Comprehensive Report on Real Estate Valuation and Appraisal

VerifiedAdded on 2020/05/28

|11

|2732

|347

Report

AI Summary

This report provides a detailed analysis of real estate valuation and appraisal techniques. It explores the term and reversion and hardcore methods for determining market value, using cash flow analysis and risk assessment. The report examines various scenarios, including single and multi-tenant properties, and evaluates the impact of factors such as lease terms, interest rates, and loan-to-value ratios on investment returns. It also considers the uncertainties associated with property investments, such as vacancy periods and refurbishment costs, and analyzes the perspectives of both investors and lenders. The report concludes by highlighting the key considerations for successful real estate investment and financing, emphasizing the importance of comprehensive analysis and risk management.

REAL ESTATE: VALUATION AND APPRAISAL

A REPORT

Introduction

Rental values are subjected to occasional rise and fall, hence the contractual

rent, also known as ‘Passing Rent’, agreed upon in an existing lease is bound to

differ from the current market value of rent. In case the passing rent is less than

the value of the market rent, it is considered that the investment is

‘reversionary’. To evaluate the investment value of an asset, there are different

methods employed by investors, depending on their internal contribution and

the amount borrowed. In the current case, we shall be focussing on the ‘Term

and Reversion’ and the ‘Layer / Hardcore’ methods for determining the

‘Market Value’ of the property under consideration.

Interpreting Valuations

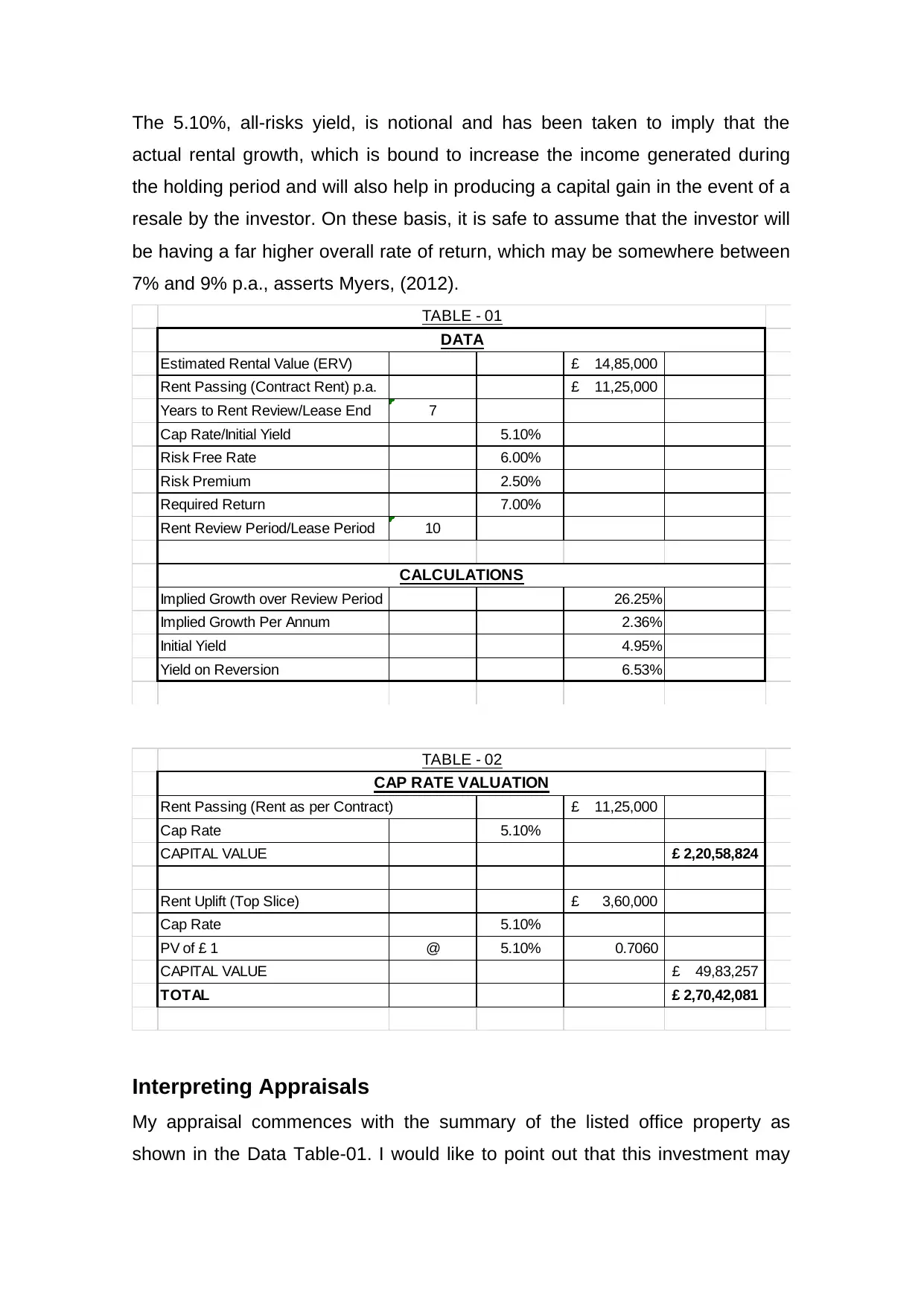

I will illustrate both the methods here, so that it is easy to understand the

calculations and the results shown in the Table. We need to value the property

under consideration by assuming that the ‘Passing Rent’ is £1,125,000 per

annum and this is expected to revert to the market rent valued at £1,148,000

per annum in about 7 years’ time, as per Baum & Baum, (2015).

We have established that the present value at 5.10% of £1 is shown in Table-

02. Through Table-01 we have also established that the initial yield is 4.95%

and the reversionary yield is calculated as 6.53%. The approach adopted here

is known as the ‘Term and Reversion Method’ and as shown in Table-03, the

derived cash flow is considered as ‘sliced vertically’.

I have also adopted an alternative approach and this also generates the same

result. This method is the ‘Hardcore Method’ and here the cash flow is ‘sliced

horizontally’. The results have been shown in Table-04. For the benefit of the

investor, I wish to make a note that the ‘Total Returns’ shown in the calculations

on the basis of 5.10% initial yield are not the investor’s total or overall returns.

A REPORT

Introduction

Rental values are subjected to occasional rise and fall, hence the contractual

rent, also known as ‘Passing Rent’, agreed upon in an existing lease is bound to

differ from the current market value of rent. In case the passing rent is less than

the value of the market rent, it is considered that the investment is

‘reversionary’. To evaluate the investment value of an asset, there are different

methods employed by investors, depending on their internal contribution and

the amount borrowed. In the current case, we shall be focussing on the ‘Term

and Reversion’ and the ‘Layer / Hardcore’ methods for determining the

‘Market Value’ of the property under consideration.

Interpreting Valuations

I will illustrate both the methods here, so that it is easy to understand the

calculations and the results shown in the Table. We need to value the property

under consideration by assuming that the ‘Passing Rent’ is £1,125,000 per

annum and this is expected to revert to the market rent valued at £1,148,000

per annum in about 7 years’ time, as per Baum & Baum, (2015).

We have established that the present value at 5.10% of £1 is shown in Table-

02. Through Table-01 we have also established that the initial yield is 4.95%

and the reversionary yield is calculated as 6.53%. The approach adopted here

is known as the ‘Term and Reversion Method’ and as shown in Table-03, the

derived cash flow is considered as ‘sliced vertically’.

