Financial Analysis: Comparative Ratio Report on Stockland & Mirvac

VerifiedAdded on 2023/06/05

Paraphrase This Document

The preparation and presentation of financial statements form a crucial task of the management,

analyzing such financial statements with the best possible tools is a crucial task for the investors

and all such users intending to use these statements. Ratio analysis is one such comparative tool

used to understand the financial position of the company, its performance over the last years, it's

trend analysis, comparison with other companies in the same industry, etc. Ratio analysis

however considers only financial information and neglects every non-financial information

which might be important to understand the actions of the company better than the numbers

itself.

INTRODUCTION...........................................................................................................................4

RATIO ANALYSIS........................................................................................................................5

COMPARISON OF OVERALL PERFORMANCE.....................................................................25

RECOMMENDATION.................................................................................................................26

CONCLUSION..............................................................................................................................27

Bibliography..................................................................................................................................28

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As a business management consultant, being appointed by Mr. Benson Evans who is the Chief

Operations Officer of Hotel Properties Limited (HPL), the companies to be compared are

Stockland Group and Mirvac Group. Both of these companies are involved in real estate business

and have approached HPL for potential partnership in residential and resort development

(Atkinson, 2012). As part of the consultancy agreement, the overall performance of both the

companies have been analyzed individually using ratio analysis as stated below (Alvarez, 2013):

Paraphrase This Document

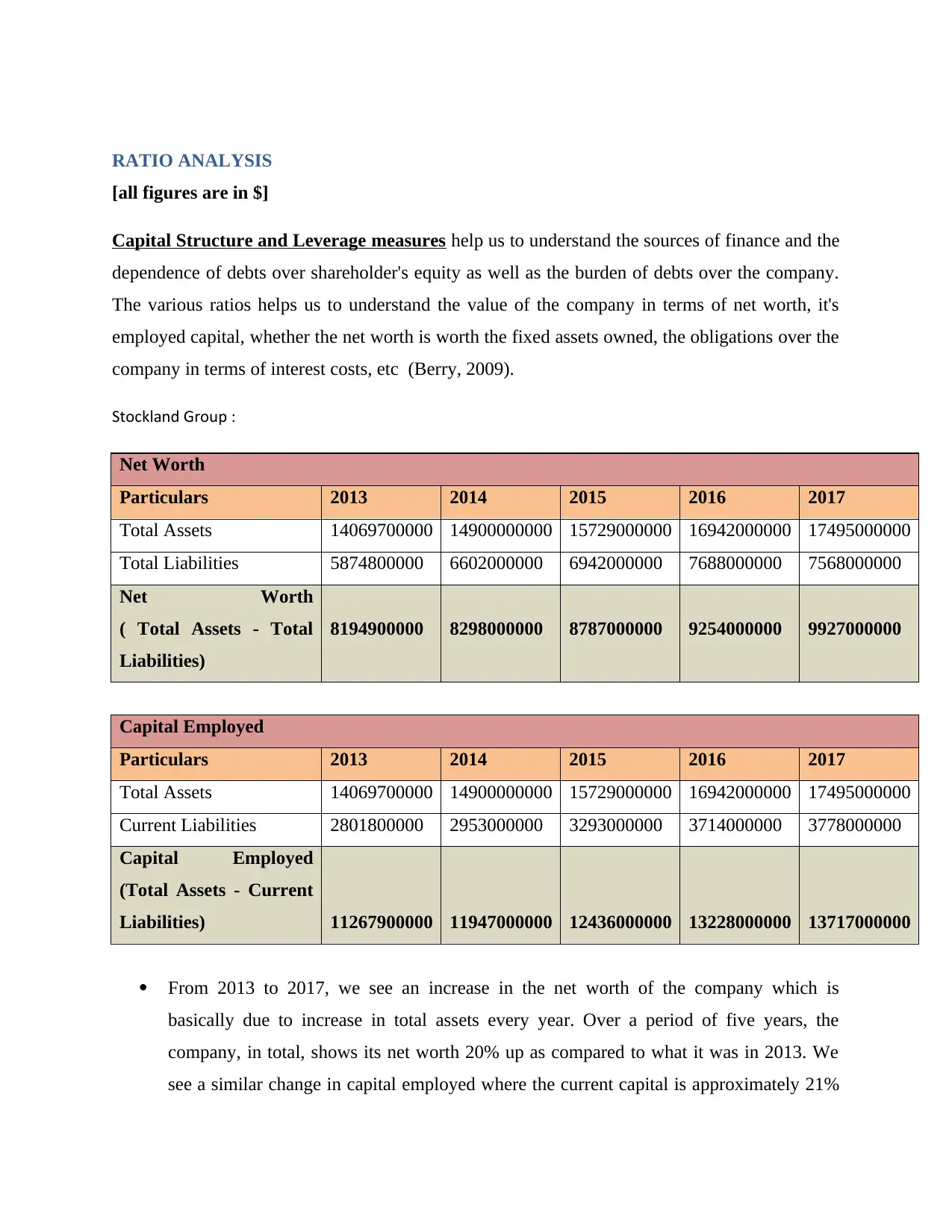

[all figures are in $]

Capital Structure and Leverage measures help us to understand the sources of finance and the

dependence of debts over shareholder's equity as well as the burden of debts over the company.

The various ratios helps us to understand the value of the company in terms of net worth, it's

employed capital, whether the net worth is worth the fixed assets owned, the obligations over the

company in terms of interest costs, etc (Berry, 2009).

Stockland Group :

Net Worth

Particulars 2013 2014 2015 2016 2017

Total Assets 14069700000 14900000000 15729000000 16942000000 17495000000

Total Liabilities 5874800000 6602000000 6942000000 7688000000 7568000000

Net Worth

( Total Assets - Total

Liabilities)

8194900000 8298000000 8787000000 9254000000 9927000000

Capital Employed

Particulars 2013 2014 2015 2016 2017

Total Assets 14069700000 14900000000 15729000000 16942000000 17495000000

Current Liabilities 2801800000 2953000000 3293000000 3714000000 3778000000

Capital Employed

(Total Assets - Current

Liabilities) 11267900000 11947000000 12436000000 13228000000 13717000000

From 2013 to 2017, we see an increase in the net worth of the company which is

basically due to increase in total assets every year. Over a period of five years, the

company, in total, shows its net worth 20% up as compared to what it was in 2013. We

see a similar change in capital employed where the current capital is approximately 21%

employed.

Fixed Assets To Net Worth Ratio

Particulars 2013 2014 2015 2016 2017

Fixed Assets 12862800000 13294000000 14575000000 15531000000 16172000000

Net Worth 8194900000 8298000000 8787000000 9254000000 9927000000

Fixed Assets to Net

Worth Ratio (Fixed

Assets / Net Worth) 1.57 1.60 1.66 1.68 1.63

Current Liablities To Net Worth

Particulars 2013 2014 2015 2016 2017

Current Liabilities 2801800000 2953000000 3293000000 3714000000 3778000000

Net Worth 8194900000 8298000000 8787000000 9254000000 9927000000

Current Liabilities to

Net Worth (Current

Liabilities / Net Worth)

0.34 0.36 0.37 0.40 0.38

From 2013 to 2017, we see increasing fixed assets to net worth ratio, which is

undesirable in normal business days as it shows the extent of owner's cash being locked

up in fixed assets and how much cash is left for business operating activities. However,

Stockland shows 1.63 times of net worth in fixed assets. Also, we see an increase in

current liabilities to net worth ratio which is undesirable for a business (Easton, 2010).

Total Debt Ratio

Particulars 2013 2014 2015 2016 2017

Total Liabilities 5874800000 6602000000 6942000000 7688000000 7568000000

Total Assets 14069700000 14900000000 15729000000 16942000000 17495000000

Total Debt Ratio

(total liabilities / total

0.42 0.44 0.44 0.45 0.43

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

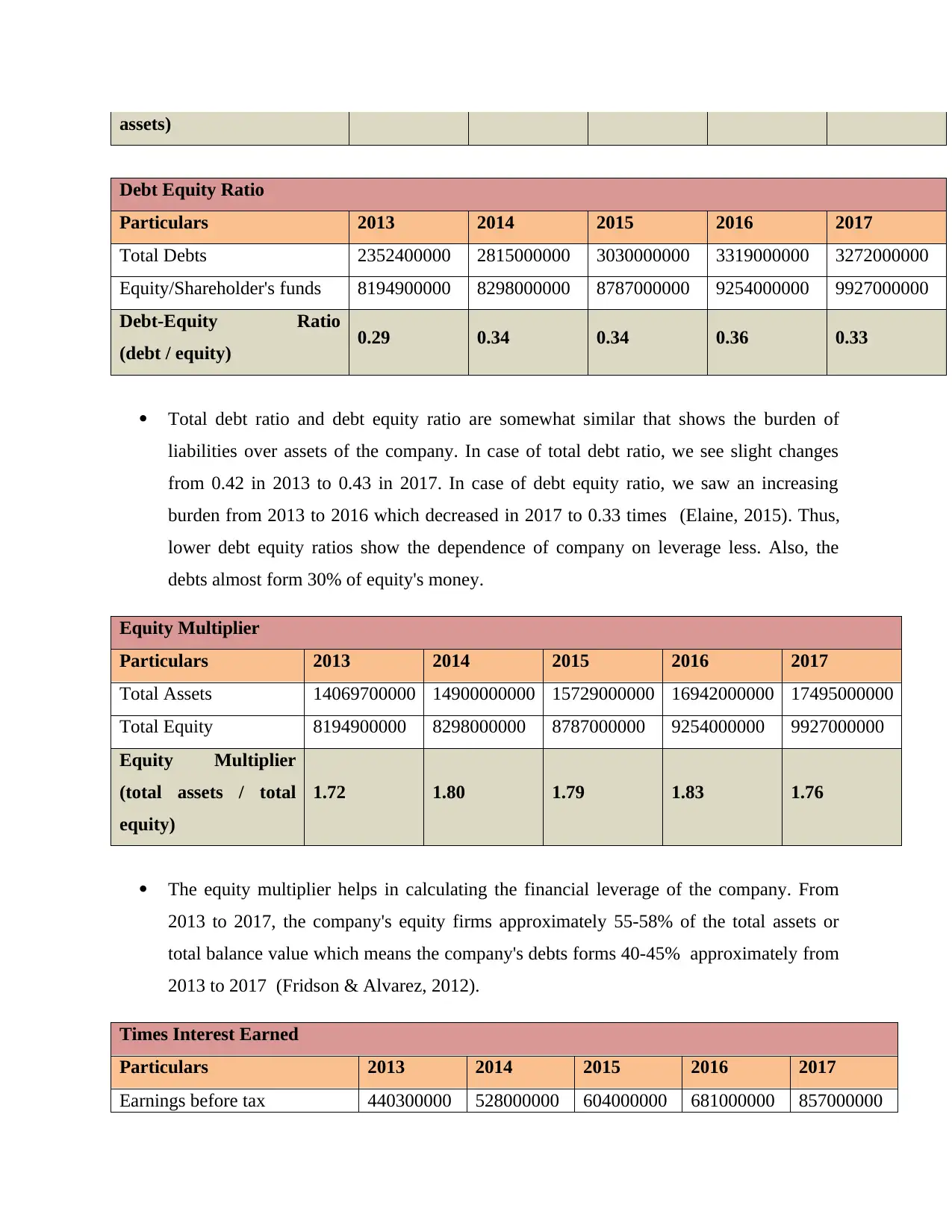

Debt Equity Ratio

Particulars 2013 2014 2015 2016 2017

Total Debts 2352400000 2815000000 3030000000 3319000000 3272000000

Equity/Shareholder's funds 8194900000 8298000000 8787000000 9254000000 9927000000

Debt-Equity Ratio

(debt / equity) 0.29 0.34 0.34 0.36 0.33

Total debt ratio and debt equity ratio are somewhat similar that shows the burden of

liabilities over assets of the company. In case of total debt ratio, we see slight changes

from 0.42 in 2013 to 0.43 in 2017. In case of debt equity ratio, we saw an increasing

burden from 2013 to 2016 which decreased in 2017 to 0.33 times (Elaine, 2015). Thus,

lower debt equity ratios show the dependence of company on leverage less. Also, the

debts almost form 30% of equity's money.

