Corporate Accounting: Comparative Analysis of Equity Elements

VerifiedAdded on 2023/06/05

|9

|1762

|122

Report

AI Summary

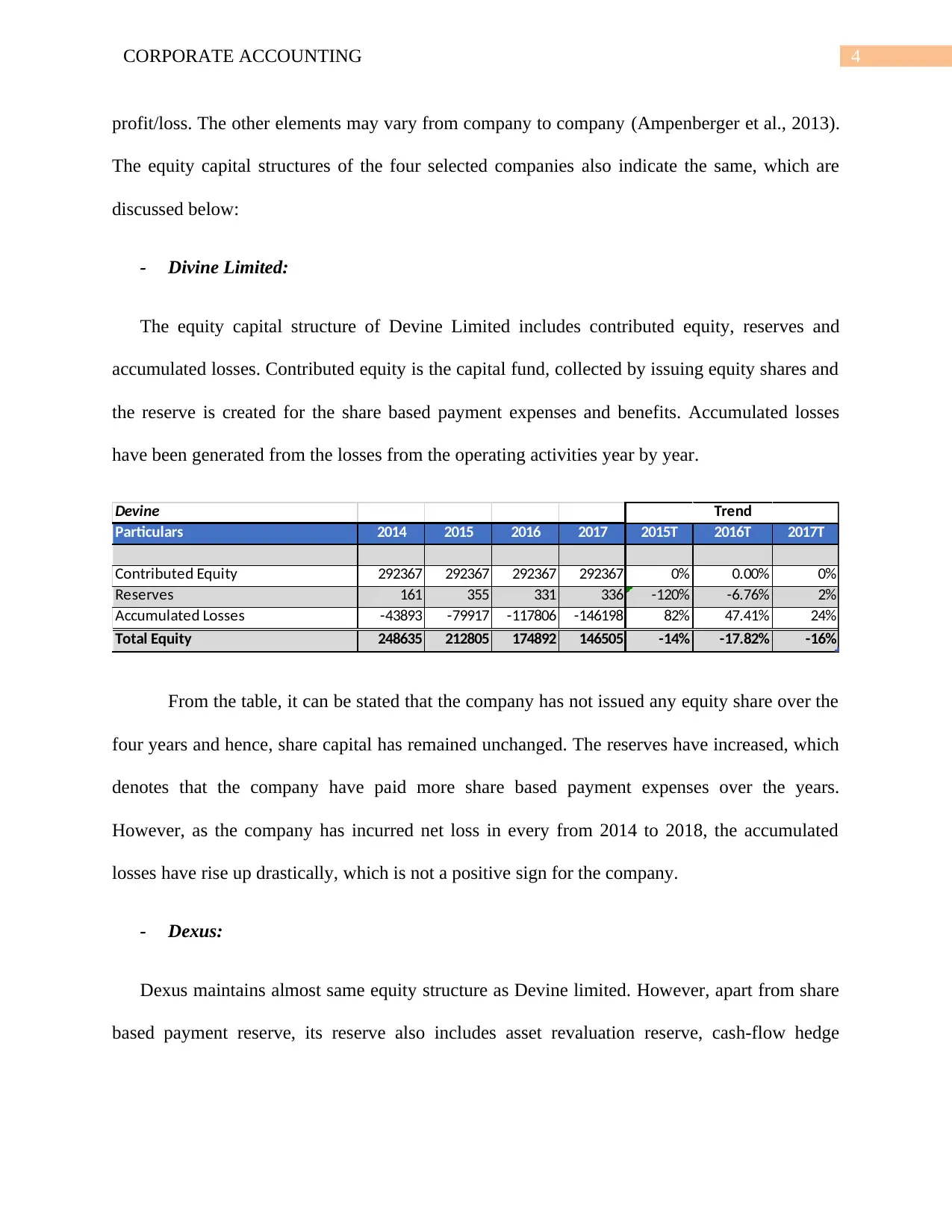

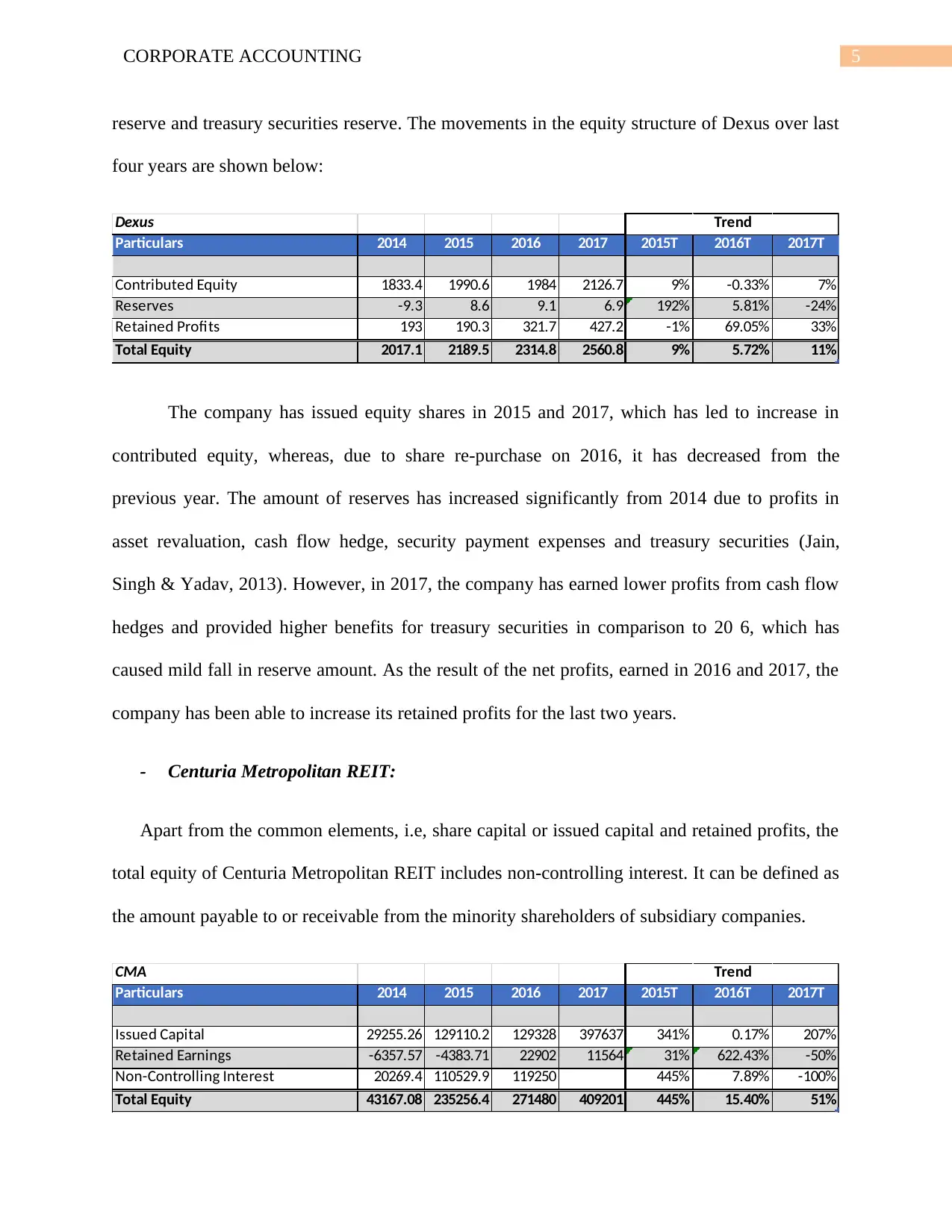

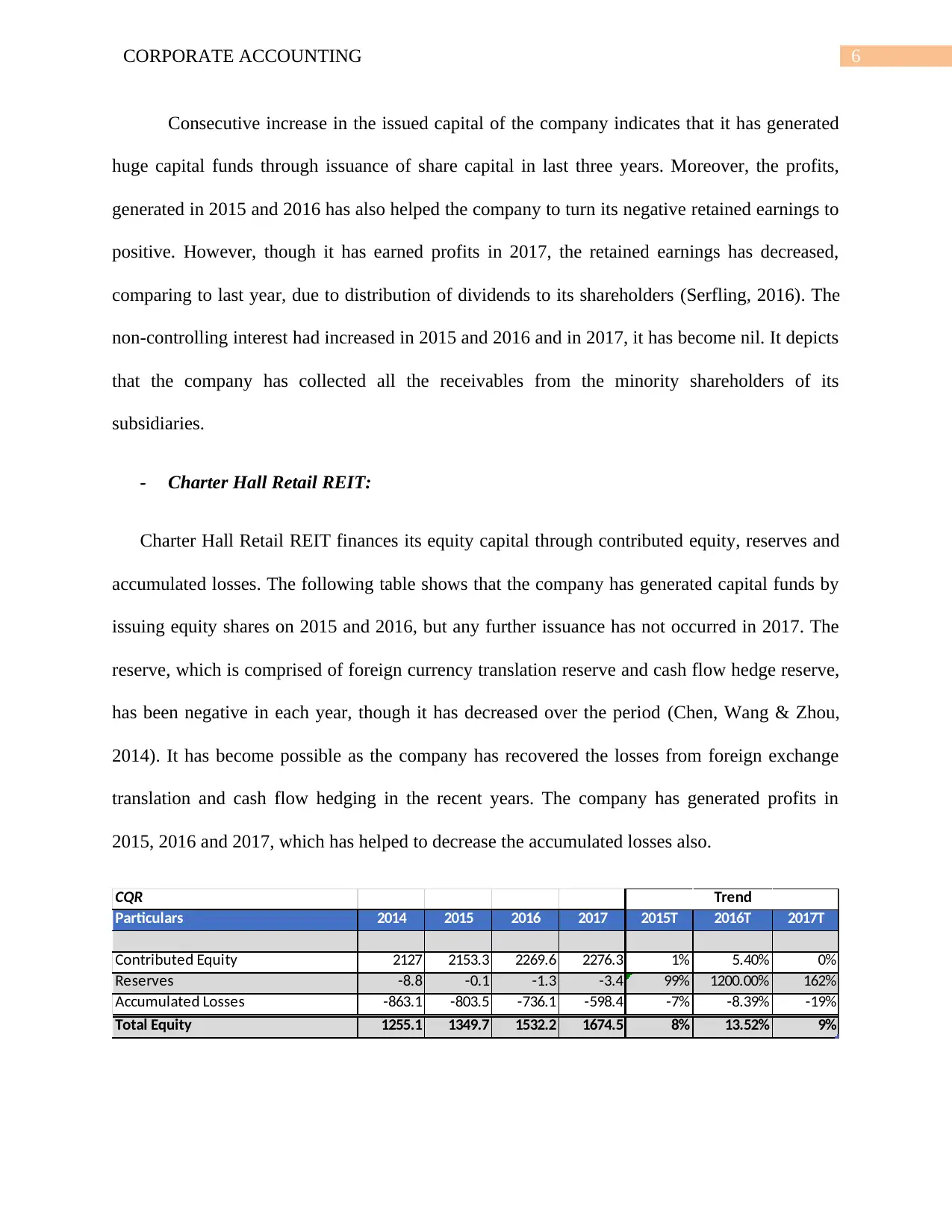

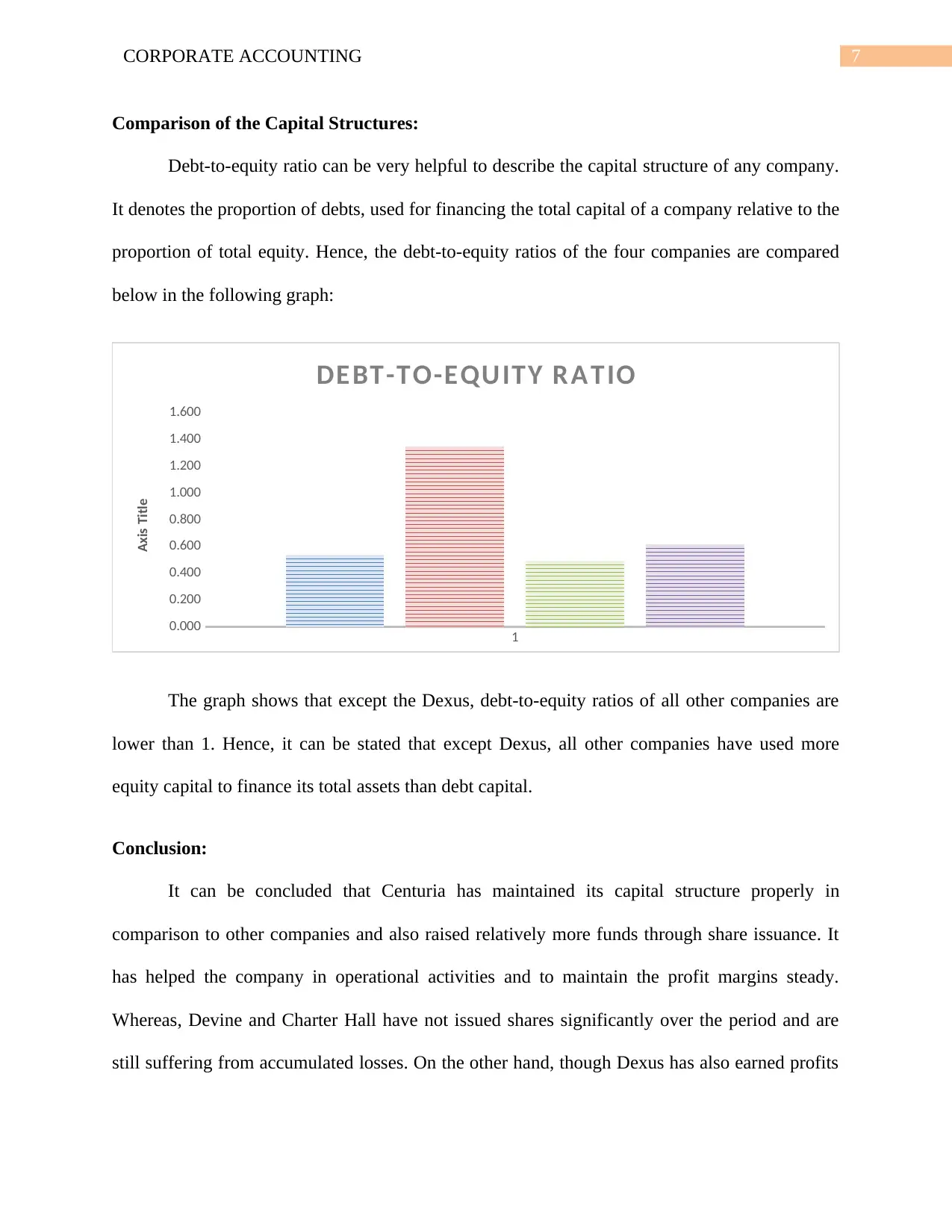

This report provides an in-depth analysis of the capital structures and equity elements of four real estate companies: Divine Limited, Dexus, Centuria Metropolitan REIT, and Charter Hall Retail REIT. The analysis focuses on key equity components such as share capital, retained earnings, and reserves, examining their movements and trends over a four-year period. The report compares the debt-to-equity ratios of the companies, revealing insights into their financing strategies. Centuria Metropolitan REIT is highlighted for its effective capital structure management through share issuance, while Divine Limited and Charter Hall Retail REIT are noted for their ongoing accumulated losses. Dexus, despite generating profits, is cautioned about its higher debt levels. The report concludes that effective capital structure management is crucial for maintaining profitability and operational stability, emphasizing the importance of balancing debt and equity financing.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.