I have also adopted an alternative approach and this also generates the same

result. This method is the ‘Hardcore Method’ and here the cash flow is ‘sliced

horizontally’. The results have been shown in Table-04. For the benefit of the

investor, I wish to make a note that the ‘Total Returns’ shown in the calculations

on the basis of 5.10% initial yield are not the investor’s total or overall returns.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The 5.10%, all-risks yield, is notional and has been taken to imply that the

actual rental growth, which is bound to increase the income generated during

the holding period and will also help in producing a capital gain in the event of a

resale by the investor. On these basis, it is safe to assume that the investor will

be having a far higher overall rate of return, which may be somewhere between

7% and 9% p.a., asserts Myers, (2012).

Estimated Rental Value (ERV) 14,85,000£

Rent Passing (Contract Rent) p.a. 11,25,000£

Years to Rent Review/Lease End 7

Cap Rate/Initial Yield 5.10%

Risk Free Rate 6.00%

Risk Premium 2.50%

Required Return 7.00%

Rent Review Period/Lease Period 10

Implied Growth over Review Period 26.25%

Implied Growth Per Annum 2.36%

Initial Yield 4.95%

Yield on Reversion 6.53%

TABLE - 01

DATA

CALCULATIONS

Rent Passing (Rent as per Contract) 11,25,000£

Cap Rate 5.10%

CAPITAL VALUE 2,20,58,824£

Rent Uplift (Top Slice) 3,60,000£

Cap Rate 5.10%

PV of £ 1 @ 5.10% 0.7060

CAPITAL VALUE 49,83,257£

TOTAL 2,70,42,081£

TABLE - 02

CAP RATE VALUATION

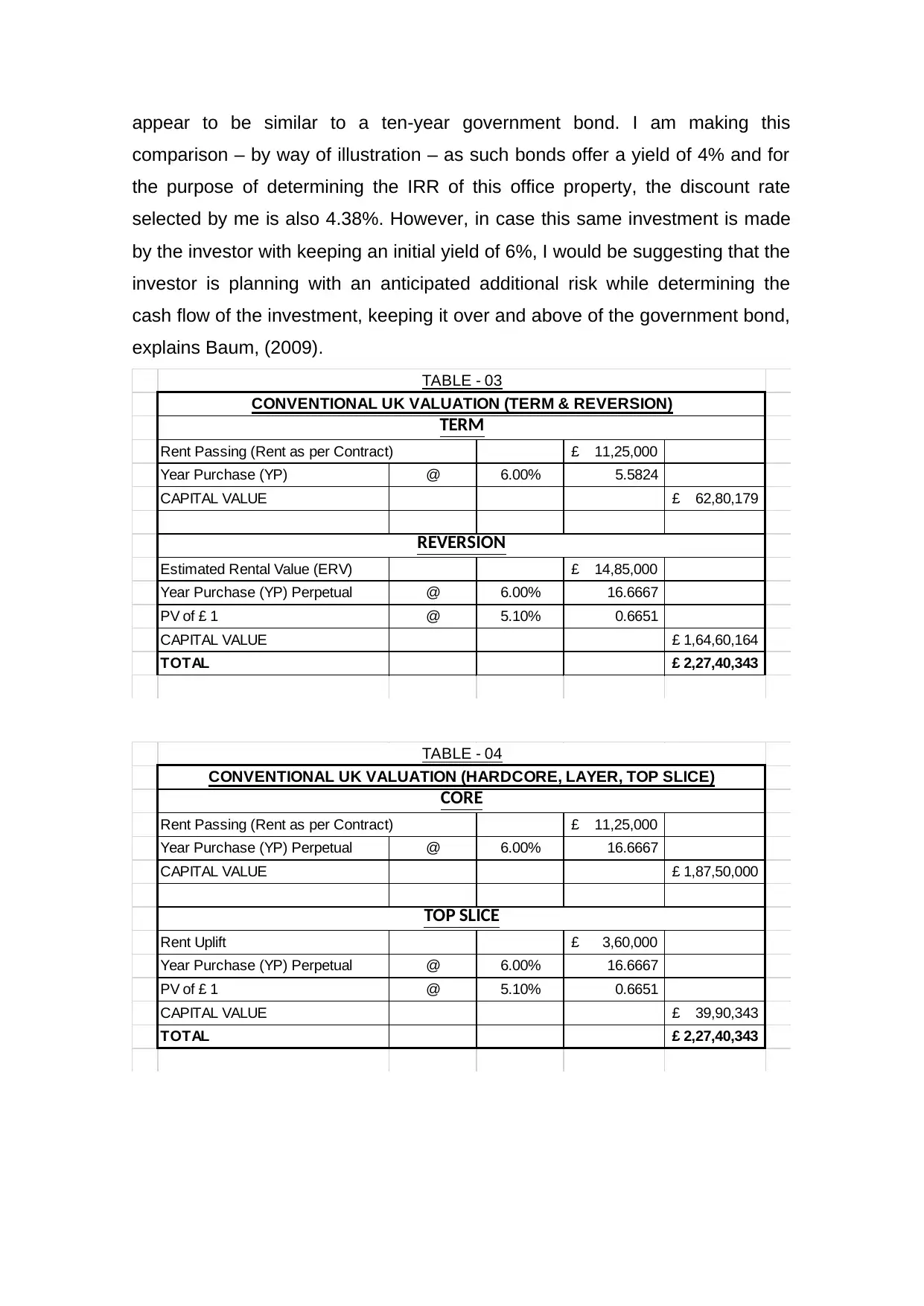

Interpreting Appraisals

My appraisal commences with the summary of the listed office property as

shown in the Data Table-01. I would like to point out that this investment may

actual rental growth, which is bound to increase the income generated during

the holding period and will also help in producing a capital gain in the event of a

resale by the investor. On these basis, it is safe to assume that the investor will

be having a far higher overall rate of return, which may be somewhere between

7% and 9% p.a., asserts Myers, (2012).

Estimated Rental Value (ERV) 14,85,000£

Rent Passing (Contract Rent) p.a. 11,25,000£

Years to Rent Review/Lease End 7

Cap Rate/Initial Yield 5.10%

Risk Free Rate 6.00%

Risk Premium 2.50%

Required Return 7.00%

Rent Review Period/Lease Period 10

Implied Growth over Review Period 26.25%

Implied Growth Per Annum 2.36%

Initial Yield 4.95%

Yield on Reversion 6.53%

TABLE - 01

DATA

CALCULATIONS

Rent Passing (Rent as per Contract) 11,25,000£

Cap Rate 5.10%

CAPITAL VALUE 2,20,58,824£

Rent Uplift (Top Slice) 3,60,000£

Cap Rate 5.10%

PV of £ 1 @ 5.10% 0.7060

CAPITAL VALUE 49,83,257£

TOTAL 2,70,42,081£

TABLE - 02

CAP RATE VALUATION

Interpreting Appraisals

My appraisal commences with the summary of the listed office property as

shown in the Data Table-01. I would like to point out that this investment may

appear to be similar to a ten-year government bond. I am making this

comparison – by way of illustration – as such bonds offer a yield of 4% and for

the purpose of determining the IRR of this office property, the discount rate

selected by me is also 4.38%. However, in case this same investment is made

by the investor with keeping an initial yield of 6%, I would be suggesting that the

investor is planning with an anticipated additional risk while determining the

cash flow of the investment, keeping it over and above of the government bond,

explains Baum, (2009).

