Recording Business Transactions

VerifiedAdded on 2022/12/29

|14

|2125

|23

AI Summary

This document provides a comprehensive guide on recording business transactions and its significance in evaluating company performance. It covers topics such as T accounts, ledger accounts, trial balance, income statement, financial position, and ratio analysis. The document also includes a comparison of Linda's firm's ratios with industry averages.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording Business

Transactions

Transactions

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION ..........................................................................................................................3

PART A ..........................................................................................................................................3

a) Perpetration of T Accounts.....................................................................................................3

b) Ledger Accounts.....................................................................................................................4

c) Trial Balance as on 31st October 2020...................................................................................7

d) Income Statement for period ending 31st October 2020........................................................7

e) Financial Position as at 31st October 2020.............................................................................8

f) What are drawings concerned for small business and clarification of the query....................8

PART B............................................................................................................................................8

a) Ratios Calculation...................................................................................................................8

b) Ratio Analysis of Linda's firm in comparison with the Industry Ratios.................................9

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION ..........................................................................................................................3

PART A ..........................................................................................................................................3

a) Perpetration of T Accounts.....................................................................................................3

b) Ledger Accounts.....................................................................................................................4

c) Trial Balance as on 31st October 2020...................................................................................7

d) Income Statement for period ending 31st October 2020........................................................7

e) Financial Position as at 31st October 2020.............................................................................8

f) What are drawings concerned for small business and clarification of the query....................8

PART B............................................................................................................................................8

a) Ratios Calculation...................................................................................................................8

b) Ratio Analysis of Linda's firm in comparison with the Industry Ratios.................................9

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

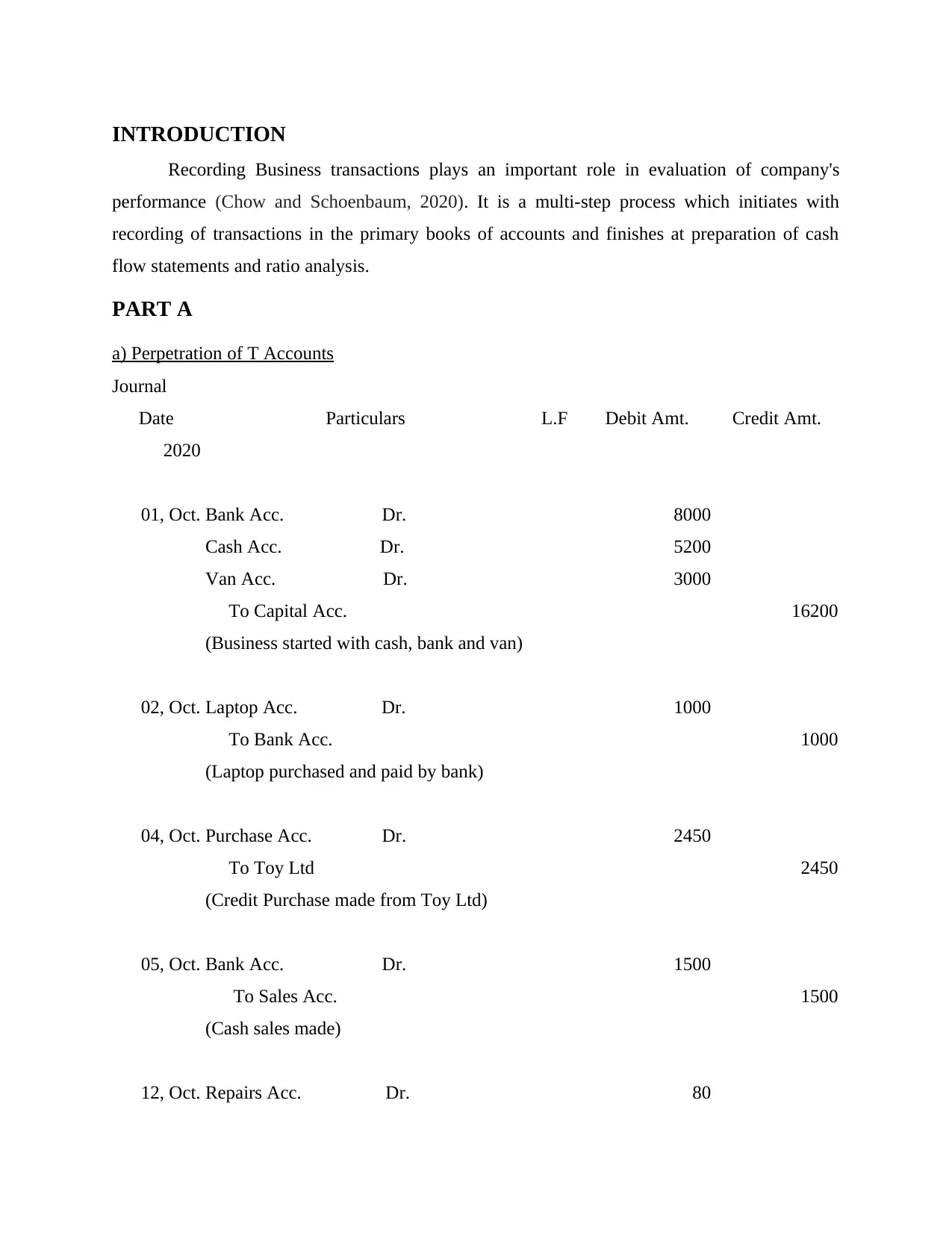

INTRODUCTION

Recording Business transactions plays an important role in evaluation of company's

performance (Chow and Schoenbaum, 2020). It is a multi-step process which initiates with

recording of transactions in the primary books of accounts and finishes at preparation of cash

flow statements and ratio analysis.

PART A

a) Perpetration of T Accounts

Journal

Date Particulars L.F Debit Amt. Credit Amt.

2020

01, Oct. Bank Acc. Dr. 8000

Cash Acc. Dr. 5200

Van Acc. Dr. 3000

To Capital Acc. 16200

(Business started with cash, bank and van)

02, Oct. Laptop Acc. Dr. 1000

To Bank Acc. 1000

(Laptop purchased and paid by bank)

04, Oct. Purchase Acc. Dr. 2450

To Toy Ltd 2450

(Credit Purchase made from Toy Ltd)

05, Oct. Bank Acc. Dr. 1500

To Sales Acc. 1500

(Cash sales made)

12, Oct. Repairs Acc. Dr. 80

Recording Business transactions plays an important role in evaluation of company's

performance (Chow and Schoenbaum, 2020). It is a multi-step process which initiates with

recording of transactions in the primary books of accounts and finishes at preparation of cash

flow statements and ratio analysis.

