Analysis of IAS-36 and Financial Instruments for Reckitt Benckiser PLC

VerifiedAdded on 2023/06/09

|15

|3320

|246

Report

AI Summary

This report provides an in-depth analysis of Reckitt Benckiser Group PLC's financial reporting practices, particularly focusing on the application of IAS-36 and its impact on asset valuation and impairment of goodwill. The report details the company's approach to determining cash-generating units, assessing cash flows, and recognizing impairment losses. It examines the assumptions underlying impairment tests, including discount rates, terminal growth rates, and revenue and EBIT growth projections. Furthermore, the report explores Reckitt's financial risk management strategies, including the handling of financial instruments, currency fluctuations, and interest rate risks. It also analyzes the company's defined benefit pension plan, including the calculation of obligations, discount rates, and alignment with industry practices. The analysis incorporates information from Reckitt's annual reports, financial statements, and relevant accounting standards to provide a comprehensive overview of the company's financial performance and risk management strategies.

UMACTT-15-M 1

Written Assignment – Component B

Advanced Corporate Reporting

Instructor:

Word count: 2060

Written Assignment – Component B

Advanced Corporate Reporting

Instructor:

Word count: 2060

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UMACTT-15-M 2

Executive Summary

Reckitt Benckiser Group PLC commonly known as Reckitt is a multinational consumer goods

corporation headquartered in England that produces nutrition, hygiene and health products. The

report has shed light on the application of IAS-36 by the “Reckitt Benckiser Group PLC” to

“value its assets” and “impairments of goodwill” in the firm. The firm has been reflecting,

“Impaired value of goodwill” to “985 million pounds” at the end of financial period of 2020.

The report also includes the information’s related to the financial instruments used by the

company. In the analysis report, the financial risk management analysis of Reckitt is mentioned

along with critical revelation of their benefits pension plans that are impaired with IAS 39 and

IFRS 9. These financial statements are impaired with the IASB conceptual framework that

reflects the qualitative characteristics.

Executive Summary

Reckitt Benckiser Group PLC commonly known as Reckitt is a multinational consumer goods

corporation headquartered in England that produces nutrition, hygiene and health products. The

report has shed light on the application of IAS-36 by the “Reckitt Benckiser Group PLC” to

“value its assets” and “impairments of goodwill” in the firm. The firm has been reflecting,

“Impaired value of goodwill” to “985 million pounds” at the end of financial period of 2020.

The report also includes the information’s related to the financial instruments used by the

company. In the analysis report, the financial risk management analysis of Reckitt is mentioned

along with critical revelation of their benefits pension plans that are impaired with IAS 39 and

IFRS 9. These financial statements are impaired with the IASB conceptual framework that

reflects the qualitative characteristics.

UMACTT-15-M 3

Table of Contents

1. Introduction..............................................................................................................................4

2. Analysis and discussion of the accounting policy....................................................................6

2.1 Depth analysis and synthesizing question 2 (a).....................................................................6

2.2 Depth analysis and synthesizing question 2 (b).....................................................................9

2.3 Depth analysis and synthesizing question 2 (c)...................................................................12

3. Conclusion..............................................................................................................................15

References......................................................................................................................................16

Table of Contents

1. Introduction..............................................................................................................................4

2. Analysis and discussion of the accounting policy....................................................................6

2.1 Depth analysis and synthesizing question 2 (a).....................................................................6

2.2 Depth analysis and synthesizing question 2 (b).....................................................................9

2.3 Depth analysis and synthesizing question 2 (c)...................................................................12

3. Conclusion..............................................................................................................................15

References......................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

UMACTT-15-M 4

1. Introduction

“Reckitt Benckiser Group PLC” commonly known as Reckitt is a multinational consumer

goods corporation headquartered in England. The market capitalization of Reckitt is 54.935

Billion along with a “Forward Dividend & Yield” of 0.47 and market volume of 299,562. Based

on the financial highlights of the last released annual report of 2020 this company has revealed

its revenue generation to be £14.0bn (Reckitt.com, 2020). The regulatory framework of Reckitt

is impactful regarding the funding basis that will be caused by the changes in regulations, which

are objectified to keep consistent and transparent by Reckitt. The regulatory framework of the

company consists of corporate governance, environmental issues, interim reporting and even

social disclosure reports.

