficacy, liquidity and solvency (Higgins 2012).

2.2) Benefits of Ratio Analysis

The benefits are shown below:

Ratio analysis provides assistance in the process of forecasting and planning as the trends

of costs, sales, profit and others are largely helpful.

With the help of the results of ratio analysis, accountants can estimate the figures for

preparing budget.

Ratio analysis provides necessary information to the management for assisting in

decision-making process.

1.4) Future Prospects

There has been expansion in the profit margin of ITV Plc for the last five years as

11.34% and 7.24% growth was there in net income and revenue respectively. At present, 13.45%

growth can be seen in the company. Thus, as per the forecast, it can be seen that the growth trend

will continue for future years and it will provide ITV Plc with the scope for business expansion

(simplywall.st 2018).

2) Ratio Analysis

2.1) Need For Ratio Analysis

Both the internal management and the external users use the results of ratio analysis for

the evaluation of the financial performance of the companies. Ratio analysis refers to the

quantitative analysis of financial information of the companies from the financial statements.

The main need for the use of ratio analysis is the analysis and evaluation of financial position of

the companies in the areas of profitability, efficacy, liquidity and solvency (Higgins 2012).

2.2) Benefits of Ratio Analysis

The benefits are shown below:

Ratio analysis provides assistance in the process of forecasting and planning as the trends

of costs, sales, profit and others are largely helpful.

With the help of the results of ratio analysis, accountants can estimate the figures for

preparing budget.

Ratio analysis provides necessary information to the management for assisting in

decision-making process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTS AND FINANCE

Ratio analysis provides the simplified form of financial statements that provides better

understandability.

Effective ratio analysis can provide signals about the weak financial conduction of the

business organizations.

Ratio analysis helps in showing long-term profitability position of the companies

(Brigham and Ehrhardt 2013).

2.3) Limitations of Ratio Analysis

The limitations are discussed below:

As ratio analysis deals with historical information, the results do not reflect the current

financial condition of the companies.

Financial statements have different kinds of limitations. As ratio analysis is done from

taking information from financial statements, the limitations of financial statements also

affect the results of ratio analysis.

As ratio analysis is a quantitative analysis, the qualitative factors are ignored while

computing the ratios.

Ratio analysis often fails to provide the correct picture of the company as it accounts for

one variable (Brigham and Houston 2012).

2.4) Analysis of Financial Statements

The analysis of the financial statements of ITV Plc from 2013 to 2016 states that there

has been a significant rise in the revenue of the company that is from £2,389 million in 2013 to

£3,064 million in 2016. The rise in revenue contributed towards a healthy rise in the adjusted

EBITA of the company; that is from £620 million in 2013 to £885 million in 2016. It needs to be

Ratio analysis provides the simplified form of financial statements that provides better

understandability.

Effective ratio analysis can provide signals about the weak financial conduction of the

business organizations.

Ratio analysis helps in showing long-term profitability position of the companies

(Brigham and Ehrhardt 2013).

2.3) Limitations of Ratio Analysis

The limitations are discussed below:

As ratio analysis deals with historical information, the results do not reflect the current

financial condition of the companies.

Financial statements have different kinds of limitations. As ratio analysis is done from

taking information from financial statements, the limitations of financial statements also

affect the results of ratio analysis.

As ratio analysis is a quantitative analysis, the qualitative factors are ignored while

computing the ratios.

Ratio analysis often fails to provide the correct picture of the company as it accounts for

one variable (Brigham and Houston 2012).

2.4) Analysis of Financial Statements

The analysis of the financial statements of ITV Plc from 2013 to 2016 states that there

has been a significant rise in the revenue of the company that is from £2,389 million in 2013 to

£3,064 million in 2016. The rise in revenue contributed towards a healthy rise in the adjusted

EBITA of the company; that is from £620 million in 2013 to £885 million in 2016. It needs to be

