Receivable Management - Analysis of Debtor's Management Strategy

VerifiedAdded on 2023/05/29

|8

|1884

|419

AI Summary

The assessment aims at analyzing the debtor’s management strategy of Sooner Pharmaceuticals to forecast the revenue of the business. It includes account receivable balance, uncollected balances, quarterly costs, and ageing schedule.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: RECEIVABLE MANAGEMENT

RECEIVABLE MANAGEMENT

Name of the Student:

Name of the University:

Author’s Note

RECEIVABLE MANAGEMENT

Name of the Student:

Name of the University:

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

RECEIVABLE MANAGEMENT

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Account Receivable Balance.......................................................................................................2

Uncollected Balances of Account Receivables...........................................................................4

Quarterly Costs of the Business...................................................................................................4

Ageing Schedule..........................................................................................................................5

Reference.........................................................................................................................................7

RECEIVABLE MANAGEMENT

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Account Receivable Balance.......................................................................................................2

Uncollected Balances of Account Receivables...........................................................................4

Quarterly Costs of the Business...................................................................................................4

Ageing Schedule..........................................................................................................................5

Reference.........................................................................................................................................7

2

RECEIVABLE MANAGEMENT

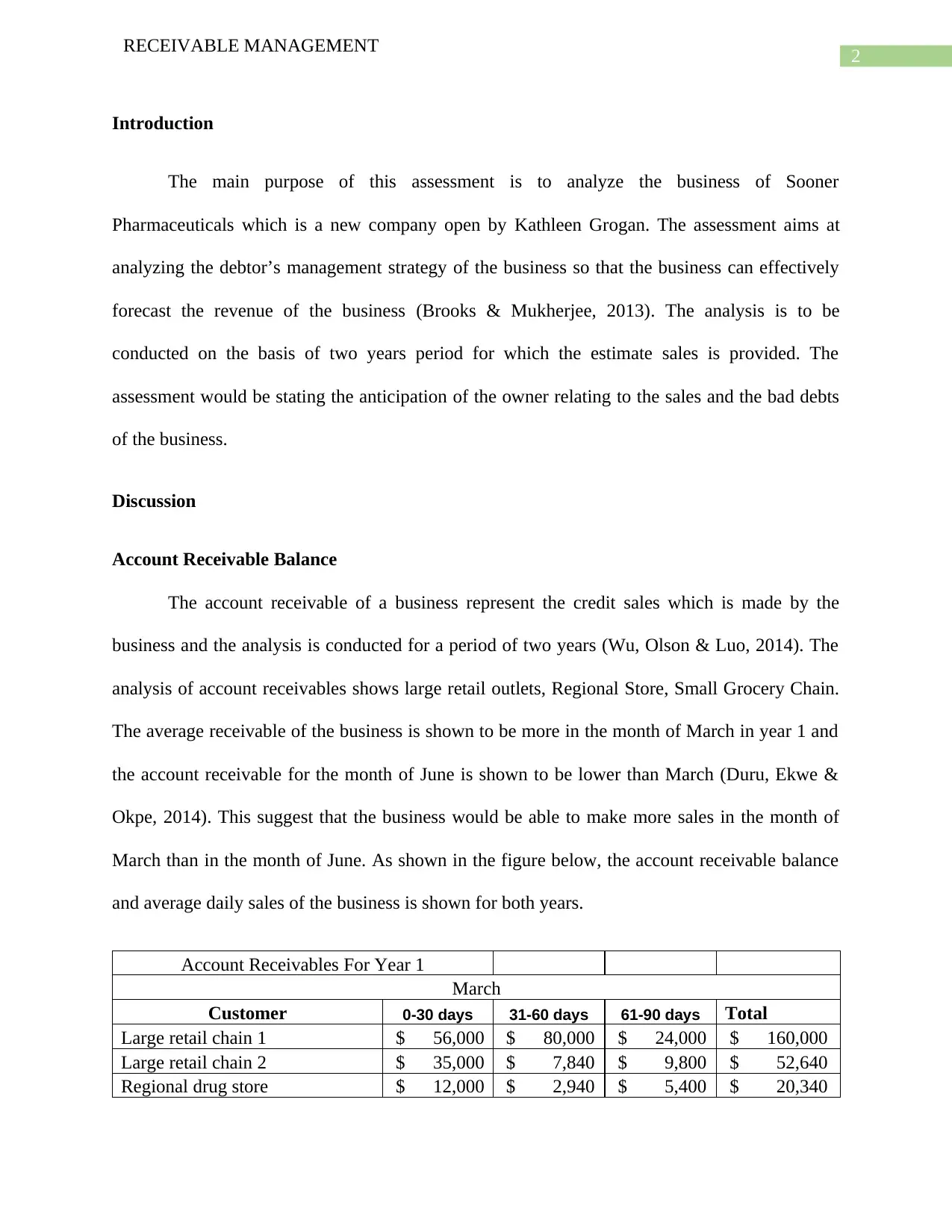

Introduction

The main purpose of this assessment is to analyze the business of Sooner

Pharmaceuticals which is a new company open by Kathleen Grogan. The assessment aims at

analyzing the debtor’s management strategy of the business so that the business can effectively

forecast the revenue of the business (Brooks & Mukherjee, 2013). The analysis is to be