1. Introduction

“Reckitt Benckiser Group PLC” commonly known as Reckitt is a multinational consumer

goods corporation headquartered in England. The market capitalization of Reckitt is 54.935

Billion along with a “Forward Dividend & Yield” of 0.47 and market volume of 299,562. Based

on the financial highlights of the last released annual report of 2020 this company has revealed

its revenue generation to be £14.0bn (Reckitt.com, 2020). The regulatory framework of Reckitt

is impactful regarding the funding basis that will be caused by the changes in regulations, which

are objectified to keep consistent and transparent by Reckitt. The regulatory framework of the

company consists of corporate governance, environmental issues, interim reporting and even

social disclosure reports.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UMACTT-15-M 5

2. Analysis and discussion of the accounting policy

2.1 Depth analysis and synthesizing question 2 (a)

The “IAS-36” has reflected impairment of intangible assets while preceding the impairment test

of generating cash. The company has determined CGU on the basis of smallest identifiable group

of assets that are expected to generate cash inflows which are independent of other group of

assets. The assessment of cash flows for the purpose of impairment is done through cash flow

projections forming part of one-year budget or 3-5-year strategic plan and beyond that terminal

growth rates are used.

As per the financial report of the company, the value of “impairment of goodwill” has

been valued to “985 million pound” until 2020 (Reckitt, 2020). The basic requirement to

determine recoverable amount is dependent on the fair value of investment reduced by cost

incurred for selling it and applicable value of it. Based on the industrial practices the impairment

of goodwill is allocated as per the cash-generating units of the acquirer, which are expected to

get sheer benefits. As per IAS 36, the impairment loss is allocated to compensate the carrying

amount for the assets in the industry comparatively.

The impact of impairment test results was such where impairment of Goodwill lead to

reduction in the amount of capital employed which in turn enhances the ROCE used for LTIP

purposes. To ensure that the goodwill impairment doesn’t lead to increase in vesting with regards

to the proportion of LTIP associated with ROCE, the capital employed was then adjusted

accordingly. If the overly optimistic assumptions are being used for impairment assessment, then

it could result in no impairment charges recognition. After completing the impairment test,

Reckitt determined the value in use with respect to IFCN have high degree of estimation

uncertainty which could result in changing key assumptions and accordingly changes would take

place in IFCN valuation. A circumstance or event resulting from impairment test if indicates that

the carrying value is exceeding the recoverable amount of goodwill or intangible assets with

indefinite life, then the difference between the two is recognised in the income statement of the

company and accordingly, reduces the profitability of the concern.

2. Analysis and discussion of the accounting policy

2.1 Depth analysis and synthesizing question 2 (a)

The “IAS-36” has reflected impairment of intangible assets while preceding the impairment test

of generating cash. The company has determined CGU on the basis of smallest identifiable group

of assets that are expected to generate cash inflows which are independent of other group of

assets. The assessment of cash flows for the purpose of impairment is done through cash flow

projections forming part of one-year budget or 3-5-year strategic plan and beyond that terminal

growth rates are used.

As per the financial report of the company, the value of “impairment of goodwill” has

been valued to “985 million pound” until 2020 (Reckitt, 2020). The basic requirement to

determine recoverable amount is dependent on the fair value of investment reduced by cost

incurred for selling it and applicable value of it. Based on the industrial practices the impairment

of goodwill is allocated as per the cash-generating units of the acquirer, which are expected to

get sheer benefits. As per IAS 36, the impairment loss is allocated to compensate the carrying

amount for the assets in the industry comparatively.

The impact of impairment test results was such where impairment of Goodwill lead to

reduction in the amount of capital employed which in turn enhances the ROCE used for LTIP

purposes. To ensure that the goodwill impairment doesn’t lead to increase in vesting with regards

to the proportion of LTIP associated with ROCE, the capital employed was then adjusted

accordingly. If the overly optimistic assumptions are being used for impairment assessment, then

it could result in no impairment charges recognition. After completing the impairment test,

Reckitt determined the value in use with respect to IFCN have high degree of estimation

uncertainty which could result in changing key assumptions and accordingly changes would take

place in IFCN valuation. A circumstance or event resulting from impairment test if indicates that

the carrying value is exceeding the recoverable amount of goodwill or intangible assets with

indefinite life, then the difference between the two is recognised in the income statement of the

company and accordingly, reduces the profitability of the concern.