Equity Multiplier

Particulars 2013 2014 2015 2016 2017

Total Assets 14069700000 14900000000 15729000000 16942000000 17495000000

Total Equity 8194900000 8298000000 8787000000 9254000000 9927000000

Equity Multiplier

(total assets / total

equity)

1.72 1.80 1.79 1.83 1.76

The equity multiplier helps in calculating the financial leverage of the company. From

2013 to 2017, the company's equity firms approximately 55-58% of the total assets or

total balance value which means the company's debts forms 40-45% approximately from

2013 to 2017 (Fridson & Alvarez, 2012).

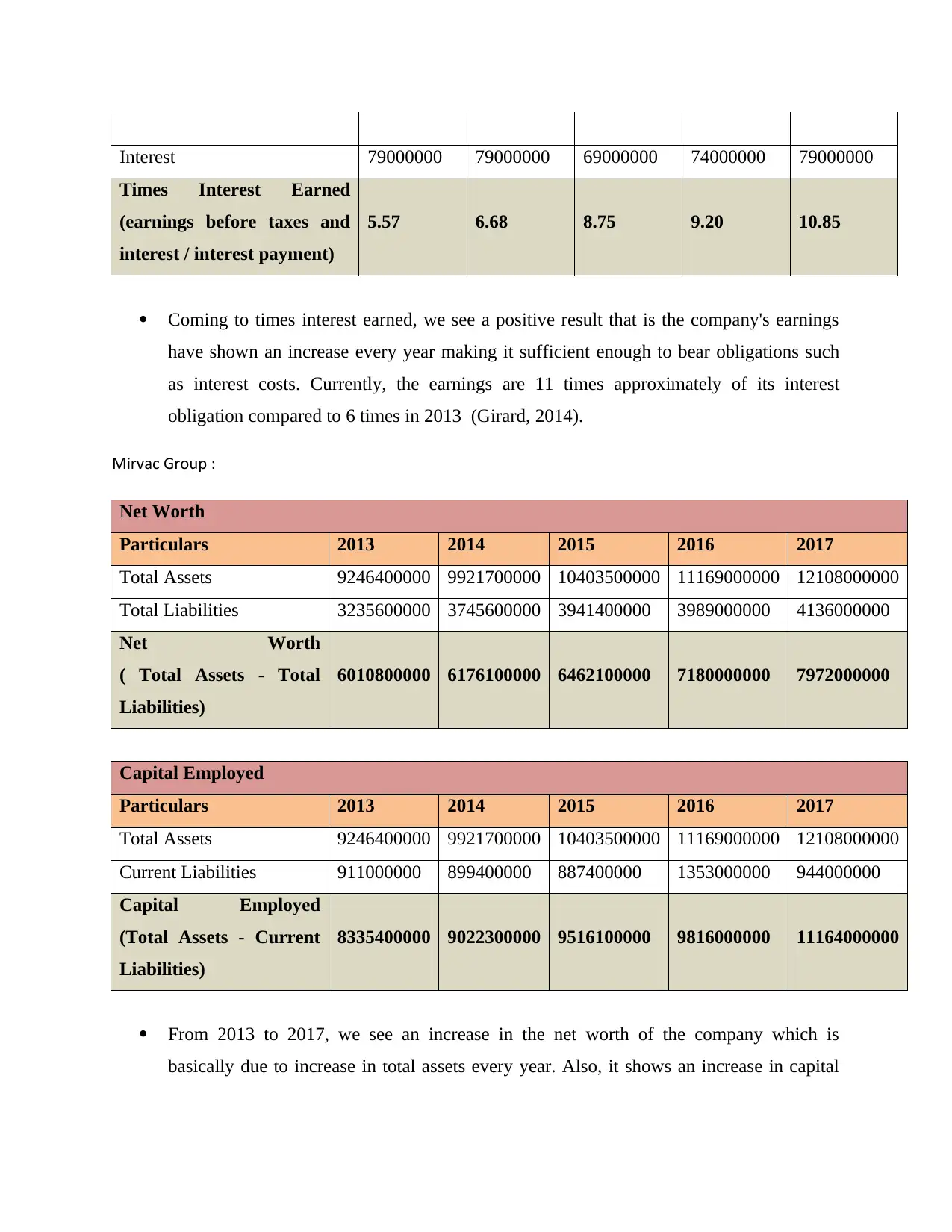

Times Interest Earned

Particulars 2013 2014 2015 2016 2017

Earnings before tax 440300000 528000000 604000000 681000000 857000000

Paraphrase This Document

Times Interest Earned

(earnings before taxes and

interest / interest payment)

5.57 6.68 8.75 9.20 10.85

Coming to times interest earned, we see a positive result that is the company's earnings

have shown an increase every year making it sufficient enough to bear obligations such

as interest costs. Currently, the earnings are 11 times approximately of its interest

obligation compared to 6 times in 2013 (Girard, 2014).

Mirvac Group :

Net Worth

Particulars 2013 2014 2015 2016 2017

Total Assets 9246400000 9921700000 10403500000 11169000000 12108000000

Total Liabilities 3235600000 3745600000 3941400000 3989000000 4136000000

Net Worth

( Total Assets - Total

Liabilities)

6010800000 6176100000 6462100000 7180000000 7972000000

Capital Employed

Particulars 2013 2014 2015 2016 2017

Total Assets 9246400000 9921700000 10403500000 11169000000 12108000000

Current Liabilities 911000000 899400000 887400000 1353000000 944000000

Capital Employed

(Total Assets - Current

Liabilities)

8335400000 9022300000 9516100000 9816000000 11164000000

From 2013 to 2017, we see an increase in the net worth of the company which is

basically due to increase in total assets every year. Also, it shows an increase in capital

employed (Ittelson, 2009).

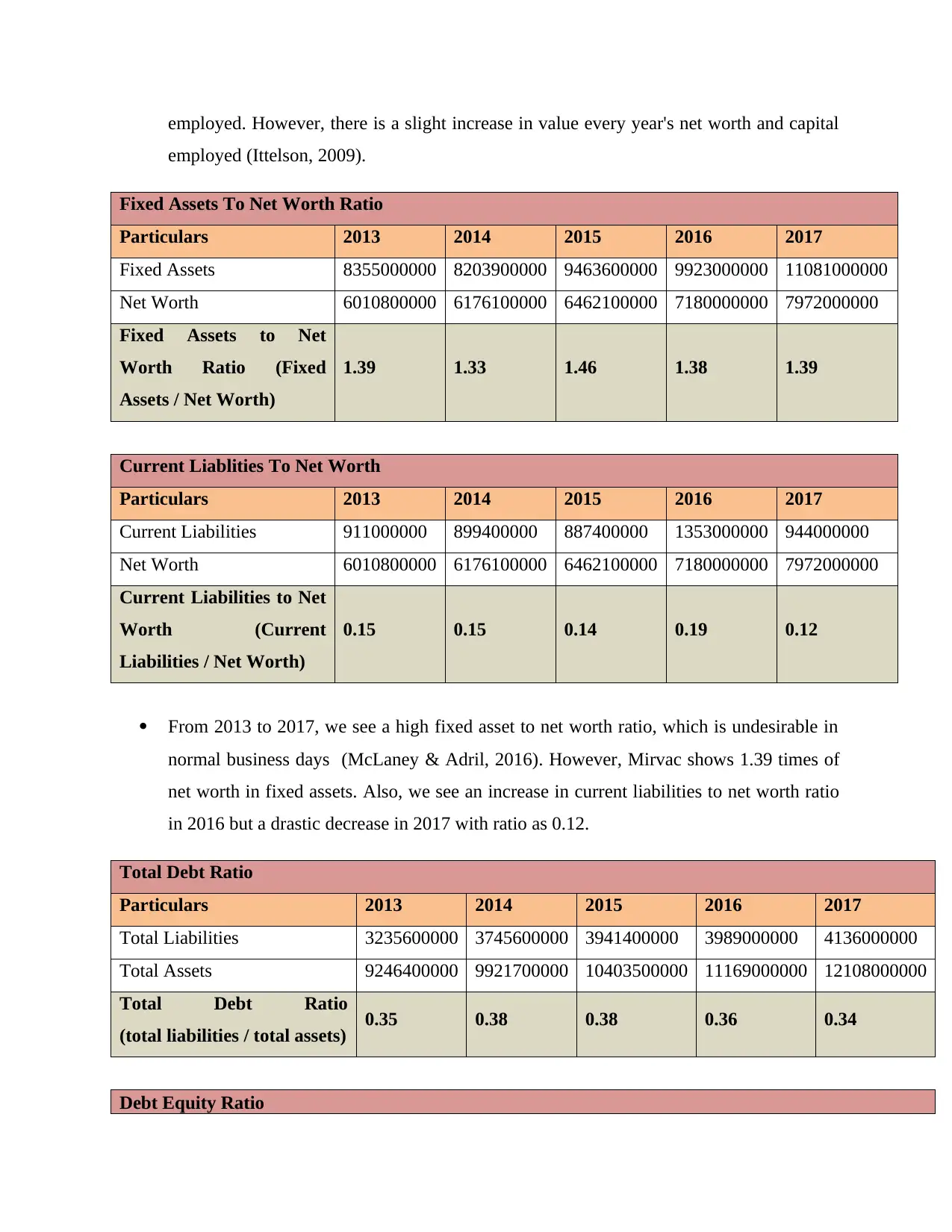

Fixed Assets To Net Worth Ratio

Particulars 2013 2014 2015 2016 2017

Fixed Assets 8355000000 8203900000 9463600000 9923000000 11081000000

Net Worth 6010800000 6176100000 6462100000 7180000000 7972000000

Fixed Assets to Net

Worth Ratio (Fixed

Assets / Net Worth)

1.39 1.33 1.46 1.38 1.39

Current Liablities To Net Worth

Particulars 2013 2014 2015 2016 2017

Current Liabilities 911000000 899400000 887400000 1353000000 944000000

Net Worth 6010800000 6176100000 6462100000 7180000000 7972000000

Current Liabilities to Net

Worth (Current

Liabilities / Net Worth)

0.15 0.15 0.14 0.19 0.12

From 2013 to 2017, we see a high fixed asset to net worth ratio, which is undesirable in

normal business days (McLaney & Adril, 2016). However, Mirvac shows 1.39 times of

net worth in fixed assets. Also, we see an increase in current liabilities to net worth ratio

in 2016 but a drastic decrease in 2017 with ratio as 0.12.

