Recording Business Transaction: Journal Entry, Ledger Account, Trial Balance, Income Statement, Balance Sheet

VerifiedAdded on 2022/12/15

|17

|2418

|56

AI Summary

This document provides a detailed explanation of recording business transactions through journal entry, ledger account, trial balance, income statement, and balance sheet. It emphasizes the importance of accurate financial statements and ratio analysis in analyzing business performance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording business

transaction

transaction

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Part A...............................................................................................................................................3

(a) Journal Entry..........................................................................................................................3

(b) Ledger Account......................................................................................................................4

(c) Trial Balance as at 31st October 2020....................................................................................9

(d) Income Statement.................................................................................................................10

(e) Balance Sheet as at 31st October 2020.................................................................................11

(f)................................................................................................................................................11

Part B.............................................................................................................................................12

(i) Ratio Analysis.......................................................................................................................12

(ii) Evaluation of the Linda's business performance on the basis of ratio analysis...................13

CONCLUSION..............................................................................................................................14

REFERENCE.................................................................................................................................15

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Part A...............................................................................................................................................3

(a) Journal Entry..........................................................................................................................3

(b) Ledger Account......................................................................................................................4

(c) Trial Balance as at 31st October 2020....................................................................................9

(d) Income Statement.................................................................................................................10

(e) Balance Sheet as at 31st October 2020.................................................................................11

(f)................................................................................................................................................11

Part B.............................................................................................................................................12

(i) Ratio Analysis.......................................................................................................................12

(ii) Evaluation of the Linda's business performance on the basis of ratio analysis...................13

CONCLUSION..............................................................................................................................14

REFERENCE.................................................................................................................................15

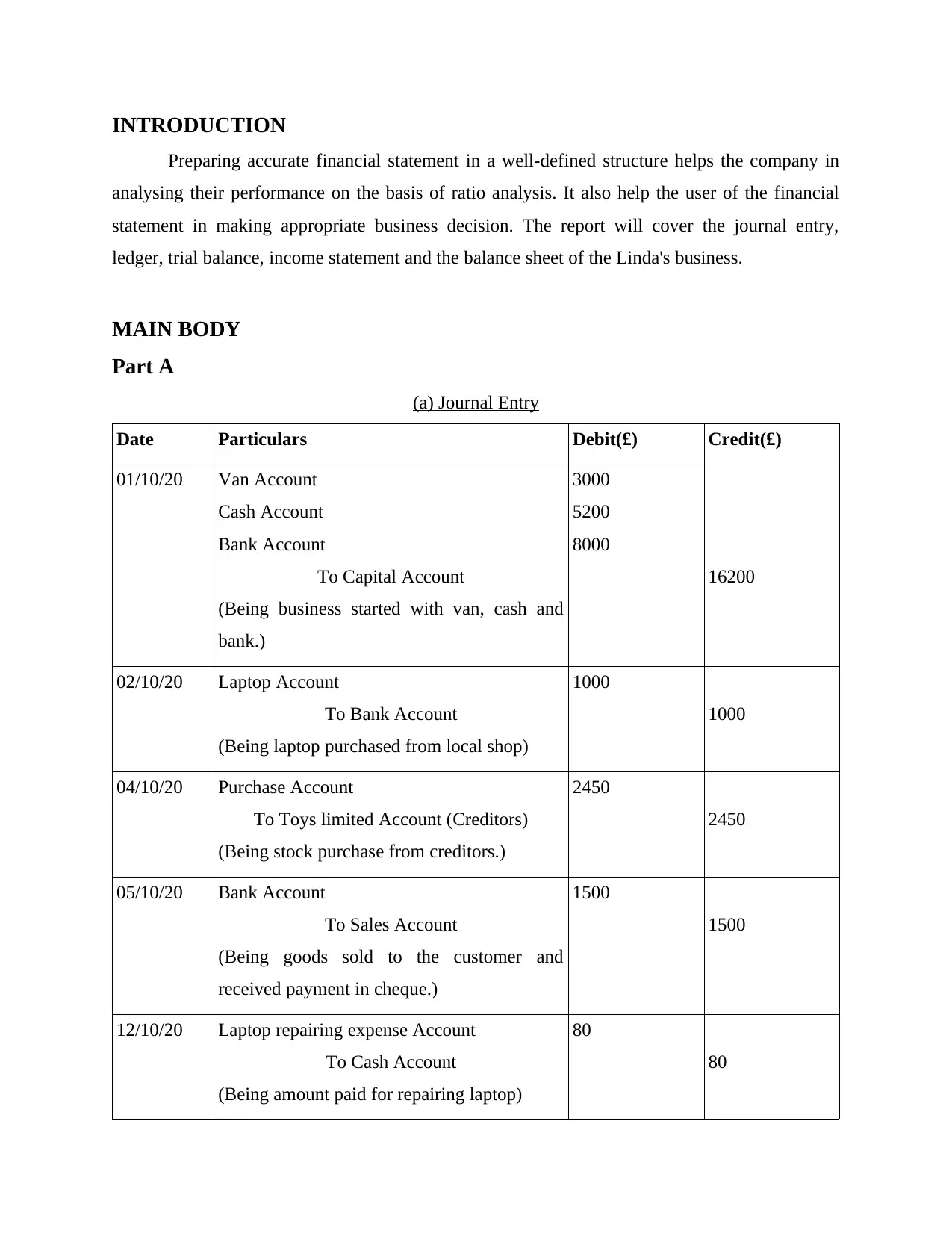

INTRODUCTION

Preparing accurate financial statement in a well-defined structure helps the company in

analysing their performance on the basis of ratio analysis. It also help the user of the financial

statement in making appropriate business decision. The report will cover the journal entry,

ledger, trial balance, income statement and the balance sheet of the Linda's business.

MAIN BODY

Part A

(a) Journal Entry

Date Particulars Debit(£) Credit(£)

01/10/20 Van Account

Cash Account

Bank Account

To Capital Account

(Being business started with van, cash and

bank.)

3000

5200

8000

16200

02/10/20 Laptop Account

To Bank Account

(Being laptop purchased from local shop)

1000

1000

04/10/20 Purchase Account

To Toys limited Account (Creditors)

(Being stock purchase from creditors.)

2450

2450

05/10/20 Bank Account

To Sales Account

(Being goods sold to the customer and

received payment in cheque.)

1500

1500

12/10/20 Laptop repairing expense Account

To Cash Account

(Being amount paid for repairing laptop)

80

80

Preparing accurate financial statement in a well-defined structure helps the company in

analysing their performance on the basis of ratio analysis. It also help the user of the financial

statement in making appropriate business decision. The report will cover the journal entry,

ledger, trial balance, income statement and the balance sheet of the Linda's business.

MAIN BODY

Part A

(a) Journal Entry

Date Particulars Debit(£) Credit(£)

01/10/20 Van Account

Cash Account

Bank Account

To Capital Account

(Being business started with van, cash and

bank.)

3000

5200

8000

16200

02/10/20 Laptop Account

To Bank Account

(Being laptop purchased from local shop)

1000

1000

04/10/20 Purchase Account

To Toys limited Account (Creditors)

(Being stock purchase from creditors.)

2450

2450

05/10/20 Bank Account

To Sales Account

(Being goods sold to the customer and

received payment in cheque.)

1500

1500

12/10/20 Laptop repairing expense Account

To Cash Account

(Being amount paid for repairing laptop)

