Recording Business Transaction

VerifiedAdded on 2022/12/28

|16

|2239

|56

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

RECORDING BUSINESS

TRANSACTION

TRANSACTION

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART A...........................................................................................................................................3

Journal..........................................................................................................................................3

Ledger..........................................................................................................................................4

Trial balance as at 31st October 2020..........................................................................................8

Statement for Profit and Loss Account for the period ended 31st October 2020........................9

Balance sheet as at 31st October 2020.........................................................................................9

Drawings concerning small business.........................................................................................10

PART B..........................................................................................................................................10

Ratio estimation.........................................................................................................................10

Comparative evaluation of performance of the businesses........................................................12

CONCLUSION..............................................................................................................................12

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART A...........................................................................................................................................3

Journal..........................................................................................................................................3

Ledger..........................................................................................................................................4

Trial balance as at 31st October 2020..........................................................................................8

Statement for Profit and Loss Account for the period ended 31st October 2020........................9

Balance sheet as at 31st October 2020.........................................................................................9

Drawings concerning small business.........................................................................................10

PART B..........................................................................................................................................10

Ratio estimation.........................................................................................................................10

Comparative evaluation of performance of the businesses........................................................12

CONCLUSION..............................................................................................................................12

REFERENCES................................................................................................................................1

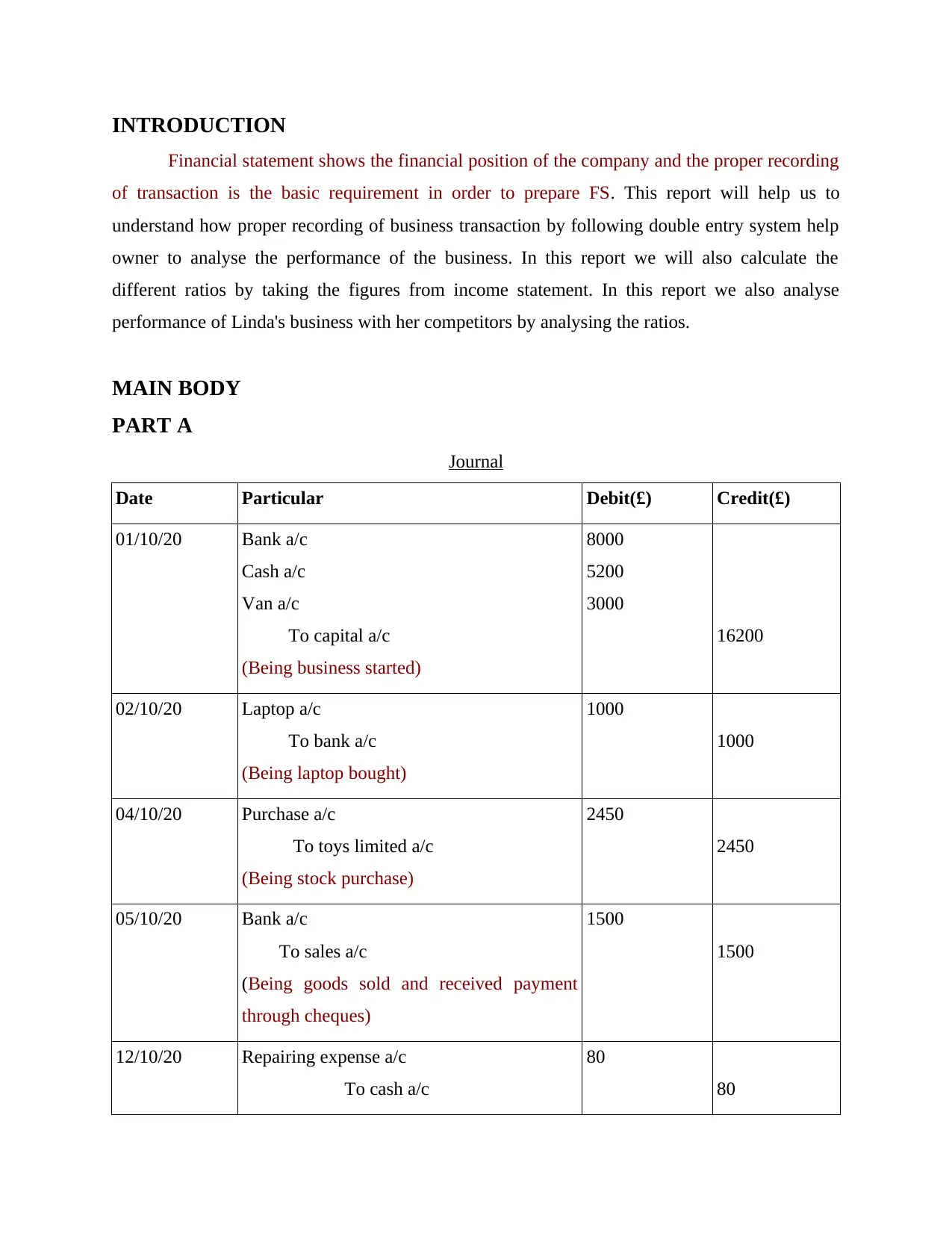

INTRODUCTION

Financial statement shows the financial position of the company and the proper recording

of transaction is the basic requirement in order to prepare FS. This report will help us to

understand how proper recording of business transaction by following double entry system help

owner to analyse the performance of the business. In this report we will also calculate the

different ratios by taking the figures from income statement. In this report we also analyse

performance of Linda's business with her competitors by analysing the ratios.

MAIN BODY

PART A

Journal

Date Particular Debit(£) Credit(£)

01/10/20 Bank a/c

Cash a/c

Van a/c

To capital a/c

(Being business started)

8000

5200

3000

16200

02/10/20 Laptop a/c

To bank a/c

(Being laptop bought)

1000

1000

04/10/20 Purchase a/c

To toys limited a/c

(Being stock purchase)

2450

2450

05/10/20 Bank a/c

To sales a/c

(Being goods sold and received payment

through cheques)

1500

1500

12/10/20 Repairing expense a/c

To cash a/c

80

80

Financial statement shows the financial position of the company and the proper recording

of transaction is the basic requirement in order to prepare FS. This report will help us to

understand how proper recording of business transaction by following double entry system help

owner to analyse the performance of the business. In this report we will also calculate the

different ratios by taking the figures from income statement. In this report we also analyse

performance of Linda's business with her competitors by analysing the ratios.