PART A

a) Perpetration of T Accounts

Journal

Date Particulars L.F Debit Amt. Credit Amt.

2020

01, Oct. Bank Acc. Dr. 8000

Cash Acc. Dr. 5200

Van Acc. Dr. 3000

To Capital Acc. 16200

(Business started with cash, bank and van)

02, Oct. Laptop Acc. Dr. 1000

To Bank Acc. 1000

(Laptop purchased and paid by bank)

04, Oct. Purchase Acc. Dr. 2450

To Toy Ltd 2450

(Credit Purchase made from Toy Ltd)

05, Oct. Bank Acc. Dr. 1500

To Sales Acc. 1500

(Cash sales made)

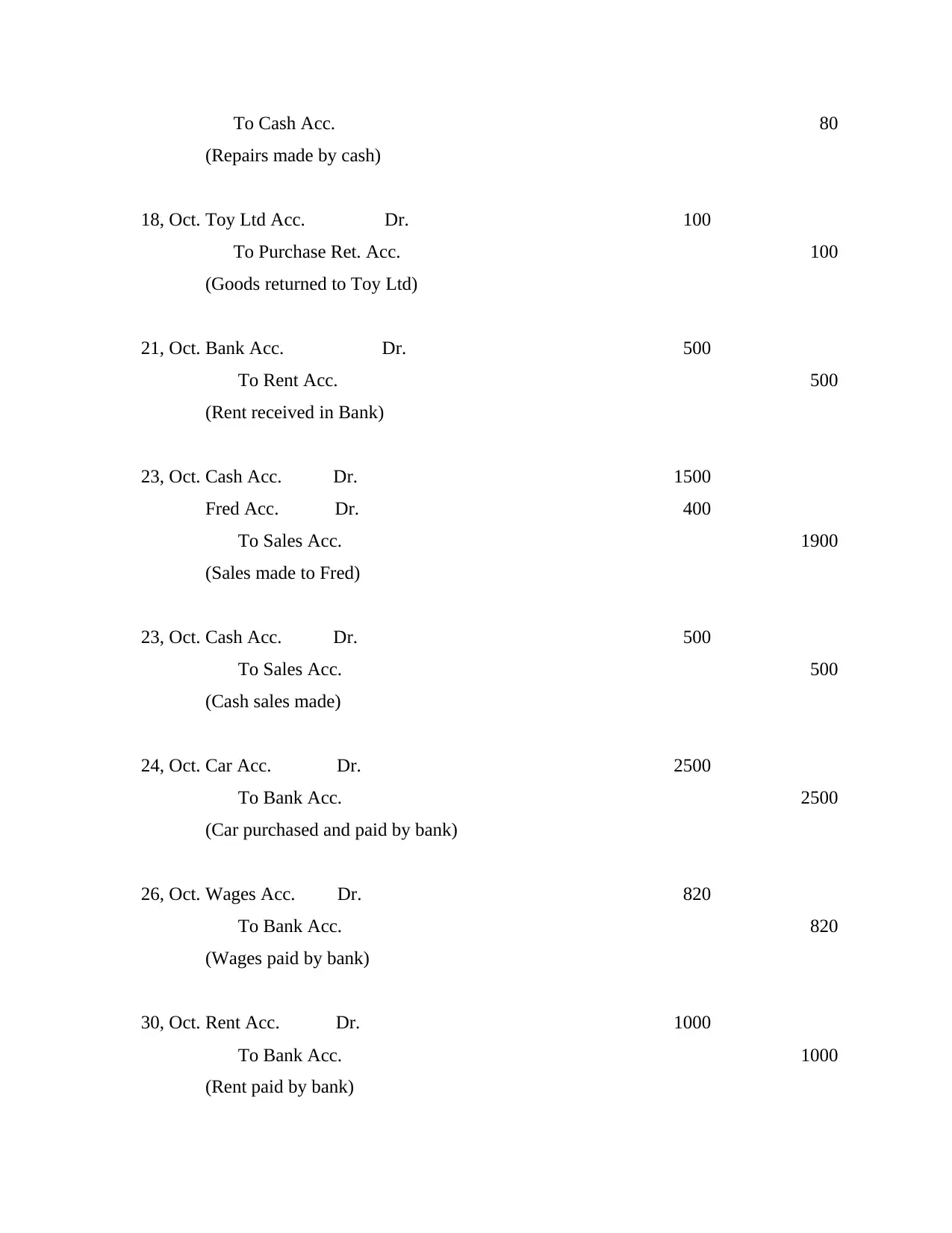

12, Oct. Repairs Acc. Dr. 80

To Cash Acc. 80

(Repairs made by cash)

18, Oct. Toy Ltd Acc. Dr. 100

To Purchase Ret. Acc. 100

(Goods returned to Toy Ltd)

21, Oct. Bank Acc. Dr. 500

To Rent Acc. 500

(Rent received in Bank)

23, Oct. Cash Acc. Dr. 1500

Fred Acc. Dr. 400

To Sales Acc. 1900

(Sales made to Fred)

23, Oct. Cash Acc. Dr. 500

To Sales Acc. 500

(Cash sales made)

24, Oct. Car Acc. Dr. 2500

To Bank Acc. 2500

(Car purchased and paid by bank)

26, Oct. Wages Acc. Dr. 820

To Bank Acc. 820

(Wages paid by bank)

30, Oct. Rent Acc. Dr. 1000

To Bank Acc. 1000

(Rent paid by bank)

(Repairs made by cash)

18, Oct. Toy Ltd Acc. Dr. 100

To Purchase Ret. Acc. 100

(Goods returned to Toy Ltd)

21, Oct. Bank Acc. Dr. 500

To Rent Acc. 500

(Rent received in Bank)

23, Oct. Cash Acc. Dr. 1500

Fred Acc. Dr. 400

To Sales Acc. 1900

(Sales made to Fred)

23, Oct. Cash Acc. Dr. 500

To Sales Acc. 500

(Cash sales made)

24, Oct. Car Acc. Dr. 2500

To Bank Acc. 2500

(Car purchased and paid by bank)

26, Oct. Wages Acc. Dr. 820

To Bank Acc. 820

(Wages paid by bank)