5ACCOUNTS AND FINANCE

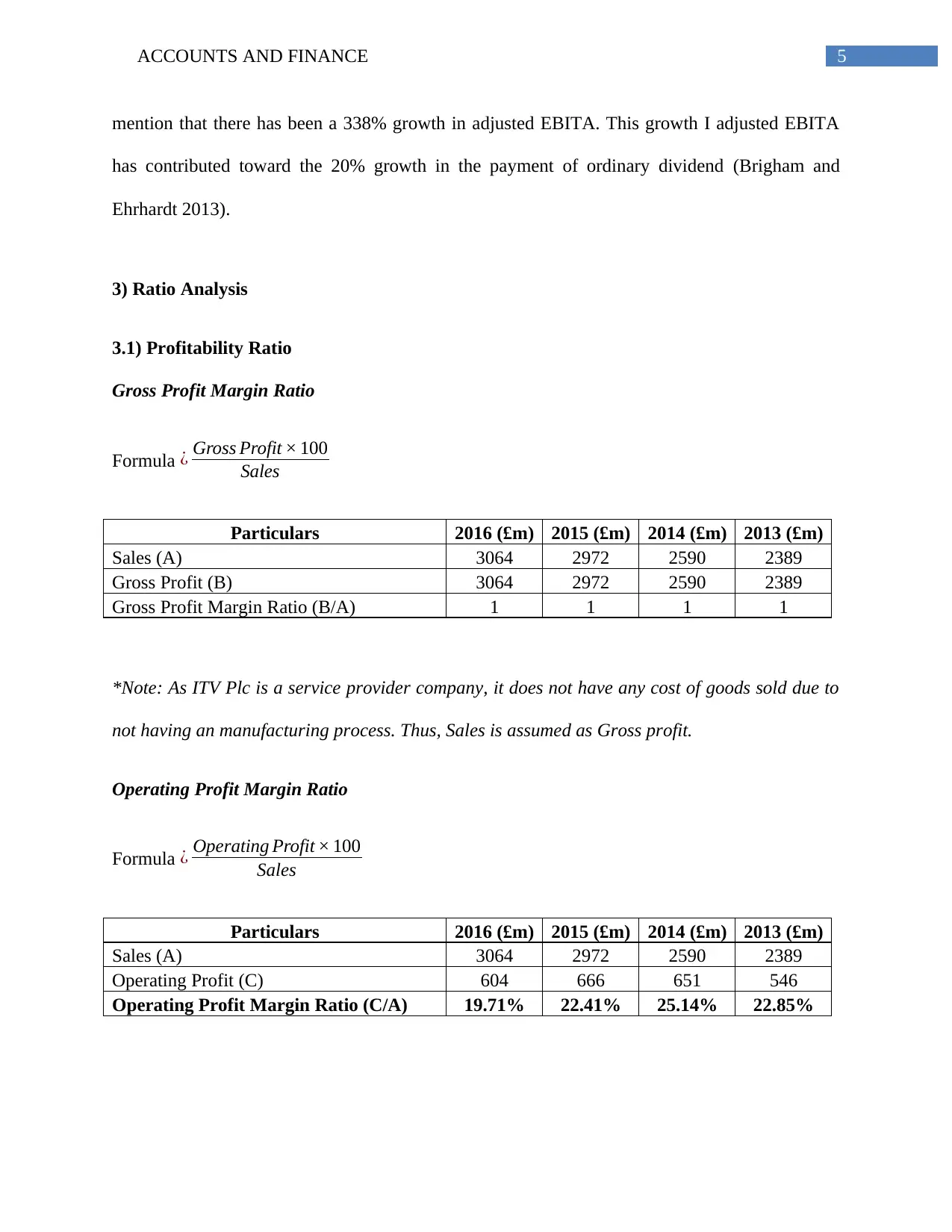

mention that there has been a 338% growth in adjusted EBITA. This growth I adjusted EBITA

has contributed toward the 20% growth in the payment of ordinary dividend (Brigham and

Ehrhardt 2013).

3) Ratio Analysis

3.1) Profitability Ratio

Gross Profit Margin Ratio

Formula ¿ Gross Profit × 100

Sales

Particulars 2016 (£m) 2015 (£m) 2014 (£m) 2013 (£m)

Sales (A) 3064 2972 2590 2389

Gross Profit (B) 3064 2972 2590 2389

Gross Profit Margin Ratio (B/A) 1 1 1 1

*Note: As ITV Plc is a service provider company, it does not have any cost of goods sold due to

not having an manufacturing process. Thus, Sales is assumed as Gross profit.

Operating Profit Margin Ratio

Formula ¿ Operating Profit × 100

Sales

Particulars 2016 (£m) 2015 (£m) 2014 (£m) 2013 (£m)

Sales (A) 3064 2972 2590 2389

Operating Profit (C) 604 666 651 546

Operating Profit Margin Ratio (C/A) 19.71% 22.41% 25.14% 22.85%

mention that there has been a 338% growth in adjusted EBITA. This growth I adjusted EBITA

has contributed toward the 20% growth in the payment of ordinary dividend (Brigham and

Ehrhardt 2013).

