Financial Performance Analysis of REA Group

VerifiedAdded on 2023/04/21

|18

|3922

|295

AI Summary

This report provides a detailed analysis of the financial performance of REA Group, including capital structure and financial health. Techniques like Beta, Cost of Equity, Gearing Ratios, WACC, and more are used to analyze the company's financial health. The report also discusses the models of CAPM and DGM, along with the capital structure of the company. Ratios are calculated to provide a transparent view of the company's finances.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: REA GROUP 0

REA GROUP

REA GROUP

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REA GROUP 1

Executive Summary

Under this report the detailed analysis of the financial performance of the Rea Group with

regards to the capita; structure and the financial health of the company. To analyse the

financial health different techniques have been used such as Beta, Cost of Equity, Gearing

Ratios, WACC and lot more. The share price of the REA Group is $75.50 and the share price

movement of the Rea Group is less movable in comparison to the market. According to the

findings it was observed that the REA Group can be treated as the company which faces the

less risk and is readily giving the return on equity to the investors. In this report further the

models of the CAPM and the DGM have been discussed in detail and alongside the capital

structure of the company are also displayed. Further the ratios are also calculated to give a

transparent view of the finances of the company via equity and debt.

1

Executive Summary

Under this report the detailed analysis of the financial performance of the Rea Group with

regards to the capita; structure and the financial health of the company. To analyse the

financial health different techniques have been used such as Beta, Cost of Equity, Gearing

Ratios, WACC and lot more. The share price of the REA Group is $75.50 and the share price

movement of the Rea Group is less movable in comparison to the market. According to the

findings it was observed that the REA Group can be treated as the company which faces the

less risk and is readily giving the return on equity to the investors. In this report further the

models of the CAPM and the DGM have been discussed in detail and alongside the capital

structure of the company are also displayed. Further the ratios are also calculated to give a

transparent view of the finances of the company via equity and debt.

1

REA GROUP 2

Table of Contents

Executive Summary...................................................................................................................3

Introduction................................................................................................................................4

2. Weighted Average Cost of Capital (WACC).....................................................................4

2.1. Cost of Equity (COE)/ Return on Equity........................................................................5

2.1.1. CAPM..........................................................................................................................5

2.1.2. DGM............................................................................................................................8

3. Capital Structure of REA Group......................................................................................11

3.1. Debt to Value Ratio.......................................................................................................11

3.2 Equity to Value Ratio.....................................................................................................12

3.3 Debt to Equity Ratio......................................................................................................13

4. Analysis and Recommendation............................................................................................13

References................................................................................................................................15

6. Appendix I............................................................................................................................16

7. Appendix II..........................................................................................................................19

2

Table of Contents

Executive Summary...................................................................................................................3

Introduction................................................................................................................................4

2. Weighted Average Cost of Capital (WACC).....................................................................4

2.1. Cost of Equity (COE)/ Return on Equity........................................................................5

2.1.1. CAPM..........................................................................................................................5

2.1.2. DGM............................................................................................................................8

3. Capital Structure of REA Group......................................................................................11

3.1. Debt to Value Ratio.......................................................................................................11

3.2 Equity to Value Ratio.....................................................................................................12

3.3 Debt to Equity Ratio......................................................................................................13

4. Analysis and Recommendation............................................................................................13

References................................................................................................................................15

6. Appendix I............................................................................................................................16

7. Appendix II..........................................................................................................................19

2

REA GROUP 3

Introduction

REA Group Limited and its subsidiary companies known as the REA Group which makes up

one of the most renowned flagship know for the global estate advertising company. The

headquarters of the REA Group is situated in Melbourne, Australia. The company is listed on

the Australian Stock Exchange and had A$807 million in the form of the revenue. The

company was founded in the year 1995 and furthermore, the company now operates in the

property websites among the 10 countries and it is being utilised by the 19000 agents. The

number of the visitors per month is approximately 8.8 million (REA GROUP, 2018). The

company also purchased the most demanded magazine Square foot in the year 2007, which is

also known as the first acquisition in Asia. Furthermore, the scenario changed for the

managers when the booking rental inspections were made easier as the company went into

the agreement with the Inspect Real estate. In this report, authors have gathered the financial

information regarding the REA Group from the website of the company, annual reports, the

other websites inclusive of Morningstar, Morning Star. After collecting the data from these

websites the authors have applied the technique of the CAPM, DGM, further using the cost of

equity the WACC has been calculated. Also the ratio analysis have been calculated and

necessary recommendations have also been provided to the company to make the necessary

changes where there are any variances and the negative impact on the performance of the

company (REA, 2018).

2. Weighted Average Cost of Capital (WACC)

Security holders are required to finance the assets and this can be done by applying the rate of

the weighted average cost of capital to pay on an average to all the holders of the assets. In

simpler words the shareholders are expecting the return on the investments made by them.

For the calculation of WACC there is a formula derived, and the formula is outlined below

(Frank & Shen, 2016).

3

Introduction

REA Group Limited and its subsidiary companies known as the REA Group which makes up

one of the most renowned flagship know for the global estate advertising company. The

headquarters of the REA Group is situated in Melbourne, Australia. The company is listed on

the Australian Stock Exchange and had A$807 million in the form of the revenue. The

company was founded in the year 1995 and furthermore, the company now operates in the

property websites among the 10 countries and it is being utilised by the 19000 agents. The

number of the visitors per month is approximately 8.8 million (REA GROUP, 2018). The

company also purchased the most demanded magazine Square foot in the year 2007, which is

also known as the first acquisition in Asia. Furthermore, the scenario changed for the

managers when the booking rental inspections were made easier as the company went into

the agreement with the Inspect Real estate. In this report, authors have gathered the financial

information regarding the REA Group from the website of the company, annual reports, the

other websites inclusive of Morningstar, Morning Star. After collecting the data from these

websites the authors have applied the technique of the CAPM, DGM, further using the cost of

equity the WACC has been calculated. Also the ratio analysis have been calculated and

necessary recommendations have also been provided to the company to make the necessary

changes where there are any variances and the negative impact on the performance of the

company (REA, 2018).

2. Weighted Average Cost of Capital (WACC)

Security holders are required to finance the assets and this can be done by applying the rate of

the weighted average cost of capital to pay on an average to all the holders of the assets. In

simpler words the shareholders are expecting the return on the investments made by them.

For the calculation of WACC there is a formula derived, and the formula is outlined below

(Frank & Shen, 2016).

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REA GROUP 4

WACC = Value of equity

value of the company ×Cost ofEquiry+ Value of Preference Shares

Value of the company ×Cost of Preference Shares+ V

Valu

2.1. Cost of Equity (COE)/ Return on Equity

The cost of equity is the required return that is the basic requirement of the company to figure

out whether the investment is meeting the capital return requirements. It is basically the

requirement of most of the companies and it is also used as a capital budgeting threshold rate.

The cost of equity is nothing but a demand from the market in the form of the compensation

against maintaining the assets and having the ability to bear the risk of the ownership. The

traditional formula to calculate the cost of the equity can be found below (Dhaliwal, Judd,

Serfling & Shaikh, 2016).

2.1.1. CAPM

Capital asset pricing model is the model designed to determine the theoretically rate of return

to make the decisions whether the investment shall be added in the portfolio or not.

In order to calculate CAPM, following formula can be used. The main purpose of this model

is to set a path for the asset’s sensitivity to the non-diversifiable risk can also be termed as the

market risk or the systematic risk. The risk is determined the Beta quantity along with the risk

free rate of return and the market rate of return (Barberis, Greenwood, Jin & Shleifer, 2015).

CAPM =Risk free return +( Market Risk Premium)

4

COST OF EQUITY= DIVIDENDS PER SHARE / CURRENT MARKET VALUE OF

STOCK + GROWTH ARTE OF DIVIDENDS

WACC = Value of equity

value of the company ×Cost ofEquiry+ Value of Preference Shares

Value of the company ×Cost of Preference Shares+ V

Valu

2.1. Cost of Equity (COE)/ Return on Equity

The cost of equity is the required return that is the basic requirement of the company to figure

out whether the investment is meeting the capital return requirements. It is basically the

requirement of most of the companies and it is also used as a capital budgeting threshold rate.

The cost of equity is nothing but a demand from the market in the form of the compensation

against maintaining the assets and having the ability to bear the risk of the ownership. The

traditional formula to calculate the cost of the equity can be found below (Dhaliwal, Judd,

Serfling & Shaikh, 2016).

2.1.1. CAPM

Capital asset pricing model is the model designed to determine the theoretically rate of return

to make the decisions whether the investment shall be added in the portfolio or not.

In order to calculate CAPM, following formula can be used. The main purpose of this model

is to set a path for the asset’s sensitivity to the non-diversifiable risk can also be termed as the

market risk or the systematic risk. The risk is determined the Beta quantity along with the risk

free rate of return and the market rate of return (Barberis, Greenwood, Jin & Shleifer, 2015).

