Recording Business Transactions and Financial Statement Preparation

VerifiedAdded on 2023/06/14

|12

|1294

|230

Practical Assignment

AI Summary

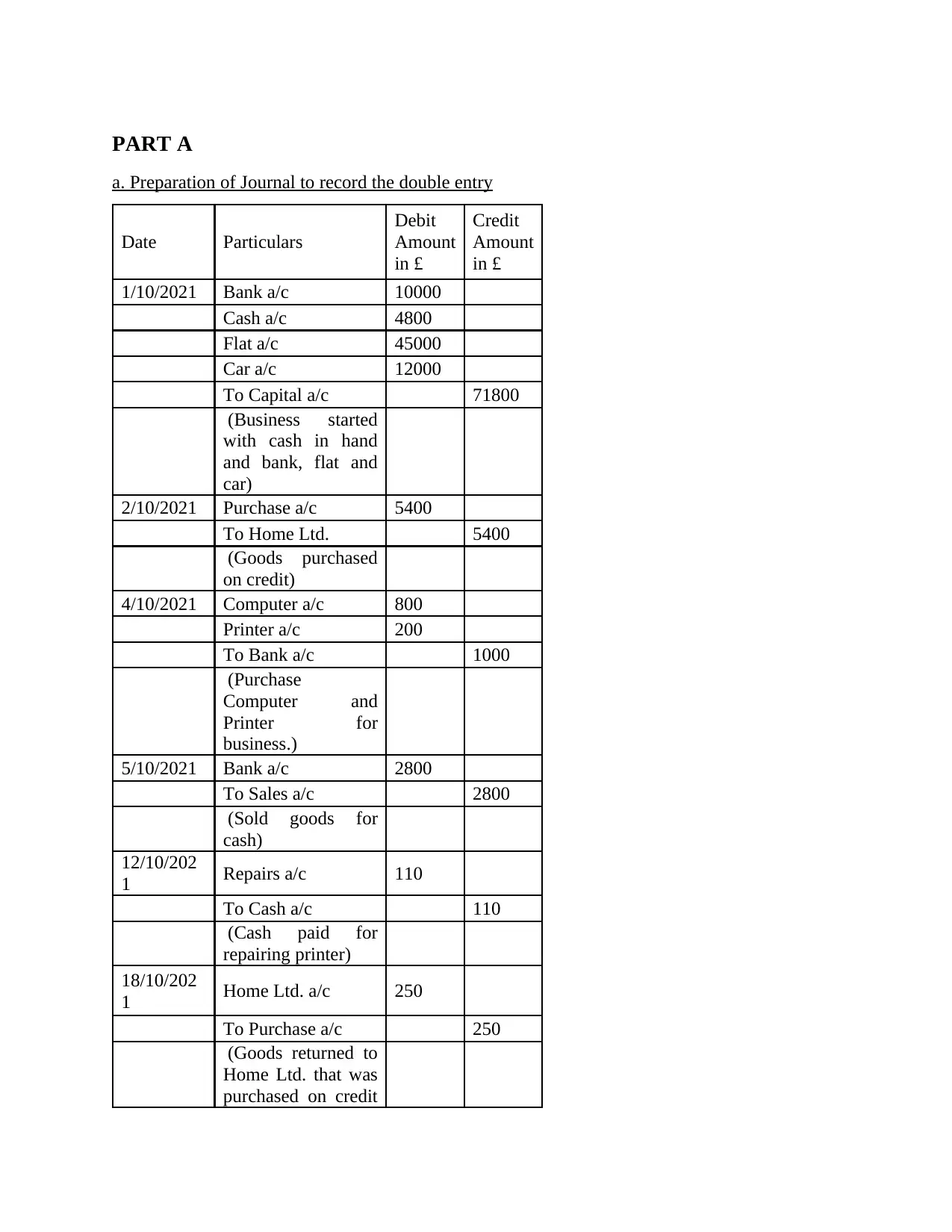

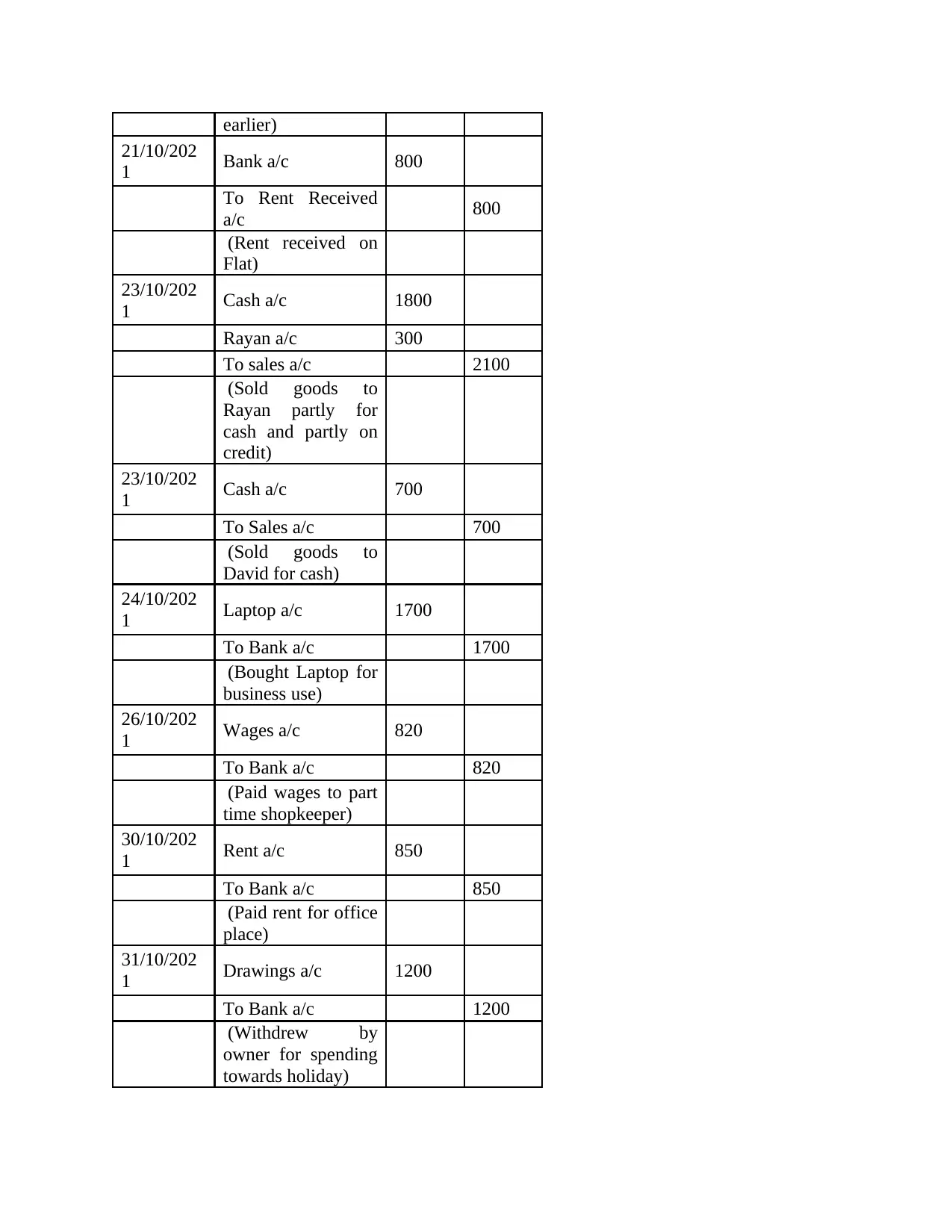

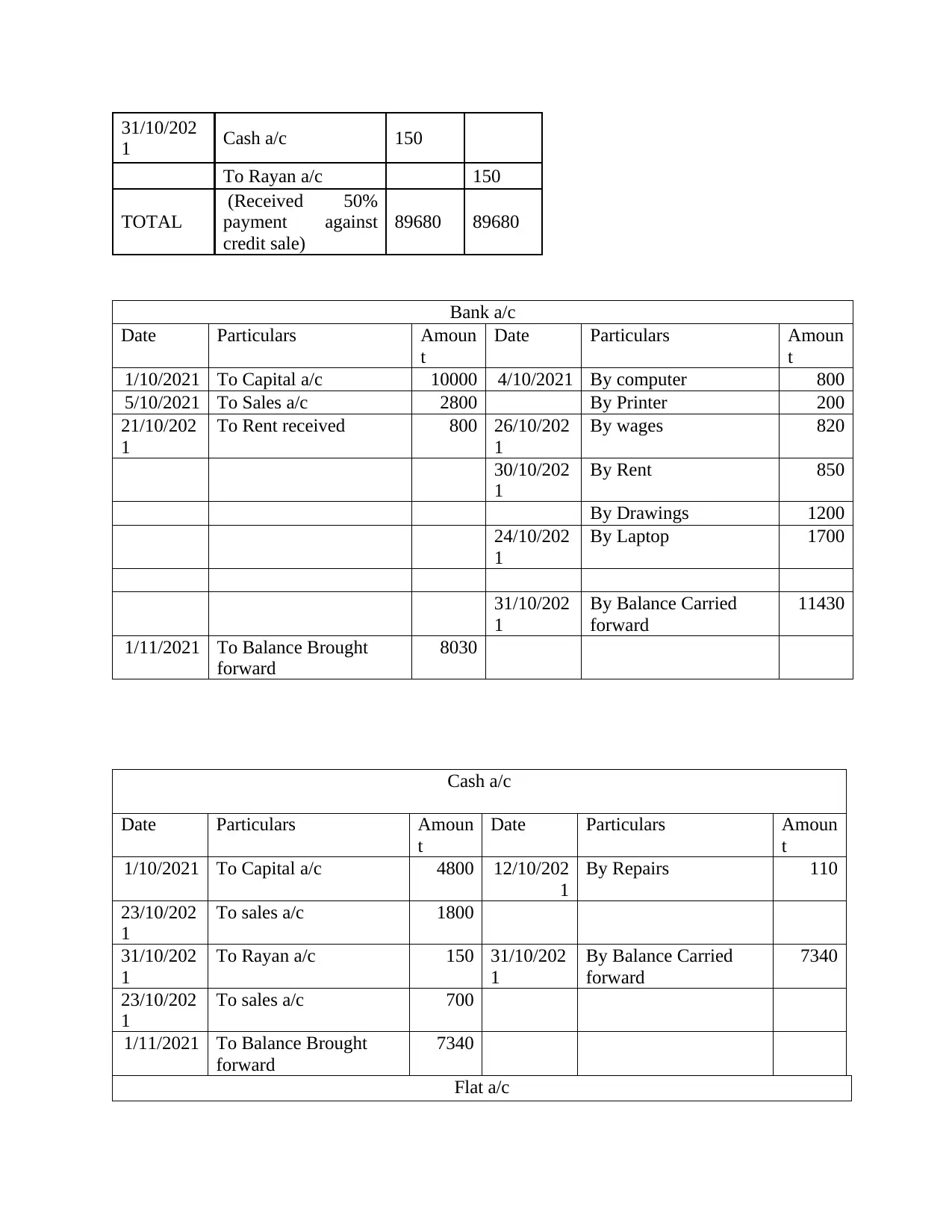

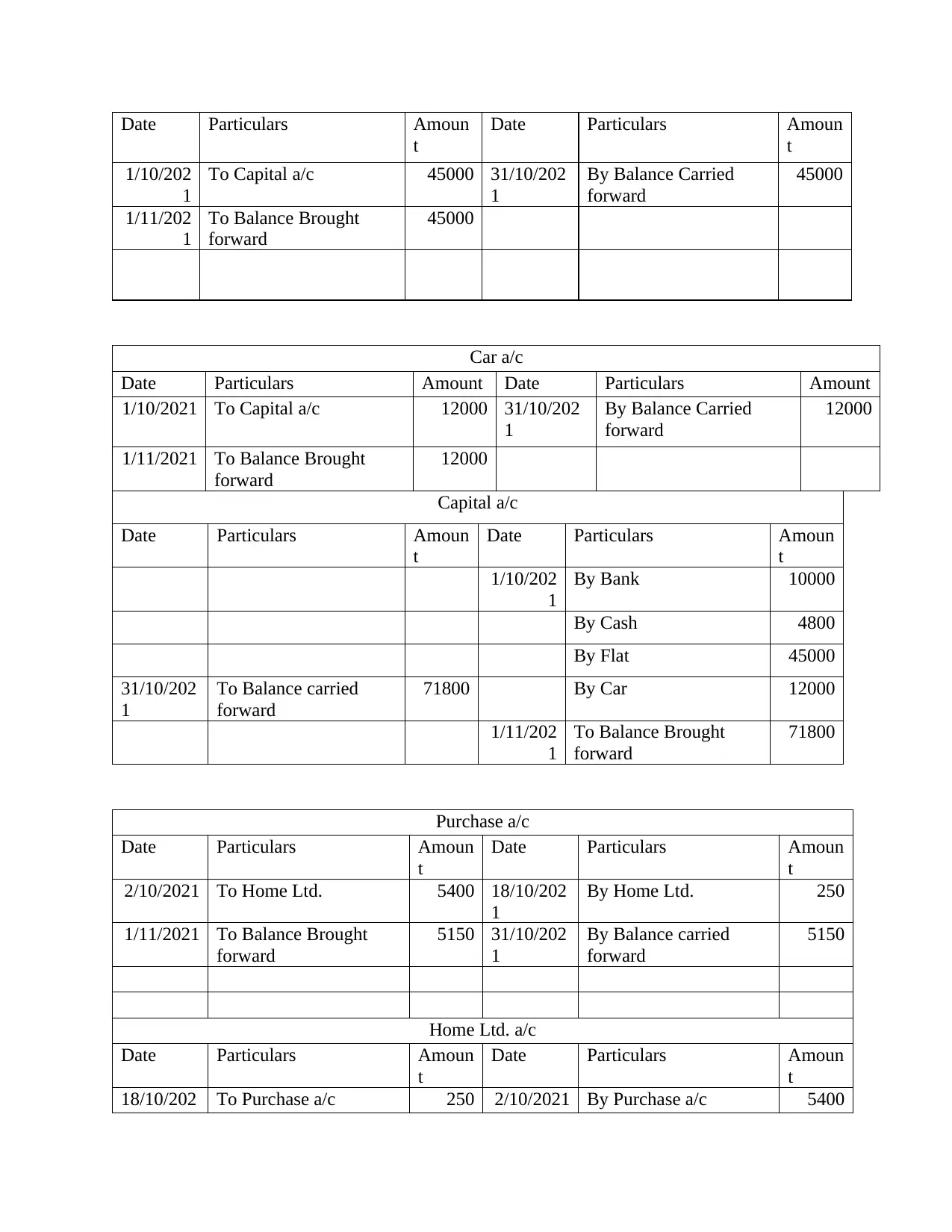