Total Debt Ratio

Particulars 2013 2014 2015 2016 2017

Total Liabilities 3235600000 3745600000 3941400000 3989000000 4136000000

Total Assets 9246400000 9921700000 10403500000 11169000000 12108000000

Total Debt Ratio

(total liabilities / total assets) 0.35 0.38 0.38 0.36 0.34

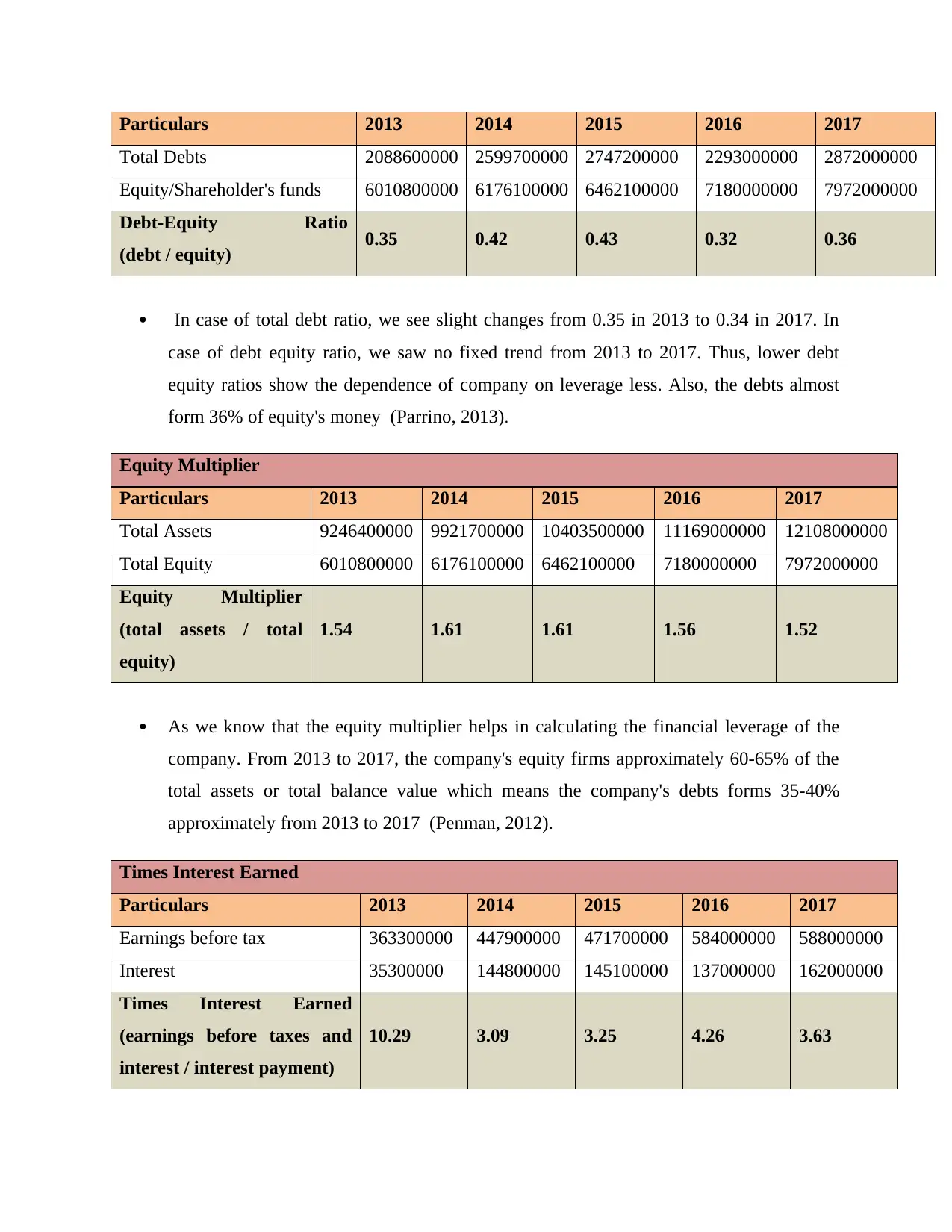

Debt Equity Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Debts 2088600000 2599700000 2747200000 2293000000 2872000000

Equity/Shareholder's funds 6010800000 6176100000 6462100000 7180000000 7972000000

Debt-Equity Ratio

(debt / equity) 0.35 0.42 0.43 0.32 0.36

In case of total debt ratio, we see slight changes from 0.35 in 2013 to 0.34 in 2017. In

case of debt equity ratio, we saw no fixed trend from 2013 to 2017. Thus, lower debt

equity ratios show the dependence of company on leverage less. Also, the debts almost

form 36% of equity's money (Parrino, 2013).

Equity Multiplier

Particulars 2013 2014 2015 2016 2017

Total Assets 9246400000 9921700000 10403500000 11169000000 12108000000

Total Equity 6010800000 6176100000 6462100000 7180000000 7972000000

Equity Multiplier

(total assets / total

equity)

1.54 1.61 1.61 1.56 1.52

As we know that the equity multiplier helps in calculating the financial leverage of the

company. From 2013 to 2017, the company's equity firms approximately 60-65% of the

total assets or total balance value which means the company's debts forms 35-40%

approximately from 2013 to 2017 (Penman, 2012).

Times Interest Earned

Particulars 2013 2014 2015 2016 2017

Earnings before tax 363300000 447900000 471700000 584000000 588000000

Interest 35300000 144800000 145100000 137000000 162000000

Times Interest Earned

(earnings before taxes and

interest / interest payment)

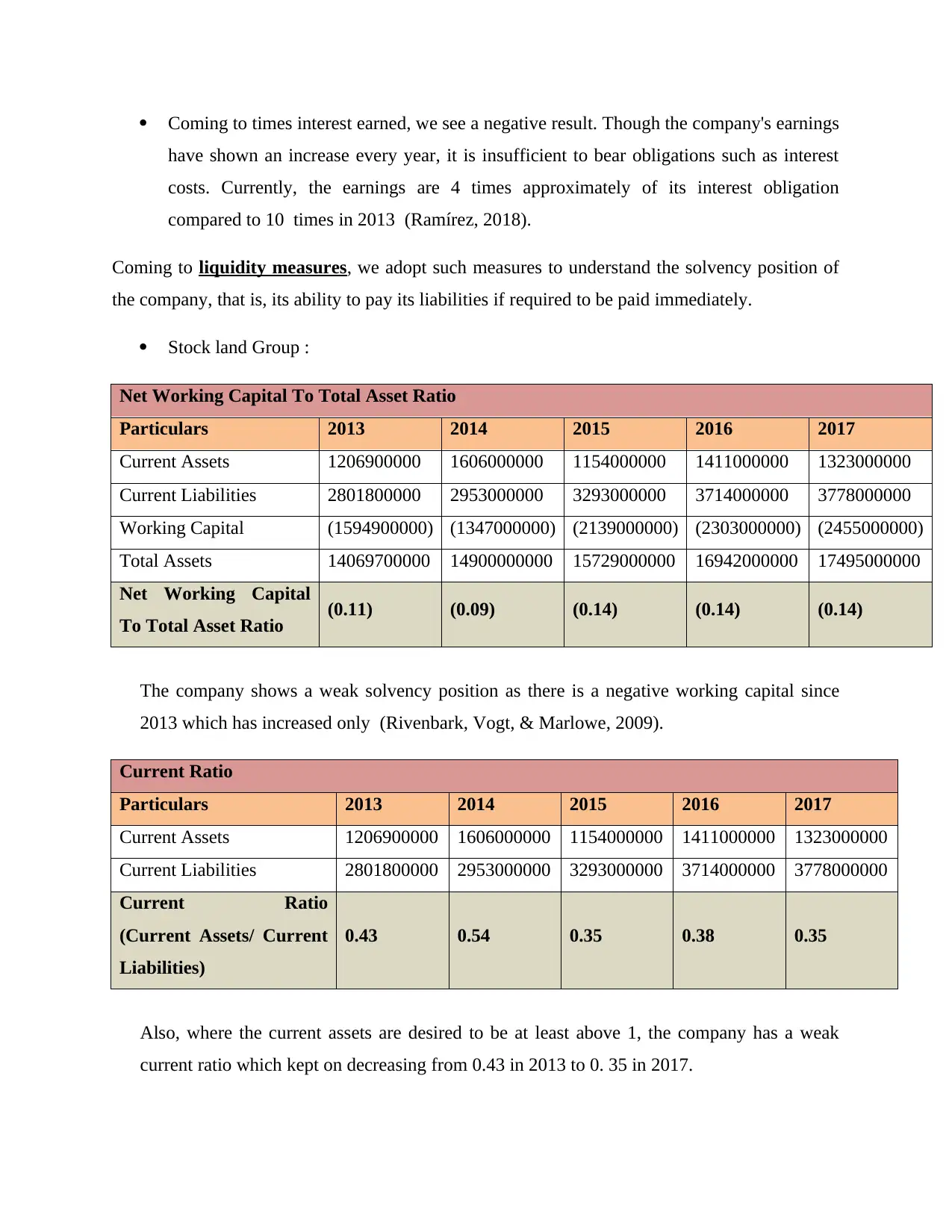

10.29 3.09 3.25 4.26 3.63

Paraphrase This Document

have shown an increase every year, it is insufficient to bear obligations such as interest

costs. Currently, the earnings are 4 times approximately of its interest obligation

compared to 10 times in 2013 (Ramírez, 2018).

Coming to liquidity measures, we adopt such measures to understand the solvency position of

the company, that is, its ability to pay its liabilities if required to be paid immediately.

Stock land Group :

Net Working Capital To Total Asset Ratio

Particulars 2013 2014 2015 2016 2017

Current Assets 1206900000 1606000000 1154000000 1411000000 1323000000

Current Liabilities 2801800000 2953000000 3293000000 3714000000 3778000000

Working Capital (1594900000) (1347000000) (2139000000) (2303000000) (2455000000)

Total Assets 14069700000 14900000000 15729000000 16942000000 17495000000

Net Working Capital

To Total Asset Ratio (0.11) (0.09) (0.14) (0.14) (0.14)

The company shows a weak solvency position as there is a negative working capital since

2013 which has increased only (Rivenbark, Vogt, & Marlowe, 2009).

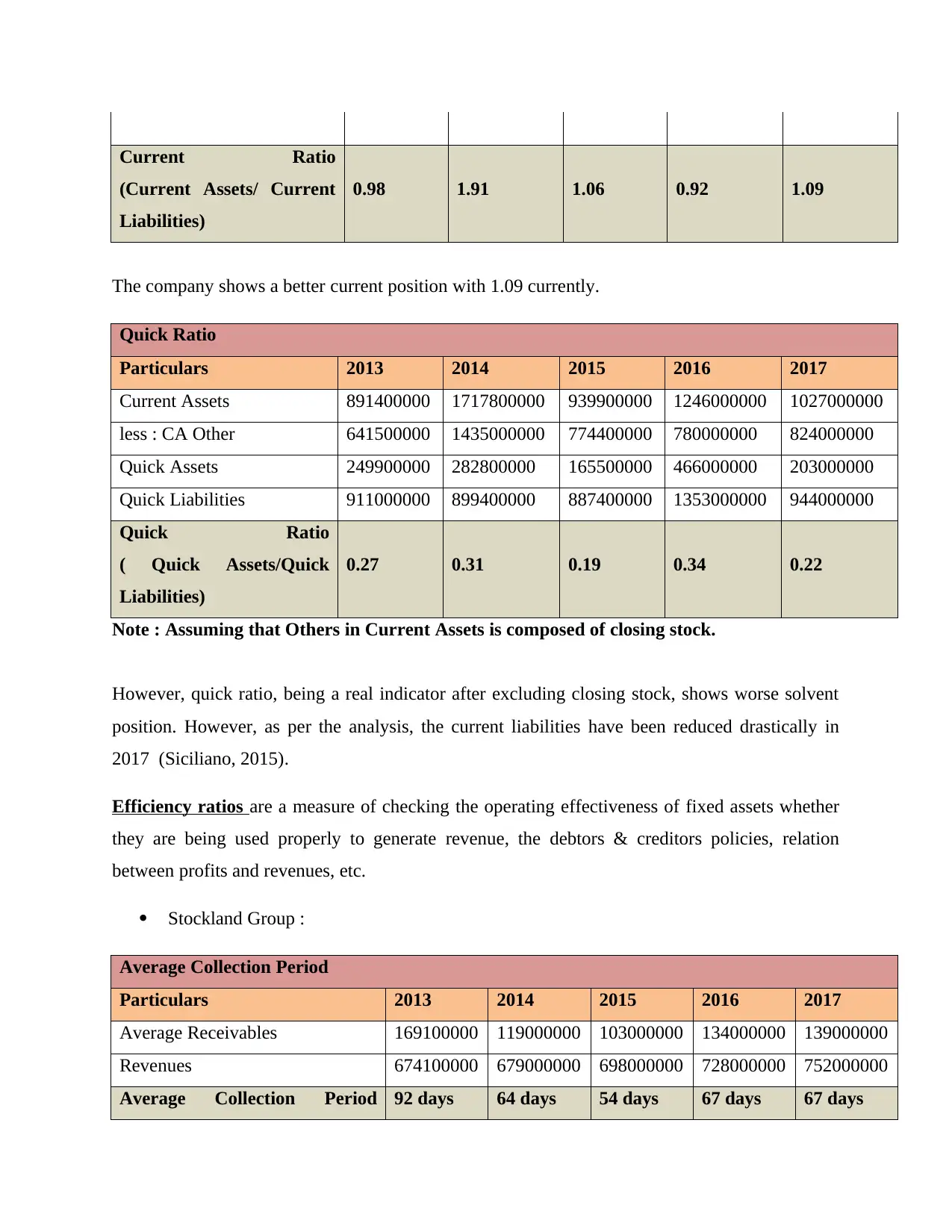

Current Ratio

Particulars 2013 2014 2015 2016 2017

Current Assets 1206900000 1606000000 1154000000 1411000000 1323000000

Current Liabilities 2801800000 2953000000 3293000000 3714000000 3778000000

Current Ratio

(Current Assets/ Current

Liabilities)