CAPM =Risk free return +( Market Risk Premium)

4

COST OF EQUITY= DIVIDENDS PER SHARE / CURRENT MARKET VALUE OF

STOCK + GROWTH ARTE OF DIVIDENDS

REA GROUP 5

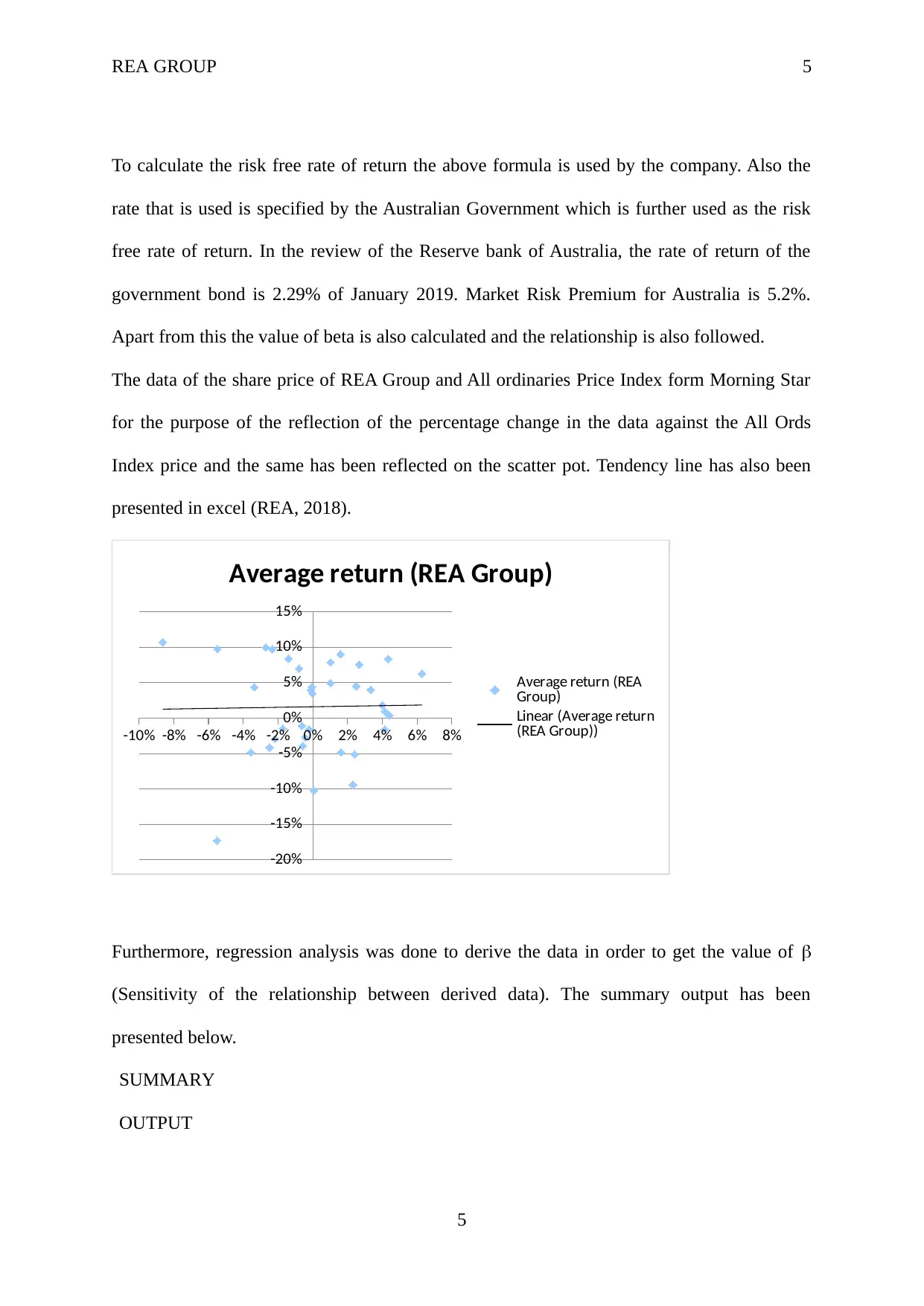

To calculate the risk free rate of return the above formula is used by the company. Also the

rate that is used is specified by the Australian Government which is further used as the risk

free rate of return. In the review of the Reserve bank of Australia, the rate of return of the

government bond is 2.29% of January 2019. Market Risk Premium for Australia is 5.2%.

Apart from this the value of beta is also calculated and the relationship is also followed.

The data of the share price of REA Group and All ordinaries Price Index form Morning Star

for the purpose of the reflection of the percentage change in the data against the All Ords

Index price and the same has been reflected on the scatter pot. Tendency line has also been

presented in excel (REA, 2018).

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Average return (REA Group)

Average return (REA

Group)

Linear (Average return

(REA Group))

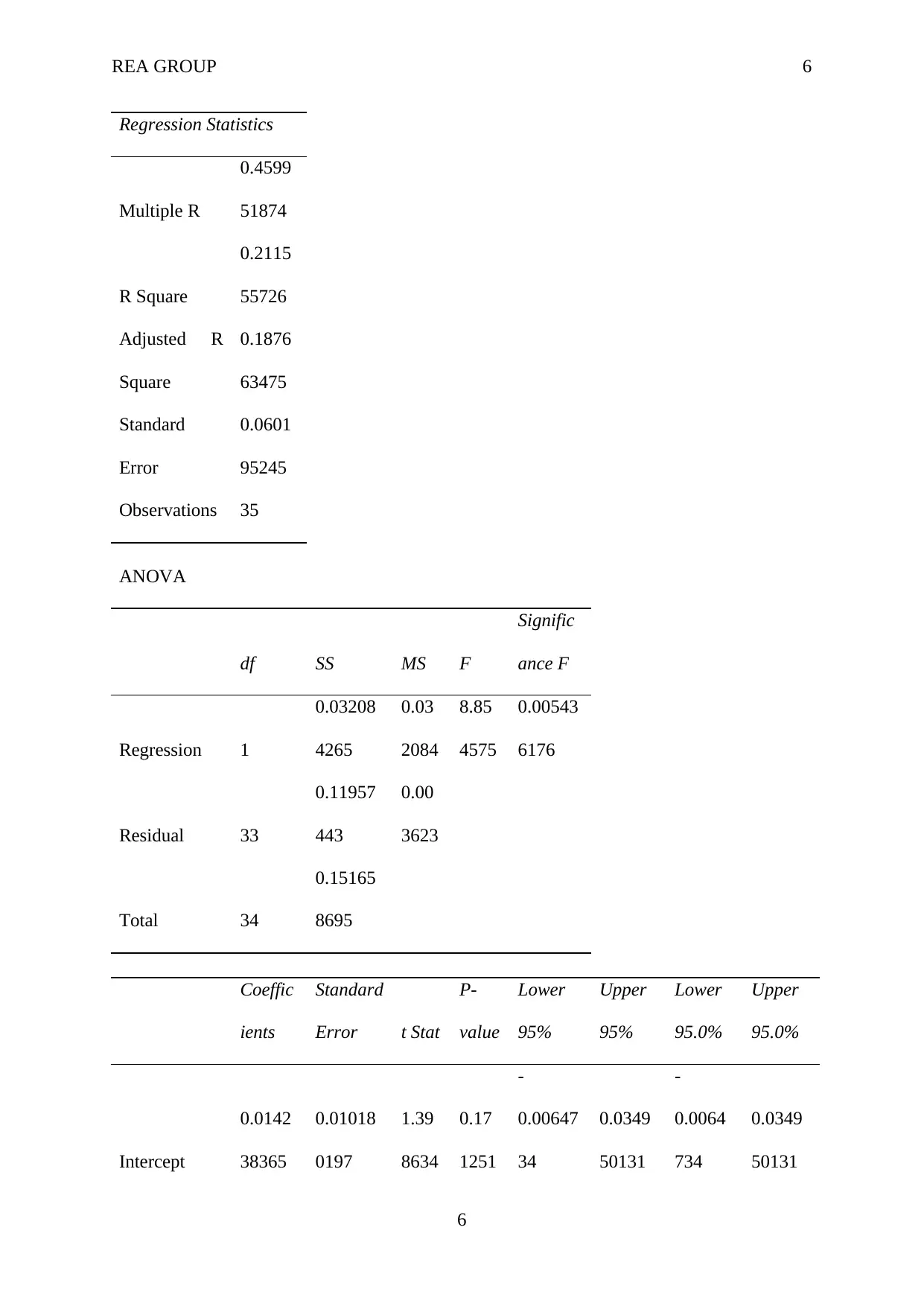

Furthermore, regression analysis was done to derive the data in order to get the value of

(Sensitivity of the relationship between derived data). The summary output has been

presented below.