MAIN BODY

PART A

Journal

Date Particular Debit(£) Credit(£)

01/10/20 Bank a/c

Cash a/c

Van a/c

To capital a/c

(Being business started)

8000

5200

3000

16200

02/10/20 Laptop a/c

To bank a/c

(Being laptop bought)

1000

1000

04/10/20 Purchase a/c

To toys limited a/c

(Being stock purchase)

2450

2450

05/10/20 Bank a/c

To sales a/c

(Being goods sold and received payment

through cheques)

1500

1500

12/10/20 Repairing expense a/c

To cash a/c

80

80

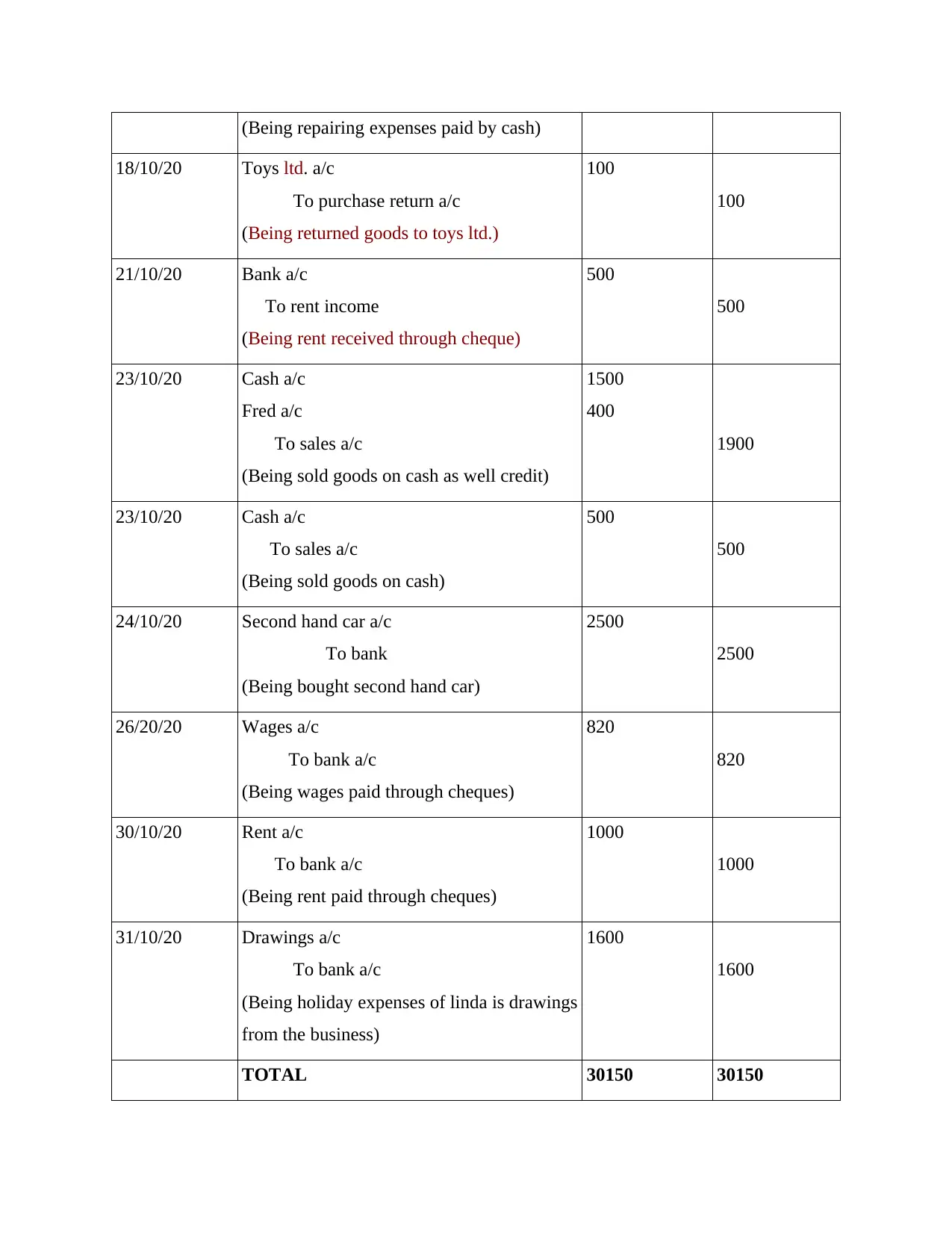

(Being repairing expenses paid by cash)

18/10/20 Toys ltd. a/c

To purchase return a/c

(Being returned goods to toys ltd.)

100

100

21/10/20 Bank a/c

To rent income

(Being rent received through cheque)

500

500

23/10/20 Cash a/c

Fred a/c

To sales a/c

(Being sold goods on cash as well credit)

1500

400

1900

23/10/20 Cash a/c

To sales a/c

(Being sold goods on cash)

500

500

24/10/20 Second hand car a/c

To bank

(Being bought second hand car)

2500

2500

26/20/20 Wages a/c

To bank a/c

(Being wages paid through cheques)

820

820

30/10/20 Rent a/c

To bank a/c

(Being rent paid through cheques)

1000

1000

31/10/20 Drawings a/c

To bank a/c

(Being holiday expenses of linda is drawings

from the business)

1600

1600

TOTAL 30150 30150

18/10/20 Toys ltd. a/c

To purchase return a/c

(Being returned goods to toys ltd.)

100

100

21/10/20 Bank a/c

To rent income

(Being rent received through cheque)

500

500

23/10/20 Cash a/c

Fred a/c

To sales a/c

(Being sold goods on cash as well credit)

1500

400

1900

23/10/20 Cash a/c

To sales a/c

(Being sold goods on cash)

500

500

24/10/20 Second hand car a/c

To bank

(Being bought second hand car)

2500

2500

26/20/20 Wages a/c

To bank a/c

(Being wages paid through cheques)

820

820

30/10/20 Rent a/c

To bank a/c

(Being rent paid through cheques)

1000

1000

31/10/20 Drawings a/c

To bank a/c

(Being holiday expenses of linda is drawings

from the business)

