Financial Analysis of Business Transactions: An Accounting Report

VerifiedAdded on 2022/12/29

|13

|2482

|21

Report

AI Summary

This report delves into the core principles of accounting, starting with the meticulous process of recording business transactions through journal entries and the subsequent preparation of ledgers and trial balances. It then moves on to the formulation of key financial statements, including the income statement and balance sheet, providing a comprehensive view of a business's financial position. Furthermore, the report extends to the analysis of financial performance by calculating and interpreting various financial ratios, such as net profit ratio, gross profit ratio, current ratio, quick ratio, accounts receivable turnover, and accounts payable turnover. These ratios are then used to compare the performance of Linda's business with industry standards, providing insights into areas of strength and areas needing improvement. The report also includes a brief discussion on the treatment of drawings in accounting. The report aims to demonstrate how accounting tools are used to record, manage, and present business transactions to stakeholders. This report is available on Desklib which provides past papers and assignments.

Recording business transaction

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

PART A.................................................................................................................................................3

a) Journal..........................................................................................................................................3

b) Preparation of ledger...................................................................................................................4

c) Trial balance.................................................................................................................................7

d) Formulation of income statement................................................................................................8

e) Preparation of balance sheet .......................................................................................................8

f) brief description about drawing .................................................................................................9

PART B.................................................................................................................................................9

b)Analysis and compare financial performance of Linda's business with industries performance

.......................................................................................................................................................10

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................12

INTRODUCTION................................................................................................................................3

PART A.................................................................................................................................................3

a) Journal..........................................................................................................................................3

b) Preparation of ledger...................................................................................................................4

c) Trial balance.................................................................................................................................7

d) Formulation of income statement................................................................................................8

e) Preparation of balance sheet .......................................................................................................8

f) brief description about drawing .................................................................................................9

PART B.................................................................................................................................................9

b)Analysis and compare financial performance of Linda's business with industries performance

.......................................................................................................................................................10

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................12

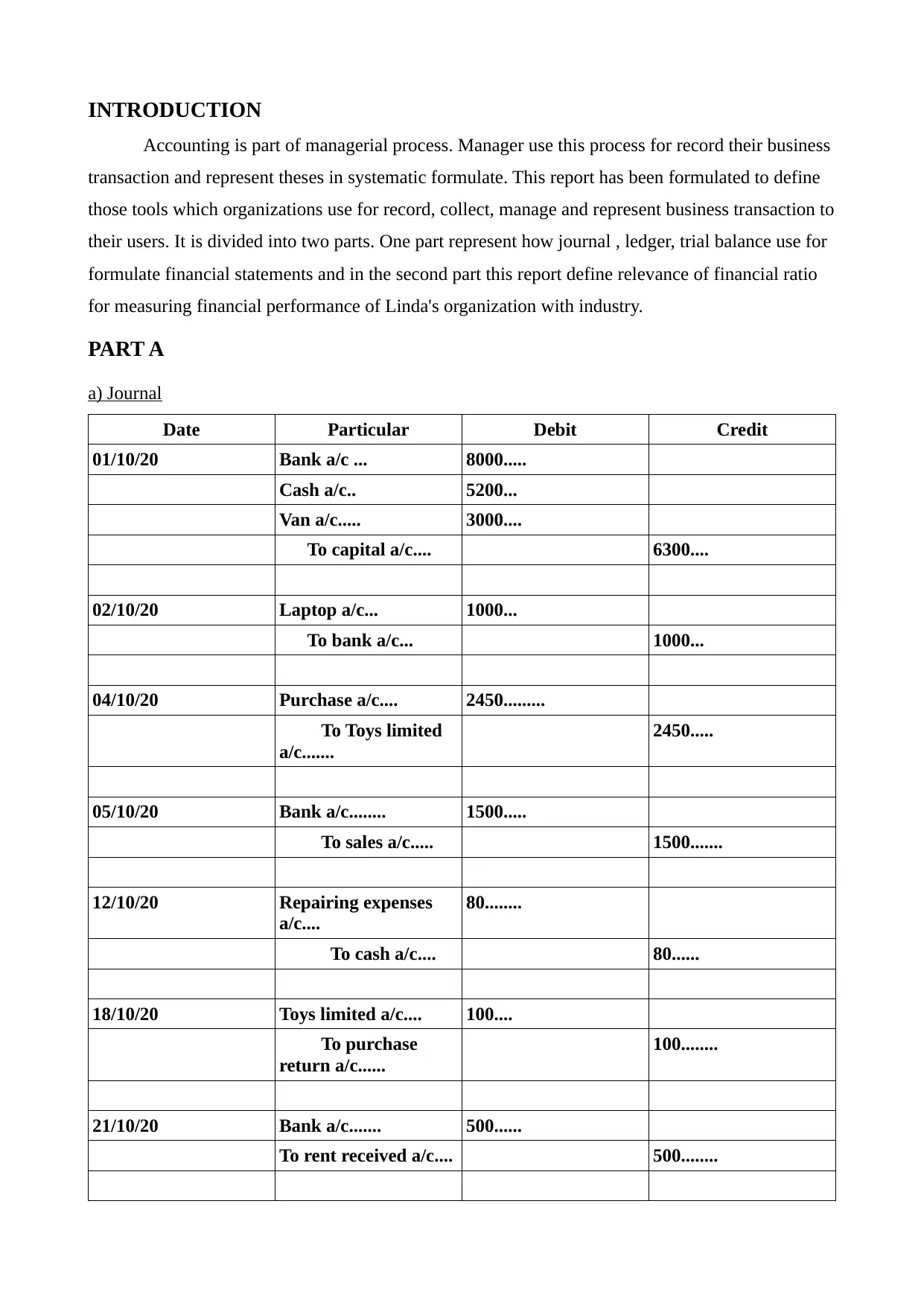

INTRODUCTION

Accounting is part of managerial process. Manager use this process for record their business

transaction and represent theses in systematic formulate. This report has been formulated to define

those tools which organizations use for record, collect, manage and represent business transaction to

their users. It is divided into two parts. One part represent how journal , ledger, trial balance use for

formulate financial statements and in the second part this report define relevance of financial ratio

for measuring financial performance of Linda's organization with industry.