SUMMARY

OUTPUT

5

To calculate the risk free rate of return the above formula is used by the company. Also the

rate that is used is specified by the Australian Government which is further used as the risk

free rate of return. In the review of the Reserve bank of Australia, the rate of return of the

government bond is 2.29% of January 2019. Market Risk Premium for Australia is 5.2%.

Apart from this the value of beta is also calculated and the relationship is also followed.

The data of the share price of REA Group and All ordinaries Price Index form Morning Star

for the purpose of the reflection of the percentage change in the data against the All Ords

Index price and the same has been reflected on the scatter pot. Tendency line has also been

presented in excel (REA, 2018).

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Average return (REA Group)

Average return (REA

Group)

Linear (Average return

(REA Group))

Furthermore, regression analysis was done to derive the data in order to get the value of

(Sensitivity of the relationship between derived data). The summary output has been

presented below.

SUMMARY

OUTPUT

5

REA GROUP 6

Regression Statistics

Multiple R

0.4599

51874

R Square

0.2115

55726

Adjusted R

Square

0.1876

63475

Standard

Error

0.0601

95245

Observations 35

ANOVA

df SS MS F

Signific

ance F

Regression 1

0.03208

4265

0.03

2084

8.85

4575

0.00543

6176

Residual 33

0.11957

443

0.00

3623

Total 34

0.15165

8695

Coeffic

ients

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.0142

38365

0.01018

0197

1.39

8634

0.17

1251

-

0.00647

34

0.0349

50131

-

0.0064

734

0.0349

50131

6

Regression Statistics

Multiple R

0.4599

51874

R Square

0.2115

55726

Adjusted R

Square

0.1876

63475

Standard

Error

0.0601

95245

Observations 35

ANOVA

df SS MS F

Signific

ance F

Regression 1

0.03208

4265

0.03

2084

8.85

4575

0.00543

6176

Residual 33

0.11957

443

0.00

3623

Total 34

0.15165

8695

Coeffic

ients

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.0142

38365

0.01018

0197

1.39

8634

0.17

1251

-

0.00647

34

0.0349

50131

-

0.0064

734

0.0349

50131

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REA GROUP 7

X Variable 1

0.9445

22919

0.31741

5873

2.97

5664

0.00

5436

0.29873

5471

1.5903

10368

0.2987

35471

1.5903

10368

According to the summary of the regression output the final analysis is that the sensitivity

relationship accounts for 94.4%, i.e. the value of the = 0.944522919. Furthermore, the

website of the Morning Star showcase the value of Beta is 1.21, whereas the beta value

according to the website of the Reuters of beta value is 1.31 (Reuters, 2018). Be that as it

may, the estimation of will rely upon the timeframe taken in to calculations, for example,

week after week/month to month information (Austin & Steyerberg, 2015). In this way,

creators have futher determined for the future estimations = 0.944522919 (Chatterjee &

Hadi, 2015).

Based on the calculated figures, CAPM has been calculated as follows.

CAPM =0.029+0.523 (0.94)

= 0.522

2.1.2. DGM

Dividend Growth model, also known as the Gordon growth model, is the method of

calculating the intrinsic value of the stock which does not include the impact of the current

market conditions. The main feature of this model is the equalisation of the present value to

the stock’s future dividend (Zhang, Lü, Ran & Han, 2016).

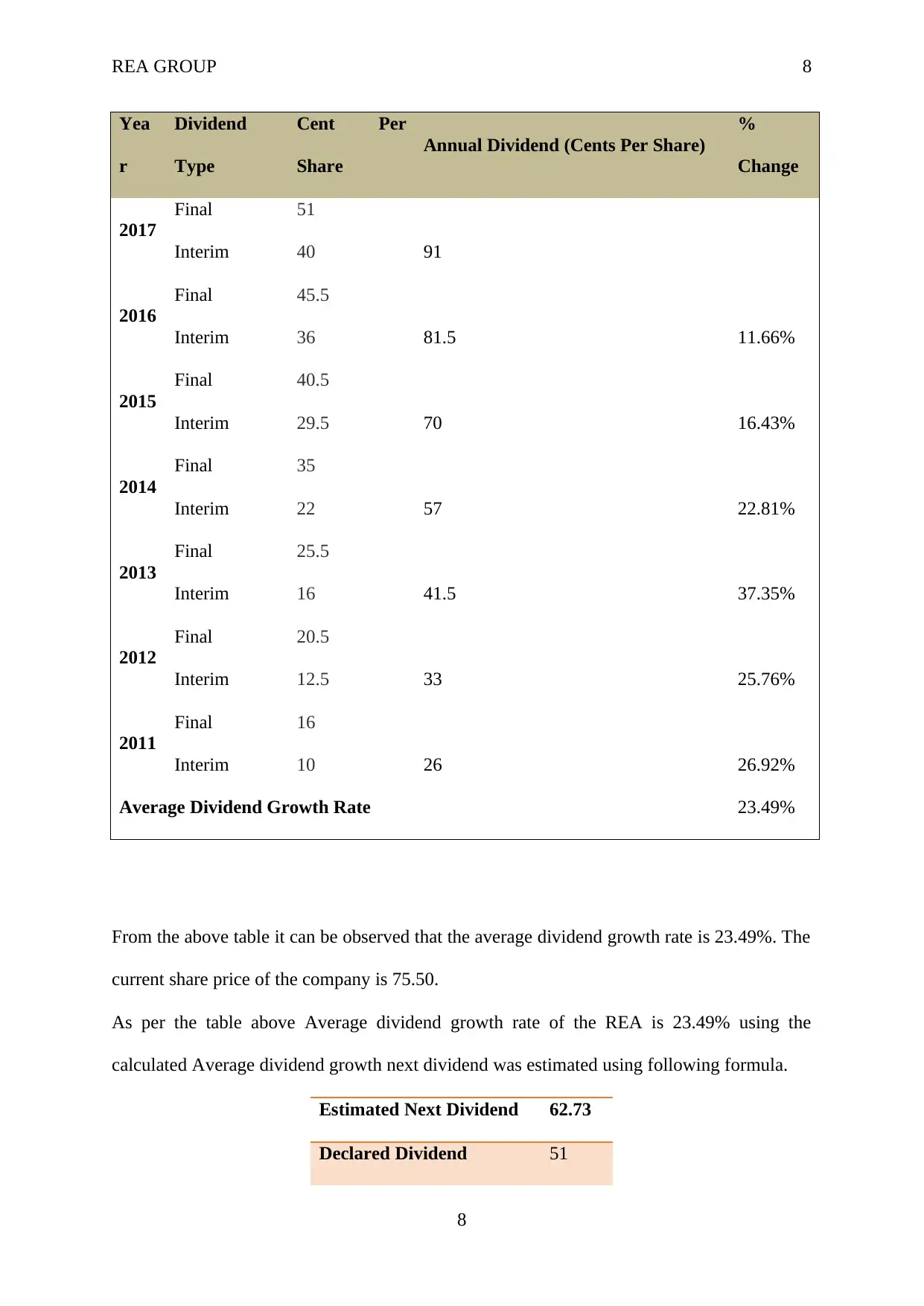

Return on equity is also calculated using the assistance of the DGM Model taking the

dividends as the base which is extracted from the annual reports of the REA Group and also

from the website of the morning star. The dividends declared by the company from the year

2011 to 2017 are presented in the table below.

7

X Variable 1

0.9445

22919

0.31741

5873

2.97

5664

0.00

5436

0.29873

5471

1.5903

10368

0.2987

35471

1.5903

10368

According to the summary of the regression output the final analysis is that the sensitivity

relationship accounts for 94.4%, i.e. the value of the = 0.944522919. Furthermore, the

website of the Morning Star showcase the value of Beta is 1.21, whereas the beta value

according to the website of the Reuters of beta value is 1.31 (Reuters, 2018). Be that as it

may, the estimation of will rely upon the timeframe taken in to calculations, for example,

week after week/month to month information (Austin & Steyerberg, 2015). In this way,

creators have futher determined for the future estimations = 0.944522919 (Chatterjee &

Hadi, 2015).

Based on the calculated figures, CAPM has been calculated as follows.

CAPM =0.029+0.523 (0.94)

= 0.522

2.1.2. DGM

Dividend Growth model, also known as the Gordon growth model, is the method of

calculating the intrinsic value of the stock which does not include the impact of the current

market conditions. The main feature of this model is the equalisation of the present value to

the stock’s future dividend (Zhang, Lü, Ran & Han, 2016).

Return on equity is also calculated using the assistance of the DGM Model taking the

dividends as the base which is extracted from the annual reports of the REA Group and also

from the website of the morning star. The dividends declared by the company from the year

2011 to 2017 are presented in the table below.