3) Ratio Analysis

3.1) Profitability Ratio

Gross Profit Margin Ratio

Formula ¿ Gross Profit × 100

Sales

Particulars 2016 (£m) 2015 (£m) 2014 (£m) 2013 (£m)

Sales (A) 3064 2972 2590 2389

Gross Profit (B) 3064 2972 2590 2389

Gross Profit Margin Ratio (B/A) 1 1 1 1

*Note: As ITV Plc is a service provider company, it does not have any cost of goods sold due to

not having an manufacturing process. Thus, Sales is assumed as Gross profit.

Operating Profit Margin Ratio

Formula ¿ Operating Profit × 100

Sales

Particulars 2016 (£m) 2015 (£m) 2014 (£m) 2013 (£m)

Sales (A) 3064 2972 2590 2389

Operating Profit (C) 604 666 651 546

Operating Profit Margin Ratio (C/A) 19.71% 22.41% 25.14% 22.85%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTS AND FINANCE

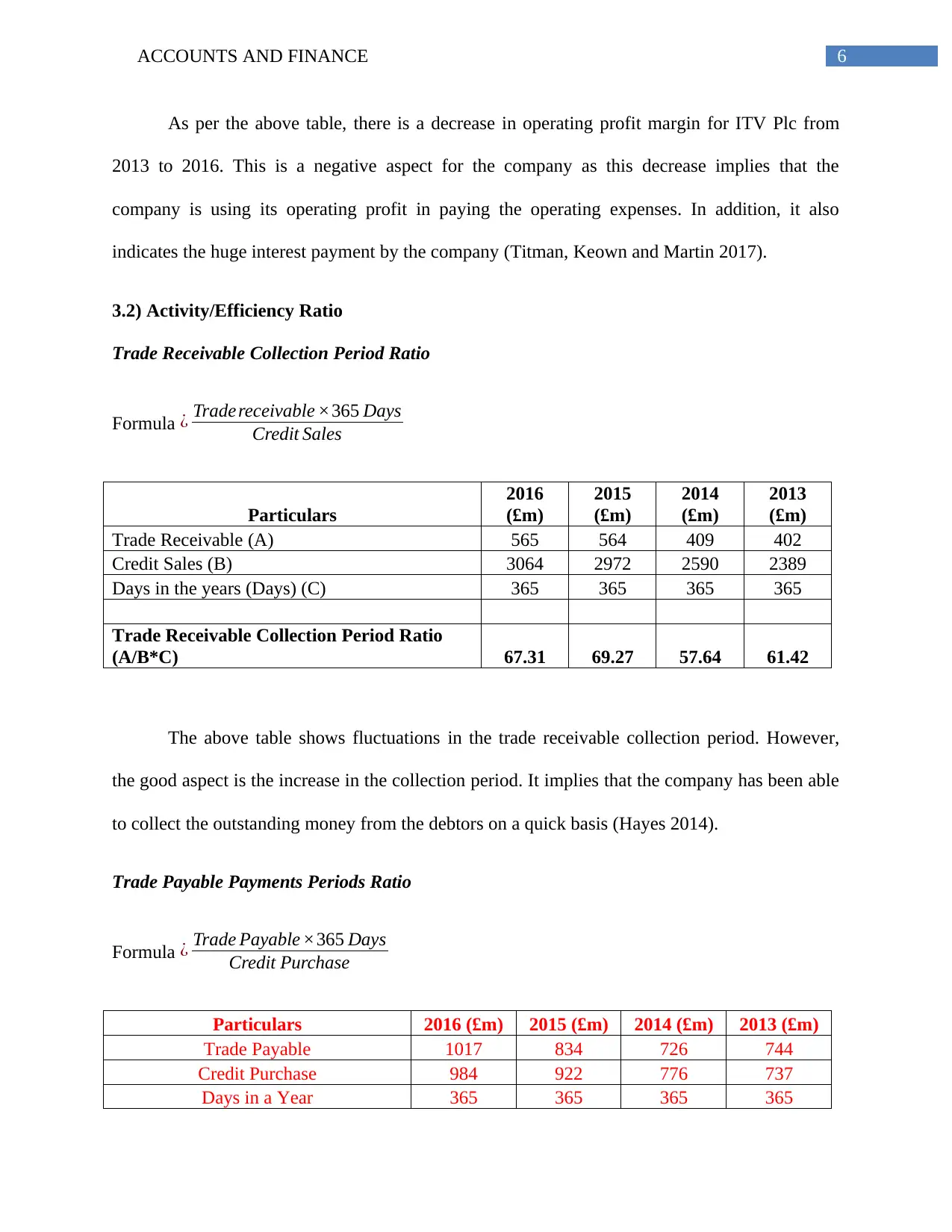

As per the above table, there is a decrease in operating profit margin for ITV Plc from

