Recording Business Transaction

VerifiedAdded on 2022/12/29

|15

|2324

|56

AI Summary

This report discusses the process of recording business transactions in the double entry system, ledger accounts, trial balance, profit & loss statement, and balance sheet. It also covers ratio calculations and compares Linda's ratios with industry standards. The report provides insights into the importance of proper accounting practices for small businesses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording Business

Transaction

Transaction

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

(a) Transactions are recorded in double entry system ................................................................1

b) Ledger accounts......................................................................................................................3

c) Develop a Trial Balance..........................................................................................................6

d) Profit & loss statement............................................................................................................7

e) Balance Sheet..........................................................................................................................8

f) ….Write a brief letter to Linda................................................................................................8

PART B............................................................................................................................................9

….Ratio calculations...................................................................................................................9

…..Linda's competitors ratio.......................................................................................................9

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

(a) Transactions are recorded in double entry system ................................................................1

b) Ledger accounts......................................................................................................................3

c) Develop a Trial Balance..........................................................................................................6

d) Profit & loss statement............................................................................................................7

e) Balance Sheet..........................................................................................................................8

f) ….Write a brief letter to Linda................................................................................................8

PART B............................................................................................................................................9

….Ratio calculations...................................................................................................................9

…..Linda's competitors ratio.......................................................................................................9

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

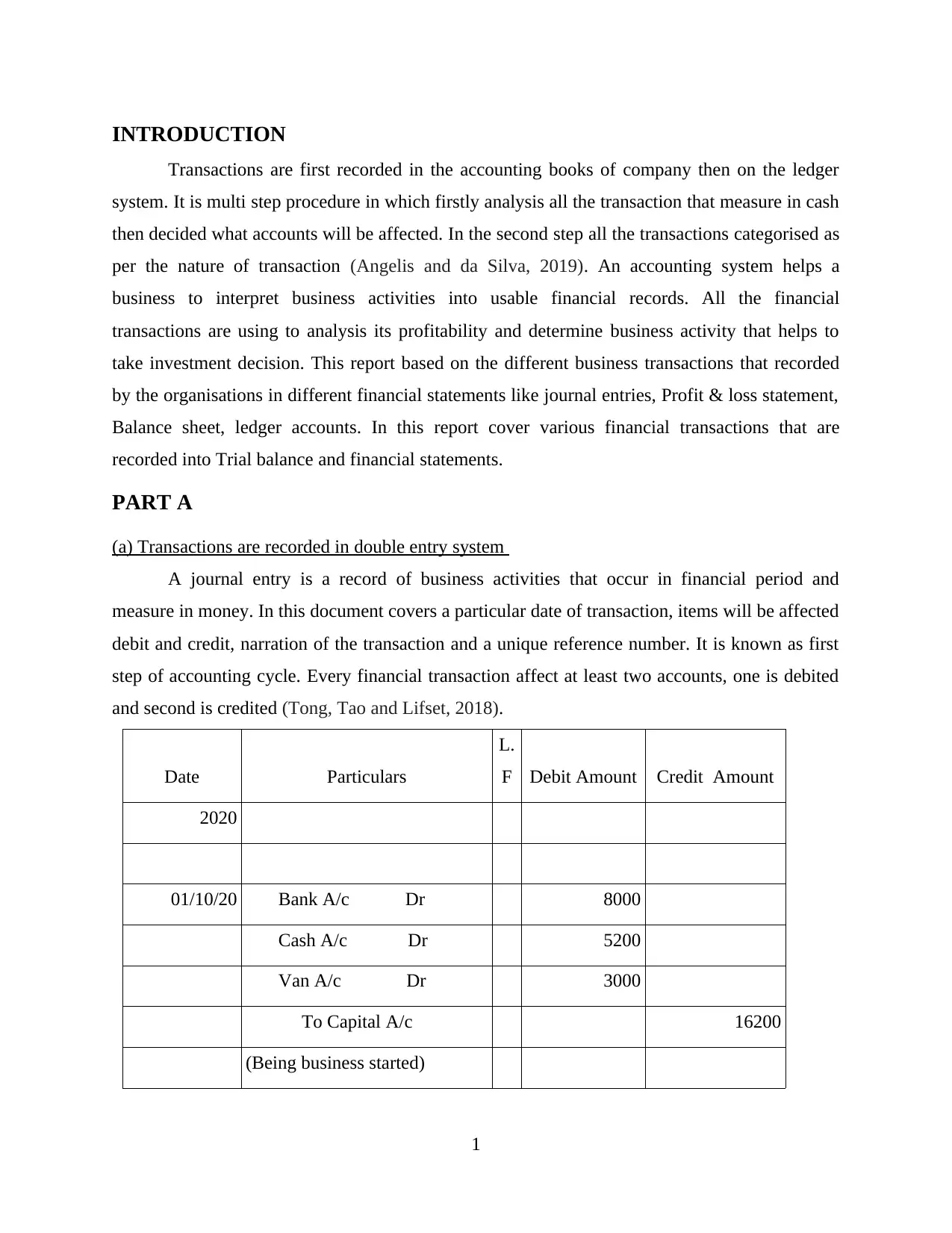

INTRODUCTION

Transactions are first recorded in the accounting books of company then on the ledger

system. It is multi step procedure in which firstly analysis all the transaction that measure in cash

then decided what accounts will be affected. In the second step all the transactions categorised as

per the nature of transaction (Angelis and da Silva, 2019). An accounting system helps a

business to interpret business activities into usable financial records. All the financial

transactions are using to analysis its profitability and determine business activity that helps to

take investment decision. This report based on the different business transactions that recorded

by the organisations in different financial statements like journal entries, Profit & loss statement,

Balance sheet, ledger accounts. In this report cover various financial transactions that are

recorded into Trial balance and financial statements.

PART A

(a) Transactions are recorded in double entry system ..............

A journal entry is a record of business activities that occur in financial period and

measure in money. In this document covers a particular date of transaction, items will be affected

debit and credit, narration of the transaction and a unique reference number. It is known as first

step of accounting cycle. Every financial transaction affect at least two accounts, one is debited

and second is credited (Tong, Tao and Lifset, 2018).

Date Particulars

L.

F Debit Amount Credit Amount

2020

01/10/20 …...Bank A/c Dr…... 8000

…...Cash A/c Dr…... 5200

…...Van A/c Dr…... 3000

…...To Capital A/c 16200

(Being business started)

1

Transactions are first recorded in the accounting books of company then on the ledger

system. It is multi step procedure in which firstly analysis all the transaction that measure in cash

then decided what accounts will be affected. In the second step all the transactions categorised as

per the nature of transaction (Angelis and da Silva, 2019). An accounting system helps a

business to interpret business activities into usable financial records. All the financial

transactions are using to analysis its profitability and determine business activity that helps to

take investment decision. This report based on the different business transactions that recorded

by the organisations in different financial statements like journal entries, Profit & loss statement,

Balance sheet, ledger accounts. In this report cover various financial transactions that are

recorded into Trial balance and financial statements.

PART A

(a) Transactions are recorded in double entry system ..............

A journal entry is a record of business activities that occur in financial period and

measure in money. In this document covers a particular date of transaction, items will be affected

debit and credit, narration of the transaction and a unique reference number. It is known as first

step of accounting cycle. Every financial transaction affect at least two accounts, one is debited

and second is credited (Tong, Tao and Lifset, 2018).

Date Particulars

L.