conducted on the basis of two years period for which the estimate sales is provided. The

assessment would be stating the anticipation of the owner relating to the sales and the bad debts

of the business.

Discussion

Account Receivable Balance

The account receivable of a business represent the credit sales which is made by the

business and the analysis is conducted for a period of two years (Wu, Olson & Luo, 2014). The

analysis of account receivables shows large retail outlets, Regional Store, Small Grocery Chain.

The average receivable of the business is shown to be more in the month of March in year 1 and

the account receivable for the month of June is shown to be lower than March (Duru, Ekwe &

Okpe, 2014). This suggest that the business would be able to make more sales in the month of

March than in the month of June. As shown in the figure below, the account receivable balance

and average daily sales of the business is shown for both years.

Account Receivables For Year 1

March

Customer 0-30 days 31-60 days 61-90 days Total

Large retail chain 1 $ 56,000 $ 80,000 $ 24,000 $ 160,000

Large retail chain 2 $ 35,000 $ 7,840 $ 9,800 $ 52,640

Regional drug store $ 12,000 $ 2,940 $ 5,400 $ 20,340

RECEIVABLE MANAGEMENT

Introduction

The main purpose of this assessment is to analyze the business of Sooner

Pharmaceuticals which is a new company open by Kathleen Grogan. The assessment aims at

analyzing the debtor’s management strategy of the business so that the business can effectively

forecast the revenue of the business (Brooks & Mukherjee, 2013). The analysis is to be

conducted on the basis of two years period for which the estimate sales is provided. The

assessment would be stating the anticipation of the owner relating to the sales and the bad debts

of the business.

Discussion

Account Receivable Balance

The account receivable of a business represent the credit sales which is made by the

business and the analysis is conducted for a period of two years (Wu, Olson & Luo, 2014). The

analysis of account receivables shows large retail outlets, Regional Store, Small Grocery Chain.

The average receivable of the business is shown to be more in the month of March in year 1 and

the account receivable for the month of June is shown to be lower than March (Duru, Ekwe &

Okpe, 2014). This suggest that the business would be able to make more sales in the month of

March than in the month of June. As shown in the figure below, the account receivable balance

and average daily sales of the business is shown for both years.