80

80

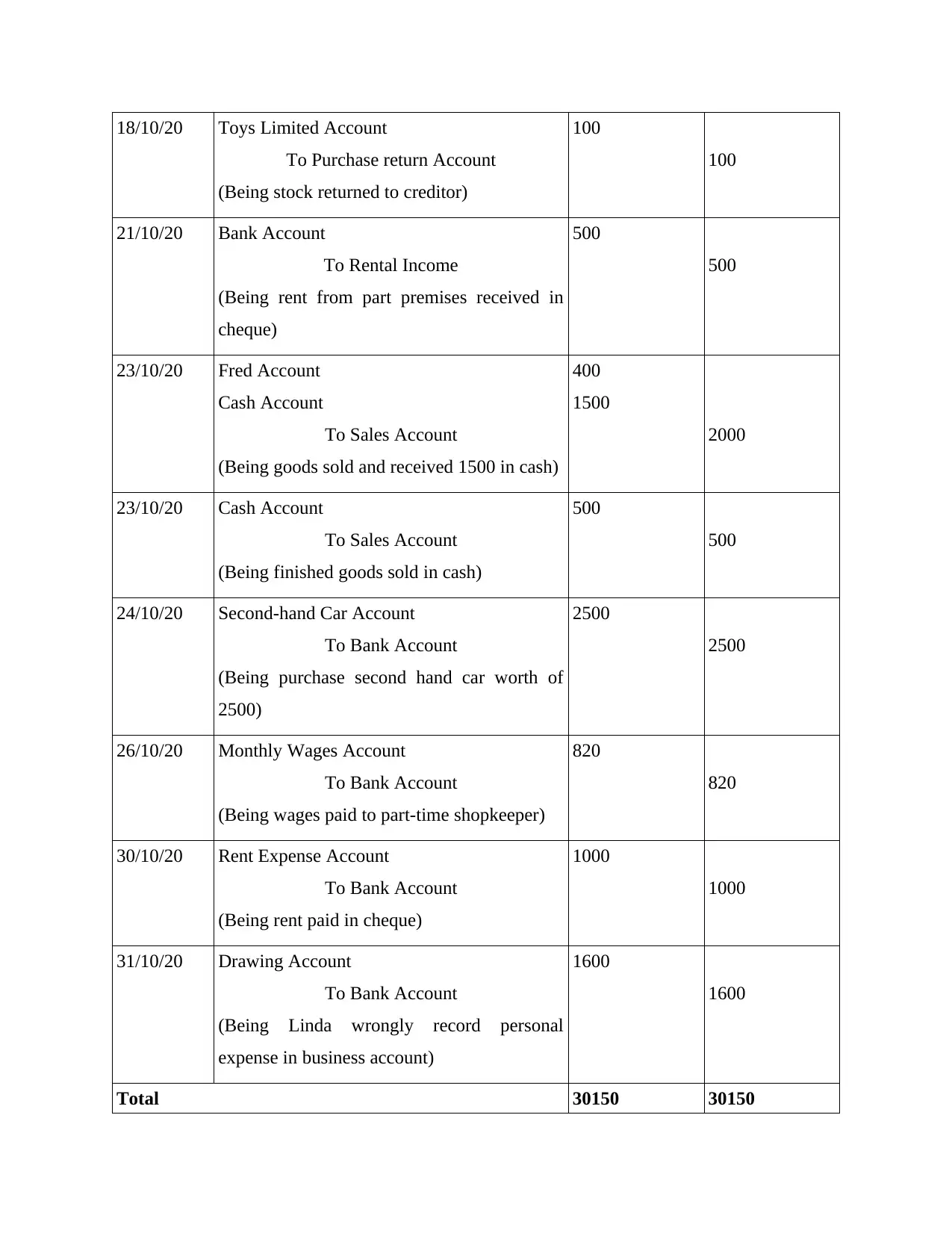

18/10/20 Toys Limited Account

To Purchase return Account

(Being stock returned to creditor)

100

100

21/10/20 Bank Account

To Rental Income

(Being rent from part premises received in

cheque)

500

500

23/10/20 Fred Account

Cash Account

To Sales Account

(Being goods sold and received 1500 in cash)

400

1500

2000

23/10/20 Cash Account

To Sales Account

(Being finished goods sold in cash)

500

500

24/10/20 Second-hand Car Account

To Bank Account

(Being purchase second hand car worth of

2500)

2500

2500

26/10/20 Monthly Wages Account

To Bank Account

(Being wages paid to part-time shopkeeper)

820

820

30/10/20 Rent Expense Account

To Bank Account

(Being rent paid in cheque)

1000

1000

31/10/20 Drawing Account

To Bank Account

(Being Linda wrongly record personal

expense in business account)

1600

1600

Total 30150 30150

To Purchase return Account

(Being stock returned to creditor)

100

100

21/10/20 Bank Account

To Rental Income

(Being rent from part premises received in

cheque)

500

500

23/10/20 Fred Account

Cash Account

To Sales Account

(Being goods sold and received 1500 in cash)

400

1500

2000

23/10/20 Cash Account

To Sales Account

(Being finished goods sold in cash)

500

500

24/10/20 Second-hand Car Account

To Bank Account

(Being purchase second hand car worth of

2500)

2500

2500

26/10/20 Monthly Wages Account

To Bank Account

(Being wages paid to part-time shopkeeper)

820

820

30/10/20 Rent Expense Account

To Bank Account

(Being rent paid in cheque)

1000

1000

31/10/20 Drawing Account

To Bank Account

(Being Linda wrongly record personal

expense in business account)

