Rangemaster PLC: Comprehensive Ratio Analysis and Financial Report

VerifiedAdded on 2023/01/10

|9

|1965

|22

Report

AI Summary

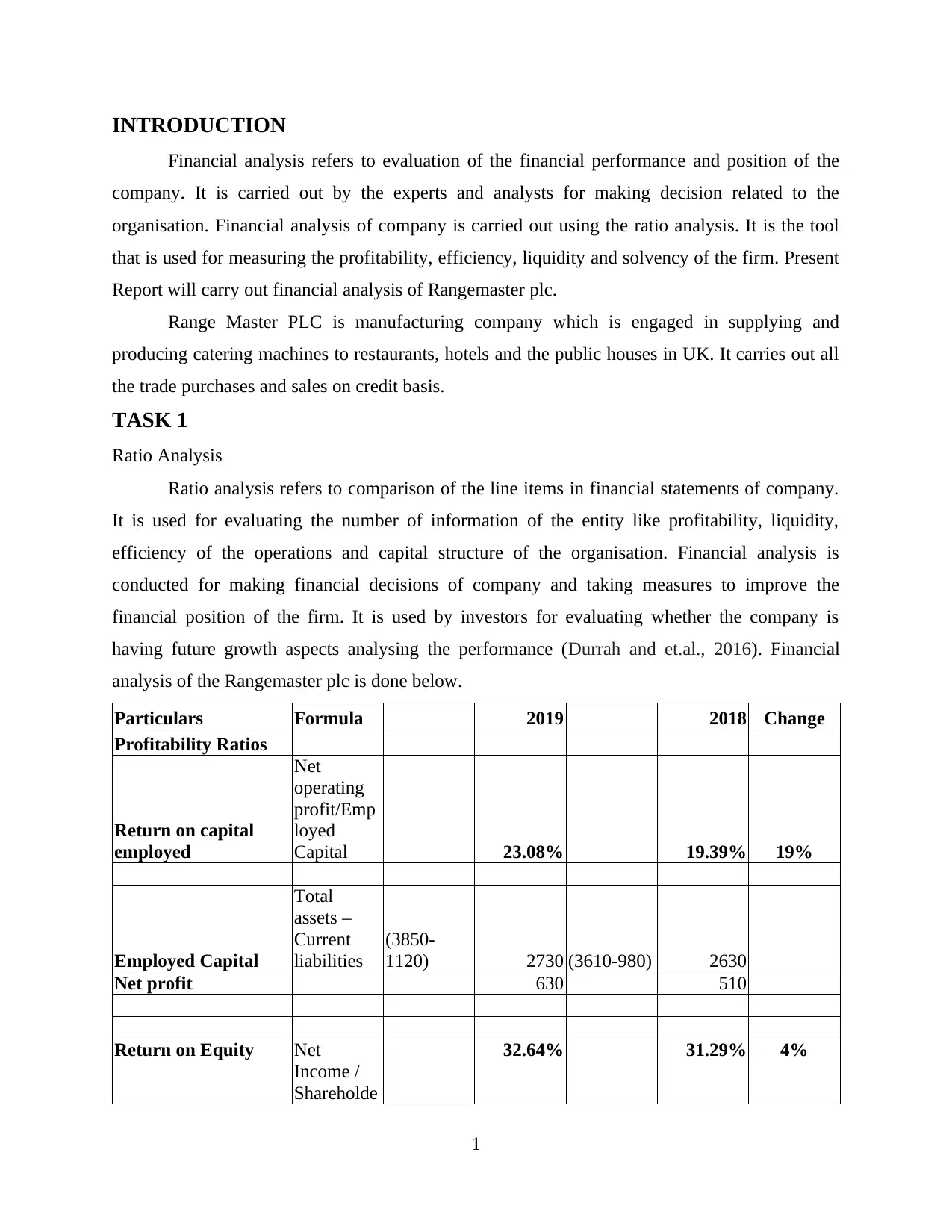

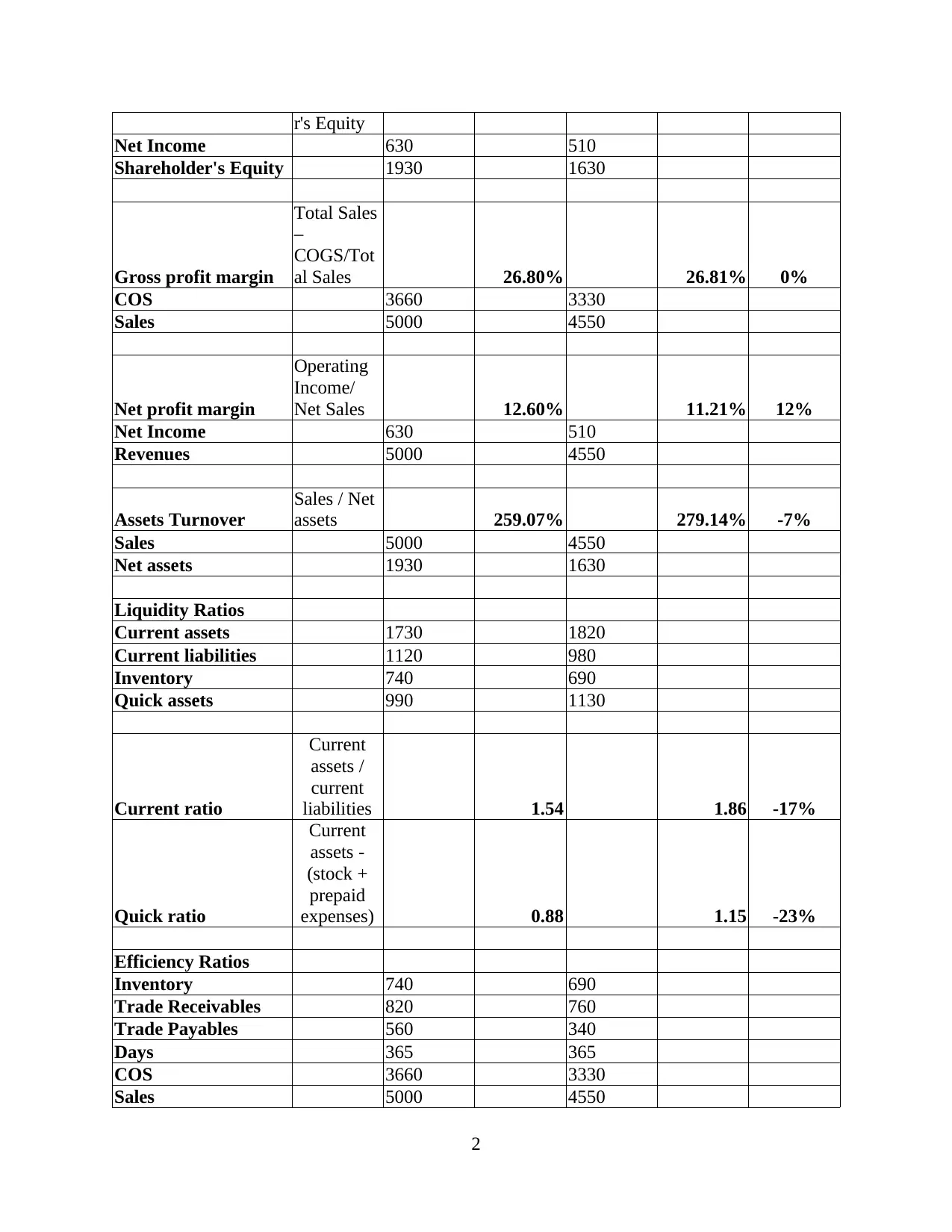

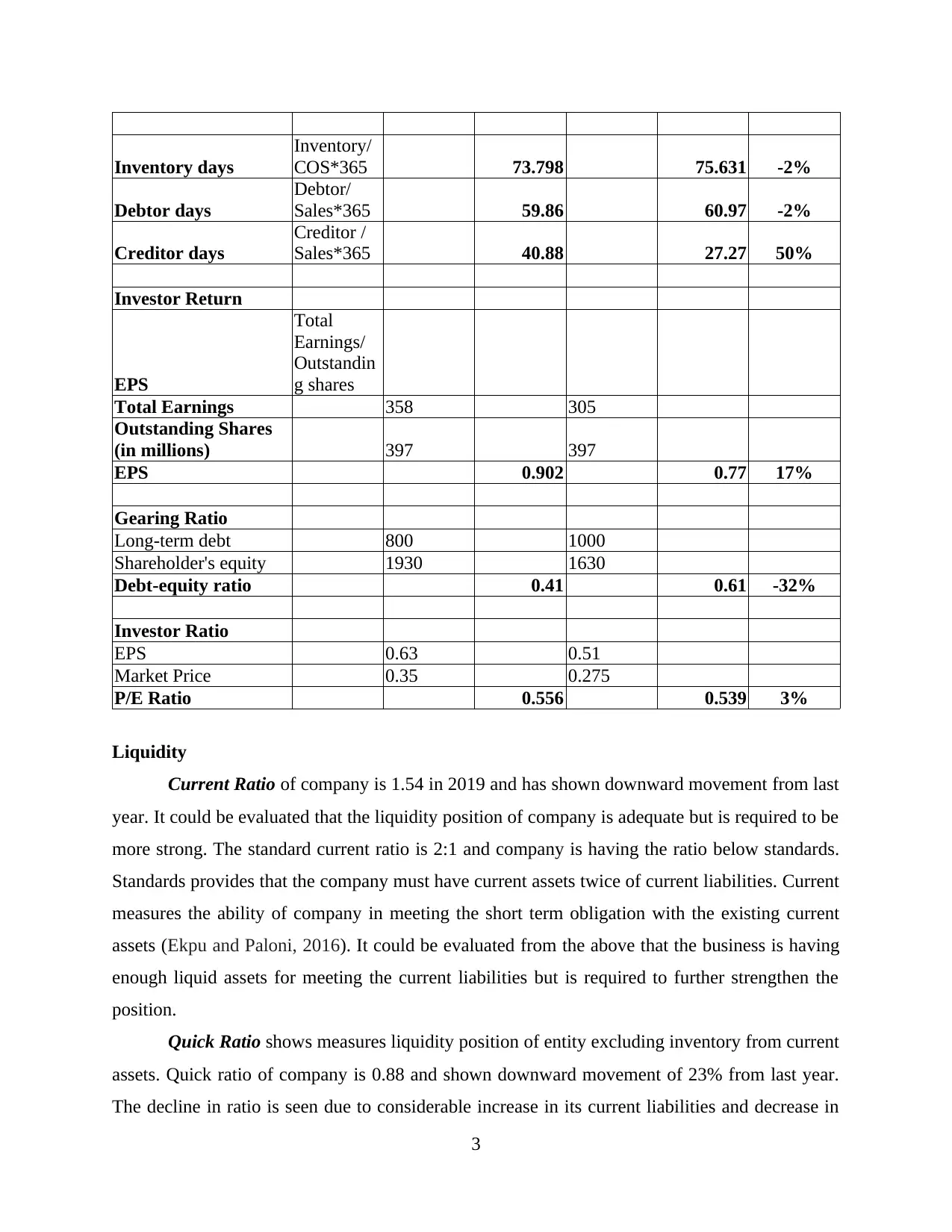

This report presents a detailed financial analysis of Rangemaster PLC using ratio analysis, evaluating its performance and financial position. The introduction outlines the purpose and scope, followed by an analysis of profitability, liquidity, efficiency, and capital structure. Profitability ratios, including Return on Capital Employed (ROCE) and Return on Equity (ROE), are assessed to gauge management's efficiency and return generation. Liquidity ratios, such as the current and quick ratios, are examined to determine the company's ability to meet short-term obligations. Efficiency ratios, including inventory, debtor, and creditor days, are analyzed to assess operational efficiency and cash cycle. The capital structure is evaluated using the debt-equity ratio, and investor ratios, such as the P/E ratio, are considered. The analysis reveals Rangemaster's strong financial performance, highlighting efficient resource utilization, adequate returns, and a favorable financial position, with recommendations for continued sustainability and growth. The report concludes with references to supporting literature.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.