University of West London: Recording Business Transactions Assignment

VerifiedAdded on 2022/12/28

|14

|2431

|96

Homework Assignment

AI Summary

This assignment focuses on the process of recording business transactions for Linda Ltd. It begins with journal entries detailing various transactions, followed by the creation of ledger accounts and the extraction of a trial balance. The assignment then proceeds to prepare a profitability statement and a...

RECORDING BUSINESS

TRANSACTION

TRANSACTION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................2

PART A...........................................................................................................................................2

(a) Journal Entries in the books of Linda Ltd..............................................................................2

(B) Ledger A/c.............................................................................................................................4

(c). Extracting a trial balance.......................................................................................................5

(d). Preparing profitability statement for the year ended on 31st Oct 2020.................................7

(e). Drafting statement of financial position for Linda business Ltd...........................................7

(f). Presenting a brief letter to Linda Ltd for explaining concerns about drawings.....................8

PART B...........................................................................................................................................9

(i) Calculating ratios for Linda Ltd..............................................................................................9

(ii) Analysis of Linda's financial performance..........................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

1

INTRODUCTION...........................................................................................................................2

PART A...........................................................................................................................................2

(a) Journal Entries in the books of Linda Ltd..............................................................................2

(B) Ledger A/c.............................................................................................................................4

(c). Extracting a trial balance.......................................................................................................5

(d). Preparing profitability statement for the year ended on 31st Oct 2020.................................7

(e). Drafting statement of financial position for Linda business Ltd...........................................7

(f). Presenting a brief letter to Linda Ltd for explaining concerns about drawings.....................8

PART B...........................................................................................................................................9

(i) Calculating ratios for Linda Ltd..............................................................................................9

(ii) Analysis of Linda's financial performance..........................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

1

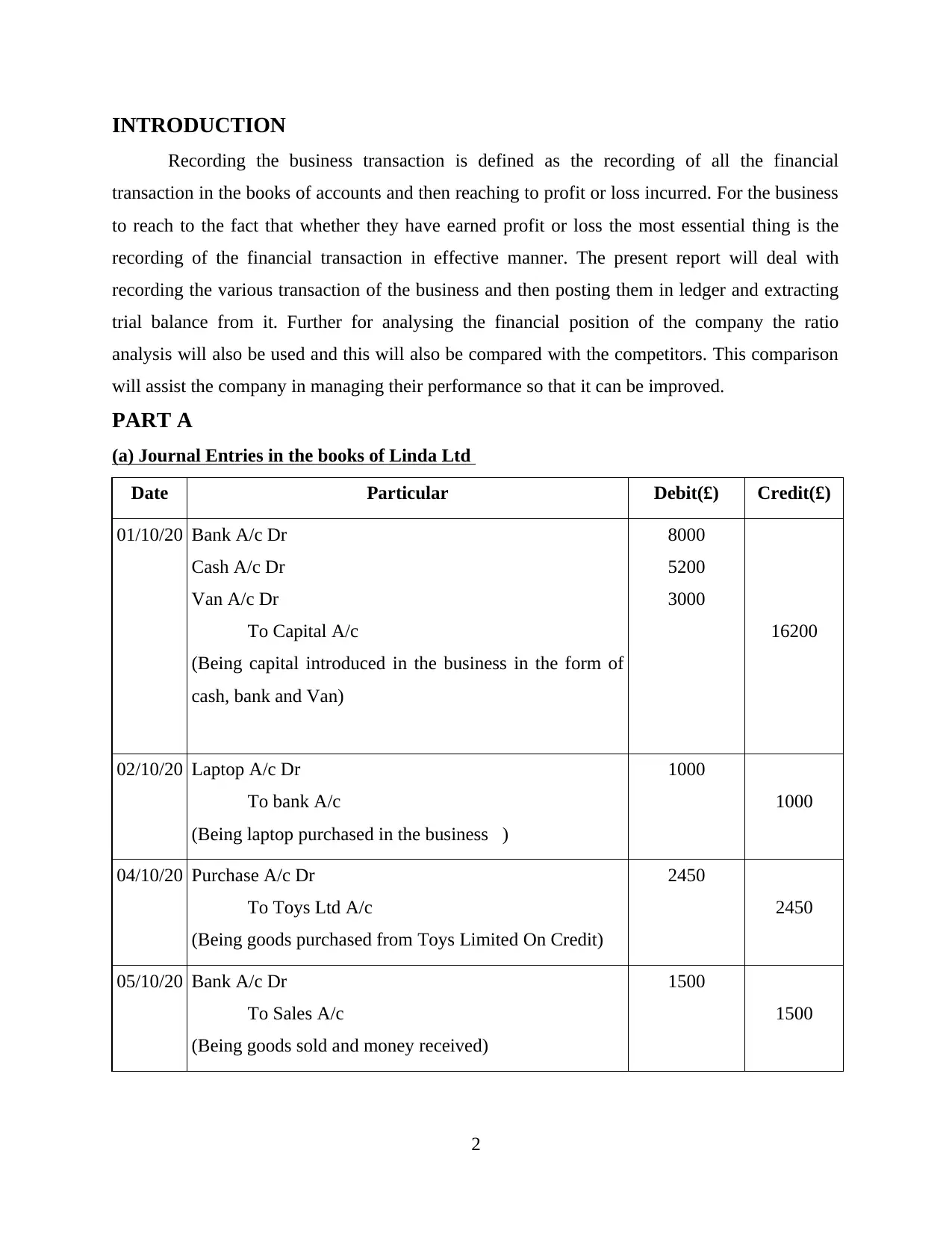

INTRODUCTION

Recording the business transaction is defined as the recording of all the financial

transaction in the books of accounts and then reaching to profit or loss incurred. For the business

to reach to the fact that whether they have earned profit or loss the most essential thing is the

recording of the financial transaction in effective manner. The present report will deal with

recording the various transaction of the business and then posting them in ledger and extracting

trial balance from it. Further for analysing the financial position of the company the ratio

analysis will also be used and this will also be compared with the competitors. This comparison

will assist the company in managing their performance so that it can be improved.

PART A

(a) Journal Entries in the books of Linda Ltd

Date Particular Debit(£) Credit(£)

01/10/20 Bank A/c Dr

Cash A/c Dr

Van A/c Dr

To Capital A/c

(Being capital introduced in the business in the form of

cash, bank and Van)

8000

5200

3000

16200

02/10/20 Laptop A/c Dr

To bank A/c

(Being laptop purchased in the business )

1000

1000

04/10/20 Purchase A/c Dr

To Toys Ltd A/c

(Being goods purchased from Toys Limited On Credit)

2450

2450

05/10/20 Bank A/c Dr

To Sales A/c

(Being goods sold and money received)

1500

1500

2

Recording the business transaction is defined as the recording of all the financial

transaction in the books of accounts and then reaching to profit or loss incurred. For the business

to reach to the fact that whether they have earned profit or loss the most essential thing is the

recording of the financial transaction in effective manner. The present report will deal with

recording the various transaction of the business and then posting them in ledger and extracting

trial balance from it. Further for analysing the financial position of the company the ratio

analysis will also be used and this will also be compared with the competitors. This comparison

will assist the company in managing their performance so that it can be improved.