PART A

a) Journal

Date Particular Debit Credit

01/10/20 Bank a/c ... 8000.....

Cash a/c.. 5200...

Van a/c..... 3000....

To capital a/c.... 6300....

02/10/20 Laptop a/c... 1000...

To bank a/c... 1000...

04/10/20 Purchase a/c.... 2450.........

To Toys limited

a/c.......

2450.....

05/10/20 Bank a/c........ 1500.....

To sales a/c..... 1500.......

12/10/20 Repairing expenses

a/c....

80........

To cash a/c.... 80......

18/10/20 Toys limited a/c.... 100....

To purchase

return a/c......

100........

21/10/20 Bank a/c....... 500......

To rent received a/c.... 500........

Accounting is part of managerial process. Manager use this process for record their business

transaction and represent theses in systematic formulate. This report has been formulated to define

those tools which organizations use for record, collect, manage and represent business transaction to

their users. It is divided into two parts. One part represent how journal , ledger, trial balance use for

formulate financial statements and in the second part this report define relevance of financial ratio

for measuring financial performance of Linda's organization with industry.

PART A

a) Journal

Date Particular Debit Credit

01/10/20 Bank a/c ... 8000.....

Cash a/c.. 5200...

Van a/c..... 3000....

To capital a/c.... 6300....

02/10/20 Laptop a/c... 1000...

To bank a/c... 1000...

04/10/20 Purchase a/c.... 2450.........

To Toys limited

a/c.......

2450.....

05/10/20 Bank a/c........ 1500.....

To sales a/c..... 1500.......

12/10/20 Repairing expenses

a/c....

80........

To cash a/c.... 80......

18/10/20 Toys limited a/c.... 100....

To purchase

return a/c......

100........

21/10/20 Bank a/c....... 500......

To rent received a/c.... 500........

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

23/10/20 Cash a/c...... 1500.....

Fred a/c... 400....

To sales a/c …... 1900....

21/10/20 Cash a/c... 500...

To sales a/c.. 500......

24/10/20 Car a/c... 2500..

To bank a/c... 2500.

26/10/20 Wages a/c...... 820...

To bank a/c.. 820.......

30/10/20 Rent a/c... 1000......

To bank a/c...... 1000

31/10/20 Drawing a/c... 1600..

To bank a/c.... 1600..