30, Oct. Rent Acc. Dr. 1000

To Bank Acc. 1000

(Rent paid by bank)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

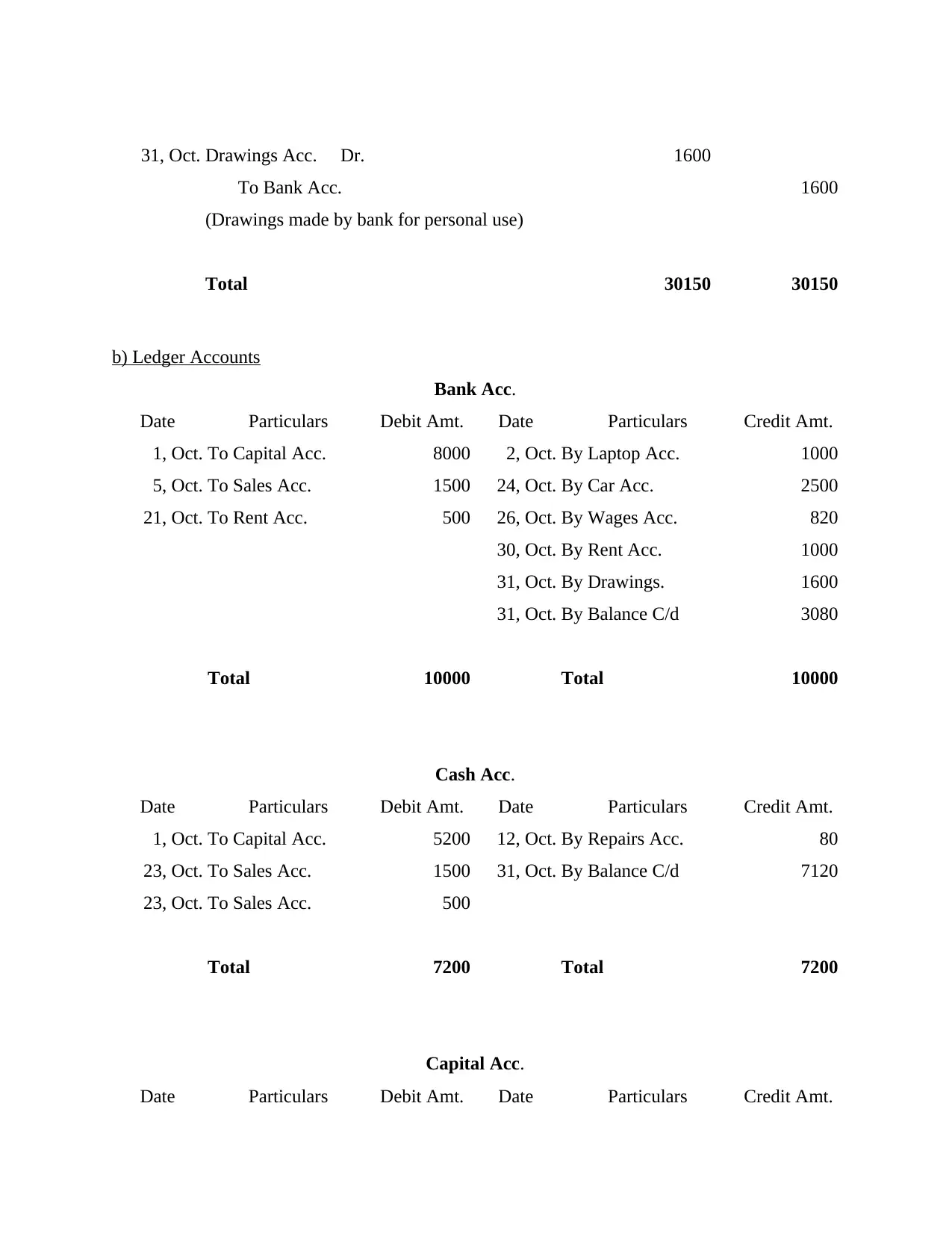

31, Oct. Drawings Acc. Dr. 1600

To Bank Acc. 1600

(Drawings made by bank for personal use)

Total 30150 30150

b) Ledger Accounts

Bank Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

1, Oct. To Capital Acc. 8000 2, Oct. By Laptop Acc. 1000

5, Oct. To Sales Acc. 1500 24, Oct. By Car Acc. 2500

21, Oct. To Rent Acc. 500 26, Oct. By Wages Acc. 820

30, Oct. By Rent Acc. 1000

31, Oct. By Drawings. 1600

31, Oct. By Balance C/d 3080

Total 10000 Total 10000

Cash Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

1, Oct. To Capital Acc. 5200 12, Oct. By Repairs Acc. 80

23, Oct. To Sales Acc. 1500 31, Oct. By Balance C/d 7120

23, Oct. To Sales Acc. 500

Total 7200 Total 7200

Capital Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

To Bank Acc. 1600

(Drawings made by bank for personal use)