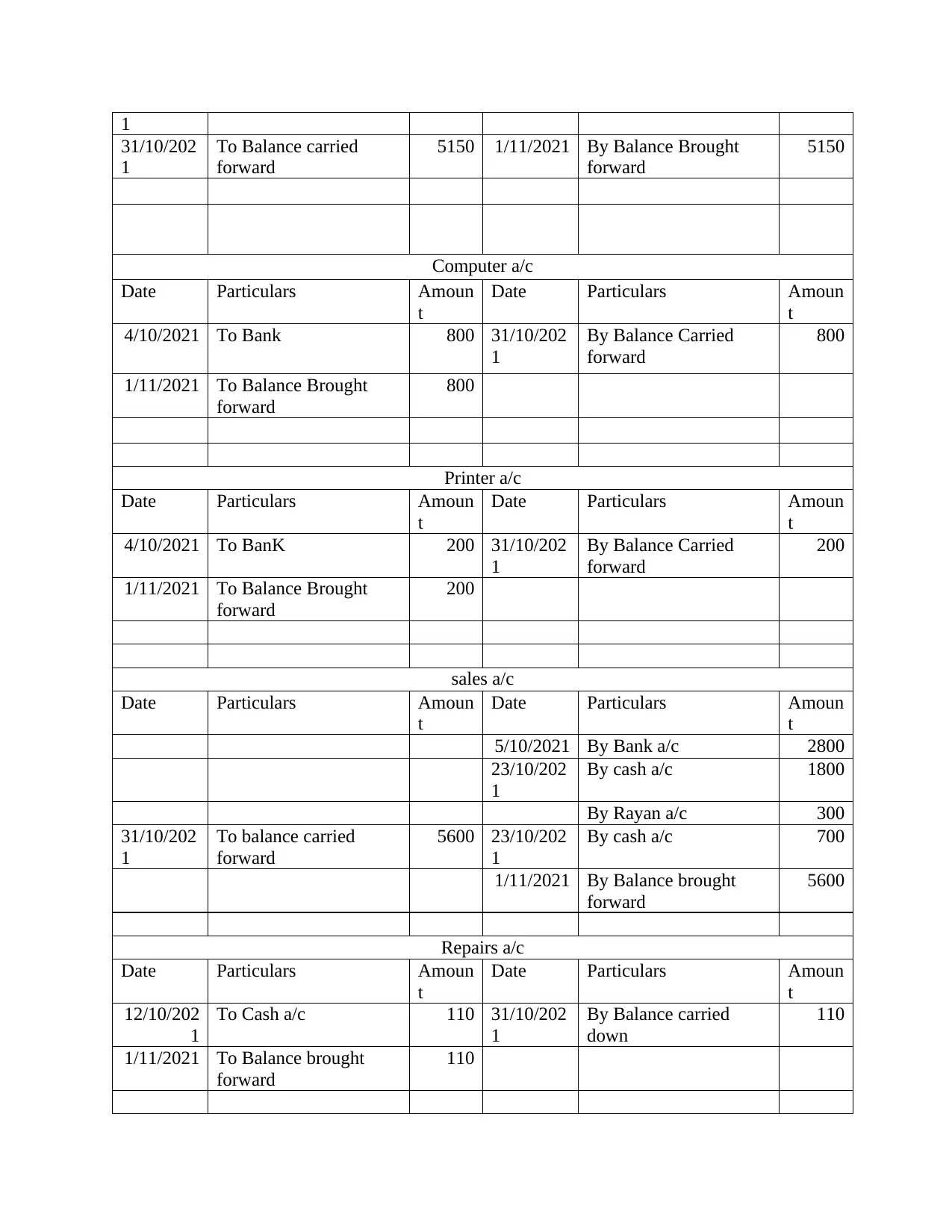

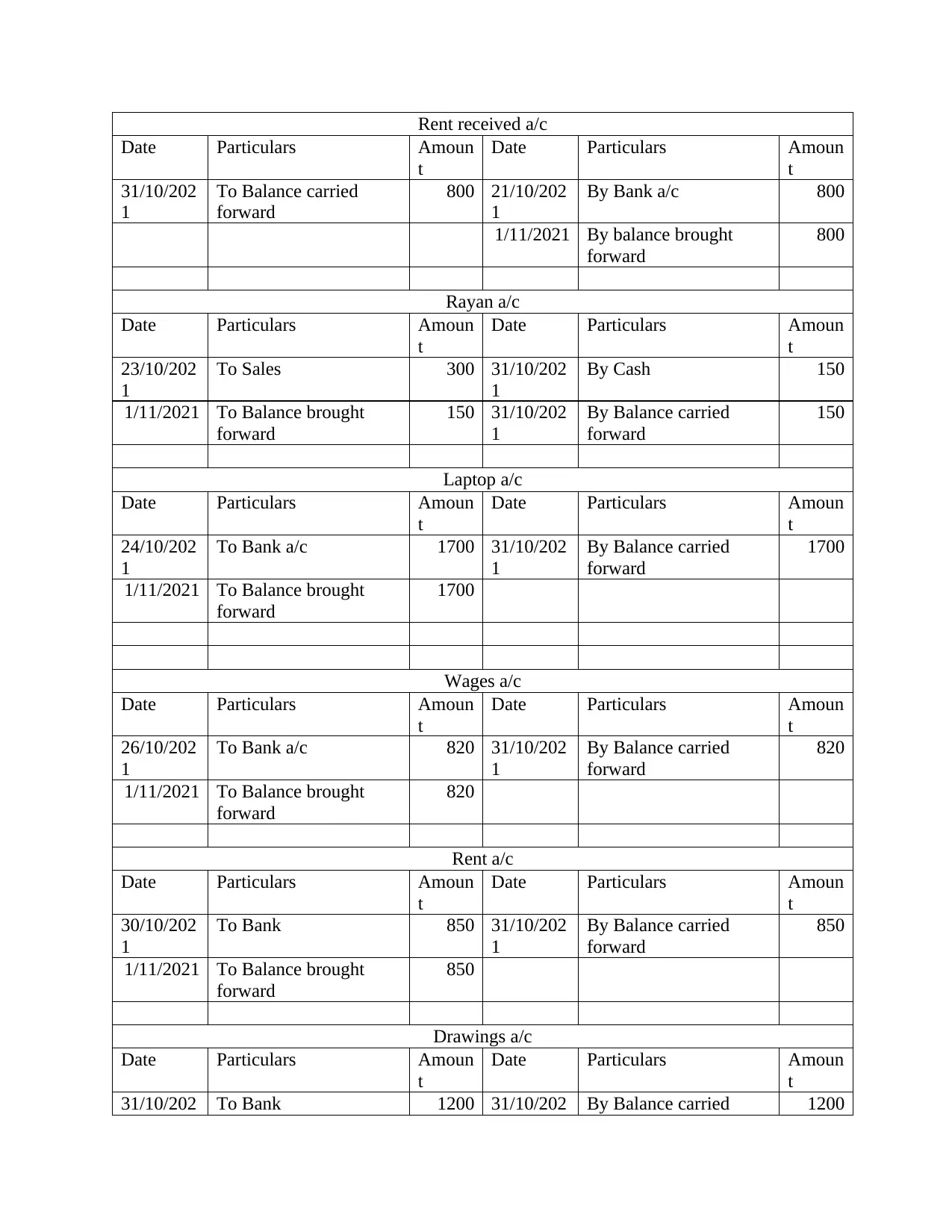

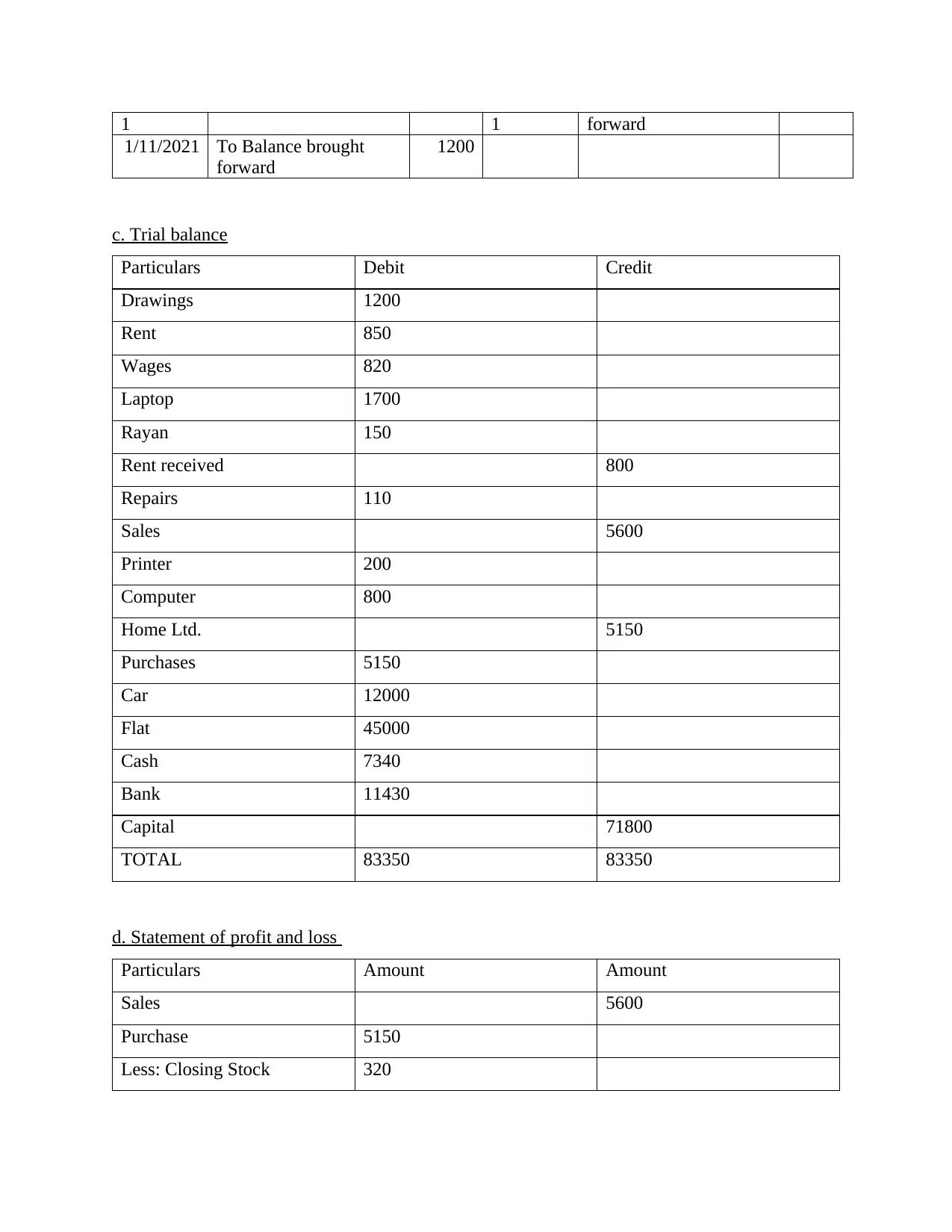

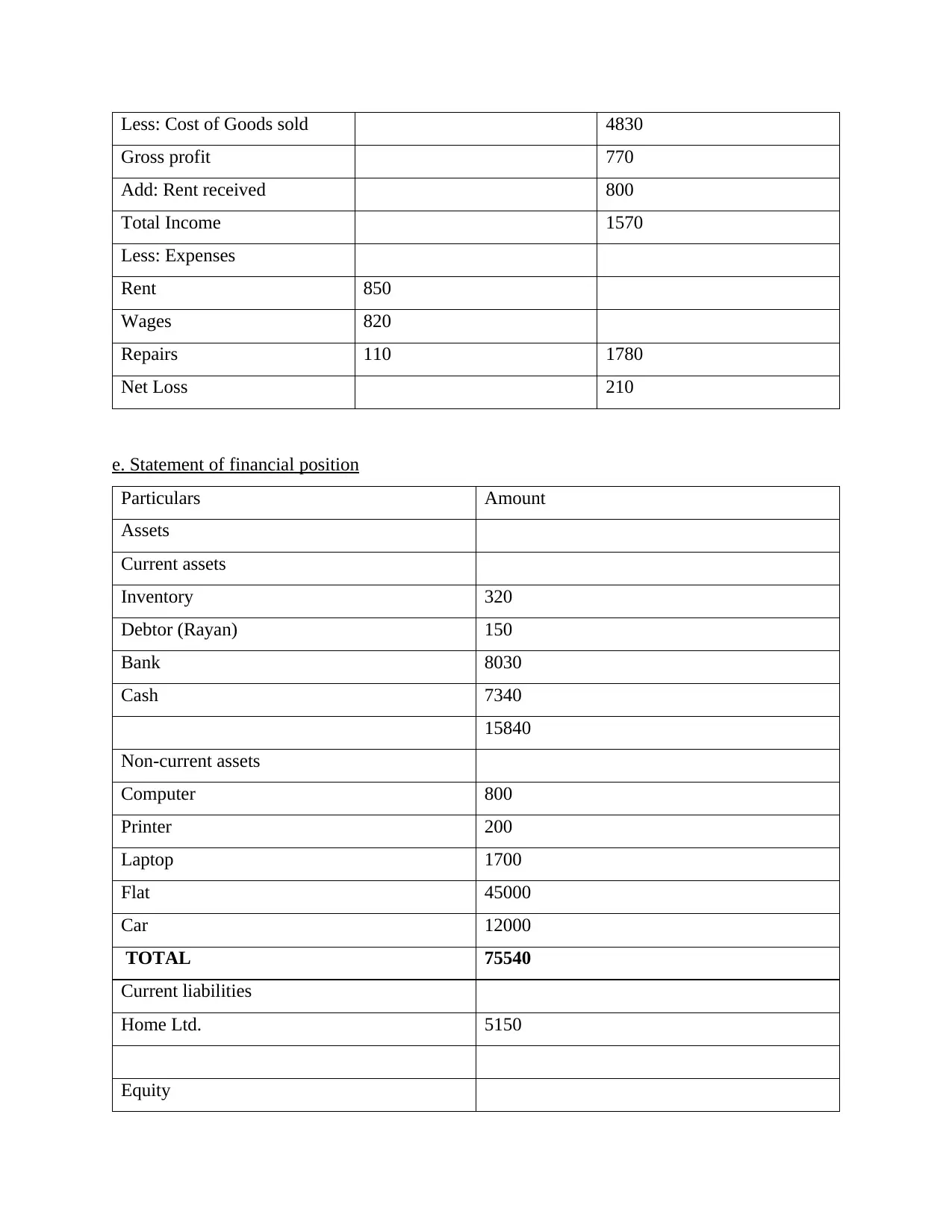