F Debit Amount Credit Amount

2020

01/10/20 …...Bank A/c Dr…... 8000

…...Cash A/c Dr…... 5200

…...Van A/c Dr…... 3000

…...To Capital A/c 16200

(Being business started)

1

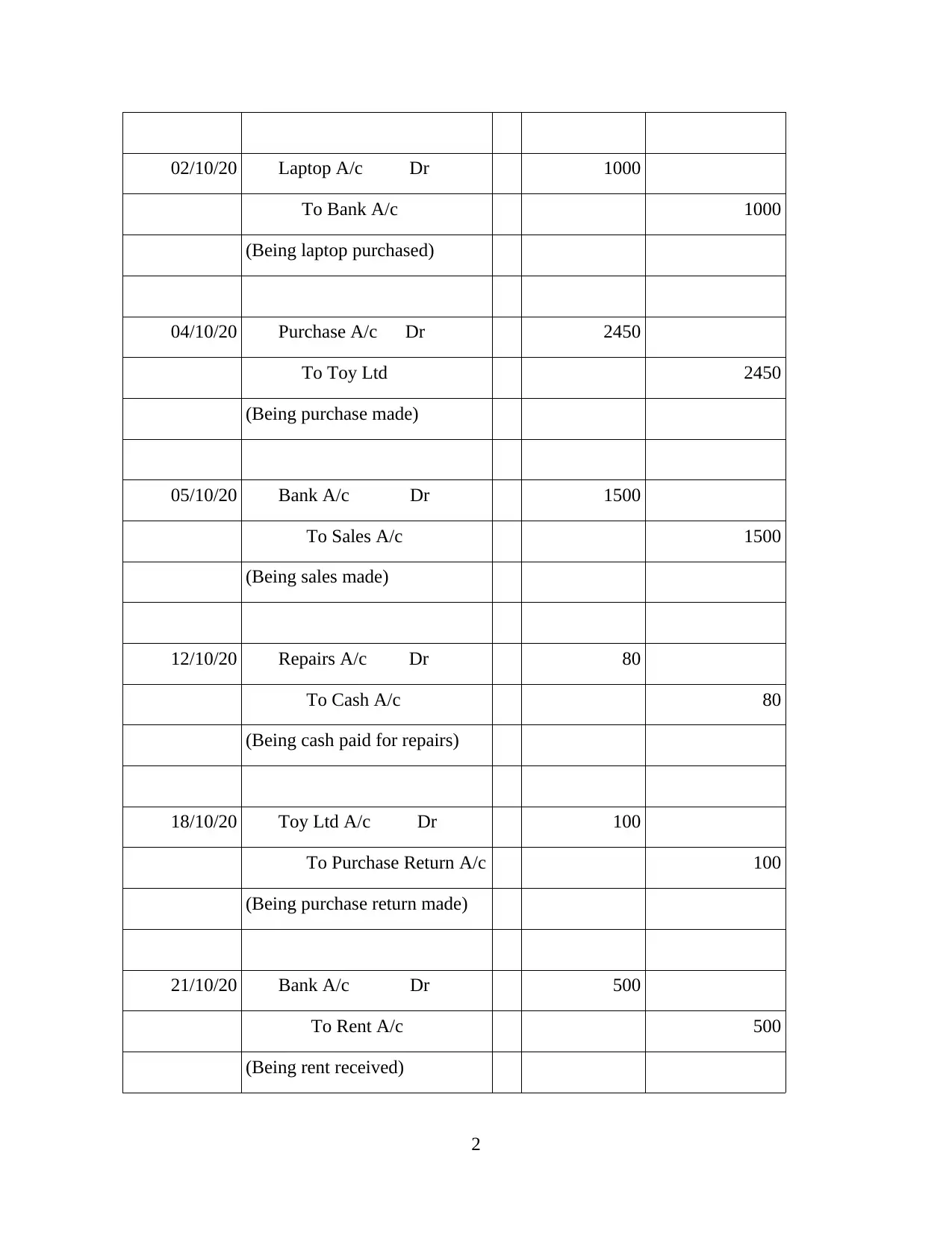

02/10/20 …...Laptop A/c Dr…... 1000

…...To Bank A/c 1000

(Being laptop purchased)

04/10/20 …...Purchase A/c Dr…... 2450

…...To Toy Ltd 2450

(Being purchase made)

05/10/20 …...Bank A/c Dr…... 1500

…...To Sales A/c 1500

(Being sales made)

12/10/20 …...Repairs A/c Dr…... 80

…...To Cash A/c 80

(Being cash paid for repairs)

18/10/20 …...Toy Ltd A/c Dr…... 100

…...To Purchase Return A/c 100

(Being purchase return made)

21/10/20 …...Bank A/c Dr…... 500

…...To Rent A/c 500

(Being rent received)

2

…...To Bank A/c 1000

(Being laptop purchased)

04/10/20 …...Purchase A/c Dr…... 2450

…...To Toy Ltd 2450

(Being purchase made)

05/10/20 …...Bank A/c Dr…... 1500

…...To Sales A/c 1500

(Being sales made)

12/10/20 …...Repairs A/c Dr…... 80

…...To Cash A/c 80

(Being cash paid for repairs)

18/10/20 …...Toy Ltd A/c Dr…... 100

…...To Purchase Return A/c 100

(Being purchase return made)

21/10/20 …...Bank A/c Dr…... 500

…...To Rent A/c 500

(Being rent received)

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

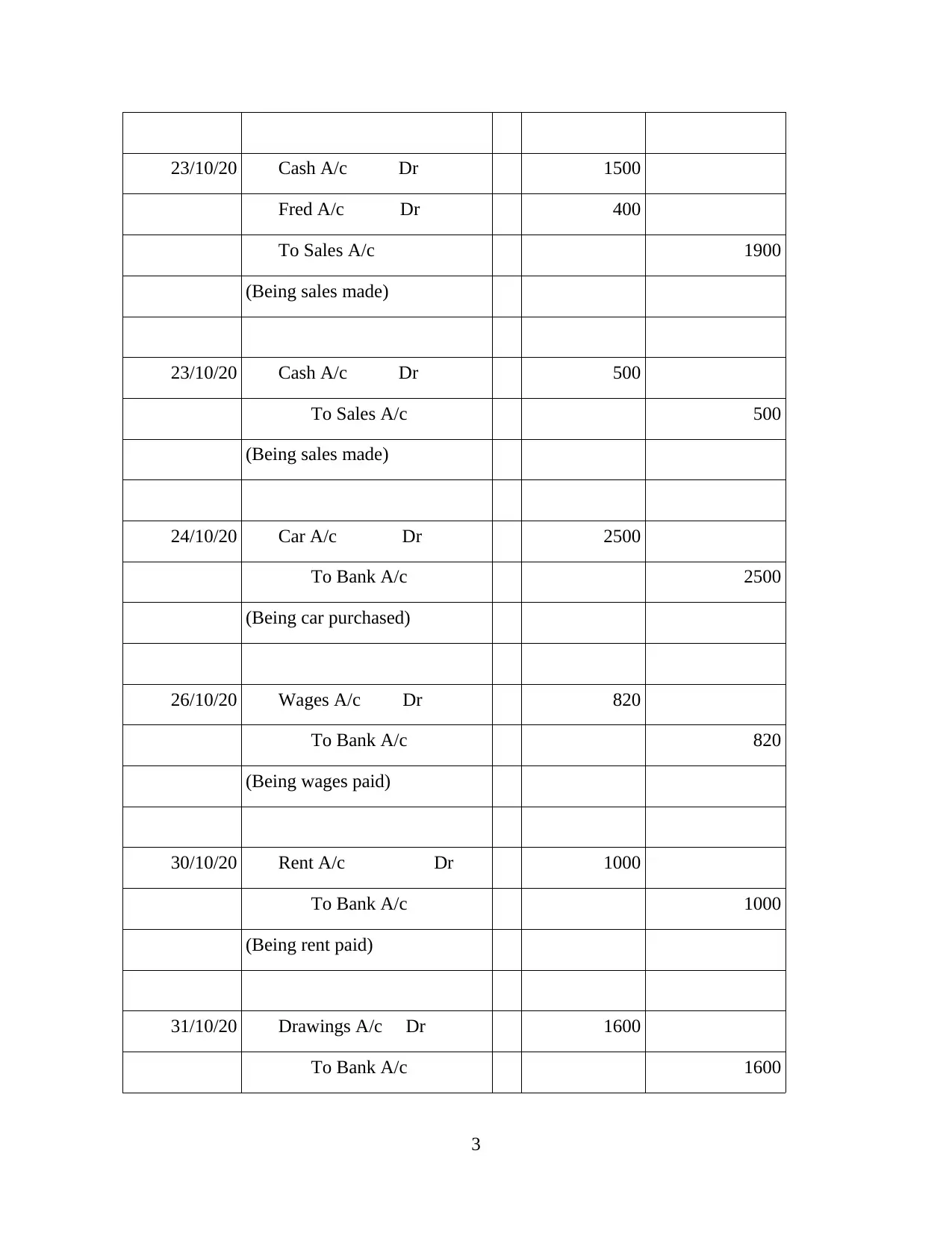

23/10/20 …...Cash A/c Dr…... 1500

…...Fred A/c Dr…... 400

To Sales A/c 1900

(Being sales made)