0.43 0.54 0.35 0.38 0.35

Also, where the current assets are desired to be at least above 1, the company has a weak

current ratio which kept on decreasing from 0.43 in 2013 to 0. 35 in 2017.

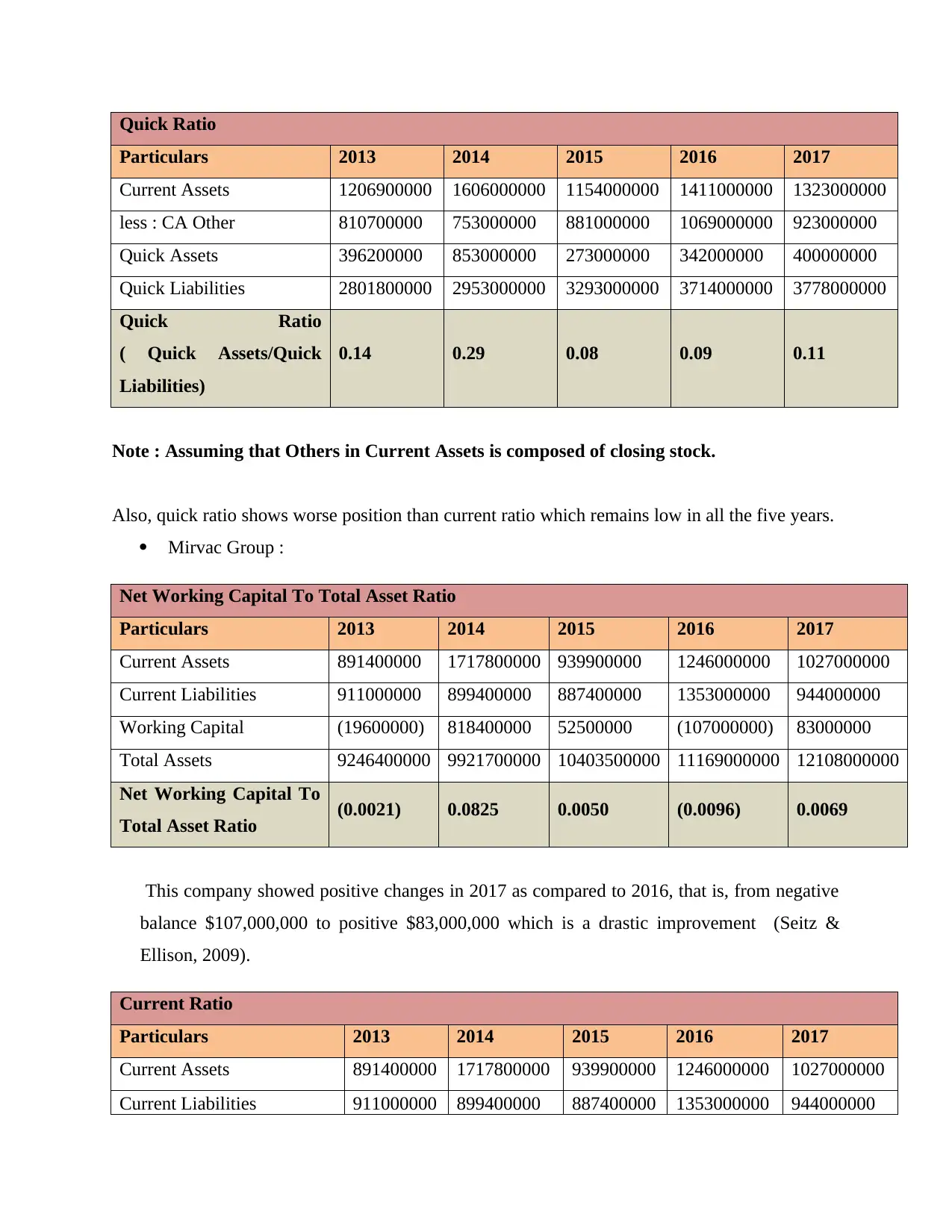

Particulars 2013 2014 2015 2016 2017

Current Assets 1206900000 1606000000 1154000000 1411000000 1323000000

less : CA Other 810700000 753000000 881000000 1069000000 923000000

Quick Assets 396200000 853000000 273000000 342000000 400000000

Quick Liabilities 2801800000 2953000000 3293000000 3714000000 3778000000

Quick Ratio

( Quick Assets/Quick

Liabilities)

0.14 0.29 0.08 0.09 0.11

Note : Assuming that Others in Current Assets is composed of closing stock.

Also, quick ratio shows worse position than current ratio which remains low in all the five years.

Mirvac Group :

Net Working Capital To Total Asset Ratio

Particulars 2013 2014 2015 2016 2017

Current Assets 891400000 1717800000 939900000 1246000000 1027000000

Current Liabilities 911000000 899400000 887400000 1353000000 944000000

Working Capital (19600000) 818400000 52500000 (107000000) 83000000

Total Assets 9246400000 9921700000 10403500000 11169000000 12108000000

Net Working Capital To

Total Asset Ratio (0.0021) 0.0825 0.0050 (0.0096) 0.0069

This company showed positive changes in 2017 as compared to 2016, that is, from negative

balance $107,000,000 to positive $83,000,000 which is a drastic improvement (Seitz &

Ellison, 2009).

Current Ratio

Particulars 2013 2014 2015 2016 2017

Current Assets 891400000 1717800000 939900000 1246000000 1027000000

Current Liabilities 911000000 899400000 887400000 1353000000 944000000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Current Assets/ Current

Liabilities)

0.98 1.91 1.06 0.92 1.09

The company shows a better current position with 1.09 currently.

Quick Ratio

Particulars 2013 2014 2015 2016 2017

Current Assets 891400000 1717800000 939900000 1246000000 1027000000

less : CA Other 641500000 1435000000 774400000 780000000 824000000

Quick Assets 249900000 282800000 165500000 466000000 203000000

Quick Liabilities 911000000 899400000 887400000 1353000000 944000000

Quick Ratio

( Quick Assets/Quick

Liabilities)

0.27 0.31 0.19 0.34 0.22

Note : Assuming that Others in Current Assets is composed of closing stock.

However, quick ratio, being a real indicator after excluding closing stock, shows worse solvent

position. However, as per the analysis, the current liabilities have been reduced drastically in

2017 (Siciliano, 2015).

Efficiency ratios are a measure of checking the operating effectiveness of fixed assets whether

they are being used properly to generate revenue, the debtors & creditors policies, relation

between profits and revenues, etc.

Stockland Group :

Average Collection Period

Particulars 2013 2014 2015 2016 2017

Average Receivables 169100000 119000000 103000000 134000000 139000000

Revenues 674100000 679000000 698000000 728000000 752000000

Average Collection Period 92 days 64 days 54 days 67 days 67 days

Paraphrase This Document

Receivables*365/revenues)

[in days]

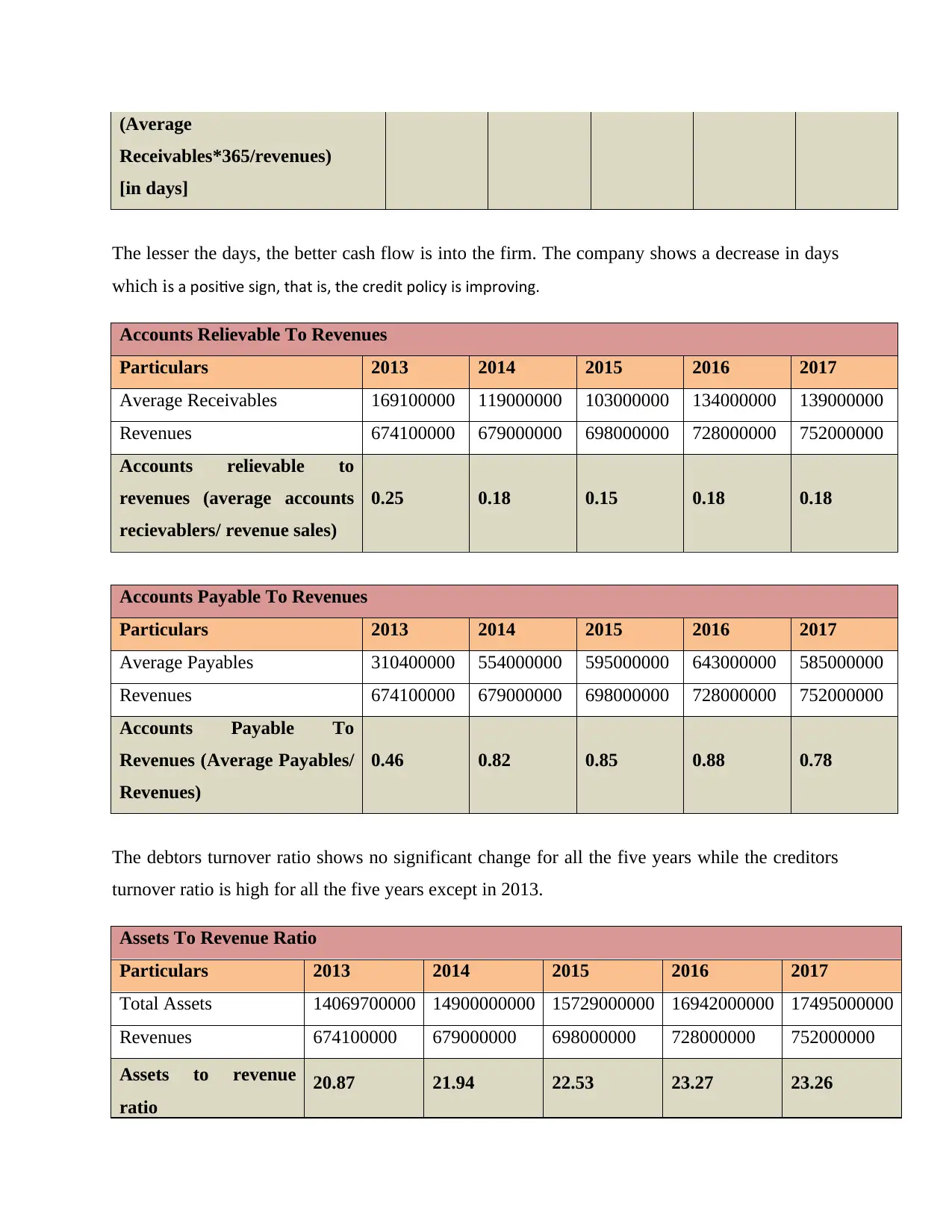

The lesser the days, the better cash flow is into the firm. The company shows a decrease in days

which is a positive sign, that is, the credit policy is improving.