Total 30150 30150

b) Ledger Accounts

Bank Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

1, Oct. To Capital Acc. 8000 2, Oct. By Laptop Acc. 1000

5, Oct. To Sales Acc. 1500 24, Oct. By Car Acc. 2500

21, Oct. To Rent Acc. 500 26, Oct. By Wages Acc. 820

30, Oct. By Rent Acc. 1000

31, Oct. By Drawings. 1600

31, Oct. By Balance C/d 3080

Total 10000 Total 10000

Cash Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

1, Oct. To Capital Acc. 5200 12, Oct. By Repairs Acc. 80

23, Oct. To Sales Acc. 1500 31, Oct. By Balance C/d 7120

23, Oct. To Sales Acc. 500

Total 7200 Total 7200

Capital Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

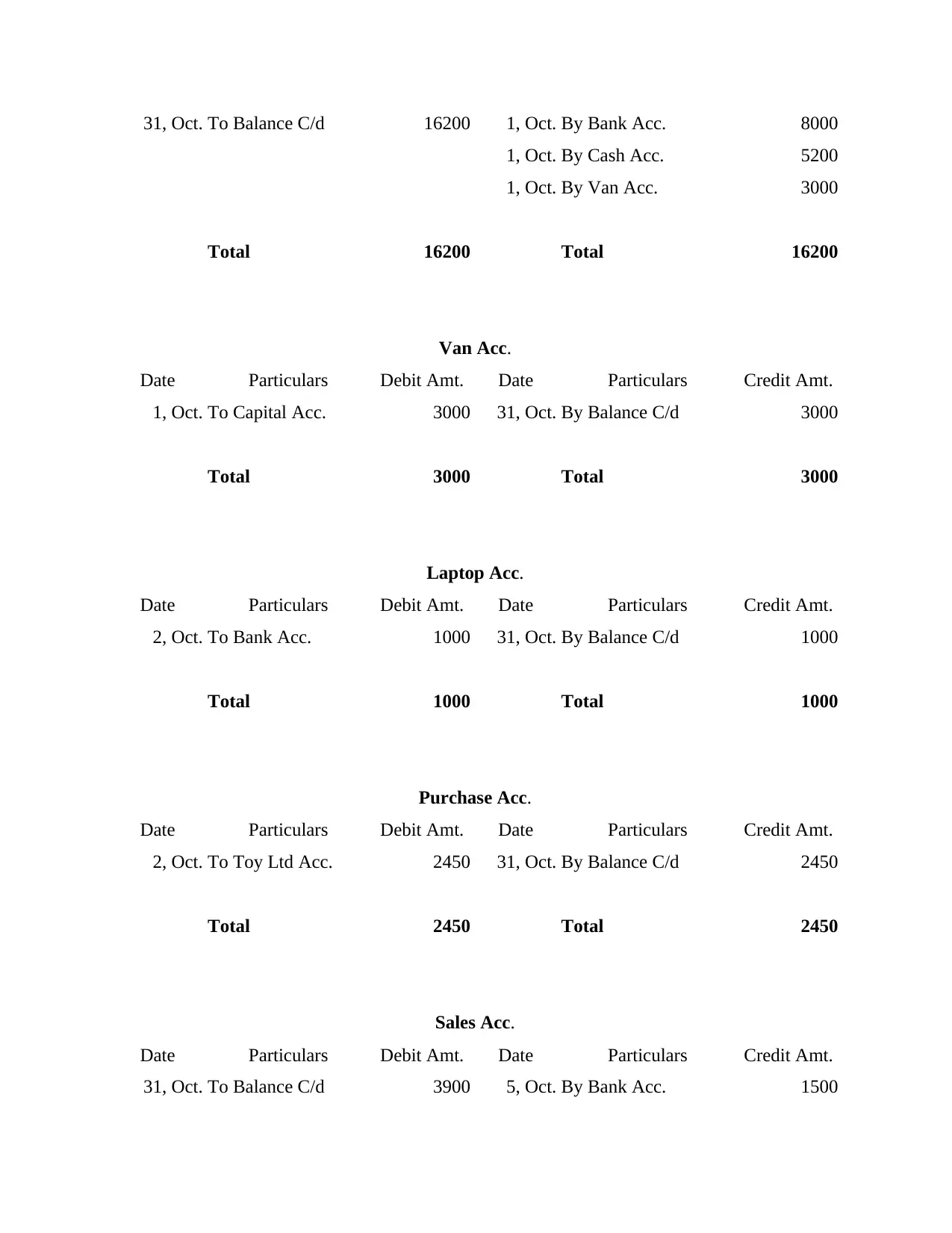

31, Oct. To Balance C/d 16200 1, Oct. By Bank Acc. 8000

1, Oct. By Cash Acc. 5200

1, Oct. By Van Acc. 3000

Total 16200 Total 16200

Van Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

1, Oct. To Capital Acc. 3000 31, Oct. By Balance C/d 3000

Total 3000 Total 3000

Laptop Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

2, Oct. To Bank Acc. 1000 31, Oct. By Balance C/d 1000

Total 1000 Total 1000

Purchase Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

2, Oct. To Toy Ltd Acc. 2450 31, Oct. By Balance C/d 2450

Total 2450 Total 2450

Sales Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

31, Oct. To Balance C/d 3900 5, Oct. By Bank Acc. 1500

1, Oct. By Cash Acc. 5200

1, Oct. By Van Acc. 3000

Total 16200 Total 16200

Van Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

1, Oct. To Capital Acc. 3000 31, Oct. By Balance C/d 3000

Total 3000 Total 3000

Laptop Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