PART A

(a) Journal Entries in the books of Linda Ltd

Date Particular Debit(£) Credit(£)

01/10/20 Bank A/c Dr

Cash A/c Dr

Van A/c Dr

To Capital A/c

(Being capital introduced in the business in the form of

cash, bank and Van)

8000

5200

3000

16200

02/10/20 Laptop A/c Dr

To bank A/c

(Being laptop purchased in the business )

1000

1000

04/10/20 Purchase A/c Dr

To Toys Ltd A/c

(Being goods purchased from Toys Limited On Credit)

2450

2450

05/10/20 Bank A/c Dr

To Sales A/c

(Being goods sold and money received)

1500

1500

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

12/10/20 Repairing A/c Dr

To cash A/c

(Being laptop Repaired and paid in cash)

80

80

18/10/20 Toys Ltd A/c Dr

To Purchase Return A/c

(Being goods return To Toys limited)

100

100

21/10/20 Bank A/c Dr

To Rent A/c

(Being Rent received for premises By cheque)

500

500

23/10/20 Cash A/c Dr

To sales A/c

(Being good sold to David And received cash)

500

500

23/10/20 Cash a/c Dr

Fred A/c Dr

To sales a/c

(being goods sold to Fred in cash and credit both)

1500

400

1900

24/10/20 Car A/c Dr

To Bank A/c

(Being car purchased from Ox Ford motor vehicle

Auction)

2500

2500

26/10/20 Wages A/c Dr

To Bank A/c

(Being wages paid By cheque)

820

820

30/10/20 Rent A/c Dr

To Bank a/c

(being wages paid to the part time shopkeeper)

1000

1000

31/10/20 Drawings A/c Dr

To bank a/c

1600

1600

3

To cash A/c

(Being laptop Repaired and paid in cash)

80

80

18/10/20 Toys Ltd A/c Dr

To Purchase Return A/c

(Being goods return To Toys limited)

100

100

21/10/20 Bank A/c Dr

To Rent A/c

(Being Rent received for premises By cheque)

500

500

23/10/20 Cash A/c Dr

To sales A/c

(Being good sold to David And received cash)

500

500

23/10/20 Cash a/c Dr

Fred A/c Dr

To sales a/c

(being goods sold to Fred in cash and credit both)

1500

400

1900

24/10/20 Car A/c Dr

To Bank A/c

(Being car purchased from Ox Ford motor vehicle

Auction)

2500

2500

26/10/20 Wages A/c Dr

To Bank A/c

(Being wages paid By cheque)

820

820

30/10/20 Rent A/c Dr

To Bank a/c

(being wages paid to the part time shopkeeper)

1000

1000

31/10/20 Drawings A/c Dr

To bank a/c

1600

1600

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

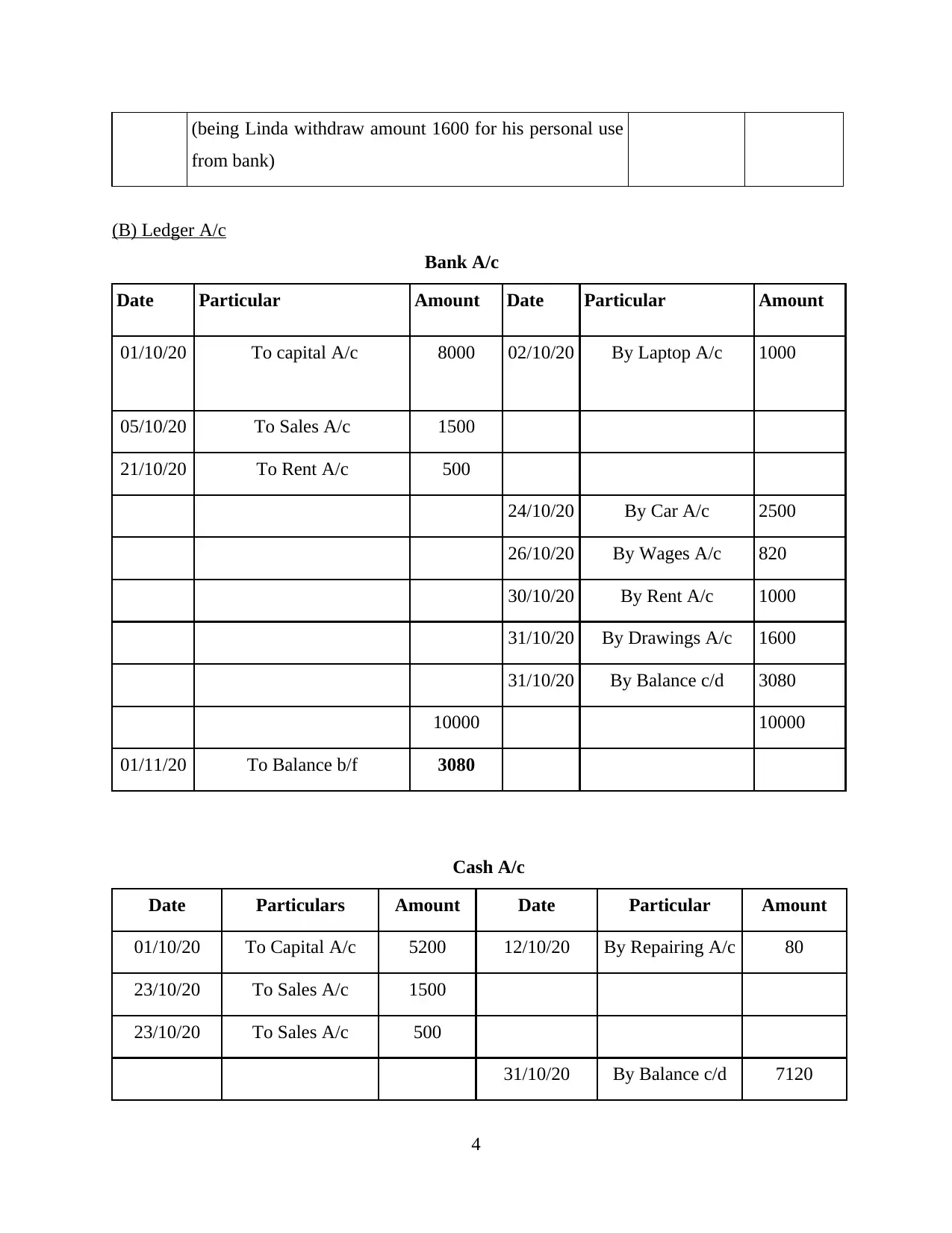

(being Linda withdraw amount 1600 for his personal use

from bank)