2013 to 2016. This is a negative aspect for the company as this decrease implies that the

company is using its operating profit in paying the operating expenses. In addition, it also

indicates the huge interest payment by the company (Titman, Keown and Martin 2017).

3.2) Activity/Efficiency Ratio

Trade Receivable Collection Period Ratio

Formula ¿ Trade receivable ×365 Days

Credit Sales

Particulars

2016

(£m)

2015

(£m)

2014

(£m)

2013

(£m)

Trade Receivable (A) 565 564 409 402

Credit Sales (B) 3064 2972 2590 2389

Days in the years (Days) (C) 365 365 365 365

Trade Receivable Collection Period Ratio

(A/B*C) 67.31 69.27 57.64 61.42

The above table shows fluctuations in the trade receivable collection period. However,

the good aspect is the increase in the collection period. It implies that the company has been able

to collect the outstanding money from the debtors on a quick basis (Hayes 2014).

Trade Payable Payments Periods Ratio

Formula ¿ Trade Payable ×365 Days

Credit Purchase

Particulars 2016 (£m) 2015 (£m) 2014 (£m) 2013 (£m)

Trade Payable 1017 834 726 744

Credit Purchase 984 922 776 737

Days in a Year 365 365 365 365

As per the above table, there is a decrease in operating profit margin for ITV Plc from

2013 to 2016. This is a negative aspect for the company as this decrease implies that the

company is using its operating profit in paying the operating expenses. In addition, it also

indicates the huge interest payment by the company (Titman, Keown and Martin 2017).

3.2) Activity/Efficiency Ratio

Trade Receivable Collection Period Ratio

Formula ¿ Trade receivable ×365 Days

Credit Sales

Particulars

2016

(£m)

2015

(£m)

2014

(£m)

2013

(£m)

Trade Receivable (A) 565 564 409 402

Credit Sales (B) 3064 2972 2590 2389

Days in the years (Days) (C) 365 365 365 365

Trade Receivable Collection Period Ratio

(A/B*C) 67.31 69.27 57.64 61.42

The above table shows fluctuations in the trade receivable collection period. However,

the good aspect is the increase in the collection period. It implies that the company has been able

to collect the outstanding money from the debtors on a quick basis (Hayes 2014).

Trade Payable Payments Periods Ratio

Formula ¿ Trade Payable ×365 Days

Credit Purchase

Particulars 2016 (£m) 2015 (£m) 2014 (£m) 2013 (£m)