Accounts Relievable To Revenues

Particulars 2013 2014 2015 2016 2017

Average Receivables 169100000 119000000 103000000 134000000 139000000

Revenues 674100000 679000000 698000000 728000000 752000000

Accounts relievable to

revenues (average accounts

recievablers/ revenue sales)

0.25 0.18 0.15 0.18 0.18

Accounts Payable To Revenues

Particulars 2013 2014 2015 2016 2017

Average Payables 310400000 554000000 595000000 643000000 585000000

Revenues 674100000 679000000 698000000 728000000 752000000

Accounts Payable To

Revenues (Average Payables/

Revenues)

0.46 0.82 0.85 0.88 0.78

The debtors turnover ratio shows no significant change for all the five years while the creditors

turnover ratio is high for all the five years except in 2013.

Assets To Revenue Ratio

Particulars 2013 2014 2015 2016 2017

Total Assets 14069700000 14900000000 15729000000 16942000000 17495000000

Revenues 674100000 679000000 698000000 728000000 752000000

Assets to revenue

ratio

20.87 21.94 22.53 23.27 23.26

Revenues)

Total Assets Ratio

Particulars 2013 2014 2015 2016 2017

Revenues 674100000 679000000 698000000 728000000 752000000

Total Assets 14069700000 14900000000 15729000000 16942000000 17495000000

Total Assets Ratio

( Revenues/ Total

Sales)

0.05 0.05 0.04 0.04 0.04

The asset to revenue shows a positive result which is 24% in 2017. However, the total asset ratio

shows a negative result meaning that the company isn't using it fixed assets in the most effecient

way.

Working Capital Turnovers

Particulars 2013 2014 2015 2016 2017

Revenues 674100000 679000000 698000000 728000000 752000000

Working Capital (1594900000) (1347000000) (2139000000) (2303000000) (2455000000)

Working Capital

Turnover

( Revenues/Working

Capital)

(0.42) (0.50) (0.33) (0.32) (0.31)

Operational Efficiency Ratio

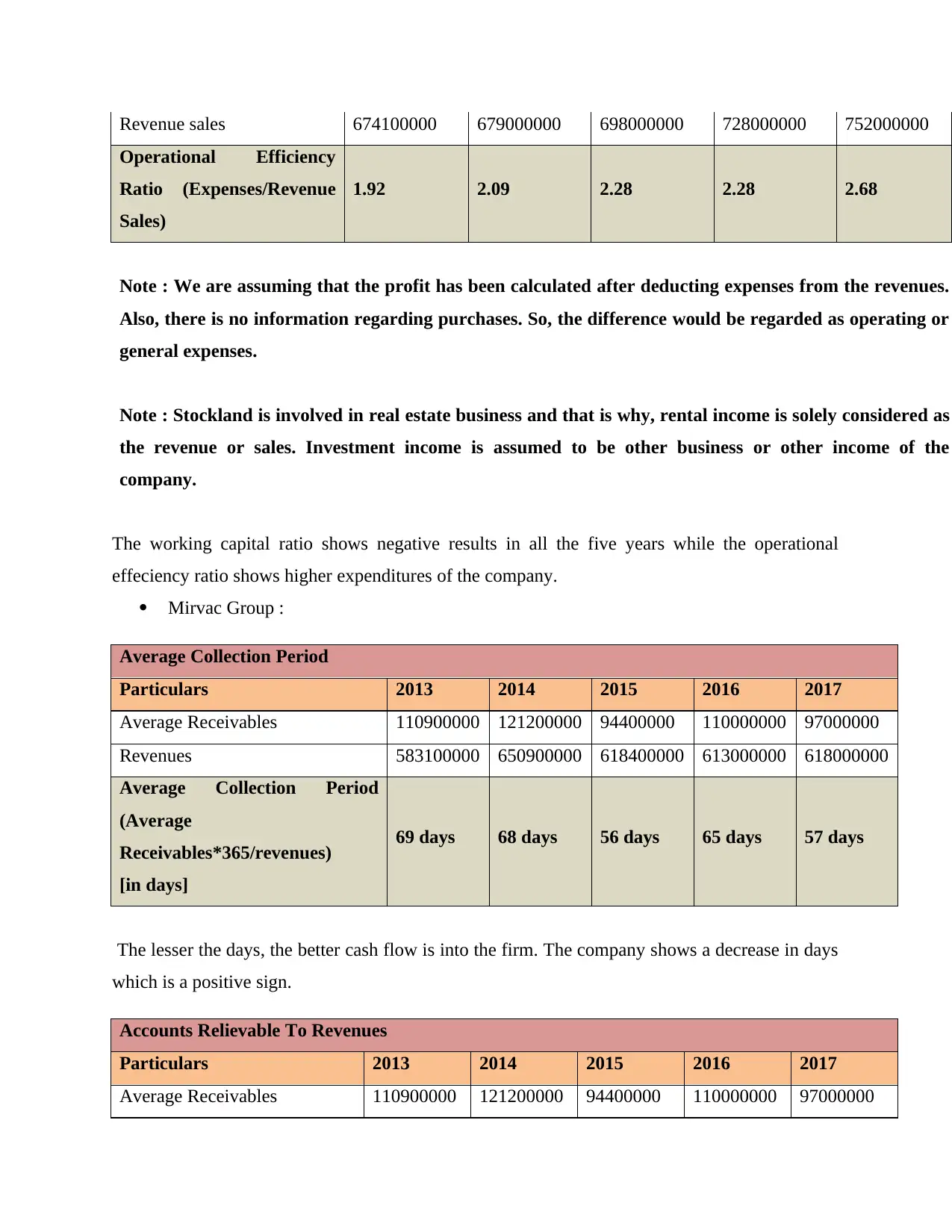

Particulars 2013 2014 2015 2016 2017

Rental Income 674100000 679000000 698000000 728000000 752000000

Investment Income 7100000 24000000 86000000 12000000 75000000

Other Income 1053200000 1241000000 1412000000 1600000000 2043000000

PreTax Profit 440300000 528000000 604000000 681000000 857000000

Expenses 1294100000 1416000000 1592000000 1659000000 2013000000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Operational Efficiency

Ratio (Expenses/Revenue

Sales)

1.92 2.09 2.28 2.28 2.68

Note : We are assuming that the profit has been calculated after deducting expenses from the revenues.

Also, there is no information regarding purchases. So, the difference would be regarded as operating or

general expenses.

Note : Stockland is involved in real estate business and that is why, rental income is solely considered as

the revenue or sales. Investment income is assumed to be other business or other income of the

company.

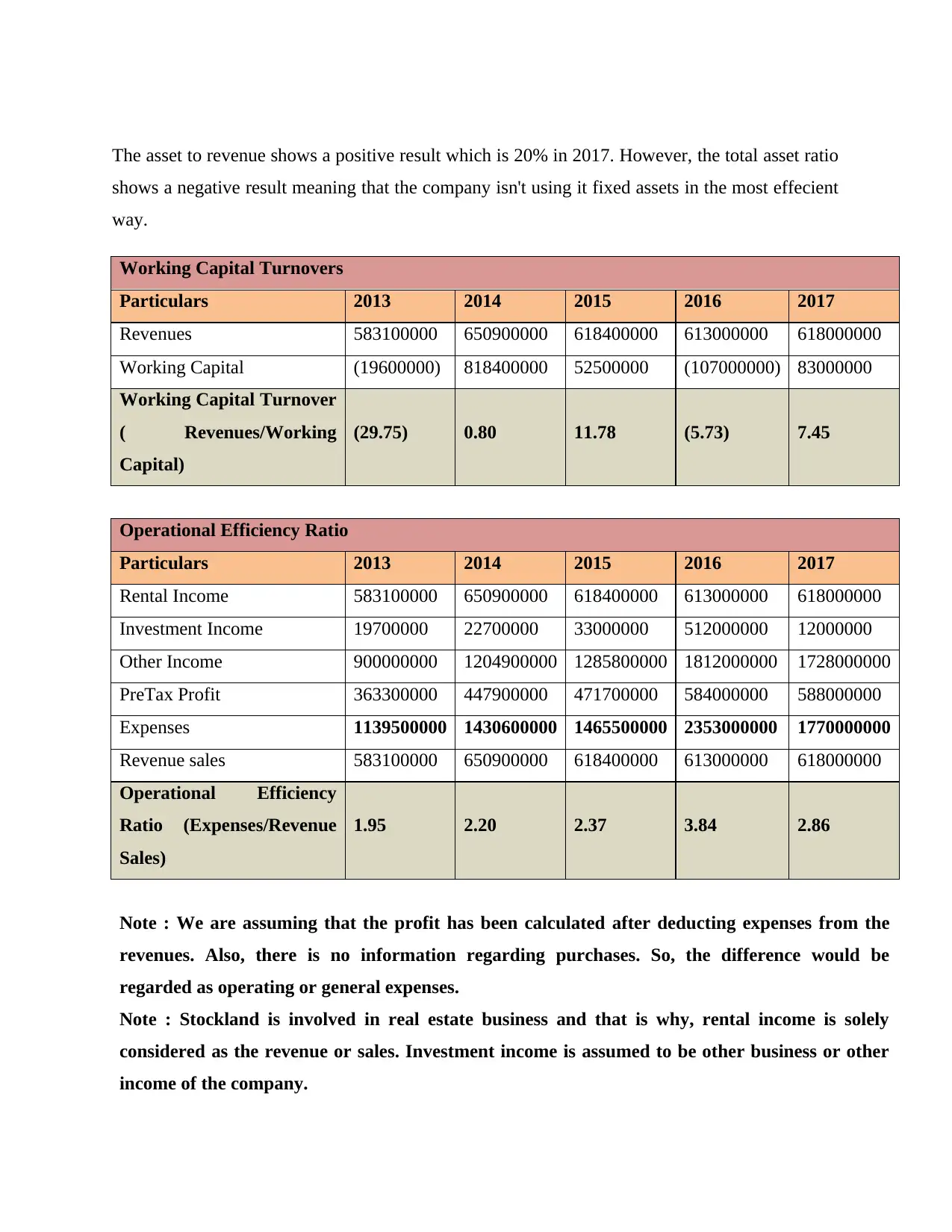

The working capital ratio shows negative results in all the five years while the operational

effeciency ratio shows higher expenditures of the company.

Mirvac Group :

Average Collection Period

Particulars 2013 2014 2015 2016 2017

Average Receivables 110900000 121200000 94400000 110000000 97000000

Revenues 583100000 650900000 618400000 613000000 618000000

Average Collection Period

(Average

Receivables*365/revenues)

[in days]

69 days 68 days 56 days 65 days 57 days

The lesser the days, the better cash flow is into the firm. The company shows a decrease in days

which is a positive sign.