Rent Passing (Rent as per Contract) 11,25,000£

Year Purchase (YP) @ 6.00% 5.5824

CAPITAL VALUE 62,80,179£

Estimated Rental Value (ERV) 14,85,000£

Year Purchase (YP) Perpetual @ 6.00% 16.6667

PV of £ 1 @ 5.10% 0.6651

CAPITAL VALUE 1,64,60,164£

TOTAL 2,27,40,343£

TABLE - 03

CONVENTIONAL UK VALUATION (TERM & REVERSION)

TERM

REVERSION

Rent Passing (Rent as per Contract) 11,25,000£

Year Purchase (YP) Perpetual @ 6.00% 16.6667

CAPITAL VALUE 1,87,50,000£

Rent Uplift 3,60,000£

Year Purchase (YP) Perpetual @ 6.00% 16.6667

PV of £ 1 @ 5.10% 0.6651

CAPITAL VALUE 39,90,343£

TOTAL 2,27,40,343£

TABLE - 04

CONVENTIONAL UK VALUATION (HARDCORE, LAYER, TOP SLICE)

CORE

TOP SLICE

comparison – by way of illustration – as such bonds offer a yield of 4% and for

the purpose of determining the IRR of this office property, the discount rate

selected by me is also 4.38%. However, in case this same investment is made

by the investor with keeping an initial yield of 6%, I would be suggesting that the

investor is planning with an anticipated additional risk while determining the

cash flow of the investment, keeping it over and above of the government bond,

explains Baum, (2009).

Rent Passing (Rent as per Contract) 11,25,000£

Year Purchase (YP) @ 6.00% 5.5824

CAPITAL VALUE 62,80,179£

Estimated Rental Value (ERV) 14,85,000£

Year Purchase (YP) Perpetual @ 6.00% 16.6667

PV of £ 1 @ 5.10% 0.6651

CAPITAL VALUE 1,64,60,164£

TOTAL 2,27,40,343£

TABLE - 03

CONVENTIONAL UK VALUATION (TERM & REVERSION)

TERM

REVERSION

Rent Passing (Rent as per Contract) 11,25,000£

Year Purchase (YP) Perpetual @ 6.00% 16.6667

CAPITAL VALUE 1,87,50,000£

Rent Uplift 3,60,000£

Year Purchase (YP) Perpetual @ 6.00% 16.6667

PV of £ 1 @ 5.10% 0.6651

CAPITAL VALUE 39,90,343£

TOTAL 2,27,40,343£

TABLE - 04

CONVENTIONAL UK VALUATION (HARDCORE, LAYER, TOP SLICE)

CORE

TOP SLICE

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

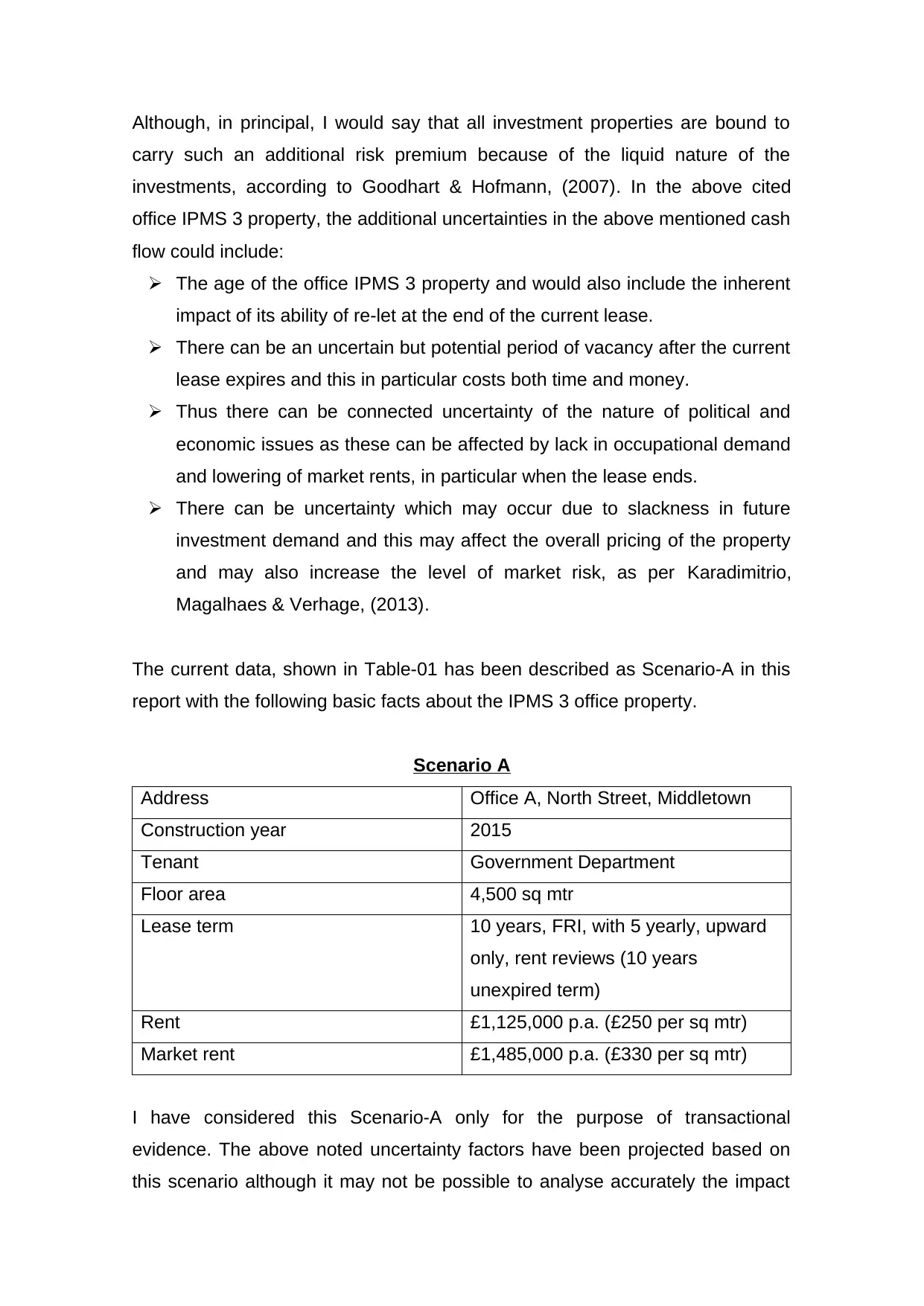

Although, in principal, I would say that all investment properties are bound to

carry such an additional risk premium because of the liquid nature of the

investments, according to Goodhart & Hofmann, (2007). In the above cited

office IPMS 3 property, the additional uncertainties in the above mentioned cash

flow could include:

The age of the office IPMS 3 property and would also include the inherent

impact of its ability of re-let at the end of the current lease.

There can be an uncertain but potential period of vacancy after the current

lease expires and this in particular costs both time and money.

Thus there can be connected uncertainty of the nature of political and

economic issues as these can be affected by lack in occupational demand

and lowering of market rents, in particular when the lease ends.

There can be uncertainty which may occur due to slackness in future

investment demand and this may affect the overall pricing of the property

and may also increase the level of market risk, as per Karadimitrio,

Magalhaes & Verhage, (2013).

The current data, shown in Table-01 has been described as Scenario-A in this

report with the following basic facts about the IPMS 3 office property.

Scenario A

Address Office A, North Street, Middletown

Construction year 2015

Tenant Government Department

Floor area 4,500 sq mtr

Lease term 10 years, FRI, with 5 yearly, upward

only, rent reviews (10 years

unexpired term)

Rent £1,125,000 p.a. (£250 per sq mtr)

Market rent £1,485,000 p.a. (£330 per sq mtr)

I have considered this Scenario-A only for the purpose of transactional

evidence. The above noted uncertainty factors have been projected based on

this scenario although it may not be possible to analyse accurately the impact

carry such an additional risk premium because of the liquid nature of the

investments, according to Goodhart & Hofmann, (2007). In the above cited

office IPMS 3 property, the additional uncertainties in the above mentioned cash

flow could include:

The age of the office IPMS 3 property and would also include the inherent

impact of its ability of re-let at the end of the current lease.