23/10/20 …...Cash A/c Dr…... 500

…...To Sales A/c 500

(Being sales made)

24/10/20 …...Car A/c Dr…... 2500

…...To Bank A/c 2500

(Being car purchased)

26/10/20 …...Wages A/c Dr…... 820

…...To Bank A/c 820

(Being wages paid)

30/10/20 …...Rent A/c…... Dr…... 1000

…...To Bank A/c…... 1000

(Being rent paid)

31/10/20 …...Drawings A/c Dr…... 1600

…...To Bank A/c 1600

3

…...Fred A/c Dr…... 400

To Sales A/c 1900

(Being sales made)

23/10/20 …...Cash A/c Dr…... 500

…...To Sales A/c 500

(Being sales made)

24/10/20 …...Car A/c Dr…... 2500

…...To Bank A/c 2500

(Being car purchased)

26/10/20 …...Wages A/c Dr…... 820

…...To Bank A/c 820

(Being wages paid)

30/10/20 …...Rent A/c…... Dr…... 1000

…...To Bank A/c…... 1000

(Being rent paid)

31/10/20 …...Drawings A/c Dr…... 1600

…...To Bank A/c 1600

3

(Being drawings made)

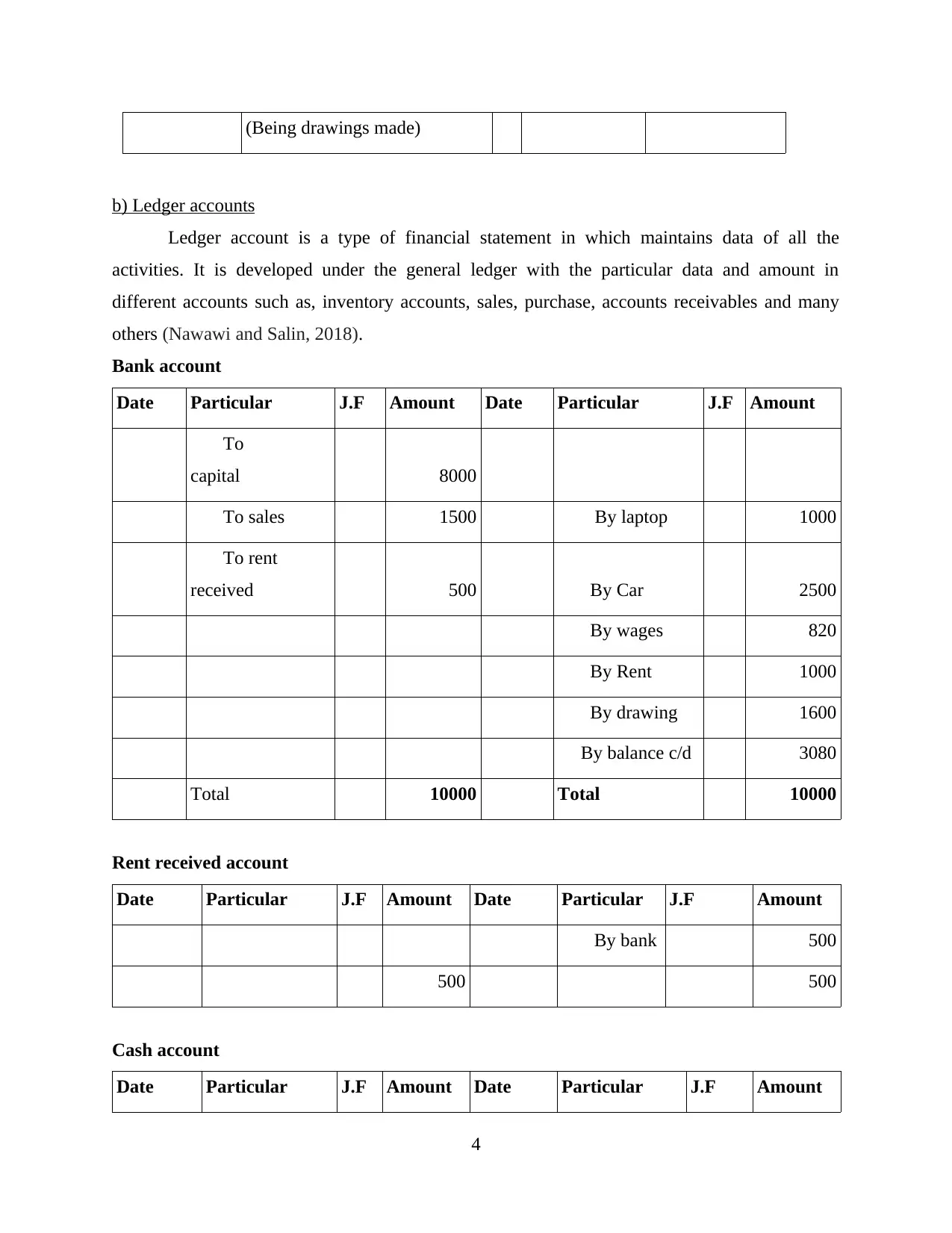

b) Ledger accounts.............

Ledger account is a type of financial statement in which maintains data of all the

activities. It is developed under the general ledger with the particular data and amount in

different accounts such as, inventory accounts, sales, purchase, accounts receivables and many

others (Nawawi and Salin, 2018).

Bank account

Date Particular J.F Amount Date Particular J.F Amount

…...To

capital…... …...8000

…...To sales…... …...1500 …....By laptop …...1000

…...To rent

received…... …...500 …...By Car …...2500

…...By wages …...820

…...By Rent …...1000

…...By drawing …...1600

….By balance c/d …...3080

Total …...10000 Total …...10000

Rent received account

Date Particular J.F Amount Date Particular J.F Amount

…...By bank 500

500 500

Cash account

Date Particular J.F Amount Date Particular J.F Amount

4

b) Ledger accounts.............

Ledger account is a type of financial statement in which maintains data of all the

activities. It is developed under the general ledger with the particular data and amount in

different accounts such as, inventory accounts, sales, purchase, accounts receivables and many

others (Nawawi and Salin, 2018).