2, Oct. To Bank Acc. 1000 31, Oct. By Balance C/d 1000

Total 1000 Total 1000

Purchase Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

2, Oct. To Toy Ltd Acc. 2450 31, Oct. By Balance C/d 2450

Total 2450 Total 2450

Sales Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

31, Oct. To Balance C/d 3900 5, Oct. By Bank Acc. 1500

23, Oct. By Cash Acc. 1500

23, Oct. By Fred Acc. 400

23, Oct. By Cash Acc. 500

Total 3900 Total 3900

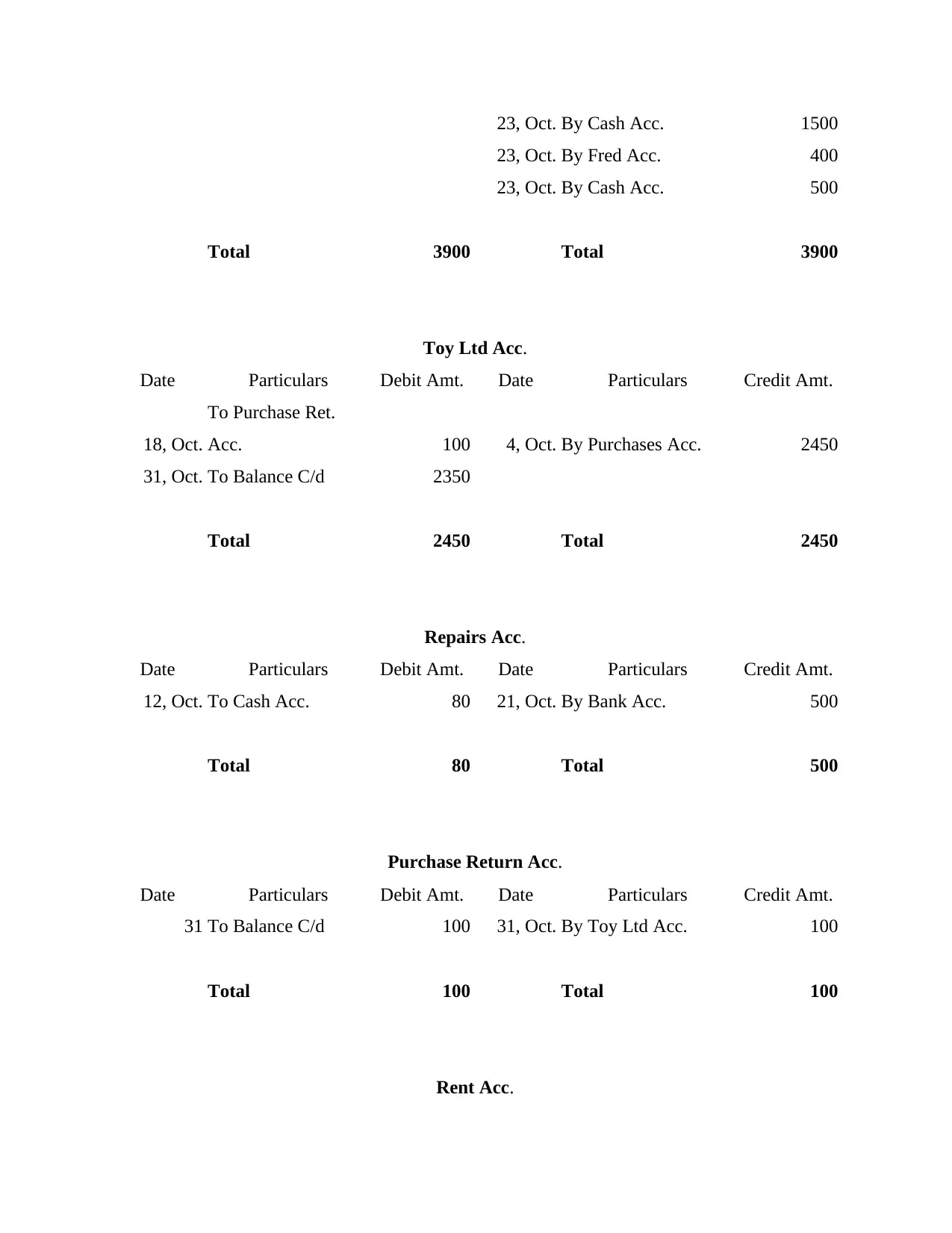

Toy Ltd Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

18, Oct.

To Purchase Ret.

Acc. 100 4, Oct. By Purchases Acc. 2450

31, Oct. To Balance C/d 2350

Total 2450 Total 2450

Repairs Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

12, Oct. To Cash Acc. 80 21, Oct. By Bank Acc. 500

Total 80 Total 500

Purchase Return Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

31 To Balance C/d 100 31, Oct. By Toy Ltd Acc. 100

Total 100 Total 100

Rent Acc.

23, Oct. By Fred Acc. 400

23, Oct. By Cash Acc. 500

Total 3900 Total 3900

Toy Ltd Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

18, Oct.

To Purchase Ret.

Acc. 100 4, Oct. By Purchases Acc. 2450

31, Oct. To Balance C/d 2350

Total 2450 Total 2450

Repairs Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

12, Oct. To Cash Acc. 80 21, Oct. By Bank Acc. 500

Total 80 Total 500

Purchase Return Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

31 To Balance C/d 100 31, Oct. By Toy Ltd Acc. 100

Total 100 Total 100

Rent Acc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Particulars Debit Amt. Date Particulars Credit Amt.