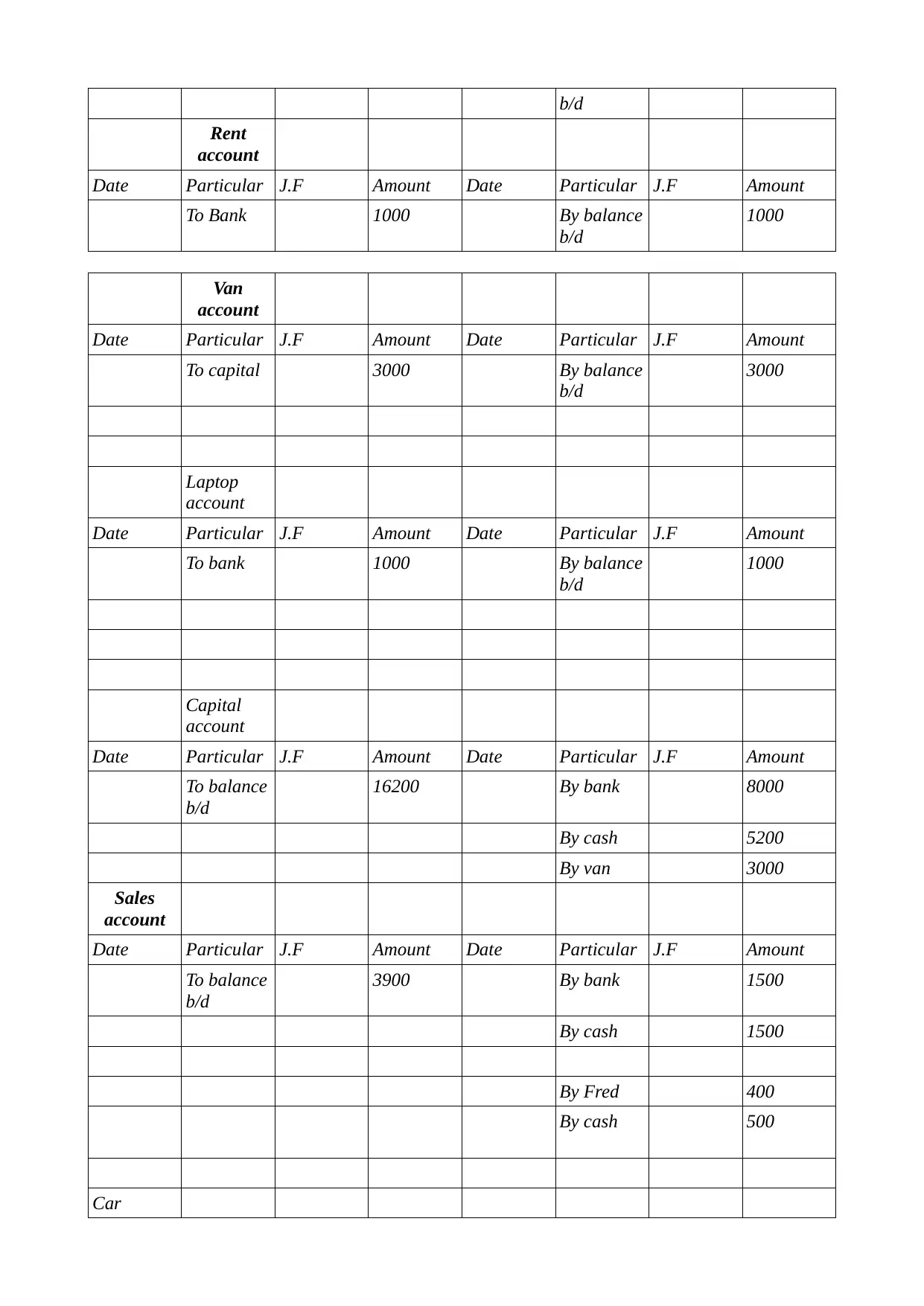

b) Preparation of ledger

Bank

account

Date Particular J.F Amount Date Particular J.F Amount

To capital 8000

To sales 1500 By laptop 1000

To rent

received

500 By Car 2500

By wages 820

By Rent 1000

By

drawing

1600

By balance

c/d

3080

10000 10000

Cash

account

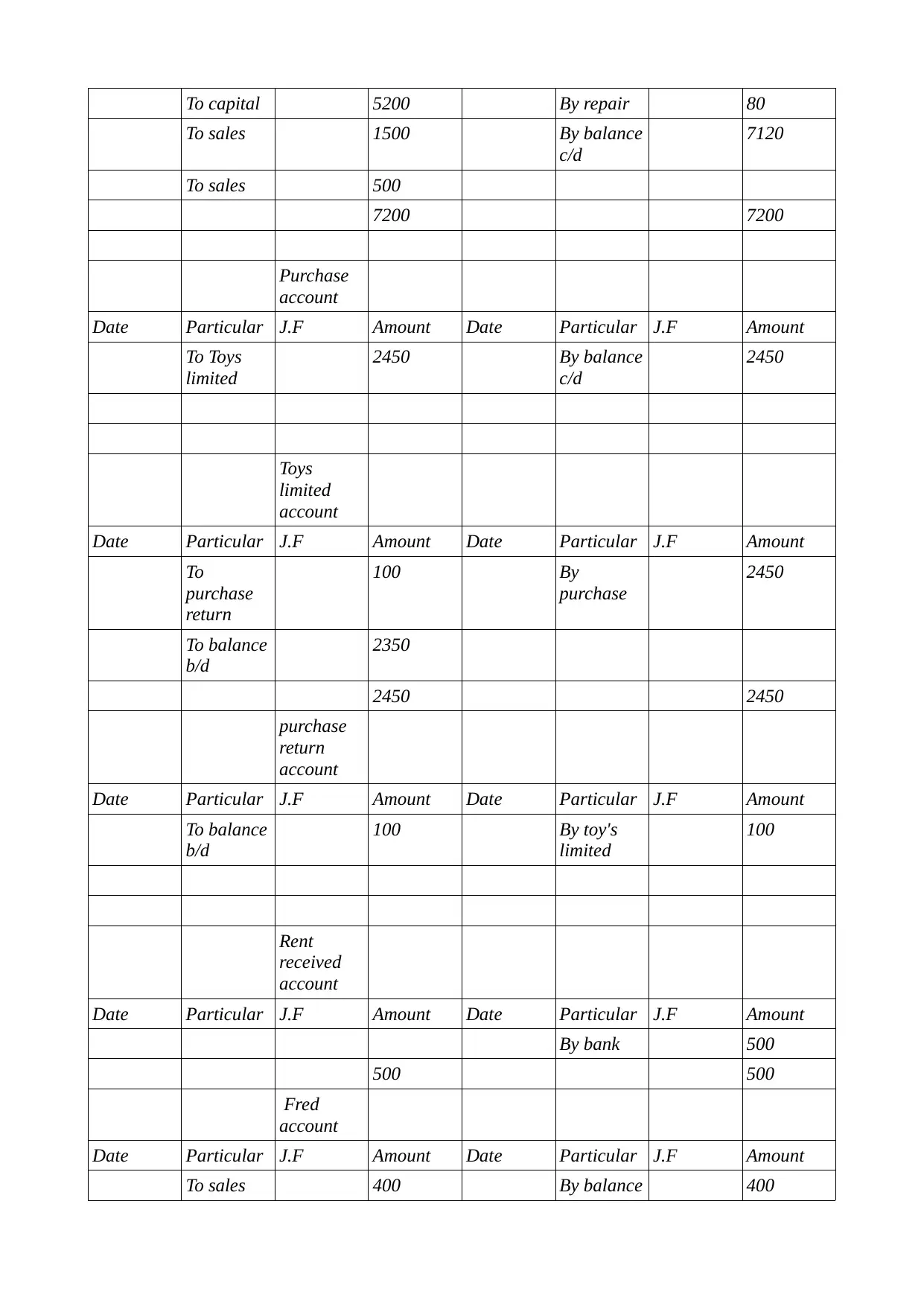

Date Particular J.F Amount Date Particular J.F Amount

Fred a/c... 400....