Bank account

Date Particular J.F Amount Date Particular J.F Amount

…...To

capital…... …...8000

…...To sales…... …...1500 …....By laptop …...1000

…...To rent

received…... …...500 …...By Car …...2500

…...By wages …...820

…...By Rent …...1000

…...By drawing …...1600

….By balance c/d …...3080

Total …...10000 Total …...10000

Rent received account

Date Particular J.F Amount Date Particular J.F Amount

…...By bank 500

500 500

Cash account

Date Particular J.F Amount Date Particular J.F Amount

4

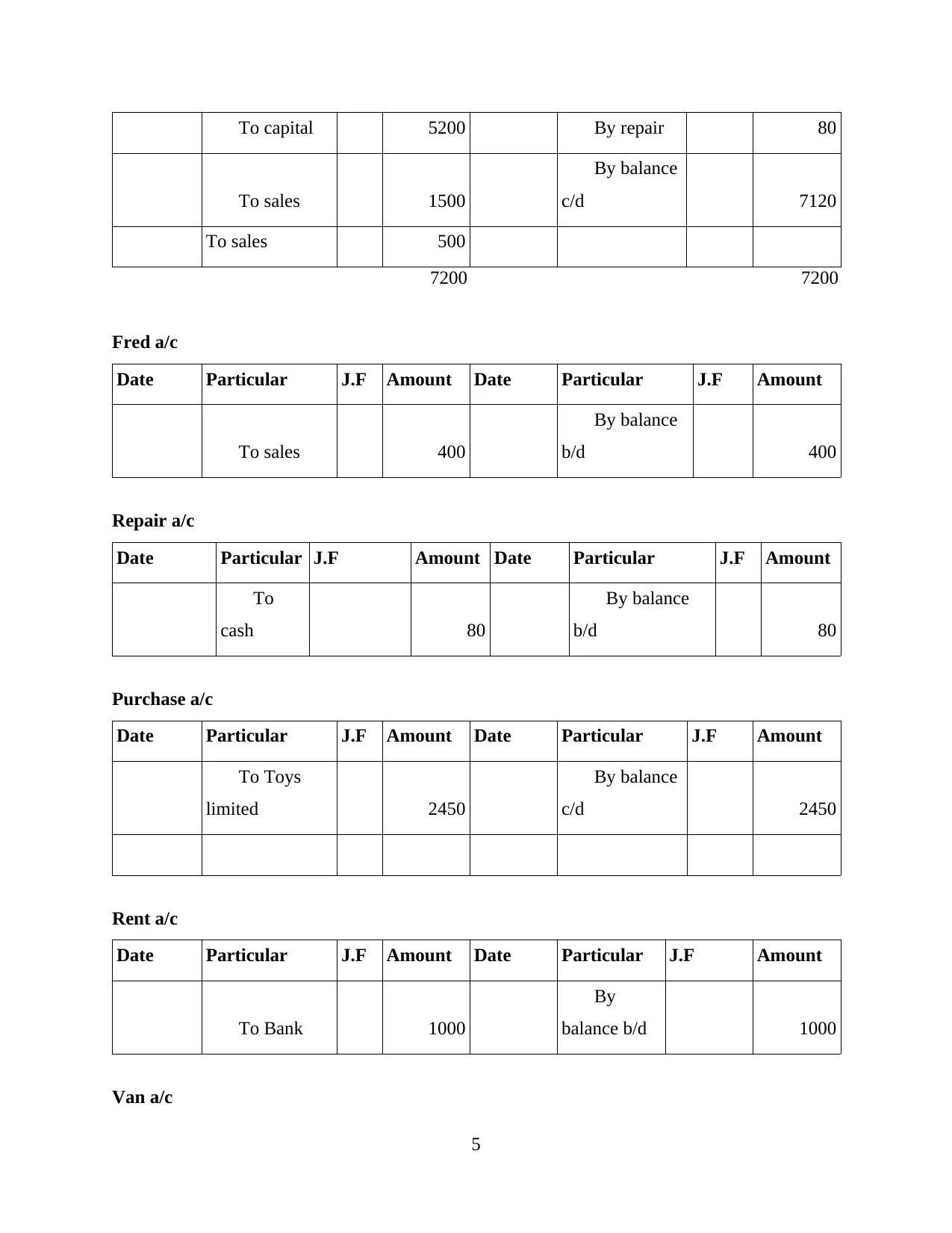

…...To capital 5200 …...By repair 80

…...To sales 1500

…...By balance

c/d... 7120

To sales 500

7200 7200

Fred a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To sales 400

…...By balance

b/d... 400

Repair a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

cash... 80

…...By balance

b/d... 80

Purchase a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To Toys

limited 2450

…...By balance

c/d 2450

Rent a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To Bank 1000

…...By

balance b/d 1000

Van a/c

5

…...To sales 1500

…...By balance

c/d... 7120

To sales 500

7200 7200

Fred a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To sales 400

…...By balance

b/d... 400

Repair a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

cash... 80

…...By balance

b/d... 80

Purchase a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To Toys

limited 2450

…...By balance

c/d 2450

Rent a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To Bank 1000

…...By

balance b/d 1000

Van a/c

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

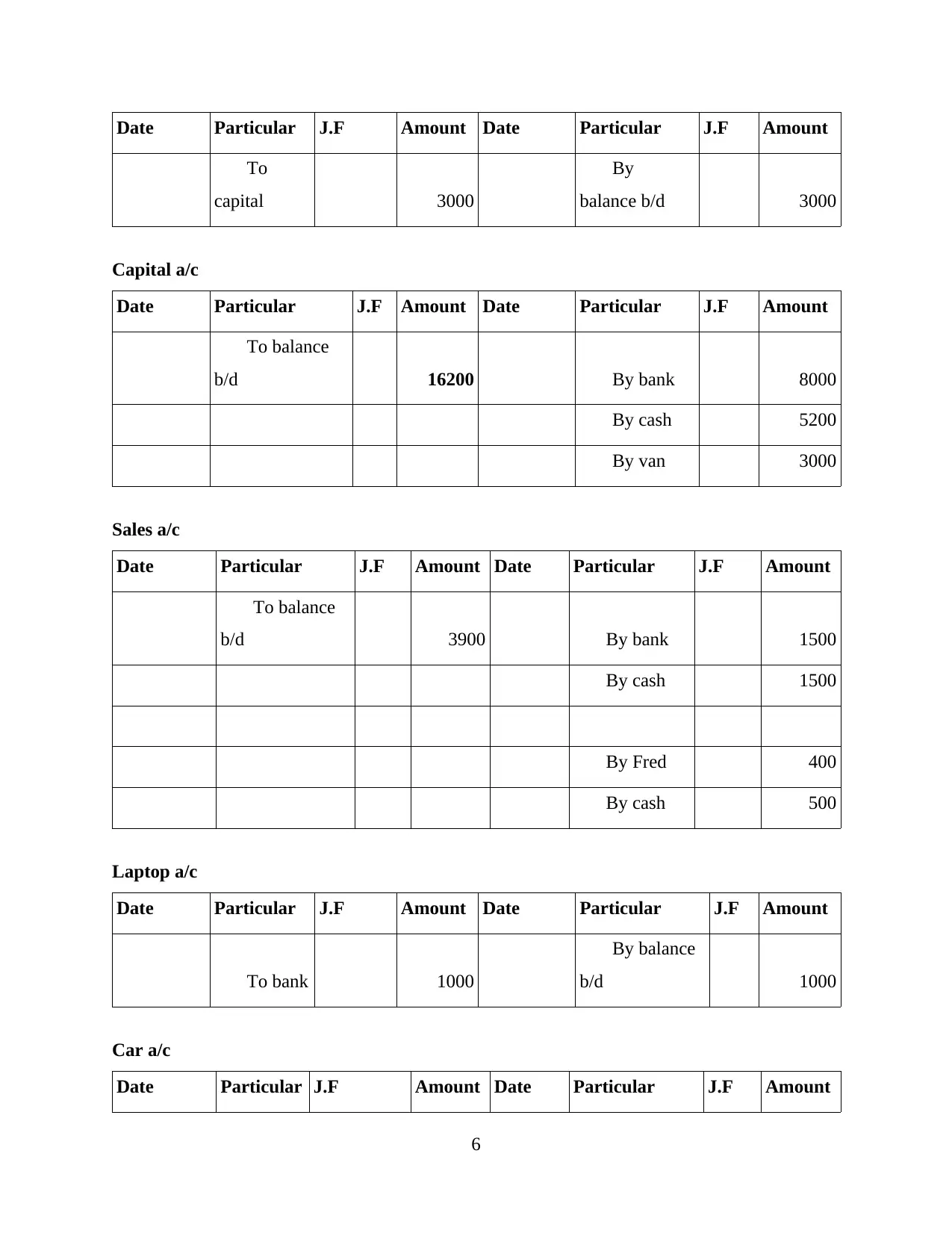

Date Particular J.F Amount Date Particular J.F Amount

…...To

capital 3000

…...By

balance b/d... 3000