(B) Ledger A/c

Bank A/c

Date Particular Amount Date Particular Amount

01/10/20 To capital A/c 8000 02/10/20 By Laptop A/c 1000

05/10/20 To Sales A/c 1500

21/10/20 To Rent A/c 500

24/10/20 By Car A/c 2500

26/10/20 By Wages A/c 820

30/10/20 By Rent A/c 1000

31/10/20 By Drawings A/c 1600

31/10/20 By Balance c/d 3080

10000 10000

01/11/20 To Balance b/f 3080

Cash A/c

Date Particulars Amount Date Particular Amount

01/10/20 To Capital A/c 5200 12/10/20 By Repairing A/c 80

23/10/20 To Sales A/c 1500

23/10/20 To Sales A/c 500

31/10/20 By Balance c/d 7120

4

from bank)

(B) Ledger A/c

Bank A/c

Date Particular Amount Date Particular Amount

01/10/20 To capital A/c 8000 02/10/20 By Laptop A/c 1000

05/10/20 To Sales A/c 1500

21/10/20 To Rent A/c 500

24/10/20 By Car A/c 2500

26/10/20 By Wages A/c 820

30/10/20 By Rent A/c 1000

31/10/20 By Drawings A/c 1600

31/10/20 By Balance c/d 3080

10000 10000

01/11/20 To Balance b/f 3080

Cash A/c

Date Particulars Amount Date Particular Amount

01/10/20 To Capital A/c 5200 12/10/20 By Repairing A/c 80

23/10/20 To Sales A/c 1500

23/10/20 To Sales A/c 500

31/10/20 By Balance c/d 7120

4

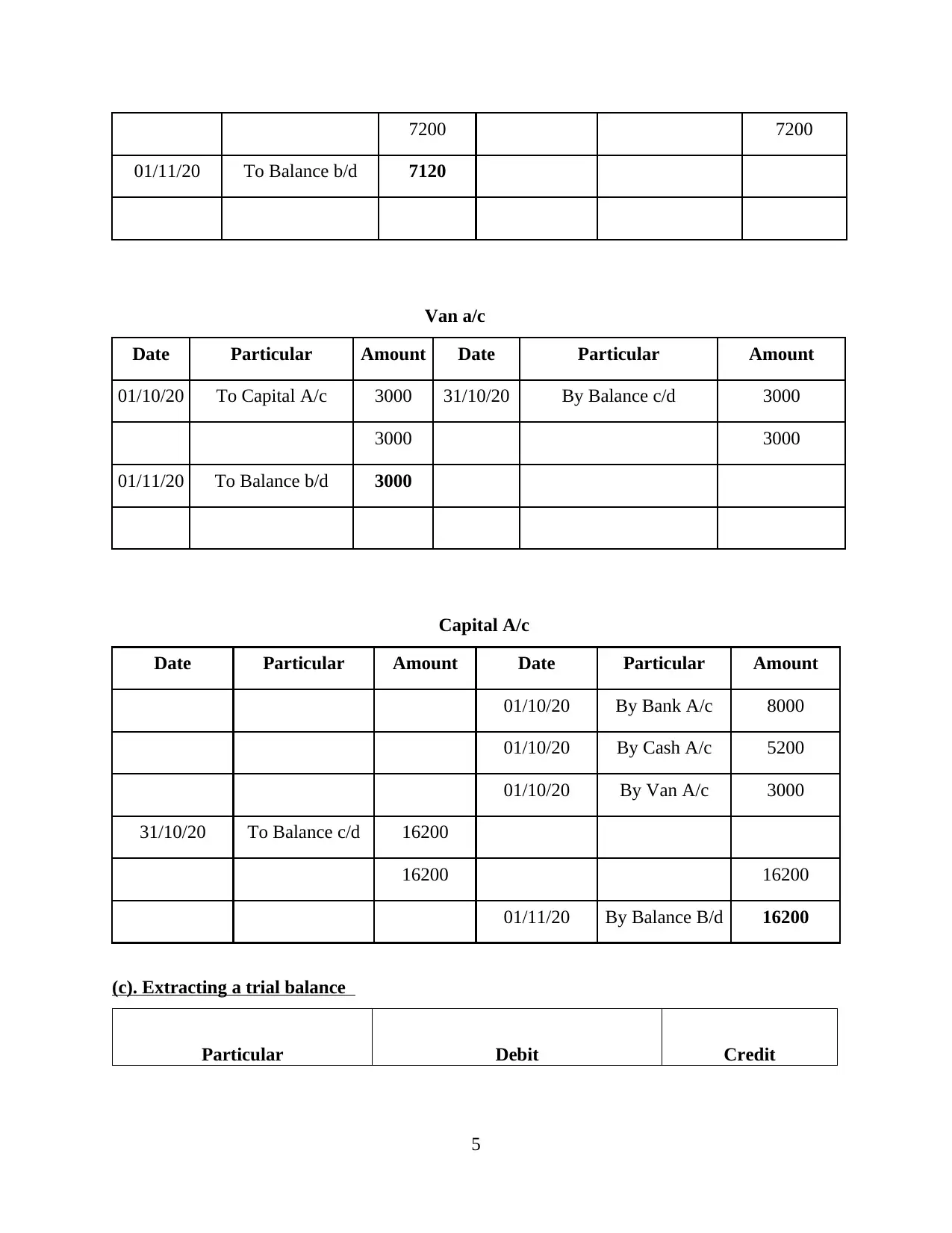

7200 7200

01/11/20 To Balance b/d 7120

Van a/c

Date Particular Amount Date Particular Amount

01/10/20 To Capital A/c 3000 31/10/20 By Balance c/d 3000

3000 3000

01/11/20 To Balance b/d 3000

Capital A/c

Date Particular Amount Date Particular Amount

01/10/20 By Bank A/c 8000

01/10/20 By Cash A/c 5200

01/10/20 By Van A/c 3000

31/10/20 To Balance c/d 16200

16200 16200

01/11/20 By Balance B/d 16200

(c). Extracting a trial balance

Particular Debit Credit

5

01/11/20 To Balance b/d 7120

Van a/c