1600

1600

TOTAL 30150 30150

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

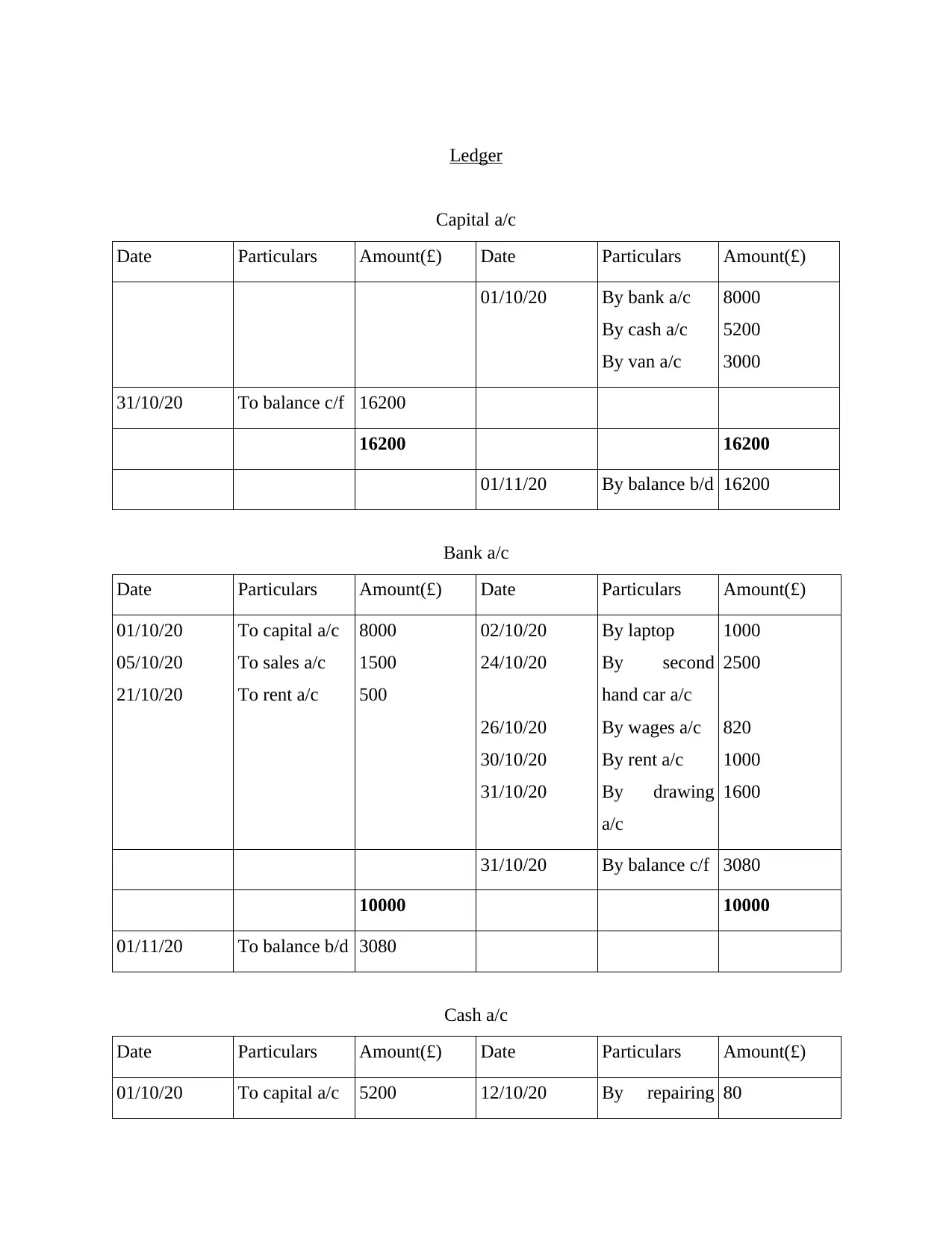

Ledger

Capital a/c

Date Particulars Amount(£) Date Particulars Amount(£)

01/10/20 By bank a/c

By cash a/c

By van a/c

8000

5200

3000

31/10/20 To balance c/f 16200

16200 16200

01/11/20 By balance b/d 16200

Bank a/c

Date Particulars Amount(£) Date Particulars Amount(£)

01/10/20

05/10/20

21/10/20

To capital a/c

To sales a/c

To rent a/c

8000

1500

500

02/10/20

24/10/20

26/10/20

30/10/20

31/10/20

By laptop

By second

hand car a/c

By wages a/c

By rent a/c

By drawing

a/c

1000

2500

820

1000

1600

31/10/20 By balance c/f 3080

10000 10000

01/11/20 To balance b/d 3080

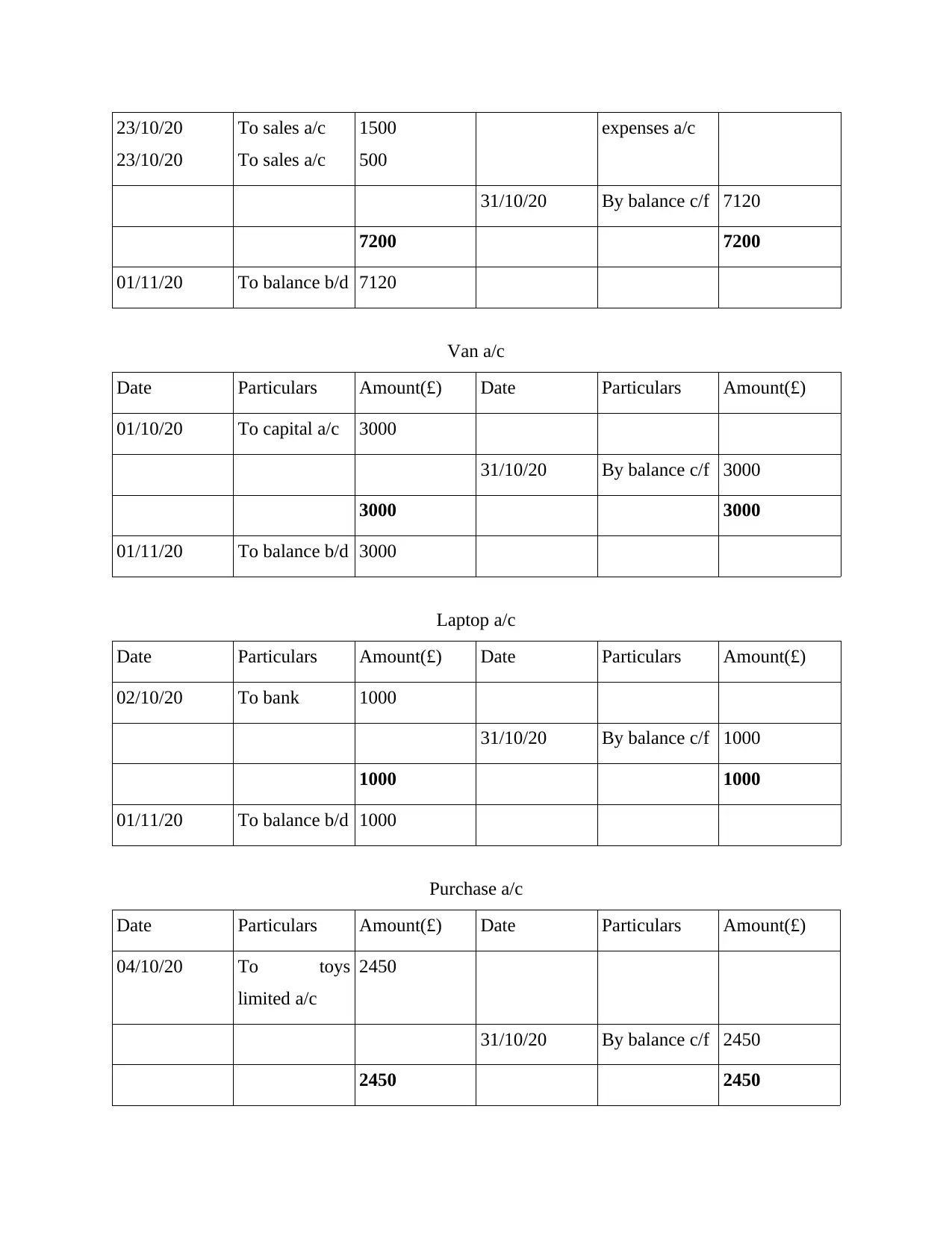

Cash a/c

Date Particulars Amount(£) Date Particulars Amount(£)

01/10/20 To capital a/c 5200 12/10/20 By repairing 80

Capital a/c

Date Particulars Amount(£) Date Particulars Amount(£)

01/10/20 By bank a/c

By cash a/c

By van a/c

8000

5200

3000

31/10/20 To balance c/f 16200

16200 16200

01/11/20 By balance b/d 16200

Bank a/c

Date Particulars Amount(£) Date Particulars Amount(£)

01/10/20

05/10/20

21/10/20

To capital a/c

To sales a/c

To rent a/c

8000

1500

500

02/10/20

24/10/20

26/10/20

30/10/20

31/10/20

By laptop

By second

hand car a/c

By wages a/c

By rent a/c

By drawing

a/c

1000

2500

820

1000

1600

31/10/20 By balance c/f 3080

10000 10000

01/11/20 To balance b/d 3080

Cash a/c

Date Particulars Amount(£) Date Particulars Amount(£)

01/10/20 To capital a/c 5200 12/10/20 By repairing 80

23/10/20

23/10/20

To sales a/c

To sales a/c

1500

500

expenses a/c

31/10/20 By balance c/f 7120

7200 7200

01/11/20 To balance b/d 7120

Van a/c

Date Particulars Amount(£) Date Particulars Amount(£)