Trade Payable 1017 834 726 744

Credit Purchase 984 922 776 737

Days in a Year 365 365 365 365

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTS AND FINANCE

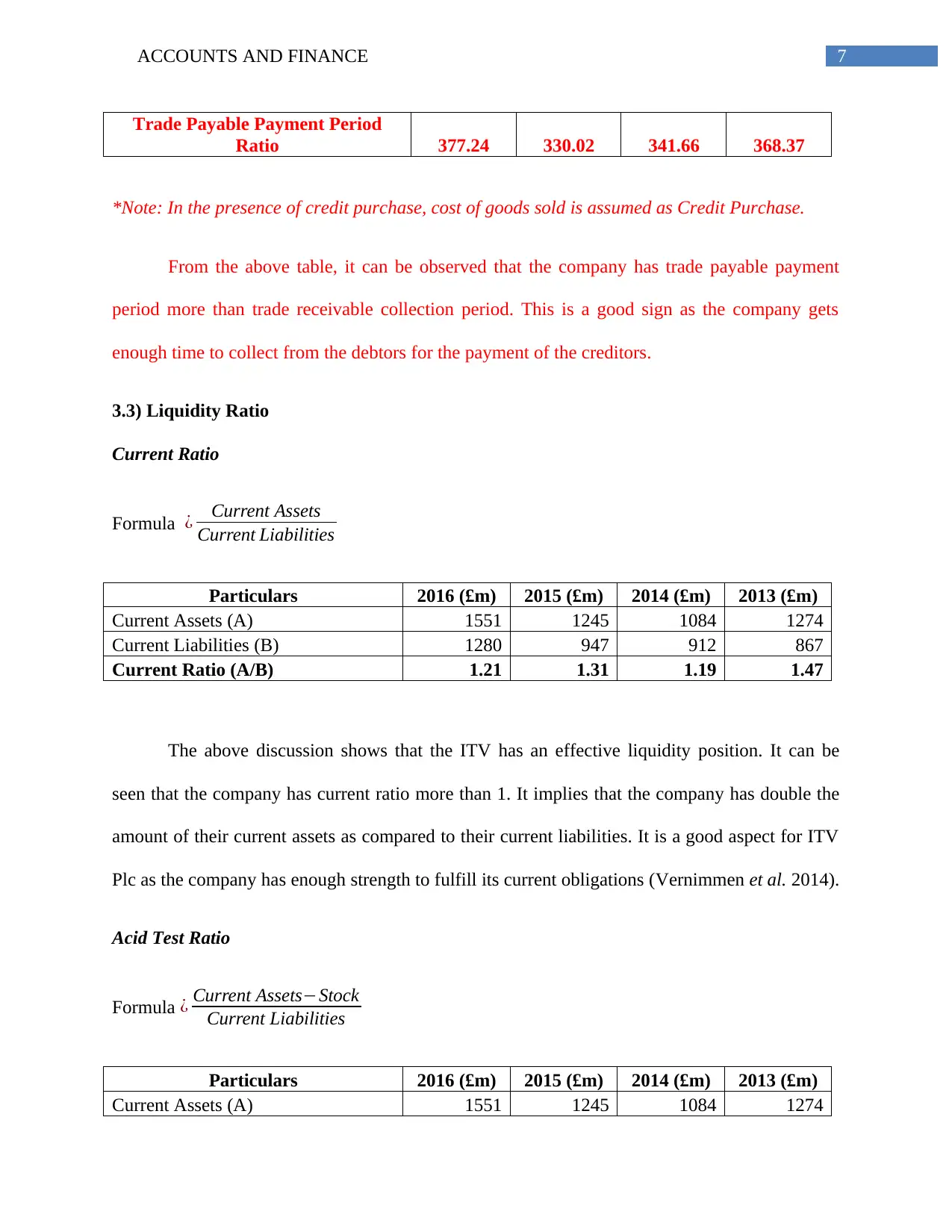

Trade Payable Payment Period

Ratio 377.24 330.02 341.66 368.37

*Note: In the presence of credit purchase, cost of goods sold is assumed as Credit Purchase.

From the above table, it can be observed that the company has trade payable payment

period more than trade receivable collection period. This is a good sign as the company gets

enough time to collect from the debtors for the payment of the creditors.

3.3) Liquidity Ratio

Current Ratio

Formula ¿ Current Assets

Current Liabilities

Particulars 2016 (£m) 2015 (£m) 2014 (£m) 2013 (£m)

Current Assets (A) 1551 1245 1084 1274

Current Liabilities (B) 1280 947 912 867

Current Ratio (A/B) 1.21 1.31 1.19 1.47

The above discussion shows that the ITV has an effective liquidity position. It can be

seen that the company has current ratio more than 1. It implies that the company has double the

amount of their current assets as compared to their current liabilities. It is a good aspect for ITV

Plc as the company has enough strength to fulfill its current obligations (Vernimmen et al. 2014).

Acid Test Ratio

Formula ¿ Current Assets−Stock

Current Liabilities

Particulars 2016 (£m) 2015 (£m) 2014 (£m) 2013 (£m)

Current Assets (A) 1551 1245 1084 1274

Trade Payable Payment Period

Ratio 377.24 330.02 341.66 368.37

*Note: In the presence of credit purchase, cost of goods sold is assumed as Credit Purchase.

From the above table, it can be observed that the company has trade payable payment

period more than trade receivable collection period. This is a good sign as the company gets

enough time to collect from the debtors for the payment of the creditors.