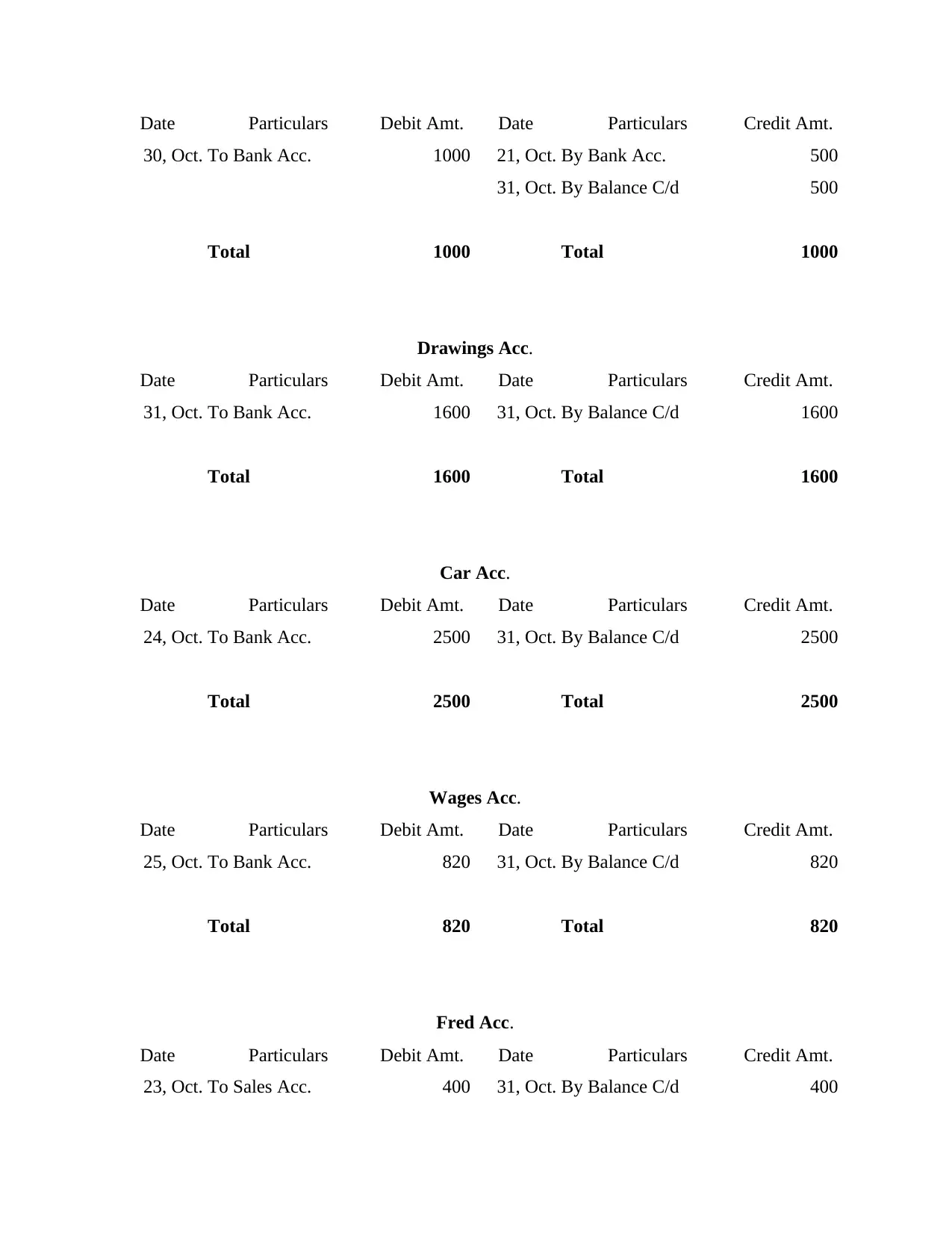

30, Oct. To Bank Acc. 1000 21, Oct. By Bank Acc. 500

31, Oct. By Balance C/d 500

Total 1000 Total 1000

Drawings Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

31, Oct. To Bank Acc. 1600 31, Oct. By Balance C/d 1600

Total 1600 Total 1600

Car Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

24, Oct. To Bank Acc. 2500 31, Oct. By Balance C/d 2500

Total 2500 Total 2500

Wages Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

25, Oct. To Bank Acc. 820 31, Oct. By Balance C/d 820

Total 820 Total 820

Fred Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

23, Oct. To Sales Acc. 400 31, Oct. By Balance C/d 400

30, Oct. To Bank Acc. 1000 21, Oct. By Bank Acc. 500

31, Oct. By Balance C/d 500

Total 1000 Total 1000

Drawings Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

31, Oct. To Bank Acc. 1600 31, Oct. By Balance C/d 1600

Total 1600 Total 1600

Car Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

24, Oct. To Bank Acc. 2500 31, Oct. By Balance C/d 2500

Total 2500 Total 2500

Wages Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

25, Oct. To Bank Acc. 820 31, Oct. By Balance C/d 820

Total 820 Total 820

Fred Acc.

Date Particulars Debit Amt. Date Particulars Credit Amt.

23, Oct. To Sales Acc. 400 31, Oct. By Balance C/d 400

Total 400 Total 400

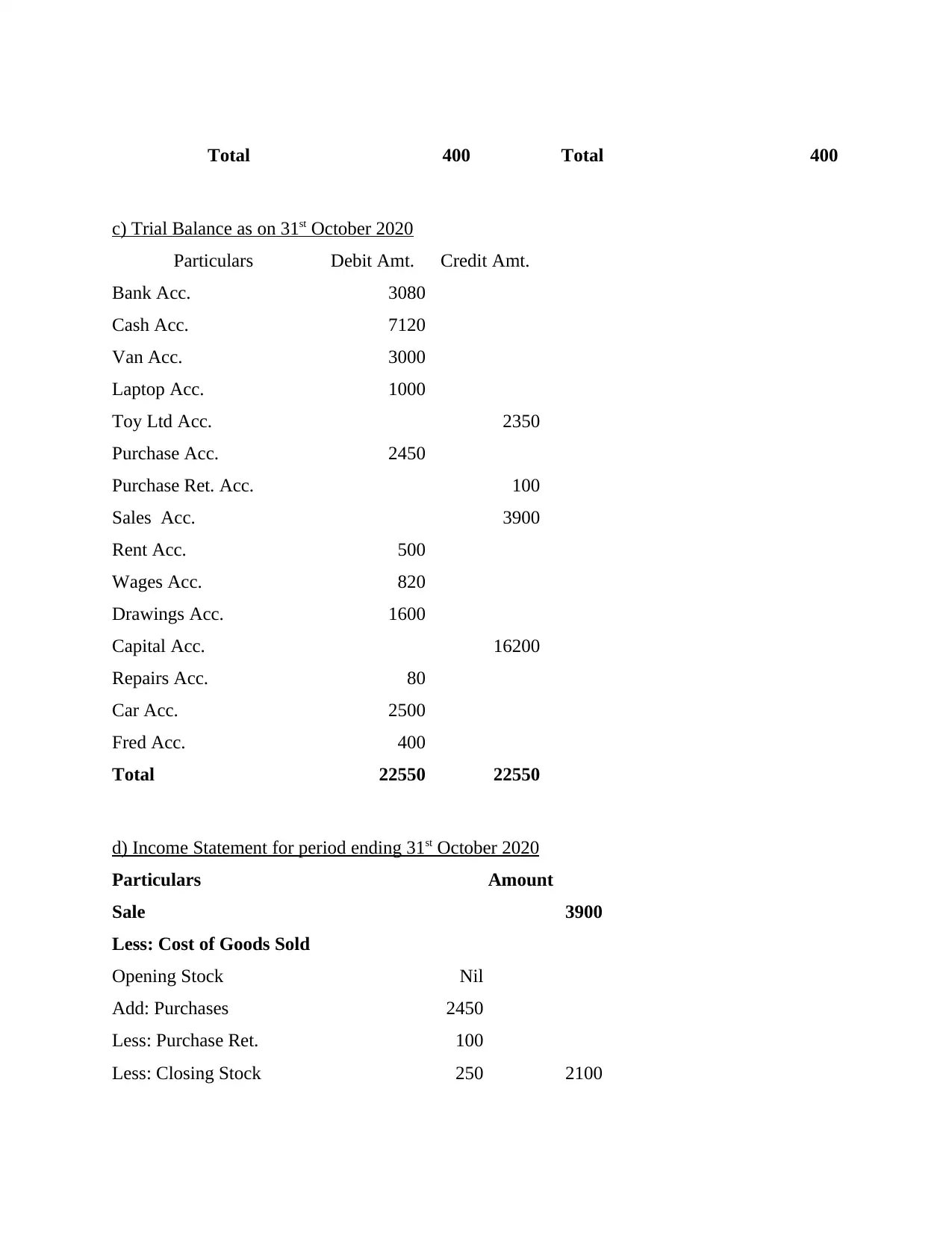

c) Trial Balance as on 31st October 2020

Particulars Debit Amt. Credit Amt.

Bank Acc. 3080

Cash Acc. 7120

Van Acc. 3000

Laptop Acc. 1000

Toy Ltd Acc. 2350

Purchase Acc. 2450

Purchase Ret. Acc. 100

Sales Acc. 3900

Rent Acc. 500

Wages Acc. 820

Drawings Acc. 1600

Capital Acc. 16200

Repairs Acc. 80

Car Acc. 2500

Fred Acc. 400

Total 22550 22550

d) Income Statement for period ending 31st October 2020

Particulars Amount

Sale 3900

Less: Cost of Goods Sold

Opening Stock Nil

Add: Purchases 2450

Less: Purchase Ret. 100

Less: Closing Stock 250 2100

c) Trial Balance as on 31st October 2020

Particulars Debit Amt. Credit Amt.