01/10/20 To capital a/c 3000

31/10/20 By balance c/f 3000

3000 3000

01/11/20 To balance b/d 3000

Laptop a/c

Date Particulars Amount(£) Date Particulars Amount(£)

02/10/20 To bank 1000

31/10/20 By balance c/f 1000

1000 1000

01/11/20 To balance b/d 1000

Purchase a/c

Date Particulars Amount(£) Date Particulars Amount(£)

04/10/20 To toys

limited a/c

2450

31/10/20 By balance c/f 2450

2450 2450

23/10/20

To sales a/c

To sales a/c

1500

500

expenses a/c

31/10/20 By balance c/f 7120

7200 7200

01/11/20 To balance b/d 7120

Van a/c

Date Particulars Amount(£) Date Particulars Amount(£)

01/10/20 To capital a/c 3000

31/10/20 By balance c/f 3000

3000 3000

01/11/20 To balance b/d 3000

Laptop a/c

Date Particulars Amount(£) Date Particulars Amount(£)

02/10/20 To bank 1000

31/10/20 By balance c/f 1000

1000 1000

01/11/20 To balance b/d 1000

Purchase a/c

Date Particulars Amount(£) Date Particulars Amount(£)

04/10/20 To toys

limited a/c

2450

31/10/20 By balance c/f 2450

2450 2450

01/11/20 To balance b/d 2450

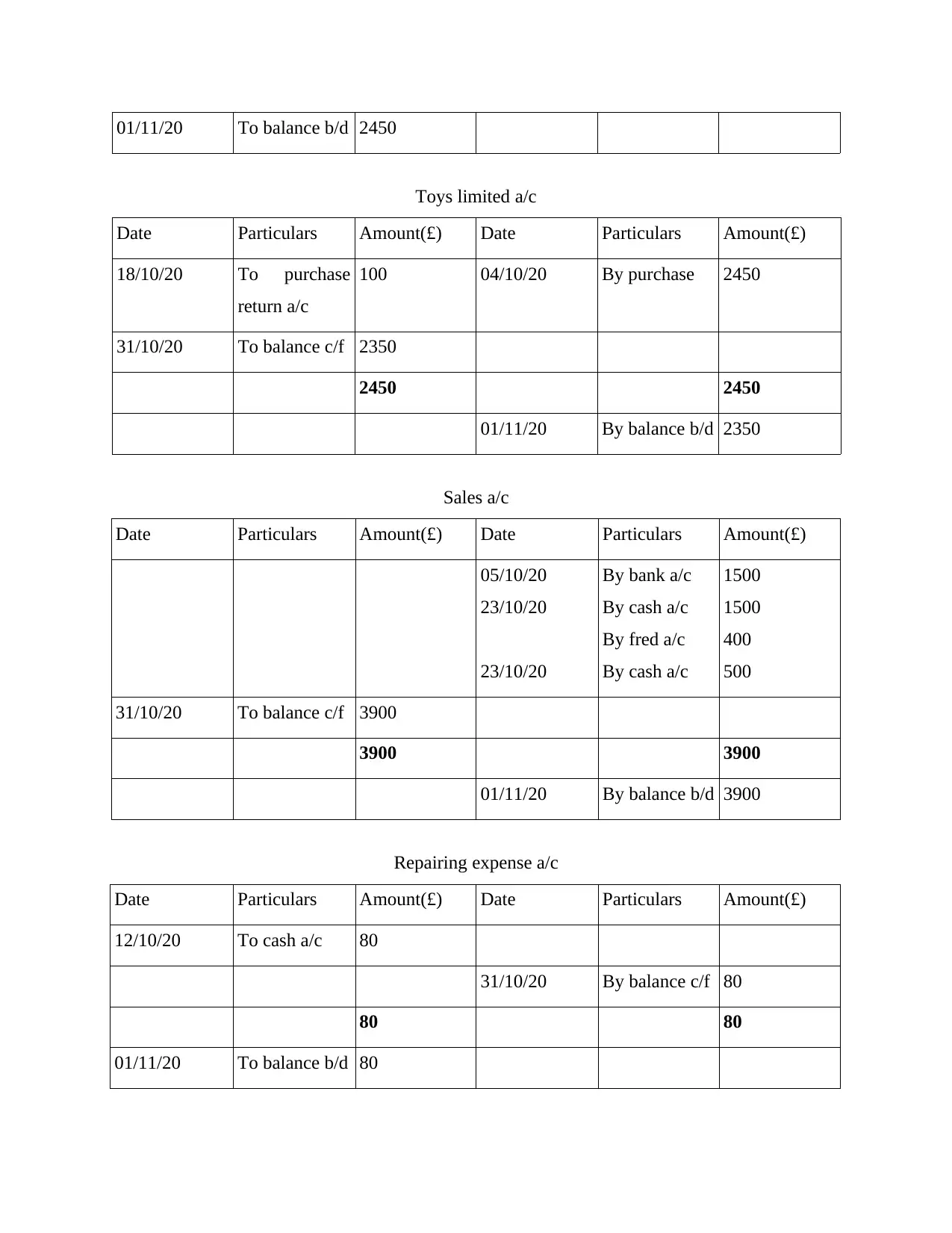

Toys limited a/c

Date Particulars Amount(£) Date Particulars Amount(£)

18/10/20 To purchase

return a/c

100 04/10/20 By purchase 2450

31/10/20 To balance c/f 2350

2450 2450

01/11/20 By balance b/d 2350

Sales a/c

Date Particulars Amount(£) Date Particulars Amount(£)

05/10/20

23/10/20

23/10/20

By bank a/c

By cash a/c

By fred a/c

By cash a/c

1500

1500

400

500

31/10/20 To balance c/f 3900

3900 3900

01/11/20 By balance b/d 3900

Repairing expense a/c

Date Particulars Amount(£) Date Particulars Amount(£)

12/10/20 To cash a/c 80

31/10/20 By balance c/f 80

80 80

01/11/20 To balance b/d 80

Toys limited a/c

Date Particulars Amount(£) Date Particulars Amount(£)

18/10/20 To purchase

return a/c

100 04/10/20 By purchase 2450

31/10/20 To balance c/f 2350

2450 2450

01/11/20 By balance b/d 2350

Sales a/c

Date Particulars Amount(£) Date Particulars Amount(£)

05/10/20

23/10/20

23/10/20

By bank a/c

By cash a/c

By fred a/c

By cash a/c

1500

1500

400

500

31/10/20 To balance c/f 3900

3900 3900

01/11/20 By balance b/d 3900

Repairing expense a/c

Date Particulars Amount(£) Date Particulars Amount(£)