To sales a/c …... 1900....

21/10/20 Cash a/c... 500...

To sales a/c.. 500......

24/10/20 Car a/c... 2500..

To bank a/c... 2500.

26/10/20 Wages a/c...... 820...

To bank a/c.. 820.......

30/10/20 Rent a/c... 1000......

To bank a/c...... 1000

31/10/20 Drawing a/c... 1600..

To bank a/c.... 1600..

b) Preparation of ledger

Bank

account

Date Particular J.F Amount Date Particular J.F Amount

To capital 8000

To sales 1500 By laptop 1000

To rent

received

500 By Car 2500

By wages 820

By Rent 1000

By

drawing

1600

By balance

c/d

3080

10000 10000

Cash

account

Date Particular J.F Amount Date Particular J.F Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To capital 5200 By repair 80

To sales 1500 By balance

c/d

7120

To sales 500

7200 7200

Purchase

account

Date Particular J.F Amount Date Particular J.F Amount

To Toys

limited

2450 By balance

c/d

2450

Toys

limited

account

Date Particular J.F Amount Date Particular J.F Amount

To

purchase

return

100 By

purchase

2450

To balance

b/d

2350

2450 2450

purchase

return

account

Date Particular J.F Amount Date Particular J.F Amount

To balance

b/d

100 By toy's

limited

100

Rent

received

account

Date Particular J.F Amount Date Particular J.F Amount

By bank 500

500 500

Fred

account

Date Particular J.F Amount Date Particular J.F Amount

To sales 400 By balance 400

To sales 1500 By balance

c/d

7120

To sales 500

7200 7200

Purchase

account

Date Particular J.F Amount Date Particular J.F Amount

To Toys

limited

2450 By balance

c/d

2450

Toys

limited

account

Date Particular J.F Amount Date Particular J.F Amount

To

purchase

return

100 By

purchase

2450

To balance

b/d

2350

2450 2450

purchase

return

account

Date Particular J.F Amount Date Particular J.F Amount

To balance

b/d

100 By toy's

limited

100

Rent

received

account

Date Particular J.F Amount Date Particular J.F Amount

By bank 500

500 500

Fred

account

Date Particular J.F Amount Date Particular J.F Amount

To sales 400 By balance 400

b/d

Rent

account

Date Particular J.F Amount Date Particular J.F Amount

To Bank 1000 By balance

b/d

1000

Van

account

Date Particular J.F Amount Date Particular J.F Amount

To capital 3000 By balance

b/d

3000

Laptop

account

Date Particular J.F Amount Date Particular J.F Amount

To bank 1000 By balance

b/d

1000

Capital

account

Date Particular J.F Amount Date Particular J.F Amount

To balance

b/d

16200 By bank 8000

By cash 5200

By van 3000

Sales

account

Date Particular J.F Amount Date Particular J.F Amount

To balance

b/d

3900 By bank 1500

By cash 1500

By Fred 400

By cash 500

Car

Rent

account

Date Particular J.F Amount Date Particular J.F Amount

To Bank 1000 By balance

b/d

1000

Van

account

