Real Estate Valuations: Property Details, Lease Clauses, and Rental Value Determination

VerifiedAdded on 2023/06/10

|20

|5619

|101

AI Summary

This article provides an overview of real estate valuations, covering property details such as size and location, lease clauses such as subletting and repair obligations, and rental value determination. It is relevant for students studying real estate valuation courses in universities.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Real Estate Valuations 1

Real Estate Valuations

By

(Student’s Name)

Course Name:

Professor Name:

University Name:

Date of Submission:

Real Estate Valuations

By

(Student’s Name)

Course Name:

Professor Name:

University Name:

Date of Submission:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Real Estate Valuations 2

Property Details

Size

The estimated size of the property is approximately 298.174 square meters. The property mainly

divided into three main areas which include ground, first and basement. In essence, the ground

dimension mostly is given as 29.03m by 5.66m (164.31 meters square), first floor on the other

hand given as 13.72m by 5.66m (77.66 meters squares). Finally, the dimensions for the basement

are given as 9.93m by 5.66m (56.2038 meters square).

Location

This property is situated on the provisional market within the main shopping in the town street.

The location of this property in this area makes it possible for the dwellers to access the social

amenities more easily. The value of the rental unit concerning leasing is likely to rise as a result

of the proximity of the property to the main shopping. Thus, the rent of the leased property can

be beneficial and profitable to the tenant if he or she decided to lease the property to the third

party under the subletting clause (Unbehaun and Fuerst 2018 p.43).

Physical Characteristics

This property is situated within the town premises and has attracted many multiple retailers. This

is mainly depicted by the availability of street traders and the plan outline. Moreover, there is

ample parking space for vehicles. In fact, the car parking is located at approximately 300 meters

at the down end of Moss Street (Beracha, Hardin and Skiba, 2018 p.256).

Property Details

Size

The estimated size of the property is approximately 298.174 square meters. The property mainly

divided into three main areas which include ground, first and basement. In essence, the ground

dimension mostly is given as 29.03m by 5.66m (164.31 meters square), first floor on the other

hand given as 13.72m by 5.66m (77.66 meters squares). Finally, the dimensions for the basement

are given as 9.93m by 5.66m (56.2038 meters square).

Location

This property is situated on the provisional market within the main shopping in the town street.

The location of this property in this area makes it possible for the dwellers to access the social

amenities more easily. The value of the rental unit concerning leasing is likely to rise as a result

of the proximity of the property to the main shopping. Thus, the rent of the leased property can

be beneficial and profitable to the tenant if he or she decided to lease the property to the third

party under the subletting clause (Unbehaun and Fuerst 2018 p.43).

Physical Characteristics

This property is situated within the town premises and has attracted many multiple retailers. This

is mainly depicted by the availability of street traders and the plan outline. Moreover, there is

ample parking space for vehicles. In fact, the car parking is located at approximately 300 meters

at the down end of Moss Street (Beracha, Hardin and Skiba, 2018 p.256).

Real Estate Valuations 3

The total marking slots designed is about 250 slots. However, on the moss street, the available

space is set to accommodate approximately 200 cars. The main access point for the parking is

situated on the off Bridge Street.

Lease Major Clause

The leasing of commercial properties is grounded on the code of practice of 2002. This practice

implies that the lease terms at all times must be taken regarding the appropriately priced

recommendations. The recommendations at all times must adhere to either five or six alternative

lease terms. Appropriate price mainly refers to that price which is taken with the systematic

approach with the aim of ensuring that it takes into consideration the aspirations of the landlord

and the tenant (Duca and Ling 2018). Thus, in the occasion that it is biased in the mechanism of

price and it is leaning towards one party, and then there is a likelihood that it will interfere with

the other party as the price, on the other hand, will be inappropriate. The application of the code

of the practice of the commercial lease terms is minimal across the board. The leading cause of

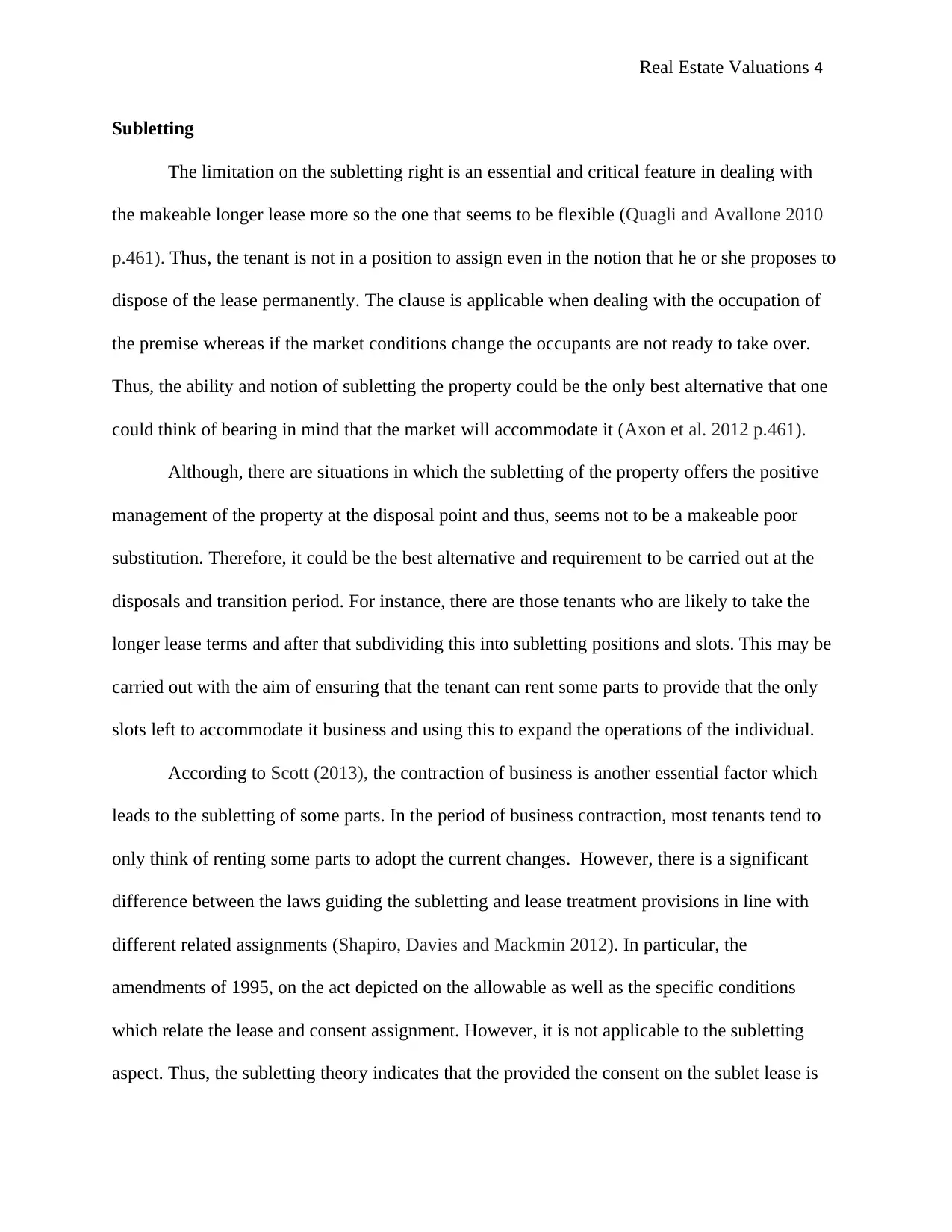

this is the inadequate knowledge which most parties have regarding this act. Thus, the graph

below shows the visible results taken from the sample survey carried out on the same

(McCollum and Milcheva 2018).