1600

1600

Total 30150 30150

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

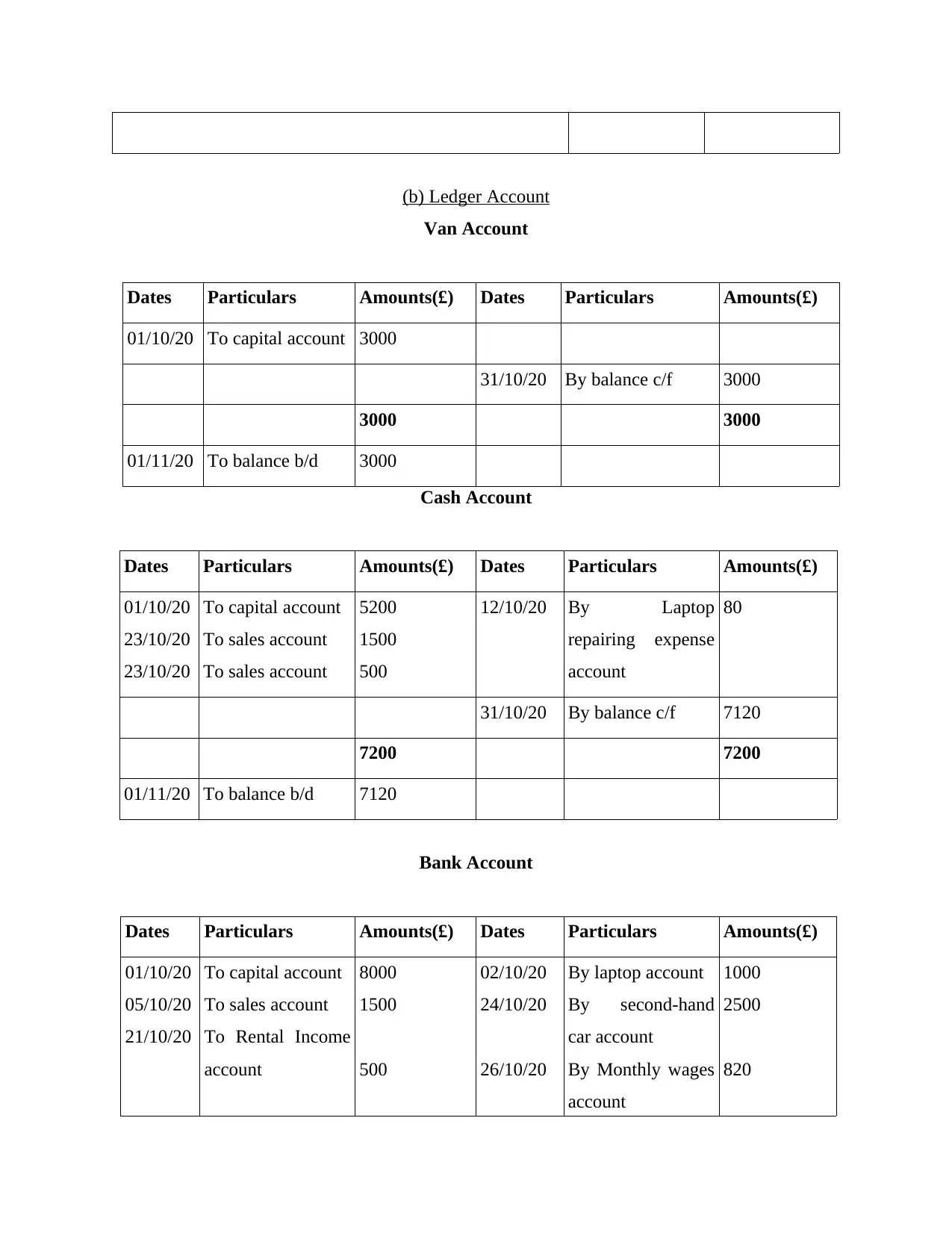

(b) Ledger Account

Van Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

01/10/20 To capital account 3000

31/10/20 By balance c/f 3000

3000 3000

01/11/20 To balance b/d 3000

Cash Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

01/10/20

23/10/20

23/10/20

To capital account

To sales account

To sales account

5200

1500

500

12/10/20 By Laptop

repairing expense

account

80

31/10/20 By balance c/f 7120

7200 7200

01/11/20 To balance b/d 7120

Bank Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

01/10/20

05/10/20

21/10/20

To capital account

To sales account

To Rental Income

account

8000

1500

500

02/10/20

24/10/20

26/10/20

By laptop account

By second-hand

car account

By Monthly wages

account

1000

2500

820

Van Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

01/10/20 To capital account 3000

31/10/20 By balance c/f 3000

3000 3000

01/11/20 To balance b/d 3000

Cash Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

01/10/20

23/10/20

23/10/20

To capital account

To sales account

To sales account

5200

1500

500

12/10/20 By Laptop

repairing expense

account

80

31/10/20 By balance c/f 7120

7200 7200

01/11/20 To balance b/d 7120

Bank Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

01/10/20

05/10/20

21/10/20

To capital account

To sales account

To Rental Income

account

8000

1500

500

02/10/20

24/10/20

26/10/20

By laptop account

By second-hand

car account

By Monthly wages

account

1000

2500

820

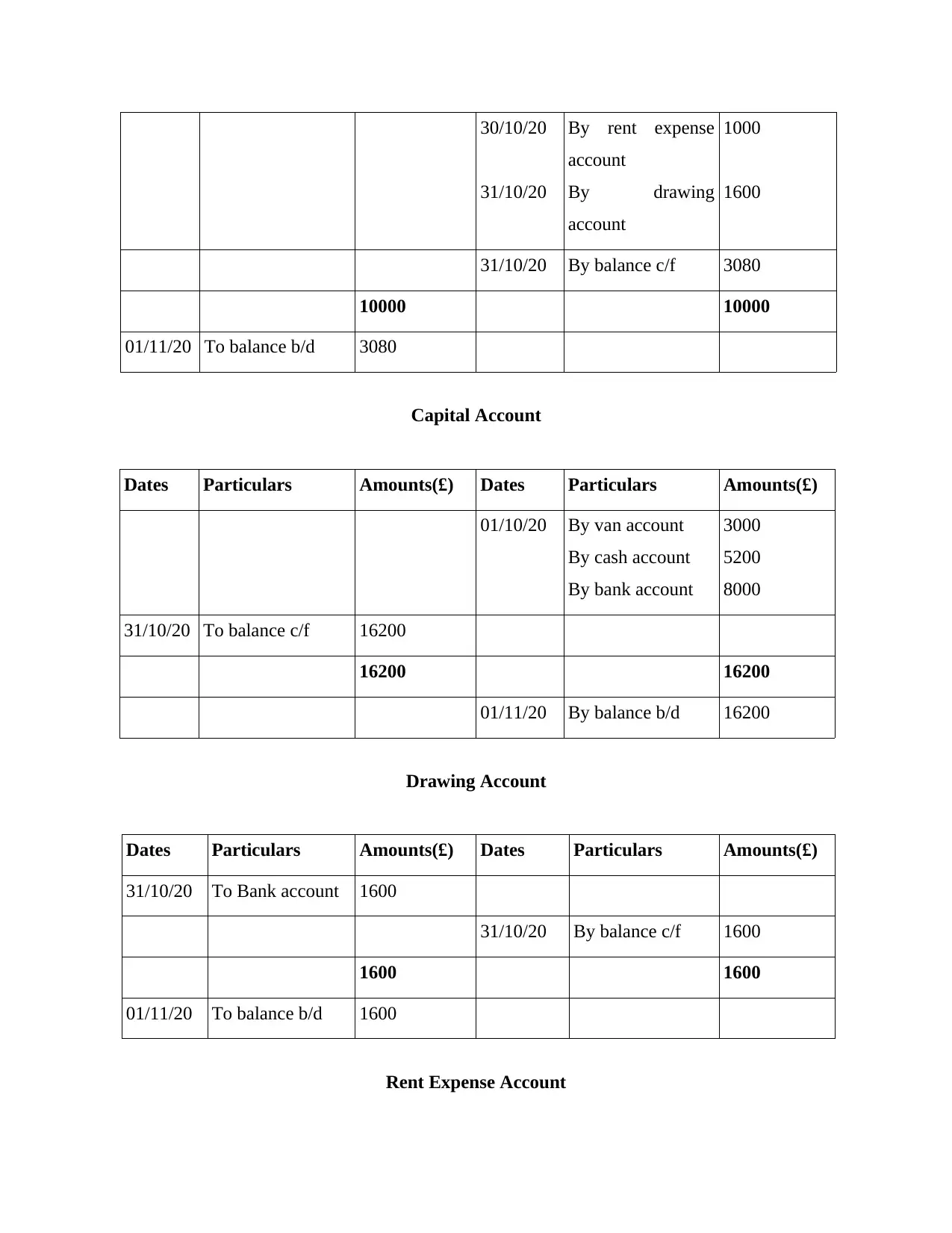

30/10/20

31/10/20

By rent expense

account

By drawing

account

1000

1600

31/10/20 By balance c/f 3080

10000 10000

01/11/20 To balance b/d 3080

Capital Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

01/10/20 By van account

By cash account

By bank account

3000

5200

8000

31/10/20 To balance c/f 16200

16200 16200

01/11/20 By balance b/d 16200

Drawing Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

31/10/20 To Bank account 1600

31/10/20 By balance c/f 1600

1600 1600

01/11/20 To balance b/d 1600

Rent Expense Account

31/10/20

By rent expense

account

By drawing

account

1000

1600

31/10/20 By balance c/f 3080

10000 10000

01/11/20 To balance b/d 3080

Capital Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

01/10/20 By van account

By cash account

By bank account

3000

5200

8000

31/10/20 To balance c/f 16200