Bank Acc. 3080

Cash Acc. 7120

Van Acc. 3000

Laptop Acc. 1000

Toy Ltd Acc. 2350

Purchase Acc. 2450

Purchase Ret. Acc. 100

Sales Acc. 3900

Rent Acc. 500

Wages Acc. 820

Drawings Acc. 1600

Capital Acc. 16200

Repairs Acc. 80

Car Acc. 2500

Fred Acc. 400

Total 22550 22550

d) Income Statement for period ending 31st October 2020

Particulars Amount

Sale 3900

Less: Cost of Goods Sold

Opening Stock Nil

Add: Purchases 2450

Less: Purchase Ret. 100

Less: Closing Stock 250 2100

Gross Profit 1800

Less: Operating Expanses

Repairs 80

Wages 820

Rent 1000 1900

Add: Other Incomes

Rent 500

Net Profit 400

e) Financial Position as at 31st October 2020

Particulars Amount

Assets

Fixed Assets

Car 2500

Van 3000

Laptop 1000 6500

Current Assets

Cash 7120

Bank 3080

Debtors 400

Stock 250 10850

Total Assets 17350

Equity & Liability

Capital 16200

Less: Drawings 1600

Add: Profits 400 15000

Current Liabilities

Creditors 2350

Total Equity & Liability 17350

Less: Operating Expanses

Repairs 80

Wages 820

Rent 1000 1900

Add: Other Incomes

Rent 500

Net Profit 400

e) Financial Position as at 31st October 2020

Particulars Amount

Assets

Fixed Assets

Car 2500

Van 3000

Laptop 1000 6500

Current Assets

Cash 7120

Bank 3080

Debtors 400

Stock 250 10850

Total Assets 17350

Equity & Liability

Capital 16200

Less: Drawings 1600

Add: Profits 400 15000

Current Liabilities

Creditors 2350

Total Equity & Liability 17350

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

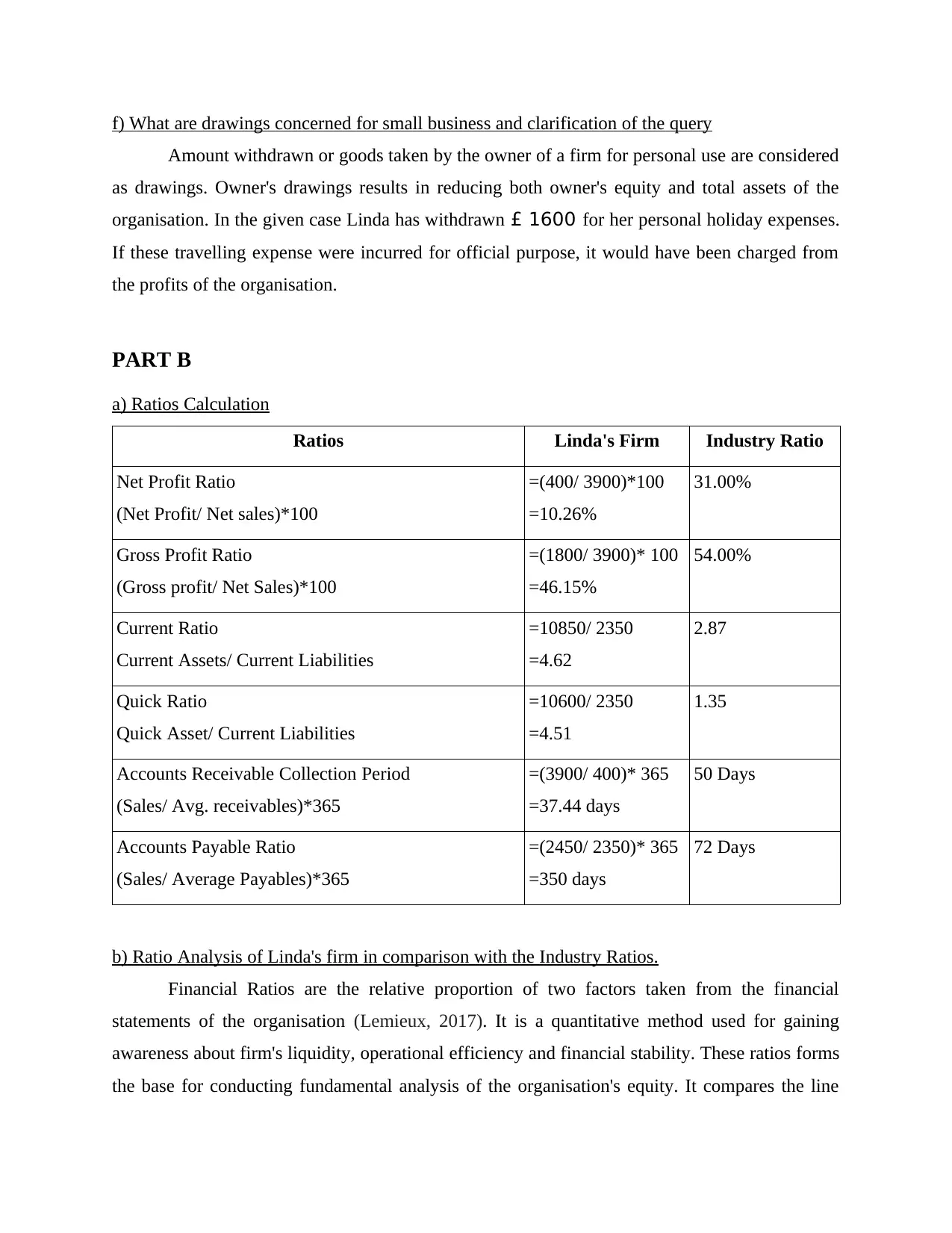

f) What are drawings concerned for small business and clarification of the query

Amount withdrawn or goods taken by the owner of a firm for personal use are considered

as drawings. Owner's drawings results in reducing both owner's equity and total assets of the

organisation. In the given case Linda has withdrawn £ 1600 for her personal holiday expenses.

If these travelling expense were incurred for official purpose, it would have been charged from

the profits of the organisation.

PART B

a) Ratios Calculation

Ratios Linda's Firm Industry Ratio

Net Profit Ratio

(Net Profit/ Net sales)*100

=(400/ 3900)*100

=10.26%

31.00%

Gross Profit Ratio

(Gross profit/ Net Sales)*100

=(1800/ 3900)* 100

=46.15%

54.00%

Current Ratio

Current Assets/ Current Liabilities

=10850/ 2350

=4.62

2.87

Quick Ratio

Quick Asset/ Current Liabilities

=10600/ 2350

=4.51

1.35

Accounts Receivable Collection Period

(Sales/ Avg. receivables)*365

=(3900/ 400)* 365

=37.44 days

50 Days

Accounts Payable Ratio

(Sales/ Average Payables)*365

=(2450/ 2350)* 365

=350 days

72 Days

b) Ratio Analysis of Linda's firm in comparison with the Industry Ratios.