UMACTT-15-M 6

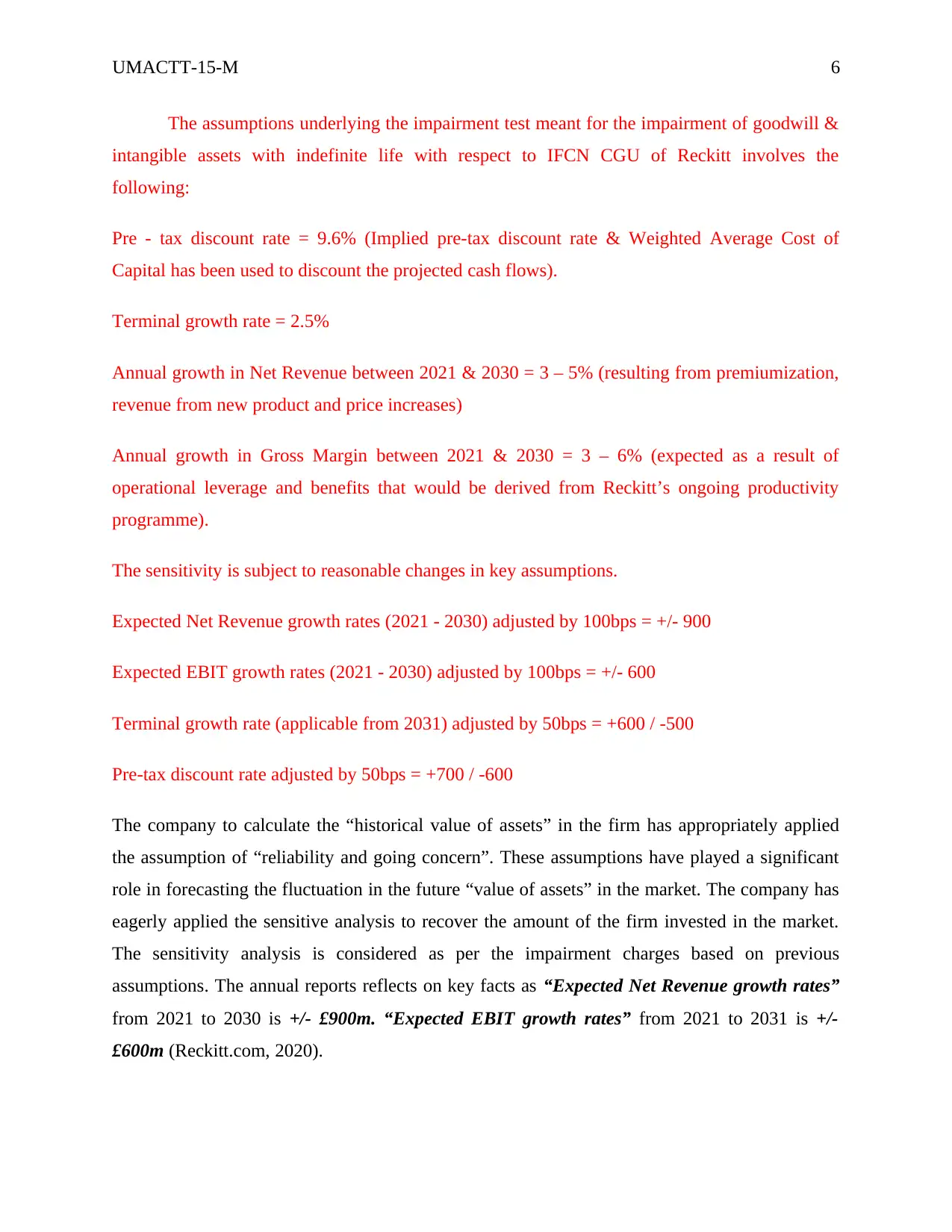

The assumptions underlying the impairment test meant for the impairment of goodwill &

intangible assets with indefinite life with respect to IFCN CGU of Reckitt involves the

following:

Pre - tax discount rate = 9.6% (Implied pre-tax discount rate & Weighted Average Cost of

Capital has been used to discount the projected cash flows).

Terminal growth rate = 2.5%

Annual growth in Net Revenue between 2021 & 2030 = 3 – 5% (resulting from premiumization,

revenue from new product and price increases)

Annual growth in Gross Margin between 2021 & 2030 = 3 – 6% (expected as a result of

operational leverage and benefits that would be derived from Reckitt’s ongoing productivity

programme).