3.3) Liquidity Ratio

Current Ratio

Formula ¿ Current Assets

Current Liabilities

Particulars 2016 (£m) 2015 (£m) 2014 (£m) 2013 (£m)

Current Assets (A) 1551 1245 1084 1274

Current Liabilities (B) 1280 947 912 867

Current Ratio (A/B) 1.21 1.31 1.19 1.47

The above discussion shows that the ITV has an effective liquidity position. It can be

seen that the company has current ratio more than 1. It implies that the company has double the

amount of their current assets as compared to their current liabilities. It is a good aspect for ITV

Plc as the company has enough strength to fulfill its current obligations (Vernimmen et al. 2014).

Acid Test Ratio

Formula ¿ Current Assets−Stock

Current Liabilities

Particulars 2016 (£m) 2015 (£m) 2014 (£m) 2013 (£m)

Current Assets (A) 1551 1245 1084 1274

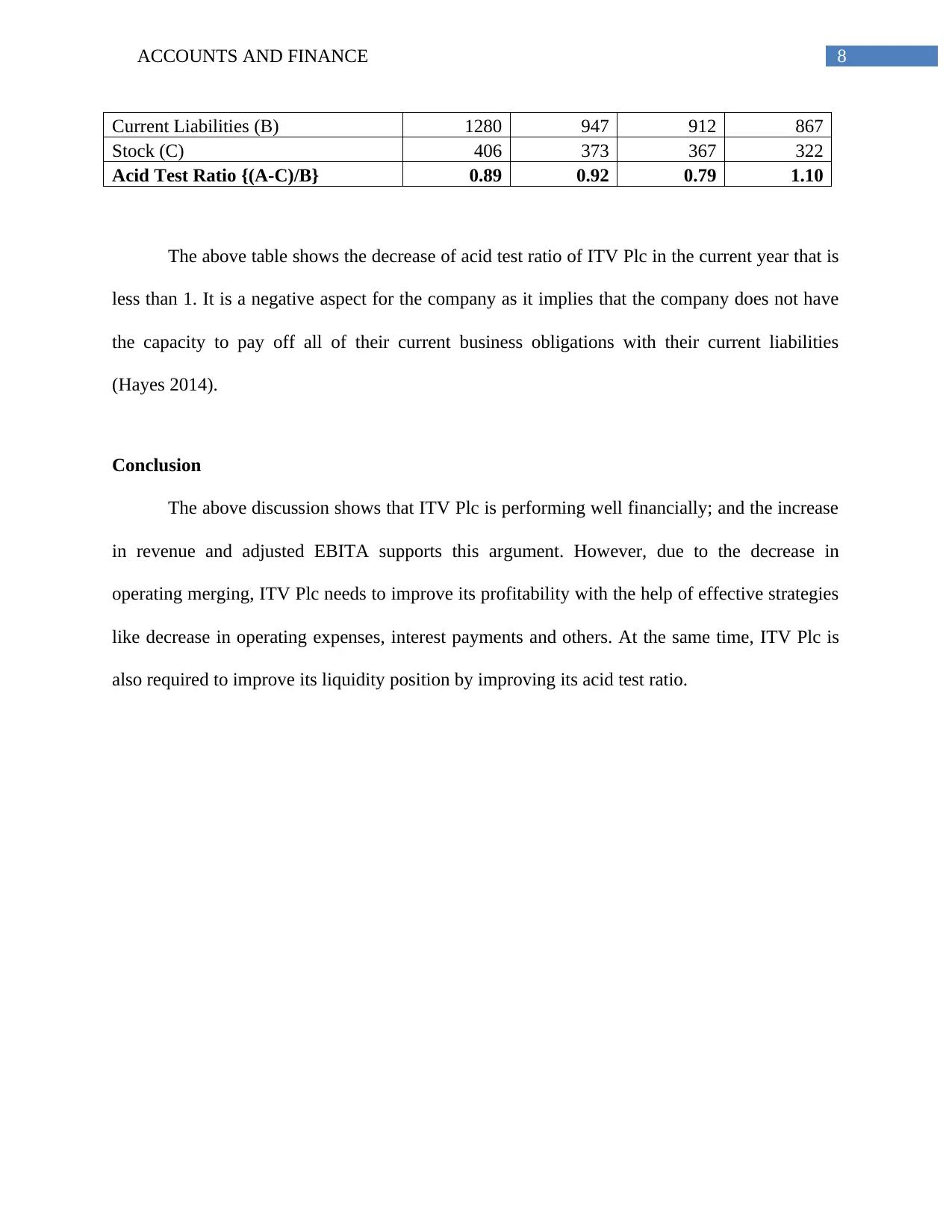

8ACCOUNTS AND FINANCE

Current Liabilities (B) 1280 947 912 867

Stock (C) 406 373 367 322

Acid Test Ratio {(A-C)/B} 0.89 0.92 0.79 1.10

The above table shows the decrease of acid test ratio of ITV Plc in the current year that is

less than 1. It is a negative aspect for the company as it implies that the company does not have

the capacity to pay off all of their current business obligations with their current liabilities

(Hayes 2014).