12/10/20 To cash a/c 80

31/10/20 By balance c/f 80

80 80

01/11/20 To balance b/d 80

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

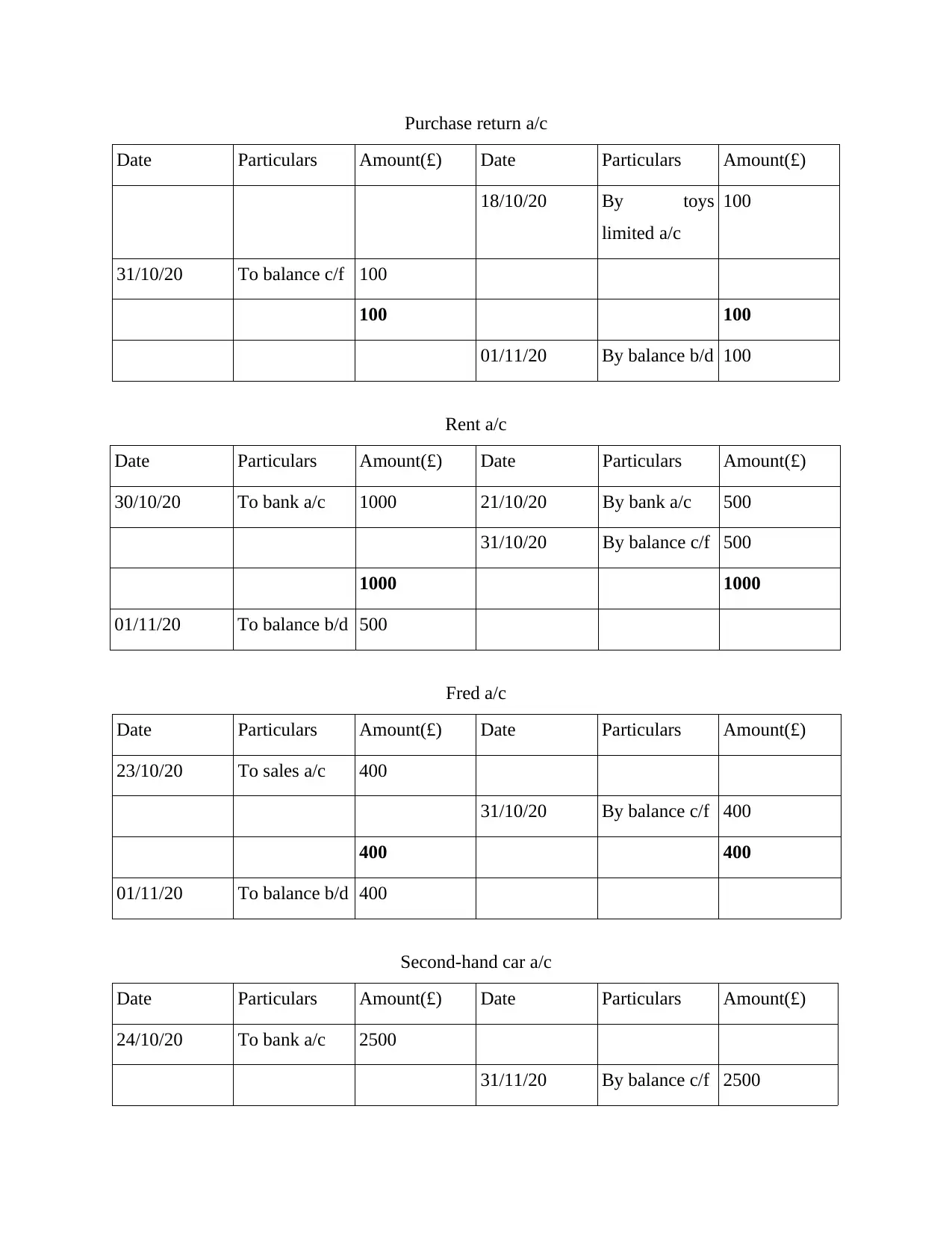

Purchase return a/c

Date Particulars Amount(£) Date Particulars Amount(£)

18/10/20 By toys

limited a/c

100

31/10/20 To balance c/f 100

100 100

01/11/20 By balance b/d 100

Rent a/c

Date Particulars Amount(£) Date Particulars Amount(£)

30/10/20 To bank a/c 1000 21/10/20 By bank a/c 500

31/10/20 By balance c/f 500

1000 1000

01/11/20 To balance b/d 500

Fred a/c

Date Particulars Amount(£) Date Particulars Amount(£)

23/10/20 To sales a/c 400

31/10/20 By balance c/f 400

400 400

01/11/20 To balance b/d 400

Second-hand car a/c

Date Particulars Amount(£) Date Particulars Amount(£)

24/10/20 To bank a/c 2500

31/11/20 By balance c/f 2500

Date Particulars Amount(£) Date Particulars Amount(£)

18/10/20 By toys

limited a/c

100

31/10/20 To balance c/f 100

100 100

01/11/20 By balance b/d 100

Rent a/c

Date Particulars Amount(£) Date Particulars Amount(£)

30/10/20 To bank a/c 1000 21/10/20 By bank a/c 500

31/10/20 By balance c/f 500

1000 1000

01/11/20 To balance b/d 500

Fred a/c

Date Particulars Amount(£) Date Particulars Amount(£)

23/10/20 To sales a/c 400

31/10/20 By balance c/f 400

400 400

01/11/20 To balance b/d 400

Second-hand car a/c

Date Particulars Amount(£) Date Particulars Amount(£)