Date Particular Amount Date Particular Amount

01/10/20 To Capital A/c 3000 31/10/20 By Balance c/d 3000

3000 3000

01/11/20 To Balance b/d 3000

Capital A/c

Date Particular Amount Date Particular Amount

01/10/20 By Bank A/c 8000

01/10/20 By Cash A/c 5200

01/10/20 By Van A/c 3000

31/10/20 To Balance c/d 16200

16200 16200

01/11/20 By Balance B/d 16200

(c). Extracting a trial balance

Particular Debit Credit

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

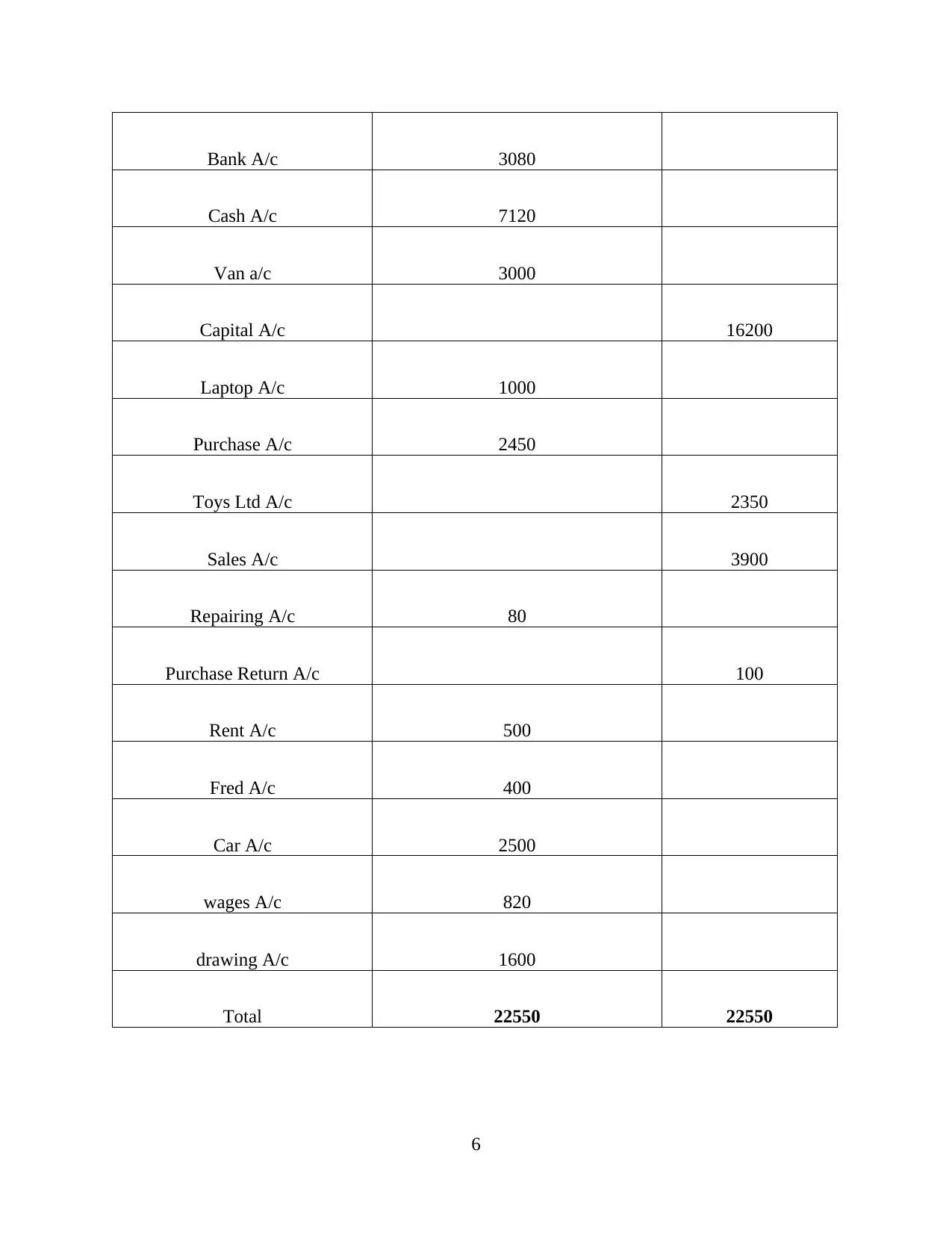

Bank A/c 3080

Cash A/c 7120

Van a/c 3000

Capital A/c 16200

Laptop A/c 1000

Purchase A/c 2450

Toys Ltd A/c 2350

Sales A/c 3900

Repairing A/c 80

Purchase Return A/c 100

Rent A/c 500

Fred A/c 400

Car A/c 2500

wages A/c 820

drawing A/c 1600

Total 22550 22550

6

Cash A/c 7120

Van a/c 3000

Capital A/c 16200

Laptop A/c 1000

Purchase A/c 2450

Toys Ltd A/c 2350

Sales A/c 3900

Repairing A/c 80

Purchase Return A/c 100

Rent A/c 500

Fred A/c 400

Car A/c 2500

wages A/c 820

drawing A/c 1600

Total 22550 22550

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

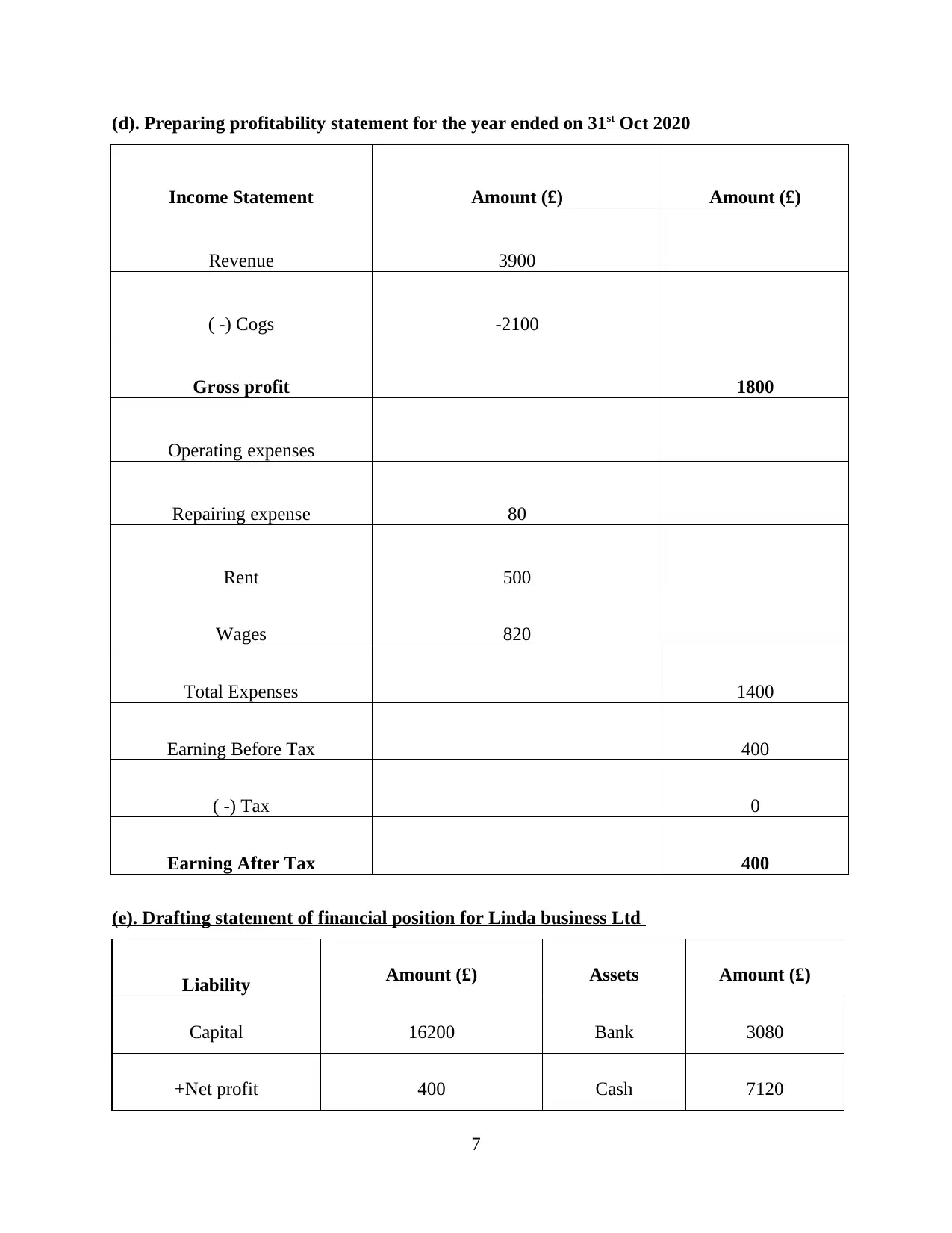

(d). Preparing profitability statement for the year ended on 31st Oct 2020

Income Statement Amount (£) Amount (£)

Revenue 3900

( -) Cogs -2100

Gross profit 1800

Operating expenses

Repairing expense 80

Rent 500

Wages 820

Total Expenses 1400

Earning Before Tax 400

( -) Tax 0

Earning After Tax 400

(e). Drafting statement of financial position for Linda business Ltd

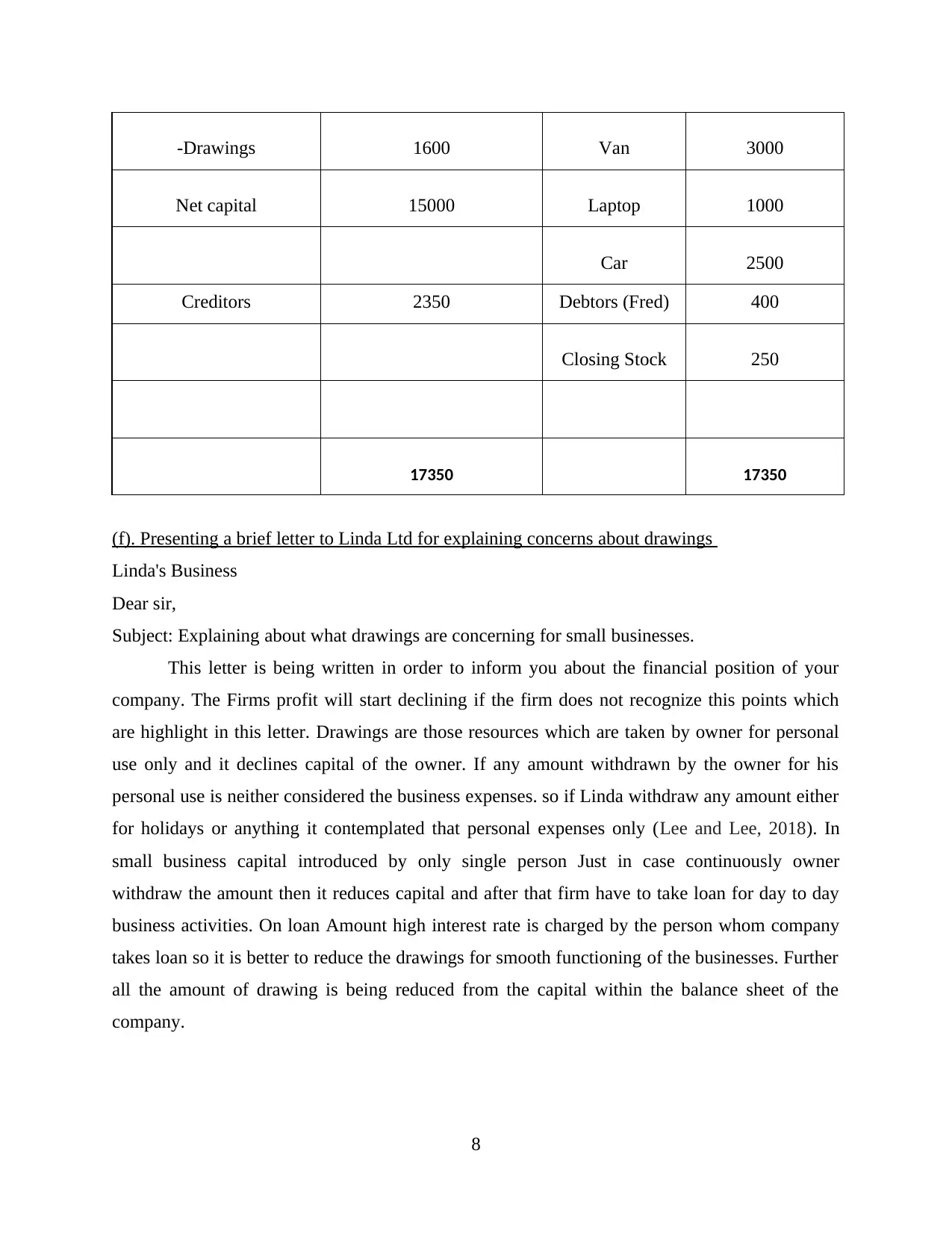

Liability Amount (£) Assets Amount (£)

Capital 16200 Bank 3080

+Net profit 400 Cash 7120

7

Income Statement Amount (£) Amount (£)

Revenue 3900