Conclusion

The above discussion shows that ITV Plc is performing well financially; and the increase

in revenue and adjusted EBITA supports this argument. However, due to the decrease in

operating merging, ITV Plc needs to improve its profitability with the help of effective strategies

like decrease in operating expenses, interest payments and others. At the same time, ITV Plc is

also required to improve its liquidity position by improving its acid test ratio.

Current Liabilities (B) 1280 947 912 867

Stock (C) 406 373 367 322

Acid Test Ratio {(A-C)/B} 0.89 0.92 0.79 1.10

The above table shows the decrease of acid test ratio of ITV Plc in the current year that is

less than 1. It is a negative aspect for the company as it implies that the company does not have

the capacity to pay off all of their current business obligations with their current liabilities

(Hayes 2014).

Conclusion

The above discussion shows that ITV Plc is performing well financially; and the increase

in revenue and adjusted EBITA supports this argument. However, due to the decrease in

operating merging, ITV Plc needs to improve its profitability with the help of effective strategies

like decrease in operating expenses, interest payments and others. At the same time, ITV Plc is

also required to improve its liquidity position by improving its acid test ratio.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTS AND FINANCE

References

Amalia, C. (2017). What Are Analysts Saying About the future of ITV plc’s (LON:ITV) Earnings

Prospects?. [online] Simply Wall St. Available at:

https://simplywall.st/stocks/gb/media/lse-itv/itv-shares/news/what-are-analysts-saying-about-the-

future-of-itv-plcs-lonitv-earnings-prospects/ [Accessed 28 Mar. 2018].

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Brigham, E.F. and Houston, J.F., 2012. Fundamentals of financial management. Cengage

Learning.

Editorial, R. (2018). ${Instrument_CompanyName} ${Instrument_Ric} Company Profile |

Reuters.com. [online] U.S. Available at: https://www.reuters.com/finance/stocks/company-

profile/ITV.L [Accessed 28 Mar. 2018].

Hayes, J., 2014. The theory and practice of change management. Palgrave Macmillan.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Itvplc.com. (2018). Market review. [online] Available at: http://www.itvplc.com/about/market-

review [Accessed 28 Mar. 2018].

Itvplc.com. (2018). What we do. [online] Available at: http://www.itvplc.com/about/what-we-do

[Accessed 28 Mar. 2018].

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

References

Amalia, C. (2017). What Are Analysts Saying About the future of ITV plc’s (LON:ITV) Earnings

Prospects?. [online] Simply Wall St. Available at:

https://simplywall.st/stocks/gb/media/lse-itv/itv-shares/news/what-are-analysts-saying-about-the-

future-of-itv-plcs-lonitv-earnings-prospects/ [Accessed 28 Mar. 2018].

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Brigham, E.F. and Houston, J.F., 2012. Fundamentals of financial management. Cengage

Learning.

Editorial, R. (2018). ${Instrument_CompanyName} ${Instrument_Ric} Company Profile |

Reuters.com. [online] U.S. Available at: https://www.reuters.com/finance/stocks/company-

profile/ITV.L [Accessed 28 Mar. 2018].

Hayes, J., 2014. The theory and practice of change management. Palgrave Macmillan.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Itvplc.com. (2018). Market review. [online] Available at: http://www.itvplc.com/about/market-

review [Accessed 28 Mar. 2018].

Itvplc.com. (2018). What we do. [online] Available at: http://www.itvplc.com/about/what-we-do

[Accessed 28 Mar. 2018].

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTS AND FINANCE

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate finance:

theory and practice. John Wiley & Sons.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate finance:

theory and practice. John Wiley & Sons.