Date Particular J.F Amount Date Particular J.F Amount

To capital 3000 By balance

b/d

3000

Laptop

account

Date Particular J.F Amount Date Particular J.F Amount

To bank 1000 By balance

b/d

1000

Capital

account

Date Particular J.F Amount Date Particular J.F Amount

To balance

b/d

16200 By bank 8000

By cash 5200

By van 3000

Sales

account

Date Particular J.F Amount Date Particular J.F Amount

To balance

b/d

3900 By bank 1500

By cash 1500

By Fred 400

By cash 500

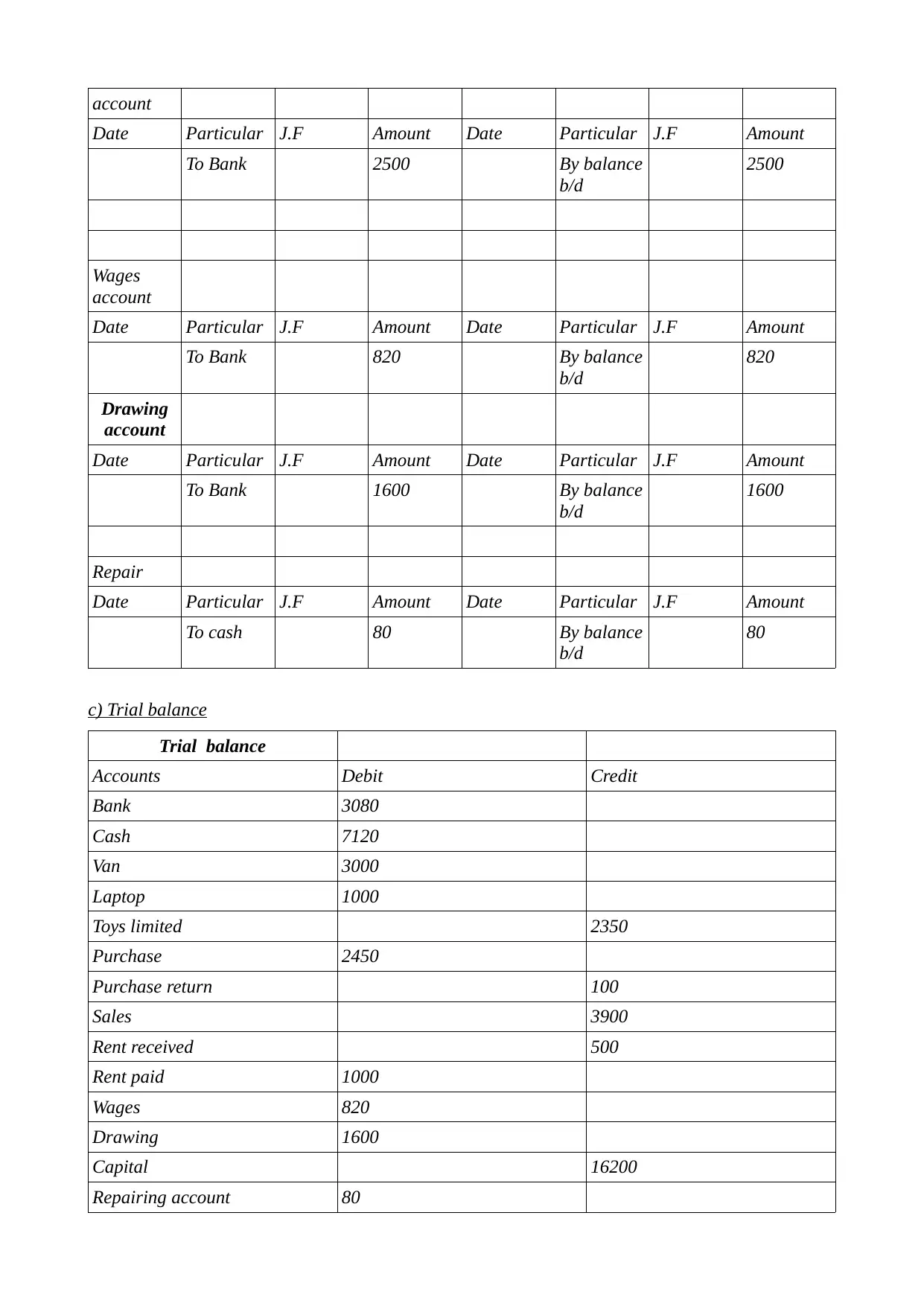

Car

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

account

Date Particular J.F Amount Date Particular J.F Amount

To Bank 2500 By balance

b/d

2500

Wages

account

Date Particular J.F Amount Date Particular J.F Amount

To Bank 820 By balance

b/d

820

Drawing

account

Date Particular J.F Amount Date Particular J.F Amount

To Bank 1600 By balance

b/d

1600

Repair

Date Particular J.F Amount Date Particular J.F Amount

To cash 80 By balance

b/d

80

c) Trial balance

Trial balance

Accounts Debit Credit

Bank 3080

Cash 7120

Van 3000

Laptop 1000

Toys limited 2350

Purchase 2450

Purchase return 100

Sales 3900

Rent received 500

Rent paid 1000

Wages 820

Drawing 1600

Capital 16200

Repairing account 80

Date Particular J.F Amount Date Particular J.F Amount

To Bank 2500 By balance

b/d

2500

Wages

account

Date Particular J.F Amount Date Particular J.F Amount

To Bank 820 By balance

b/d

820

Drawing

account

Date Particular J.F Amount Date Particular J.F Amount

To Bank 1600 By balance

b/d

1600

Repair

Date Particular J.F Amount Date Particular J.F Amount

To cash 80 By balance

b/d

80

c) Trial balance

Trial balance

Accounts Debit Credit

Bank 3080

Cash 7120

Van 3000

Laptop 1000

Toys limited 2350

Purchase 2450

Purchase return 100

Sales 3900

Rent received 500

Rent paid 1000

Wages 820

Drawing 1600

Capital 16200

Repairing account 80

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

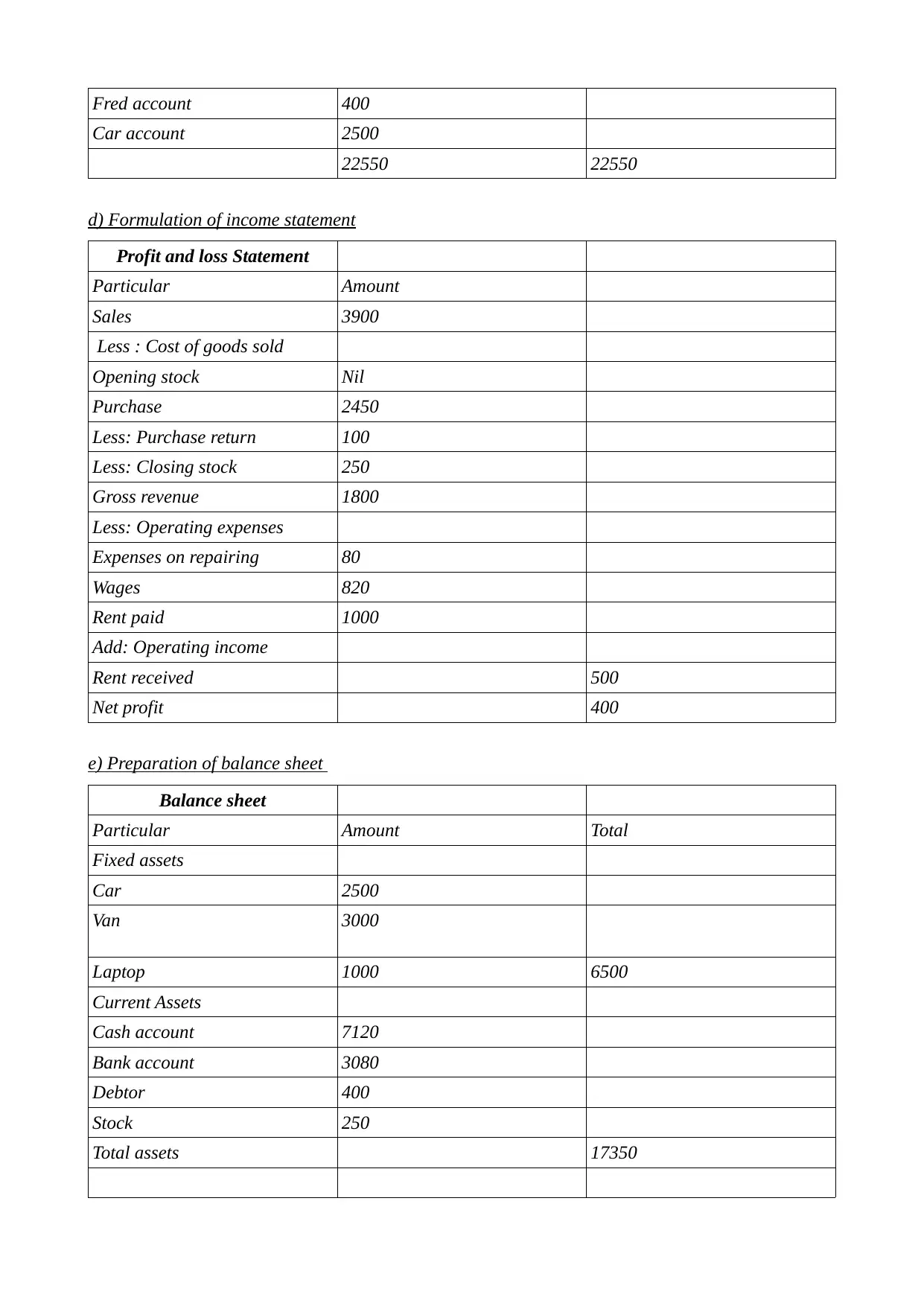

Fred account 400

Car account 2500

22550 22550

d) Formulation of income statement

Profit and loss Statement

Particular Amount

Sales 3900

Less : Cost of goods sold

Opening stock Nil

Purchase 2450

Less: Purchase return 100

Less: Closing stock 250

Gross revenue 1800

Less: Operating expenses

Expenses on repairing 80

Wages 820

Rent paid 1000

Add: Operating income

Rent received 500

Net profit 400

e) Preparation of balance sheet

Balance sheet

Particular Amount Total

Fixed assets

Car 2500

Van 3000

Laptop 1000 6500

Current Assets

Cash account 7120

Bank account 3080

Debtor 400

Stock 250

Total assets 17350

Car account 2500

22550 22550

d) Formulation of income statement

Profit and loss Statement

Particular Amount

Sales 3900

Less : Cost of goods sold

Opening stock Nil