There can be an uncertain but potential period of vacancy after the current

lease expires and this in particular costs both time and money.

Thus there can be connected uncertainty of the nature of political and

economic issues as these can be affected by lack in occupational demand

and lowering of market rents, in particular when the lease ends.

There can be uncertainty which may occur due to slackness in future

investment demand and this may affect the overall pricing of the property

and may also increase the level of market risk, as per Karadimitrio,

Magalhaes & Verhage, (2013).

The current data, shown in Table-01 has been described as Scenario-A in this

report with the following basic facts about the IPMS 3 office property.

Scenario A

Address Office A, North Street, Middletown

Construction year 2015

Tenant Government Department

Floor area 4,500 sq mtr

Lease term 10 years, FRI, with 5 yearly, upward

only, rent reviews (10 years

unexpired term)

Rent £1,125,000 p.a. (£250 per sq mtr)

Market rent £1,485,000 p.a. (£330 per sq mtr)

I have considered this Scenario-A only for the purpose of transactional

evidence. The above noted uncertainty factors have been projected based on

this scenario although it may not be possible to analyse accurately the impact

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

created by each one of the listed factors on the final cash flow. I can safely say

that any adjustments, made to the initial yield, shall be dependent on the

differing characteristics of the property and also rely largely on the experience

and skill of the valuer, aseert Ashworth & Perera, (2015).