( -) Cogs -2100

Gross profit 1800

Operating expenses

Repairing expense 80

Rent 500

Wages 820

Total Expenses 1400

Earning Before Tax 400

( -) Tax 0

Earning After Tax 400

(e). Drafting statement of financial position for Linda business Ltd

Liability Amount (£) Assets Amount (£)

Capital 16200 Bank 3080

+Net profit 400 Cash 7120

7

-Drawings 1600 Van 3000

Net capital 15000 Laptop 1000

Car 2500

Creditors 2350 Debtors (Fred) 400

Closing Stock 250

17350 17350

(f). Presenting a brief letter to Linda Ltd for explaining concerns about drawings

Linda's Business

Dear sir,

Subject: Explaining about what drawings are concerning for small businesses.

This letter is being written in order to inform you about the financial position of your

company. The Firms profit will start declining if the firm does not recognize this points which

are highlight in this letter. Drawings are those resources which are taken by owner for personal

use only and it declines capital of the owner. If any amount withdrawn by the owner for his

personal use is neither considered the business expenses. so if Linda withdraw any amount either

for holidays or anything it contemplated that personal expenses only (Lee and Lee, 2018). In

small business capital introduced by only single person Just in case continuously owner

withdraw the amount then it reduces capital and after that firm have to take loan for day to day

business activities. On loan Amount high interest rate is charged by the person whom company

takes loan so it is better to reduce the drawings for smooth functioning of the businesses. Further

all the amount of drawing is being reduced from the capital within the balance sheet of the

company.