7

REA GROUP 8

Yea

r

Dividend

Type

Cent Per

Share

Annual Dividend (Cents Per Share)

%

Change

2017

Final 51

Interim 40 91

2016

Final 45.5

Interim 36 81.5 11.66%

2015

Final 40.5

Interim 29.5 70 16.43%

2014

Final 35

Interim 22 57 22.81%

2013

Final 25.5

Interim 16 41.5 37.35%

2012

Final 20.5

Interim 12.5 33 25.76%

2011

Final 16

Interim 10 26 26.92%

Average Dividend Growth Rate 23.49%

From the above table it can be observed that the average dividend growth rate is 23.49%. The

current share price of the company is 75.50.

As per the table above Average dividend growth rate of the REA is 23.49% using the

calculated Average dividend growth next dividend was estimated using following formula.

Estimated Next Dividend 62.73

Declared Dividend 51

8

Yea

r

Dividend

Type

Cent Per

Share

Annual Dividend (Cents Per Share)

%

Change

2017

Final 51

Interim 40 91

2016

Final 45.5

Interim 36 81.5 11.66%

2015

Final 40.5

Interim 29.5 70 16.43%

2014

Final 35

Interim 22 57 22.81%

2013

Final 25.5

Interim 16 41.5 37.35%

2012

Final 20.5

Interim 12.5 33 25.76%

2011

Final 16

Interim 10 26 26.92%

Average Dividend Growth Rate 23.49%

From the above table it can be observed that the average dividend growth rate is 23.49%. The

current share price of the company is 75.50.

As per the table above Average dividend growth rate of the REA is 23.49% using the

calculated Average dividend growth next dividend was estimated using following formula.

Estimated Next Dividend 62.73

Declared Dividend 51

8

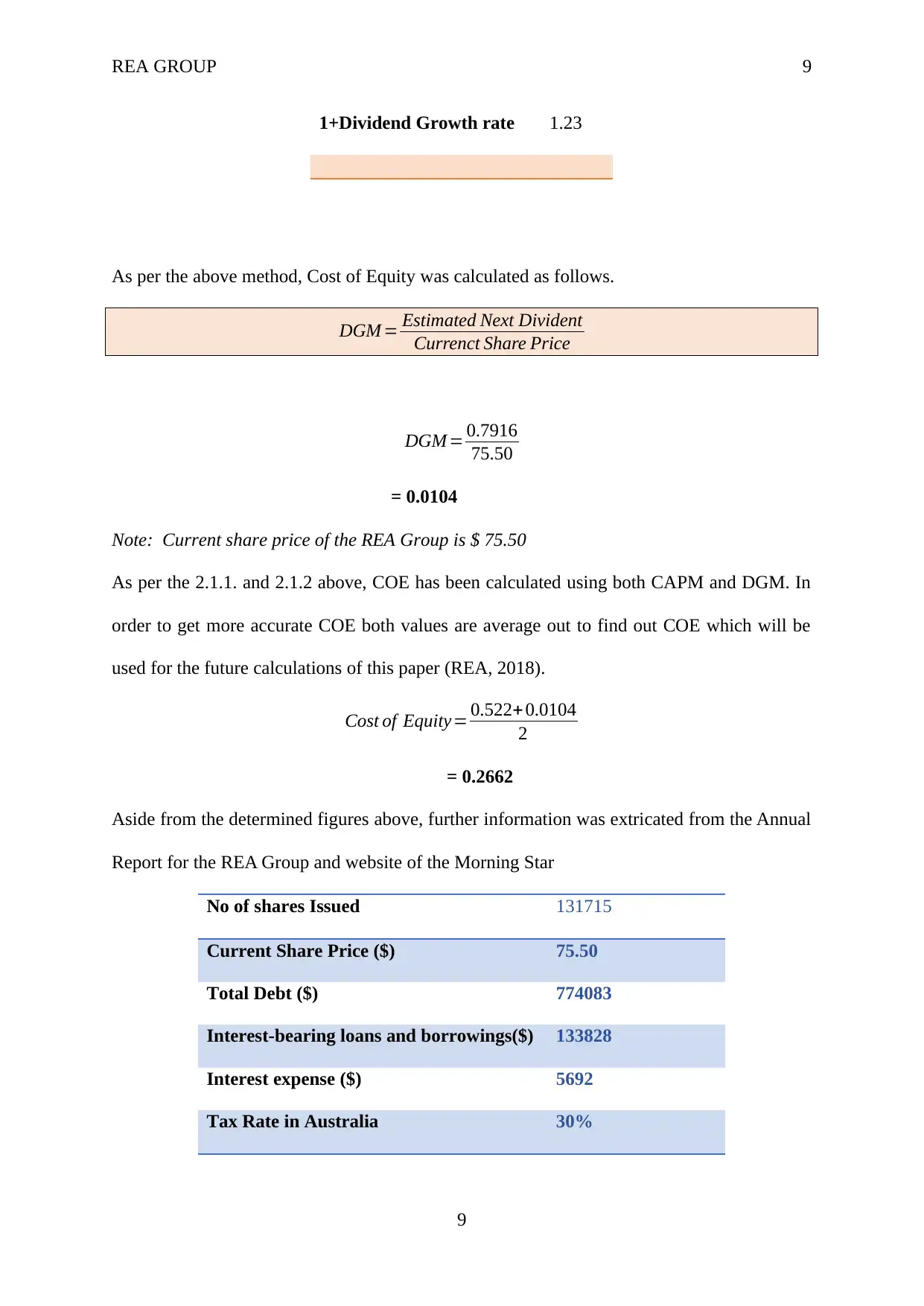

REA GROUP 9

1+Dividend Growth rate 1.23

As per the above method, Cost of Equity was calculated as follows.

DGM = Estimated Next Divident

Currenct Share Price

DGM = 0.7916

75.50

= 0.0104

Note: Current share price of the REA Group is $ 75.50

As per the 2.1.1. and 2.1.2 above, COE has been calculated using both CAPM and DGM. In

order to get more accurate COE both values are average out to find out COE which will be

used for the future calculations of this paper (REA, 2018).

Cost of Equity= 0.522+ 0.0104

2

= 0.2662

Aside from the determined figures above, further information was extricated from the Annual

Report for the REA Group and website of the Morning Star

No of shares Issued 131715

Current Share Price ($) 75.50

Total Debt ($) 774083

Interest-bearing loans and borrowings($) 133828

Interest expense ($) 5692

Tax Rate in Australia 30%

9

1+Dividend Growth rate 1.23

As per the above method, Cost of Equity was calculated as follows.

DGM = Estimated Next Divident

Currenct Share Price

DGM = 0.7916

75.50

= 0.0104

Note: Current share price of the REA Group is $ 75.50

As per the 2.1.1. and 2.1.2 above, COE has been calculated using both CAPM and DGM. In

order to get more accurate COE both values are average out to find out COE which will be

used for the future calculations of this paper (REA, 2018).

Cost of Equity= 0.522+ 0.0104

2

= 0.2662

Aside from the determined figures above, further information was extricated from the Annual

Report for the REA Group and website of the Morning Star

No of shares Issued 131715

Current Share Price ($) 75.50

Total Debt ($) 774083

Interest-bearing loans and borrowings($) 133828

Interest expense ($) 5692

Tax Rate in Australia 30%

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REA GROUP 10

Based on the above table, followings were calculated.

Cost of Debt= Interest expense

Interest −bearingloans∧borrowings

= 5692/133828

= 0.0425

Market value of the Equity ($) = No of shares outstanding x Share price

= 131715 x 75.50

= 9944482.5

Market Value of company ($) = Market Value of Equity + Total Debt

= 9944482.5 + 774083

= 10718565.5

Since the preference shares has not been issued by REA Group WACC calculated as follows.

WACC= Value of equity / value of the company × Cost of Equity+ Value of Preference Shares / Value of the

+ Value of Debt

Value of the company ×Cost of Debt × (1-Corporate Tax Rate )

WACC = 9944482.5

10718565.5 × 0.266+ 774083

10718565.5 ×0.0425 ×(1−0.3)

= 0.259

3. Capital Structure of REA Group

So as to break down the organization top to bottom following analysis was undertaken out.

3.1. Debt to Value Ratio

The debt to the value ratio is the ratio which comes under the category of the gearing ratio

and the same are calculated to determine how the company is being financed in comparison

10

Based on the above table, followings were calculated.

Cost of Debt= Interest expense

Interest −bearingloans∧borrowings

= 5692/133828

= 0.0425

Market value of the Equity ($) = No of shares outstanding x Share price

= 131715 x 75.50

= 9944482.5

Market Value of company ($) = Market Value of Equity + Total Debt

= 9944482.5 + 774083

= 10718565.5

Since the preference shares has not been issued by REA Group WACC calculated as follows.