The sensitivity is subject to reasonable changes in key assumptions.

Expected Net Revenue growth rates (2021 - 2030) adjusted by 100bps = +/- 900

Expected EBIT growth rates (2021 - 2030) adjusted by 100bps = +/- 600

Terminal growth rate (applicable from 2031) adjusted by 50bps = +600 / -500

Pre-tax discount rate adjusted by 50bps = +700 / -600

The company to calculate the “historical value of assets” in the firm has appropriately applied

the assumption of “reliability and going concern”. These assumptions have played a significant

role in forecasting the fluctuation in the future “value of assets” in the market. The company has

eagerly applied the sensitive analysis to recover the amount of the firm invested in the market.

The sensitivity analysis is considered as per the impairment charges based on previous

assumptions. The annual reports reflects on key facts as “Expected Net Revenue growth rates”

from 2021 to 2030 is +/- £900m. “Expected EBIT growth rates” from 2021 to 2031 is +/-

£600m (Reckitt.com, 2020).

The assumptions underlying the impairment test meant for the impairment of goodwill &

intangible assets with indefinite life with respect to IFCN CGU of Reckitt involves the

following:

Pre - tax discount rate = 9.6% (Implied pre-tax discount rate & Weighted Average Cost of

Capital has been used to discount the projected cash flows).

Terminal growth rate = 2.5%

Annual growth in Net Revenue between 2021 & 2030 = 3 – 5% (resulting from premiumization,

revenue from new product and price increases)

Annual growth in Gross Margin between 2021 & 2030 = 3 – 6% (expected as a result of

operational leverage and benefits that would be derived from Reckitt’s ongoing productivity

programme).

The sensitivity is subject to reasonable changes in key assumptions.

Expected Net Revenue growth rates (2021 - 2030) adjusted by 100bps = +/- 900

Expected EBIT growth rates (2021 - 2030) adjusted by 100bps = +/- 600

Terminal growth rate (applicable from 2031) adjusted by 50bps = +600 / -500

Pre-tax discount rate adjusted by 50bps = +700 / -600

The company to calculate the “historical value of assets” in the firm has appropriately applied

the assumption of “reliability and going concern”. These assumptions have played a significant

role in forecasting the fluctuation in the future “value of assets” in the market. The company has

eagerly applied the sensitive analysis to recover the amount of the firm invested in the market.

The sensitivity analysis is considered as per the impairment charges based on previous

assumptions. The annual reports reflects on key facts as “Expected Net Revenue growth rates”

from 2021 to 2030 is +/- £900m. “Expected EBIT growth rates” from 2021 to 2031 is +/-

£600m (Reckitt.com, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

UMACTT-15-M 7

Yes, the company has appropriately “impaired the goodwill” by applying the concept of

“amortisation of the goodwill” valued in the company. The amount charged as amortisation has

shown in the “income statement” of the company added in the “cash flow statement” to reflect

actual profit of the firm.

The loss in the impairment has been reflected on the debit side of “income statement” as per the

“principle of conservatism”. This approach of accounting practice has reflected the outdated

tendency of the company. The company has been using the policies of “share-based payment

transactions” as per “IAS-36”. The appropriate scope of transaction leasing has applied to

calculate and analyse “fair value” and “realisable value” of the company as per “IFRS-2 and

IAS-17” (Elakova, 2020, p.73). However, other companies have followed the policies of

reducing the cost from the fair value rather than “shared-based payments transactions” as per

“IAS-36”. The company follows the impairment practice in alignment with the industry based on

IAS 36 where difference between the recoverable amount and carrying value is recognised in

income statement for the year.

2.2 Depth analysis and synthesizing question 2 (b)

The financial instrument category of “Reckitt Benckiser Group PLC” contains company shares

of 5,747.00 GBX (Londonstockexchange.com, 2022). Reckitt is facing the main financial risk

from the climate perspective along with market prices, interest rates, liquidity, credit and foreign

exchange risk. The financial risks are managed by Reckitt by rightsizing their portfolio and

adapting to channel strategy with an accelerating e-commerce portfolio (Finance.yahoo.com,

2022). These financial risks are affecting Reckitt by disrupting their sustainability, value chain,

logistics functions along with having potential impacts on the financial statements reflecting in

economic downturns in future. This risk results in translation exposure of company’s profit after

tax generated in foreign currency. This would affect the value of the firm in future. Interest rate

risk may result in lower return on investment or higher debt servicing costs.