Account Receivables For Year 1

March

Customer 0-30 days 31-60 days 61-90 days Total

Large retail chain 1 $ 56,000 $ 80,000 $ 24,000 $ 160,000

Large retail chain 2 $ 35,000 $ 7,840 $ 9,800 $ 52,640

Regional drug store $ 12,000 $ 2,940 $ 5,400 $ 20,340

3

RECEIVABLE MANAGEMENT

Small grocery chain $ 12,000 $ 22,000 $ 6,000 $ 40,000

Total Account Receivables $ 272,980

Daily Collection $ 9,099.33

Average collection period(Days) 30

June

Customer 0-30 days 31-60 days 61-90 days Total

Large retail chain 1 $ 42,000 $ 60,000 $ 18,000 $ 120,000

Large retail chain 2 $ 26,250 $ 5,880 $ 7,350 $ 39,480

Regional drug store $ 9,000 $ 2,205 $ 4,050 $ 15,255

Small grocery chain $ 9,000 $ 16,500 $ 4,500 $ 30,000

Total Account Receivables $ 204,735

Daily Collection $ 6,825

Average collection period(Days) 30

Account Receivables For Year 2

March

Customer 0-30 days 31-60 days 61-90 days Total

Large retail chain 1 $ 70,000 $ 100,000 $ 30,000 $ 200,000

Large retail chain 2 $ 43,750 $ 70,000 $ 61,250 $ 175,000

Regional drug store $ 15,000 $ 26,250 $ 33,750 $ 75,000

Small grocery chain $ 15,000 $ 27,500 $ 7,500 $ 50,000

Total Account Receivables $ 500,000

Daily Collection $ 16,666.67

Average collection period(Days) 30

June

Customer 0-30 days 31-60 days 61-90 days Total

Large retail chain 1 $ 49,000 $ 70,000 $ 21,000 $ 140,000

Large retail chain 2 $ 30,625 $ 49,000 $ 42,875 $ 122,500

Regional drug store $ 10,500 $ 18,375 $ 23,625 $ 52,500

Small grocery chain $ 10,500 $ 19,250 $ 5,250 $ 35,000

Total Account Receivables $ 350,000

Daily Collection $ 11,666.67

Average collection period(Days) 30

The average collection period for both the years is considered to be 30 days for both the

month of March and June. The total debtors for the first year in the month of March is shown to

RECEIVABLE MANAGEMENT

Small grocery chain $ 12,000 $ 22,000 $ 6,000 $ 40,000

Total Account Receivables $ 272,980

Daily Collection $ 9,099.33

Average collection period(Days) 30

June

Customer 0-30 days 31-60 days 61-90 days Total

Large retail chain 1 $ 42,000 $ 60,000 $ 18,000 $ 120,000

Large retail chain 2 $ 26,250 $ 5,880 $ 7,350 $ 39,480

Regional drug store $ 9,000 $ 2,205 $ 4,050 $ 15,255

Small grocery chain $ 9,000 $ 16,500 $ 4,500 $ 30,000

Total Account Receivables $ 204,735

Daily Collection $ 6,825

Average collection period(Days) 30

Account Receivables For Year 2

March

Customer 0-30 days 31-60 days 61-90 days Total

Large retail chain 1 $ 70,000 $ 100,000 $ 30,000 $ 200,000

Large retail chain 2 $ 43,750 $ 70,000 $ 61,250 $ 175,000

Regional drug store $ 15,000 $ 26,250 $ 33,750 $ 75,000

Small grocery chain $ 15,000 $ 27,500 $ 7,500 $ 50,000

Total Account Receivables $ 500,000

Daily Collection $ 16,666.67

Average collection period(Days) 30

June

Customer 0-30 days 31-60 days 61-90 days Total

Large retail chain 1 $ 49,000 $ 70,000 $ 21,000 $ 140,000

Large retail chain 2 $ 30,625 $ 49,000 $ 42,875 $ 122,500

Regional drug store $ 10,500 $ 18,375 $ 23,625 $ 52,500

Small grocery chain $ 10,500 $ 19,250 $ 5,250 $ 35,000

Total Account Receivables $ 350,000

Daily Collection $ 11,666.67

Average collection period(Days) 30

The average collection period for both the years is considered to be 30 days for both the

month of March and June. The total debtors for the first year in the month of March is shown to