WACC= Value of equity / value of the company × Cost of Equity+ Value of Preference Shares / Value of the

+ Value of Debt

Value of the company ×Cost of Debt × (1-Corporate Tax Rate )

WACC = 9944482.5

10718565.5 × 0.266+ 774083

10718565.5 ×0.0425 ×(1−0.3)

= 0.259

3. Capital Structure of REA Group

So as to break down the organization top to bottom following analysis was undertaken out.

3.1. Debt to Value Ratio

The debt to the value ratio is the ratio which comes under the category of the gearing ratio

and the same are calculated to determine how the company is being financed in comparison

10

REA GROUP 11

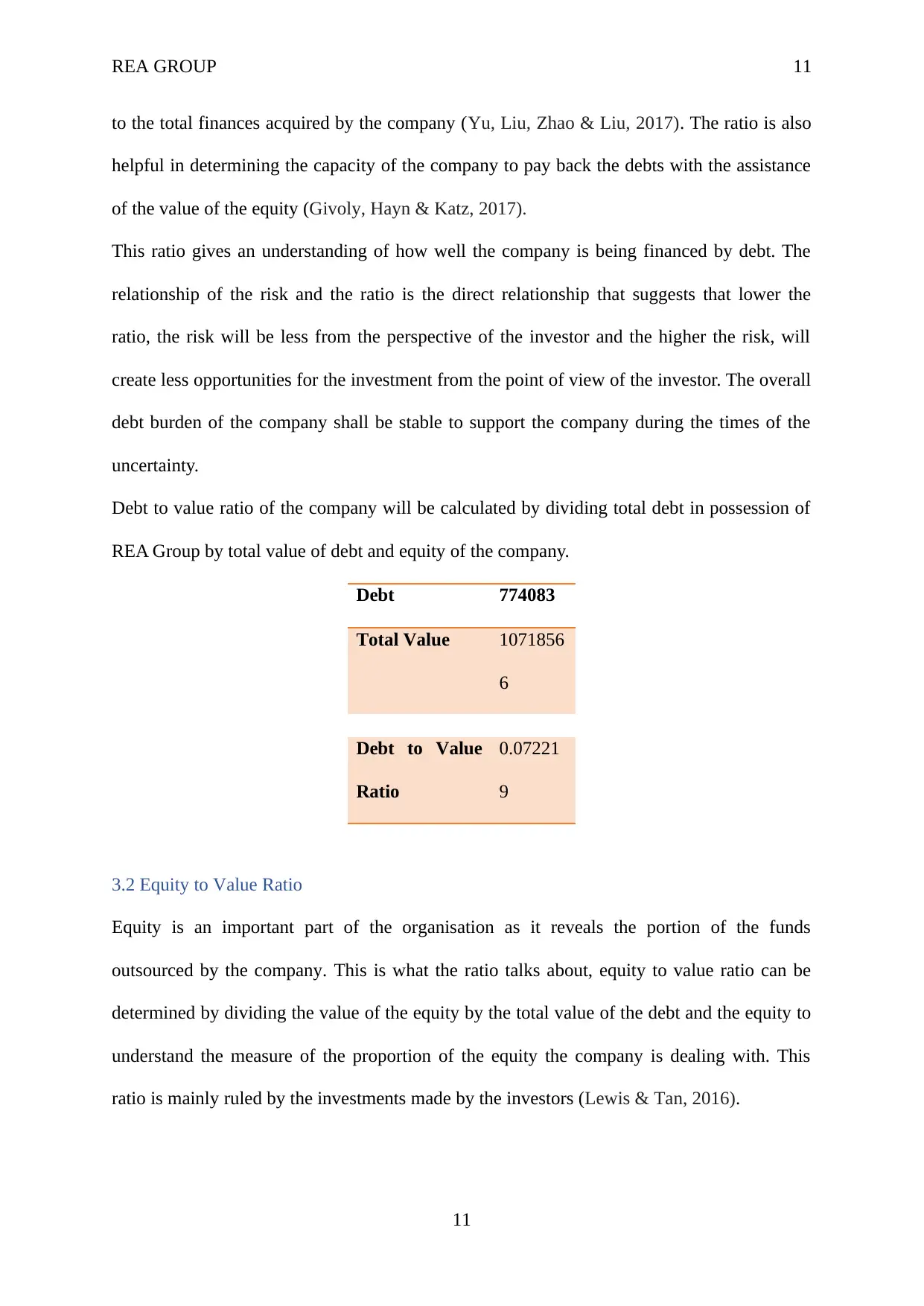

to the total finances acquired by the company (Yu, Liu, Zhao & Liu, 2017). The ratio is also

helpful in determining the capacity of the company to pay back the debts with the assistance

of the value of the equity (Givoly, Hayn & Katz, 2017).

This ratio gives an understanding of how well the company is being financed by debt. The

relationship of the risk and the ratio is the direct relationship that suggests that lower the

ratio, the risk will be less from the perspective of the investor and the higher the risk, will

create less opportunities for the investment from the point of view of the investor. The overall

debt burden of the company shall be stable to support the company during the times of the

uncertainty.

Debt to value ratio of the company will be calculated by dividing total debt in possession of

REA Group by total value of debt and equity of the company.

Debt 774083

Total Value 1071856

6

Debt to Value

Ratio

0.07221

9

3.2 Equity to Value Ratio

Equity is an important part of the organisation as it reveals the portion of the funds

outsourced by the company. This is what the ratio talks about, equity to value ratio can be

determined by dividing the value of the equity by the total value of the debt and the equity to

understand the measure of the proportion of the equity the company is dealing with. This

ratio is mainly ruled by the investments made by the investors (Lewis & Tan, 2016).

11

to the total finances acquired by the company (Yu, Liu, Zhao & Liu, 2017). The ratio is also

helpful in determining the capacity of the company to pay back the debts with the assistance

of the value of the equity (Givoly, Hayn & Katz, 2017).

This ratio gives an understanding of how well the company is being financed by debt. The

relationship of the risk and the ratio is the direct relationship that suggests that lower the

ratio, the risk will be less from the perspective of the investor and the higher the risk, will

create less opportunities for the investment from the point of view of the investor. The overall

debt burden of the company shall be stable to support the company during the times of the

uncertainty.

Debt to value ratio of the company will be calculated by dividing total debt in possession of

REA Group by total value of debt and equity of the company.

Debt 774083

Total Value 1071856

6

Debt to Value

Ratio

0.07221

9

3.2 Equity to Value Ratio

Equity is an important part of the organisation as it reveals the portion of the funds

outsourced by the company. This is what the ratio talks about, equity to value ratio can be

determined by dividing the value of the equity by the total value of the debt and the equity to

understand the measure of the proportion of the equity the company is dealing with. This

ratio is mainly ruled by the investments made by the investors (Lewis & Tan, 2016).

11

REA GROUP 12

Equity to value ratio of the REA Group will be calculated by dividing total equity from total

value of the company as follows.

Equity 9944484

Total Value 1071856

6

Equity to Value

Ratio

0.92778

1

3.3 Debt to Equity Ratio

This ratio is the combination of the above two ratios and displays the overall risk the

company is possessing. If the ratio is high it indicates that the finances made by the company

are more form the use of the credit facilities such as bank loans rather than utilising the

equity. The total value is segregated between the investors and the creditors and the same is

represented with the help of analysing this ratio (Abel, 2018).

Debt to Equity ratio will be calculated by dividing total debt by total equity of REA Group.

Debt 774083

Equity 994448

3

Debt to Equity

Ratio

0.07784

All the calculated figures can be summarized as follows.

12

Equity to value ratio of the REA Group will be calculated by dividing total equity from total

value of the company as follows.

Equity 9944484

Total Value 1071856

6

Equity to Value

Ratio

0.92778

1

3.3 Debt to Equity Ratio

This ratio is the combination of the above two ratios and displays the overall risk the

company is possessing. If the ratio is high it indicates that the finances made by the company

are more form the use of the credit facilities such as bank loans rather than utilising the

equity. The total value is segregated between the investors and the creditors and the same is

represented with the help of analysing this ratio (Abel, 2018).

Debt to Equity ratio will be calculated by dividing total debt by total equity of REA Group.

Debt 774083

Equity 994448

3

Debt to Equity

Ratio

0.07784

All the calculated figures can be summarized as follows.