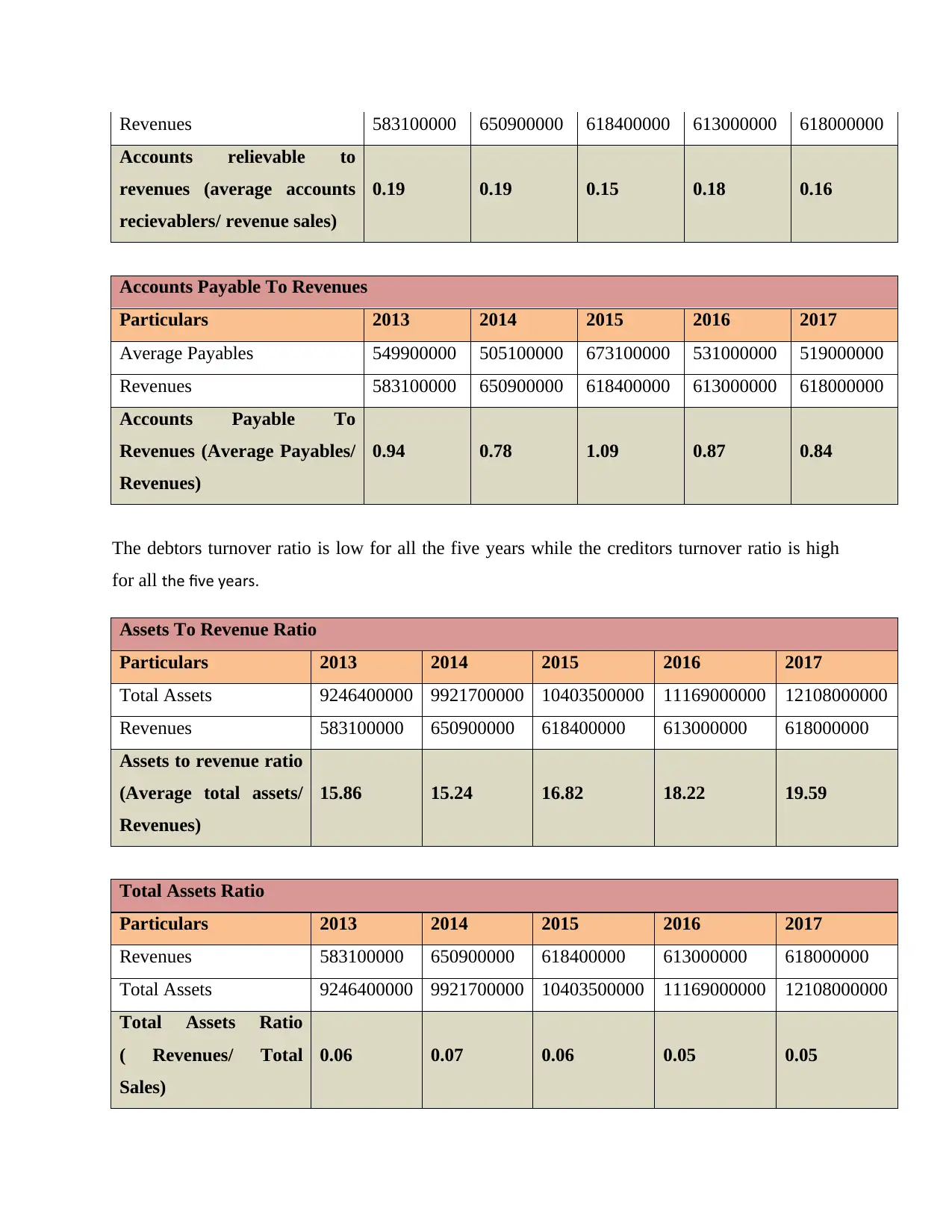

Accounts Relievable To Revenues

Particulars 2013 2014 2015 2016 2017

Average Receivables 110900000 121200000 94400000 110000000 97000000

Paraphrase This Document

Accounts relievable to

revenues (average accounts

recievablers/ revenue sales)

0.19 0.19 0.15 0.18 0.16

Accounts Payable To Revenues

Particulars 2013 2014 2015 2016 2017

Average Payables 549900000 505100000 673100000 531000000 519000000

Revenues 583100000 650900000 618400000 613000000 618000000

Accounts Payable To

Revenues (Average Payables/

Revenues)

0.94 0.78 1.09 0.87 0.84

The debtors turnover ratio is low for all the five years while the creditors turnover ratio is high

for all the five years.

Assets To Revenue Ratio

Particulars 2013 2014 2015 2016 2017

Total Assets 9246400000 9921700000 10403500000 11169000000 12108000000

Revenues 583100000 650900000 618400000 613000000 618000000

Assets to revenue ratio

(Average total assets/

Revenues)

15.86 15.24 16.82 18.22 19.59

Total Assets Ratio

Particulars 2013 2014 2015 2016 2017

Revenues 583100000 650900000 618400000 613000000 618000000

Total Assets 9246400000 9921700000 10403500000 11169000000 12108000000

Total Assets Ratio

( Revenues/ Total

Sales)

0.06 0.07 0.06 0.05 0.05

shows a negative result meaning that the company isn't using it fixed assets in the most effecient

way.

Working Capital Turnovers

Particulars 2013 2014 2015 2016 2017

Revenues 583100000 650900000 618400000 613000000 618000000

Working Capital (19600000) 818400000 52500000 (107000000) 83000000

Working Capital Turnover

( Revenues/Working

Capital)

(29.75) 0.80 11.78 (5.73) 7.45

Operational Efficiency Ratio

Particulars 2013 2014 2015 2016 2017

Rental Income 583100000 650900000 618400000 613000000 618000000

Investment Income 19700000 22700000 33000000 512000000 12000000

Other Income 900000000 1204900000 1285800000 1812000000 1728000000

PreTax Profit 363300000 447900000 471700000 584000000 588000000

Expenses 1139500000 1430600000 1465500000 2353000000 1770000000

Revenue sales 583100000 650900000 618400000 613000000 618000000

Operational Efficiency

Ratio (Expenses/Revenue

Sales)

1.95 2.20 2.37 3.84 2.86

Note : We are assuming that the profit has been calculated after deducting expenses from the

revenues. Also, there is no information regarding purchases. So, the difference would be

regarded as operating or general expenses.

Note : Stockland is involved in real estate business and that is why, rental income is solely

considered as the revenue or sales. Investment income is assumed to be other business or other

income of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ratio shows higher expenditures of the company.

Profitability measures show the relation between the profits and revenues of the company and

the return to equity shareholders. Also, it shows the return on assets to show how well the assets

are being used to generate revenues.

Stockland Group :

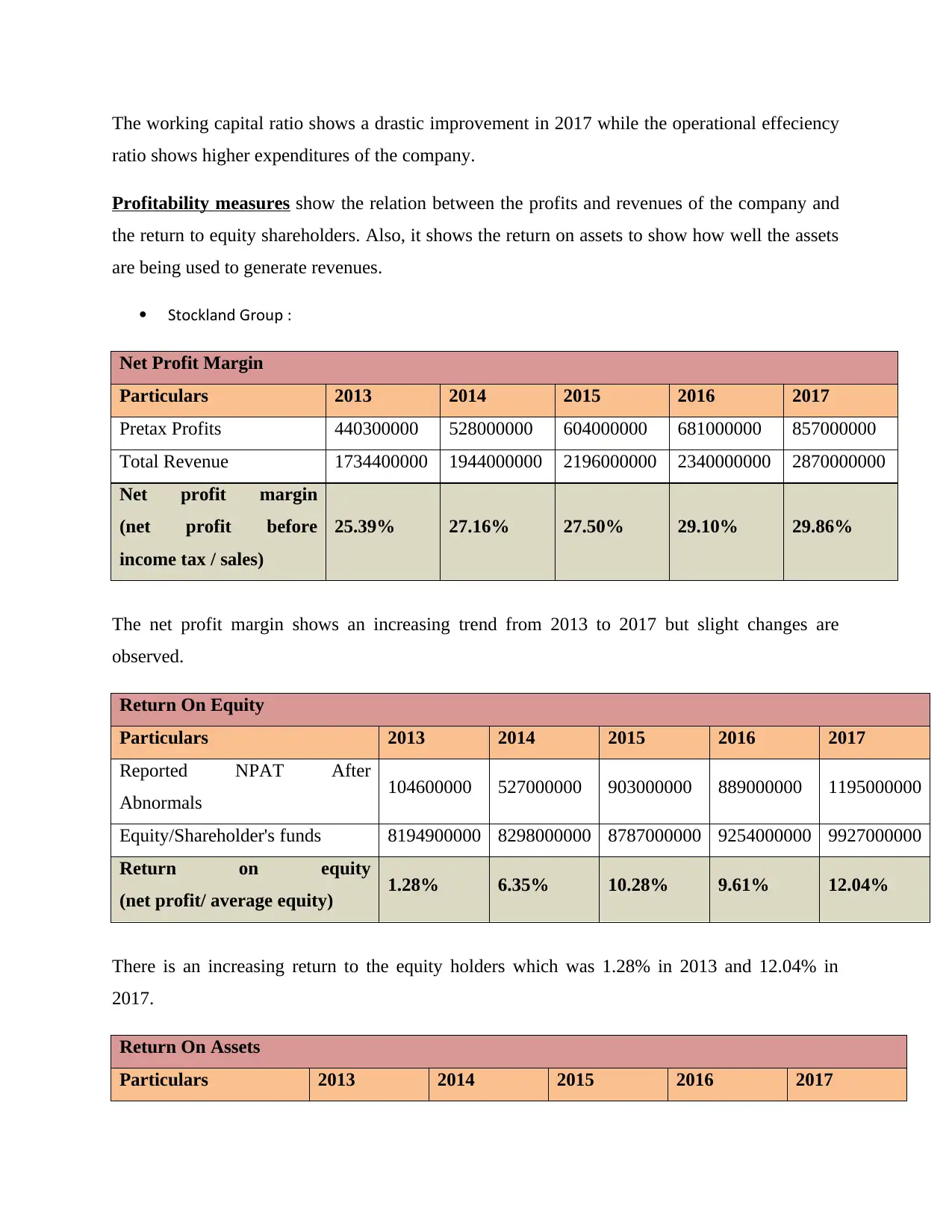

Net Profit Margin

Particulars 2013 2014 2015 2016 2017

Pretax Profits 440300000 528000000 604000000 681000000 857000000

Total Revenue 1734400000 1944000000 2196000000 2340000000 2870000000

Net profit margin

(net profit before

income tax / sales)

25.39% 27.16% 27.50% 29.10% 29.86%

The net profit margin shows an increasing trend from 2013 to 2017 but slight changes are

observed.

Return On Equity

Particulars 2013 2014 2015 2016 2017

Reported NPAT After

Abnormals 104600000 527000000 903000000 889000000 1195000000

Equity/Shareholder's funds 8194900000 8298000000 8787000000 9254000000 9927000000

Return on equity

(net profit/ average equity) 1.28% 6.35% 10.28% 9.61% 12.04%

There is an increasing return to the equity holders which was 1.28% in 2013 and 12.04% in

2017.