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

RECEIVABLE MANAGEMENT

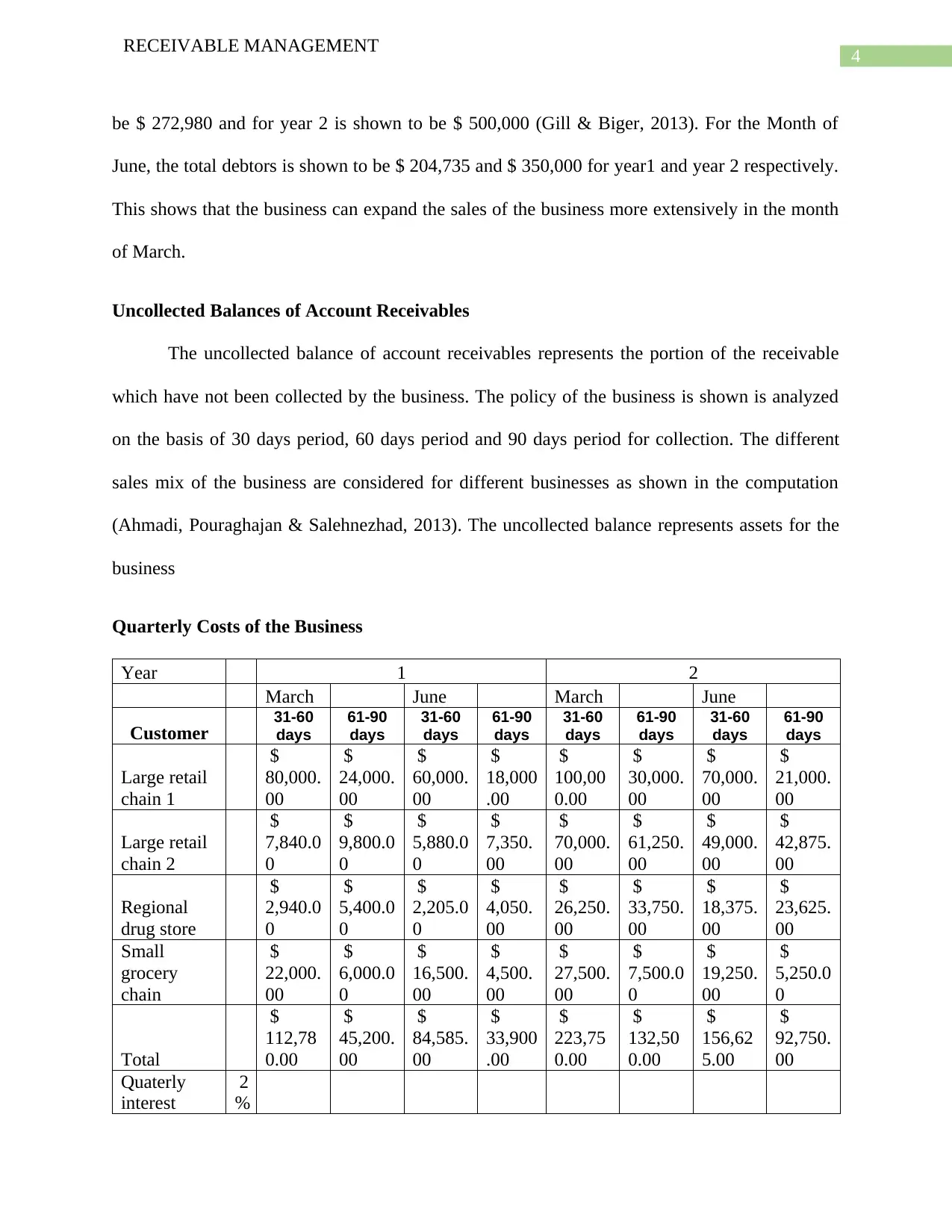

be $ 272,980 and for year 2 is shown to be $ 500,000 (Gill & Biger, 2013). For the Month of

June, the total debtors is shown to be $ 204,735 and $ 350,000 for year1 and year 2 respectively.

This shows that the business can expand the sales of the business more extensively in the month

of March.

Uncollected Balances of Account Receivables

The uncollected balance of account receivables represents the portion of the receivable

which have not been collected by the business. The policy of the business is shown is analyzed

on the basis of 30 days period, 60 days period and 90 days period for collection. The different

sales mix of the business are considered for different businesses as shown in the computation

(Ahmadi, Pouraghajan & Salehnezhad, 2013). The uncollected balance represents assets for the

business

Quarterly Costs of the Business

Year 1 2

March June March June

Customer 31-60

days

61-90

days

31-60

days

61-90

days

31-60

days

61-90

days

31-60

days

61-90

days

Large retail

chain 1

$

80,000.

00

$

24,000.

00

$

60,000.