8

Net capital 15000 Laptop 1000

Car 2500

Creditors 2350 Debtors (Fred) 400

Closing Stock 250

17350 17350

(f). Presenting a brief letter to Linda Ltd for explaining concerns about drawings

Linda's Business

Dear sir,

Subject: Explaining about what drawings are concerning for small businesses.

This letter is being written in order to inform you about the financial position of your

company. The Firms profit will start declining if the firm does not recognize this points which

are highlight in this letter. Drawings are those resources which are taken by owner for personal

use only and it declines capital of the owner. If any amount withdrawn by the owner for his

personal use is neither considered the business expenses. so if Linda withdraw any amount either

for holidays or anything it contemplated that personal expenses only (Lee and Lee, 2018). In

small business capital introduced by only single person Just in case continuously owner

withdraw the amount then it reduces capital and after that firm have to take loan for day to day

business activities. On loan Amount high interest rate is charged by the person whom company

takes loan so it is better to reduce the drawings for smooth functioning of the businesses. Further

all the amount of drawing is being reduced from the capital within the balance sheet of the

company.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART B

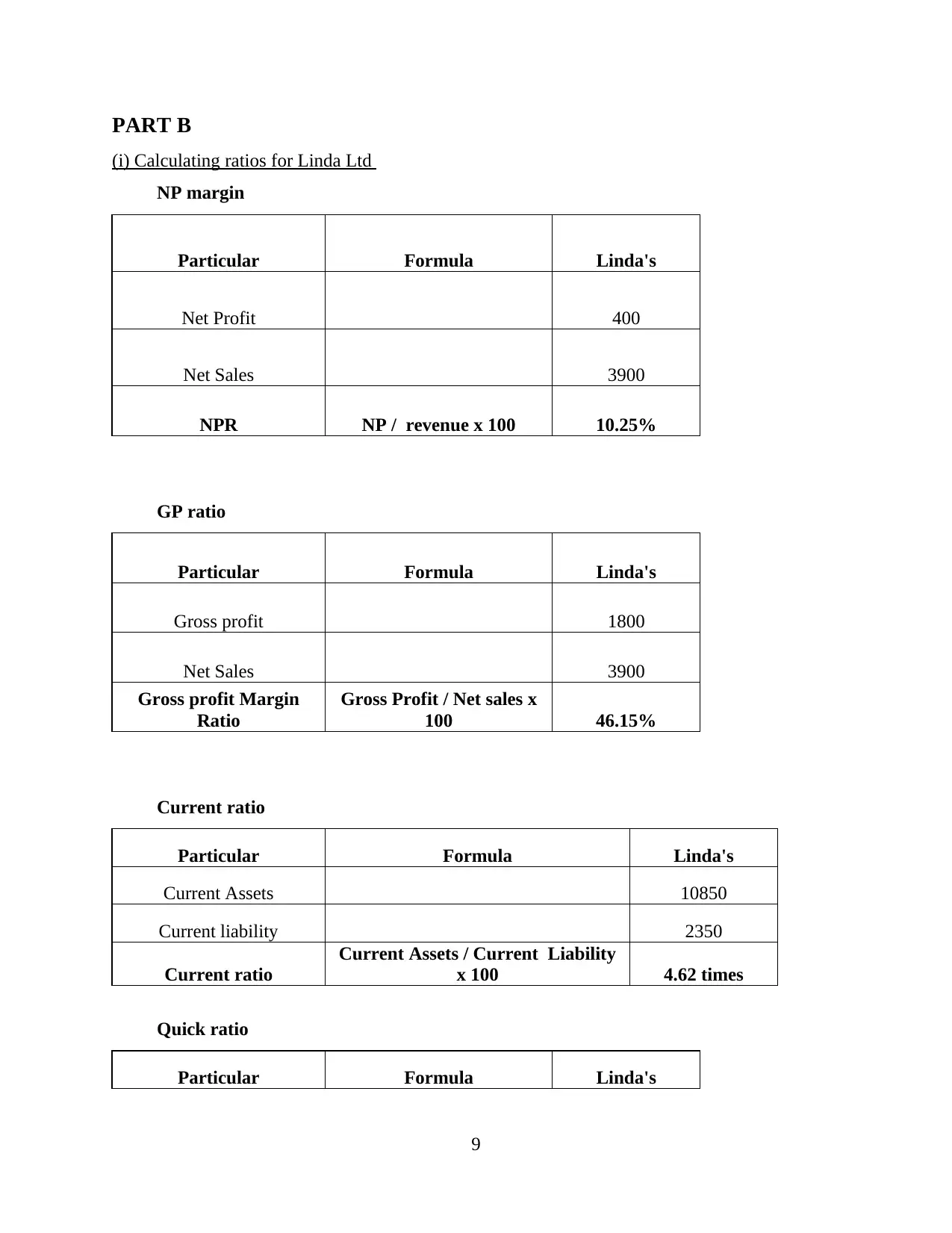

(i) Calculating ratios for Linda Ltd

NP margin

Particular Formula Linda's

Net Profit 400

Net Sales 3900

NPR NP / revenue x 100 10.25%

GP ratio

Particular Formula Linda's

Gross profit 1800

Net Sales 3900

Gross profit Margin

Ratio

Gross Profit / Net sales x

100 46.15%

Current ratio

Particular Formula Linda's

Current Assets 10850

Current liability 2350

Current ratio

Current Assets / Current Liability

x 100 4.62 times

Quick ratio

Particular Formula Linda's

9

(i) Calculating ratios for Linda Ltd

NP margin

Particular Formula Linda's

Net Profit 400

Net Sales 3900

NPR NP / revenue x 100 10.25%

GP ratio

Particular Formula Linda's

Gross profit 1800

Net Sales 3900

Gross profit Margin

Ratio

Gross Profit / Net sales x

100 46.15%

Current ratio

Particular Formula Linda's

Current Assets 10850

Current liability 2350

Current ratio

Current Assets / Current Liability

x 100 4.62 times

Quick ratio

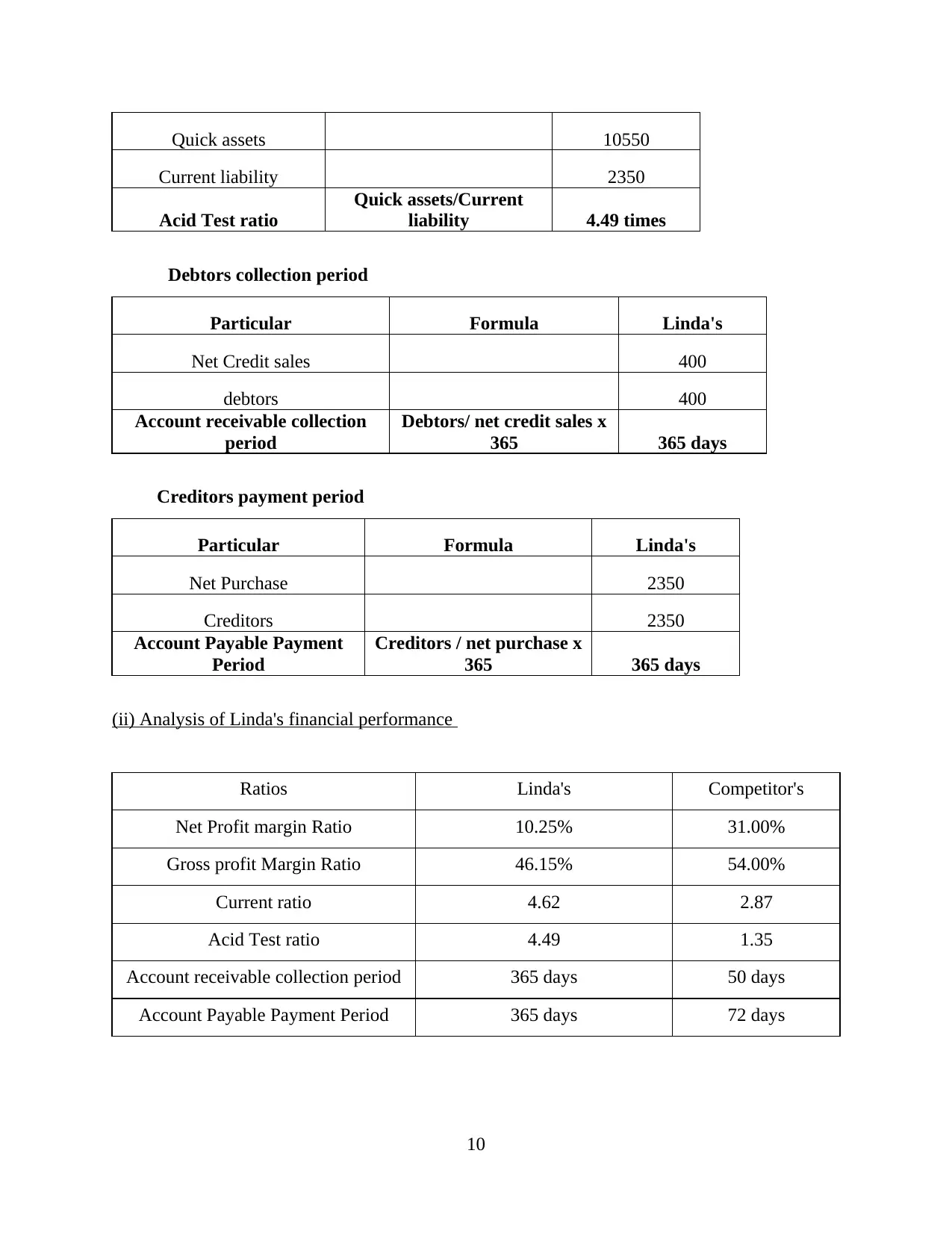

Particular Formula Linda's

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Quick assets 10550

Current liability 2350

Acid Test ratio

Quick assets/Current

liability 4.49 times

Debtors collection period

Particular Formula Linda's

Net Credit sales 400

debtors 400

Account receivable collection

period

Debtors/ net credit sales x

365 365 days

Creditors payment period

Particular Formula Linda's

Net Purchase 2350

Creditors 2350

Account Payable Payment

Period

Creditors / net purchase x

365 365 days

(ii) Analysis of Linda's financial performance

Ratios Linda's Competitor's

Net Profit margin Ratio 10.25% 31.00%

Gross profit Margin Ratio 46.15% 54.00%

Current ratio 4.62 2.87

Acid Test ratio 4.49 1.35

Account receivable collection period 365 days 50 days

Account Payable Payment Period 365 days 72 days