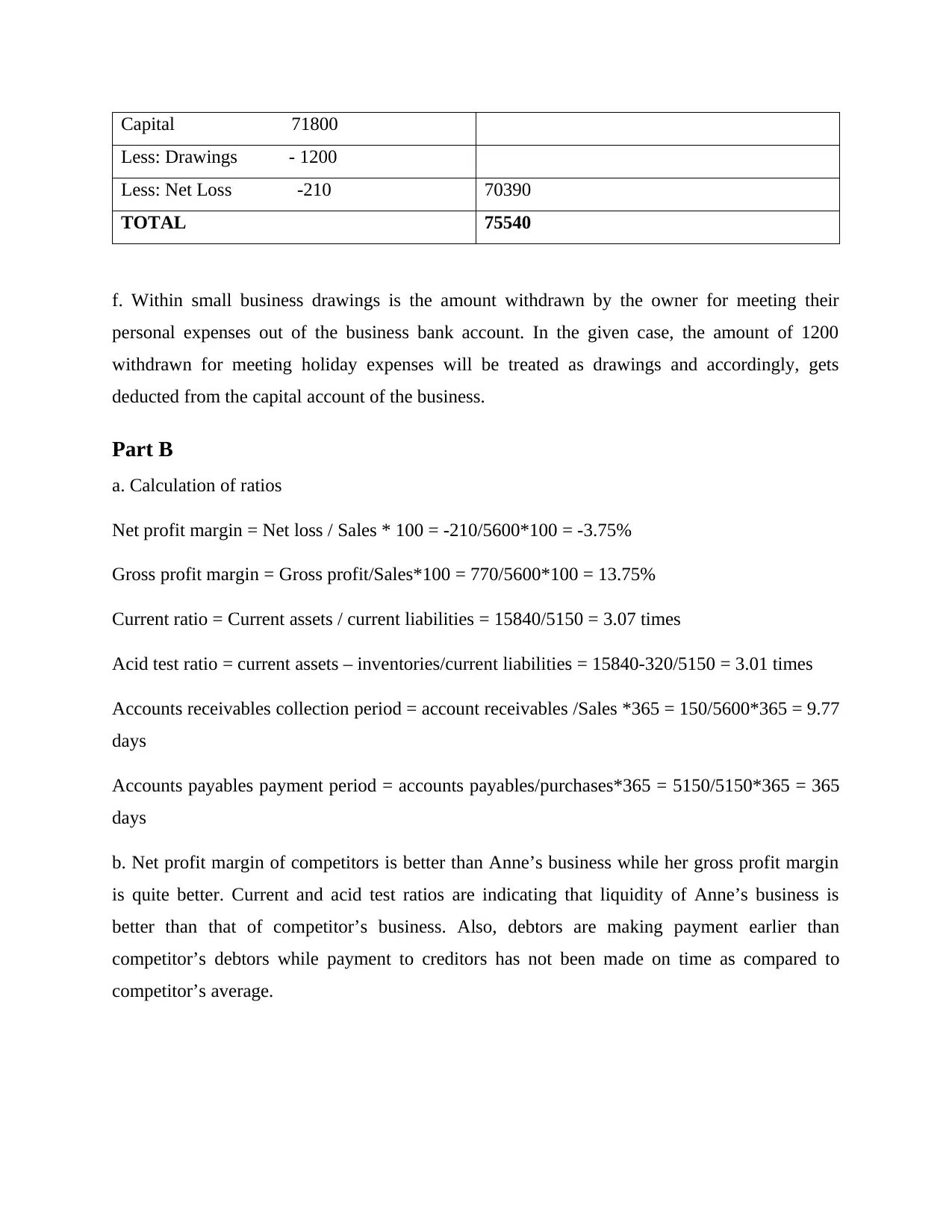

This practical assignment demonstrates the process of recording business transactions through journal entries, creating a trial balance, preparing a statement of profit and loss, and constructing a statement of financial position. It includes calculations of key financial ratios such as net profit margin, gross profit margin, current ratio, acid test ratio, accounts receivables collection period, and accounts payables payment period. The assignment also provides an analysis of these ratios in comparison to competitors, highlighting the strengths and weaknesses of the business's financial performance. The document further explains the treatment of drawings within a small business context, emphasizing its impact on the capital account.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.