Purchase 2450

Less: Purchase return 100

Less: Closing stock 250

Gross revenue 1800

Less: Operating expenses

Expenses on repairing 80

Wages 820

Rent paid 1000

Add: Operating income

Rent received 500

Net profit 400

e) Preparation of balance sheet

Balance sheet

Particular Amount Total

Fixed assets

Car 2500

Van 3000

Laptop 1000 6500

Current Assets

Cash account 7120

Bank account 3080

Debtor 400

Stock 250

Total assets 17350

Equity and liabilities

Equity

Capital 16200

Less: Drawing 1600 14600

Retain earnings 400

Current liabilities

Toys limited account 2350

Total equities and liabilities 17350

f) brief description about drawing

Accounting in general term use for recording each and every business transaction which

directly and indirectly impacted on business performance. Various accounts are formulated to

systematically manage and record business transaction which further help in managing business

cash assets. When individual withdraw money from business bank account and they use this only

for their personal use then these types of business transaction is recorded in drawing account

(Hoyos and Nunez-del-Prado, 2018).

This account is formulated for control insider business trading activities as personal take

unfair trade advantages by using business money. Amount of drawing is deducted from capital

account and in case if individual use goods for their person use then value of these goods are

deducted from stock account. In this case Linda use its money from their business account to go on

holiday trip, this trip will not be beneficial for their organization as the main motive of this trip is to

reduce her stress thus expenses incurred for holiday trip is treated and includes in drawing account.

This amount will be deducted from capital account.

PART B

Calculation of financial ratio.

Particular Formula Linda

organization

Industry ratio

Net profit ratio Net profit/ Net

sales*100

400/3900*100 10.26% 31

Gross profit ratio Gross profit/ Net

revenue* 100

1800/3900*100 46.15% 54

Current ratio Current assets / 10850/ 2350 4.62 2.8

Equity

Capital 16200

Less: Drawing 1600 14600

Retain earnings 400

Current liabilities

Toys limited account 2350

Total equities and liabilities 17350

f) brief description about drawing

Accounting in general term use for recording each and every business transaction which

directly and indirectly impacted on business performance. Various accounts are formulated to

systematically manage and record business transaction which further help in managing business

cash assets. When individual withdraw money from business bank account and they use this only

for their personal use then these types of business transaction is recorded in drawing account

(Hoyos and Nunez-del-Prado, 2018).