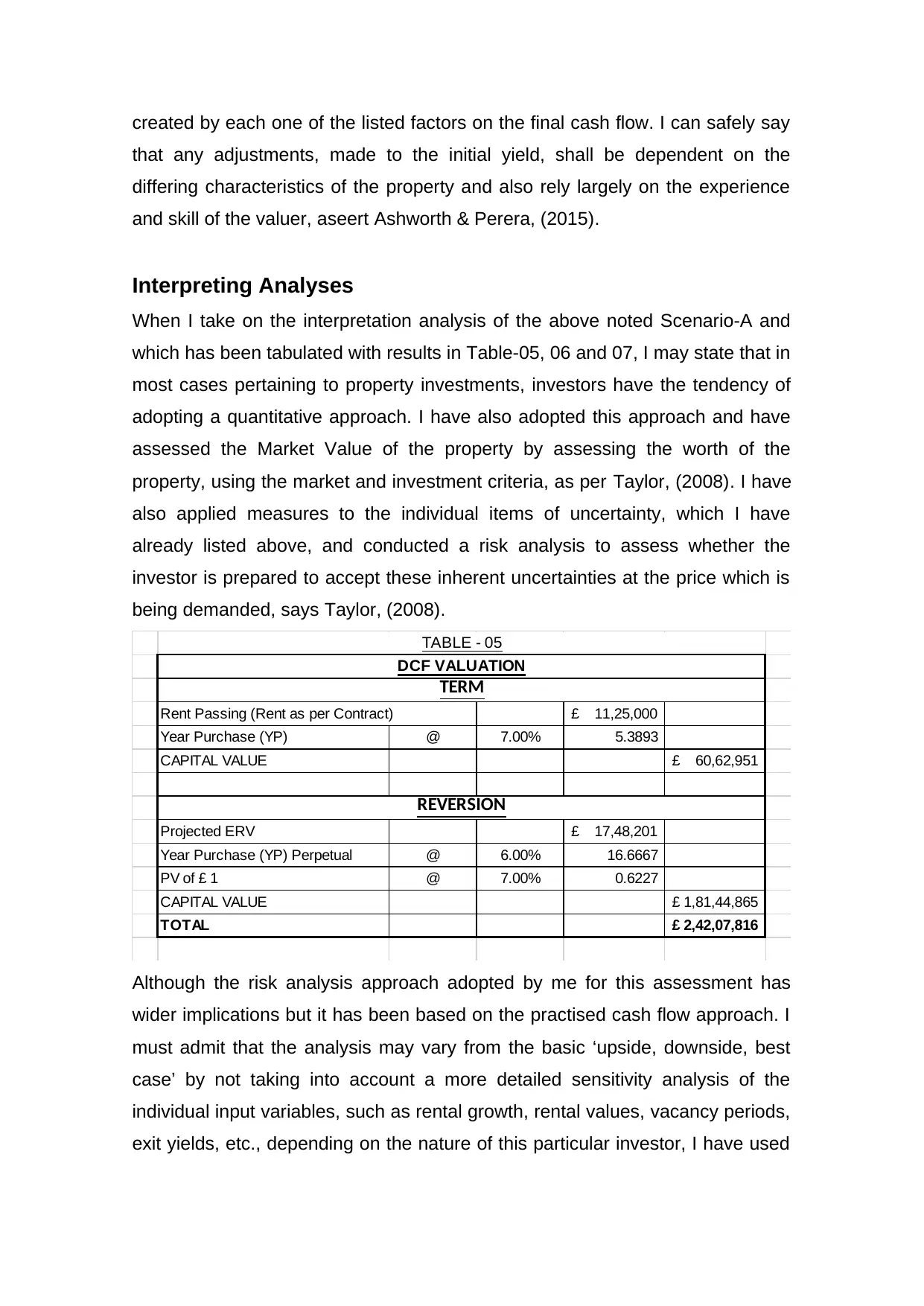

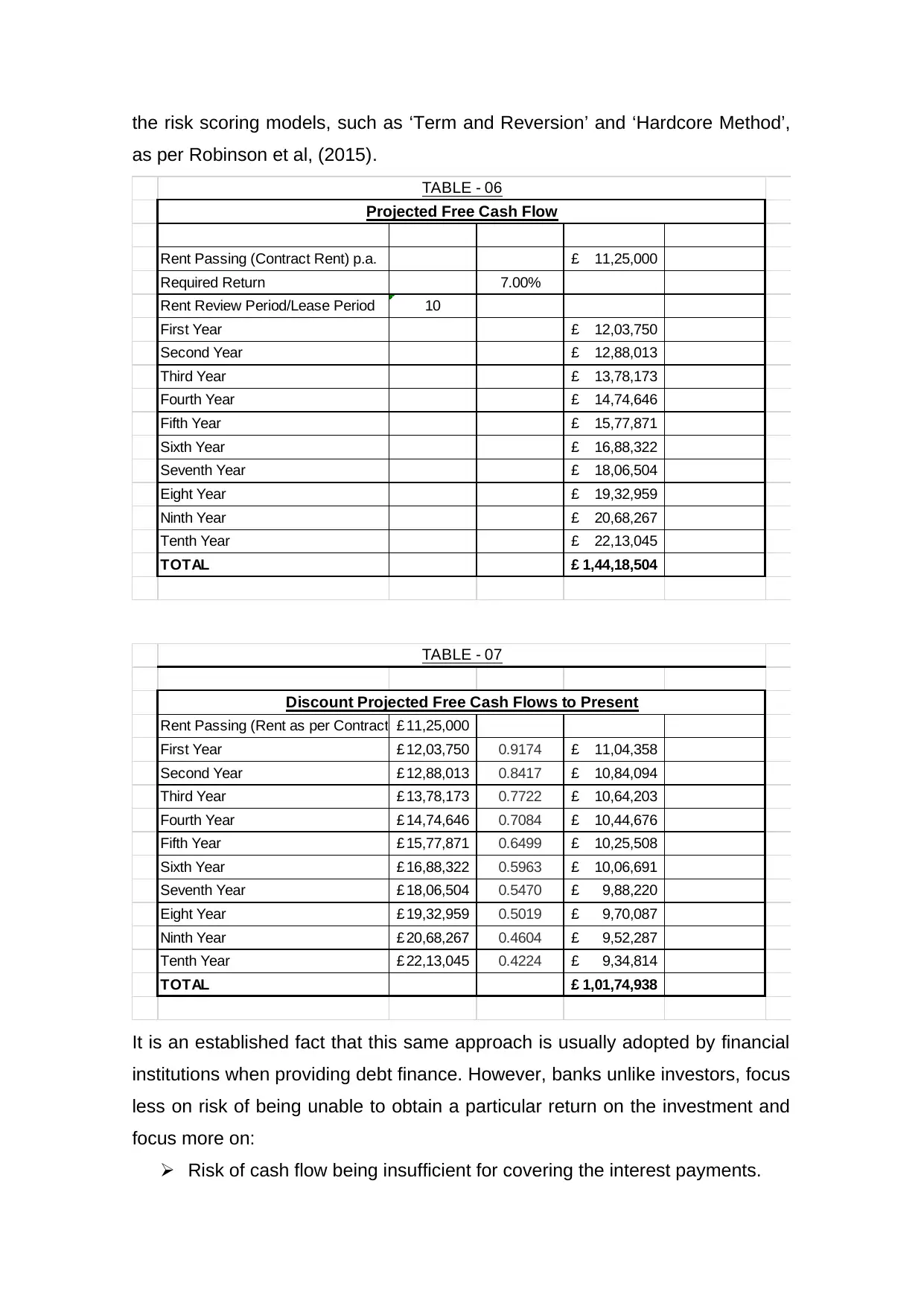

Interpreting Analyses

When I take on the interpretation analysis of the above noted Scenario-A and

which has been tabulated with results in Table-05, 06 and 07, I may state that in

most cases pertaining to property investments, investors have the tendency of

adopting a quantitative approach. I have also adopted this approach and have

assessed the Market Value of the property by assessing the worth of the

property, using the market and investment criteria, as per Taylor, (2008). I have

also applied measures to the individual items of uncertainty, which I have

already listed above, and conducted a risk analysis to assess whether the

investor is prepared to accept these inherent uncertainties at the price which is

being demanded, says Taylor, (2008).

Rent Passing (Rent as per Contract) 11,25,000£

Year Purchase (YP) @ 7.00% 5.3893

CAPITAL VALUE 60,62,951£

Projected ERV 17,48,201£

Year Purchase (YP) Perpetual @ 6.00% 16.6667

PV of £ 1 @ 7.00% 0.6227

CAPITAL VALUE 1,81,44,865£

TOTAL 2,42,07,816£

TABLE - 05

REVERSION

TERM

DCF VALUATION

Although the risk analysis approach adopted by me for this assessment has

wider implications but it has been based on the practised cash flow approach. I

must admit that the analysis may vary from the basic ‘upside, downside, best

case’ by not taking into account a more detailed sensitivity analysis of the

individual input variables, such as rental growth, rental values, vacancy periods,

exit yields, etc., depending on the nature of this particular investor, I have used

that any adjustments, made to the initial yield, shall be dependent on the

differing characteristics of the property and also rely largely on the experience

and skill of the valuer, aseert Ashworth & Perera, (2015).

Interpreting Analyses

When I take on the interpretation analysis of the above noted Scenario-A and

which has been tabulated with results in Table-05, 06 and 07, I may state that in

most cases pertaining to property investments, investors have the tendency of

adopting a quantitative approach. I have also adopted this approach and have

assessed the Market Value of the property by assessing the worth of the

property, using the market and investment criteria, as per Taylor, (2008). I have

also applied measures to the individual items of uncertainty, which I have

already listed above, and conducted a risk analysis to assess whether the

investor is prepared to accept these inherent uncertainties at the price which is

being demanded, says Taylor, (2008).

Rent Passing (Rent as per Contract) 11,25,000£

Year Purchase (YP) @ 7.00% 5.3893

CAPITAL VALUE 60,62,951£

Projected ERV 17,48,201£

Year Purchase (YP) Perpetual @ 6.00% 16.6667

PV of £ 1 @ 7.00% 0.6227

CAPITAL VALUE 1,81,44,865£

TOTAL 2,42,07,816£

TABLE - 05

REVERSION

TERM

DCF VALUATION

Although the risk analysis approach adopted by me for this assessment has

wider implications but it has been based on the practised cash flow approach. I

must admit that the analysis may vary from the basic ‘upside, downside, best

case’ by not taking into account a more detailed sensitivity analysis of the

individual input variables, such as rental growth, rental values, vacancy periods,

exit yields, etc., depending on the nature of this particular investor, I have used

the risk scoring models, such as ‘Term and Reversion’ and ‘Hardcore Method’,

as per Robinson et al, (2015).

Rent Passing (Contract Rent) p.a. 11,25,000£

Required Return 7.00%

Rent Review Period/Lease Period 10

First Year 12,03,750£

Second Year 12,88,013£

Third Year 13,78,173£

Fourth Year 14,74,646£

Fifth Year 15,77,871£

Sixth Year 16,88,322£

Seventh Year 18,06,504£

Eight Year 19,32,959£

Ninth Year 20,68,267£

Tenth Year 22,13,045£

TOTAL 1,44,18,504£

Projected Free Cash Flow

TABLE - 06

Rent Passing (Rent as per Contract) 11,25,000£

First Year 12,03,750£ 0.9174 11,04,358£

Second Year 12,88,013£ 0.8417 10,84,094£

Third Year 13,78,173£ 0.7722 10,64,203£

Fourth Year 14,74,646£ 0.7084 10,44,676£

Fifth Year 15,77,871£ 0.6499 10,25,508£

Sixth Year 16,88,322£ 0.5963 10,06,691£

Seventh Year 18,06,504£ 0.5470 9,88,220£

Eight Year 19,32,959£ 0.5019 9,70,087£

Ninth Year 20,68,267£ 0.4604 9,52,287£

Tenth Year 22,13,045£ 0.4224 9,34,814£

TOTAL 1,01,74,938£

Discount Projected Free Cash Flows to Present

TABLE - 07

It is an established fact that this same approach is usually adopted by financial

institutions when providing debt finance. However, banks unlike investors, focus

less on risk of being unable to obtain a particular return on the investment and

focus more on:

Risk of cash flow being insufficient for covering the interest payments.

as per Robinson et al, (2015).

Rent Passing (Contract Rent) p.a. 11,25,000£

Required Return 7.00%

Rent Review Period/Lease Period 10

First Year 12,03,750£

Second Year 12,88,013£

Third Year 13,78,173£

Fourth Year 14,74,646£

Fifth Year 15,77,871£

Sixth Year 16,88,322£

Seventh Year 18,06,504£

Eight Year 19,32,959£

Ninth Year 20,68,267£

Tenth Year 22,13,045£

TOTAL 1,44,18,504£

Projected Free Cash Flow

TABLE - 06

Rent Passing (Rent as per Contract) 11,25,000£

First Year 12,03,750£ 0.9174 11,04,358£

Second Year 12,88,013£ 0.8417 10,84,094£

Third Year 13,78,173£ 0.7722 10,64,203£

Fourth Year 14,74,646£ 0.7084 10,44,676£

Fifth Year 15,77,871£ 0.6499 10,25,508£

Sixth Year 16,88,322£ 0.5963 10,06,691£

Seventh Year 18,06,504£ 0.5470 9,88,220£

Eight Year 19,32,959£ 0.5019 9,70,087£

Ninth Year 20,68,267£ 0.4604 9,52,287£

Tenth Year 22,13,045£ 0.4224 9,34,814£

TOTAL 1,01,74,938£

Discount Projected Free Cash Flows to Present

TABLE - 07

It is an established fact that this same approach is usually adopted by financial

institutions when providing debt finance. However, banks unlike investors, focus

less on risk of being unable to obtain a particular return on the investment and

focus more on:

Risk of cash flow being insufficient for covering the interest payments.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risk of the residual value of the investment, at the time of maturity of the

loan, being insufficient in being able to repaying the outstanding laon

balance, as detailed by Ostrowski, (2013).