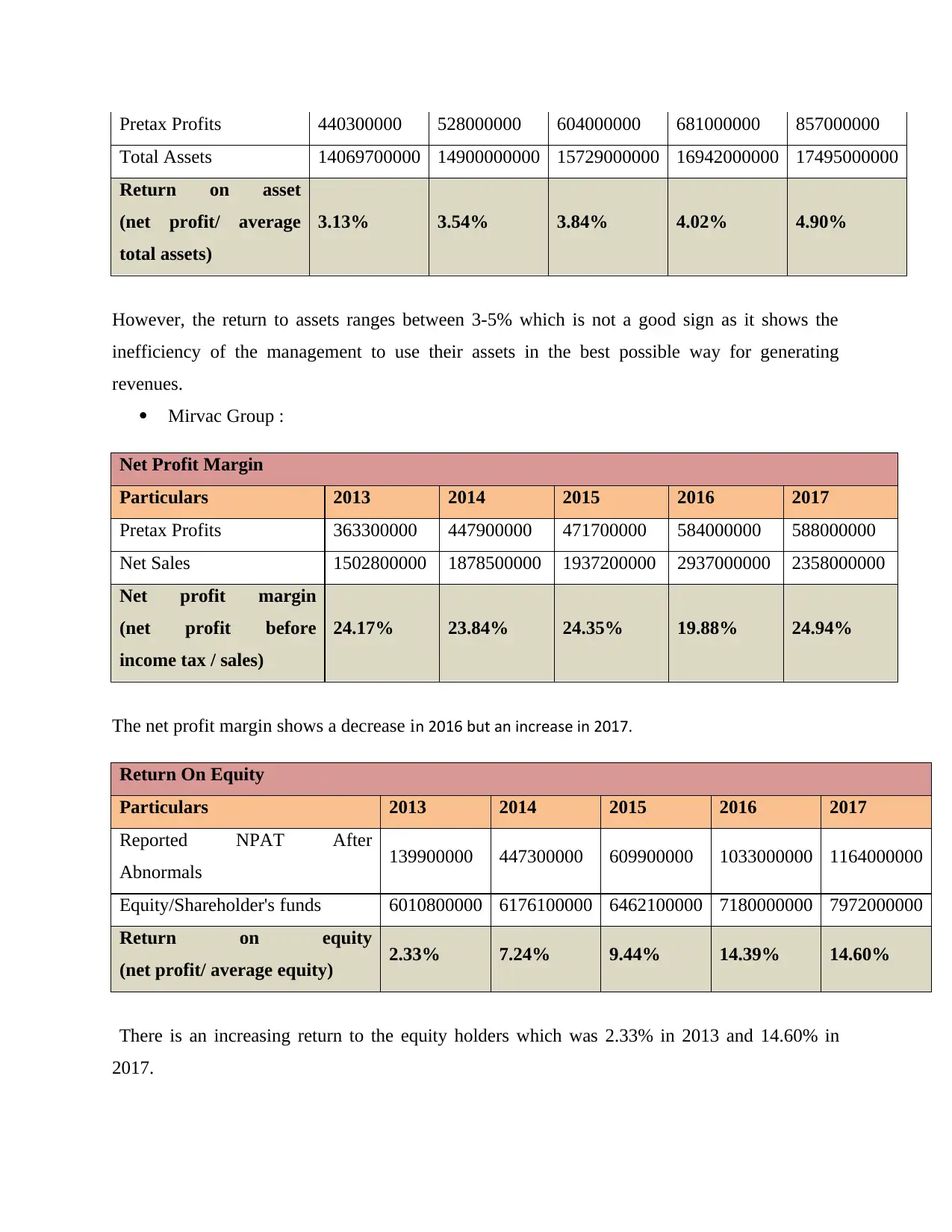

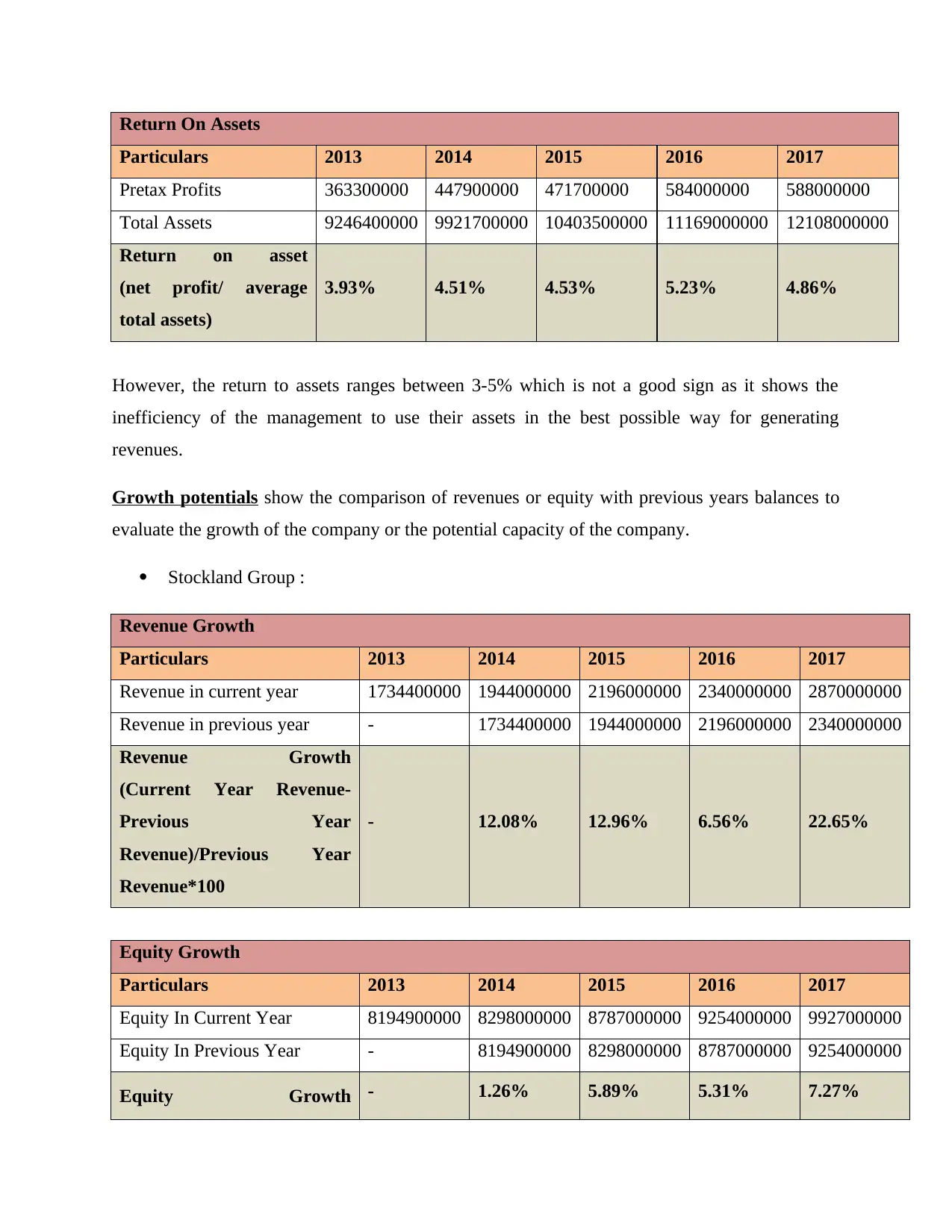

Return On Assets

Particulars 2013 2014 2015 2016 2017

Paraphrase This Document

Total Assets 14069700000 14900000000 15729000000 16942000000 17495000000

Return on asset

(net profit/ average

total assets)

3.13% 3.54% 3.84% 4.02% 4.90%

However, the return to assets ranges between 3-5% which is not a good sign as it shows the

inefficiency of the management to use their assets in the best possible way for generating

revenues.

Mirvac Group :

Net Profit Margin

Particulars 2013 2014 2015 2016 2017

Pretax Profits 363300000 447900000 471700000 584000000 588000000

Net Sales 1502800000 1878500000 1937200000 2937000000 2358000000

Net profit margin

(net profit before

income tax / sales)

24.17% 23.84% 24.35% 19.88% 24.94%

The net profit margin shows a decrease in 2016 but an increase in 2017.

Return On Equity

Particulars 2013 2014 2015 2016 2017

Reported NPAT After

Abnormals 139900000 447300000 609900000 1033000000 1164000000

Equity/Shareholder's funds 6010800000 6176100000 6462100000 7180000000 7972000000

Return on equity

(net profit/ average equity) 2.33% 7.24% 9.44% 14.39% 14.60%

There is an increasing return to the equity holders which was 2.33% in 2013 and 14.60% in

2017.

Particulars 2013 2014 2015 2016 2017

Pretax Profits 363300000 447900000 471700000 584000000 588000000

Total Assets 9246400000 9921700000 10403500000 11169000000 12108000000

Return on asset

(net profit/ average

total assets)

3.93% 4.51% 4.53% 5.23% 4.86%

However, the return to assets ranges between 3-5% which is not a good sign as it shows the

inefficiency of the management to use their assets in the best possible way for generating

revenues.

Growth potentials show the comparison of revenues or equity with previous years balances to

evaluate the growth of the company or the potential capacity of the company.

Stockland Group :

Revenue Growth

Particulars 2013 2014 2015 2016 2017

Revenue in current year 1734400000 1944000000 2196000000 2340000000 2870000000

Revenue in previous year - 1734400000 1944000000 2196000000 2340000000

Revenue Growth

(Current Year Revenue-

Previous Year

Revenue)/Previous Year

Revenue*100

- 12.08% 12.96% 6.56% 22.65%

Equity Growth

Particulars 2013 2014 2015 2016 2017

Equity In Current Year 8194900000 8298000000 8787000000 9254000000 9927000000

Equity In Previous Year - 8194900000 8298000000 8787000000 9254000000

Equity Growth - 1.26% 5.89% 5.31% 7.27%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

equity in previous

year/previous year

equity)*100

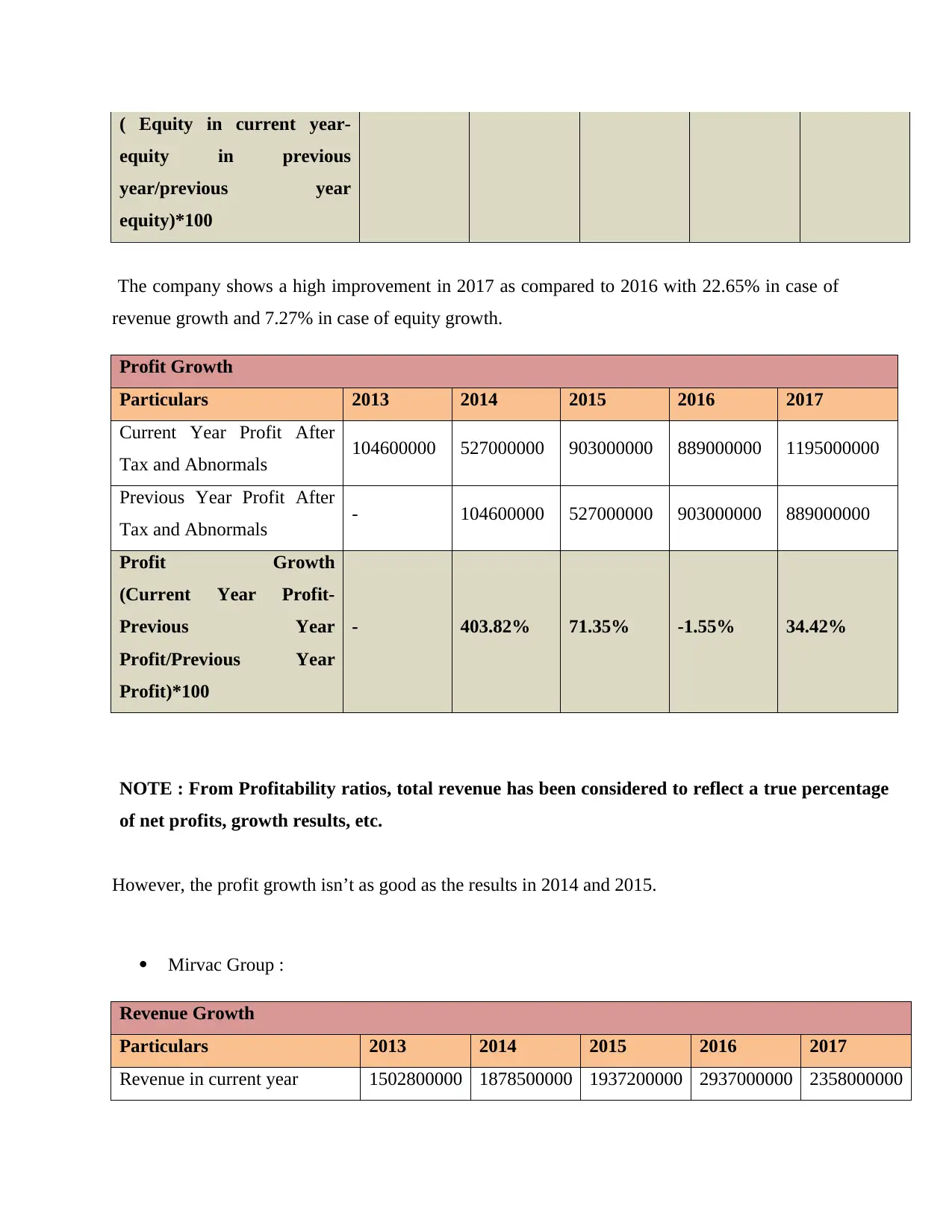

The company shows a high improvement in 2017 as compared to 2016 with 22.65% in case of

revenue growth and 7.27% in case of equity growth.