Financial Ratios are the relative proportion of two factors taken from the financial

statements of the organisation (Lemieux, 2017). It is a quantitative method used for gaining

awareness about firm's liquidity, operational efficiency and financial stability. These ratios forms

the base for conducting fundamental analysis of the organisation's equity. It compares the line

Amount withdrawn or goods taken by the owner of a firm for personal use are considered

as drawings. Owner's drawings results in reducing both owner's equity and total assets of the

organisation. In the given case Linda has withdrawn £ 1600 for her personal holiday expenses.

If these travelling expense were incurred for official purpose, it would have been charged from

the profits of the organisation.

PART B

a) Ratios Calculation

Ratios Linda's Firm Industry Ratio

Net Profit Ratio

(Net Profit/ Net sales)*100

=(400/ 3900)*100

=10.26%

31.00%

Gross Profit Ratio

(Gross profit/ Net Sales)*100

=(1800/ 3900)* 100

=46.15%

54.00%

Current Ratio

Current Assets/ Current Liabilities

=10850/ 2350

=4.62

2.87

Quick Ratio

Quick Asset/ Current Liabilities

=10600/ 2350

=4.51

1.35

Accounts Receivable Collection Period

(Sales/ Avg. receivables)*365

=(3900/ 400)* 365

=37.44 days

50 Days

Accounts Payable Ratio

(Sales/ Average Payables)*365

=(2450/ 2350)* 365

=350 days

72 Days

b) Ratio Analysis of Linda's firm in comparison with the Industry Ratios.

Financial Ratios are the relative proportion of two factors taken from the financial

statements of the organisation (Lemieux, 2017). It is a quantitative method used for gaining

awareness about firm's liquidity, operational efficiency and financial stability. These ratios forms

the base for conducting fundamental analysis of the organisation's equity. It compares the line

items information and mark company's performance over a period of time and facilitates

comparison with company's past performance and other competitors of the industry. Analysis of

above computed ratios are as follows:

Net Profit Ratio- It shows the proportion between the net profit earned by the company

after paying off its tax liability with the net sales made over a period of time. It is

computed by dividing net profit by net sales. Linda's NP ratio is very less in comparison

with that of the industry, she should work on maximising it.

Gross Profit Ratio- It is the profitability ratio that shows the relationship between the

gross profit earned with the net sales of the company. It is used foe evaluating the

operational efficiency of the company (Rechtman, 2017). In the give case Linda is

earning a good gross profit in comparison with that of the industry.

Current Ratio- It is used for evaluating the firms ability to pay its short term liabilities.

The ideal current ratio is 2:1. It is the most popular tool used by creditors and analysts in

gaining knowledge that if the company is in a position to pay off their debts using its

current assets. Linda's firm current ratio is not good enough both when compared to the

industry average ratio or with the ideal ratio. She should work on improving this ratio.

Quick Ratio- It is used for indicating company's ability for paying off its short term

liabilities without utilising its stock or getting additional funding. The high the ratio is the

better it is for the company. It can be stated that Linda's firm is having a good quick ratio.

Account- Receivable Ratio- It measures firms efficiency for collecting money from its

debtors (Smith and Williams, 2018). It illustrates how well the company manages its

credit extension to its customers and how quickly they are realised.

Accounts Payable Ratio- It is used for analysing the firm's ability for paying its

creditors in the minimum possible time. It represents how many times the company pays

off its accounts.

CONCLUSION

From the above report it can be concluded that financial statements plays a vital role in

analysing and comparing a company's performance with its past and also with other its

competitors of the industry. Ratio analysis facilitates in evaluating the company's performance,

find deviation and taking corrective measures.

comparison with company's past performance and other competitors of the industry. Analysis of

above computed ratios are as follows:

Net Profit Ratio- It shows the proportion between the net profit earned by the company

after paying off its tax liability with the net sales made over a period of time. It is

computed by dividing net profit by net sales. Linda's NP ratio is very less in comparison

with that of the industry, she should work on maximising it.

Gross Profit Ratio- It is the profitability ratio that shows the relationship between the

gross profit earned with the net sales of the company. It is used foe evaluating the

operational efficiency of the company (Rechtman, 2017). In the give case Linda is

earning a good gross profit in comparison with that of the industry.

Current Ratio- It is used for evaluating the firms ability to pay its short term liabilities.

The ideal current ratio is 2:1. It is the most popular tool used by creditors and analysts in

gaining knowledge that if the company is in a position to pay off their debts using its

current assets. Linda's firm current ratio is not good enough both when compared to the

industry average ratio or with the ideal ratio. She should work on improving this ratio.

Quick Ratio- It is used for indicating company's ability for paying off its short term

liabilities without utilising its stock or getting additional funding. The high the ratio is the

better it is for the company. It can be stated that Linda's firm is having a good quick ratio.

Account- Receivable Ratio- It measures firms efficiency for collecting money from its

debtors (Smith and Williams, 2018). It illustrates how well the company manages its

credit extension to its customers and how quickly they are realised.

Accounts Payable Ratio- It is used for analysing the firm's ability for paying its

creditors in the minimum possible time. It represents how many times the company pays

off its accounts.

CONCLUSION

From the above report it can be concluded that financial statements plays a vital role in

analysing and comparing a company's performance with its past and also with other its

competitors of the industry. Ratio analysis facilitates in evaluating the company's performance,

find deviation and taking corrective measures.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Chow, D.C. and Schoenbaum, T.J., 2020. International business transactions: problems, cases,

and materials. Wolters Kluwer Law & Business.

Lemieux, V.L., 2017. Evaluating the use of blockchain in land transactions: An archival science

perspective. European Property Law Journal. 6(3). pp.392-440.

Rechtman, Y., 2017. Blockchain: The Making of a Simple, Secure Recording Concept. The CPA

Journal. 87(6). pp.15-17.

Smith, D.G. and Williams, C.A., 2018. Business Organizations: Cases, Problems, and Case

Studies. Aspen Publishers.

Books and Journals

Chow, D.C. and Schoenbaum, T.J., 2020. International business transactions: problems, cases,

and materials. Wolters Kluwer Law & Business.

Lemieux, V.L., 2017. Evaluating the use of blockchain in land transactions: An archival science

perspective. European Property Law Journal. 6(3). pp.392-440.

Rechtman, Y., 2017. Blockchain: The Making of a Simple, Secure Recording Concept. The CPA

Journal. 87(6). pp.15-17.

Smith, D.G. and Williams, C.A., 2018. Business Organizations: Cases, Problems, and Case

Studies. Aspen Publishers.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.