This account is formulated for control insider business trading activities as personal take

unfair trade advantages by using business money. Amount of drawing is deducted from capital

account and in case if individual use goods for their person use then value of these goods are

deducted from stock account. In this case Linda use its money from their business account to go on

holiday trip, this trip will not be beneficial for their organization as the main motive of this trip is to

reduce her stress thus expenses incurred for holiday trip is treated and includes in drawing account.

This amount will be deducted from capital account.

PART B

Calculation of financial ratio.

Particular Formula Linda

organization

Industry ratio

Net profit ratio Net profit/ Net

sales*100

400/3900*100 10.26% 31

Gross profit ratio Gross profit/ Net

revenue* 100

1800/3900*100 46.15% 54

Current ratio Current assets / 10850/ 2350 4.62 2.8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current liabilities

Quick ratio Quick assets /

Current liabilities

10600/2350 4.51 1.5

Account

receivable

collection period

Sales/ Average

account

receivables*365

3900/400*365 37.44 days Gross profit ratio

Account payable

ratio

Average payable/

Average creditors

2450/2350*365 350 days 72 days

b)Analysis and compare financial performance of Linda's business with industries performance

Financial ratio are part of financial management, this technique is used for , measure

performance of organization on the basis of calculating relation between two variables of financial

statements. Following are some ratio through which help in measure financial performance of Linda

and industries

Net profit ratio: Organizations use net profit ratio to measure their level of profitability . On

the basis of that they can able to recognize the value of net profit an organization can

generate by selling their products. This ratio define relationship between net profit with sales

(Ryoo, 2017).

Higher net profit ratio showcase high rate of efficiency level that an organization have to attract

and influence their customers to buy products. Which will useful in raise profitability rate of

organization. In this case, net profit ratio of Linda's organization is valued at 10.26 % and on the

other side value of net profit of industries was valued at 31 % which means that as compare to

Linda industries able to generate more net profit. Linda need to focus on implement their selling

strategy through which she can able to improve profitability rate of their businesses.

Gross profit ratio: This ratio is calculated to showcase relation between gross profit with

sales. This is useful to assess financial health of business by evaluating or measuring

relationship with gross profit ratio. This ratio define ability of organization to generate profit

before adjustment of any kind of operating and selling business expenses. Higher ratio

represent better position of organization. Linda's organization generate 46 % of gross profit

ratio and on the other side 54% gross profit ratio measure of industries which represent that

Linda's business's not able to generate high rate of gross profit ratio which showcase that

Quick ratio Quick assets /

Current liabilities

10600/2350 4.51 1.5

Account

receivable

collection period

Sales/ Average

account

receivables*365

3900/400*365 37.44 days Gross profit ratio

Account payable

ratio

Average payable/

Average creditors

2450/2350*365 350 days 72 days

b)Analysis and compare financial performance of Linda's business with industries performance

Financial ratio are part of financial management, this technique is used for , measure

performance of organization on the basis of calculating relation between two variables of financial

statements. Following are some ratio through which help in measure financial performance of Linda

and industries

Net profit ratio: Organizations use net profit ratio to measure their level of profitability . On

the basis of that they can able to recognize the value of net profit an organization can

generate by selling their products. This ratio define relationship between net profit with sales

(Ryoo, 2017).

Higher net profit ratio showcase high rate of efficiency level that an organization have to attract

and influence their customers to buy products. Which will useful in raise profitability rate of

organization. In this case, net profit ratio of Linda's organization is valued at 10.26 % and on the

other side value of net profit of industries was valued at 31 % which means that as compare to

Linda industries able to generate more net profit. Linda need to focus on implement their selling

strategy through which she can able to improve profitability rate of their businesses.

Gross profit ratio: This ratio is calculated to showcase relation between gross profit with

sales. This is useful to assess financial health of business by evaluating or measuring

relationship with gross profit ratio. This ratio define ability of organization to generate profit

before adjustment of any kind of operating and selling business expenses. Higher ratio

represent better position of organization. Linda's organization generate 46 % of gross profit

ratio and on the other side 54% gross profit ratio measure of industries which represent that

Linda's business's not able to generate high rate of gross profit ratio which showcase that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organization need to focus on their trading business strategies to increase rate of gross profit

ratio.

This ratio help in define the rate of gearing profit on the basis of selling their business products.

Value of gross profit is help in maintaining net profit ratio as this value is use by organizations to

deduct or bear all the essential business operating expenses. Thus business organizations focus on

enhance the rate of their gross [profit ratio.

Current ratio:This ratio measure the relation between current asset with current business

liabilities, through which manager can analysis ability of organization to pay their current

debt by using their current business assets (Tsai, Wang, Ting and Hong, 2020). Current

ratio help in recognize liquid business position of organization which used for manage

balance of working capital.