12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REA GROUP 13

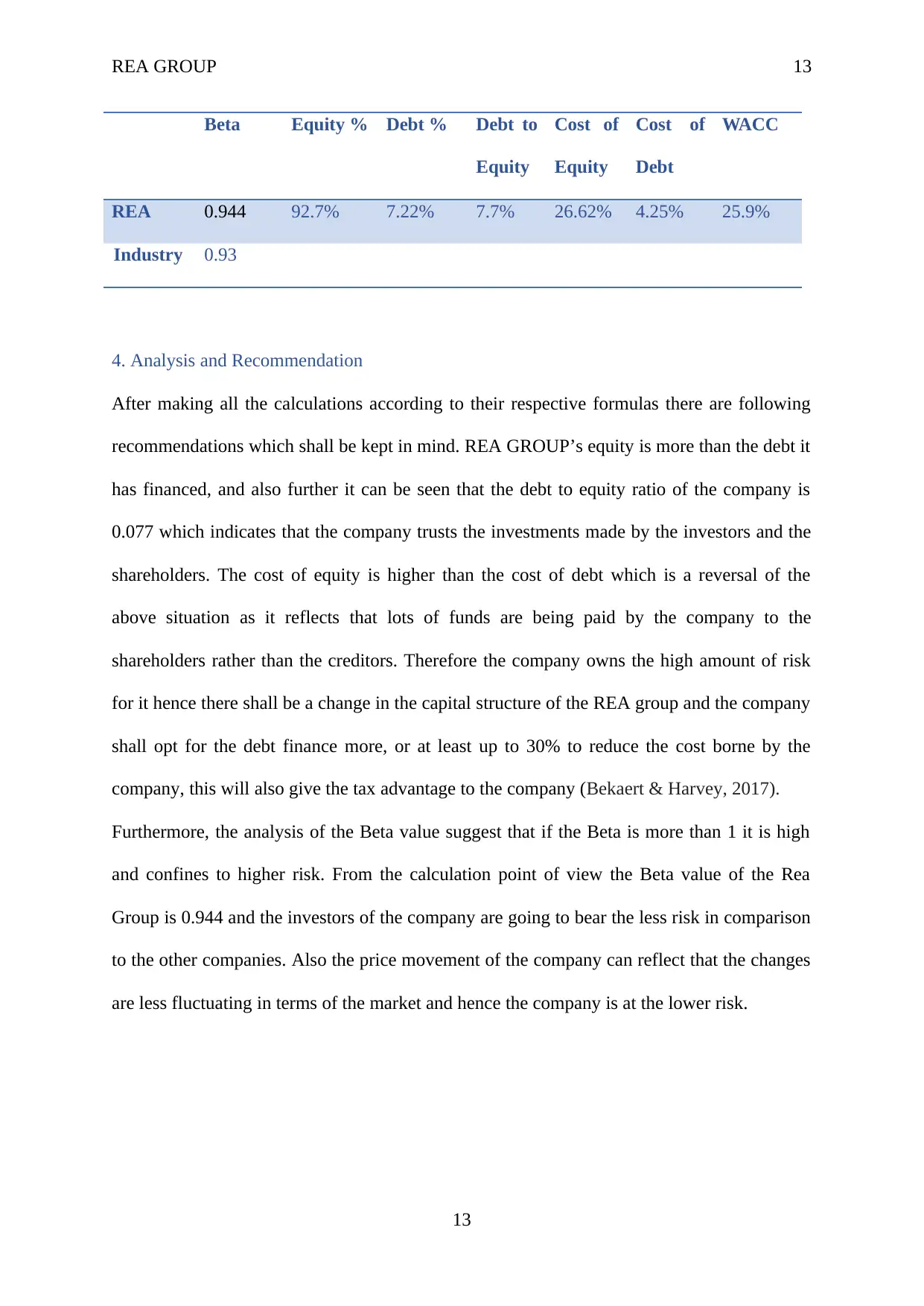

Beta Equity % Debt % Debt to

Equity

Cost of

Equity

Cost of

Debt

WACC

REA 0.944 92.7% 7.22% 7.7% 26.62% 4.25% 25.9%

Industry 0.93

4. Analysis and Recommendation

After making all the calculations according to their respective formulas there are following

recommendations which shall be kept in mind. REA GROUP’s equity is more than the debt it

has financed, and also further it can be seen that the debt to equity ratio of the company is

0.077 which indicates that the company trusts the investments made by the investors and the

shareholders. The cost of equity is higher than the cost of debt which is a reversal of the

above situation as it reflects that lots of funds are being paid by the company to the

shareholders rather than the creditors. Therefore the company owns the high amount of risk

for it hence there shall be a change in the capital structure of the REA group and the company

shall opt for the debt finance more, or at least up to 30% to reduce the cost borne by the

company, this will also give the tax advantage to the company (Bekaert & Harvey, 2017).

Furthermore, the analysis of the Beta value suggest that if the Beta is more than 1 it is high

and confines to higher risk. From the calculation point of view the Beta value of the Rea

Group is 0.944 and the investors of the company are going to bear the less risk in comparison

to the other companies. Also the price movement of the company can reflect that the changes

are less fluctuating in terms of the market and hence the company is at the lower risk.

13

Beta Equity % Debt % Debt to

Equity

Cost of

Equity

Cost of

Debt

WACC

REA 0.944 92.7% 7.22% 7.7% 26.62% 4.25% 25.9%

Industry 0.93

4. Analysis and Recommendation

After making all the calculations according to their respective formulas there are following

recommendations which shall be kept in mind. REA GROUP’s equity is more than the debt it

has financed, and also further it can be seen that the debt to equity ratio of the company is

0.077 which indicates that the company trusts the investments made by the investors and the

shareholders. The cost of equity is higher than the cost of debt which is a reversal of the

above situation as it reflects that lots of funds are being paid by the company to the

shareholders rather than the creditors. Therefore the company owns the high amount of risk

for it hence there shall be a change in the capital structure of the REA group and the company

shall opt for the debt finance more, or at least up to 30% to reduce the cost borne by the

company, this will also give the tax advantage to the company (Bekaert & Harvey, 2017).

Furthermore, the analysis of the Beta value suggest that if the Beta is more than 1 it is high

and confines to higher risk. From the calculation point of view the Beta value of the Rea

Group is 0.944 and the investors of the company are going to bear the less risk in comparison

to the other companies. Also the price movement of the company can reflect that the changes

are less fluctuating in terms of the market and hence the company is at the lower risk.

13

REA GROUP 14

References

Abel, A. B. (2018). Optimal Debt and Profitability in the Trade‐Off Theory. The Journal of

Finance, 73(1), 95-143.

Ai, H., Bansal, R., Im, J., & Ying, C. (2018). A Model of the Macroeconomic Announcement

Premium with Production. Available at SSRN 3286693.

Austin, P. C., & Steyerberg, E. W. (2015). The number of subjects per variable required in

linear regression analyses. Journal of clinical epidemiology, 68(6), 627-636.

Barberis, N., Greenwood, R., Jin, L., & Shleifer, A. (2015). X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), 1-24.

Bekaert, G., & Harvey, C. (2017). Emerging equity markets in a globalizing world.

Brusov, P., Filatova, T., Orekhova, N., & Eskindarov, M. (2018). New meaningful effects in

modern capital structure theory. In Modern Corporate Finance, Investments, Taxation and

Ratings (pp. 537-568). Springer, Cham.

Chatterjee, S., & Hadi, A. S. (2015). Regression analysis by example. John Wiley & Sons.

Dhaliwal, D., Judd, J. S., Serfling, M., & Shaikh, S. (2016). Customer concentration risk and

the cost of equity capital. Journal of Accounting and Economics, 61(1), 23-48.

Frank, M. Z., & Shen, T. (2016). Investment and the weighted average cost of

capital. Journal of Financial Economics, 119(2), 300-315.

Givoly, D., Hayn, C., & Katz, S. (2017). The changing relevance of accounting information

to debt holders over time. Review of Accounting Studies, 22(1), 64-108.

Hoepner, A., Oikonomou, I., Scholtens, B., & Schröder, M. (2016). The effects of corporate

and country sustainability characteristics on the cost of debt: An international

investigation. Journal of Business Finance & Accounting, 43(1-2), 158-190.

Lewis, C. M., & Tan, Y. (2016). Debt-equity choices, R&D investment and market

timing. Journal of Financial Economics, 119(3), 599-610.

14

References

Abel, A. B. (2018). Optimal Debt and Profitability in the Trade‐Off Theory. The Journal of

Finance, 73(1), 95-143.

Ai, H., Bansal, R., Im, J., & Ying, C. (2018). A Model of the Macroeconomic Announcement

Premium with Production. Available at SSRN 3286693.

Austin, P. C., & Steyerberg, E. W. (2015). The number of subjects per variable required in

linear regression analyses. Journal of clinical epidemiology, 68(6), 627-636.

Barberis, N., Greenwood, R., Jin, L., & Shleifer, A. (2015). X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), 1-24.

Bekaert, G., & Harvey, C. (2017). Emerging equity markets in a globalizing world.

Brusov, P., Filatova, T., Orekhova, N., & Eskindarov, M. (2018). New meaningful effects in

modern capital structure theory. In Modern Corporate Finance, Investments, Taxation and

Ratings (pp. 537-568). Springer, Cham.