Yes, the company has appropriately “impaired the goodwill” by applying the concept of

“amortisation of the goodwill” valued in the company. The amount charged as amortisation has

shown in the “income statement” of the company added in the “cash flow statement” to reflect

actual profit of the firm.

The loss in the impairment has been reflected on the debit side of “income statement” as per the

“principle of conservatism”. This approach of accounting practice has reflected the outdated

tendency of the company. The company has been using the policies of “share-based payment

transactions” as per “IAS-36”. The appropriate scope of transaction leasing has applied to

calculate and analyse “fair value” and “realisable value” of the company as per “IFRS-2 and

IAS-17” (Elakova, 2020, p.73). However, other companies have followed the policies of

reducing the cost from the fair value rather than “shared-based payments transactions” as per

“IAS-36”. The company follows the impairment practice in alignment with the industry based on

IAS 36 where difference between the recoverable amount and carrying value is recognised in

income statement for the year.

2.2 Depth analysis and synthesizing question 2 (b)

The financial instrument category of “Reckitt Benckiser Group PLC” contains company shares

of 5,747.00 GBX (Londonstockexchange.com, 2022). Reckitt is facing the main financial risk

from the climate perspective along with market prices, interest rates, liquidity, credit and foreign

exchange risk. The financial risks are managed by Reckitt by rightsizing their portfolio and

adapting to channel strategy with an accelerating e-commerce portfolio (Finance.yahoo.com,

2022). These financial risks are affecting Reckitt by disrupting their sustainability, value chain,

logistics functions along with having potential impacts on the financial statements reflecting in

economic downturns in future. This risk results in translation exposure of company’s profit after

tax generated in foreign currency. This would affect the value of the firm in future. Interest rate

risk may result in lower return on investment or higher debt servicing costs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UMACTT-15-M 8

3

Reckitt has material sensitivity that can cause changes to its financial risks relating to factors like

goodwill recoverability, revenue recognition, providing uncertain tax provisions and contingent

liabilities. The assumptions made by Reckitt for its fair value measurements consist of quoted

prices from active markets, observable values for non-quoted prices and inputs for non-

observable values by valuation methodology No provision for impairment of financial

instrument was identified in the annual reports of the company as the impairment loss associated

with the financial instruments are recognised in comprehensive income or expenses. The firm’s

valuation and performance in the future is sensitive to the exchange rates due to operating

internationally. Currency fluctuation would affect the profitability of the company. Also, the

interest rate risk would affect the firm’s valuation.

Measurement bases

The fair value of forward exchange contract was determined which was then discounted to fair

value.

The equity instruments are measured on the basis of quoted share price in the market.

Interest rate swaps & cross currency interest rate swaps are measured at their present value.

Rest all other financial instruments are measured at their fair value except for bonds & senior

notes measured on the basis of their quoted market rates (Reckitt Annual Report & Account.

2021). The industry within which the RB plc is operating has a tendency to value their financial

instruments either at amortised value or fair value, therefore, the measurement of financial

instrument is in alignment with the industry practices.

As Reckitt follows the IFRS 9, where the financial instruments are valued at their fair value as

per the industry practices. Accordingly, the unrealized gains or losses are recognised in

comprehensive income statement while the realised gains or losses are recognised in income

statement, thus affecting the financial performance of the company. Fair value is beneficial in

3

Reckitt has material sensitivity that can cause changes to its financial risks relating to factors like

goodwill recoverability, revenue recognition, providing uncertain tax provisions and contingent

liabilities. The assumptions made by Reckitt for its fair value measurements consist of quoted

prices from active markets, observable values for non-quoted prices and inputs for non-

observable values by valuation methodology No provision for impairment of financial

instrument was identified in the annual reports of the company as the impairment loss associated

with the financial instruments are recognised in comprehensive income or expenses. The firm’s

valuation and performance in the future is sensitive to the exchange rates due to operating

internationally. Currency fluctuation would affect the profitability of the company. Also, the

interest rate risk would affect the firm’s valuation.

Measurement bases

The fair value of forward exchange contract was determined which was then discounted to fair

value.