Interpreting Results

In Scenario-A, I had made allowance within the enhanced purchase price, to the

possibility of refurbishing the building after the expiry of its current lease. This

does not remove the uncertainty of the building’s obsolescence and any future

vacancy issues, but it allows the investor in making an assessment of the

impact on his Target Return and in deciding whether it is acceptable, says

Kirkham, (2014). To give an alternate to the existing scenario, I have illustrated,

in Scenario-B below, considering a new debt finance, in the ratio of 65:35,

whereas 65% is the borrowing and 35% is the investor’s contribution. This

borrowing is considered to be secured against the IPMS 3 office building stated

in Scenario-A above. At the time of maturity of this loan, which is in five years’

time, there will still be another five years’ time remaining for the lease term to

expire, but this would not be of concern for the lender as there will not be any

time-lapse in re-letting, asserts Lavender, (2014).

Scenario B

Loan period 5 years

Sum advanced £2 835 000

Loan to value ratio 60%

Interest rate 5% pa Interest cover ratio Minimum × 1.5

(rent/interest)

Amortisation rate 2% pa of sum advanced

Even after allowing for a small downfall in the ‘Market Value’ of the property

during the loan term period, the probability of the borrower in not repaying the

loan remains very low as the ability of the borrower in meeting the finance

interest payments remains comfortable throughout the loan period, as per

Towey, (2013). Thus, despite a shortening of the unexpired term of lease, the

loan, being insufficient in being able to repaying the outstanding laon

balance, as detailed by Ostrowski, (2013).

Interpreting Results

In Scenario-A, I had made allowance within the enhanced purchase price, to the

possibility of refurbishing the building after the expiry of its current lease. This

does not remove the uncertainty of the building’s obsolescence and any future

vacancy issues, but it allows the investor in making an assessment of the

impact on his Target Return and in deciding whether it is acceptable, says

Kirkham, (2014). To give an alternate to the existing scenario, I have illustrated,

in Scenario-B below, considering a new debt finance, in the ratio of 65:35,

whereas 65% is the borrowing and 35% is the investor’s contribution. This

borrowing is considered to be secured against the IPMS 3 office building stated

in Scenario-A above. At the time of maturity of this loan, which is in five years’

time, there will still be another five years’ time remaining for the lease term to

expire, but this would not be of concern for the lender as there will not be any

time-lapse in re-letting, asserts Lavender, (2014).

Scenario B

Loan period 5 years

Sum advanced £2 835 000

Loan to value ratio 60%

Interest rate 5% pa Interest cover ratio Minimum × 1.5

(rent/interest)

Amortisation rate 2% pa of sum advanced

Even after allowing for a small downfall in the ‘Market Value’ of the property

during the loan term period, the probability of the borrower in not repaying the

loan remains very low as the ability of the borrower in meeting the finance

interest payments remains comfortable throughout the loan period, as per

Towey, (2013). Thus, despite a shortening of the unexpired term of lease, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

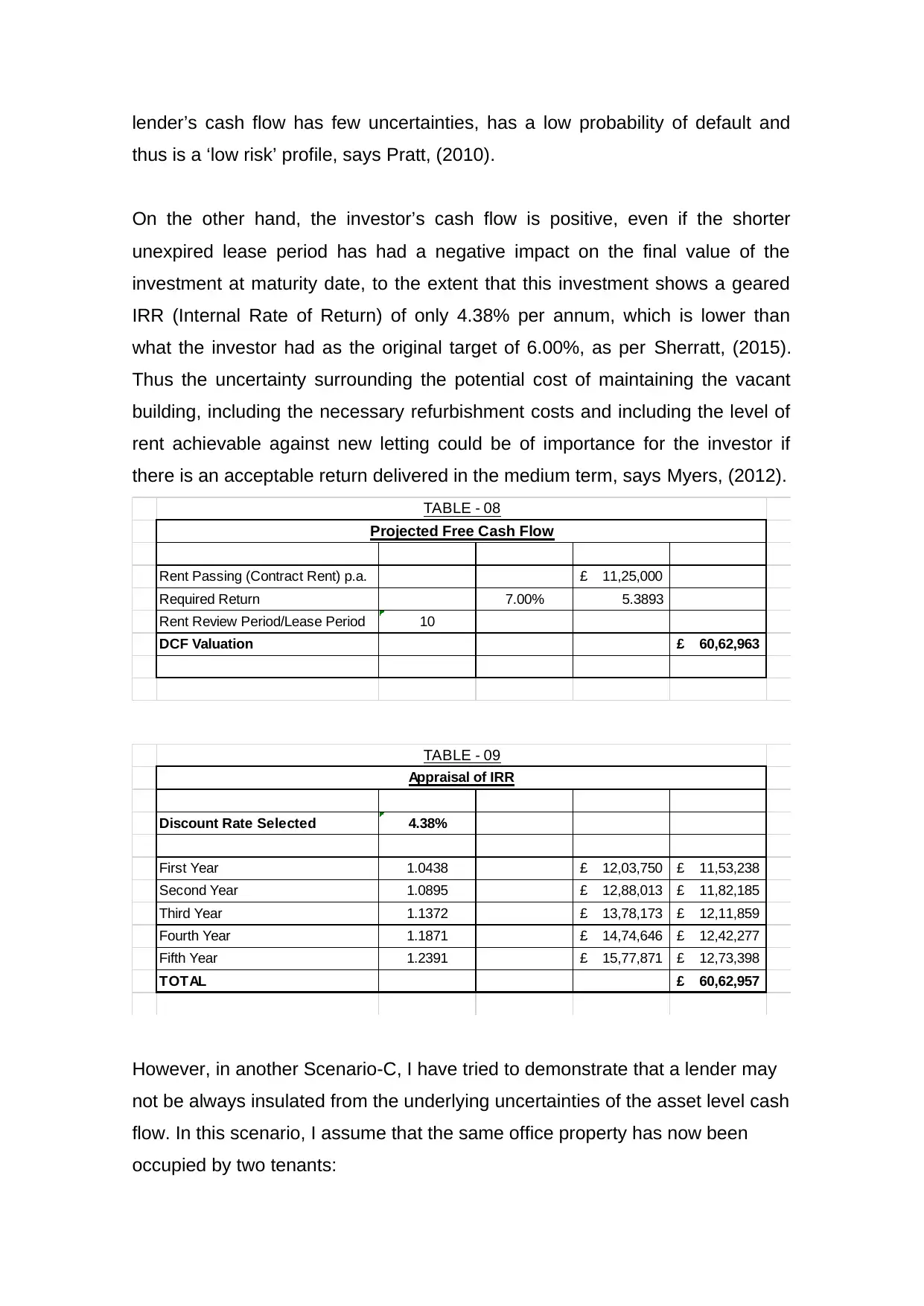

lender’s cash flow has few uncertainties, has a low probability of default and

thus is a ‘low risk’ profile, says Pratt, (2010).