Chatterjee, S., & Hadi, A. S. (2015). Regression analysis by example. John Wiley & Sons.

Dhaliwal, D., Judd, J. S., Serfling, M., & Shaikh, S. (2016). Customer concentration risk and

the cost of equity capital. Journal of Accounting and Economics, 61(1), 23-48.

Frank, M. Z., & Shen, T. (2016). Investment and the weighted average cost of

capital. Journal of Financial Economics, 119(2), 300-315.

Givoly, D., Hayn, C., & Katz, S. (2017). The changing relevance of accounting information

to debt holders over time. Review of Accounting Studies, 22(1), 64-108.

Hoepner, A., Oikonomou, I., Scholtens, B., & Schröder, M. (2016). The effects of corporate

and country sustainability characteristics on the cost of debt: An international

investigation. Journal of Business Finance & Accounting, 43(1-2), 158-190.

Lewis, C. M., & Tan, Y. (2016). Debt-equity choices, R&D investment and market

timing. Journal of Financial Economics, 119(3), 599-610.

14

REA GROUP 15

Lorenz, D., Kruschwitz, L., & Löffler, A. (2016). Are costs of capital necessarily constant

over time and across states of nature?: Some remarks on the debate on ‘WACC is not quite

right’. The Quarterly Review of Economics and Finance, 60, 81-85.

REA GROUP, (2018). REA Group Ltd. REA. Retrieved from

https://www.morningstar.com.au/Stocks/NewsAndQuotes/REA

REA, (2018). Annual Reports. Retrieved from https://www.rea-group.com/company/investor-

centre/annual-reports/

REA, (2018). REA Group Ltd (REA.AX). Retrieved from

https://www.reuters.com/finance/stocks/overview/REA.AX

Yu, Z., Liu, K., Zhao, C., & Liu, Y. (2017, April). Combined Forecasting Model of Traffic

Flow Based on DGM (1, 1) and GRNN. In Computing Intelligence and Information System

(CIIS), 2017 International Conference on (pp. 58-61). IEEE.

Zhang, J., Lü, X., Ran, M., & Han, G. (2016). DGM model based on anti-cotangent function

and its application. Journal of Grey System, 28(3), 63.

15

Lorenz, D., Kruschwitz, L., & Löffler, A. (2016). Are costs of capital necessarily constant

over time and across states of nature?: Some remarks on the debate on ‘WACC is not quite

right’. The Quarterly Review of Economics and Finance, 60, 81-85.

REA GROUP, (2018). REA Group Ltd. REA. Retrieved from

https://www.morningstar.com.au/Stocks/NewsAndQuotes/REA

REA, (2018). Annual Reports. Retrieved from https://www.rea-group.com/company/investor-

centre/annual-reports/

REA, (2018). REA Group Ltd (REA.AX). Retrieved from

https://www.reuters.com/finance/stocks/overview/REA.AX

Yu, Z., Liu, K., Zhao, C., & Liu, Y. (2017, April). Combined Forecasting Model of Traffic

Flow Based on DGM (1, 1) and GRNN. In Computing Intelligence and Information System

(CIIS), 2017 International Conference on (pp. 58-61). IEEE.

Zhang, J., Lü, X., Ran, M., & Han, G. (2016). DGM model based on anti-cotangent function

and its application. Journal of Grey System, 28(3), 63.

15

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REA GROUP 16

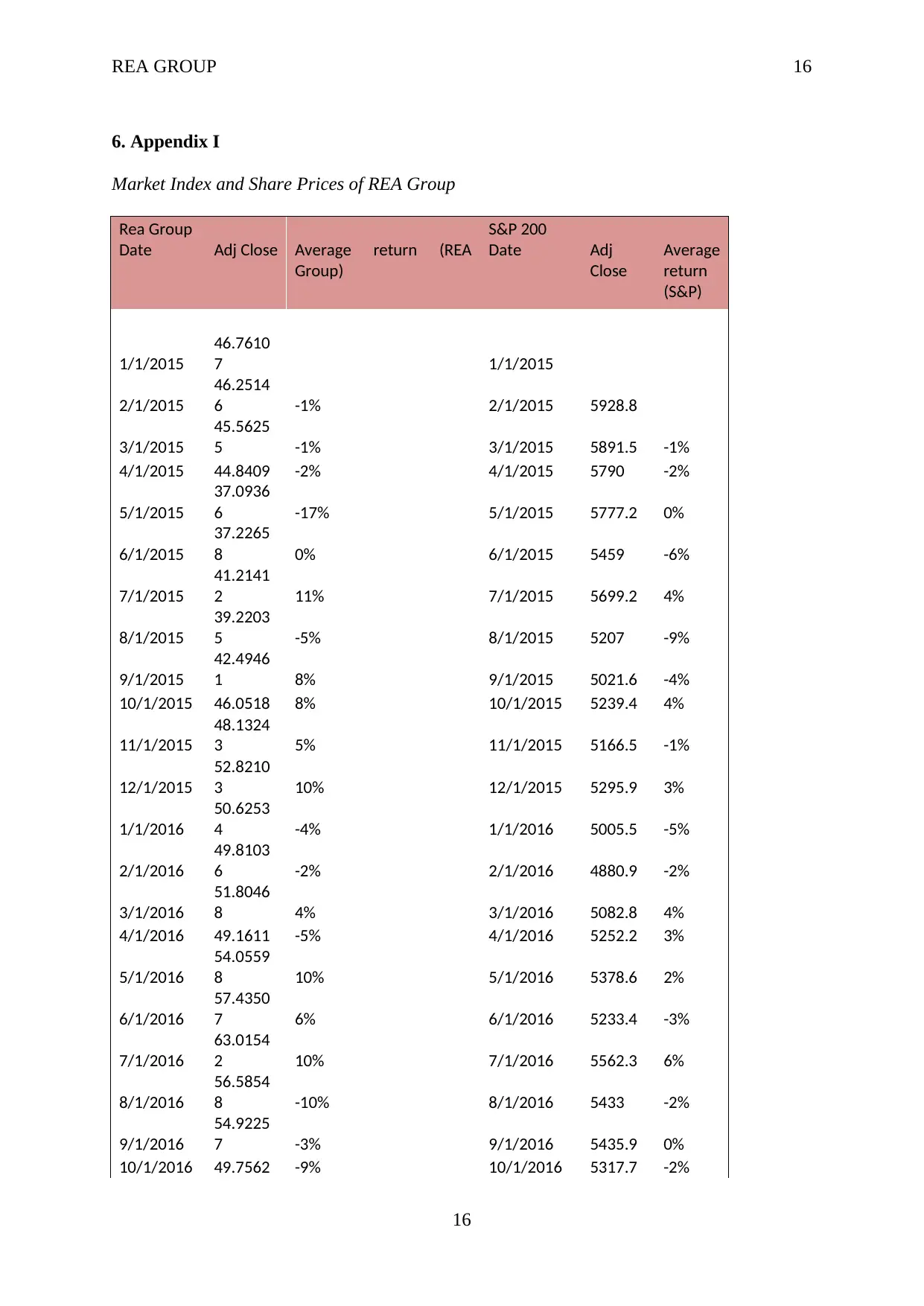

6. Appendix I

Market Index and Share Prices of REA Group

Rea Group S&P 200

Date Adj Close Average return (REA

Group)

Date Adj

Close

Average

return

(S&P)

1/1/2015

46.7610

7 1/1/2015

2/1/2015

46.2514

6 -1% 2/1/2015 5928.8

3/1/2015

45.5625

5 -1% 3/1/2015 5891.5 -1%

4/1/2015 44.8409 -2% 4/1/2015 5790 -2%

5/1/2015

37.0936

6 -17% 5/1/2015 5777.2 0%

6/1/2015

37.2265

8 0% 6/1/2015 5459 -6%

7/1/2015

41.2141

2 11% 7/1/2015 5699.2 4%

8/1/2015

39.2203

5 -5% 8/1/2015 5207 -9%

9/1/2015

42.4946

1 8% 9/1/2015 5021.6 -4%

10/1/2015 46.0518 8% 10/1/2015 5239.4 4%

11/1/2015

48.1324

3 5% 11/1/2015 5166.5 -1%

12/1/2015

52.8210

3 10% 12/1/2015 5295.9 3%

1/1/2016

50.6253

4 -4% 1/1/2016 5005.5 -5%

2/1/2016

49.8103

6 -2% 2/1/2016 4880.9 -2%

3/1/2016

51.8046

8 4% 3/1/2016 5082.8 4%

4/1/2016 49.1611 -5% 4/1/2016 5252.2 3%

5/1/2016

54.0559

8 10% 5/1/2016 5378.6 2%

6/1/2016

57.4350

7 6% 6/1/2016 5233.4 -3%

7/1/2016

63.0154

2 10% 7/1/2016 5562.3 6%

8/1/2016

56.5854

8 -10% 8/1/2016 5433 -2%

9/1/2016

54.9225

7 -3% 9/1/2016 5435.9 0%

10/1/2016 49.7562 -9% 10/1/2016 5317.7 -2%

16

6. Appendix I

Market Index and Share Prices of REA Group

Rea Group S&P 200

Date Adj Close Average return (REA

Group)