There are various clauses on leasing of the property, and these are discussed as follows

The total marking slots designed is about 250 slots. However, on the moss street, the available

space is set to accommodate approximately 200 cars. The main access point for the parking is

situated on the off Bridge Street.

Lease Major Clause

The leasing of commercial properties is grounded on the code of practice of 2002. This practice

implies that the lease terms at all times must be taken regarding the appropriately priced

recommendations. The recommendations at all times must adhere to either five or six alternative

lease terms. Appropriate price mainly refers to that price which is taken with the systematic

approach with the aim of ensuring that it takes into consideration the aspirations of the landlord

and the tenant (Duca and Ling 2018). Thus, in the occasion that it is biased in the mechanism of

price and it is leaning towards one party, and then there is a likelihood that it will interfere with

the other party as the price, on the other hand, will be inappropriate. The application of the code

of the practice of the commercial lease terms is minimal across the board. The leading cause of

this is the inadequate knowledge which most parties have regarding this act. Thus, the graph

below shows the visible results taken from the sample survey carried out on the same

(McCollum and Milcheva 2018).

There are various clauses on leasing of the property, and these are discussed as follows

Real Estate Valuations 4

Subletting

The limitation on the subletting right is an essential and critical feature in dealing with

the makeable longer lease more so the one that seems to be flexible (Quagli and Avallone 2010

p.461). Thus, the tenant is not in a position to assign even in the notion that he or she proposes to

dispose of the lease permanently. The clause is applicable when dealing with the occupation of

the premise whereas if the market conditions change the occupants are not ready to take over.

Thus, the ability and notion of subletting the property could be the only best alternative that one

could think of bearing in mind that the market will accommodate it (Axon et al. 2012 p.461).

Although, there are situations in which the subletting of the property offers the positive

management of the property at the disposal point and thus, seems not to be a makeable poor

substitution. Therefore, it could be the best alternative and requirement to be carried out at the

disposals and transition period. For instance, there are those tenants who are likely to take the

longer lease terms and after that subdividing this into subletting positions and slots. This may be

carried out with the aim of ensuring that the tenant can rent some parts to provide that the only

slots left to accommodate it business and using this to expand the operations of the individual.

According to Scott (2013), the contraction of business is another essential factor which

leads to the subletting of some parts. In the period of business contraction, most tenants tend to

only think of renting some parts to adopt the current changes. However, there is a significant

difference between the laws guiding the subletting and lease treatment provisions in line with

different related assignments (Shapiro, Davies and Mackmin 2012). In particular, the

amendments of 1995, on the act depicted on the allowable as well as the specific conditions

which relate the lease and consent assignment. However, it is not applicable to the subletting

aspect. Thus, the subletting theory indicates that the provided the consent on the sublet lease is

Subletting

The limitation on the subletting right is an essential and critical feature in dealing with

the makeable longer lease more so the one that seems to be flexible (Quagli and Avallone 2010

p.461). Thus, the tenant is not in a position to assign even in the notion that he or she proposes to

dispose of the lease permanently. The clause is applicable when dealing with the occupation of

the premise whereas if the market conditions change the occupants are not ready to take over.

Thus, the ability and notion of subletting the property could be the only best alternative that one

could think of bearing in mind that the market will accommodate it (Axon et al. 2012 p.461).

Although, there are situations in which the subletting of the property offers the positive

management of the property at the disposal point and thus, seems not to be a makeable poor

substitution. Therefore, it could be the best alternative and requirement to be carried out at the

disposals and transition period. For instance, there are those tenants who are likely to take the

longer lease terms and after that subdividing this into subletting positions and slots. This may be

carried out with the aim of ensuring that the tenant can rent some parts to provide that the only

slots left to accommodate it business and using this to expand the operations of the individual.

According to Scott (2013), the contraction of business is another essential factor which

leads to the subletting of some parts. In the period of business contraction, most tenants tend to

only think of renting some parts to adopt the current changes. However, there is a significant

difference between the laws guiding the subletting and lease treatment provisions in line with

different related assignments (Shapiro, Davies and Mackmin 2012). In particular, the

amendments of 1995, on the act depicted on the allowable as well as the specific conditions

which relate the lease and consent assignment. However, it is not applicable to the subletting

aspect. Thus, the subletting theory indicates that the provided the consent on the sublet lease is

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Real Estate Valuations 5

signed and agreed upon by both the landlord and the tenant it cannot be withdrawn. Thus, the

unreasonably withdraw of the subletting is unacceptable as per this clause. Conversely, most true

situations in the lease agreement and related subletting clause are often masked by this

amendment (Kok and Jennen 2012 p.489).

Other lease Provisions

Wyatt (2013) noted that the lease provisions and the lease length governing the ability of

tenants to exit the property is not the only essential ingredient and lease flexibility measure.

However, it is impossible and difficult to determine other parameters which can be used in

designing and developing relevant lease provisions which tenants regard as important.

The lease provisions mainly considered on the basis that these elements do not have any

constraints in dealing with the changing circumstances in business. However, any lease

provisions which impacts either directly or indirectly on the rent, as well as related other

outgoings, must at all times be considered and appraise decisively. Most successive governments

have only shifted their attention on the ratchet dominance upward system in line with the rent

review. In essence, the establishments in the enactment of the new Code of Practice have

significantly shown the extent of the pressure and depict it as instrumental (Nase, Berry and

Adair 2013 p.47).

Rental Value from Letter 1

Rental values mainly defined from the economic concept as the value which an individual may

add to obtain profit from the goods being traded or exchanged in the market. At all time the

rental amount is often classified as a fixed cost and is enormously alone in line with the trader'

ownership. Thus, it is defined as the fair value in terms of the market which a given property

tends to offer in the likely event that the property is leased on the rented out basis. This rental

signed and agreed upon by both the landlord and the tenant it cannot be withdrawn. Thus, the

unreasonably withdraw of the subletting is unacceptable as per this clause. Conversely, most true

situations in the lease agreement and related subletting clause are often masked by this

amendment (Kok and Jennen 2012 p.489).

Other lease Provisions

Wyatt (2013) noted that the lease provisions and the lease length governing the ability of

tenants to exit the property is not the only essential ingredient and lease flexibility measure.

However, it is impossible and difficult to determine other parameters which can be used in

designing and developing relevant lease provisions which tenants regard as important.

The lease provisions mainly considered on the basis that these elements do not have any

constraints in dealing with the changing circumstances in business. However, any lease

provisions which impacts either directly or indirectly on the rent, as well as related other

outgoings, must at all times be considered and appraise decisively. Most successive governments

have only shifted their attention on the ratchet dominance upward system in line with the rent

review. In essence, the establishments in the enactment of the new Code of Practice have

significantly shown the extent of the pressure and depict it as instrumental (Nase, Berry and

Adair 2013 p.47).

Rental Value from Letter 1

Rental values mainly defined from the economic concept as the value which an individual may

add to obtain profit from the goods being traded or exchanged in the market. At all time the

rental amount is often classified as a fixed cost and is enormously alone in line with the trader'

ownership. Thus, it is defined as the fair value in terms of the market which a given property

tends to offer in the likely event that the property is leased on the rented out basis. This rental

Real Estate Valuations 6

value tends to have various considerations which include the pay which one gives, occupancy

right, returns received for the property by either the landlord or the lessor (Reichardt et al. 2012

p.99).

Rental Value and Rates Determination

Jameel et al. (2013) indicate that the rental value and rates determination is part and

parcel of the lease document. It is essential for the landlord to consider the analogy and

established all the related facts about more decisively. Placing of the highest price possible in

line with the rent value is not recommended at all time. In essence, most issues which increase

such as the calls and the issues raised by the tenant as well as the complaints mainly arise due to

the increased rent. Thus, the pricing of the property needs to follow both the logic and

regulations governing strategy to be used in your area (Udoekanem 2012 p.13).