The equity instruments are measured on the basis of quoted share price in the market.

Interest rate swaps & cross currency interest rate swaps are measured at their present value.

Rest all other financial instruments are measured at their fair value except for bonds & senior

notes measured on the basis of their quoted market rates (Reckitt Annual Report & Account.

2021). The industry within which the RB plc is operating has a tendency to value their financial

instruments either at amortised value or fair value, therefore, the measurement of financial

instrument is in alignment with the industry practices.

As Reckitt follows the IFRS 9, where the financial instruments are valued at their fair value as

per the industry practices. Accordingly, the unrealized gains or losses are recognised in

comprehensive income statement while the realised gains or losses are recognised in income

statement, thus affecting the financial performance of the company. Fair value is beneficial in

UMACTT-15-M 9

terms of accurate valuation of financial assets/liabilities along with determining the true income

of the business. In meeting the financial risk management protocols Reckitt uses hedge

accounting for forecasted transactions and other exposure to potential risks (Reckitt.com, 2021).

Based on the IFRS 9, the industry follows hedge ineffectiveness to other comprehensive income

sources.

Hedging transactions undertaken by Reckitt are highly effective for offsetting the

changes taking place in fair values of hedged items and cash flows. Hedge accounting gets

discontinued prospectively when it no longer meets the hedging criteria (Reckitt Annual Report

& Account. 2021). Reckitt is using portfolio constructions, volatility indicators and options as

hedging policies to reduce volatility (Reckitt.com, 2020). These practices are considered to be in

line with that of industrial practices as companies in hedge accounting commonly use these

policies. Industries used such techniques to mitigate and limit their proportionate risks in stock

markets based on forward and future contracts.

2.3 Depth analysis and synthesizing question 2 (c)

Reckitt has measured a “defined benefit pension plan” for its employees in 2021 as £37 m

(Reckitt.com, 2020). It is charged to income statement once the contributions are made. Reckitt

assumes no-payment obligations once the contributions are paid. Further, the surplus or deficit

recognised in the balance sheet with respect to DBPP is considered as the present value of

defined benefit obligations. The benefit plan is calculated annually by discounting future cash

flows using the “projected unit credit method” (Reckitt.com, 2021). Yield on high quality

corporate bond is used as the discounting rate. The industry follows the practice of recognising

DBP in BS as PV of DB obligations + actuarial gains – past service cost – fair value of plan

assets at the balance sheet. The company’s practice is quite in alignment with the industry and

thus is rational because it is based on IAS 19. The assumptions that Reckitt follows for their

defined pension benefit plan is realistic as these values are accrued over the employment period.

As an impact on the financial statement of these assumptions are recorded as past-service costs

in the statement for profit and loss.

terms of accurate valuation of financial assets/liabilities along with determining the true income

of the business. In meeting the financial risk management protocols Reckitt uses hedge

accounting for forecasted transactions and other exposure to potential risks (Reckitt.com, 2021).

Based on the IFRS 9, the industry follows hedge ineffectiveness to other comprehensive income

sources.

Hedging transactions undertaken by Reckitt are highly effective for offsetting the

changes taking place in fair values of hedged items and cash flows. Hedge accounting gets

discontinued prospectively when it no longer meets the hedging criteria (Reckitt Annual Report

& Account. 2021). Reckitt is using portfolio constructions, volatility indicators and options as

hedging policies to reduce volatility (Reckitt.com, 2020). These practices are considered to be in

line with that of industrial practices as companies in hedge accounting commonly use these

policies. Industries used such techniques to mitigate and limit their proportionate risks in stock

markets based on forward and future contracts.

2.3 Depth analysis and synthesizing question 2 (c)

Reckitt has measured a “defined benefit pension plan” for its employees in 2021 as £37 m

(Reckitt.com, 2020). It is charged to income statement once the contributions are made. Reckitt

assumes no-payment obligations once the contributions are paid. Further, the surplus or deficit

recognised in the balance sheet with respect to DBPP is considered as the present value of

defined benefit obligations. The benefit plan is calculated annually by discounting future cash

flows using the “projected unit credit method” (Reckitt.com, 2021). Yield on high quality

corporate bond is used as the discounting rate. The industry follows the practice of recognising

DBP in BS as PV of DB obligations + actuarial gains – past service cost – fair value of plan

assets at the balance sheet. The company’s practice is quite in alignment with the industry and

thus is rational because it is based on IAS 19. The assumptions that Reckitt follows for their

defined pension benefit plan is realistic as these values are accrued over the employment period.