The value of current ratio was measure at 4.62 of Linda's organization and on the other hand in

industries, current ratio was measure at 2.5 % which means that industry as well as Linda's business

able to fulfil their debt liabilities within given time by using their current assets resource however

Linda's current ratio is comparatively high then ideal current ratio which is 2 :1 , which depicts that

Linda need to manage their current assets to control the wastage use of theses assets. Quick ratio: This ratio define the ration between quick asset and current liability. Qui9ck

assets include only cash and cash relevance assets. Higher ratio showcase high rate of

liquidity and efficiency to manage their cash assets. Value of quick ratio of Linda's

organization was 4.51 and on the other side industrial ratio valued at 1.35 which showcase

that Lind's business is in much better position in fulfil their debt liability as they have

comparatively more cash assets to fulfil their current debt business liability (Wangerin,

2019). Account receivables ratio: This ratio is calculated to define required by organizations to

collect money from their debtors for selling their products at credit rate. Long time of

account receivable ratio showcase that organization require more time for collection of

money and vice versa. In this case Linda's account receivable ratio is valued at 37 days and

Industries valued at 50 days which showcase that as compare to financial performance

Linda' s organization is able to receive money from their debtors in less time as compare to

industry. Linda use effective management policies which help in influence their debtors to

fulfill their debt liability in short time period.

Account payable ratio: This ratio is useful for recognize financial performance of business

entities by recognize time required by organizations to pay their creditors. It is define

relationship between credit sales and average account payable. Long time required showcase

that organization need to take more time for fulfil their debt liability. In this case Linda's

ratio.

This ratio help in define the rate of gearing profit on the basis of selling their business products.

Value of gross profit is help in maintaining net profit ratio as this value is use by organizations to

deduct or bear all the essential business operating expenses. Thus business organizations focus on

enhance the rate of their gross [profit ratio.

Current ratio:This ratio measure the relation between current asset with current business

liabilities, through which manager can analysis ability of organization to pay their current

debt by using their current business assets (Tsai, Wang, Ting and Hong, 2020). Current

ratio help in recognize liquid business position of organization which used for manage

balance of working capital.

The value of current ratio was measure at 4.62 of Linda's organization and on the other hand in

industries, current ratio was measure at 2.5 % which means that industry as well as Linda's business

able to fulfil their debt liabilities within given time by using their current assets resource however

Linda's current ratio is comparatively high then ideal current ratio which is 2 :1 , which depicts that

Linda need to manage their current assets to control the wastage use of theses assets. Quick ratio: This ratio define the ration between quick asset and current liability. Qui9ck

assets include only cash and cash relevance assets. Higher ratio showcase high rate of

liquidity and efficiency to manage their cash assets. Value of quick ratio of Linda's

organization was 4.51 and on the other side industrial ratio valued at 1.35 which showcase

that Lind's business is in much better position in fulfil their debt liability as they have

comparatively more cash assets to fulfil their current debt business liability (Wangerin,

2019). Account receivables ratio: This ratio is calculated to define required by organizations to

collect money from their debtors for selling their products at credit rate. Long time of

account receivable ratio showcase that organization require more time for collection of

money and vice versa. In this case Linda's account receivable ratio is valued at 37 days and

Industries valued at 50 days which showcase that as compare to financial performance

Linda' s organization is able to receive money from their debtors in less time as compare to

industry. Linda use effective management policies which help in influence their debtors to

fulfill their debt liability in short time period.

Account payable ratio: This ratio is useful for recognize financial performance of business

entities by recognize time required by organizations to pay their creditors. It is define

relationship between credit sales and average account payable. Long time required showcase

that organization need to take more time for fulfil their debt liability. In this case Linda's

organization took 350 days in order to fulfil their current debt ability and on the other side

industries took 72 days in order to fulfill their debt business ability. Theses ratio are useful to

represent credit enterprise performance which useful for represent organization 's position

in running business environment. On the basis of calculating this ratio it analysis that Linda'

organization took long time which showcase that they face cash liquidity issue or working

capital related problem thus they are not able to fulfil their debt liability. They need to start

working on formulating those policies wand control wastage of accessibility of current asset

to manage their account payable ratio.

From the evaluation of all the financial ratio it recognized that Linda need to work on her

organizations operational businesses and financial policies in order to maintain its liquid position as

well as increase profitability business rate. Only then they can able to maintain sustainability of

their organization in market and enhance their financial performance as compare with their rival

business companies (Zaza, Bimonte, Faccilongo, La Sala, Contò and Gallo, 2018)

CONCLUSION

From the above analysis it has been concluded that accounting is essential part of

management process. Through accounting procedure, organization able to collect , record and

manage their monetary business transaction by formulating , trial balance and financial statements,

theses statements. Theses statement help in formulating or calculating financial ratio through which

manager able to recognizance or measure performance of their business organization for specific

period of time and able to compare it with other organization to evaluate their position in market

economy.

industries took 72 days in order to fulfill their debt business ability. Theses ratio are useful to

represent credit enterprise performance which useful for represent organization 's position

in running business environment. On the basis of calculating this ratio it analysis that Linda'

organization took long time which showcase that they face cash liquidity issue or working

capital related problem thus they are not able to fulfil their debt liability. They need to start

working on formulating those policies wand control wastage of accessibility of current asset

to manage their account payable ratio.

From the evaluation of all the financial ratio it recognized that Linda need to work on her

organizations operational businesses and financial policies in order to maintain its liquid position as

well as increase profitability business rate. Only then they can able to maintain sustainability of

their organization in market and enhance their financial performance as compare with their rival

business companies (Zaza, Bimonte, Faccilongo, La Sala, Contò and Gallo, 2018)

CONCLUSION

From the above analysis it has been concluded that accounting is essential part of

management process. Through accounting procedure, organization able to collect , record and

manage their monetary business transaction by formulating , trial balance and financial statements,

theses statements. Theses statement help in formulating or calculating financial ratio through which

manager able to recognizance or measure performance of their business organization for specific

period of time and able to compare it with other organization to evaluate their position in market

economy.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.