00

$

18,000

.00

$

100,00

0.00

$

30,000.

00

$

70,000.

00

$

21,000.

00

Large retail

chain 2

$

7,840.0

0

$

9,800.0

0

$

5,880.0

0

$

7,350.

00

$

70,000.

00

$

61,250.

00

$

49,000.

00

$

42,875.

00

Regional

drug store

$

2,940.0

0

$

5,400.0

0

$

2,205.0

0

$

4,050.

00

$

26,250.

00

$

33,750.

00

$

18,375.

00

$

23,625.

00

Small

grocery

chain

$

22,000.

00

$

6,000.0

0

$

16,500.

00

$

4,500.

00

$

27,500.

00

$

7,500.0

0

$

19,250.

00

$

5,250.0

0

Total

$

112,78

0.00

$

45,200.

00

$

84,585.

00

$

33,900

.00

$

223,75

0.00

$

132,50

0.00

$

156,62

5.00

$

92,750.

00

Quaterly

interest

2

%

RECEIVABLE MANAGEMENT

be $ 272,980 and for year 2 is shown to be $ 500,000 (Gill & Biger, 2013). For the Month of

June, the total debtors is shown to be $ 204,735 and $ 350,000 for year1 and year 2 respectively.

This shows that the business can expand the sales of the business more extensively in the month

of March.

Uncollected Balances of Account Receivables

The uncollected balance of account receivables represents the portion of the receivable

which have not been collected by the business. The policy of the business is shown is analyzed

on the basis of 30 days period, 60 days period and 90 days period for collection. The different

sales mix of the business are considered for different businesses as shown in the computation

(Ahmadi, Pouraghajan & Salehnezhad, 2013). The uncollected balance represents assets for the

business

Quarterly Costs of the Business

Year 1 2

March June March June

Customer 31-60

days

61-90

days

31-60

days

61-90

days

31-60

days

61-90

days

31-60

days

61-90

days

Large retail

chain 1

$

80,000.

00

$

24,000.

00

$

60,000.

00

$

18,000

.00

$

100,00

0.00

$

30,000.

00

$

70,000.

00

$

21,000.

00

Large retail

chain 2

$

7,840.0

0

$

9,800.0

0

$

5,880.0

0

$

7,350.

00

$

70,000.

00

$

61,250.

00

$

49,000.

00

$

42,875.

00

Regional

drug store

$

2,940.0

0

$

5,400.0

0

$

2,205.0

0

$

4,050.

00

$

26,250.

00

$

33,750.

00

$

18,375.

00

$

23,625.

00

Small

grocery

chain

$

22,000.

00

$

6,000.0

0

$

16,500.

00

$

4,500.

00

$

27,500.

00

$

7,500.0

0

$

19,250.

00

$

5,250.0

0

Total

$

112,78

0.00

$

45,200.

00

$

84,585.

00

$

33,900

.00

$

223,75

0.00

$

132,50

0.00

$

156,62

5.00

$

92,750.

00

Quaterly

interest

2

%

5

RECEIVABLE MANAGEMENT

Quaterly

Carrying

Cost

$

370.78

$

222.90

$

278.09

$

167.18

$

735.62

$

653.42

$

514.93

$

457.40

The above table shows the quarterly costs of the business which is computed on the basis

of the quarterly sales which is incurred by the business and the same is done on an estimation

basis. The interest rate which is charged is shown to be 2% which is on quarterly basis. The

lowest quarterly carrying costs is in the month of June of year 1 under 60-90 days policy (Seifert,

Seifert & Protopappa-Sieke, 2013). The same is shown to have increased in year 2 which is

mainly to due to expansion of the operations of the business and therefore the sales of the

business have also increased significantly. The increase in the carrying costs and also the

forecasts of sales suggest that the management is planning to expand the operations of the

business in year.

Ageing Schedule

Assumed

Collection

Period

year 1 March June

Customer

0-30

days

31-60

days

61-90

days Total

0-30

days

31-60

days

61-90

days Total

Large retail

chain 1

$56,00

0.00

$80,00

0.00

$24,00

0.00

$

42,000.

00

$

60,000.

00

$

18,000

.00

Large retail

chain 2

$35,00

0.00

$7,840.