Profit Growth

Particulars 2013 2014 2015 2016 2017

Current Year Profit After

Tax and Abnormals 104600000 527000000 903000000 889000000 1195000000

Previous Year Profit After

Tax and Abnormals - 104600000 527000000 903000000 889000000

Profit Growth

(Current Year Profit-

Previous Year

Profit/Previous Year

Profit)*100

- 403.82% 71.35% -1.55% 34.42%

NOTE : From Profitability ratios, total revenue has been considered to reflect a true percentage

of net profits, growth results, etc.

However, the profit growth isn’t as good as the results in 2014 and 2015.

Mirvac Group :

Revenue Growth

Particulars 2013 2014 2015 2016 2017

Revenue in current year 1502800000 1878500000 1937200000 2937000000 2358000000

Paraphrase This Document

Revenue Growth

(Current Year Revenue-

Previous Year

Revenue)/Previous Year

Revenue*100

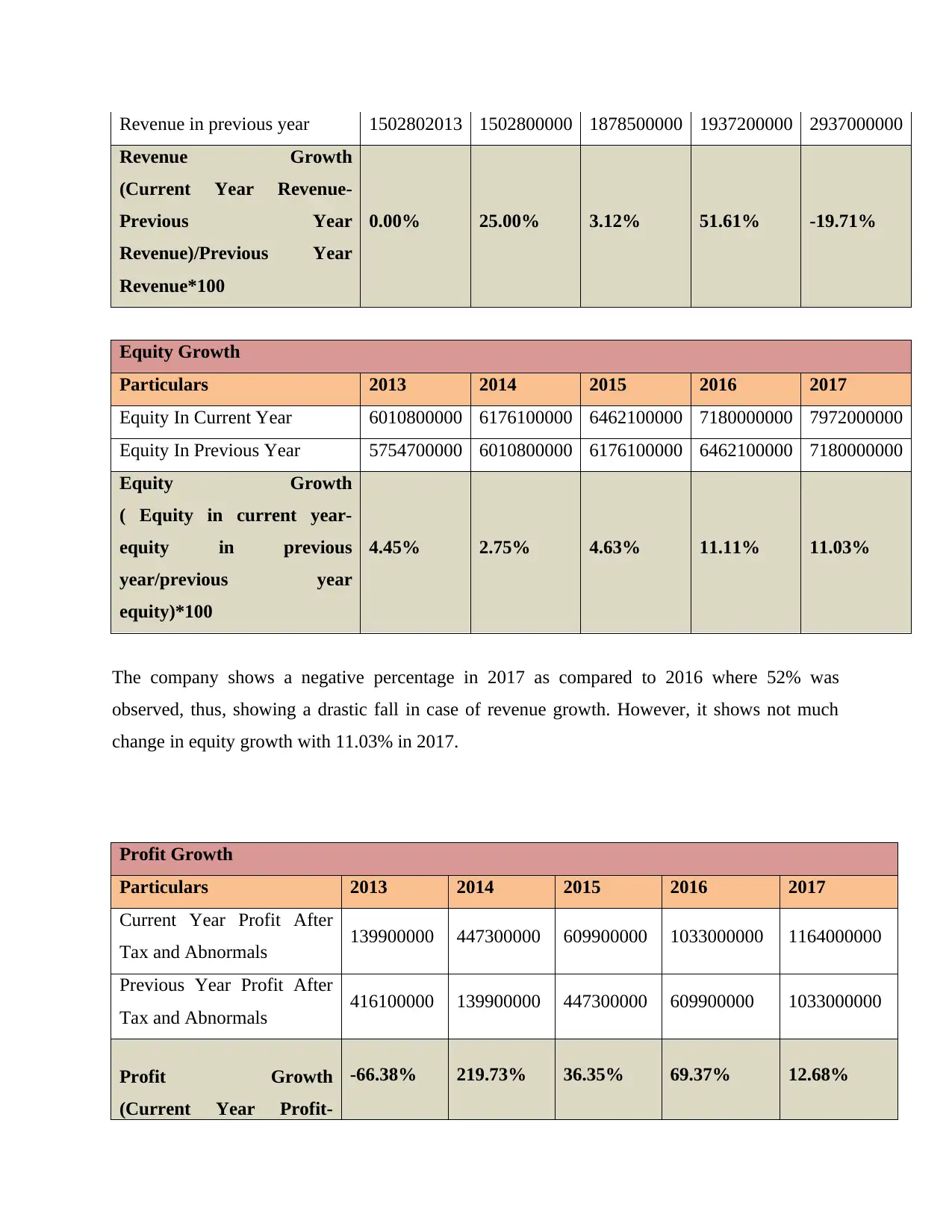

0.00% 25.00% 3.12% 51.61% -19.71%

Equity Growth

Particulars 2013 2014 2015 2016 2017

Equity In Current Year 6010800000 6176100000 6462100000 7180000000 7972000000

Equity In Previous Year 5754700000 6010800000 6176100000 6462100000 7180000000

Equity Growth

( Equity in current year-

equity in previous

year/previous year

equity)*100

4.45% 2.75% 4.63% 11.11% 11.03%

The company shows a negative percentage in 2017 as compared to 2016 where 52% was

observed, thus, showing a drastic fall in case of revenue growth. However, it shows not much

change in equity growth with 11.03% in 2017.

Profit Growth

Particulars 2013 2014 2015 2016 2017

Current Year Profit After

Tax and Abnormals 139900000 447300000 609900000 1033000000 1164000000

Previous Year Profit After

Tax and Abnormals 416100000 139900000 447300000 609900000 1033000000

Profit Growth

(Current Year Profit-

-66.38% 219.73% 36.35% 69.37% 12.68%

Profit/Previous Year

Profit)*100

NOTE : From Profitability ratios, total revenue has been considered to reflect a true percentage

of net profits, growth results, etc.

Also, the profit growth isn’t as good as the results in 2014 and 2016. It is much lower in the

current year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Comparing the overall performance of both the companies:

Stockland shows negative working capital for all the five years indicating heavy burden

of liabilities over it while Mirvac did show a negative balance in 2016 but showed a

drastic improvement in 2017 by reducing its liabilities.

Stockland shows higher net worth than Mirvac while Mirvac shows higher capital

employed than Stockland. Mirvac has lesser burden lf debts over it as compared to

Stockland. However, the interest bearing ratio is way better in case of Stockland with

approximately 10 times while it is just 4 times in case of Mirvac in the year 2017.

Mirvac shows a better current ratio than Stockland. Also, the credit policy of Mirvac is

better with 57 days in 2017 as compared to 67 days in case of Stockland. Both the

companies show drastic revenue to asset ratios. However, the Mirvac has a better

working capital turnover in 2017 as compared to negative results in Stockland.

The net profit margin is higher in case of Stockland while return on equity is higher in

case of Mirvac. The revenue growth of Mirvac shows a negative change while Stockland

shows a good & high change in revenue growth. On the other hand, Mirvac shows better

equity growth than Stockland. However, the profit growth of Stockland is much higher

than Mirvac Group (Skonieczny, 2012).

Paraphrase This Document

Analyzing the companies individually and comparing their results, the observations say that both

the companies have flaws and therefore, relevant decision is hard to be formed. However, we

consider Mirvac Group to be a better capitalizing and ideal partner. The following organization

will form the most appropriate potential partnership with HPL.

The reasons behind recommending this company can be enumerated as below:

The company shows drastic improvements in 2017 as compared to 2016. For example,

the positive change in working capital but Stockland Group shows negative working

capital balances over the last five years.

Mirvac Group has a better capital structure than Stockland in terms of equity debt

structure, that is, it has a lesser proportion of debts in its capital structure. Also, the

company has a better current ratio reflecting a better liquidity status. Mirvac has a better

credit policy (Taillard, 2013).

It’s true that a better revenue growth is observed in Stockland which is a vital need for

every company but having a better equity growth is a positive signal for long term

sustainability as it shows the external stakeholders increasing trust and confidence in the

company.

However, the most commendable part of Mirvac Group is its drastic improvements in the year

2017 which were worse in 2016. This somewhere shows the company's ability to take strong

decisions and focusing more on other factors than higher revenues. The company's changes such

as reduction of current liabilities, increase in current assets, increase in equity growth, better

debtor turnover, etc reflects its strong determination towards taking its company onto higher

levels. This also proves their promising nature towards the coming up projects and thus, we

recommend Mirvac Group for this deal.

The above comparative analysis is however restricted to the financial information. The certain

information such as a company's future plans, or some ongoing projects due to which it is

incurring heavy expenditure and such other non financial information are equally important to

understand the business operations and accordingly, compare it with other companies. However,

ratio analysis tool aren't based on such information. We can conclude by choosing Mirvac over

Stockland for HPL Limited on the basis of above analysis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Alvarez, F. (2013). Financial statement analysis. Hoboken, N.J.: Wiley.

Atkinson, A. A. (2012). Management accounting. Upper Saddle River, N.J.: Paerson.

Berry, L. E. (2009). Management accounting demystified. New York: McGraw-Hill.

Boyd, W. K. (2013). Cost Accounting For Dummies. Hoboken: Wiley.

Easton, P. (2010). Financial statement analysis & valuation. Cambridge, UK: Cambridge

Business Publishers.

Elaine, H. (2015). International financial statement analysis. Hoboken: John Wiley & Sons.

Fridson, M., & Alvarez, F. (2012). Financial Statement Analysis: A Practitioner's Guide. New

York: John Wiley & Sons.

Girard, S. L. (2014). Business finance basics. Pompton Plains, NJ: Career Press.

Ittelson, T. (2009). Financial Statements: A Step-by-Step Guide to Understanding and Creating

Financial Reports. Franklin Lakes, N.J.: Career Press.

McLaney, E., & Adril, D. P. (2016). Accounting and Finance: An Introduction. United

Kingdom: Pearson.

Menifield, C. E. (2014). The Basics of Public Budgeting and Financial Management: A

Handbook for Academics and Practitioners. Lanham, Md.: University Press of America.

Parrino, R. (2013). Fundamentals of Corporate Finance, 2nd Edition. Milton: John Wiley &

Sons.

Penman, S. (2012). Financial statement analysis and security valuation. Boston, Mass.:

McGraw-Hill.

Ramírez, C. Z. (2018). The Impact of IFRS 16 on Key Financial Ratios: A New Methodological

Approach. Accounting in Europe .

Paraphrase This Document

Local Governments. Washington, D.C.: ICMA Press.

Seitz, N., & Ellison, M. (2009). Capital Budgeting and Long-Term Financing Decisions. New

York: Thomson Learning.

Siciliano, G. (2015). Finance for Nonfinancial Managers. New York: McGraw-Hill.

Simpson, M. (2012). Financial accounting. Basingstoke: Macmillan Press.

Skonieczny, M. (2012). The basics of understanding financial statements. Schaumburg, Ill.:

Investment Publishing.

Taillard, M. (2013). Corporate finance for dummies. Hoboken, N.J.: Wiley.

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.