Rent Review Patter

This is an essential aspect in the valuation of the real estate value. The primary

considerations taken into account is a review period, lease length, user clause, type, repairs as

well as the proposed improvements. However, these factors are not constant and may have some

variation at the renewal time as well as the rental interpretation level in line with the rating

process. On the other hand, leasing of the property continues to raise various concerns more so in

the situations where the standard and long institutional leases are depicted to have dominated the

market. However, the leasing drafting is applied with the aim of ensuring that the rent is

determined at each level. The rent is grounded on the original terms of the overall lease and not

necessary for the unexpired term. Therefore, this notion shows that the landlords should expect

lower rents when dealing with the short terms. This argument has continued to raise various

concerns and debates whereby most people tend to point out that the use of longer and assumed

value tends to have various considerations which include the pay which one gives, occupancy

right, returns received for the property by either the landlord or the lessor (Reichardt et al. 2012

p.99).

Rental Value and Rates Determination

Jameel et al. (2013) indicate that the rental value and rates determination is part and

parcel of the lease document. It is essential for the landlord to consider the analogy and

established all the related facts about more decisively. Placing of the highest price possible in

line with the rent value is not recommended at all time. In essence, most issues which increase

such as the calls and the issues raised by the tenant as well as the complaints mainly arise due to

the increased rent. Thus, the pricing of the property needs to follow both the logic and

regulations governing strategy to be used in your area (Udoekanem 2012 p.13).

Rent Review Patter

This is an essential aspect in the valuation of the real estate value. The primary

considerations taken into account is a review period, lease length, user clause, type, repairs as

well as the proposed improvements. However, these factors are not constant and may have some

variation at the renewal time as well as the rental interpretation level in line with the rating

process. On the other hand, leasing of the property continues to raise various concerns more so in

the situations where the standard and long institutional leases are depicted to have dominated the

market. However, the leasing drafting is applied with the aim of ensuring that the rent is

determined at each level. The rent is grounded on the original terms of the overall lease and not

necessary for the unexpired term. Therefore, this notion shows that the landlords should expect

lower rents when dealing with the short terms. This argument has continued to raise various

concerns and debates whereby most people tend to point out that the use of longer and assumed

Real Estate Valuations 7

terms can lead to too long lease period and thereby attract low rents in return. By the virtue that

there is no proper channel for handling the absence of both the up and down rents as far the

current lease is concerned. Most people have left with no option but to go to the courts to seek

for the interpretation and pleas for the various questions regarding the review of both the down

and up a price in line with the rent (Udoekanem 2012 p.65).

Currently, there are no proper channels and mechanisms for controlling the rent reviews,

and this is extended to the commercial lease well. It is noted that most courts have not found it

significant and vital to monitor and ensure that there is a proper channel for controlling the rent

reviews in line with the various provisions. The argument has been to the extent to which the

regulation can be considered either reasonable or fair. Thus, the court has opted out more so in

the situations in which the requirements seem to be harshly regarding the operations. In essence,

most courts have avoided such discussions and ruling unless proper logistics and regulations are

enacted which have a definite and particular clause (Kim, Leung and Wagman 2017 p.309).

Conversely, Upward only rent review clauses tend to take a different analogy and

approach. This theory indicates that the estimated rent should not fall at the makeable highest

level and that the total estimate should not exceed the rent which is approximate in the course of

the lease period. In essence, the clause is based on the ratchet open market review form. It has to

reference the particular concerns and related issues from the government. Thus, this review is the

dominant lease act in the commercial market (Geoghegan, Kinsella and O’Donoghue 2017

p.392).

Moreover, the threshold is another essential review which is considered decisively in the rent

review pattern. This norm stipulates that the estimated rent in line with the provision can rise or

fall. In essence, it is expected that the rent can either move downwards or upwards as far as the

terms can lead to too long lease period and thereby attract low rents in return. By the virtue that

there is no proper channel for handling the absence of both the up and down rents as far the

current lease is concerned. Most people have left with no option but to go to the courts to seek

for the interpretation and pleas for the various questions regarding the review of both the down

and up a price in line with the rent (Udoekanem 2012 p.65).

Currently, there are no proper channels and mechanisms for controlling the rent reviews,

and this is extended to the commercial lease well. It is noted that most courts have not found it

significant and vital to monitor and ensure that there is a proper channel for controlling the rent

reviews in line with the various provisions. The argument has been to the extent to which the

regulation can be considered either reasonable or fair. Thus, the court has opted out more so in

the situations in which the requirements seem to be harshly regarding the operations. In essence,

most courts have avoided such discussions and ruling unless proper logistics and regulations are

enacted which have a definite and particular clause (Kim, Leung and Wagman 2017 p.309).

Conversely, Upward only rent review clauses tend to take a different analogy and

approach. This theory indicates that the estimated rent should not fall at the makeable highest

level and that the total estimate should not exceed the rent which is approximate in the course of

the lease period. In essence, the clause is based on the ratchet open market review form. It has to

reference the particular concerns and related issues from the government. Thus, this review is the

dominant lease act in the commercial market (Geoghegan, Kinsella and O’Donoghue 2017

p.392).

Moreover, the threshold is another essential review which is considered decisively in the rent

review pattern. This norm stipulates that the estimated rent in line with the provision can rise or

fall. In essence, it is expected that the rent can either move downwards or upwards as far as the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Real Estate Valuations 8

lease course is concerned but all points it should never be below the overall initial rent. Notably,

it is evidential that threshold form for the upward review differs only with the ratchet review in

the situations in which the lease has more than one rent review (Tian 2013).

Repairing Obligation Lease Term

The acts in most cases have obligated landlords to carry out repairs on their property in

line with the extended terms of the leasing the item. However, the situation seems to be relatively

different when dealing with the tenant who occupies the property for a period of fewer than

seven years. These tenants mainly adhere to tenant acts of 1985 as well as the landlord

agreements and contracts. Leasing period is the paramount and essential ingredient in

determining the landlord obligation in line with the property repair norms (Joshua Adegoke 2014

p.223). Conveyancing solicitors are obligated with the critical and vital task of ensuring that the

leaseholders at all times adhere to the rule of law and the lease used at all times have makeable

sufficient obligations regarding the repairs (Epple, Quintero and Sieg 2014 p.69).

On the other hand, the existence of the established rules and laws on the residential leases

and the related approaches is essential when dealing with the leasing and repairs of the property.

There are some laws on the lease obligations which offers enormous as well as a variety of

approaches for dealing with the repairing debts. This context is mainly defined as repairing the

convents. The following business regarding the leasing drafting is depicted to have been

evolutionary concept and meaning. In essence, the idea primarily depends on the nature and the

initial intended purpose of the rental unit. For instance, whether the rental unit was developed

concerning flats or whether the overall mansion needs to be separated into makeable apartments

(Simon et al. 2015 p.165).

lease course is concerned but all points it should never be below the overall initial rent. Notably,

it is evidential that threshold form for the upward review differs only with the ratchet review in

the situations in which the lease has more than one rent review (Tian 2013).

Repairing Obligation Lease Term

The acts in most cases have obligated landlords to carry out repairs on their property in

line with the extended terms of the leasing the item. However, the situation seems to be relatively

different when dealing with the tenant who occupies the property for a period of fewer than

seven years. These tenants mainly adhere to tenant acts of 1985 as well as the landlord

agreements and contracts. Leasing period is the paramount and essential ingredient in

determining the landlord obligation in line with the property repair norms (Joshua Adegoke 2014

p.223). Conveyancing solicitors are obligated with the critical and vital task of ensuring that the

leaseholders at all times adhere to the rule of law and the lease used at all times have makeable

sufficient obligations regarding the repairs (Epple, Quintero and Sieg 2014 p.69).