Capital a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To balance

b/d... 16200 …...By bank 8000

…...By cash 5200

…...By van 3000

Sales a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To balance

b/d... 3900 …...By bank 1500

…...By cash 1500

…...By Fred 400

…...By cash 500

Laptop a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To bank 1000

…...By balance

b/d 1000

Car a/c

Date Particular J.F Amount Date Particular J.F Amount

6

…...To

capital 3000

…...By

balance b/d... 3000

Capital a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To balance

b/d... 16200 …...By bank 8000

…...By cash 5200

…...By van 3000

Sales a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To balance

b/d... 3900 …...By bank 1500

…...By cash 1500

…...By Fred 400

…...By cash 500

Laptop a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To bank 1000

…...By balance

b/d 1000

Car a/c

Date Particular J.F Amount Date Particular J.F Amount

6

…...To

Bank 2500

…...By balance

b/d 2500

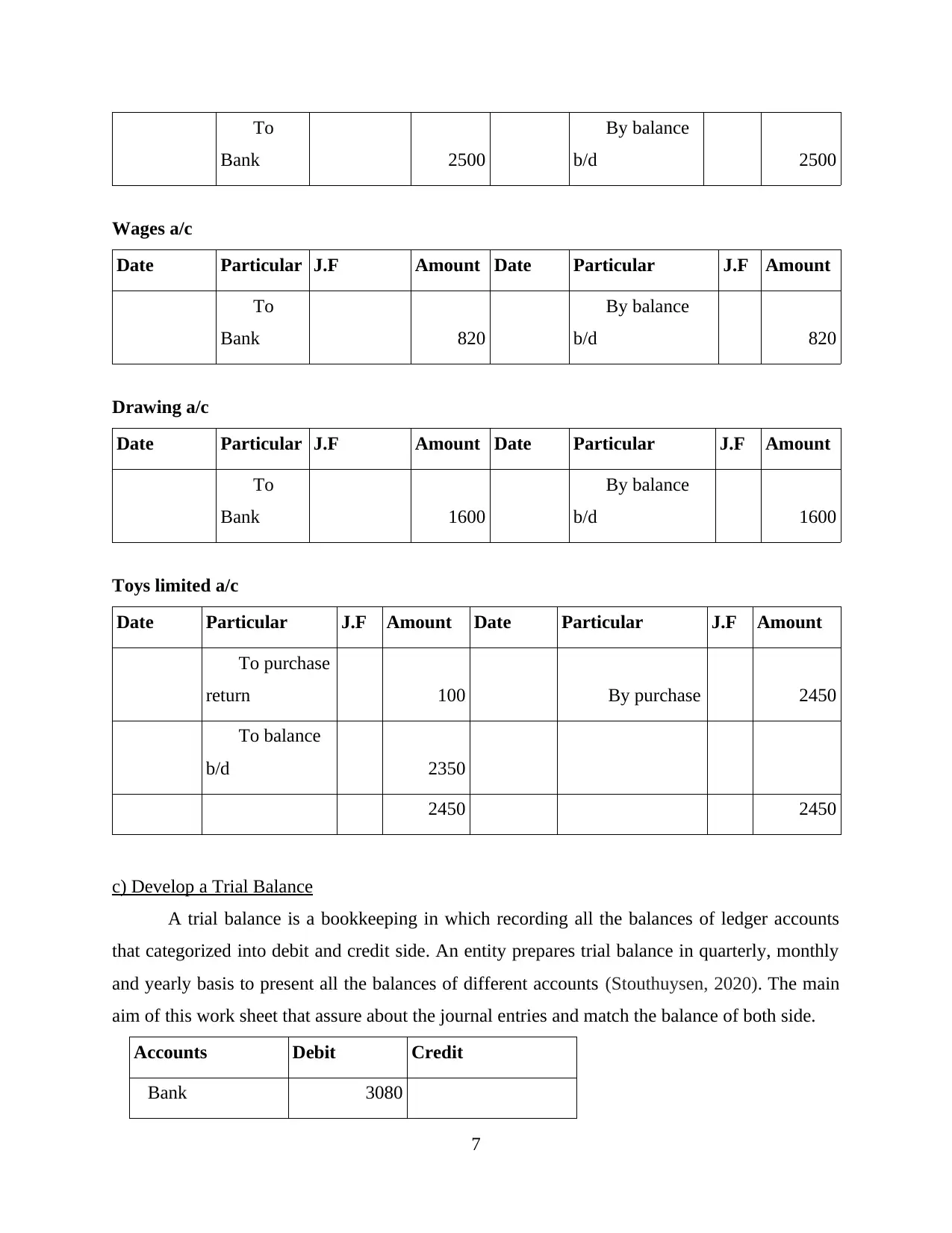

Wages a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 820

…...By balance

b/d 820

Drawing a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 1600

…...By balance

b/d 1600

Toys limited a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To purchase

return 100 …......By purchase 2450

…...To balance

b/d 2350

2450 2450

c) Develop a Trial Balance..........

A trial balance is a bookkeeping in which recording all the balances of ledger accounts

that categorized into debit and credit side. An entity prepares trial balance in quarterly, monthly

and yearly basis to present all the balances of different accounts (Stouthuysen, 2020). The main

aim of this work sheet that assure about the journal entries and match the balance of both side.