24/10/20 To bank a/c 2500

31/11/20 By balance c/f 2500

2500 2500

01/11/20 To balance b/d 2500

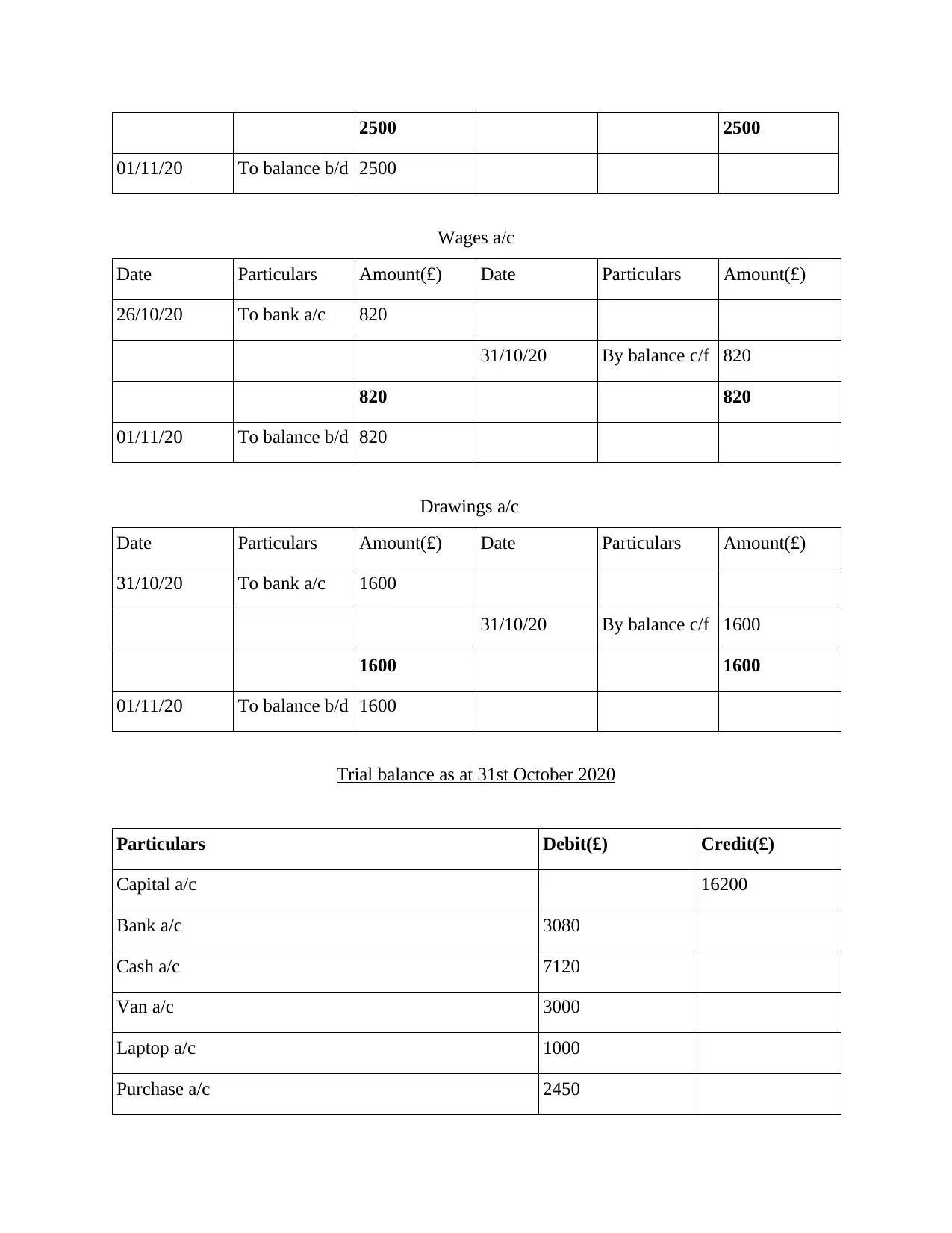

Wages a/c

Date Particulars Amount(£) Date Particulars Amount(£)

26/10/20 To bank a/c 820

31/10/20 By balance c/f 820

820 820

01/11/20 To balance b/d 820

Drawings a/c

Date Particulars Amount(£) Date Particulars Amount(£)

31/10/20 To bank a/c 1600

31/10/20 By balance c/f 1600

1600 1600

01/11/20 To balance b/d 1600

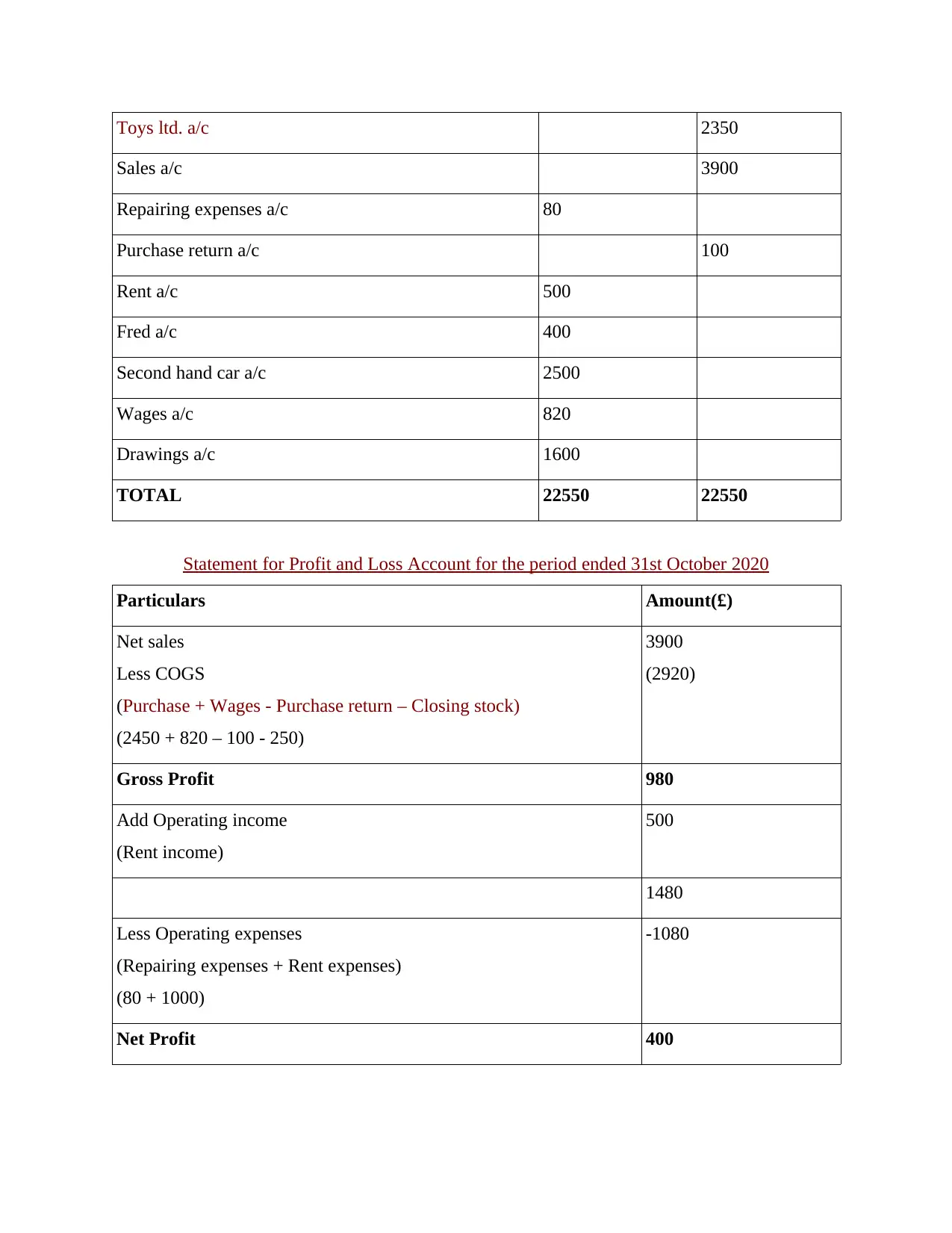

Trial balance as at 31st October 2020

Particulars Debit(£) Credit(£)

Capital a/c 16200

Bank a/c 3080

Cash a/c 7120

Van a/c 3000

Laptop a/c 1000

Purchase a/c 2450

01/11/20 To balance b/d 2500

Wages a/c

Date Particulars Amount(£) Date Particulars Amount(£)

26/10/20 To bank a/c 820

31/10/20 By balance c/f 820

820 820

01/11/20 To balance b/d 820

Drawings a/c

Date Particulars Amount(£) Date Particulars Amount(£)

31/10/20 To bank a/c 1600

31/10/20 By balance c/f 1600

1600 1600

01/11/20 To balance b/d 1600

Trial balance as at 31st October 2020

Particulars Debit(£) Credit(£)

Capital a/c 16200

Bank a/c 3080

Cash a/c 7120

Van a/c 3000

Laptop a/c 1000

Purchase a/c 2450

Toys ltd. a/c 2350

Sales a/c 3900

Repairing expenses a/c 80

Purchase return a/c 100

Rent a/c 500

Fred a/c 400

Second hand car a/c 2500

Wages a/c 820

Drawings a/c 1600

TOTAL 22550 22550

Statement for Profit and Loss Account for the period ended 31st October 2020

Particulars Amount(£)

Net sales

Less COGS

(Purchase + Wages - Purchase return – Closing stock)

(2450 + 820 – 100 - 250)

3900

(2920)

Gross Profit 980

Add Operating income

(Rent income)

500

1480

Less Operating expenses

(Repairing expenses + Rent expenses)

(80 + 1000)

-1080

Net Profit 400

Sales a/c 3900

Repairing expenses a/c 80

Purchase return a/c 100

Rent a/c 500

Fred a/c 400

Second hand car a/c 2500

Wages a/c 820

Drawings a/c 1600

TOTAL 22550 22550

Statement for Profit and Loss Account for the period ended 31st October 2020

Particulars Amount(£)