On the other hand, the existence of the established rules and laws on the residential leases

and the related approaches is essential when dealing with the leasing and repairs of the property.

There are some laws on the lease obligations which offers enormous as well as a variety of

approaches for dealing with the repairing debts. This context is mainly defined as repairing the

convents. The following business regarding the leasing drafting is depicted to have been

evolutionary concept and meaning. In essence, the idea primarily depends on the nature and the

initial intended purpose of the rental unit. For instance, whether the rental unit was developed

concerning flats or whether the overall mansion needs to be separated into makeable apartments

(Simon et al. 2015 p.165).

Real Estate Valuations 9

Preferably, it is essential to have an in-depth understanding and interpretation of the laws as this

form the cornerstone in the area being tacked. For instance, the obligation and legalization

regarding the leasing of the property in line with the overall repair do not mean that the landlord

must actualize the norm (Eppl et al. 2011 p240).

In the matters of laws and regulations, the court tends to take the argument that the lease

at all-time tends to have the overall agreement between the participant parties. Thus, the rules

tend to imply rarely in the situations in which the repairing obligation is involved unless

stipulated in the exceptional circumstances. Thus, the burden on the repair gives the tenants a

leeway if the landlord turned and failed to fulfill the obligated duty in line with the replacement.

In essence, the norm tends to provide most tenants some next and potential options. Thus, the

tenant has the freedom to seek for a plea from the court to grant him or her prayer of being given

specific performance regarding the damages as well as the injunctions ( Allen Klaiber, Salhofer

and Thompson p.710).

According to Napoli et al. (2017), specific performance refers to the act of issuing an

order to direct someone to do an imminent and precise action. For example, the tenants move to

various courts to seek and obtain laws which will address their respective landlords to carry out

the required repairs in their rental units. In the imposition regarding the norm tend to function as

a remedy in situations in which the lease obligation is depicted as entirely discretionary. Thus,

most claimants tend to view the analogy as not just seeking for anything but the makeable right

of the individuals. However, there is extended and the overall considerations which the court

tend to follow in giving such direction. For example, the court may turn down the specific

performance granting in situations in which the repair seems to be more complicated and thus,

will require more cautious elements. Concerning the arising damages, the court only award and

Preferably, it is essential to have an in-depth understanding and interpretation of the laws as this

form the cornerstone in the area being tacked. For instance, the obligation and legalization

regarding the leasing of the property in line with the overall repair do not mean that the landlord

must actualize the norm (Eppl et al. 2011 p240).

In the matters of laws and regulations, the court tends to take the argument that the lease

at all-time tends to have the overall agreement between the participant parties. Thus, the rules

tend to imply rarely in the situations in which the repairing obligation is involved unless

stipulated in the exceptional circumstances. Thus, the burden on the repair gives the tenants a

leeway if the landlord turned and failed to fulfill the obligated duty in line with the replacement.

In essence, the norm tends to provide most tenants some next and potential options. Thus, the

tenant has the freedom to seek for a plea from the court to grant him or her prayer of being given

specific performance regarding the damages as well as the injunctions ( Allen Klaiber, Salhofer

and Thompson p.710).

According to Napoli et al. (2017), specific performance refers to the act of issuing an

order to direct someone to do an imminent and precise action. For example, the tenants move to

various courts to seek and obtain laws which will address their respective landlords to carry out

the required repairs in their rental units. In the imposition regarding the norm tend to function as

a remedy in situations in which the lease obligation is depicted as entirely discretionary. Thus,

most claimants tend to view the analogy as not just seeking for anything but the makeable right

of the individuals. However, there is extended and the overall considerations which the court

tend to follow in giving such direction. For example, the court may turn down the specific

performance granting in situations in which the repair seems to be more complicated and thus,

will require more cautious elements. Concerning the arising damages, the court only award and

Real Estate Valuations 10

give the direction regarding the situation in line with the implementation cost repair (Bejol and

Livingstone 2018 ).

Transaction Evidence

The analysis is essential and vital in developing and establishing the net effective rent. This

analysis aims at determining the effective net rent, and this is carried out in line with the

incentive packages which are often incorporated in the overall specific transaction. In the

transaction evidence, two main approaches are used as the primary evaluation techniques. These

two methods include computation of devaluing of the net effective rent as well as using the

comparative method in establishing the market package. Some of the essential elements

considered in the market package include incentives and the headline rent. These elements are

discussed and agreed upon and after that adjusted to suit the transactions to depict the assumed

terms of the lease. Once, the net market package for the given premise is established, then the

overall effective rent is computed using either method one or the alternative method two above

(Bujol and Livingstone 2018). However, the computation of the data is based on some guidelines

and principles. These guidelines and principles incorporated in this study include

The applying the incentives treatment approaches in most cases do not depend on its nature.

Conversely, the mode used by the client to pay the rent may have some impacts on it. These

impacts include tax implication and accounting terms (Mangioni 2014).

In some cases, the evaluator needs to check and determine whether or not it is essential to

exclude or include the rent-free period in the computation of the net effective rent. It is during

this rent-free period that various operations relating to the fitting out works are carried out. Both

the renewals of lease legislation as well as the associated cases are applied when dealing with the

elements to be included and excluded from the project. Preferably, it is important to note that the

give the direction regarding the situation in line with the implementation cost repair (Bejol and

Livingstone 2018 ).

Transaction Evidence

The analysis is essential and vital in developing and establishing the net effective rent. This

analysis aims at determining the effective net rent, and this is carried out in line with the

incentive packages which are often incorporated in the overall specific transaction. In the

transaction evidence, two main approaches are used as the primary evaluation techniques. These

two methods include computation of devaluing of the net effective rent as well as using the

comparative method in establishing the market package. Some of the essential elements

considered in the market package include incentives and the headline rent. These elements are

discussed and agreed upon and after that adjusted to suit the transactions to depict the assumed

terms of the lease. Once, the net market package for the given premise is established, then the

overall effective rent is computed using either method one or the alternative method two above

(Bujol and Livingstone 2018). However, the computation of the data is based on some guidelines

and principles. These guidelines and principles incorporated in this study include

The applying the incentives treatment approaches in most cases do not depend on its nature.

Conversely, the mode used by the client to pay the rent may have some impacts on it. These

impacts include tax implication and accounting terms (Mangioni 2014).

In some cases, the evaluator needs to check and determine whether or not it is essential to

exclude or include the rent-free period in the computation of the net effective rent. It is during

this rent-free period that various operations relating to the fitting out works are carried out. Both

the renewals of lease legislation as well as the associated cases are applied when dealing with the

elements to be included and excluded from the project. Preferably, it is important to note that the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Real Estate Valuations 11

act in most cases is silent on the application of the fitting out and the related assumptions in line

with the rental value definition (Rigi and Prey 2015 p.399).

Notably, considerations must be taken when dealing with the rent case reviews, and thus, the

lease wording in the context is essential and need to be evaluated and checked carefully.

However, there two fundamental approaches which can be used and utilized in dealing with this

element. The first approach used in the process estimates that there is the likelihood that the

tenant will receive a monopoly period in which both the fitting-out period and the rent-free

period will be equal. This analogy is based on the net effective rent deal' and grounded under the

questionable assumption. On the other hand, the second alternative approach is that the fit-out

time comes before the lease term commencement time (Henneberry and Mouzakis 2014 p.546).