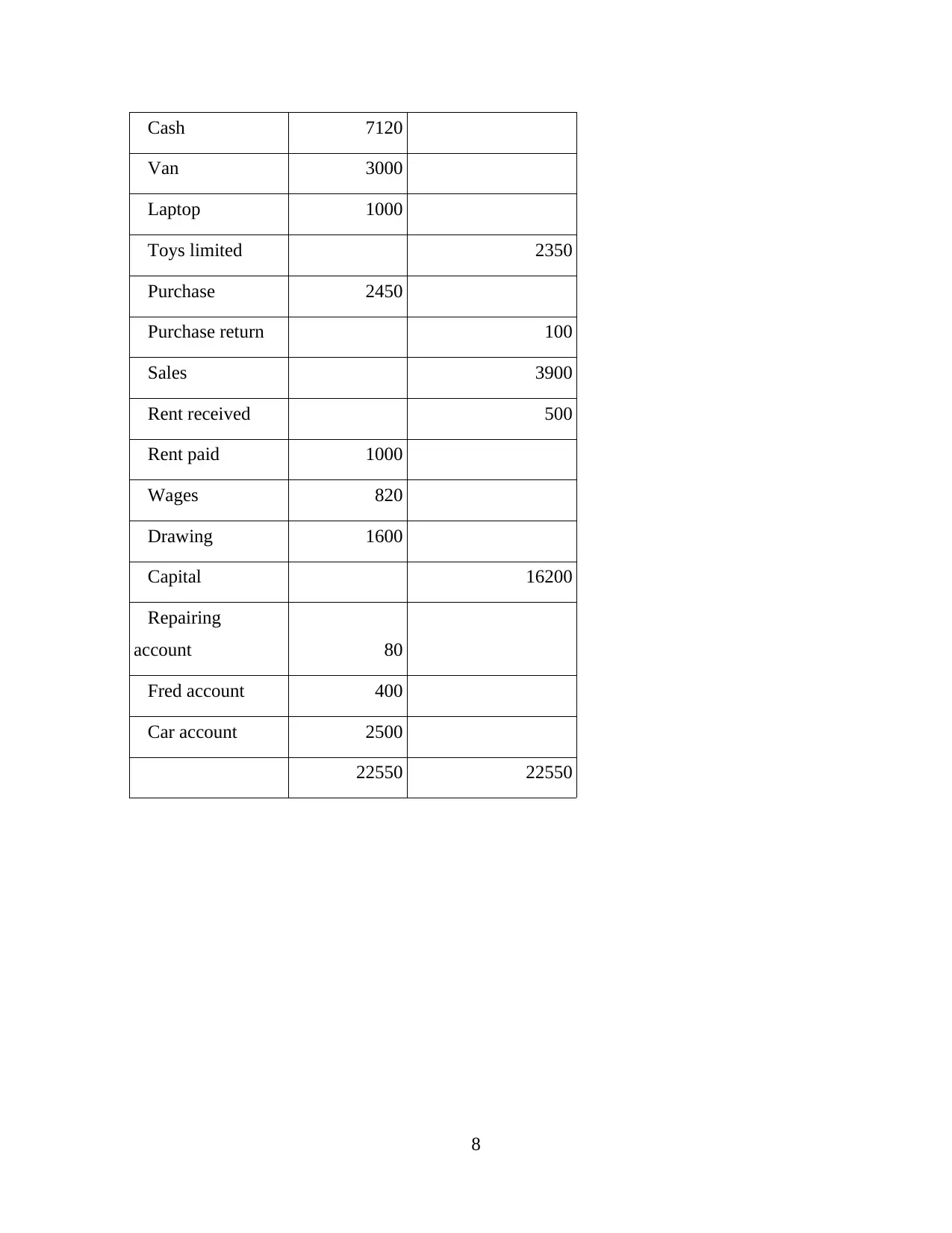

Accounts Debit Credit

...Bank... 3080

7

Bank 2500

…...By balance

b/d 2500

Wages a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 820

…...By balance

b/d 820

Drawing a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 1600

…...By balance

b/d 1600

Toys limited a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To purchase

return 100 …......By purchase 2450

…...To balance

b/d 2350

2450 2450

c) Develop a Trial Balance..........

A trial balance is a bookkeeping in which recording all the balances of ledger accounts

that categorized into debit and credit side. An entity prepares trial balance in quarterly, monthly

and yearly basis to present all the balances of different accounts (Stouthuysen, 2020). The main

aim of this work sheet that assure about the journal entries and match the balance of both side.

Accounts Debit Credit

...Bank... 3080

7

...Cash... 7120

...Van... 3000

...Laptop... 1000

...Toys limited... 2350

...Purchase... 2450

...Purchase return... 100

...Sales... 3900

...Rent received... 500

...Rent paid... 1000

...Wages... 820

...Drawing... 1600

...Capital... 16200

...Repairing

account... 80

...Fred account... 400

...Car account... 2500

22550 22550

8

...Van... 3000

...Laptop... 1000

...Toys limited... 2350

...Purchase... 2450

...Purchase return... 100

...Sales... 3900

...Rent received... 500

...Rent paid... 1000

...Wages... 820

...Drawing... 1600

...Capital... 16200

...Repairing

account... 80

...Fred account... 400

...Car account... 2500

22550 22550

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

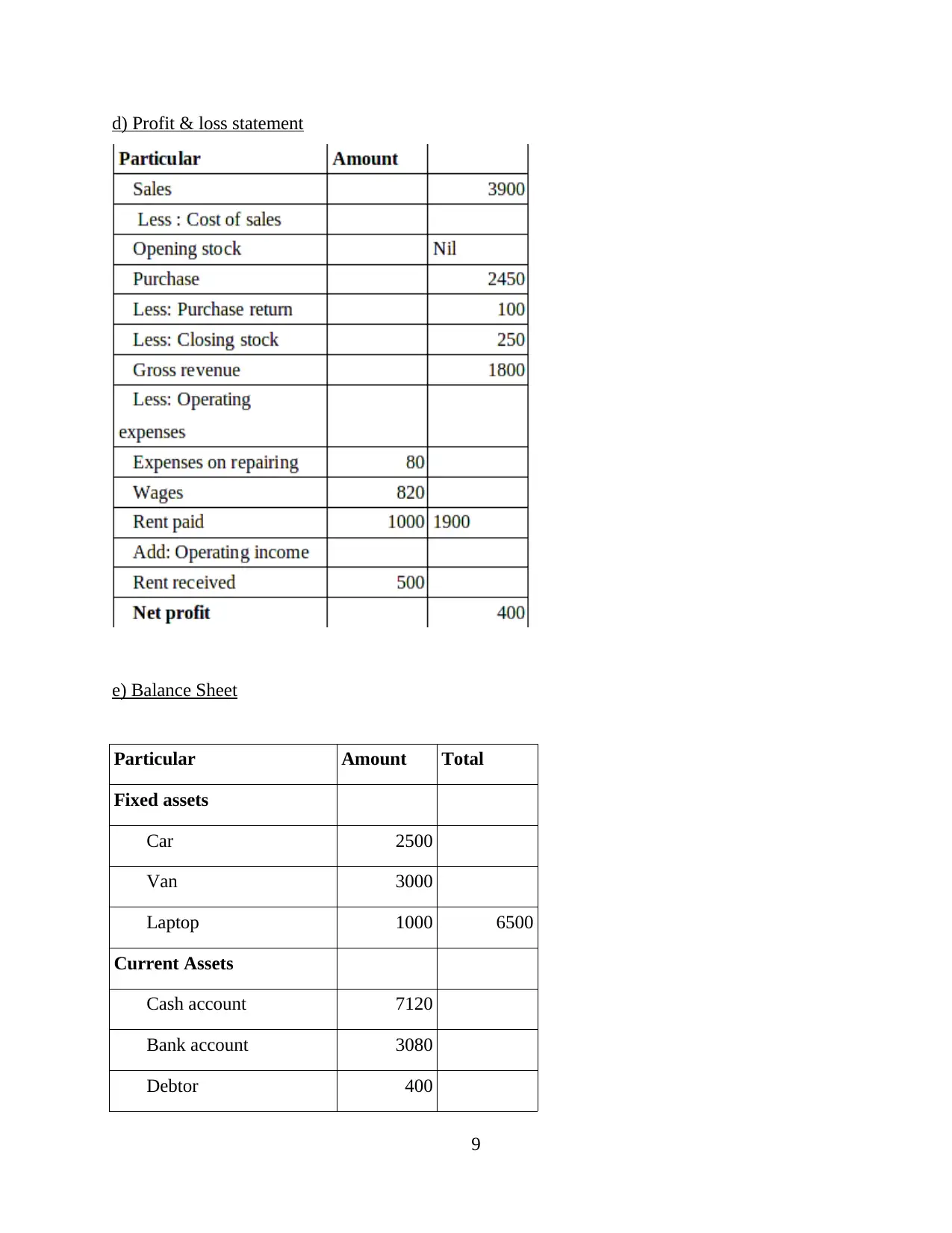

d) Profit & loss statement

e) Balance Sheet............

Particular Amount Total

Fixed assets

…...Car 2500

…...Van 3000

…...Laptop 1000 6500

Current Assets

…...Cash account 7120

…...Bank account 3080

…...Debtor 400

9

e) Balance Sheet............