As an impact on the financial statement of these assumptions are recorded as past-service costs

in the statement for profit and loss.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

UMACTT-15-M 10

The discount rate on the assumptions of Reckitt’s “defined pension benefit plan” is by

computing the current value of the “future pension obligations”. This discount plan is realistic

as amount is determined after estimation of “expected rates of return” including margins acting

as a cushion to adverse deviations. The assumptions that are set by Reckitt are not different from

the historical data outcomes and industrial forecasts rather this company is seen to follow the

mentioned methodologies for making justified assumptions. In recent times, the “defined

pension benefit plan” amounted to £37 m in 2020 which was -£82 m in 2020 (Reckitt.com,

2021). The improvements taken place in pension benefit plans, certain re-measurements are

projected which have increased such fund values since the last years.

In the years 2019 and 2020, this pension fund was valued in negative figures however, this fund

value was assumed best in 2018 as £123 m (Londonstockexchange.com, 2022). The actual and

forecasted parameters for the “defined pension benefit plan” are assumed as the estimated

service life years for the current employees, assumptions in salary raises and the mortality rate

are forecasted.

The pension contribution to the plan are recorded as a pension expense and in “cash flow

statements”, and as annual contributions (Wsj.com, 2022). Therefore, a critical impact on the

financial performance is projected having a probable impact in future in terms of profitability of

the company getting lower. The interest paid on net pension plan is reported as finance expense

and thus affects the profitability of the company (Reckitt Annual Report & Account. 2021).

The discount rate on the assumptions of Reckitt’s “defined pension benefit plan” is by

computing the current value of the “future pension obligations”. This discount plan is realistic

as amount is determined after estimation of “expected rates of return” including margins acting

as a cushion to adverse deviations. The assumptions that are set by Reckitt are not different from

the historical data outcomes and industrial forecasts rather this company is seen to follow the

mentioned methodologies for making justified assumptions. In recent times, the “defined

pension benefit plan” amounted to £37 m in 2020 which was -£82 m in 2020 (Reckitt.com,

2021). The improvements taken place in pension benefit plans, certain re-measurements are

projected which have increased such fund values since the last years.

In the years 2019 and 2020, this pension fund was valued in negative figures however, this fund

value was assumed best in 2018 as £123 m (Londonstockexchange.com, 2022). The actual and

forecasted parameters for the “defined pension benefit plan” are assumed as the estimated

service life years for the current employees, assumptions in salary raises and the mortality rate

are forecasted.

The pension contribution to the plan are recorded as a pension expense and in “cash flow

statements”, and as annual contributions (Wsj.com, 2022). Therefore, a critical impact on the

financial performance is projected having a probable impact in future in terms of profitability of

the company getting lower. The interest paid on net pension plan is reported as finance expense

and thus affects the profitability of the company (Reckitt Annual Report & Account. 2021).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UMACTT-15-M 11

3. Conclusion

In summary, after the detailed discussions of the accounting policies of Reckitt it can be

concluded that the company has revealed useful and quality financial information. Reckitt has

disclosed the financial risk management protocols and accounting policies they are following

concerning pension benefit plans. Reckitt has also revealed essential facts about their impairment

policies in the generation of cash under IAS 36, IAS 39 and IFRS 9. Disclosure pertaining to

impairment of goodwill & financial instrument facilitate better assessment of company’s

management by investors & analysts. However, it also gives negative indication among investors

that managers have not made good investment choices. Also, greater financial risk and

impairment of assets disclosed in the financial statements gives an indication of business failures.

For instance, in the Reckitt’s financial statement, it has been identified that both in the year 2019

and 2020 the impairment of goodwill take place amounting to 5116 and 985 m respectively

while in the year 2021 there were no impairment of goodwill. This gives good indication among

investors with respect to reporting financial performance of the company as the company’s

choice for investment has improved.