Valuation Basis

Market Valuation

Market value is defined as the estimated amount for a given liability or asset at which it can be

exchanged between the two parties. The parties which are often involved in the exchange process

include the willing buyer and the willing seller. The process has three critical features in line

with the parties these include prudently, compulsion as well as knowledgeably acts from the two

parties involved (Caballero, Farhi, and p.618).

Assumptions in Market Valuation

There are various assumptions which one needs to adhere to consider in tackling the market

valuation, and some of these assumptions include

i. The transfer of the property will only take places when there no possession or there is a

vacancy.

act in most cases is silent on the application of the fitting out and the related assumptions in line

with the rental value definition (Rigi and Prey 2015 p.399).

Notably, considerations must be taken when dealing with the rent case reviews, and thus, the

lease wording in the context is essential and need to be evaluated and checked carefully.

However, there two fundamental approaches which can be used and utilized in dealing with this

element. The first approach used in the process estimates that there is the likelihood that the

tenant will receive a monopoly period in which both the fitting-out period and the rent-free

period will be equal. This analogy is based on the net effective rent deal' and grounded under the

questionable assumption. On the other hand, the second alternative approach is that the fit-out

time comes before the lease term commencement time (Henneberry and Mouzakis 2014 p.546).

Valuation Basis

Market Valuation

Market value is defined as the estimated amount for a given liability or asset at which it can be

exchanged between the two parties. The parties which are often involved in the exchange process

include the willing buyer and the willing seller. The process has three critical features in line

with the parties these include prudently, compulsion as well as knowledgeably acts from the two

parties involved (Caballero, Farhi, and p.618).

Assumptions in Market Valuation

There are various assumptions which one needs to adhere to consider in tackling the market

valuation, and some of these assumptions include

i. The transfer of the property will only take places when there no possession or there is a

vacancy.

Real Estate Valuations 12

ii. All relevant permissions and documents should be available. These include statutory

approvals, permits, alterations and extension plan documents. Thus, the valuer needs not

to demarcate and inquiries into the makeable town plan. It is essential under this slot to

identify any significant and recent alterations as well as extensions to alert the legal

adviser in case he or she wants to make any inquiries regarding the property. Although

the valuer in most cases does not have to search and source for the statutory notices, it

will be necessary for the legal adviser should ask any relevant questions that he or she

might come across during the study

Tenant on Rent Review

It is mainly carried out with the aim of ensuring that the current market level and the

commercial rents are approximately equivalent. This is often carried out periodically, and it is

actualized from the review date. However, the review of rents in most cases takes place with

reference the intervals which have been agreed upon by the parties involved and referenced from

the commercial lease clause of the rental review. In the United Kingdom, the rental survey is

conducted at an interval of three to about five years. However, recent research has shown that the

frequency of the makeable leasing length has continued to shorten.

Traditionally, the United Kingdom offered a commercial lease for at 20 years and beyond.

Currently, the shorter terms in line with the contracts are manifested in the current, and this

ranges from 10 years to about 15 years and the main event between tenants and landlords. The

critical issues to evaluate in dealing with the rent review include the place, review method, the

disregards and the assumptions made as far as the premises valuation is concerned. Furthermore,

it is essential to consider the reasons and logic for reviewing the rent, the stipulated and applied

ii. All relevant permissions and documents should be available. These include statutory

approvals, permits, alterations and extension plan documents. Thus, the valuer needs not

to demarcate and inquiries into the makeable town plan. It is essential under this slot to

identify any significant and recent alterations as well as extensions to alert the legal

adviser in case he or she wants to make any inquiries regarding the property. Although

the valuer in most cases does not have to search and source for the statutory notices, it

will be necessary for the legal adviser should ask any relevant questions that he or she

might come across during the study

Tenant on Rent Review

It is mainly carried out with the aim of ensuring that the current market level and the

commercial rents are approximately equivalent. This is often carried out periodically, and it is

actualized from the review date. However, the review of rents in most cases takes place with

reference the intervals which have been agreed upon by the parties involved and referenced from

the commercial lease clause of the rental review. In the United Kingdom, the rental survey is

conducted at an interval of three to about five years. However, recent research has shown that the

frequency of the makeable leasing length has continued to shorten.

Traditionally, the United Kingdom offered a commercial lease for at 20 years and beyond.

Currently, the shorter terms in line with the contracts are manifested in the current, and this

ranges from 10 years to about 15 years and the main event between tenants and landlords. The

critical issues to evaluate in dealing with the rent review include the place, review method, the

disregards and the assumptions made as far as the premises valuation is concerned. Furthermore,

it is essential to consider the reasons and logic for reviewing the rent, the stipulated and applied

Real Estate Valuations 13

procedures as well as the provisions which were followed in evaluating the rent and the

emerging disputes (Cieleback 2017).

Furthermore, the provisions which will be applied in the process mainly based on the

leasing codes and the industry-standard in line with the overall procedures for conducting the

business premises in Wales and England being that this property is located in the United

Kingdom. The striking techniques applied in the review of the rent for the commercial lease in

the open market revaluation method (Zhao and Webster 2011).

Thus, the tenant should take keen note on this and apply it immensely. In the event that

there is arising dispute, then it will be advisable for both the tenant and the landlord to depict and

refer to the rent review clause (Fuerst and McAllister 2011).

In essence, this will help them by outlining the stipulated procedure for handling the issue

via the third party. This is important as poorly analyzed and conducted reviews on the makeable

rent can lead to the stalemate, financial losses as well as the permanent lease termination. Thus,

it is essential for the tenant and the landlord to involve a chartered valuation surveyor to help

them in reviewing the rent. This is essential as the vast knowledge which the individual will

assist in curbing the emerging issues between the tenant and the landlord (Wiley et al. 2010

p.243).

Although there are various laws and clauses which depicts and explains the approaches

which the involved parties need to follow, it is often advisable for the parties to have a

consultative framework and agree on the rent review. All, considerations and the reasons for

reviewing rent should be stipulated out by the tenant as per the previous agreement which the

two parties signed. The current market value should be applied, and therefore the rent reviewed

should not be too high. Consultation of the third party should be the least and the last option,

procedures as well as the provisions which were followed in evaluating the rent and the

emerging disputes (Cieleback 2017).

Furthermore, the provisions which will be applied in the process mainly based on the

leasing codes and the industry-standard in line with the overall procedures for conducting the

business premises in Wales and England being that this property is located in the United

Kingdom. The striking techniques applied in the review of the rent for the commercial lease in

the open market revaluation method (Zhao and Webster 2011).

Thus, the tenant should take keen note on this and apply it immensely. In the event that

there is arising dispute, then it will be advisable for both the tenant and the landlord to depict and

refer to the rent review clause (Fuerst and McAllister 2011).

In essence, this will help them by outlining the stipulated procedure for handling the issue

via the third party. This is important as poorly analyzed and conducted reviews on the makeable

rent can lead to the stalemate, financial losses as well as the permanent lease termination. Thus,

it is essential for the tenant and the landlord to involve a chartered valuation surveyor to help

them in reviewing the rent. This is essential as the vast knowledge which the individual will

assist in curbing the emerging issues between the tenant and the landlord (Wiley et al. 2010

p.243).

Although there are various laws and clauses which depicts and explains the approaches

which the involved parties need to follow, it is often advisable for the parties to have a

consultative framework and agree on the rent review. All, considerations and the reasons for

reviewing rent should be stipulated out by the tenant as per the previous agreement which the

two parties signed. The current market value should be applied, and therefore the rent reviewed

should not be too high. Consultation of the third party should be the least and the last option,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Real Estate Valuations 14

however, both parties that are the tenant and the landlord must refer to the clauses as the

guideline framework (Jefferies 2010 p.435).