11ACCOUNTS AND FINANCE

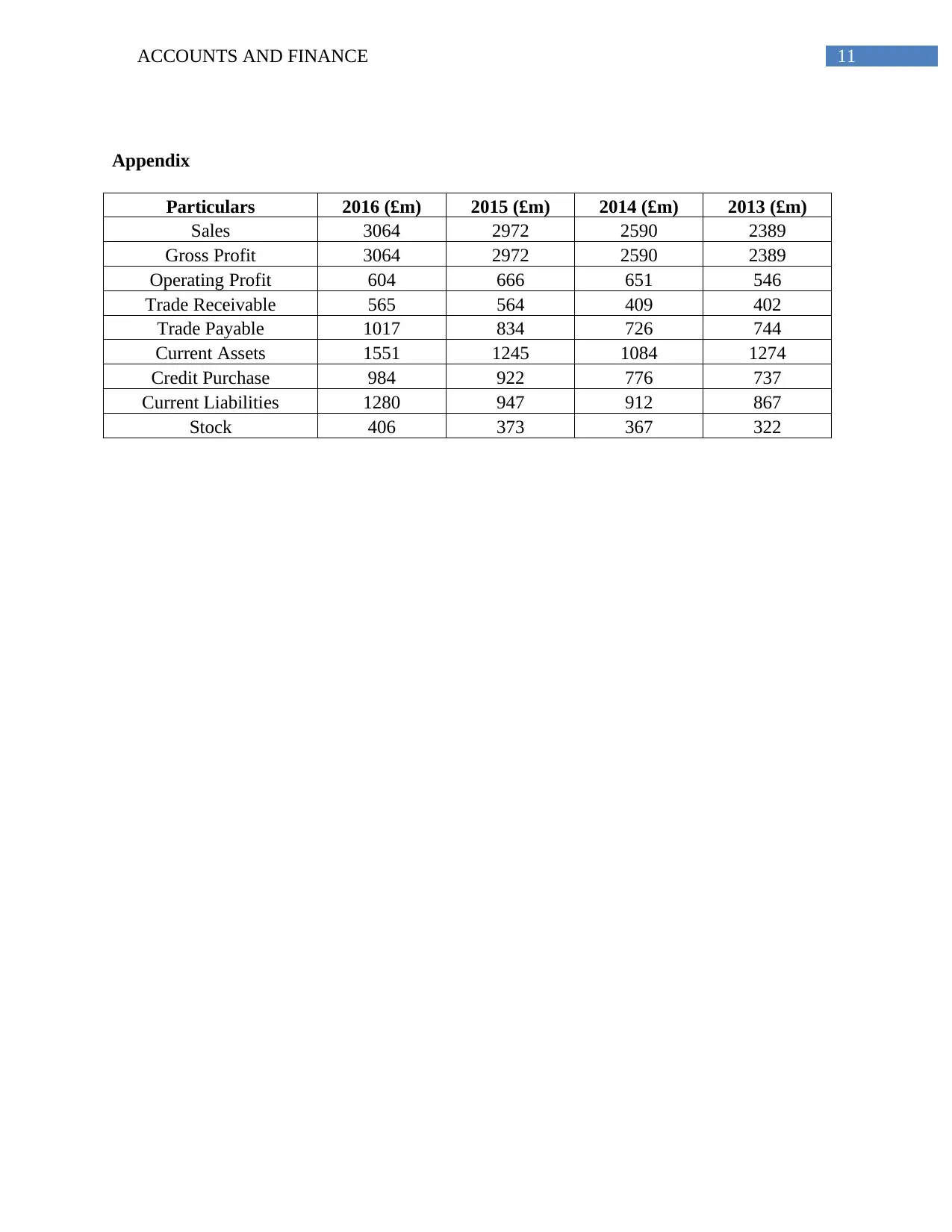

Appendix

Particulars 2016 (£m) 2015 (£m) 2014 (£m) 2013 (£m)

Sales 3064 2972 2590 2389

Gross Profit 3064 2972 2590 2389

Operating Profit 604 666 651 546

Trade Receivable 565 564 409 402

Trade Payable 1017 834 726 744

Current Assets 1551 1245 1084 1274

Credit Purchase 984 922 776 737

Current Liabilities 1280 947 912 867

Stock 406 373 367 322

Appendix

Particulars 2016 (£m) 2015 (£m) 2014 (£m) 2013 (£m)

Sales 3064 2972 2590 2389

Gross Profit 3064 2972 2590 2389

Operating Profit 604 666 651 546

Trade Receivable 565 564 409 402

Trade Payable 1017 834 726 744

Current Assets 1551 1245 1084 1274

Credit Purchase 984 922 776 737

Current Liabilities 1280 947 912 867

Stock 406 373 367 322

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.