00

$9,800.

00

$

26,250.

00

$

5,880.0

0

$

7,350.

00

Regional drug

store

$12,00

0.00

$2,940.

00

$5,400.

00

$

9,000.0

0

$

2,205.0

0

$

4,050.

00

Small grocery

chain

$12,00

0.00

$22,00

0.00

$6,000.

00

$

9,000.0

0

$

16,500.

00

$

4,500.

00

TOTAL

$115,0

00.00

$112,7

80.00

$45,20

0.00

$86,25

0.00

$84,58

5.00

$33,90

0.00

RECEIVABLE MANAGEMENT

Quaterly

Carrying

Cost

$

370.78

$

222.90

$

278.09

$

167.18

$

735.62

$

653.42

$

514.93

$

457.40

The above table shows the quarterly costs of the business which is computed on the basis

of the quarterly sales which is incurred by the business and the same is done on an estimation

basis. The interest rate which is charged is shown to be 2% which is on quarterly basis. The

lowest quarterly carrying costs is in the month of June of year 1 under 60-90 days policy (Seifert,

Seifert & Protopappa-Sieke, 2013). The same is shown to have increased in year 2 which is

mainly to due to expansion of the operations of the business and therefore the sales of the

business have also increased significantly. The increase in the carrying costs and also the

forecasts of sales suggest that the management is planning to expand the operations of the

business in year.

Ageing Schedule

Assumed

Collection

Period

year 1 March June

Customer

0-30

days

31-60

days

61-90

days Total

0-30

days

31-60

days

61-90

days Total

Large retail

chain 1

$56,00

0.00

$80,00

0.00

$24,00

0.00

$

42,000.

00

$

60,000.

00

$

18,000

.00

Large retail

chain 2

$35,00

0.00

$7,840.

00

$9,800.

00

$

26,250.

00

$

5,880.0

0

$

7,350.

00

Regional drug

store

$12,00

0.00

$2,940.

00

$5,400.

00

$

9,000.0

0

$

2,205.0

0

$

4,050.

00

Small grocery

chain

$12,00

0.00

$22,00

0.00

$6,000.

00

$

9,000.0

0

$

16,500.

00

$

4,500.