Date Adj

Close

Average

return

(S&P)

1/1/2015

46.7610

7 1/1/2015

2/1/2015

46.2514

6 -1% 2/1/2015 5928.8

3/1/2015

45.5625

5 -1% 3/1/2015 5891.5 -1%

4/1/2015 44.8409 -2% 4/1/2015 5790 -2%

5/1/2015

37.0936

6 -17% 5/1/2015 5777.2 0%

6/1/2015

37.2265

8 0% 6/1/2015 5459 -6%

7/1/2015

41.2141

2 11% 7/1/2015 5699.2 4%

8/1/2015

39.2203

5 -5% 8/1/2015 5207 -9%

9/1/2015

42.4946

1 8% 9/1/2015 5021.6 -4%

10/1/2015 46.0518 8% 10/1/2015 5239.4 4%

11/1/2015

48.1324

3 5% 11/1/2015 5166.5 -1%

12/1/2015

52.8210

3 10% 12/1/2015 5295.9 3%

1/1/2016

50.6253

4 -4% 1/1/2016 5005.5 -5%

2/1/2016

49.8103

6 -2% 2/1/2016 4880.9 -2%

3/1/2016

51.8046

8 4% 3/1/2016 5082.8 4%

4/1/2016 49.1611 -5% 4/1/2016 5252.2 3%

5/1/2016

54.0559

8 10% 5/1/2016 5378.6 2%

6/1/2016

57.4350

7 6% 6/1/2016 5233.4 -3%

7/1/2016

63.0154

2 10% 7/1/2016 5562.3 6%

8/1/2016

56.5854

8 -10% 8/1/2016 5433 -2%

9/1/2016

54.9225

7 -3% 9/1/2016 5435.9 0%

10/1/2016 49.7562 -9% 10/1/2016 5317.7 -2%

16

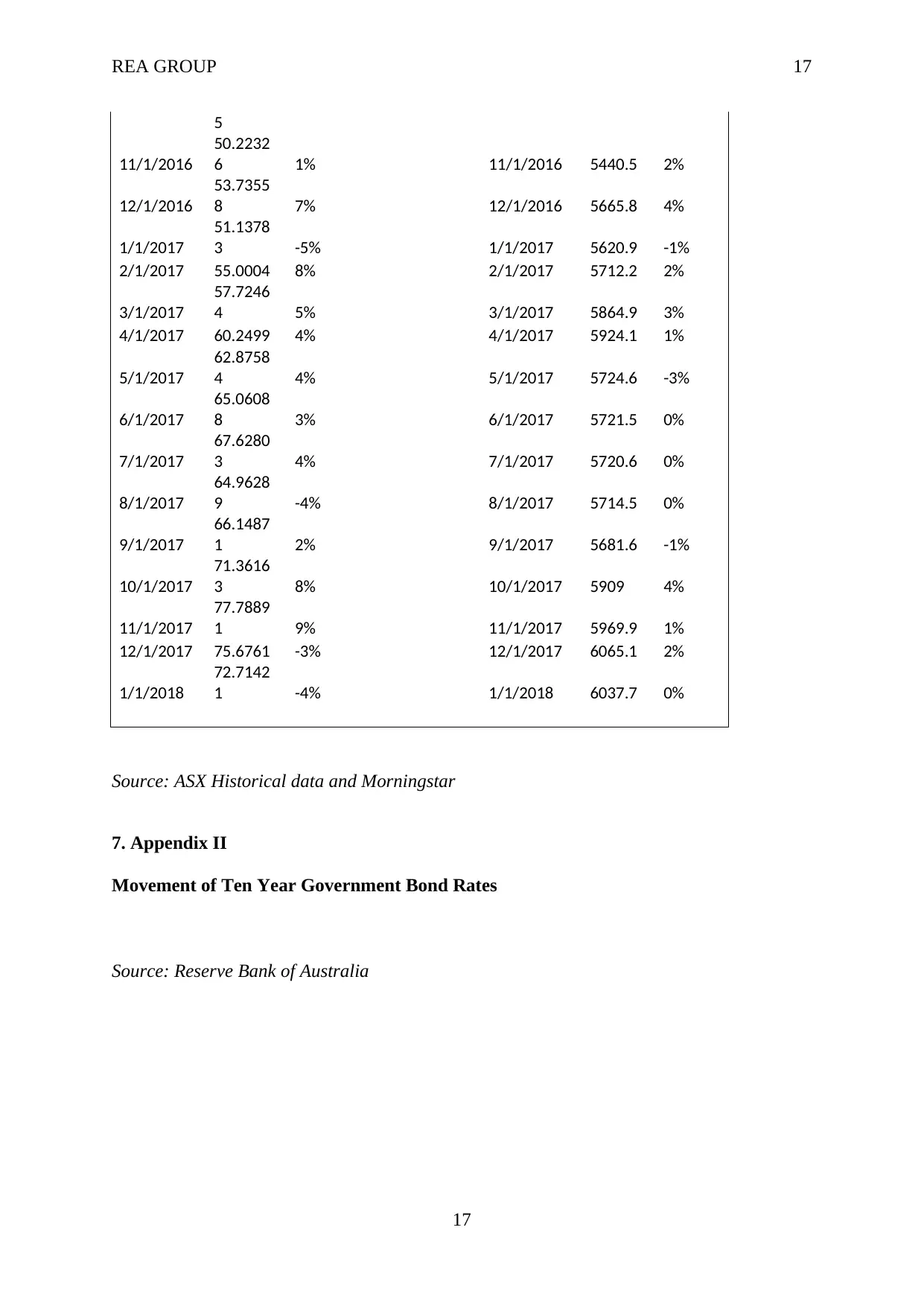

REA GROUP 17

5

11/1/2016

50.2232

6 1% 11/1/2016 5440.5 2%

12/1/2016

53.7355

8 7% 12/1/2016 5665.8 4%

1/1/2017

51.1378

3 -5% 1/1/2017 5620.9 -1%

2/1/2017 55.0004 8% 2/1/2017 5712.2 2%

3/1/2017

57.7246

4 5% 3/1/2017 5864.9 3%

4/1/2017 60.2499 4% 4/1/2017 5924.1 1%

5/1/2017

62.8758

4 4% 5/1/2017 5724.6 -3%

6/1/2017

65.0608

8 3% 6/1/2017 5721.5 0%

7/1/2017

67.6280

3 4% 7/1/2017 5720.6 0%

8/1/2017

64.9628

9 -4% 8/1/2017 5714.5 0%

9/1/2017

66.1487

1 2% 9/1/2017 5681.6 -1%

10/1/2017

71.3616

3 8% 10/1/2017 5909 4%

11/1/2017

77.7889

1 9% 11/1/2017 5969.9 1%

12/1/2017 75.6761 -3% 12/1/2017 6065.1 2%

1/1/2018

72.7142

1 -4% 1/1/2018 6037.7 0%

Source: ASX Historical data and Morningstar

7. Appendix II

Movement of Ten Year Government Bond Rates

Source: Reserve Bank of Australia

17

5

11/1/2016

50.2232

6 1% 11/1/2016 5440.5 2%

12/1/2016

53.7355

8 7% 12/1/2016 5665.8 4%

1/1/2017

51.1378

3 -5% 1/1/2017 5620.9 -1%

2/1/2017 55.0004 8% 2/1/2017 5712.2 2%

3/1/2017

57.7246

4 5% 3/1/2017 5864.9 3%

4/1/2017 60.2499 4% 4/1/2017 5924.1 1%

5/1/2017

62.8758

4 4% 5/1/2017 5724.6 -3%

6/1/2017

65.0608

8 3% 6/1/2017 5721.5 0%

7/1/2017

67.6280

3 4% 7/1/2017 5720.6 0%

8/1/2017

64.9628

9 -4% 8/1/2017 5714.5 0%

9/1/2017

66.1487

1 2% 9/1/2017 5681.6 -1%

10/1/2017

71.3616

3 8% 10/1/2017 5909 4%

11/1/2017

77.7889

1 9% 11/1/2017 5969.9 1%

12/1/2017 75.6761 -3% 12/1/2017 6065.1 2%

1/1/2018

72.7142

1 -4% 1/1/2018 6037.7 0%

Source: ASX Historical data and Morningstar

7. Appendix II

Movement of Ten Year Government Bond Rates

Source: Reserve Bank of Australia

17

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.