Net sales

Less COGS

(Purchase + Wages - Purchase return – Closing stock)

(2450 + 820 – 100 - 250)

3900

(2920)

Gross Profit 980

Add Operating income

(Rent income)

500

1480

Less Operating expenses

(Repairing expenses + Rent expenses)

(80 + 1000)

-1080

Net Profit 400

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Balance sheet as at 31st October 2020

Particulars Amount(£)

ASSETS

Fixed assets

Van

Laptop

Second-hand car

Current assets

Bank

Cash

Closing stocks

Debtors

3000

1000

2500

3080

7120

250

400

TOTAL 17350

LIABILITIES

Capital

( Capital + Net profit - Drawing)

(16200 + 400 - 1600)

Current liabilities

Creditors

15000

2350

TOTAL 17350

Drawings concerning small business

When owner withdraw cash or assets of the company for their personal use it is known as

drawings. Drawings are not considered as business expense of the company. Drawings are

shown on the assets side of the company. Every business expense of the company is recorded as

expense on debit side of P&L account. In case if any personal expense of the owner when

considered and recorded as business expenses it shows companies are trying to manipulate the

users of the financial statement. It must be considered as drawings from the company and

recorded on the assets side of the balance sheet. (Julien, 2018). In that case the profit of the

business will reduce and tax expense of the company will also reduce. This will show the

Particulars Amount(£)

ASSETS

Fixed assets

Van

Laptop

Second-hand car

Current assets

Bank

Cash

Closing stocks

Debtors

3000

1000

2500

3080

7120

250

400

TOTAL 17350

LIABILITIES

Capital

( Capital + Net profit - Drawing)

(16200 + 400 - 1600)

Current liabilities

Creditors

15000

2350

TOTAL 17350

Drawings concerning small business

When owner withdraw cash or assets of the company for their personal use it is known as

drawings. Drawings are not considered as business expense of the company. Drawings are

shown on the assets side of the company. Every business expense of the company is recorded as

expense on debit side of P&L account. In case if any personal expense of the owner when

considered and recorded as business expenses it shows companies are trying to manipulate the

users of the financial statement. It must be considered as drawings from the company and

recorded on the assets side of the balance sheet. (Julien, 2018). In that case the profit of the

business will reduce and tax expense of the company will also reduce. This will show the

misrepresentation of the financial statement i.e. window dressing. So the holiday expense of

Linda is considered as her personal expense not as business expense. Linda must separate its

personal account and business account in order to properly maintain the books of accounts.

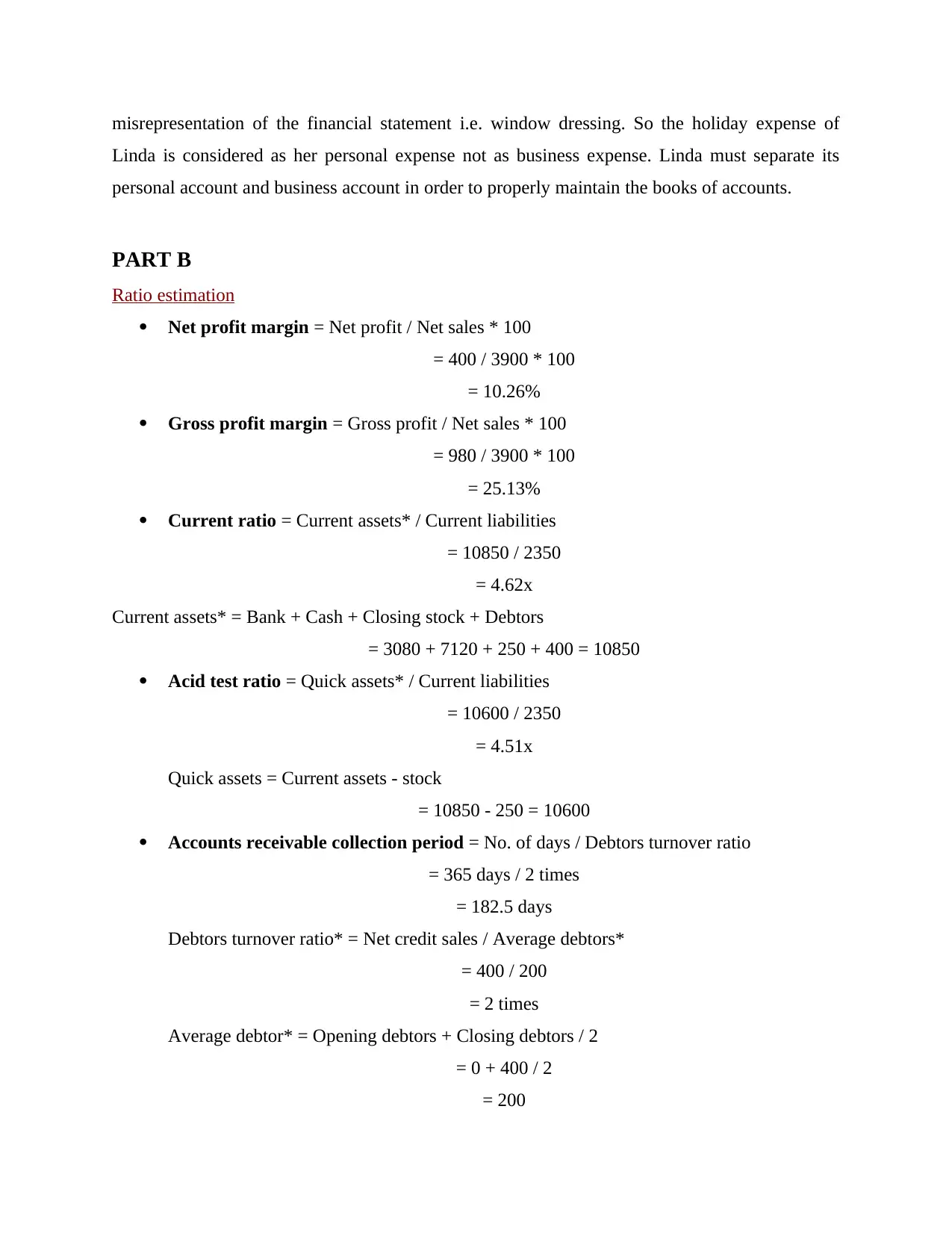

PART B

Ratio estimation

Net profit margin = Net profit / Net sales * 100

= 400 / 3900 * 100

= 10.26%

Gross profit margin = Gross profit / Net sales * 100

= 980 / 3900 * 100

= 25.13%

Current ratio = Current assets* / Current liabilities

= 10850 / 2350

= 4.62x

Current assets* = Bank + Cash + Closing stock + Debtors

= 3080 + 7120 + 250 + 400 = 10850

Acid test ratio = Quick assets* / Current liabilities

= 10600 / 2350

= 4.51x

Quick assets = Current assets - stock

= 10850 - 250 = 10600

Accounts receivable collection period = No. of days / Debtors turnover ratio

= 365 days / 2 times

= 182.5 days

Debtors turnover ratio* = Net credit sales / Average debtors*

= 400 / 200

= 2 times

Average debtor* = Opening debtors + Closing debtors / 2

= 0 + 400 / 2

= 200

Linda is considered as her personal expense not as business expense. Linda must separate its

personal account and business account in order to properly maintain the books of accounts.