00

TOTAL

$115,0

00.00

$112,7

80.00

$45,20

0.00

$86,25

0.00

$84,58

5.00

$33,90

0.00

6

RECEIVABLE MANAGEMENT

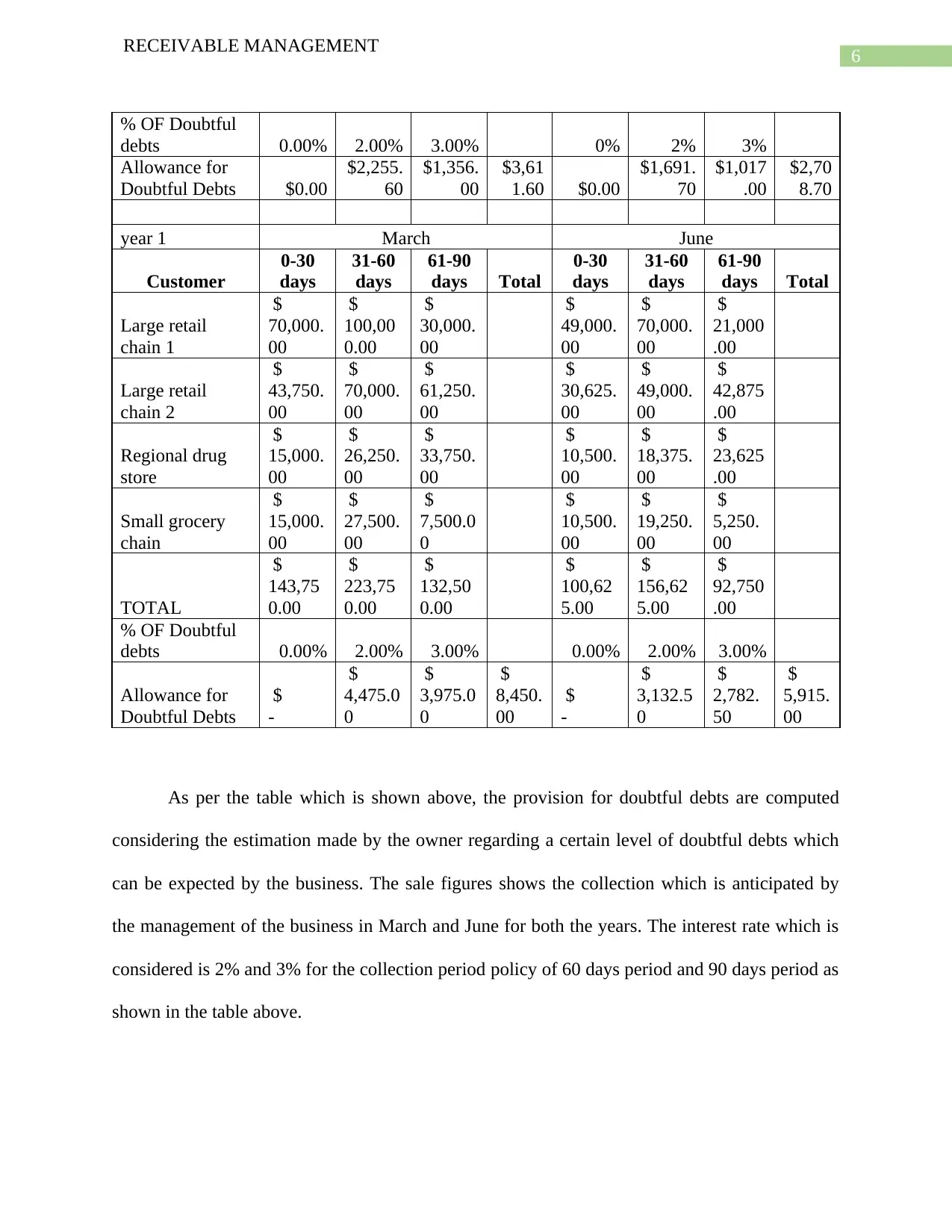

% OF Doubtful

debts 0.00% 2.00% 3.00% 0% 2% 3%

Allowance for

Doubtful Debts $0.00

$2,255.

60

$1,356.

00

$3,61

1.60 $0.00

$1,691.

70

$1,017

.00

$2,70

8.70

year 1 March June

Customer

0-30

days

31-60

days

61-90

days Total

0-30

days

31-60

days

61-90

days Total

Large retail

chain 1

$

70,000.

00

$

100,00

0.00

$

30,000.

00

$

49,000.

00

$

70,000.

00

$

21,000

.00

Large retail

chain 2

$

43,750.

00

$

70,000.

00

$

61,250.

00

$

30,625.

00

$

49,000.

00

$

42,875

.00

Regional drug

store

$

15,000.

00

$

26,250.

00

$

33,750.

00

$

10,500.

00

$

18,375.

00

$

23,625

.00

Small grocery

chain

$

15,000.

00

$

27,500.

00

$

7,500.0

0

$

10,500.

00

$

19,250.

00

$

5,250.

00

TOTAL

$

143,75

0.00

$

223,75

0.00

$

132,50

0.00

$

100,62

5.00

$

156,62

5.00

$

92,750

.00

% OF Doubtful

debts 0.00% 2.00% 3.00% 0.00% 2.00% 3.00%

Allowance for

Doubtful Debts

$

-

$

4,475.0

0

$

3,975.0

0

$

8,450.

00

$

-

$

3,132.5

0

$

2,782.

50

$

5,915.

00

As per the table which is shown above, the provision for doubtful debts are computed

considering the estimation made by the owner regarding a certain level of doubtful debts which

can be expected by the business. The sale figures shows the collection which is anticipated by

the management of the business in March and June for both the years. The interest rate which is

considered is 2% and 3% for the collection period policy of 60 days period and 90 days period as

shown in the table above.

RECEIVABLE MANAGEMENT

% OF Doubtful

debts 0.00% 2.00% 3.00% 0% 2% 3%

Allowance for

Doubtful Debts $0.00

$2,255.

60

$1,356.