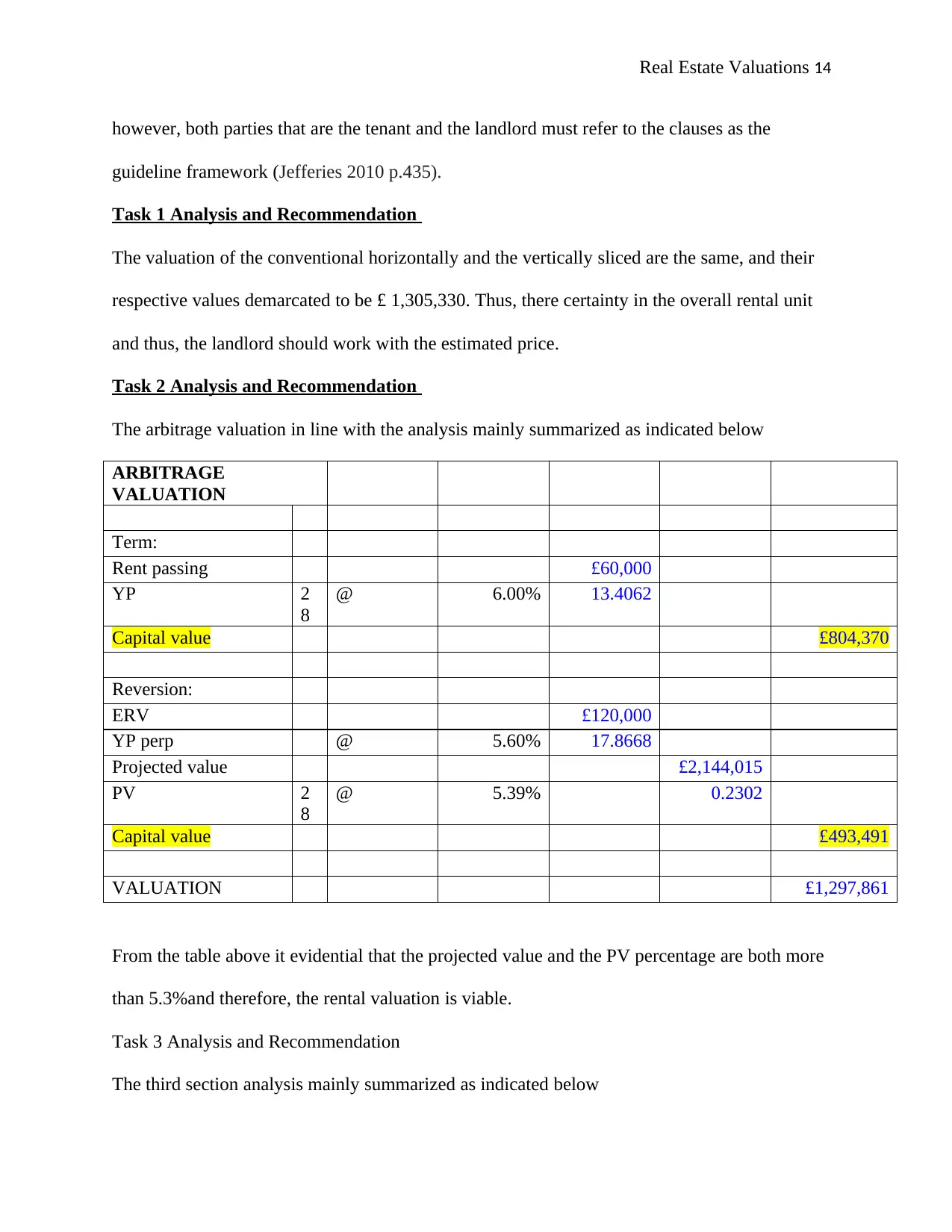

Task 1 Analysis and Recommendation

The valuation of the conventional horizontally and the vertically sliced are the same, and their

respective values demarcated to be £ 1,305,330. Thus, there certainty in the overall rental unit

and thus, the landlord should work with the estimated price.

Task 2 Analysis and Recommendation

The arbitrage valuation in line with the analysis mainly summarized as indicated below

ARBITRAGE

VALUATION

Term:

Rent passing £60,000

YP 2

8

@ 6.00% 13.4062

Capital value £804,370

Reversion:

ERV £120,000

YP perp @ 5.60% 17.8668

Projected value £2,144,015

PV 2

8

@ 5.39% 0.2302

Capital value £493,491

VALUATION £1,297,861

From the table above it evidential that the projected value and the PV percentage are both more

than 5.3%and therefore, the rental valuation is viable.

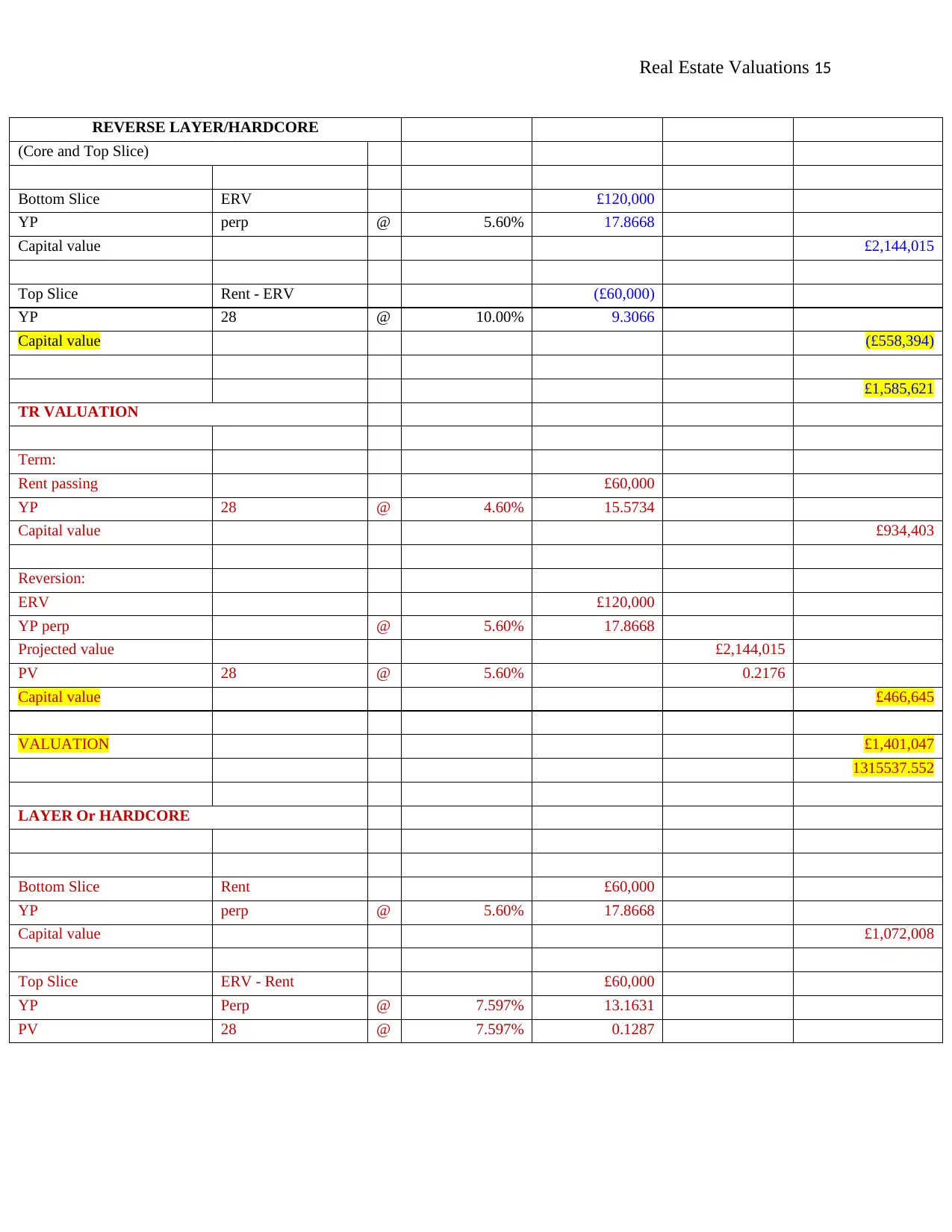

Task 3 Analysis and Recommendation

The third section analysis mainly summarized as indicated below

however, both parties that are the tenant and the landlord must refer to the clauses as the

guideline framework (Jefferies 2010 p.435).