3. Conclusion

In summary, after the detailed discussions of the accounting policies of Reckitt it can be

concluded that the company has revealed useful and quality financial information. Reckitt has

disclosed the financial risk management protocols and accounting policies they are following

concerning pension benefit plans. Reckitt has also revealed essential facts about their impairment

policies in the generation of cash under IAS 36, IAS 39 and IFRS 9. Disclosure pertaining to

impairment of goodwill & financial instrument facilitate better assessment of company’s

management by investors & analysts. However, it also gives negative indication among investors

that managers have not made good investment choices. Also, greater financial risk and

impairment of assets disclosed in the financial statements gives an indication of business failures.

For instance, in the Reckitt’s financial statement, it has been identified that both in the year 2019

and 2020 the impairment of goodwill take place amounting to 5116 and 985 m respectively

while in the year 2021 there were no impairment of goodwill. This gives good indication among

investors with respect to reporting financial performance of the company as the company’s

choice for investment has improved.

UMACTT-15-M 12

References

Elakova, A.A. (2020) Comparison of approaches to inventory valuation in RAS 5/2019 and ifrs 2

in the context of solving the problem of convergence of russian and international accounting

practices. Laplage em Revista [online], 6(Extra-B), pp.71-75. [Accessed on 04 April 2022].

Finance.yahoo.com, (2022) Reckitt Benckiser Group plc (RBGLY). Available from:

https://finance.yahoo.com/quote/RBGLY?ltr=1. [Accessed on 04 April 2022].

Kagwaini, D.M. (2019) The Role of IASB on Corporate Reporting Disclosures: Use of Artificial

Intelligence. [Accessed on 04 April 2022].

Londonstockexchange.com, (2022) Reckitt Benckiser Group Plc. Available from:

https://www.londonstockexchange.com/stock/RKT/reckitt-benckiser-group-plc/company-page

[Accessed on 04 April 2022].

Reckitt, (2020) Independent Auditor’s Report to the Members of Reckitt Benckiser Group plc.

Available from: https://www.reckitt.com/media/4089/financial-statements.pdf. [Accessed on 04

April 2022].

Reckitt.com (2021), Independent Auditor’s Report to the Members of Reckitt Benckiser Group

plc. Available from: https://www.reckitt.com/media/9219/reckitt-rns-h1-2021.pdf. [Accessed on

04 April 2022].

Reckitt.com, (2020) Reckitt Annual Report and Accounts 2020. Available from:

https://www.reckitt.com/media/8638/reckitt-annual-report-2020.pdf. [Accessed on 04 April

2022].

Tchaptchet, J.G.T. and Colot, O. (2019) Goodwill‘s Accounting Practices in Belgium and

Compliance with IAS 36 Required Disclosures. International Business Research [online], 12(3),

pp.139-152. [Accessed on 04 April 2022].

References

Elakova, A.A. (2020) Comparison of approaches to inventory valuation in RAS 5/2019 and ifrs 2

in the context of solving the problem of convergence of russian and international accounting

practices. Laplage em Revista [online], 6(Extra-B), pp.71-75. [Accessed on 04 April 2022].

Finance.yahoo.com, (2022) Reckitt Benckiser Group plc (RBGLY). Available from:

https://finance.yahoo.com/quote/RBGLY?ltr=1. [Accessed on 04 April 2022].

Kagwaini, D.M. (2019) The Role of IASB on Corporate Reporting Disclosures: Use of Artificial

Intelligence. [Accessed on 04 April 2022].

Londonstockexchange.com, (2022) Reckitt Benckiser Group Plc. Available from:

https://www.londonstockexchange.com/stock/RKT/reckitt-benckiser-group-plc/company-page

[Accessed on 04 April 2022].

Reckitt, (2020) Independent Auditor’s Report to the Members of Reckitt Benckiser Group plc.

Available from: https://www.reckitt.com/media/4089/financial-statements.pdf. [Accessed on 04

April 2022].

Reckitt.com (2021), Independent Auditor’s Report to the Members of Reckitt Benckiser Group

plc. Available from: https://www.reckitt.com/media/9219/reckitt-rns-h1-2021.pdf. [Accessed on

04 April 2022].

Reckitt.com, (2020) Reckitt Annual Report and Accounts 2020. Available from:

https://www.reckitt.com/media/8638/reckitt-annual-report-2020.pdf. [Accessed on 04 April

2022].

Tchaptchet, J.G.T. and Colot, O. (2019) Goodwill‘s Accounting Practices in Belgium and

Compliance with IAS 36 Required Disclosures. International Business Research [online], 12(3),

pp.139-152. [Accessed on 04 April 2022].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15