16200 16200

01/11/20 By balance b/d 16200

Drawing Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

31/10/20 To Bank account 1600

31/10/20 By balance c/f 1600

1600 1600

01/11/20 To balance b/d 1600

Rent Expense Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

30/10/20 To Bank account 1000

31/10/20 By balance c/f 1000

1000 1000

01/11/20 To balance b/d 1000

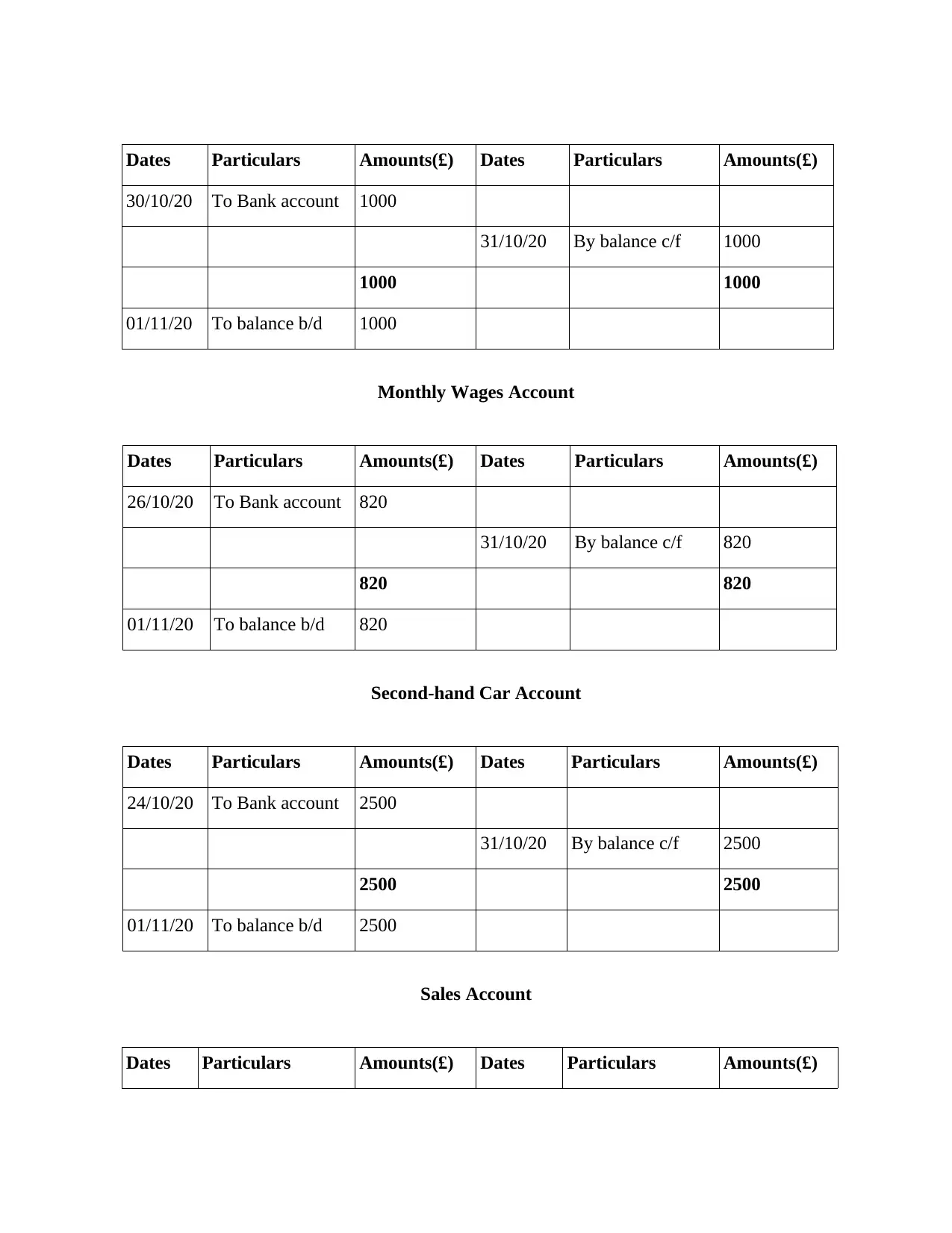

Monthly Wages Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

26/10/20 To Bank account 820

31/10/20 By balance c/f 820

820 820

01/11/20 To balance b/d 820

Second-hand Car Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

24/10/20 To Bank account 2500

31/10/20 By balance c/f 2500

2500 2500

01/11/20 To balance b/d 2500

Sales Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

30/10/20 To Bank account 1000

31/10/20 By balance c/f 1000

1000 1000

01/11/20 To balance b/d 1000

Monthly Wages Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

26/10/20 To Bank account 820

31/10/20 By balance c/f 820

820 820

01/11/20 To balance b/d 820

Second-hand Car Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

24/10/20 To Bank account 2500

31/10/20 By balance c/f 2500

2500 2500

01/11/20 To balance b/d 2500

Sales Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

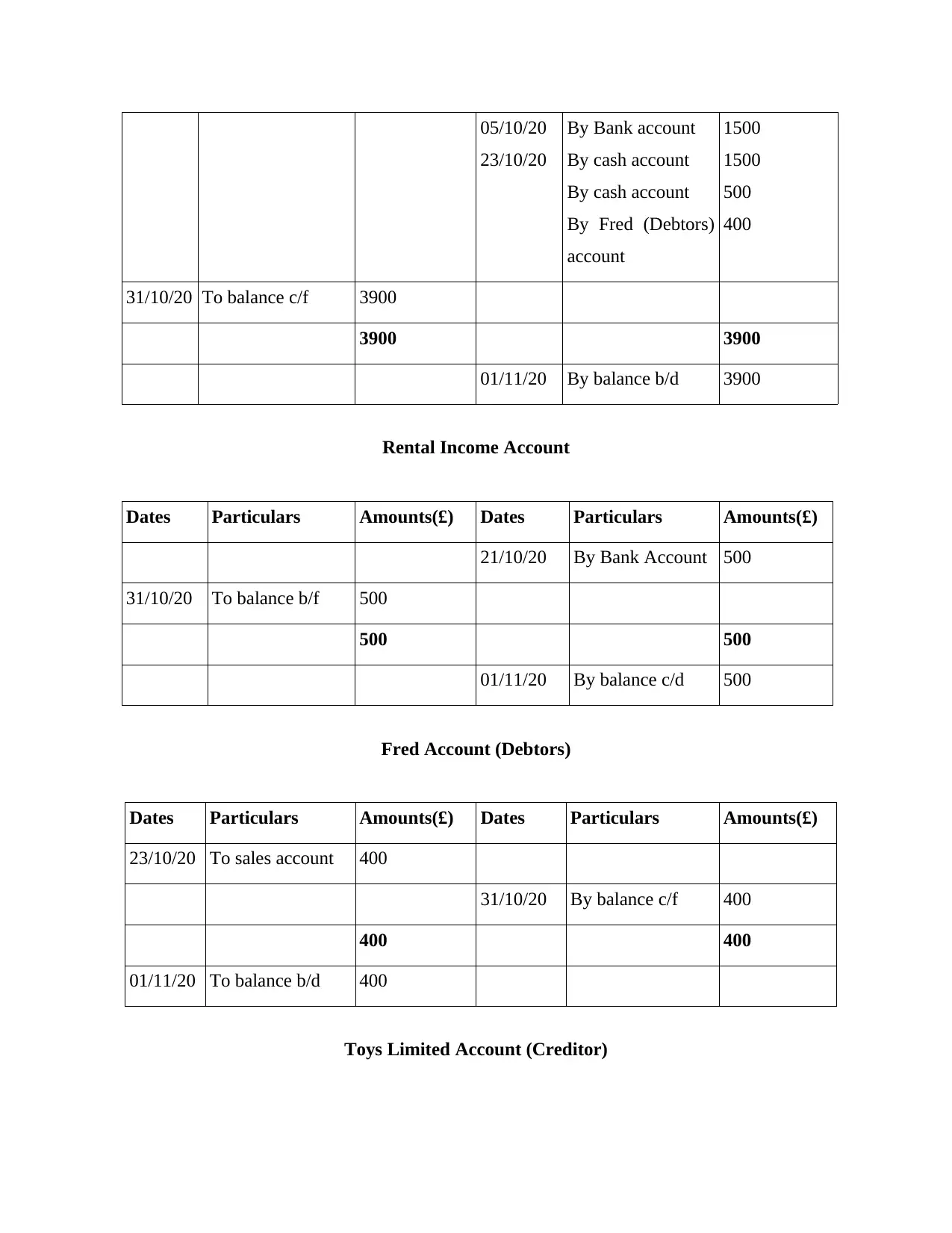

05/10/20

23/10/20

By Bank account

By cash account

By cash account

By Fred (Debtors)

account

1500

1500

500

400

31/10/20 To balance c/f 3900

3900 3900

01/11/20 By balance b/d 3900

Rental Income Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

21/10/20 By Bank Account 500

31/10/20 To balance b/f 500

500 500

01/11/20 By balance c/d 500

Fred Account (Debtors)

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

23/10/20 To sales account 400

31/10/20 By balance c/f 400

400 400

01/11/20 To balance b/d 400

Toys Limited Account (Creditor)

23/10/20

By Bank account

By cash account

By cash account

By Fred (Debtors)

account

1500

1500

500

400

31/10/20 To balance c/f 3900

3900 3900

01/11/20 By balance b/d 3900

Rental Income Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

21/10/20 By Bank Account 500

31/10/20 To balance b/f 500

500 500

01/11/20 By balance c/d 500

Fred Account (Debtors)

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

23/10/20 To sales account 400

31/10/20 By balance c/f 400

400 400

01/11/20 To balance b/d 400

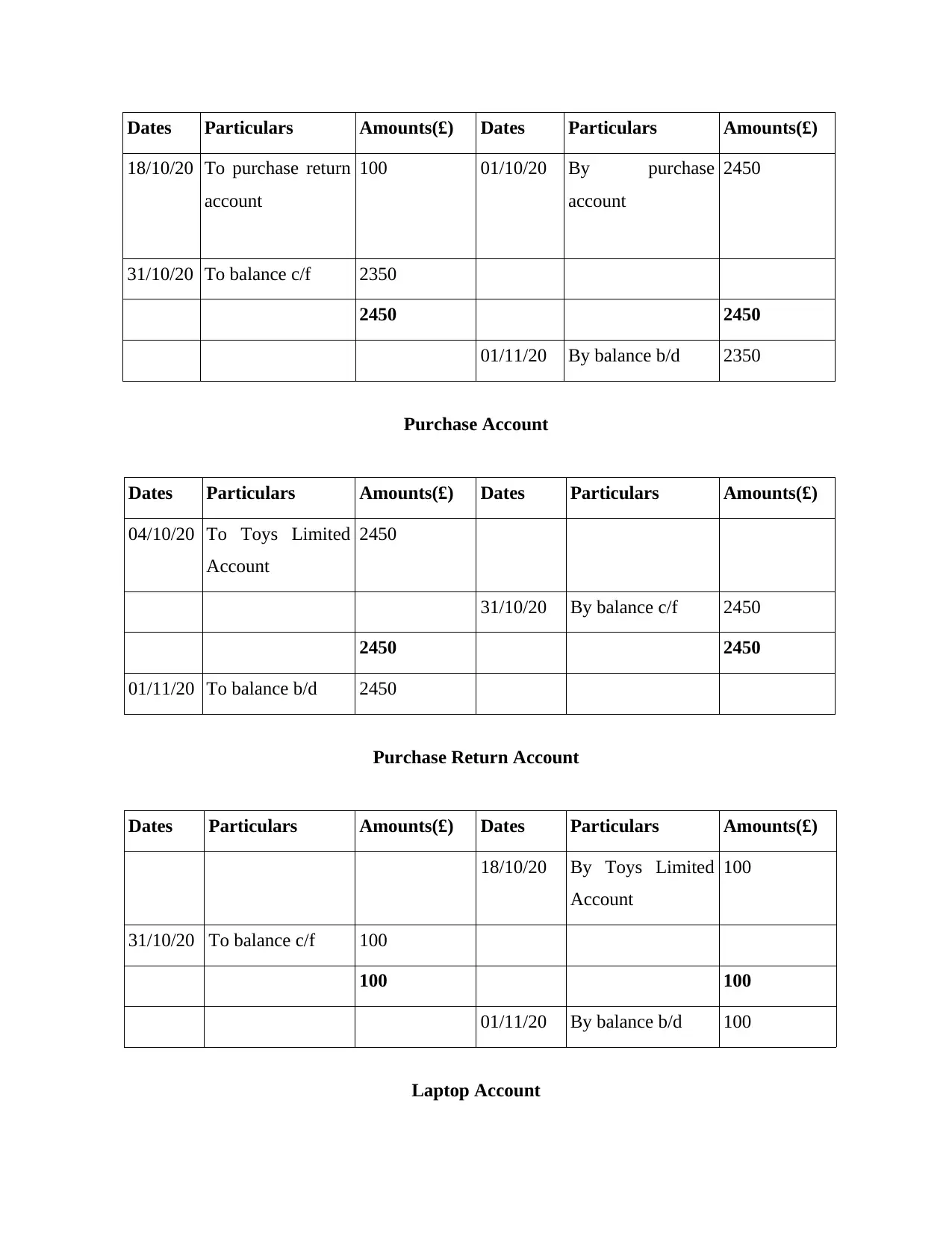

Toys Limited Account (Creditor)