PART B

Ratio estimation

Net profit margin = Net profit / Net sales * 100

= 400 / 3900 * 100

= 10.26%

Gross profit margin = Gross profit / Net sales * 100

= 980 / 3900 * 100

= 25.13%

Current ratio = Current assets* / Current liabilities

= 10850 / 2350

= 4.62x

Current assets* = Bank + Cash + Closing stock + Debtors

= 3080 + 7120 + 250 + 400 = 10850

Acid test ratio = Quick assets* / Current liabilities

= 10600 / 2350

= 4.51x

Quick assets = Current assets - stock

= 10850 - 250 = 10600

Accounts receivable collection period = No. of days / Debtors turnover ratio

= 365 days / 2 times

= 182.5 days

Debtors turnover ratio* = Net credit sales / Average debtors*

= 400 / 200

= 2 times

Average debtor* = Opening debtors + Closing debtors / 2

= 0 + 400 / 2

= 200

Accounts payable payment ratio = No. of days / Creditors turnover ratio*

= 365 days / 2 times

= 182.5 days

Creditors turnover ratio* = Net credit purchase / Average creditors*

= 2350 / 1175

= 2 times

Average creditors* = Opening creditors + Closing creditors / 2

= 0 + 2350 / 2

= 1175

Comparative evaluation of performance of the businesses

GP and NP ratio is help the business to determine the profit percentage of the company.

The difference between gross profit and net profit is operating and non operating expenses. By

analysing gross profit margin and net profit margin of the Linda's business we interpret that the

internal performance of the business are low. She is required to increase the profit margin of

business and in order to do that she has to focus towards decreasing its cost price by reducing the

wastage of resources(MUSALLAM, 2018). Increasing average order value, reducing operating

expenses, reducing inventory, reducing overheads, increasing conversion cost etc. are some

factors by adopting it Linda's profit margin can be increased.

Current ratio and acid test ratio help to determine ability of the CA to pay companies CL.

Current and acid test ratio of the companies, help us to know the ability of the business to pay its

CL is 4.62 times and pay it more quickly i.e. by acid test ratio is 4.52 times. This indicates that

the external performance of the business is better.

ARCP says that in how many days in a year company receive its money back from the

debtors. It is better for the company when the accounts receivable collection period is

less(Morales-Díaz and Zamora-Ramírez, 2018). Accounts payable payment period says that in

how many days in a year company pays its debt to its creditors. It is better if the Accounts

payable payment period is high. Linda's overall performance is good but there is need of much

more improvement in efficiency of the business.

CONCLUSION

In this report, we understand how the day to day transaction of the business is properly

recorded into journal and then posting of those entries into ledger account. We studied the format

= 365 days / 2 times

= 182.5 days

Creditors turnover ratio* = Net credit purchase / Average creditors*

= 2350 / 1175

= 2 times

Average creditors* = Opening creditors + Closing creditors / 2

= 0 + 2350 / 2

= 1175

Comparative evaluation of performance of the businesses

GP and NP ratio is help the business to determine the profit percentage of the company.

The difference between gross profit and net profit is operating and non operating expenses. By

analysing gross profit margin and net profit margin of the Linda's business we interpret that the

internal performance of the business are low. She is required to increase the profit margin of

business and in order to do that she has to focus towards decreasing its cost price by reducing the

wastage of resources(MUSALLAM, 2018). Increasing average order value, reducing operating

expenses, reducing inventory, reducing overheads, increasing conversion cost etc. are some

factors by adopting it Linda's profit margin can be increased.

Current ratio and acid test ratio help to determine ability of the CA to pay companies CL.

Current and acid test ratio of the companies, help us to know the ability of the business to pay its

CL is 4.62 times and pay it more quickly i.e. by acid test ratio is 4.52 times. This indicates that

the external performance of the business is better.

ARCP says that in how many days in a year company receive its money back from the

debtors. It is better for the company when the accounts receivable collection period is

less(Morales-Díaz and Zamora-Ramírez, 2018). Accounts payable payment period says that in

how many days in a year company pays its debt to its creditors. It is better if the Accounts

payable payment period is high. Linda's overall performance is good but there is need of much

more improvement in efficiency of the business.

CONCLUSION

In this report, we understand how the day to day transaction of the business is properly

recorded into journal and then posting of those entries into ledger account. We studied the format

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of preparing trial balance, income statement and statement of financial position. We calculate

different financial ratios and analysis it to know the internal and external performance of the

business. In this report, we also understand the term drawings and how drawings are concerning

small business.

different financial ratios and analysis it to know the internal and external performance of the

business. In this report, we also understand the term drawings and how drawings are concerning

small business.

REFERENCES

Books and journals

Fischer-Pauzenberger, C. and Schwaiger, W. S., 2017. The OntoREA Accounting Model:

Ontology-based Modeling of the Accounting Domain. CSIMQ. 11. pp.20-37.

Uddin, R. and et.al., 2017. Accounting practices of small and medium enterprises in

Rangpur. Bangladesh. Journal of Business and Financial Affairs. 6(4). pp.1-7.

Yu, T., Lin, Z. and Tang, Q., 2018. Blockchain: The introduction and its application in financial

accounting. Journal of Corporate Accounting & Finance. 29(4). pp.37-47.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. The impact of IFRS 16 on key financial ratios:

A new methodological approach. Accounting in Europe. 15(1). pp.105-133.

O’Donnell, C. J., Fallah-Fini, S. and Triantis, K., 2017. Measuring and analysing productivity

change in a metafrontier framework. Journal of Productivity Analysis. 47(2). pp.117-

128.

MUSALLAM, S. R., 2018. Exploring the relationship between financial ratios and market stock

returns. Eurasian Journal of Business and Economics. 11(21). pp.101-116.

Julien, P. A. ed., 2018. The state of the art in small business and entrepreneurship. Routledge.

Online

The process of recording business transactions, 2021 [Online]. Available

through:<https://opentuition.com/fia/fa1/the-process-of-recording-business-transactions/>

1

Books and journals

Fischer-Pauzenberger, C. and Schwaiger, W. S., 2017. The OntoREA Accounting Model:

Ontology-based Modeling of the Accounting Domain. CSIMQ. 11. pp.20-37.

Uddin, R. and et.al., 2017. Accounting practices of small and medium enterprises in

Rangpur. Bangladesh. Journal of Business and Financial Affairs. 6(4). pp.1-7.

Yu, T., Lin, Z. and Tang, Q., 2018. Blockchain: The introduction and its application in financial

accounting. Journal of Corporate Accounting & Finance. 29(4). pp.37-47.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. The impact of IFRS 16 on key financial ratios:

A new methodological approach. Accounting in Europe. 15(1). pp.105-133.

O’Donnell, C. J., Fallah-Fini, S. and Triantis, K., 2017. Measuring and analysing productivity

change in a metafrontier framework. Journal of Productivity Analysis. 47(2). pp.117-

128.

MUSALLAM, S. R., 2018. Exploring the relationship between financial ratios and market stock

returns. Eurasian Journal of Business and Economics. 11(21). pp.101-116.

Julien, P. A. ed., 2018. The state of the art in small business and entrepreneurship. Routledge.

Online

The process of recording business transactions, 2021 [Online]. Available

through:<https://opentuition.com/fia/fa1/the-process-of-recording-business-transactions/>

1

2

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.