Task 1 Analysis and Recommendation

The valuation of the conventional horizontally and the vertically sliced are the same, and their

respective values demarcated to be £ 1,305,330. Thus, there certainty in the overall rental unit

and thus, the landlord should work with the estimated price.

Task 2 Analysis and Recommendation

The arbitrage valuation in line with the analysis mainly summarized as indicated below

ARBITRAGE

VALUATION

Term:

Rent passing £60,000

YP 2

8

@ 6.00% 13.4062

Capital value £804,370

Reversion:

ERV £120,000

YP perp @ 5.60% 17.8668

Projected value £2,144,015

PV 2

8

@ 5.39% 0.2302

Capital value £493,491

VALUATION £1,297,861

From the table above it evidential that the projected value and the PV percentage are both more

than 5.3%and therefore, the rental valuation is viable.

Task 3 Analysis and Recommendation

The third section analysis mainly summarized as indicated below

Real Estate Valuations 15

REVERSE LAYER/HARDCORE

(Core and Top Slice)

Bottom Slice ERV £120,000

YP perp @ 5.60% 17.8668

Capital value £2,144,015

Top Slice Rent - ERV (£60,000)

YP 28 @ 10.00% 9.3066

Capital value (£558,394)

£1,585,621

TR VALUATION

Term:

Rent passing £60,000

YP 28 @ 4.60% 15.5734

Capital value £934,403

Reversion:

ERV £120,000

YP perp @ 5.60% 17.8668

Projected value £2,144,015

PV 28 @ 5.60% 0.2176

Capital value £466,645

VALUATION £1,401,047

1315537.552

LAYER Or HARDCORE

Bottom Slice Rent £60,000

YP perp @ 5.60% 17.8668

Capital value £1,072,008

Top Slice ERV - Rent £60,000

YP Perp @ 7.597% 13.1631

PV 28 @ 7.597% 0.1287

REVERSE LAYER/HARDCORE

(Core and Top Slice)

Bottom Slice ERV £120,000

YP perp @ 5.60% 17.8668

Capital value £2,144,015

Top Slice Rent - ERV (£60,000)

YP 28 @ 10.00% 9.3066

Capital value (£558,394)

£1,585,621

TR VALUATION

Term:

Rent passing £60,000

YP 28 @ 4.60% 15.5734

Capital value £934,403

Reversion:

ERV £120,000

YP perp @ 5.60% 17.8668

Projected value £2,144,015

PV 28 @ 5.60% 0.2176

Capital value £466,645

VALUATION £1,401,047

1315537.552

LAYER Or HARDCORE

Bottom Slice Rent £60,000

YP perp @ 5.60% 17.8668

Capital value £1,072,008

Top Slice ERV - Rent £60,000

YP Perp @ 7.597% 13.1631

PV 28 @ 7.597% 0.1287

Real Estate Valuations 16

Capital value £101,650

VALUATION £1,173,658

From the below above, it is clear that the TR valuation mainly established to be €131,557.552w

whereas the hardcore value depicted as € 1173658. This establishment affirms that the rental

premise is viable and should be leased.

Figure Summary

The three analysis gives the diagram below analysis for the overall rental unit valuation.

Capital value £101,650

VALUATION £1,173,658

From the below above, it is clear that the TR valuation mainly established to be €131,557.552w

whereas the hardcore value depicted as € 1173658. This establishment affirms that the rental

premise is viable and should be leased.

Figure Summary

The three analysis gives the diagram below analysis for the overall rental unit valuation.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Real Estate Valuations 17

Reference

Axon, C.J., Bright, S.J., Dixon, T.J., Janda, K.B. and Kolokotroni, M., 2012. Building

communities: reducing energy use in tenanted commercial property. Building Research &

Information, 40(4), pp.461-472.

Bujol, P. and Livingstone, N., 2018. Revisiting currency swaps: hedging real estate investments

in global city markets. Journal of Property Investment & Finance, 36(2), pp.191-209.

Beracha, E., Hardin, W.G. and Skiba, H.M., 2018. Real Estate Market Segmentation: Hotels as

Exemplar. The Journal of Real Estate Finance and Economics, 56(2), pp.252-273.

Caballero, R.J., Farhi, E., and Gourinchas, P.O., 2017. Rents, technical change, and risk premia

accounting for secular trends in interest rates, returns on capital, earnings yields, and factor

shares. American Economic Review, 107(5), pp.614-20.

Cieleback, M., 2017. Development of residential property. In Understanding German Real

Estate Markets (pp. 353-369). Springer, Cham.

Duca, J.V. and Ling, D.C., 2018. The other (commercial) real estate boom and bust: the effects

of risk premia and regulatory capital arbitrage. Journal of Banking & Finance.

Epple, D., Quintero, L. and Sieg, H., 2014. A new approach to estimating hedonic pricing

functions for metropolitan housing markets. FRB of Cleveland Working Paper No. 1516.

Fuerst, F. and McAllister, P., 2011. Green noise or green value? Measuring the effects of

environmental certification on office values. Real estate economics, 39(1), pp.45-69.

Geoghegan, C., Kinsella, A. and O’Donoghue, C., 2017. Institutional drivers of land mobility:

The impact of CAP rules and tax policy on land mobility incentives in Ireland. Agricultural

Finance Review, 77(3), pp.376-392.

Reference

Axon, C.J., Bright, S.J., Dixon, T.J., Janda, K.B. and Kolokotroni, M., 2012. Building

communities: reducing energy use in tenanted commercial property. Building Research &

Information, 40(4), pp.461-472.

Bujol, P. and Livingstone, N., 2018. Revisiting currency swaps: hedging real estate investments

in global city markets. Journal of Property Investment & Finance, 36(2), pp.191-209.

Beracha, E., Hardin, W.G. and Skiba, H.M., 2018. Real Estate Market Segmentation: Hotels as

Exemplar. The Journal of Real Estate Finance and Economics, 56(2), pp.252-273.

Caballero, R.J., Farhi, E., and Gourinchas, P.O., 2017. Rents, technical change, and risk premia

accounting for secular trends in interest rates, returns on capital, earnings yields, and factor

shares. American Economic Review, 107(5), pp.614-20.

Cieleback, M., 2017. Development of residential property. In Understanding German Real

Estate Markets (pp. 353-369). Springer, Cham.

Duca, J.V. and Ling, D.C., 2018. The other (commercial) real estate boom and bust: the effects

of risk premia and regulatory capital arbitrage. Journal of Banking & Finance.

Epple, D., Quintero, L. and Sieg, H., 2014. A new approach to estimating hedonic pricing

functions for metropolitan housing markets. FRB of Cleveland Working Paper No. 1516.

Fuerst, F. and McAllister, P., 2011. Green noise or green value? Measuring the effects of

environmental certification on office values. Real estate economics, 39(1), pp.45-69.