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

18/10/20 To purchase return

account

100 01/10/20 By purchase

account

2450

31/10/20 To balance c/f 2350

2450 2450

01/11/20 By balance b/d 2350

Purchase Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

04/10/20 To Toys Limited

Account

2450

31/10/20 By balance c/f 2450

2450 2450

01/11/20 To balance b/d 2450

Purchase Return Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

18/10/20 By Toys Limited

Account

100

31/10/20 To balance c/f 100

100 100

01/11/20 By balance b/d 100

Laptop Account

18/10/20 To purchase return

account

100 01/10/20 By purchase

account

2450

31/10/20 To balance c/f 2350

2450 2450

01/11/20 By balance b/d 2350

Purchase Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

04/10/20 To Toys Limited

Account

2450

31/10/20 By balance c/f 2450

2450 2450

01/11/20 To balance b/d 2450

Purchase Return Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

18/10/20 By Toys Limited

Account

100

31/10/20 To balance c/f 100

100 100

01/11/20 By balance b/d 100

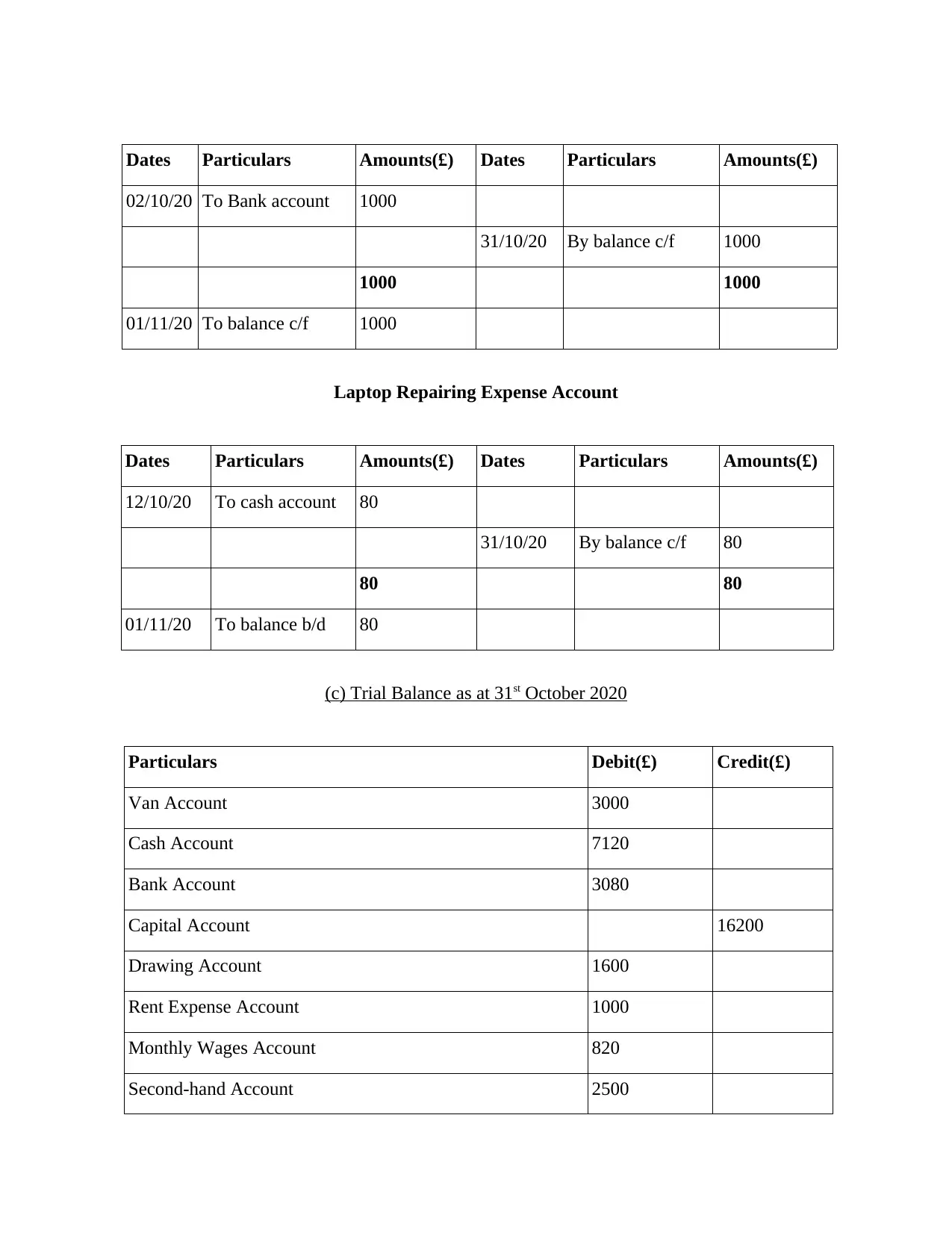

Laptop Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

02/10/20 To Bank account 1000

31/10/20 By balance c/f 1000

1000 1000

01/11/20 To balance c/f 1000

Laptop Repairing Expense Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

12/10/20 To cash account 80

31/10/20 By balance c/f 80

80 80

01/11/20 To balance b/d 80

(c) Trial Balance as at 31st October 2020

Particulars Debit(£) Credit(£)

Van Account 3000

Cash Account 7120

Bank Account 3080

Capital Account 16200

Drawing Account 1600

Rent Expense Account 1000

Monthly Wages Account 820

Second-hand Account 2500

02/10/20 To Bank account 1000

31/10/20 By balance c/f 1000

1000 1000

01/11/20 To balance c/f 1000

Laptop Repairing Expense Account

Dates Particulars Amounts(£) Dates Particulars Amounts(£)

12/10/20 To cash account 80

31/10/20 By balance c/f 80

80 80

01/11/20 To balance b/d 80

(c) Trial Balance as at 31st October 2020

Particulars Debit(£) Credit(£)