00

$3,61

1.60 $0.00

$1,691.

70

$1,017

.00

$2,70

8.70

year 1 March June

Customer

0-30

days

31-60

days

61-90

days Total

0-30

days

31-60

days

61-90

days Total

Large retail

chain 1

$

70,000.

00

$

100,00

0.00

$

30,000.

00

$

49,000.

00

$

70,000.

00

$

21,000

.00

Large retail

chain 2

$

43,750.

00

$

70,000.

00

$

61,250.

00

$

30,625.

00

$

49,000.

00

$

42,875

.00

Regional drug

store

$

15,000.

00

$

26,250.

00

$

33,750.

00

$

10,500.

00

$

18,375.

00

$

23,625

.00

Small grocery

chain

$

15,000.

00

$

27,500.

00

$

7,500.0

0

$

10,500.

00

$

19,250.

00

$

5,250.

00

TOTAL

$

143,75

0.00

$

223,75

0.00

$

132,50

0.00

$

100,62

5.00

$

156,62

5.00

$

92,750

.00

% OF Doubtful

debts 0.00% 2.00% 3.00% 0.00% 2.00% 3.00%

Allowance for

Doubtful Debts

$

-

$

4,475.0

0

$

3,975.0

0

$

8,450.

00

$

-

$

3,132.5

0

$

2,782.

50

$

5,915.

00

As per the table which is shown above, the provision for doubtful debts are computed

considering the estimation made by the owner regarding a certain level of doubtful debts which

can be expected by the business. The sale figures shows the collection which is anticipated by

the management of the business in March and June for both the years. The interest rate which is

considered is 2% and 3% for the collection period policy of 60 days period and 90 days period as

shown in the table above.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

RECEIVABLE MANAGEMENT

Reference

Ahmadi, M., Pouraghajan, A., & Salehnezhad, S. (2013). Performance measurement of

receivable accounts’ risk management: A case study of Tehran Stock

Exchange.Management Science Letters, 3(6), 1593-1598.

Brooks, R., & Mukherjee, A. K. (2013). Financial management: core concepts. Pearson.

Duru, A. N., Ekwe, M. C., & Okpe, I. I. (2014). Accounts receivable management and corporate

performance of companies in the food & beverage industry: evidence from

Nigeria. European Journal of Accounting Auditing and Finance Research, 2(10), 34-47.

Gill, A. S., & Biger, N. (2013). The impact of corporate governance on working capital

management efficiency of American manufacturing firms. Managerial Finance, 39(2),

116-132.

Seifert, D., Seifert, R. W., & Protopappa-Sieke, M. (2013). A review of trade credit literature:

Opportunities for research in operations. European Journal of Operational

Research,231(2), 245-256.

Wu, D. D., Olson, D. L., & Luo, C. (2014). A Decision Support Approach for Accounts

Receivable Risk Management. IEEE Trans. Systems, Man, and Cybernetics:

Systems, 44(12), 1624-1632.

RECEIVABLE MANAGEMENT

Reference

Ahmadi, M., Pouraghajan, A., & Salehnezhad, S. (2013). Performance measurement of

receivable accounts’ risk management: A case study of Tehran Stock

Exchange.Management Science Letters, 3(6), 1593-1598.

Brooks, R., & Mukherjee, A. K. (2013). Financial management: core concepts. Pearson.

Duru, A. N., Ekwe, M. C., & Okpe, I. I. (2014). Accounts receivable management and corporate

performance of companies in the food & beverage industry: evidence from

Nigeria. European Journal of Accounting Auditing and Finance Research, 2(10), 34-47.

Gill, A. S., & Biger, N. (2013). The impact of corporate governance on working capital

management efficiency of American manufacturing firms. Managerial Finance, 39(2),

116-132.

Seifert, D., Seifert, R. W., & Protopappa-Sieke, M. (2013). A review of trade credit literature:

Opportunities for research in operations. European Journal of Operational

Research,231(2), 245-256.

Wu, D. D., Olson, D. L., & Luo, C. (2014). A Decision Support Approach for Accounts

Receivable Risk Management. IEEE Trans. Systems, Man, and Cybernetics:

Systems, 44(12), 1624-1632.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.