Particular Amount Total

Fixed assets

…...Car 2500

…...Van 3000

…...Laptop 1000 6500

Current Assets

…...Cash account 7120

…...Bank account 3080

…...Debtor 400

9

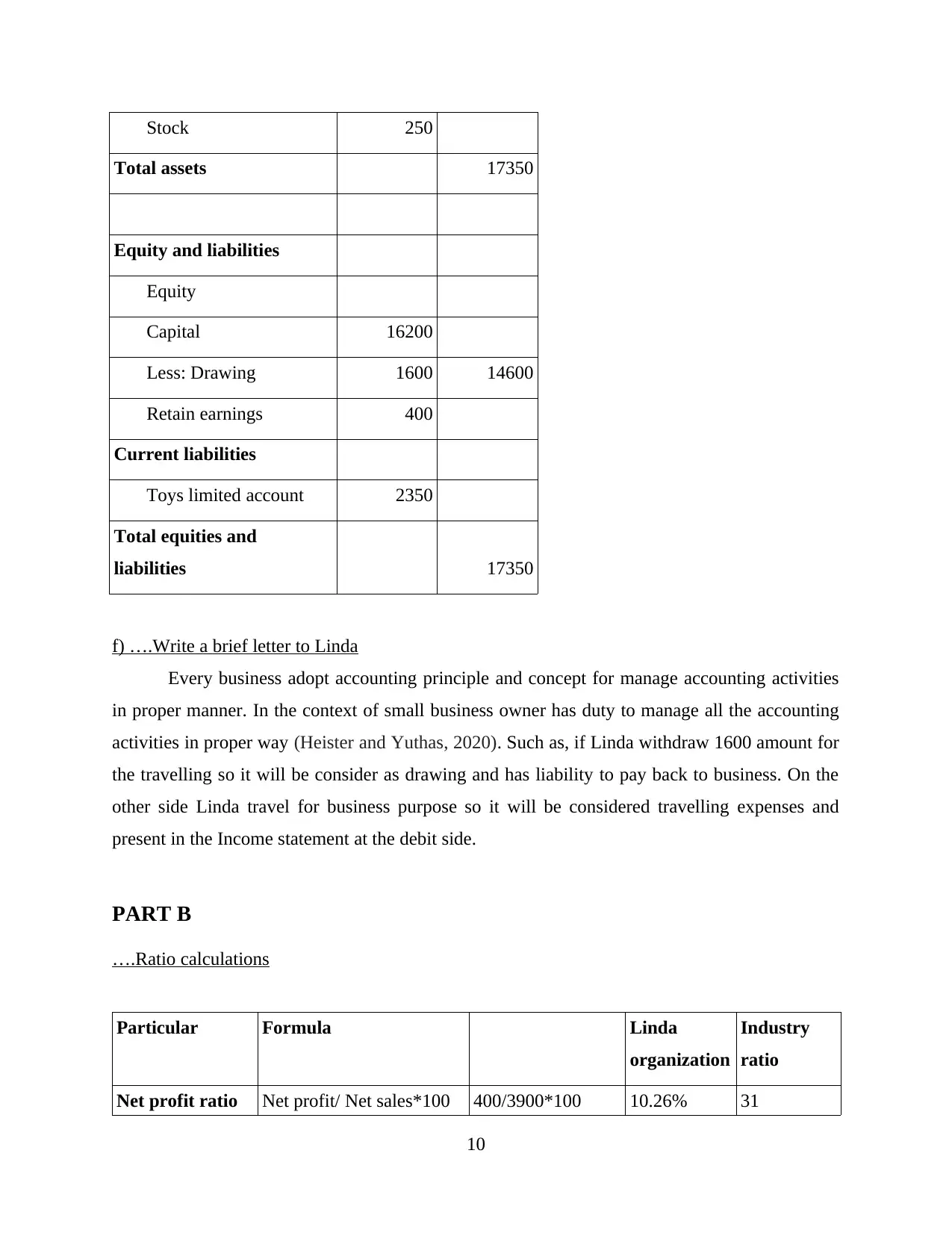

…...Stock 250

Total assets 17350

Equity and liabilities

…...Equity

…...Capital 16200

…...Less: Drawing 1600 14600

…...Retain earnings 400

Current liabilities

…...Toys limited account 2350

Total equities and

liabilities 17350

f) ….Write a brief letter to Linda..............

Every business adopt accounting principle and concept for manage accounting activities

in proper manner. In the context of small business owner has duty to manage all the accounting

activities in proper way (Heister and Yuthas, 2020). Such as, if Linda withdraw 1600 amount for

the travelling so it will be consider as drawing and has liability to pay back to business. On the

other side Linda travel for business purpose so it will be considered travelling expenses and

present in the Income statement at the debit side.

PART B

….Ratio calculations..............

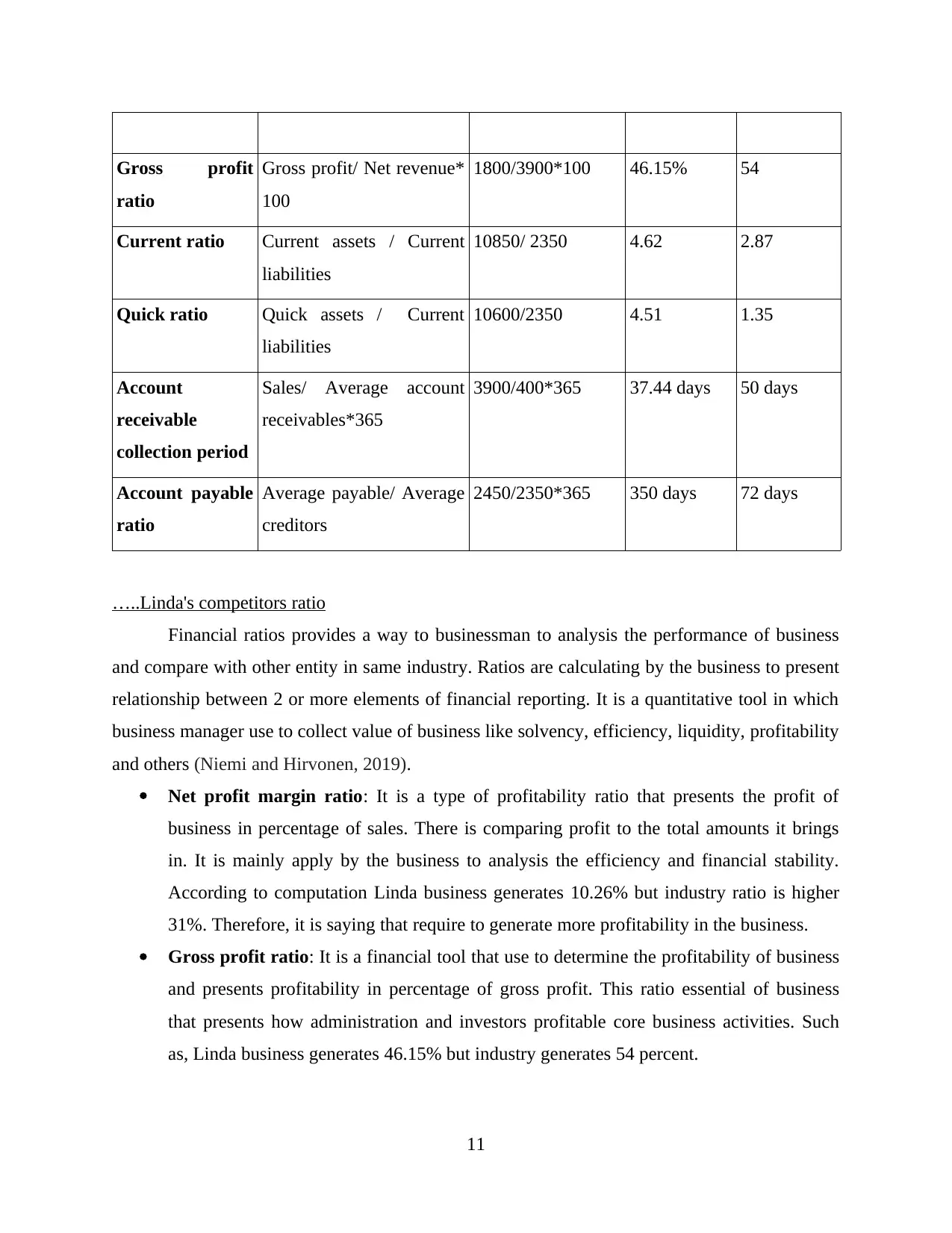

Particular Formula Linda

organization

Industry

ratio

Net profit ratio Net profit/ Net sales*100 400/3900*100 10.26% 31

10

Total assets 17350

Equity and liabilities

…...Equity

…...Capital 16200

…...Less: Drawing 1600 14600

…...Retain earnings 400

Current liabilities

…...Toys limited account 2350

Total equities and

liabilities 17350

f) ….Write a brief letter to Linda..............

Every business adopt accounting principle and concept for manage accounting activities

in proper manner. In the context of small business owner has duty to manage all the accounting

activities in proper way (Heister and Yuthas, 2020). Such as, if Linda withdraw 1600 amount for

the travelling so it will be consider as drawing and has liability to pay back to business. On the

other side Linda travel for business purpose so it will be considered travelling expenses and

present in the Income statement at the debit side.

PART B

….Ratio calculations..............