Van Account 3000

Cash Account 7120

Bank Account 3080

Capital Account 16200

Drawing Account 1600

Rent Expense Account 1000

Monthly Wages Account 820

Second-hand Account 2500

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Sales Account 3900

Rental Income Account 500

Fred (Debtor) Account 400

Toys Limited (Creditor) Account 2350

Purchase Account 2450

Purchase Return Account 100

Laptop Account 1000

Laptop Repairing Expense Account 80

Total 23050 23050

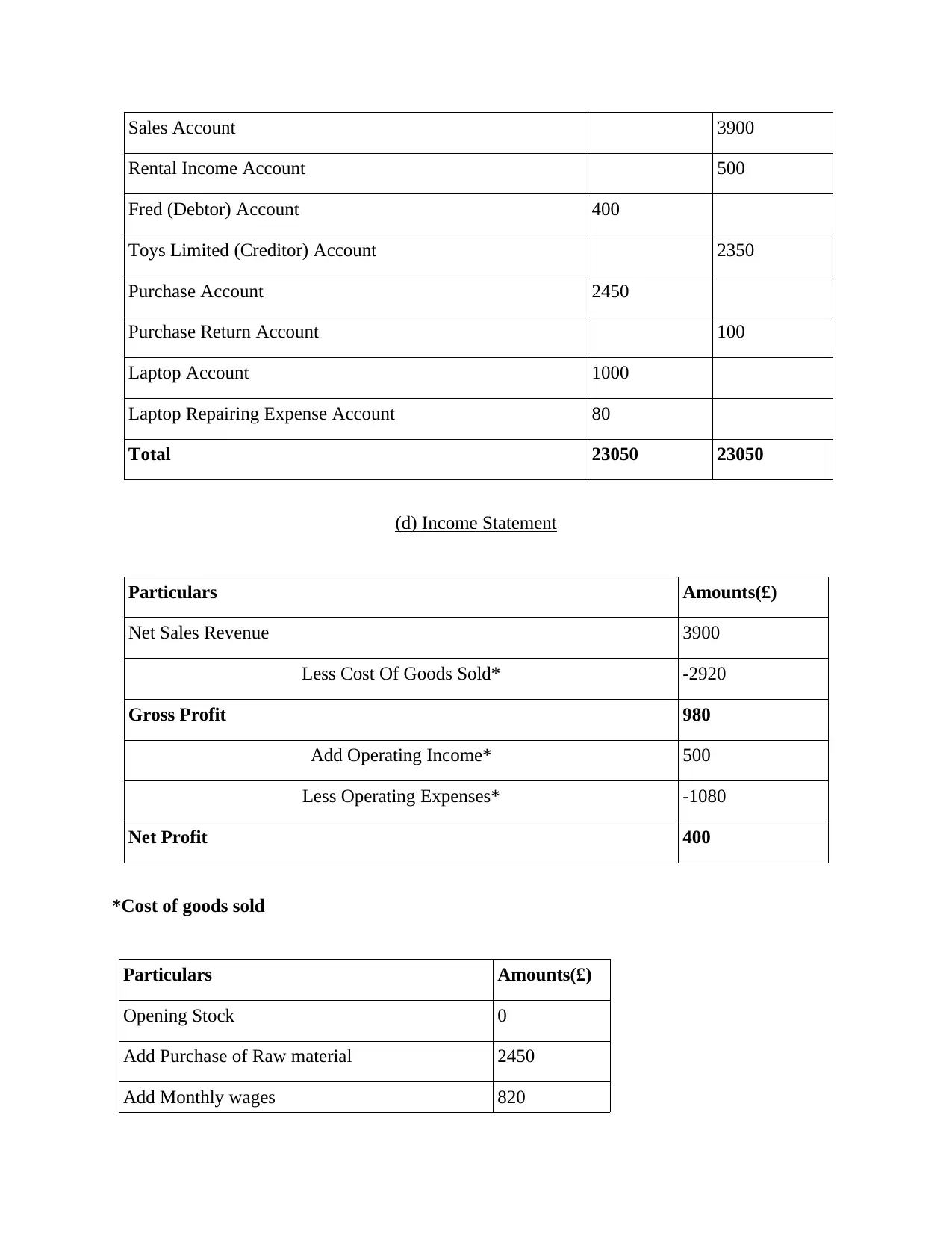

(d) Income Statement

Particulars Amounts(£)

Net Sales Revenue 3900

Less Cost Of Goods Sold* -2920

Gross Profit 980

Add Operating Income* 500

Less Operating Expenses* -1080

Net Profit 400

*Cost of goods sold

Particulars Amounts(£)

Opening Stock 0

Add Purchase of Raw material 2450

Add Monthly wages 820

Rental Income Account 500

Fred (Debtor) Account 400

Toys Limited (Creditor) Account 2350

Purchase Account 2450

Purchase Return Account 100

Laptop Account 1000

Laptop Repairing Expense Account 80

Total 23050 23050

(d) Income Statement

Particulars Amounts(£)

Net Sales Revenue 3900

Less Cost Of Goods Sold* -2920

Gross Profit 980

Add Operating Income* 500

Less Operating Expenses* -1080

Net Profit 400

*Cost of goods sold

Particulars Amounts(£)

Opening Stock 0

Add Purchase of Raw material 2450

Add Monthly wages 820

Less Purchase return -100

Less Closing stock -250

COGS 2920

*Operation income

Particulars Amounts(£)

Rental Income 500

Total 500

*Operating Expenses

Particulars Amounts(£)

Repairing expense 80

Rent Expense 1000

Total Net operating expenses 1080

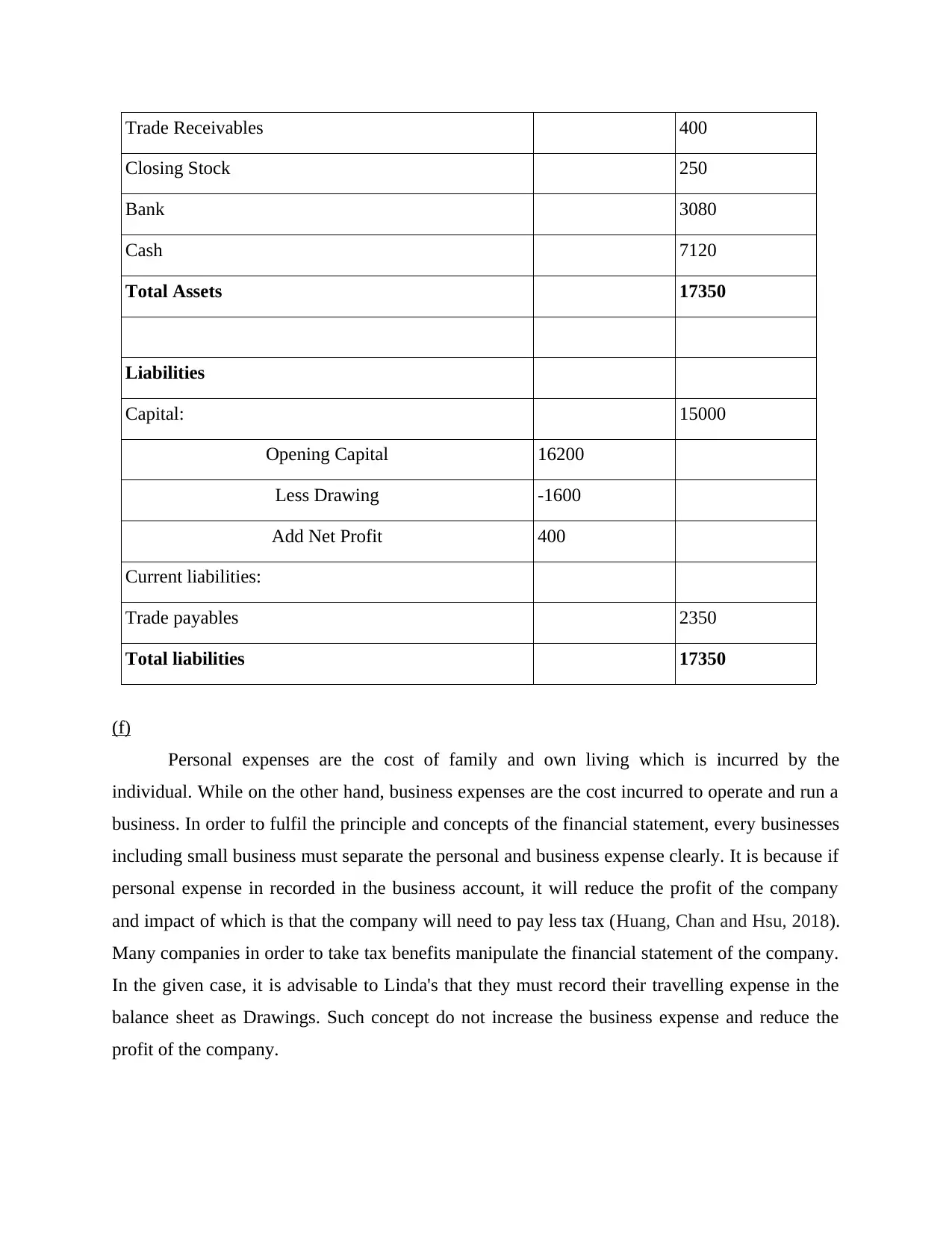

(e) Balance Sheet as at 31st October 2020

Particulars Details Amount

ASSETS

Non-current assets:

Fixed and Tangible assets: 6500

Laptop 1000

Van 3000

Second-hand Car 2500

Current assets:

Less Closing stock -250

COGS 2920

*Operation income

Particulars Amounts(£)

Rental Income 500

Total 500

*Operating Expenses

Particulars Amounts(£)

Repairing expense 80

Rent Expense 1000

Total Net operating expenses 1080

(e) Balance Sheet as at 31st October 2020

Particulars Details Amount

ASSETS

Non-current assets:

Fixed and Tangible assets: 6500

Laptop 1000

Van 3000

Second-hand Car 2500

Current assets:

Trade Receivables 400

Closing Stock 250

Bank 3080

Cash 7120

Total Assets 17350

Liabilities

Capital: 15000

Opening Capital 16200

Less Drawing -1600

Add Net Profit 400

Current liabilities:

Trade payables 2350

Total liabilities 17350

(f)

Personal expenses are the cost of family and own living which is incurred by the

individual. While on the other hand, business expenses are the cost incurred to operate and run a

business. In order to fulfil the principle and concepts of the financial statement, every businesses

including small business must separate the personal and business expense clearly. It is because if

personal expense in recorded in the business account, it will reduce the profit of the company

and impact of which is that the company will need to pay less tax (Huang, Chan and Hsu, 2018).

Many companies in order to take tax benefits manipulate the financial statement of the company.

In the given case, it is advisable to Linda's that they must record their travelling expense in the

balance sheet as Drawings. Such concept do not increase the business expense and reduce the

profit of the company.