On the other hand, the investor’s cash flow is positive, even if the shorter

unexpired lease period has had a negative impact on the final value of the

investment at maturity date, to the extent that this investment shows a geared

IRR (Internal Rate of Return) of only 4.38% per annum, which is lower than

what the investor had as the original target of 6.00%, as per Sherratt, (2015).

Thus the uncertainty surrounding the potential cost of maintaining the vacant

building, including the necessary refurbishment costs and including the level of

rent achievable against new letting could be of importance for the investor if

there is an acceptable return delivered in the medium term, says Myers, (2012).

Rent Passing (Contract Rent) p.a. 11,25,000£

Required Return 7.00% 5.3893

Rent Review Period/Lease Period 10

DCF Valuation 60,62,963£

Projected Free Cash Flow

TABLE - 08

Discount Rate Selected 4.38%

First Year 1.0438 12,03,750£ 11,53,238£

Second Year 1.0895 12,88,013£ 11,82,185£

Third Year 1.1372 13,78,173£ 12,11,859£

Fourth Year 1.1871 14,74,646£ 12,42,277£

Fifth Year 1.2391 15,77,871£ 12,73,398£

TOTAL 60,62,957£

Appraisal of IRR

TABLE - 09

However, in another Scenario-C, I have tried to demonstrate that a lender may

not be always insulated from the underlying uncertainties of the asset level cash

flow. In this scenario, I assume that the same office property has now been

occupied by two tenants:

thus is a ‘low risk’ profile, says Pratt, (2010).

On the other hand, the investor’s cash flow is positive, even if the shorter

unexpired lease period has had a negative impact on the final value of the

investment at maturity date, to the extent that this investment shows a geared

IRR (Internal Rate of Return) of only 4.38% per annum, which is lower than

what the investor had as the original target of 6.00%, as per Sherratt, (2015).

Thus the uncertainty surrounding the potential cost of maintaining the vacant

building, including the necessary refurbishment costs and including the level of

rent achievable against new letting could be of importance for the investor if

there is an acceptable return delivered in the medium term, says Myers, (2012).

Rent Passing (Contract Rent) p.a. 11,25,000£

Required Return 7.00% 5.3893

Rent Review Period/Lease Period 10

DCF Valuation 60,62,963£

Projected Free Cash Flow

TABLE - 08

Discount Rate Selected 4.38%

First Year 1.0438 12,03,750£ 11,53,238£

Second Year 1.0895 12,88,013£ 11,82,185£

Third Year 1.1372 13,78,173£ 12,11,859£

Fourth Year 1.1871 14,74,646£ 12,42,277£

Fifth Year 1.2391 15,77,871£ 12,73,398£

TOTAL 60,62,957£

Appraisal of IRR

TABLE - 09

However, in another Scenario-C, I have tried to demonstrate that a lender may

not be always insulated from the underlying uncertainties of the asset level cash

flow. In this scenario, I assume that the same office property has now been

occupied by two tenants:

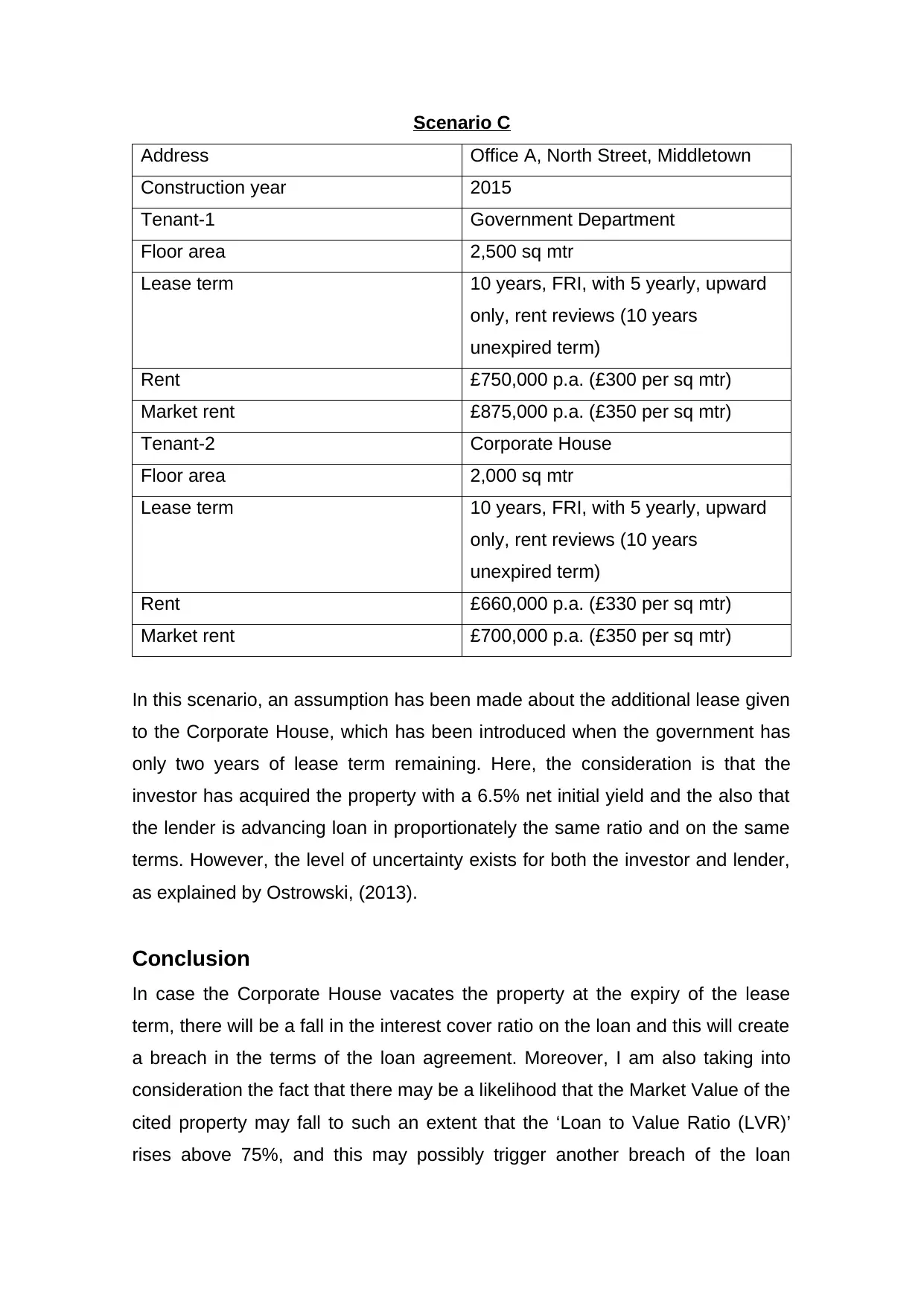

Scenario C

Address Office A, North Street, Middletown

Construction year 2015

Tenant-1 Government Department

Floor area 2,500 sq mtr

Lease term 10 years, FRI, with 5 yearly, upward

only, rent reviews (10 years

unexpired term)

Rent £750,000 p.a. (£300 per sq mtr)

Market rent £875,000 p.a. (£350 per sq mtr)

Tenant-2 Corporate House

Floor area 2,000 sq mtr

Lease term 10 years, FRI, with 5 yearly, upward

only, rent reviews (10 years

unexpired term)

Rent £660,000 p.a. (£330 per sq mtr)

Market rent £700,000 p.a. (£350 per sq mtr)

In this scenario, an assumption has been made about the additional lease given

to the Corporate House, which has been introduced when the government has

only two years of lease term remaining. Here, the consideration is that the

investor has acquired the property with a 6.5% net initial yield and the also that

the lender is advancing loan in proportionately the same ratio and on the same

terms. However, the level of uncertainty exists for both the investor and lender,

as explained by Ostrowski, (2013).