Geoghegan, C., Kinsella, A. and O’Donoghue, C., 2017. Institutional drivers of land mobility:

The impact of CAP rules and tax policy on land mobility incentives in Ireland. Agricultural

Finance Review, 77(3), pp.376-392.

Real Estate Valuations 18

Henneberry, J. and Mouzakis, F., 2014. Familiarity and the determination of yields for regional

office property investments in the UK. Regional Studies, 48(3), pp.530-546.

Jameel, A., Fung, Y.S., Laxson, J., and Stabler, B., 2013. Shared vehicle rental system including

vehicle availability determination. U.S. Patent Application 13/482,434.

Jefferies, R., 2010. Real value valuation for property in the 21st century?–A comparison of

conventional and real value models. Pacific Rim Property Research Journal, 16(4), pp.435-457.

Joshua Adegoke, O., 2014. Critical factors determining rental value of residential property in

Ibadan metropolis, Nigeria. Property Management, 32(3), pp.224-240.

Kim, J.H., Leung, T.C. and Wagman, L., 2017. Can restricting property use be value enhancing?

Evidence from short-term rental regulation. The Journal of Law and Economics, 60(2), pp.309-

334.

Kok, N. and Jennen, M., 2012. The impact of energy labels and accessibility on office

rents. Energy Policy, 46, pp.489-497.

Mangioni, V., 2014. Defining the basis of value in land value tax. In 20th Annual Pacific Rim

Real Estate Society Conference. Pacific Rim Real Estate Society.

McCollum, M. and Milcheva, S., 2018. Multifamily Rental Housing and Naturally Occurring

Affordability-The Investor Perspective.

Napoli, G., Giuffrida, S., Trovato, M.R. and Valenti, A., 2017. Cap rate as the interpretative

variable of the urban real estate capital asset: a comparison of different sub-market definitions in

Palermo, Italy. Buildings, 7(3), p.80.

Nase, I., Berry, J. and Adair, A., 2013. Real estate value and quality design in commercial office

properties. Journal of European Real Estate Research, 6(1), pp.48-62.

Henneberry, J. and Mouzakis, F., 2014. Familiarity and the determination of yields for regional

office property investments in the UK. Regional Studies, 48(3), pp.530-546.

Jameel, A., Fung, Y.S., Laxson, J., and Stabler, B., 2013. Shared vehicle rental system including

vehicle availability determination. U.S. Patent Application 13/482,434.

Jefferies, R., 2010. Real value valuation for property in the 21st century?–A comparison of

conventional and real value models. Pacific Rim Property Research Journal, 16(4), pp.435-457.

Joshua Adegoke, O., 2014. Critical factors determining rental value of residential property in

Ibadan metropolis, Nigeria. Property Management, 32(3), pp.224-240.

Kim, J.H., Leung, T.C. and Wagman, L., 2017. Can restricting property use be value enhancing?

Evidence from short-term rental regulation. The Journal of Law and Economics, 60(2), pp.309-

334.

Kok, N. and Jennen, M., 2012. The impact of energy labels and accessibility on office

rents. Energy Policy, 46, pp.489-497.

Mangioni, V., 2014. Defining the basis of value in land value tax. In 20th Annual Pacific Rim

Real Estate Society Conference. Pacific Rim Real Estate Society.

McCollum, M. and Milcheva, S., 2018. Multifamily Rental Housing and Naturally Occurring

Affordability-The Investor Perspective.

Napoli, G., Giuffrida, S., Trovato, M.R. and Valenti, A., 2017. Cap rate as the interpretative

variable of the urban real estate capital asset: a comparison of different sub-market definitions in

Palermo, Italy. Buildings, 7(3), p.80.

Nase, I., Berry, J. and Adair, A., 2013. Real estate value and quality design in commercial office

properties. Journal of European Real Estate Research, 6(1), pp.48-62.

Real Estate Valuations 19

Quagli, A. and Avallone, F., 2010. Fair value or cost model? Drivers of choice for IAS 40 in the

real estate industry. European Accounting Review, 19(3), pp.461-493.

Reichardt, A., Fuerst, F., Rottke, N. and Zietz, J., 2012. Sustainable building certification and the

rent premium: a panel data approach. Journal of Real Estate Research, 34(1), pp.99-126.

Rigi, J. and Prey, R., 2015. Value, rent, and the political economy of social media. The

Information Society, 31(5), pp.392-406.

Scott, P., 2013. The Property Masters: A history of the British commercial property sector.

Taylor & Francis.

Shapiro, E., Davies, K. and Mackmin, D., 2012. Modern methods of valuation. Estates Gazette.

Simon, Z.Z., Achsani, N.A., Manurung, A.H. and Sembel, R., 2015. The Determinants of Rental

Rates and Selling Prices of Office Spaces in Jakarta: A Macroeconometric Model Using VECM

Approach. International Journal of Economics and Finance, 7(3), p.165.

Tian, C.Y., 2013. Are Capitalization Rates Really Constant within Housing Markets?.

Udoekanem, N.B., 2012. The Relevance of Contemporary Valuation Techniques in the

Determination of Buy-Out Value of Leasehold Properties in Uyo, Nigeria. Built

Environment, 9(1), pp.13-26.

Unbehaun, F. and Fuerst, F., 2018. Cap rates and risk: a spatial analysis of commercial real

estate. Studies in Economics and Finance, 35(1), pp.25-43.

Wiley, J.A., Benefield, J.D. and Johnson, K.H., 2010. Green design and the market for

commercial office space. The Journal of Real Estate Finance and Economics, 41(2), pp.228-243.

Wyatt, P., 2013. Property valuation. John Wiley & Sons.

Zhao, Y. and Webster, C., 2011. Land dispossession and enrichment in China’s suburban

villages. Urban Studies, 48(3), pp.529-551.

Quagli, A. and Avallone, F., 2010. Fair value or cost model? Drivers of choice for IAS 40 in the

real estate industry. European Accounting Review, 19(3), pp.461-493.

Reichardt, A., Fuerst, F., Rottke, N. and Zietz, J., 2012. Sustainable building certification and the

rent premium: a panel data approach. Journal of Real Estate Research, 34(1), pp.99-126.

Rigi, J. and Prey, R., 2015. Value, rent, and the political economy of social media. The

Information Society, 31(5), pp.392-406.

Scott, P., 2013. The Property Masters: A history of the British commercial property sector.

Taylor & Francis.

Shapiro, E., Davies, K. and Mackmin, D., 2012. Modern methods of valuation. Estates Gazette.

Simon, Z.Z., Achsani, N.A., Manurung, A.H. and Sembel, R., 2015. The Determinants of Rental

Rates and Selling Prices of Office Spaces in Jakarta: A Macroeconometric Model Using VECM

Approach. International Journal of Economics and Finance, 7(3), p.165.

Tian, C.Y., 2013. Are Capitalization Rates Really Constant within Housing Markets?.

Udoekanem, N.B., 2012. The Relevance of Contemporary Valuation Techniques in the

Determination of Buy-Out Value of Leasehold Properties in Uyo, Nigeria. Built

Environment, 9(1), pp.13-26.

Unbehaun, F. and Fuerst, F., 2018. Cap rates and risk: a spatial analysis of commercial real

estate. Studies in Economics and Finance, 35(1), pp.25-43.

Wiley, J.A., Benefield, J.D. and Johnson, K.H., 2010. Green design and the market for

commercial office space. The Journal of Real Estate Finance and Economics, 41(2), pp.228-243.

Wyatt, P., 2013. Property valuation. John Wiley & Sons.

Zhao, Y. and Webster, C., 2011. Land dispossession and enrichment in China’s suburban

villages. Urban Studies, 48(3), pp.529-551.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Real Estate Valuations 20

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.