Closing Stock 250

Bank 3080

Cash 7120

Total Assets 17350

Liabilities

Capital: 15000

Opening Capital 16200

Less Drawing -1600

Add Net Profit 400

Current liabilities:

Trade payables 2350

Total liabilities 17350

(f)

Personal expenses are the cost of family and own living which is incurred by the

individual. While on the other hand, business expenses are the cost incurred to operate and run a

business. In order to fulfil the principle and concepts of the financial statement, every businesses

including small business must separate the personal and business expense clearly. It is because if

personal expense in recorded in the business account, it will reduce the profit of the company

and impact of which is that the company will need to pay less tax (Huang, Chan and Hsu, 2018).

Many companies in order to take tax benefits manipulate the financial statement of the company.

In the given case, it is advisable to Linda's that they must record their travelling expense in the

balance sheet as Drawings. Such concept do not increase the business expense and reduce the

profit of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part B

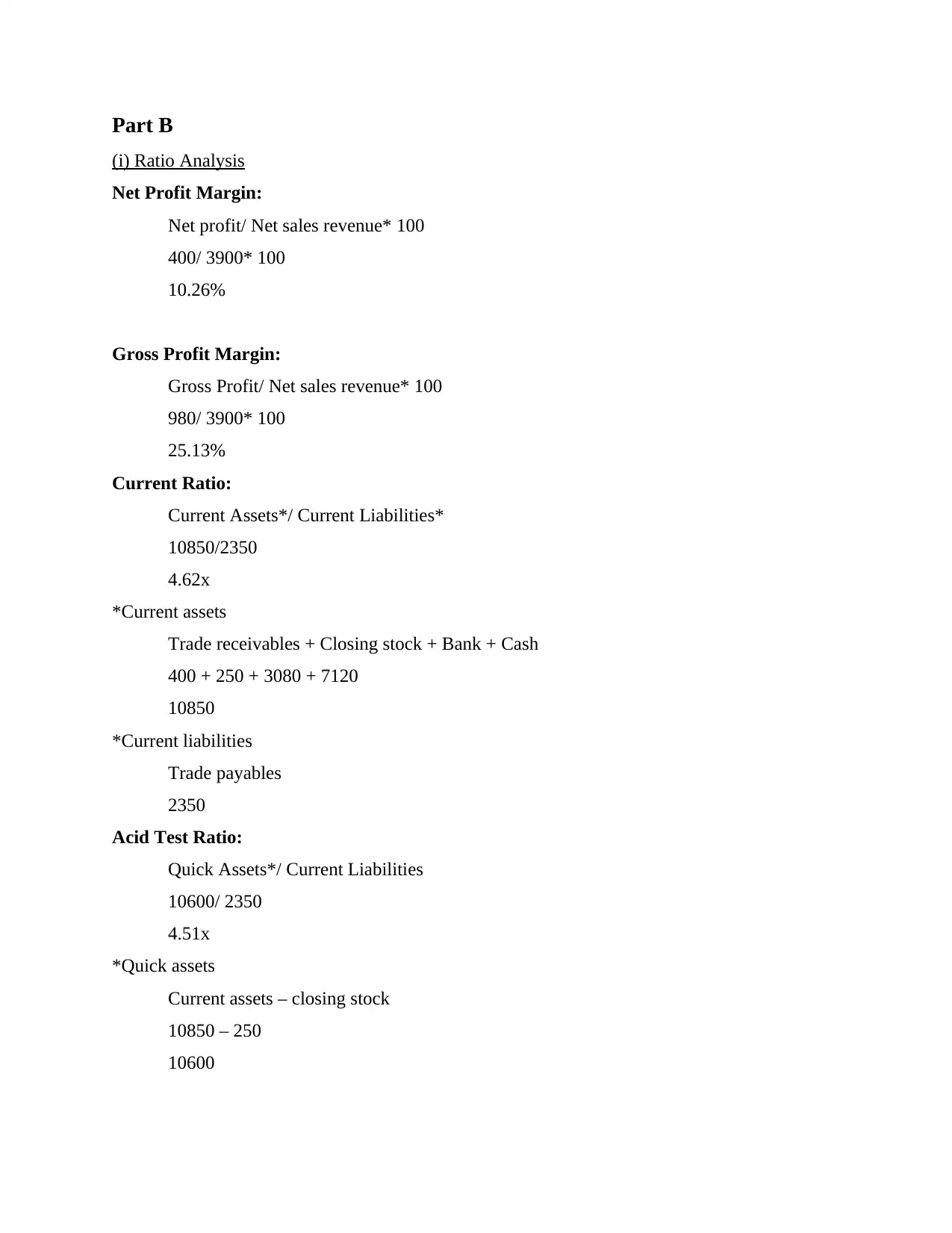

(i) Ratio Analysis

Net Profit Margin:

Net profit/ Net sales revenue* 100

400/ 3900* 100

10.26%

Gross Profit Margin:

Gross Profit/ Net sales revenue* 100

980/ 3900* 100

25.13%

Current Ratio:

Current Assets*/ Current Liabilities*

10850/2350

4.62x

*Current assets

Trade receivables + Closing stock + Bank + Cash

400 + 250 + 3080 + 7120

10850

*Current liabilities

Trade payables

2350

Acid Test Ratio:

Quick Assets*/ Current Liabilities

10600/ 2350

4.51x

*Quick assets

Current assets – closing stock

10850 – 250

10600

(i) Ratio Analysis

Net Profit Margin:

Net profit/ Net sales revenue* 100

400/ 3900* 100

10.26%

Gross Profit Margin:

Gross Profit/ Net sales revenue* 100

980/ 3900* 100

25.13%

Current Ratio:

Current Assets*/ Current Liabilities*

10850/2350

4.62x

*Current assets

Trade receivables + Closing stock + Bank + Cash

400 + 250 + 3080 + 7120

10850

*Current liabilities

Trade payables

2350

Acid Test Ratio:

Quick Assets*/ Current Liabilities

10600/ 2350

4.51x

*Quick assets

Current assets – closing stock

10850 – 250

10600

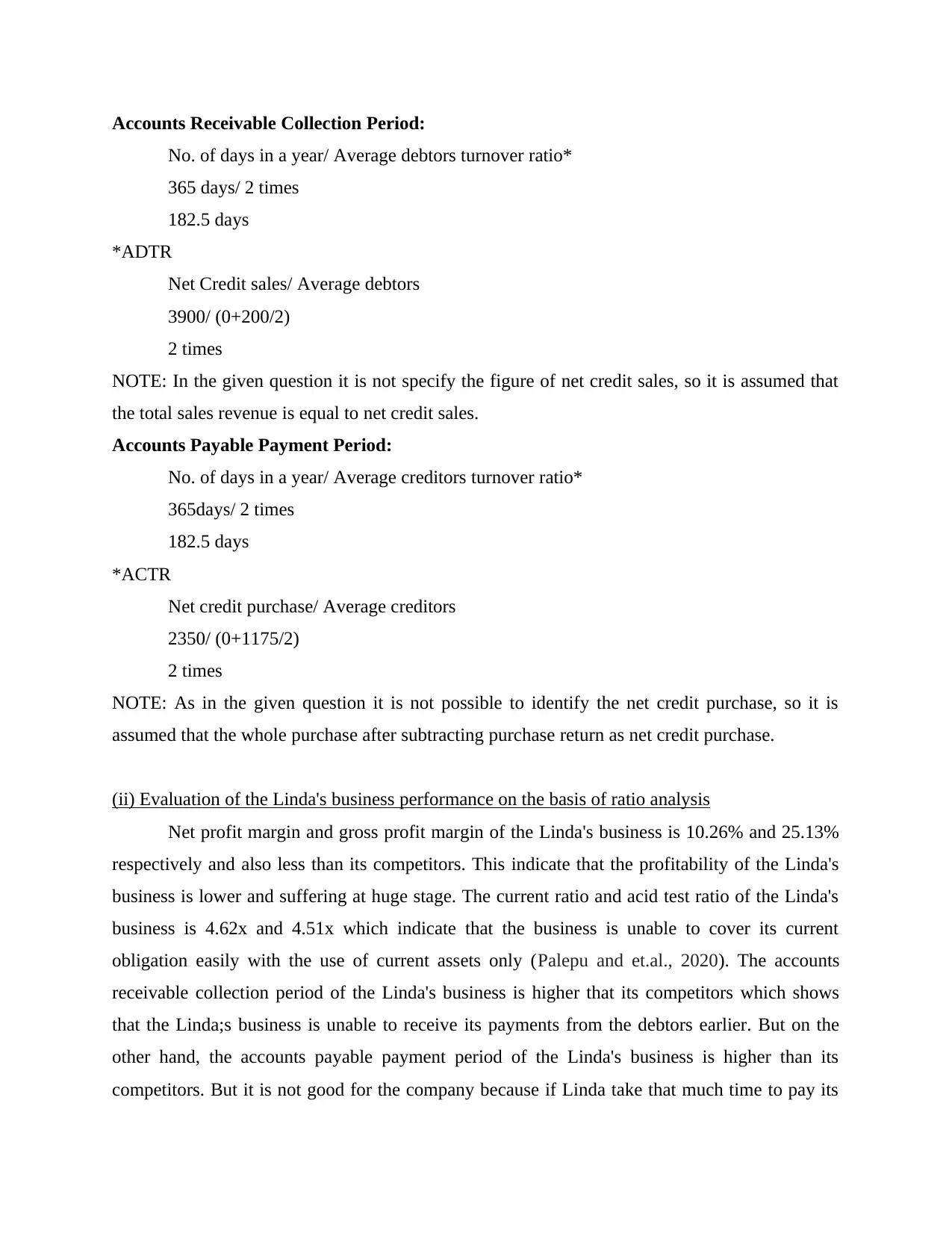

Accounts Receivable Collection Period:

No. of days in a year/ Average debtors turnover ratio*

365 days/ 2 times

182.5 days

*ADTR

Net Credit sales/ Average debtors

3900/ (0+200/2)

2 times

NOTE: In the given question it is not specify the figure of net credit sales, so it is assumed that

the total sales revenue is equal to net credit sales.

Accounts Payable Payment Period:

No. of days in a year/ Average creditors turnover ratio*

365days/ 2 times

182.5 days

*ACTR

Net credit purchase/ Average creditors

2350/ (0+1175/2)

2 times

NOTE: As in the given question it is not possible to identify the net credit purchase, so it is

assumed that the whole purchase after subtracting purchase return as net credit purchase.

(ii) Evaluation of the Linda's business performance on the basis of ratio analysis

Net profit margin and gross profit margin of the Linda's business is 10.26% and 25.13%

respectively and also less than its competitors. This indicate that the profitability of the Linda's

business is lower and suffering at huge stage. The current ratio and acid test ratio of the Linda's

business is 4.62x and 4.51x which indicate that the business is unable to cover its current

obligation easily with the use of current assets only (Palepu and et.al., 2020). The accounts

receivable collection period of the Linda's business is higher that its competitors which shows

that the Linda;s business is unable to receive its payments from the debtors earlier. But on the

other hand, the accounts payable payment period of the Linda's business is higher than its

competitors. But it is not good for the company because if Linda take that much time to pay its

No. of days in a year/ Average debtors turnover ratio*

365 days/ 2 times

182.5 days

*ADTR

Net Credit sales/ Average debtors

3900/ (0+200/2)

2 times

NOTE: In the given question it is not specify the figure of net credit sales, so it is assumed that

the total sales revenue is equal to net credit sales.

Accounts Payable Payment Period:

No. of days in a year/ Average creditors turnover ratio*

365days/ 2 times

182.5 days

*ACTR

Net credit purchase/ Average creditors

2350/ (0+1175/2)

2 times

NOTE: As in the given question it is not possible to identify the net credit purchase, so it is

assumed that the whole purchase after subtracting purchase return as net credit purchase.

(ii) Evaluation of the Linda's business performance on the basis of ratio analysis

Net profit margin and gross profit margin of the Linda's business is 10.26% and 25.13%

respectively and also less than its competitors. This indicate that the profitability of the Linda's

business is lower and suffering at huge stage. The current ratio and acid test ratio of the Linda's

business is 4.62x and 4.51x which indicate that the business is unable to cover its current

obligation easily with the use of current assets only (Palepu and et.al., 2020). The accounts

receivable collection period of the Linda's business is higher that its competitors which shows

that the Linda;s business is unable to receive its payments from the debtors earlier. But on the

other hand, the accounts payable payment period of the Linda's business is higher than its

competitors. But it is not good for the company because if Linda take that much time to pay its

creditors than they will lose their suppliers trust. The whole analysis interpret that the efficiency,

profitability and the liquidity position and performance of the Linda's business is poor than its

competitors.

In order to improve the business performance, first of all Linda need to prepare its

financial statement by following the financial reporting framework along with concepts and

conventions of the FS. After that they need to make sure that they make payment to their supplier

as early as possible in order to gain their trust and purchase the raw material in large quantity on

credit basis (Robinson, 2020). In order to receive payment quickly from the company's debtors, it

is advisable to the Linda that they should make strict rule and charge penalty and interest for late

payment. To improve the liquidity of the company, they need to use the long-term financing

options and also need to manage their receivable and payables optimally. The company need to

manage their variable cost as well as fixed cost. By concentrating more on the existing customers

and by offering them discounts on the product, Lind's business can make then feel better and

happy. The result of this is that the performance of the Linda's business will automatically

improve.

CONCLUSION

The report concludes that the performance of the Linda's business is poor as compared to

their competitors. The report also concludes the concept of drawings concerning small business

along with ways which help the Linda in improving their profitability and liquidity of the

company.

profitability and the liquidity position and performance of the Linda's business is poor than its

competitors.

In order to improve the business performance, first of all Linda need to prepare its

financial statement by following the financial reporting framework along with concepts and

conventions of the FS. After that they need to make sure that they make payment to their supplier

as early as possible in order to gain their trust and purchase the raw material in large quantity on

credit basis (Robinson, 2020). In order to receive payment quickly from the company's debtors, it

is advisable to the Linda that they should make strict rule and charge penalty and interest for late

payment. To improve the liquidity of the company, they need to use the long-term financing

options and also need to manage their receivable and payables optimally. The company need to

manage their variable cost as well as fixed cost. By concentrating more on the existing customers

and by offering them discounts on the product, Lind's business can make then feel better and

happy. The result of this is that the performance of the Linda's business will automatically

improve.

CONCLUSION

The report concludes that the performance of the Linda's business is poor as compared to

their competitors. The report also concludes the concept of drawings concerning small business

along with ways which help the Linda in improving their profitability and liquidity of the

company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCE

Books & Journals

Famiola, M. and Hartati, S., 2018. Entrepreneurship learning system in business incubators: A

case study in Indonesia. International Journal of Engineering & Technology, 7(4.28),

pp.57-62.

Huang, Y. C., Chan, J. Y. H. and Hsu, J., 2018, April. Reflection before/after practice:

learnersourcing for drawing support. In Extended Abstracts of the 2018 CHI

Conference on Human Factors in Computing Systems (pp. 1-6).

Palepu, K. G. and et.al., 2020. Business analysis and valuation: Using financial statements.

Cengage AU.

Shehab, S. F., 2019. Evaluating financial performance in Islamic banks Applied Study on the

Islamic Elaf Bank in Iraq. Tikrit Journal of Administration and Economics

Sciences, 15(45 Part 1).

Ardila, I., Zurriah, R. and Suryani, Y., 2019. Preparation of financial statements based on

financial accounting standards for micro, small and medium entities. International

Journal of Accounting & Finance in Asia Pasific (IJAFAP), 2(3), pp.1-6.

Robinson, T. R., 2020. International financial statement analysis. John Wiley & Sons.

Lubawa, G. and Van Auken, H. E., 2018. Preparation and Use of Financial Statements

byFamily owned-SMEs in Tanzania: A case Study of Sunflowers Oil Processors in

Dodoma Region. Effect Of Social And Human Capital On Access To Financial

Capital For Smes: A Comparative, p.18.

Books & Journals

Famiola, M. and Hartati, S., 2018. Entrepreneurship learning system in business incubators: A

case study in Indonesia. International Journal of Engineering & Technology, 7(4.28),

pp.57-62.

Huang, Y. C., Chan, J. Y. H. and Hsu, J., 2018, April. Reflection before/after practice:

learnersourcing for drawing support. In Extended Abstracts of the 2018 CHI

Conference on Human Factors in Computing Systems (pp. 1-6).

Palepu, K. G. and et.al., 2020. Business analysis and valuation: Using financial statements.

Cengage AU.

Shehab, S. F., 2019. Evaluating financial performance in Islamic banks Applied Study on the

Islamic Elaf Bank in Iraq. Tikrit Journal of Administration and Economics

Sciences, 15(45 Part 1).

Ardila, I., Zurriah, R. and Suryani, Y., 2019. Preparation of financial statements based on

financial accounting standards for micro, small and medium entities. International

Journal of Accounting & Finance in Asia Pasific (IJAFAP), 2(3), pp.1-6.

Robinson, T. R., 2020. International financial statement analysis. John Wiley & Sons.

Lubawa, G. and Van Auken, H. E., 2018. Preparation and Use of Financial Statements

byFamily owned-SMEs in Tanzania: A case Study of Sunflowers Oil Processors in

Dodoma Region. Effect Of Social And Human Capital On Access To Financial

Capital For Smes: A Comparative, p.18.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.