Conclusion

In case the Corporate House vacates the property at the expiry of the lease

term, there will be a fall in the interest cover ratio on the loan and this will create

a breach in the terms of the loan agreement. Moreover, I am also taking into

consideration the fact that there may be a likelihood that the Market Value of the

cited property may fall to such an extent that the ‘Loan to Value Ratio (LVR)’

rises above 75%, and this may possibly trigger another breach of the loan

Address Office A, North Street, Middletown

Construction year 2015

Tenant-1 Government Department

Floor area 2,500 sq mtr

Lease term 10 years, FRI, with 5 yearly, upward

only, rent reviews (10 years

unexpired term)

Rent £750,000 p.a. (£300 per sq mtr)

Market rent £875,000 p.a. (£350 per sq mtr)

Tenant-2 Corporate House

Floor area 2,000 sq mtr

Lease term 10 years, FRI, with 5 yearly, upward

only, rent reviews (10 years

unexpired term)

Rent £660,000 p.a. (£330 per sq mtr)

Market rent £700,000 p.a. (£350 per sq mtr)

In this scenario, an assumption has been made about the additional lease given

to the Corporate House, which has been introduced when the government has

only two years of lease term remaining. Here, the consideration is that the

investor has acquired the property with a 6.5% net initial yield and the also that

the lender is advancing loan in proportionately the same ratio and on the same

terms. However, the level of uncertainty exists for both the investor and lender,

as explained by Ostrowski, (2013).

Conclusion

In case the Corporate House vacates the property at the expiry of the lease

term, there will be a fall in the interest cover ratio on the loan and this will create

a breach in the terms of the loan agreement. Moreover, I am also taking into

consideration the fact that there may be a likelihood that the Market Value of the

cited property may fall to such an extent that the ‘Loan to Value Ratio (LVR)’

rises above 75%, and this may possibly trigger another breach of the loan

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

agreement. However, in my consideration, the biggest concern still will be

effects of refurbishment and vacancy costs, which can affect the results of the

cash outflow during the third year.

Due margin needs to be provided for the uncertainty of the length of vacancy

period, the extent of necessary refurbishment costs and also of the probability

of finding a good tenant at the required rent and lease terms, as explains Baum

& Baum, (2015). These are some of the important issues which both the

investor and the lender have to take into consideration at all times. In Scenario-

C, consideration has also to be taken for the refurbishing of the vacant offices

and re-let at £20 per sq mtr, after a void period of 12 months and another 9-

month rent-free period. Taking such a scenario into consideration, it is

imperative for the investor to achieve an IRR of around 8%, but this should be

only one among a number of possible outcomes, out of which some may be

less favourable.

LIST OF REFERENCES

Ashworth, A. and Perera, S. 2015 Cost Studies of Buildings, 6th ed. Routledge,

Oxon.

Baum, A. 2009 Commercial Real Estate Investment. Taylor & Francis, London.

effects of refurbishment and vacancy costs, which can affect the results of the

cash outflow during the third year.

Due margin needs to be provided for the uncertainty of the length of vacancy

period, the extent of necessary refurbishment costs and also of the probability

of finding a good tenant at the required rent and lease terms, as explains Baum

& Baum, (2015). These are some of the important issues which both the

investor and the lender have to take into consideration at all times. In Scenario-

C, consideration has also to be taken for the refurbishing of the vacant offices

and re-let at £20 per sq mtr, after a void period of 12 months and another 9-

month rent-free period. Taking such a scenario into consideration, it is

imperative for the investor to achieve an IRR of around 8%, but this should be

only one among a number of possible outcomes, out of which some may be

less favourable.

LIST OF REFERENCES

Ashworth, A. and Perera, S. 2015 Cost Studies of Buildings, 6th ed. Routledge,

Oxon.

Baum, A. 2009 Commercial Real Estate Investment. Taylor & Francis, London.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Baum, A. and Baum, Prof A. 2015 Real Estate Investment: A Strategic

Approach, 3rd ed. Routledge, Oxon.

Goodhart, C. and Hofmann, B. 2007 House Prices and the Macroeconomy:

Implications for Banking and Price Stability. OUP Oxford, Oxford.

Karadimitrio, N., Magalhaes, C. and Verhage, R. 2013 Planning, Risk, and

Property Development: Urban Regeneration in the England, France, and the

Netherlands. Routledge, Oxon.

Kirkham, R. 2014, Ferry and Brandon's Cost Planning of Buildings, 9th ed. John

Wiley & Sons, West Sussex.

Lavender, S. 2014, Management for the Construction Industry. Routledge,

Oxon.

Lester, A. 2013, Project Management, Planning and Control, 6th ed.

Butterworth-Heinemann, Oxon.

Myers, D. 2012 Economics and Property. Taylor & Francis, London.

Ostrowski, S.D.C. 2013, Estimating and Cost Planning Using the New Rules of

Measurement. John Wiley & Sons, West Sussex.

Pratt, D. 2010, Fundamentals of Construction Estimating, 3rd ed. Cengage

Learning, New York.

Robinson, H., Symonds, B., Gilbertson, B. and Ilozor, B. 2015, Design

Economics for the Built Environment: Impact of Sustainability on Project

Evaluation. John Wiley & Sons, West Sussex.

Sherratt, F. 2015, Introduction to Construction Management. Routledge, Oxon.

Taylor, J. 2008, Project Scheduling and Cost Control: Planning, Monitoring and

Controlling the Baseline. J. Ross Publishing, Florida.

Towey, D. 2013, Cost Management of Construction Projects. John Wiley &

Sons, West Sussex.

Approach, 3rd ed. Routledge, Oxon.

Goodhart, C. and Hofmann, B. 2007 House Prices and the Macroeconomy:

Implications for Banking and Price Stability. OUP Oxford, Oxford.

Karadimitrio, N., Magalhaes, C. and Verhage, R. 2013 Planning, Risk, and

Property Development: Urban Regeneration in the England, France, and the

Netherlands. Routledge, Oxon.

Kirkham, R. 2014, Ferry and Brandon's Cost Planning of Buildings, 9th ed. John

Wiley & Sons, West Sussex.

Lavender, S. 2014, Management for the Construction Industry. Routledge,

Oxon.

Lester, A. 2013, Project Management, Planning and Control, 6th ed.

Butterworth-Heinemann, Oxon.

Myers, D. 2012 Economics and Property. Taylor & Francis, London.

Ostrowski, S.D.C. 2013, Estimating and Cost Planning Using the New Rules of

Measurement. John Wiley & Sons, West Sussex.

Pratt, D. 2010, Fundamentals of Construction Estimating, 3rd ed. Cengage

Learning, New York.

Robinson, H., Symonds, B., Gilbertson, B. and Ilozor, B. 2015, Design

Economics for the Built Environment: Impact of Sustainability on Project

Evaluation. John Wiley & Sons, West Sussex.

Sherratt, F. 2015, Introduction to Construction Management. Routledge, Oxon.

Taylor, J. 2008, Project Scheduling and Cost Control: Planning, Monitoring and

Controlling the Baseline. J. Ross Publishing, Florida.

Towey, D. 2013, Cost Management of Construction Projects. John Wiley &

Sons, West Sussex.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.