Particular Formula Linda

organization

Industry

ratio

Net profit ratio Net profit/ Net sales*100 400/3900*100 10.26% 31

10

Gross profit

ratio

Gross profit/ Net revenue*

100

1800/3900*100 46.15% 54

Current ratio Current assets / Current

liabilities

10850/ 2350 4.62 2.87

Quick ratio Quick assets / Current

liabilities

10600/2350 4.51 1.35

Account

receivable

collection period

Sales/ Average account

receivables*365

3900/400*365 37.44 days 50 days

Account payable

ratio

Average payable/ Average

creditors

2450/2350*365 350 days 72 days

…..Linda's competitors ratio..............

Financial ratios provides a way to businessman to analysis the performance of business

and compare with other entity in same industry. Ratios are calculating by the business to present

relationship between 2 or more elements of financial reporting. It is a quantitative tool in which

business manager use to collect value of business like solvency, efficiency, liquidity, profitability

and others (Niemi and Hirvonen, 2019).

Net profit margin ratio: It is a type of profitability ratio that presents the profit of

business in percentage of sales. There is comparing profit to the total amounts it brings

in. It is mainly apply by the business to analysis the efficiency and financial stability.

According to computation Linda business generates 10.26% but industry ratio is higher

31%. Therefore, it is saying that require to generate more profitability in the business.

Gross profit ratio: It is a financial tool that use to determine the profitability of business

and presents profitability in percentage of gross profit. This ratio essential of business

that presents how administration and investors profitable core business activities. Such

as, Linda business generates 46.15% but industry generates 54 percent.

11

ratio

Gross profit/ Net revenue*

100

1800/3900*100 46.15% 54

Current ratio Current assets / Current

liabilities

10850/ 2350 4.62 2.87

Quick ratio Quick assets / Current

liabilities

10600/2350 4.51 1.35

Account

receivable

collection period

Sales/ Average account

receivables*365

3900/400*365 37.44 days 50 days

Account payable

ratio

Average payable/ Average

creditors

2450/2350*365 350 days 72 days

…..Linda's competitors ratio..............

Financial ratios provides a way to businessman to analysis the performance of business

and compare with other entity in same industry. Ratios are calculating by the business to present

relationship between 2 or more elements of financial reporting. It is a quantitative tool in which

business manager use to collect value of business like solvency, efficiency, liquidity, profitability

and others (Niemi and Hirvonen, 2019).

Net profit margin ratio: It is a type of profitability ratio that presents the profit of

business in percentage of sales. There is comparing profit to the total amounts it brings

in. It is mainly apply by the business to analysis the efficiency and financial stability.

According to computation Linda business generates 10.26% but industry ratio is higher

31%. Therefore, it is saying that require to generate more profitability in the business.

Gross profit ratio: It is a financial tool that use to determine the profitability of business

and presents profitability in percentage of gross profit. This ratio essential of business

that presents how administration and investors profitable core business activities. Such

as, Linda business generates 46.15% but industry generates 54 percent.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current ratio: It is a kind of liquidity ratio which is applying by the organisation to

measure the ability of the business to pay off their short term debts. For the calculation

use current assets as well as current liabilities (Muneeza, and Mustapha, 2019). Both

companies near their ideal ratio but Linda has too much liquidity 4:62 as compare of

industry 2:67 which is not presenting good liquid position of business.

Quick ratio: It presents as a business's indicant for its shorter term liquidity condition

that use to analysis the capacity of business to emission its short term liabilities. As per

the ratio calculation it is analysed that Linda has good liquidity 4:51 to pay off their debts

and obligation but in extra manner that is not good for business.

Accounts receivable ratio: This ratio use by business to collect amount from the debtors.

Linda is giving time period is 37.44 days as compare of industry is 50 days.

Accounts payable ratio: This ratio presents that the payable time period to their

creditors is 365 days. On the other side, industry has timing for the payable is 72 days

(Le, Amer and Holliday, 2019).

CONCLUSION

As per the above report it has been concluded that in a business entity conduct various

financial transactions in particular financial year. It is important to recording all the transactions

into different financial statements. There are recording transactions into Ledger account. Income

statement and balance sheet. At the end calculate financial ratio to present the efficiency of

business in proper manner.

REFERENCES

Books and Journals

Angelis, J. and da Silva, E. R., 2019. Blockchain adoption: A value driver perspective. Business

Horizons. 62(3). pp.307-314.

12

measure the ability of the business to pay off their short term debts. For the calculation

use current assets as well as current liabilities (Muneeza, and Mustapha, 2019). Both

companies near their ideal ratio but Linda has too much liquidity 4:62 as compare of

industry 2:67 which is not presenting good liquid position of business.

Quick ratio: It presents as a business's indicant for its shorter term liquidity condition

that use to analysis the capacity of business to emission its short term liabilities. As per

the ratio calculation it is analysed that Linda has good liquidity 4:51 to pay off their debts

and obligation but in extra manner that is not good for business.

Accounts receivable ratio: This ratio use by business to collect amount from the debtors.

Linda is giving time period is 37.44 days as compare of industry is 50 days.

Accounts payable ratio: This ratio presents that the payable time period to their

creditors is 365 days. On the other side, industry has timing for the payable is 72 days

(Le, Amer and Holliday, 2019).

CONCLUSION

As per the above report it has been concluded that in a business entity conduct various

financial transactions in particular financial year. It is important to recording all the transactions

into different financial statements. There are recording transactions into Ledger account. Income

statement and balance sheet. At the end calculate financial ratio to present the efficiency of

business in proper manner.

REFERENCES

Books and Journals

Angelis, J. and da Silva, E. R., 2019. Blockchain adoption: A value driver perspective. Business

Horizons. 62(3). pp.307-314.

12

Tong, X., Tao, D. and Lifset, R., 2018. Varieties of business models for post-consumer recycling

in China. Journal of Cleaner Production. 170. pp.665-673.

Nawawi, A. and Salin, A. S. A. P., 2018. Employee fraud and misconduct: empirical evidence

from a telecommunication company. Information & Computer Security.

Stouthuysen, K., 2020. A 2020 perspective on “The building of online trust in e-business

relationships”. Electronic Commerce Research and Applications. 40. p.100929.

Heister, S. and Yuthas, K., 2020. The blockchain and how it can influence conceptions of the

self. Technology in Society. 60. p.101218.

Niemi, J. and Hirvonen, L., 2019. Money talks: Customer-initiated price negotiation in business-

to-business sales interaction. Discourse & Communication. 13(1). pp.95-118.

Muneeza, A. and Mustapha, Z., 2019. Blockchain and its Shariah compliant structure. In Halal

Cryptocurrency Management (pp. 69-106). Palgrave Macmillan, Cham.

Le, Q., Amer, A. and Holliday, J., 2019. RAID 4SMR: RAID Array with Shingled Magnetic

Recording Disk for Mass Storage Systems. Journal of Computer Science and

Technology. 34(4). pp.854-868.

13

in China. Journal of Cleaner Production. 170. pp.665-673.

Nawawi, A. and Salin, A. S. A. P., 2018. Employee fraud and misconduct: empirical evidence

from a telecommunication company. Information & Computer Security.

Stouthuysen, K., 2020. A 2020 perspective on “The building of online trust in e-business

relationships”. Electronic Commerce Research and Applications. 40. p.100929.

Heister, S. and Yuthas, K., 2020. The blockchain and how it can influence conceptions of the

self. Technology in Society. 60. p.101218.

Niemi, J. and Hirvonen, L., 2019. Money talks: Customer-initiated price negotiation in business-

to-business sales interaction. Discourse & Communication. 13(1). pp.95-118.

Muneeza, A. and Mustapha, Z., 2019. Blockchain and its Shariah compliant structure. In Halal

Cryptocurrency Management (pp. 69-106). Palgrave Macmillan, Cham.

Le, Q., Amer, A. and Holliday, J., 2019. RAID 4SMR: RAID Array with Shingled Magnetic

Recording Disk for Mass Storage Systems. Journal of Computer Science and

Technology. 34(4). pp.854-868.

13

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.