10

Current liability 2350

Acid Test ratio

Quick assets/Current

liability 4.49 times

Debtors collection period

Particular Formula Linda's

Net Credit sales 400

debtors 400

Account receivable collection

period

Debtors/ net credit sales x

365 365 days

Creditors payment period

Particular Formula Linda's

Net Purchase 2350

Creditors 2350

Account Payable Payment

Period

Creditors / net purchase x

365 365 days

(ii) Analysis of Linda's financial performance

Ratios Linda's Competitor's

Net Profit margin Ratio 10.25% 31.00%

Gross profit Margin Ratio 46.15% 54.00%

Current ratio 4.62 2.87

Acid Test ratio 4.49 1.35

Account receivable collection period 365 days 50 days

Account Payable Payment Period 365 days 72 days

10

On the basis of Ratio Analysis Financial performance of Linda's business is being

calculated. From the above calculation it was shown that Linda profit margin ratio for the year

ended is 10.25% which shows that company is earning high profit and maximize its revenue.

while on the other side in comparison with competitors firm Linda's net profit shows lower.

Competitors NP ratio is 31% which is 20% higher from Linda's business (Kim and Im, 2017). So

company need to be mainly focused on increasing profit by declining its operating expenses and

expanding sales. In order to increase the net profit of the company it is required for the effective

and efficient reduction in the indirect expenses of the company. the major reason for this is that if

the indirect expense will be low then the net profit of the company will be increased.

As shown in above table companies GP ratio is low from its competitor. It is necessary

for the company to reduced expenses and implement strategies to maximize sales. The reason

behind the lower gross margin may be a higher cost of production or declining sales price, or if

there is any change in the sales mix. All these factors need in-depth analysis and watch

throughout the year to avoid a situation of lower gross margins. For increasing gross profit firm

need to identify those areas where company bears high expenses so only by controlling those

expenses firm increasing GP. Further in addition to this for increasing the profitability of the

company, it can go for the option of marketing so that the company can improve the sales. This

result in increase in the sales of the company and as a result of this the profitability of the

company will increase.

It was further evaluated that company’s current and quick asset ratio is very high this

shows firm has more investment in the current assets and block the funds on that assets. For

Improving this firm have to pay of its current obligations on time and can withdraw the amount

from current assets and invest the fund in that portfolio that gives higher returns to the company.

whiles the competitors firm shows that they have higher liquidity for paying off its short term

liabilities. For the management of liquidity of company, the major recommendation to the

company is that they must focus on utilising the current asset in such a manner that all the

current liabilities of the company are being utilised in the proper and effective manner (Kahn and

Baum, 2020).

Account receivable Collection period of the company is 365 days which is too high for

the company. If payments from debtors does not collect on time, then they may increase the

chances of bad debts. So it is necessary for the company to reduced its credit sales and better to

11

calculated. From the above calculation it was shown that Linda profit margin ratio for the year

ended is 10.25% which shows that company is earning high profit and maximize its revenue.

while on the other side in comparison with competitors firm Linda's net profit shows lower.

Competitors NP ratio is 31% which is 20% higher from Linda's business (Kim and Im, 2017). So

company need to be mainly focused on increasing profit by declining its operating expenses and

expanding sales. In order to increase the net profit of the company it is required for the effective

and efficient reduction in the indirect expenses of the company. the major reason for this is that if

the indirect expense will be low then the net profit of the company will be increased.

As shown in above table companies GP ratio is low from its competitor. It is necessary

for the company to reduced expenses and implement strategies to maximize sales. The reason

behind the lower gross margin may be a higher cost of production or declining sales price, or if

there is any change in the sales mix. All these factors need in-depth analysis and watch

throughout the year to avoid a situation of lower gross margins. For increasing gross profit firm

need to identify those areas where company bears high expenses so only by controlling those

expenses firm increasing GP. Further in addition to this for increasing the profitability of the

company, it can go for the option of marketing so that the company can improve the sales. This

result in increase in the sales of the company and as a result of this the profitability of the

company will increase.

It was further evaluated that company’s current and quick asset ratio is very high this

shows firm has more investment in the current assets and block the funds on that assets. For

Improving this firm have to pay of its current obligations on time and can withdraw the amount

from current assets and invest the fund in that portfolio that gives higher returns to the company.

whiles the competitors firm shows that they have higher liquidity for paying off its short term

liabilities. For the management of liquidity of company, the major recommendation to the

company is that they must focus on utilising the current asset in such a manner that all the

current liabilities of the company are being utilised in the proper and effective manner (Kahn and

Baum, 2020).

Account receivable Collection period of the company is 365 days which is too high for

the company. If payments from debtors does not collect on time, then they may increase the

chances of bad debts. So it is necessary for the company to reduced its credit sales and better to

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expand its cash sales. Competitor firm's Collection period is only 50 days which is more

adequate as compared to Linda's business. this is particularly because of the reason that the

competitor will recover their money within the time frame of 50 days only. On the other side the

Linda will have to wait of around 365 days as the account receivable collection period is 365

days.

It is further reflected that firms account collection period is 365 days which means

company paid once in a year to its creditors. It declines companies position and goodwill in the

market. So company have to pay its current obligation on time only then firm can easily get

goods on credit. It is closely related to the account receivable turnover ratio. This is not a good

position for the company as the creditors will not allow this much of time for clearing the debts.

Hence, for this it is essential for Linda to manage the allocation of the funds in such a manner

that all the debt of the business are cleared in lesser time and the good image is being created

within the credit market.

From the above analysis it is clear that the firm’s financial performance is not good from

its competitors. for long run sustainability of Linda's business firstly firm have to Decline its cost

of production and make strategy for enlarging its sales (Basioudis, 2019). Only through this

company increased its profitability ratio. after that company will withdraw the amount from

current assets and invest that fund in any profitable portfolio. Further The firm have to pay off its

all creditors and increase creditors collection period.

CONCLUSION

From the above study it is interpreted that correct financial statement of a company is

very helpful in identifying the exact financial performance and position of the company. This

statements help in making policies and future decision makings. Further the study reflected that

financial position of Linda limited is not good as compared to its competitor firm. For company's

better position Linda's firm have to reduces its operating expenses and expand its revenue for

Better growth and maximize its profit. Firm also have to pay its current obligations on time and

withdraw the same amount from current assets and invest in the profitable outcomes. Further it is

also concluded from the report that the ratio analysis is very helpful in managing and comparing

the position of the company. this is necessary because of the reason that this will list out the

actual financial position and with comparison with the competitors the position can be improved.

12

adequate as compared to Linda's business. this is particularly because of the reason that the

competitor will recover their money within the time frame of 50 days only. On the other side the

Linda will have to wait of around 365 days as the account receivable collection period is 365

days.

It is further reflected that firms account collection period is 365 days which means

company paid once in a year to its creditors. It declines companies position and goodwill in the

market. So company have to pay its current obligation on time only then firm can easily get

goods on credit. It is closely related to the account receivable turnover ratio. This is not a good

position for the company as the creditors will not allow this much of time for clearing the debts.

Hence, for this it is essential for Linda to manage the allocation of the funds in such a manner

that all the debt of the business are cleared in lesser time and the good image is being created

within the credit market.

From the above analysis it is clear that the firm’s financial performance is not good from

its competitors. for long run sustainability of Linda's business firstly firm have to Decline its cost

of production and make strategy for enlarging its sales (Basioudis, 2019). Only through this

company increased its profitability ratio. after that company will withdraw the amount from

current assets and invest that fund in any profitable portfolio. Further The firm have to pay off its

all creditors and increase creditors collection period.

CONCLUSION

From the above study it is interpreted that correct financial statement of a company is

very helpful in identifying the exact financial performance and position of the company. This

statements help in making policies and future decision makings. Further the study reflected that

financial position of Linda limited is not good as compared to its competitor firm. For company's

better position Linda's firm have to reduces its operating expenses and expand its revenue for

Better growth and maximize its profit. Firm also have to pay its current obligations on time and

withdraw the same amount from current assets and invest in the profitable outcomes. Further it is

also concluded from the report that the ratio analysis is very helpful in managing and comparing

the position of the company. this is necessary because of the reason that this will list out the

actual financial position and with comparison with the competitors the position can be improved.

12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Basioudis, I. G., 2019. The Interpretation of Financial Statements. In Financial Accounting (pp.

274-308). Routledge.

Kahn, M. J. and Baum, N., 2020. Basic Accounting and Interpretation of Financial Statements.

In The Business Basics of Building and Managing a Healthcare Practice (pp. 13-18).

Springer, Cham.

Kim, J. and Im, C., 2017. Study on corporate social responsibility (CSR): Focus on tax

avoidance and financial ratio analysis. Sustainability. 9(10). p.1710.

Lee, B. H. and Lee, S. H., 2018. A study on financial ratio and prediction of financial distress in

financial markets. The Journal of Distribution Science. 16(11). pp.21-27.

13

Books and journals

Basioudis, I. G., 2019. The Interpretation of Financial Statements. In Financial Accounting (pp.

274-308). Routledge.

Kahn, M. J. and Baum, N., 2020. Basic Accounting and Interpretation of Financial Statements.

In The Business Basics of Building and Managing a Healthcare Practice (pp. 13-18).

Springer, Cham.

Kim, J. and Im, C., 2017. Study on corporate social responsibility (CSR): Focus on tax

avoidance and financial ratio analysis. Sustainability. 9(10). p.1710.

Lee, B. H. and Lee, S. H., 2018. A study on financial ratio and prediction of financial distress in

financial markets. The Journal of Distribution Science. 16(11). pp.21-27.

13

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.